Malaysia Medical Tourism Market Size, Share, Trends and Forecast by Type, Treatment Type, and States, 2026-2034

Malaysia Medical Tourism Market Size & Forecast 2026-2034

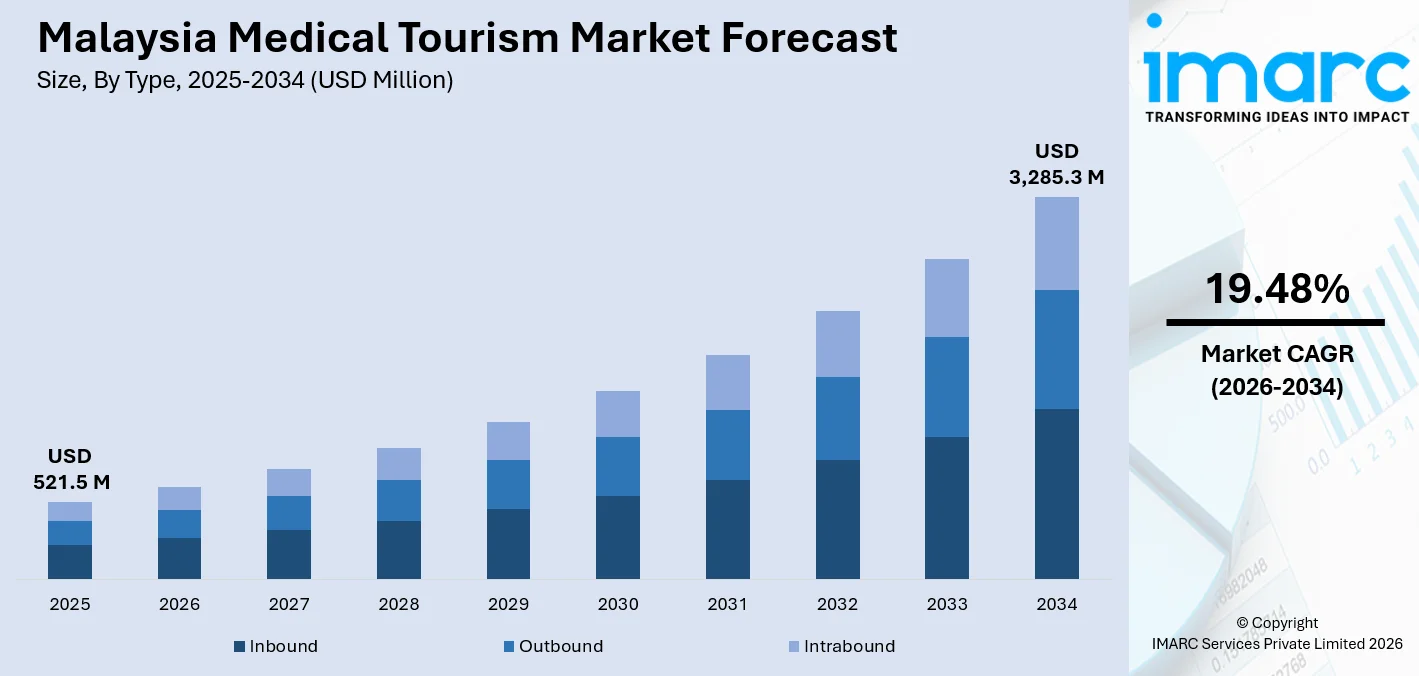

Malaysia medical tourism market size, valued at USD 521.5 Million in 2025, is projected to reach USD 3,285.3 Million by 2034, growing at a CAGR of 19.48% from 2026-2034, as Malaysia establishes its reputation as one of Southeast Asia’s most trusted destinations for affordable, high-quality healthcare. The country’s combination of internationally accredited hospitals, English-proficient medical professionals, and low treatment costs compared to Western equivalents continues to attract patients from Indonesia, Singapore, the Gulf states, and beyond.

