Managed Print Services Market Size, Share, Trends and Forecast by Type, Deployment Mode, Organization Size, Industry Vertical, and Region, 2026-2034

Global Managed Print Services Market Size, Share, Trends & Forecast (2026-2034)

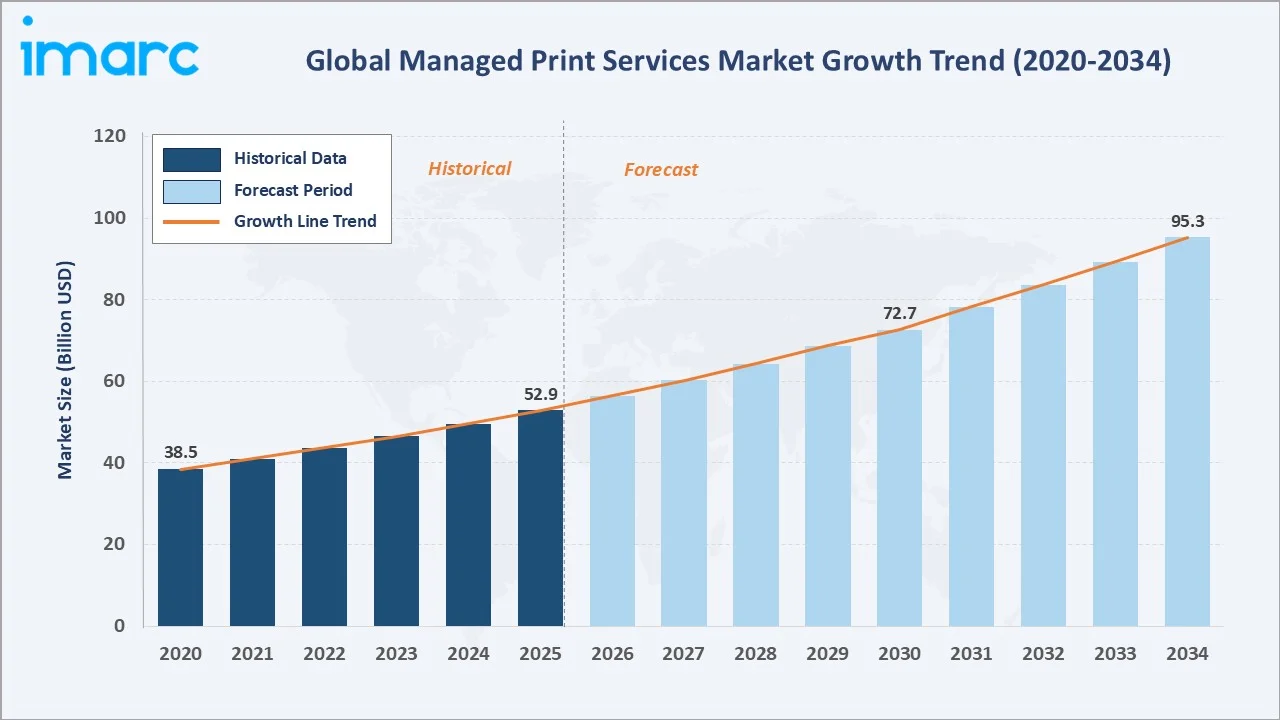

The global managed print services market size was valued at USD 52.9 Billion in 2025 and is projected to reach USD 95.3 Billion by 2034, exhibiting a CAGR of 6.56% during the forecast period 2026-2034. Rising enterprise focus on print cost optimization, accelerating cloud-based MPS adoption, growing cybersecurity requirements for document management, and expanding demand from small and medium enterprises (SMEs) are driving managed print services market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 52.9 Billion |

|

Forecast Market Size (2034) |

USD 95.3 Billion |

|

CAGR (2026-2034) |

6.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (33.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~7.5%) |

|

Leading Type |

Device Management (31.6%, 2025) |

|

Leading Deployment Mode |

Cloud-based (56.8%, 2025) |

The global managed print services market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by digital transformation, enterprise cost reduction strategies, and cloud-based service adoption across large enterprises and SMEs worldwide.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlighting cloud-based deployment and device management expansion as the fastest-growing sub-categories within the global managed print services market forecast through 2034.

Executive Summary

The global managed print services market is undergoing a significant transformation. It is driven by enterprise-wide digitization initiatives, mounting pressure to reduce operational print costs, and the accelerating shift toward cloud-managed infrastructure. Valued at USD 52.9 Billion in 2025, the market is forecast to reach USD 95.3 Billion by 2034 at a CAGR of 6.56%.