To get more information on this market Request Sample

Malaysia Medical Tourism Industry Analysis - Key Insights

- Inbound commands 78.5% of type in 2025 - foreign patients seeking affordable, accredited care are the undisputed engine of this market, and the inbound segment’s dominance reflects just how effectively Malaysia has positioned itself against regional competitors like Thailand and India on both cost and quality grounds.

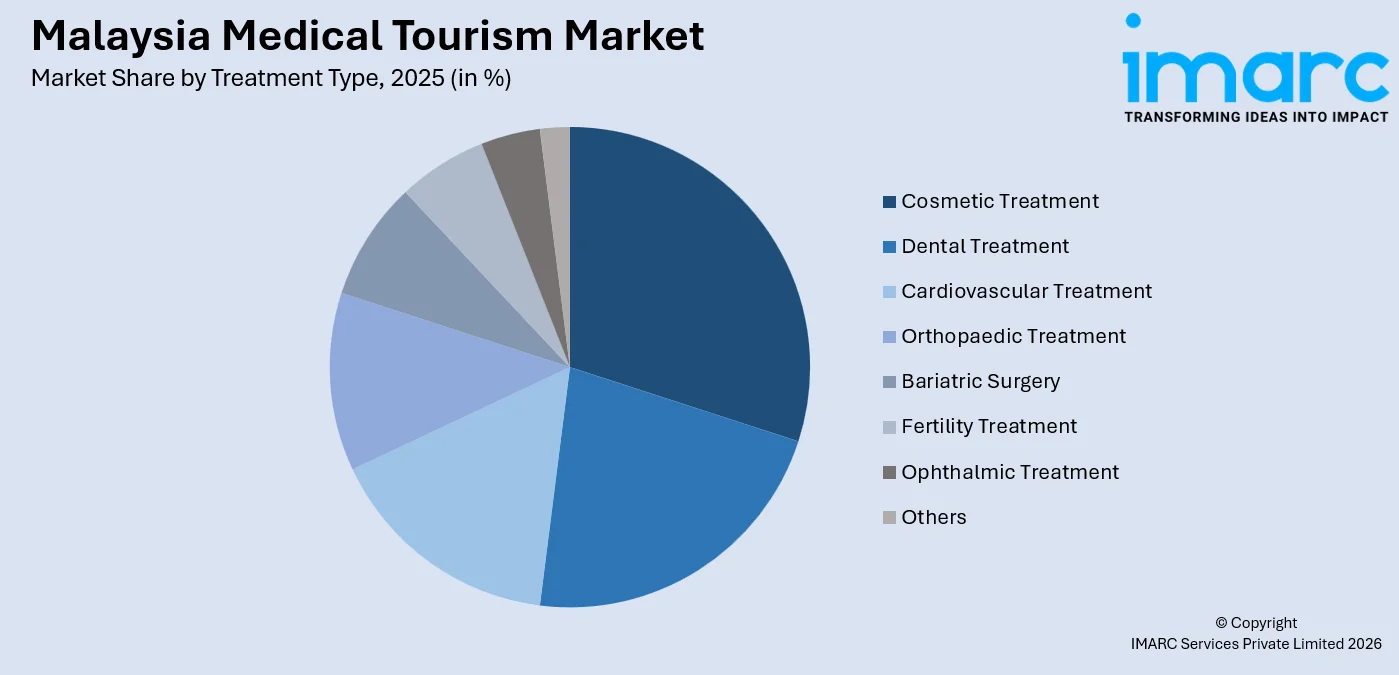

- Cosmetic treatment leads the treatment type at 20.3% in 2025 - demand from Indonesian and Middle Eastern patients for aesthetic procedures is exceptionally strong, and Malaysia’s board-certified plastic surgeons, combined with post-procedure recovery packages, have made it a preferred destination for cosmetic work over pricier alternatives in Singapore or South Korea.

- Selangor dominates state-level activity at 36.2% in 2025 - the sheer density of private hospitals, specialist centers, and international airport connectivity in the Klang Valley makes Selangor the natural hub for foreign patient intake, and that structural advantage is unlikely to shift materially regardless of how other states grow.