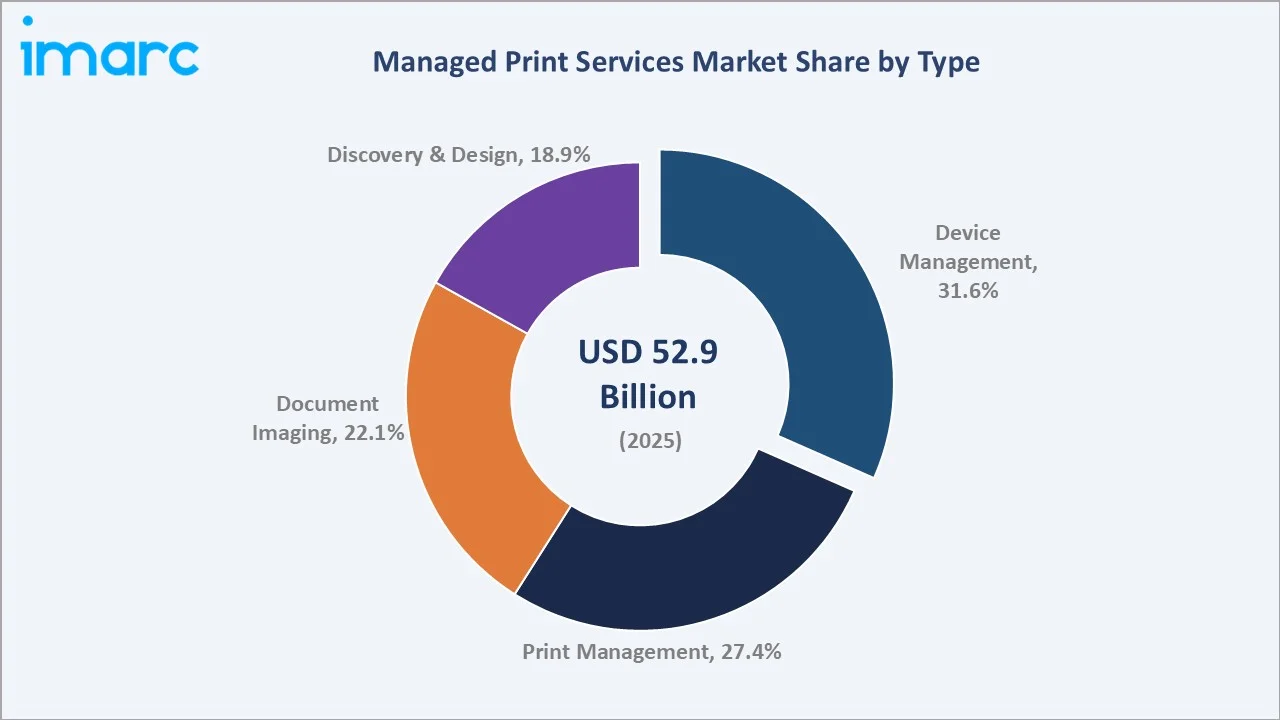

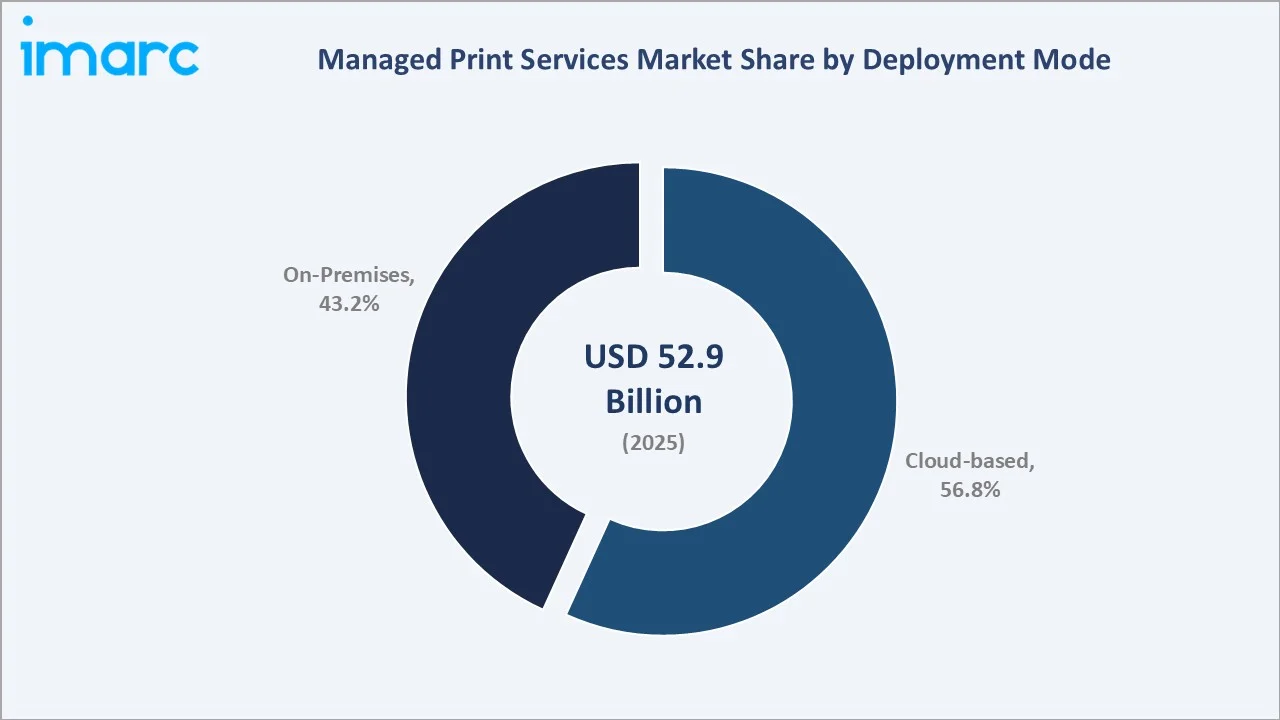

Device Management commands 31.6% share in 2025, driven by fleet optimization and predictive maintenance demand. Print Management follows at 27.4%, propelled by cost-control mandates and usage analytics capabilities. Cloud-based deployment represents 56.8% of global demand, outpacing on-premises alternatives as enterprises prioritize scalability, remote management, and reduced IT infrastructure investment.