Malaysia Medical Tourism Market Trends and Dynamic 2026

Market Trends

Indonesia remains Malaysia’s most important source market and the relationship is deepening

The Indonesian patients have been the pillars of medical tourism in Malaysia. This is due to the increase in Indonesia's middle class, who expect high-standard healthcare facilities in foreign nations. According to the Malaysian Investment Development Authority report issued in September 2024, currently, the biggest source of medical tourists for Malaysia is Indonesia. In 2023 alone, 64.9% of the total medical tourists visiting Malaysia were from Indonesia.

Digital health platforms and telemedicine are changing the way medical tourists choose Malaysian hospitals

Medical tourists now visit hospitals in Malaysia after conducting extensive research. They are aware of all the details about the surgeries they need to undergo and even have a pre-surgery video conference with the surgeons before booking their tickets. In September 2025, a secure communication platform was launched by KPJ Healthcare and NetSfere in all 30 medical facilities in Malaysia.

Government-backed promotion is more targeted and commercially aggressive.

Malaysia Healthcare Travel Council (MHTC) operates with an explicit mandate to grow healthcare tourist revenues and has become one of the region’s more sophisticated medical tourism marketing bodies. In September 2024, MHTC led a delegation visit to Xiamen, China, to strengthen collaboration with Chinese partners and promote Malaysia as a preferred medical travel destination.

- Middle East Patient Growth as a Priority Segment: The Gulf Cooperation Council patients are increasingly choosing Malaysia as a preferred medical tourism destination for treatments like oncology, cardiology, and fertility treatments due to accredited facilities, halal facilities, and a high Islamic cultural affinity; it is now becoming extremely difficult for competition to cope.

- Medical Tourism Packages Integrating Wellness and Recovery Tourism: Private healthcare facilities are now offering medical tourism packages that not only include medical procedures but also recovery and wellness, thus making medical tourism in Malaysia an extended form of tourism, benefiting the country’s economy.

- Bangladesh Emerging as a High-Growth Source Market: The growing middle class and lack of medical facilities in Bangladesh have made it one of the fastest-growing source markets for Malaysia, with cardiology, oncology, and orthopedic treatments making up most of the patients from that country.

Growth Drivers

Malaysia’s cost advantage over developed-world healthcare is enormous and structurally durable

Malaysian healthcare costs are rising slowly relative to Western benchmarks, and the country’s favorable exchange rate against major source-market currencies reinforces affordability. The Malaysia Healthcare Travel Council (MHTC) reports that foreign patients can save up to 60–80% on treatments like orthopedic surgery, cosmetic procedures, and cardiology, compared to costs in the U.S. or Europe.

International hospital accreditation gives patients clinical confidence to travel for treatment

The country also has a higher number of Joint Commission International-accredited hospitals compared to other countries in the Asia Pacific region. This has helped patients gain confidence in the quality of clinical services provided in Malaysia. Sunway Medical Centre in Sunway City was accredited with the Joint Commission International (JCI) Gold Seal of Approval in August 2024. It is the first hospital in Malaysia to attain JCI accreditation in addition to the Australian Council on Healthcare Standards (ACHS) and the Malaysian Society for Quality in Health (MSQH) accreditations.

- Well-Developed Healthcare Infrastructure Beyond Kuala Lumpur: Penang has Island Hospital, while Johor Bahru has a major private hospital cluster. Additionally, specialist medical services are now available in Sabah.

- Strong Air Connectivity Enabling Easy Patient Access: Malaysia Airports Holdings and AirAsia’s extensive regional network connects source markets, including Indonesia, Bangladesh, Myanmar, India, and the Middle East. The direct flights to Kuala Lumpur and Penang with high-frequency, low-cost flight options make repeated follow-up visits economically viable.

- Malaysia My Second Home Program Supporting Extended Medical Stay Patients: The MM2H long-stay visa program creates a cohort of affluent foreign residents who utilize Malaysian private healthcare regularly, generating a stable revenue base for private hospitals.

Market Restraints

Heightened Regional Competition: Malaysia is witnessing a surge in regional competition from other players like Thailand, Singapore, and India. Thailand's Bumrungrad International and Bangkok Hospital are targeting Indonesia and the Middle Eastern patient market.

Perception of Patient Safety and Liability Issues: The international patient population considering Malaysia as a potential medical tourism spot is often plagued by a lack of clear information about clinical results, patient complaints, and avenues for redressal of liability. This is affecting Malaysia's potential to attract high-value patients from countries like those in the Gulf region and Western nations.

Healthcare Worker Shortage: The private healthcare sector is facing a shortage of specialists in areas like oncology, cardiology, and reproductive medicine. The long training periods for new specialists are also affecting the potential expansion of healthcare services. The hospitals are thus constrained by a shortage of specialists that could allow for a rapid expansion of services to foreign patients without affecting the quality of services for existing patients.

Malaysia Medical Tourism Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Inbound | 78.5% | 2025 |

| Treatment Type | Cosmetic Treatment | 20.3% | 2025 |

| States | Selangor | 36.2% | 2025 |

Type Insights

Inbound - 78.5% market share (2025) | Leading Type

The Malaysia Healthcare Travel Council (MHTC) is the major driver for the dominance of inbound medical tourism. Accreditation of hospitals, international patient services, and government support are provided to ensure that healthcare services are exported. Patients are attracted from Indonesia, Bangladesh, Singapore, and increasingly from the Gulf Cooperation Council countries, where hospitals are recognized by insurers and governments to facilitate reimbursements.

|

Segment Breakdown Inbound (78.5%) · Outbound · Intrabound |

Treatment Type Insights

Access the comprehensive market breakdown Request Sample

Cosmetic Treatment - 20.3% market share (2025) | Leading Treatment Type

The main advantage that Malaysia has over the rest of the world in the field of cosmetic surgery is that it is affordable, and that the standard of cosmetic surgery provided by internationally qualified plastic surgeons in Malaysia is of the highest standard. Kuala Lumpur and Penang have become the new alternatives to Korea and Thailand for cosmetic surgery procedures such as rhinoplasty and breast augmentation, etc.

|

Segment Breakdown Cosmetic Treatment (20.3%) · Dental Treatment · Cardiovascular Treatment · Orthopaedic Treatment · Bariatric Surgery · Fertility Treatment · Ophthalmic Treatment · Others |

States

Selangor - 36.2% market share (2025) | Leading State

Selangor has the largest share of Malaysia’s medical tourism market due to its unparalleled infrastructure, including Klang Valley, where top-tier private hospitals and specialist facilities are located. Renowned hospitals such as Sunway Medical Centre and KPJ Damansara are located in Selangor, along with direct access to airports to facilitate logistics for foreign patients.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

36.2%

|

|

Key States

|

Petaling Jaya, Shah Alam, Subang Jaya, Klang, Kota Damansara, Puchong |

|

Major Growth Drivers

|

Klang Valley hospital cluster density, KLIA and KLIA2 international gateway access, Malaysian private hospital group headquarters concentration, specialist talent pool |

|

Outlook

|

Entrenched leader with active capacity expansion planned through 2028 |

|

States Breakdown Selangor (36.2%) · W.P. Kuala Lumpur · Johor · Sarawak· Others |

W.P. Kuala Lumpur:

W.P. Kuala Lumpur is a notable medical tourism destination with high-end medical facilities such as Gleneagles KL and Prince Court Medical Centre, where international patients seek treatment for cardiovascular diseases, cancer, and orthopedic conditions. The presence of luxury accommodations and business facilities in Kuala Lumpur makes it logistically efficient for international patients to access healthcare services. KPJ Healthcare Bhd stated that operational beds increased by 4% year on year, to facilitate an increase in patient services to cater to the rising medical tourism industry.