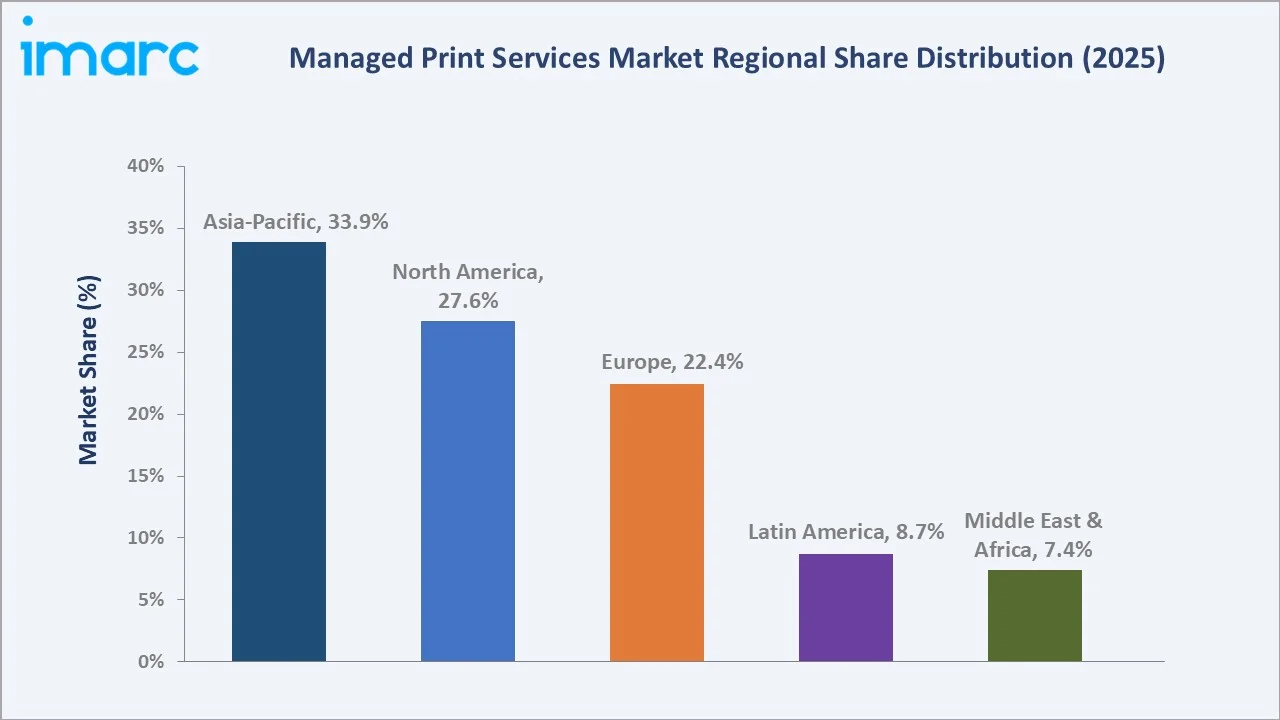

Asia-Pacific leads with 33.9% global revenue share in 2025, supported by rapid enterprise expansion across China, India, Japan, and Australia. North America holds 27.6% and Europe 22.4%. The managed print services market outlook remains positive as cost optimization, security compliance, and AI-driven print analytics converge across all major markets through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Device Management – 31.6% share (2025) |

|

Second Type |

Print Management – 27.4% share (2025) |

|

Leading Deployment Mode |

Cloud-based – 56.8% share (2025) |

|

Fastest Growing Deployment Mode |

Cloud-based Deployment – ~8.5% CAGR (2026-2034) |

|

Leading Region |

Asia-Pacific – 33.9% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific – ~7.5% CAGR (2026-2034) |

|

Top Companies |

Xerox Holdings Corporation, HP Development Company, L.P., Ricoh, Konica Minolta Inc., Canon Inc., KYOCERA Document Solutions Inc. |

|

Market Opportunity |

Cloud-MPS in SME segment – 8.5% CAGR through 2034 |

Key Analytical Observations Supporting the Above Data:

- Device Management's 31.6% dominance in 2025 reflects the growing enterprise need for real-time fleet monitoring, automated toner replenishment, and predictive maintenance contracts across multifunction device (MFD) fleets exceeding 10 units.

- Print Management's 27.4% share is driven by advanced usage tracking, per-page cost visibility, and chargeback automation. Organizations with 500+ employees increasingly mandate print management as part of IT governance and sustainability reporting.

- Cloud-based deployment's 56.8% majority underscores the accelerating shift away from on-premises print servers. Microsoft Azure Virtual Desktop and AWS WorkSpaces integrations are enabling seamless cloud-print environments, driving adoption especially in hybrid-work organizations.

- Asia-Pacific's 33.9% global dominance reflects rapid enterprise modernization in China and India. India's Digital India initiative and China's enterprise IT upgrade cycle are creating structured procurement pipelines for managed print contracts across BFSI, government, and manufacturing verticals.

- SME segment represents the fastest-growing end-user tier. Small and medium enterprises are adopting as-a-service MPS models to eliminate capital expenditure on printer hardware, with per-page pricing models reducing upfront costs versus outright hardware purchases.

Global Managed Print Services Market Overview

Managed Print Services (MPS) encompass end-to-end outsourcing of an organization's print infrastructure, including hardware procurement, fleet management, consumables supply, maintenance, and document workflow optimization. The global market spans a broad portfolio of service offerings covering device management, print management, document imaging, and discovery and design solutions. These services are delivered through cloud-based and on-premises deployment models, serving large enterprises, medium enterprises, and small enterprises across BFSI, government, healthcare, education, manufacturing, and retail verticals.

The industry operates at the convergence of IT services, document management, and enterprise cost optimization. Growth is supported by macroeconomic drivers such as rising operational costs, digital transformation mandates, and hybrid-work adoption. At the same time, the market is undergoing a structural shift toward cloud-native, AI-enabled, and security-integrated MPS solutions, which are redefining service delivery, contract structures, and competitive differentiation on a global scale.

Market Dynamics

To evaluate market opportunities, Request Sample

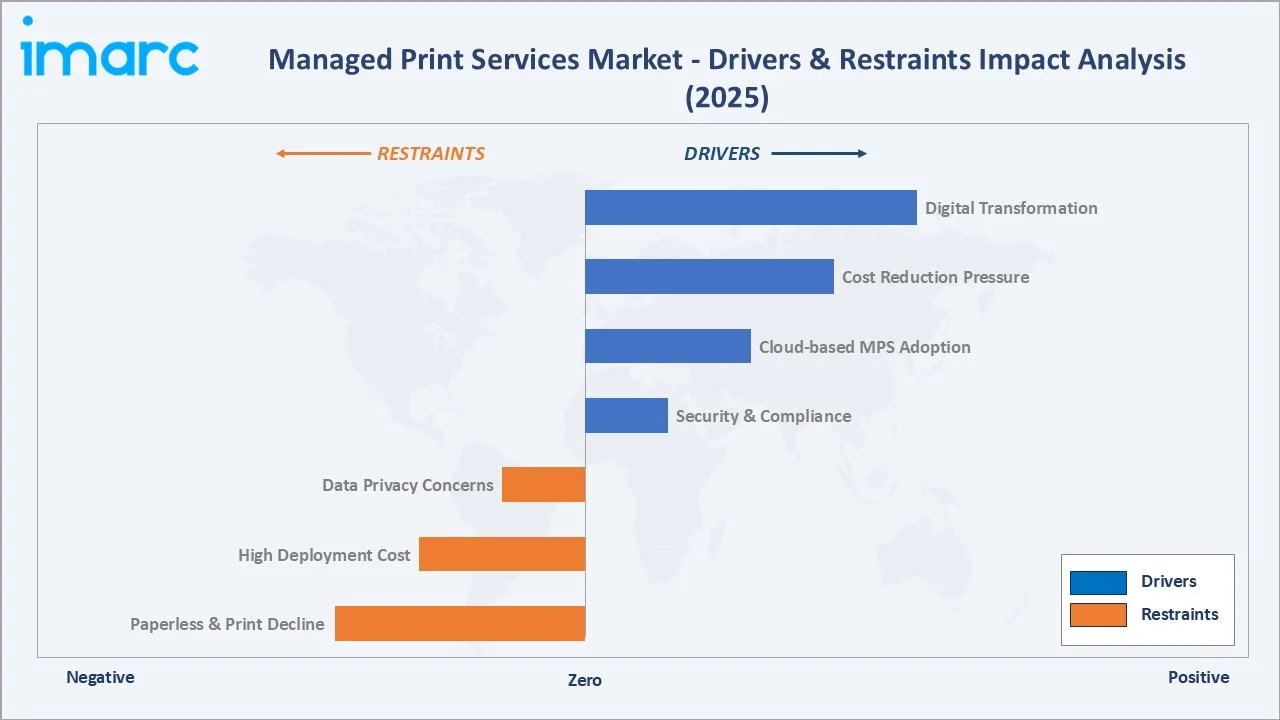

Market Drivers

- Digital Transformation and Enterprise IT Modernization: Organizations are embedding MPS contracts within broader digital transformation programs. IDC estimated global digital transformation spending at USD 2.3 Trillion in 2023, with print infrastructure consolidation a standard cost-reduction lever. MPS providers are pivoting to become document digitization partners, not just hardware managers.