|

Metric

|

Details

|

|---|---|

|

Key States

|

City Centre (KLCC/Ampang), Bangsar, KL Sentral, Chow Kit, Cheras, Ampang |

|

Major Growth Drivers

|

JCI-accredited hospital concentration, international insurance reimbursement panel coverage, luxury recovery accommodation availability, specialist physician density |

|

Outlook

|

Premium medical tourism hub anchored by a specialist hospital's prestige |

Johor:

The main driver of the Johor medical tourism market is the demand for medical care from Singaporean residents due to the cheaper cost of healthcare in Malaysia. The demand is mainly for dental care, health check-ups, and day procedures. Johor-Singapore Rapid Transit System, expected to commence in 2027. This is expected to increase the number of patients from Singapore visiting medical facilities in Johor, including the Gleneagles Medini Hospital and the KPJ Johor Specialist Hospital.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Johor Bahru, Medini (Iskandar Puteri), Tebrau, Masai, Pasir Gudang |

|

Major Growth Drivers

|

Singapore cross-border patient flow, RTS Link cross-border accessibility improvement, Iskandar Malaysia economic zone healthcare investment, dental and health screening specialization |

|

Outlook

|

Singapore patient corridor expansion via improved cross-border transport infrastructure |

Sarawak:

Sarawak is an emerging medical tourism destination within Malaysia, anchored by Kuching's growing cluster of private specialist hospitals that primarily draw cross-border patients from Kalimantan (Indonesia) seeking high-quality, affordable care. The state recorded 104,106 medical tourists in 2025, up from 76,796 in 2024 and 64,393 in 2023. In March 2026, the inaugural Borneo Global MediTourism Congress and Expo was launched at the Borneo Convention Centre Kuching, with plans for additional private hospitals already approved and under construction to support the sector's rapid growth.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Kuching, Miri, Sibu, Bintulu, Samarahan |

|

Major Growth Drivers

|

Indonesian cross-border patient proximity, expanding Kuching private hospital cluster, competitive treatment pricing, Royal Brunei Airlines increased Kuching connectivity, Sarawak General Hospital clinical research ecosystem |

|

Outlook

|

Fastest-growing East Malaysian medical tourism hub with active hospital pipeline supporting capacity through 2028 |

Market Outlook 2026-2034

What is the future outlook of the Malaysia Medical Tourism market?

Malaysia Medical Tourism market is expected to sustain steady revenue growth through 2034.

Malaysia is entering the forecast period with considerable structural strengths, including a supportive government that recognizes medical tourism as a key driver of the economy, a robust hospital accreditation system that provides reassurance to international patients, and sustained cost advantages over peer markets. With strong population and economic growth in key source markets such as Indonesia, Bangladesh, and the Gulf Cooperation Council countries, Malaysia is well-placed to realize the long-term revenue ambitions outlined by the Malaysia Healthcare Travel Council.

Malaysia Medical Tourism Market - Leading Key Players

The competitive environment in Malaysia’s medical tourism industry is dominated by large private healthcare groups that collectively manage the majority of foreign patient inflows into these hospitals. IHH Healthcare and KPJ Healthcare are the two largest healthcare conglomerates with a presence across multiple states in Malaysia and an international patient services infrastructure. There is a second layer of independent specialist hospitals and medical clinics that compete on reputation for certain patient segments.

| Company | Leading Brands | Highlights |

|---|---|---|

| IHH Healthcare Malaysia | Gleneagles KL, Gleneagles Penang, Pantai Hospital Cheras, Pantai Hospital Ampang | Malaysia’s largest private hospital group by revenue, JCI-accredited flagship hospitals, dedicated International Patient Services division handling GCC and Indonesian patient coordination; strong cardiac and oncology referral volumes |

| KPJ Healthcare Bhd | KPJ Damansara, KPJ Johor, Selangor Medical Centre, KPJ Penang Specialist | National network with international patient programs across Selangor, Johor, and Penang; active in Indonesian patient market development |

| Sunway Medical Centre | Sunway Medical Centre Velocity, Sunway Specialist Centre Damansara | High-volume Selangor hub with strong Indonesian patient intake; integrated with Sunway resort and retail ecosystem, enabling recovery tourism packages; expanding specialist suite capacity through 2025-26 |

Some of the existing key players in the market are Prince Court Medical Centre, Island Hospital Penang, Tropicana Medical Centre, Columbia Asia Hospital, Penang Adventist Hospital, Gleneagles Medini Johor, and Beacon Hospital, etc.