- Cost Reduction and Operational Efficiency: Enterprises report print cost savings after deploying managed print contracts. Per-page pricing models eliminate unpredictable consumable expenditure. Automated meter reads and remote monitoring reduce IT help desk workloads in large enterprise deployments, reinforcing the ROI case for MPS adoption.

- Cloud-based MPS and Hybrid Work Expansion: The rise of hybrid work has accelerated cloud-print adoption. Cloud-based MPS eliminates the need for on-premises print servers, enabling print from any device or location. Microsoft Universal Print integration with Azure Active Directory has become a standard deployment configuration for enterprise MPS contracts from 2023 onward.

- Security and Compliance Requirements: Print endpoints represent a significant but often under-managed cybersecurity vulnerability. GDPR, HIPAA, and ISO 27001 compliance mandates are driving formal print security policies. Secure pull-printing, encrypted document workflows, and audit trail capabilities are increasingly specified as contractual requirements, expanding the average MPS contract value.

Market Restraints

- Declining Print Volumes: Global print volumes have declined since 2019. The shift toward digital-first document workflows, e-invoicing mandates, and paperless office initiatives in Scandinavia, Germany, and Singapore are structurally reducing the addressable hardware base for traditional MPS contracts.

- High Implementation and Transition Costs: Organizations face significant upfront expenses for infrastructure upgrades, legacy system integration, and workflow redesign. Migration complexity, employee training requirements, and potential operational disruptions further increase total cost of ownership, limiting adoption, especially among cost-sensitive SMEs.

- Data Privacy and Cloud Adoption Hesitancy: Financial services and healthcare organizations in emerging markets exhibit reluctance toward cloud-based MPS due to data residency regulations and concerns over third-party document access. This constrains cloud-MPS penetration in high-sensitivity verticals, particularly across Latin America and the Middle East.

Market Opportunities

- SME Market Penetration via As-a-Service Models: SMEs represent the largest untapped MPS opportunity. As-a-service (aaS) MPS models enabling zero-capex, fully-managed print environments are gaining traction. The global SME print services addressable market is estimated by 2030, with cloud-native providers specifically targeting sub-100-employee organizations.

- AI and Predictive Analytics Integration: AI-driven print analytics platforms enable predictive maintenance, usage forecasting, and automated consumable ordering. Xerox's Intelligent Workplace Services platform and HP's Managed Print Cloud Services / HP Smart Admin analytics are embedding machine learning capabilities into MPS contracts.

- Emerging Market Expansion: India, Southeast Asia, and Africa present significant greenfield MPS opportunity. India's IT services industry supports over 5.43 million enterprise workers requiring structured print management. Government-mandated digitization programs in Indonesia, Vietnam, and Kenya are generating formal MPS procurement tenders.

Market Challenges

- Integration Complexity with Legacy IT Infrastructure: Many enterprise clients operate heterogeneous printer fleets spanning manufacturer brands. Unified fleet management requires middleware integration layers that extend deployment timelines and increase professional services costs for MPS providers.

- Talent Shortage in Field Services: MPS providers depend on certified field service engineers for hardware maintenance. The global shortage of field service talent, compounded by increasing device complexity, is elevating service delivery costs and extending mean-time-to-repair (MTTR) metrics in emerging-market deployments.

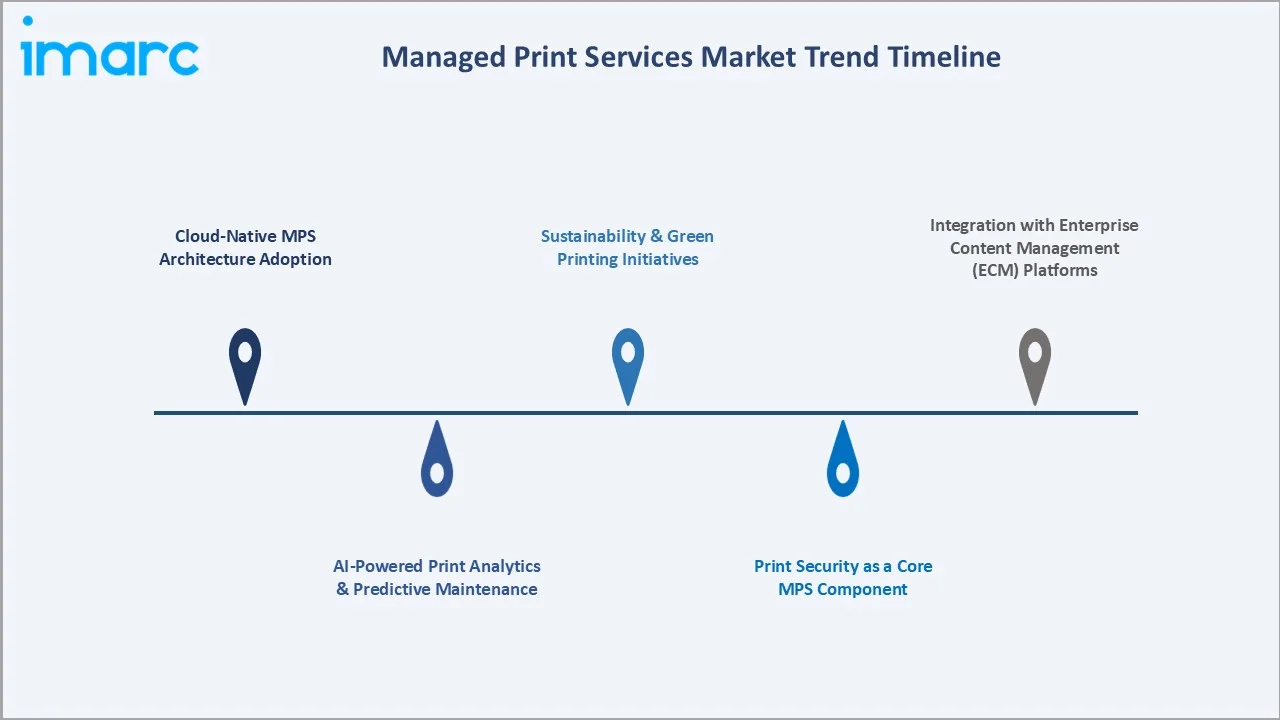

Emerging Market Trends

1. Cloud-Native MPS Architecture Adoption

Cloud-based MPS is becoming the dominant deployment architecture, accounting for 56.8% of the market in 2025. Microsoft Universal Print, Google Cloud Print alternatives, and vendor-specific cloud platforms (Xerox Connectkey, HP Smart, Ricoh Streamline NX) are enabling fully managed, serverless print environments. By 2030, cloud-MPS is projected to surpass 70% of all new MPS contract deployments globally.

2. AI-Powered Print Analytics and Predictive Maintenance

Artificial intelligence is transforming MPS from reactive break-fix models into proactive, analytics-driven service delivery. Machine learning algorithms now predict toner depletion in advance, reducing emergency service calls. HP Inc.'s print analytics dashboard and Ricoh's Smart Device Monitor platform are setting benchmarks for AI-integrated MPS capabilities.

3. Print Security as a Core MPS Component

Embedded print security is transitioning from an optional add-on to a mandatory contractual component. Secure pull-printing, user authentication at the device, and encrypted transmission protocols are standard in government and financial services MPS tenders. The print security market within MPS is estimated to grow through 2030, outpacing the broader market.

4. Sustainability and Green Printing Initiatives

ESG reporting mandates are embedding sustainability KPIs into MPS contracts. Metrics such as paper consumption reduction, CO₂ emissions per printed page, and end-of-life device recycling rates are now standard service level agreement (SLA) components. HP and Konica Minolta have introduced carbon-neutral MPS tiers that offset print-related emissions through certified programs.

5. Integration with Enterprise Content Management (ECM) Platforms

MPS providers are expanding into document digitization and workflow automation, integrating with ECM platforms such as Microsoft SharePoint, OpenText, and Hyland. This "intelligent document gateway" positioning increases average contract values and extends contract durations, improving revenue visibility for MPS providers.

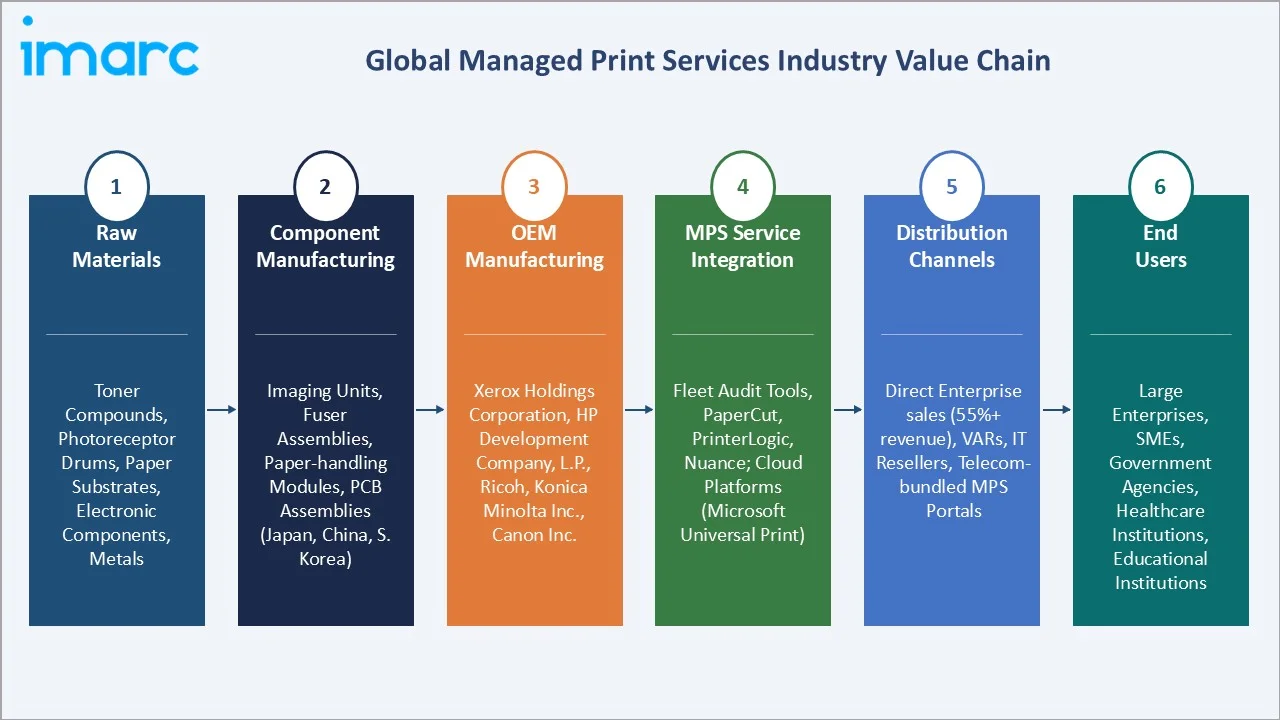

Industry Value Chain Analysis

The global managed print services industry value chain spans six integrated stages from raw material supply through end-user service delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall managed print services market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Toner compounds, photoreceptor drums, paper substrates, electronic components, metals for chassis and roller assemblies |

|

Component Manufacturing |

Imaging units, fuser assemblies, paper-handling modules, and PCB assemblies – produced by Tier-2/3 suppliers in Japan, China, and South Korea |

|

OEM Manufacturing |

Xerox Holdings Corporation, HP Development Company, L.P., Ricoh – full MFD assembly, firmware development, and certification |

|

MPS Service Integration |

Fleet audit tools, monitoring agents, print management software (PaperCut, PrinterLogic), and cloud platforms (Microsoft Universal Print) |

|

Distribution Channels |

Direct enterprise sales (55%+ of revenue), VARs, IT resellers, telecom-bundled MPS, and online procurement portals |

|

End Users |

Large enterprises (>1,000 employees), medium enterprises, SMEs, government agencies, healthcare institutions, and educational institutions |

OEM manufacturers and MPS service integrators hold the highest strategic value by combining hardware, software, and service delivery into turnkey contracts. Meanwhile, cloud platforms and direct enterprise channels are reshaping distribution, enabling MPS providers to bypass intermediaries and capture higher margin recurring revenue.