Latest Development & News

- In March 2026, IHH Healthcare Malaysia received recognition for the third consecutive year in the prestigious “World’s Best Hospitals 2026” listing published by Newsweek, with several healthcare facilities in Malaysia making it into the coveted listing for delivering high-end healthcare services. This is an endorsement of Malaysia’s reputation as a hub for top-notch healthcare, making it an ideal medical tourism hub.

- In August 2025, the Malaysia Healthcare Travel Council (MHTC) launched the “Malaysia Year of Medical Tourism 2026” campaign with the tagline “Healing Meets Hospitality.” It aims to establish Malaysia as a premier medical tourism destination in the world. It highlights Malaysia’s high-quality healthcare services and professionals, as well as its wellness programs, in an attempt to increase the number of foreign patients and revenues.

- In June 2025, KPJ Healthcare Bhd awarded nearly MYR 31.97 million in renovation contracts for upgrades at its Damansara Specialist Hospital campuses. It includes two contracts to JLG & BP Design Sdn Bhd (JLGBP) for MYR 21.47 million for the design, construction, and commissioning of Levels 8 and 9 (Premier Ward) at Damansara Specialist Hospital 2 (DSH2), and RM10.50 million for renovation and façade upgrades at KPJ Damansara Specialist Hospital (DSH).

Malaysia Medical Tourism Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Outbound, Inbound, Intrabound |

| Treatment Types Covered | Cosmetic Treatment, Dental Treatment, Cardiovascular Treatment, Orthopaedic Treatment, Bariatric Surgery, Fertility Treatment, Ophthalmic Treatment, Others |

| States Covered | Selangor, W.P. Kuala Lumpur, Johor, Sarawak, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Malaysia medical tourism market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Malaysia medical tourism market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Malaysia medical tourism industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Malaysia Medical Tourism Market Report

Malaysia medical tourism market was valued at USD 521.5 Million in 2025.

The market is anticipated to reach a value of USD 3,285.3 Million by 2034.

Inbound dominates the market with a share of 78.5% in 2025. Foreign patients drive Malaysia’s medical tourism revenues, supported by MHTC’s structured international patient acquisition programs and the competitive cost-quality proposition of Malaysian private hospitals.

Cosmetic treatment leads the market at 20.3% in 2025. Malaysian plastic surgeons’ international training credentials, hospital accreditation standards, and significantly lower procedure costs compared with those in South Korea, Singapore, and Western destinations make Malaysia a popular cosmetic surgery destination.

Selangor dominates at 36.2% in 2025. The hospital cluster density of the Klang Valley, direct international airport access via KLIA and KLIA2, and the presence of multiple JCI-accredited hospital infrastructure with international patient services infrastructure in place make Selangor the default primary destination of the majority of medical tourists arriving in Malaysia.

Some of the major players in the Malaysia medical tourism market include IHH Healthcare Malaysia, KPJ Healthcare Bhd, Sunway Medical Centre, Prince Court Medical Centre, Island Hospital Penang, Tropicana Medical Centre, Columbia Asia Hospital, Penang Adventist Hospital, Gleneagles Medini Johor, and Beacon Hospital, etc.

The major trends are the accelerating growth of patient volumes in Indonesia, driven by proximity and price advantage, the rapid growth of digital patient acquisition platforms that facilitate pre-arrival specialist consultations, and MHTC’s improved trade mission targeting in Gulf and South Asian markets.

The major challenges are increased competition from Thailand’s medical tourism hub led by Bumrungrad Hospital, competition from India’s lower-cost specialist hospitals, a dearth of senior medical specialists in key specialties, and a lack of clinical outcomes transparency compared with JCI-accredited competitors in Singapore and Bangkok.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)