Technology Landscape in the Managed Print Services Industry

Cloud Print Infrastructure

Cloud-based print management is the fastest-evolving technology layer within MPS. Microsoft Universal Print, embedded within Microsoft 365 E3/E5 subscriptions, has become the de facto cloud-print standard for enterprise MPS deployments. Vendor platforms including Xerox ConnectKey, HP Smart Admin, and Ricoh Streamline NX Cloud are enabling zero-server print environments. Cloud-MPS eliminates on-premises print server maintenance costs annually for large enterprise deployments.

AI and Predictive Analytics

Machine learning platforms embedded in MPS contracts analyze real-time device telemetry to predict failures, optimize fleet configurations, and automate consumable replenishment. Lexmark's OptraLink and Konica Minolta's Workplace Pure platform exemplify AI-driven MPS analytics. Predictive maintenance models achieve high accuracy in toner-depletion forecasting, reducing emergency service dispatches versus reactive maintenance models.

Print Security Technologies

Print security encompasses pull-printing (PIN or card authentication), network-level traffic encryption (IPsec, TLS 1.3), device firmware integrity verification, and SIEM integration for audit trail management. HP Wolf Security for Printers and Xerox Security Solutions represent enterprise-grade embedded security stacks. NIST SP 800-171 and CIS Benchmark compliance are increasingly mandated in government MPS contracts from 2024 onward.

Automation and IoT Connectivity

IoT-enabled MPS devices transmit operational data across MQTT and REST API protocols to centralized management platforms, enabling real-time fleet visibility across distributed enterprise locations. Automated meter submission, remote firmware updates, and dynamic routing of print jobs to the nearest available device are standard IoT-enabled MPS features. By 2028, most new enterprise MPS contracts are projected to include IoT monitoring as a baseline service component.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Device Management |

31.6% |

2025 |

| Deployment Mode | Cloud-based | 56.8% |

2025 |

| Organization Size | Large Enterprises |

🔒 |

2025 |

| Industry Vertical | BFSI |

🔒 |

2025 |

|

Region |

Asia-Pacific | 33.9% |

2025 |

By Type

To access detailed market analysis, Request Sample

Device Management leads the global managed print services market type with a 31.6% share in 2025. Demand is driven by enterprises seeking to consolidate heterogeneous printer fleets under unified monitoring and maintenance contracts. Device management services include real-time status monitoring, automated toner replenishment, predictive maintenance dispatch, and end-of-life device replacement. The sub-segment is projected to grow at approximately 7.2% CAGR through 2034.

By Deployment Mode

Cloud-based deployment is the dominant mode at 56.8% of global demand in 2025. The shift to cloud-MPS accelerated significantly during 2020–2022 as hybrid work models eliminated the operational case for on-premises print servers. Cloud deployment reduces IT infrastructure maintenance costs and enables centralized management of geographically distributed fleets. Cloud-MPS is projected to reach 68–72% of deployments by 2034 as Microsoft Universal Print adoption deepens.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

33.9% |

Enterprise modernization in China, India Digital India, Japan IT outsourcing, ASEAN urbanization |

|

North America |

27.6% |

Cost-reduction mandates, hybrid work MPS demand, EPA compliance, HIPAA print security |

|

Europe |

22.4% |

GDPR print compliance, EU sustainability mandates, public sector MPS tenders |

|

Latin America |

8.7% |

Enterprise IT expansion in Brazil & Mexico, manufacturing sector MPS growth |

|

Middle East & Africa |

7.4% |

GCC Vision 2030 programs, digital government initiatives, SME sector expansion |

Asia-Pacific commands 33.9% global revenue share in 2025. Japan is the most mature MPS market in the region, with Ricoh and Canon commanding dominant domestic positions through comprehensive outsourcing contracts. China's enterprise IT modernization and India's Digital India program are generating structured procurement volumes.

North America holds 27.6% of global revenue, anchored by large enterprise MPS contracts in the United States. U.S. federal government MPS contracts administered through the General Services Administration (GSA) Schedule represent multi-year, multi-hundred-million-dollar procurement programs. HIPAA print security mandates are driving healthcare MPS replacement cycles. Hybrid work adoption across Fortune 1000 companies is accelerating cloud-MPS transitions.

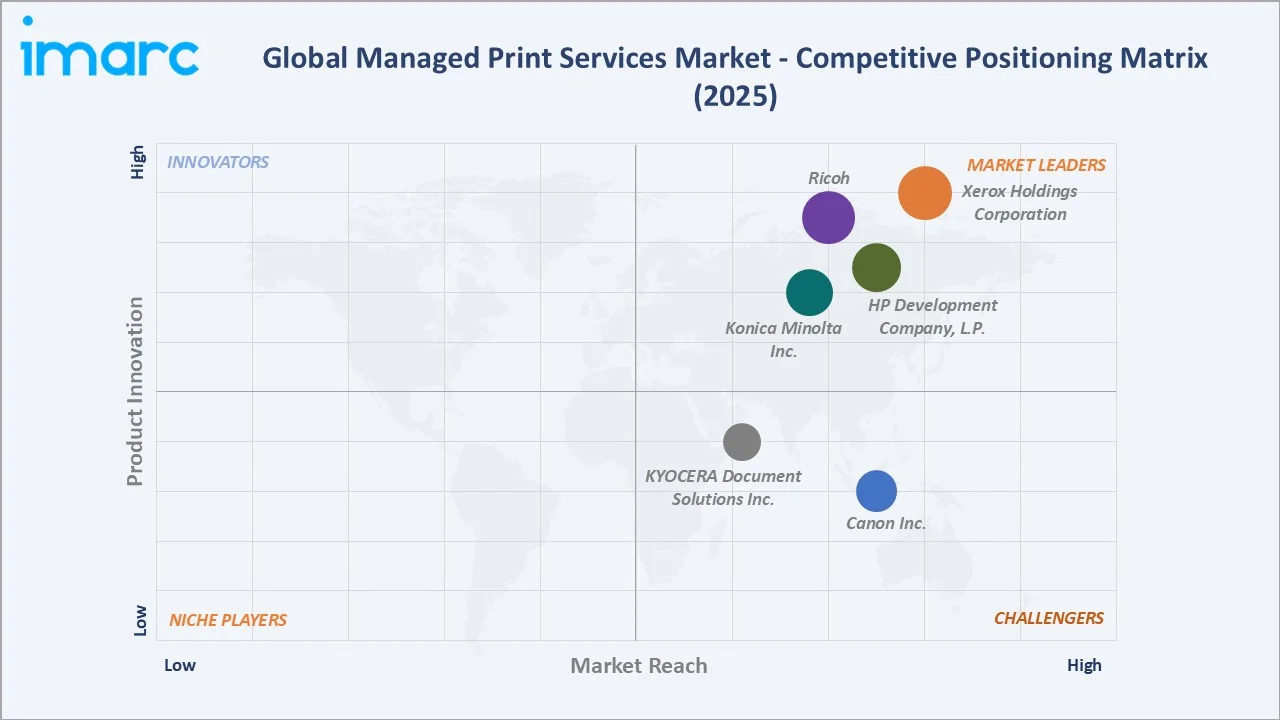

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Xerox Holdings Corporation |

Xerox Workplace Cloud |

Leader |

End-to-end MPS, global enterprise contracts, AI analytics |

|

HP Development Company, L.P. |

HP Smart, Wolf Security |

Leader |

Cloud-print, cybersecurity integration |

|

Ricoh |

Ricoh Streamline NX, Always Current Technology |

Leader |

Document workflow, cloud ECM integration, Japan-APAC reach |

|

Konica Minolta Inc. |

Workplace Pure, bizhub SECURE |

Leader |

IT services MPS, All Covered IT, security-led contracts |

|

Canon Inc. |

uniflow Online |

Challenger |

SME segment, OCR-integration, Asia-Pacific volume |

|

KYOCERA Document Solutions Inc. |

Kyocera Fleet Services (KFS) |

Challenger |

Total Document Solutions, Japan-EMEA strength |

The global managed print services market's competitive landscape is moderately concentrated, with global technology firms competing alongside regional specialists and hardware-led IT services providers. Leading players compete on service breadth, IoT platform capability, cloud-print integration, security certification compliance, and sustainability credentials.

Key Company Profiles

Xerox Holdings Corporation

Xerox Holdings Corporation is a publicly listed American workplace technology company specializing in document management, print solutions, and digital services. Xerox provides integrated hardware, software, and services that help organizations manage information across both physical and digital environments.

- Product Portfolio: Xerox's MPS portfolio spans Connectkey-enabled multifunction devices, xerox workplace cloud platform, Xerox Intelligent Workplace Services, DocuShare content management, and XMPie personalization software. Xerox serves 95% of Fortune 100 companies with MPS contracts.

- Recent Developments: In 2025, Xerox launched a new AI-powered intelligent document processing solution, strengthening its Managed Print Services (MPS) and document workflow capabilities. The solution (EveryDoc IDP App) is designed to bridge structured and unstructured data, enabling organizations to automate document extraction, improve data insights, and accelerate business processes with reduced IT complexity and costs.

- Strategic Focus: Xerox's strategy centers on AI-driven MPS differentiation, expansion of IT services alongside print contracts, and cloud-platform development. Xerox targets 60% of revenue from software and services by 2027, reducing hardware dependency.

HP Development Company, L.P.

HP Development Company, L.P. is a global technology leader in personal systems and printing, headquartered in Palo Alto, California, USA. The company focuses on delivering innovative hardware, software, and services that enable productivity, hybrid work, and digital transformation across consumer and enterprise segments.

- Product Portfolio: HP's MPS portfolio includes HP Smart Admin cloud-print platform, HP Wolf Security for Printers, HP Amplify Impact sustainability program, HP LaserJet and OfficeJet Pro enterprise MFDs, and HP PageWide XL large-format systems. HP holds the largest installed base of enterprise printers globally.

- Recent Developments: In 2025, HP Development Company, L.P. enhanced its Managed Print Services (MPS) subscription offering with faster onboarding and improved user experience. The update introduces a mobile-friendly subscription management tool for real-time monitoring of supply levels, consumable orders, and usage trends, along with an automated onboarding solution that accelerates connectivity to the HP cloud and service activation.

- Strategic Focus: HP's MPS strategy focuses on security-led differentiation, SME as-a-service model expansion, and sustainability leadership. HP targets carbon neutrality in its print products by 2030 under its HP Climate Action commitment.

Ricoh

Ricoh is a Japanese multinational imaging and electronics company headquartered in Tokyo, Japan. The company provides a broad portfolio of hardware, software, and services that enable organizations to manage information efficiently across physical and digital environments.

- Product Portfolio: Ricoh's MPS portfolio encompasses Ricoh Streamline NX cloud-print management, Always Current Technology (ACT) for firmware-current MFD fleets, Ricoh Smart Integration for ECM connectivity, and the IM-series MFDs with embedded IoT telemetry.

- Recent Developments: In 2025, Ricoh was recognized as a Leader in the Quocirca Managed Print Services (MPS) Landscape 2025 report, reinforcing its strong global positioning in the MPS market. The recognition highlights Ricoh’s continued investment in partnerships, automation, and service innovation, along with its ability to deliver integrated print, workflow, and digital transformation solutions.

- Strategic Focus: Ricoh's MPS strategy emphasizes digital workflow integration, ECM-connected print services, and services-led revenue growth. Ricoh targets 70% of group revenue from services and solutions by fiscal 2027, up from 55% in fiscal 2024.

Market Concentration Analysis

The global managed print services market exhibits moderate concentration. The top five players – Xerox Holdings Corporation, HP Development Company, L.P., Ricoh, Konica Minolta Inc., Canon Inc.– collectively account for approximately 40–48% of global market revenue in 2025.

The market is experiencing a bifurcated dynamic. At the enterprise tier, consolidation is occurring around integrated IT-plus-print outsourcing platforms, cloud-management capabilities, and security certification. Top-tier MPS contracts are dominated by the top 5 vendors. Simultaneously, the SME segment remains highly fragmented, with hundreds of regional IT resellers and VARs delivering managed print under OEM-branded programs such as HP Amplify, Xerox Authorized Agent, and Konica Minolta Dealer Channel.

Consolidation activity is intensifying. Private equity-backed regional MPS providers are being acquired by global IT services firms seeking to bundle print management within broader managed services portfolios. This dual dynamic – enterprise consolidation plus SME fragmentation – will persist through 2034, with the top 5 players collectively projected to command 50–55% of global revenue by 2030 as enterprise contract renewals increasingly favor incumbent global providers.

Investment & Growth Opportunities

Fastest-Growing Segments

Cloud-based MPS deployment is the highest-growth sub-segment through 2034. Device Management services represent the largest absolute revenue opportunity, growing significantly over the forecast period. Print security integration is the premium technology growth tier, commanding per-device price premiums over standard MPS contracts.

Emerging Market Expansion

India represents the highest-potential emerging MPS market. India's IT-BPO sector and Digital India enterprise expansion are creating structured demand for cloud-MPS contracts across Bengaluru, Hyderabad, and Chennai enterprise campuses. Southeast Asia's manufacturing MPS expansion, Saudi Arabia's Vision 2030 government digitization, and Sub-Saharan Africa's enterprise IT formalization collectively represent incremental MPS opportunity by 2034.

Venture and Strategic Investment Trends

Private equity and strategic capital are targeting AI-driven MPS analytics platforms, print security software, and cloud-print management SaaS companies. Konica Minolta's venture arm, Konica Minolta Ignite, has invested in print workflow automation startups. HP Pathfinder Labs actively scouts document AI and cloud-print innovations. Investments in ISO 15408 (Common Criteria)-certified print security platforms, Microsoft Universal Print ISV integrations, and ESG-linked MPS reporting tools are the primary focus areas for venture and corporate capital in the MPS industry through 2034.

Future Market Outlook (2026-2034)

The global managed print services market forecast projects steady value expansion from USD 52.9 Billion in 2025 to USD 95.3 Billion by 2034 at a CAGR of 6.56%. Asia-Pacific will retain regional leadership while accelerating structurally toward digital-first MPS architectures. North America and Europe will sustain premium value growth through enterprise contract renewals, security-compliance upgrades, and sustainability-linked service tiers.

Technological disruption from AI, IoT, and cloud-native print platforms will reshape competitive dynamics. Pure hardware-centric MPS vendors face margin compression as cloud-software-first providers capture recurring SaaS revenue streams. By 2028, AI-driven fleet optimization and predictive maintenance are projected to be standard contract inclusions across all enterprise MPS tiers, replacing reactive break-fix models as the dominant service delivery paradigm.

Industry transformation through 2034 will be defined by three macro-shifts: the integration of print management within broader IT outsourcing (ITO) contracts, the convergence of document digitization and MPS into unified intelligent document services, and the formalization of sustainability and ESG performance metrics within MPS SLAs. Vendors that successfully position as intelligent document ecosystem partners – rather than hardware fleet managers – will command the highest contract values and retention rates in the post-2026 MPS market.

Research Methodology

Primary Research

IMARC Group conducted structured interviews with 120+ industry participants including MPS contract managers, procurement directors, IT outsourcing specialists, field service engineers, and C-suite executives across enterprise clients and MPS providers in 18 countries. Primary research provided qualitative validation of quantitative market estimates and captured real-time pricing, contract structure, and competitive positioning insights not available from secondary sources.

Secondary Research

Secondary research encompassed analysis of company annual reports, SEC filings, IDC Worldwide Print Hardcopy Market Tracker, Gartner Magic Quadrant for Managed Print and Content Services, Quocirca Print 2025 Global Market Insights, government procurement databases, industry association publications (BTA, AIIM), and patent filing databases. Market sizing is anchored by cross-referencing device shipment data with per-device average revenue per contract.

Forecasting Models

Market forecasts are generated using econometric regression models incorporating macroeconomic indicators (GDP growth, enterprise IT spending indices), device shipment data, contract renewal cycle analysis, and technology adoption S-curve models for cloud-MPS penetration. Bottom-up segment-level forecasts are validated against top-down macro models, with scenario analysis conducted for base-case, optimistic (+1.2% CAGR), and conservative (-0.9% CAGR) trajectories. All market size estimates are expressed in constant 2025 USD.

Managed Print Services Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Print Management, Device Management, Discovery and Design, Document Imaging |

| Deployment Modes Covered | On-premises, Cloud-based |

| Organization Sizes Covered | Large Enterprises, Medium Enterprises, Small Enterprises |

| Industry Verticals Covered | BFSI, Government, Healthcare and Education, Manufacturing, Retail and Consumer Goods, IT and Telecom, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Xerox Holdings Corporation, HP Development Company, L.P., Ricoh, Konica Minolta Inc., Canon Inc., KYOCERA Document Solutions Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the managed print services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global managed print services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the managed print services industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Managed Print Services Market Report

The global managed print services market size was valued at USD 52.9 Billion in 2025, up from USD 38.5 Billion in 2020, reflecting consistent mid-single-digit annual growth.

The market is projected to grow at a CAGR of 6.56% during 2026-2034, reaching USD 95.3 Billion by 2034, driven by cloud adoption and enterprise cost optimization.

Key trends include cloud-native MPS adoption, AI-powered fleet analytics, print security integration, sustainability-linked SLAs, and convergence with ECM document management platforms.

Asia-Pacific dominates with a 33.9% global revenue share in 2025, led by Japan, China, and India. North America holds 27.6% and Europe 22.4%.

Leading companies include Xerox Holdings Corporation, HP Development Company, L.P., Ricoh, Konica Minolta Inc., Canon Inc., and KYOCERA Document Solutions Inc.

Device Management is the largest type segment at 31.6% share in 2025. Cloud-based deployment is the dominant mode at 56.8% of global demand in 2025.

Key drivers include digital transformation mandates, enterprise cost-reduction initiatives, hybrid work cloud-print adoption, and expanding print security and compliance requirements.

Cloud-based MPS delivers print fleet management, monitoring, and optimization through cloud platforms like Microsoft Universal Print, eliminating on-premises print servers entirely.

The global managed print services market is projected to reach approximately USD 72.7 Billion by 2030, from the 2025 base of USD 52.9 Billion.

Key challenges include structurally declining print volumes, high deployment costs, data privacy constraints on cloud adoption, and integration complexity with legacy IT infrastructure.

BFSI and Government are the highest-value verticals due to large device fleets, security compliance mandates, and multi-year enterprise outsourcing contract preferences globally.

The market is forecast to reach USD 95.3 Billion by 2034 from USD 52.9 Billion in 2025, representing a net addition of approximately USD 42.4 Billion over the forecast period.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade