Medical Device Outsourcing Market Report by Service (Regulatory Consulting, Product Design and Development, Product Testing and Sterilization, Product Implementation, Product Upgrade, Product Maintenance), Therapeutics (Cardiology, Diagnostic Imaging, Orthopedic, IVD, Ophthalmic, General and Plastic Surgery, Drug Delivery, Dental, Endoscopy, Diabetes Care), Application (Class I, Class II, Class III), and Region 2026-2034

Market Overview:

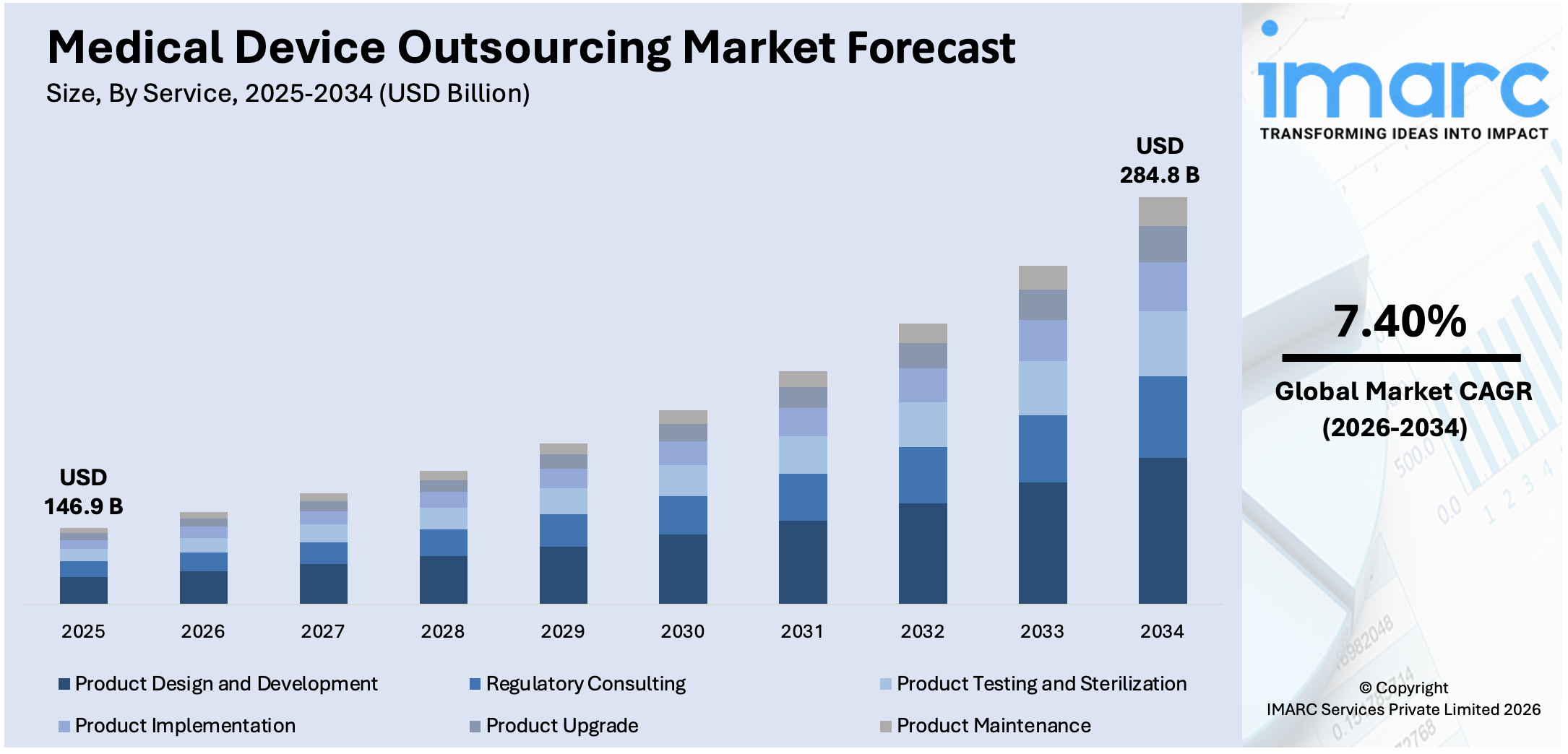

The global medical device outsourcing market size reached USD 146.9 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 284.8 Billion by 2034, exhibiting a growth rate (CAGR) of 7.40% during 2026-2034. The rising need to reduce overall medical costs, the implementation of stringent regulatory requirements and quality standards, the expanding adoption of wearable medical devices, and the surging demand for personalized medicine are among the key factors driving the market growth.

|

Report Attribute

|

Key Statistics |

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 146.9 Billion |

| Market Forecast in 2034 | USD 284.8 Billion |

| Market Growth Rate 2026-2034 | 7.40% |

Medical device outsourcing refers to the practice of contracting or partnering with external companies or service providers to handle various aspects of the medical device product lifecycle. These external partners are typically specialized contract manufacturers, design and development firms, regulatory consultants, logistics providers, or other service providers with expertise in the medical device industry. These services offer several benefits to companies, including cost savings, access to specialized expertise, increased operational efficiency, and the ability to adapt to market demands more effectively. It also allows medical device manufacturers to concentrate on core competencies, such as research and development, marketing, and strategic planning, while leveraging the capabilities of external partners to handle other essential aspects of the product lifecycle.

To get more information on this market Request Sample

The market is experiencing significant growth due to the increasing prevalence of medical ailments and the surging need for quality healthcare services. In addition, outsourcing offers medical device companies the flexibility to scale production volumes based on market demand. This adaptability is essential for managing fluctuations in product demand, especially for devices with seasonal variations or in response to unexpected market shifts. Moreover, the surging demand for personalized medicine, the expanding adoption of wearable medical devices, the growing popularity of minimally invasive surgical procedures, and the rising trend of home healthcare, telemedicine, and medical tourism are some of the other factors propelling the market. Besides, contract manufacturers with international operations can provide access to diverse markets and navigate import/export regulations, facilitating a smoother expansion into new regions and influencing the market growth.

Medical Device Outsourcing Market Trends/Drivers:

The rising need to reduce overall medical costs

Medical device outsourcing offers cost savings to healthcare providers and medical device companies. Contracting with specialized manufacturers or service providers is more cost-efficient than maintaining in-house operations. External partners have established production facilities, economies of scale, and streamlined processes, enabling them to produce medical devices at lower costs. Moreover, outsourcing non-core activities, such as manufacturing and logistics, allows medical device companies to optimize resource allocation. By delegating routine tasks to external partners, companies can focus their internal resources on core competencies like research, development, and innovation, which can lead to more cost-effective and competitive products.

The implementation of stringent regulatory requirements and quality standards

The implementation of stringent regulations places a higher compliance burden on both medical device companies and their outsourcing partners. Contract manufacturers must adhere to the same regulatory standards as the OEMs to ensure that the medical devices they produce meet the required safety and quality benchmarks. This requires rigorous documentation, quality management systems, and adherence to good manufacturing practices (GMP). Moreover, with higher regulatory scrutiny, quality assurance becomes paramount in the medical device outsourcing process. Contract manufacturers are now under pressure to implement robust quality control measures and risk management strategies to identify and mitigate potential issues in the production process.

The expanding adoption of wearable medical devices

Wearable medical devices often incorporate advanced sensors, wireless connectivity, and sophisticated data analytics capabilities. The development and manufacturing of such technology-intensive devices require specialized expertise and resources, leading to an increased demand for outsourcing partners with expertise in advanced electronics and software development. Moreover, medical devices need to be lightweight, comfortable, and ergonomically designed to ensure user compliance and long-term wearability. Contract manufacturers with expertise in miniaturization techniques and materials selection play a crucial role in achieving these design requirements.

Medical Device Outsourcing Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global medical device outsourcing market report, along with forecasts at the global, regional and country levels from 2026-2034. Our report has categorized the market based on service, therapeutics and application.

Breakup by Service:

- Regulatory Consulting

- Product Design and Development

- Product Testing and Sterilization

- Product Implementation

- Product Upgrade

- Product Maintenance

Product design and development represent the leading segment

The report has provided a detailed breakup and analysis of the market based on the service. This includes regulatory consulting, product design and development, product testing and sterilization, product implementation, product upgrade, and product maintenance. According to the report, product design and development represented the largest segment.

Medical device design and development requires a high level of technical expertise, including knowledge of regulatory requirements, engineering principles, and medical standards. Many medical device companies lack in-house capabilities or resources to handle the complex design process efficiently. Outsourcing product design and development allows them to tap into the specialized expertise of experienced design firms and engineering companies with a proven track record in the medical device industry. Moreover, outsourcing product design and development enables medical device companies to access fresh ideas, creative solutions, and cutting-edge technologies from external design partners.

Breakup by Therapeutics:

- Cardiology

- Diagnostic Imaging

- Orthopedic

- IVD

- Ophthalmic

- General and Plastic Surgery

- Drug Delivery

- Dental

- Endoscopy

- Diabetes Care

Cardiology exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on therapeutics have also been provided in the report. This includes cardiology, diagnostic imaging, orthopedic, IVD, ophthalmic, general and plastic surgery, drug delivery, dental, endoscopy, and diabetes care. According to the report, cardiology accounted for the largest market share.

Cardiovascular diseases (CVDs) remain one of the leading causes of death worldwide. The increasing prevalence of conditions such as coronary artery disease, heart failure, and arrhythmias has led to a rising demand for innovative medical devices and technologies to diagnose, treat, and manage these conditions. This high demand has driven medical device companies to focus extensively on cardiology-related products and services, leading to a dominant presence in the outsourcing market. Besides, the field of cardiology has witnessed rapid technological advancements and continuous innovation. These innovations include implantable devices such as pacemakers, defibrillators, stents, and heart valves, as well as diagnostic devices like electrocardiograms (ECGs) and cardiac imaging equipment. To keep up with the pace of innovation and meet market demands, medical device companies often seek specialized outsourcing partners with expertise in cardiology product development.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Class I

- Class II

- Class III

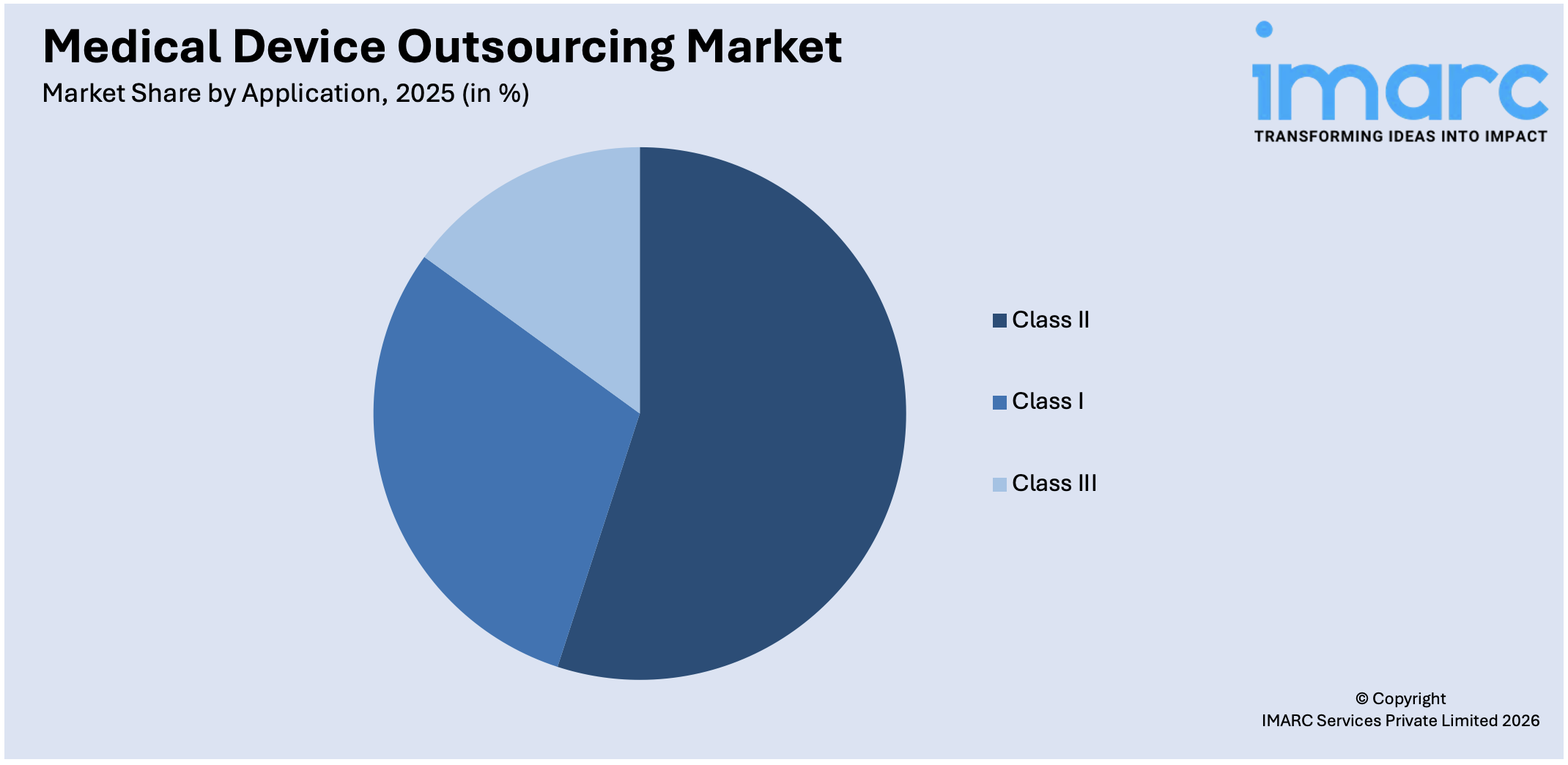

Class II accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the application. This includes class I, II, and III. According to the report, class II represented the largest segment.

Class II medical devices encompass a wide range of products, including moderate to high-risk devices that do not fall into the highest-risk Class III category. This broad product range includes items such as infusion pumps, diagnostic imaging equipment, electrocardiographs, surgical instruments, and certain implantable devices. The diversity of Class II devices contributes to a larger market share in the outsourcing industry. Moreover, these medical devices are subject to intermediate levels of regulatory scrutiny compared to Class III devices. While Class II devices must still meet strict regulatory requirements for safety and efficacy, the regulatory process is generally less burdensome and time-consuming than that for Class III devices, which is escalating their demand.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific exhibits a clear dominance, accounting for the largest medical device outsourcing market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Latin America (Mexico, Brazil, Others); Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others); and Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others). According to the report, Asia Pacific was the largest market for medical device outsourcing.

Asia Pacific countries, such as China, India, and Southeast Asian nations, offer a significant cost advantage in terms of labor and manufacturing. The lower labor costs, combined with well-developed manufacturing infrastructure and supply chain networks, make the region an attractive option for medical device companies seeking cost-effective outsourcing solutions. Moreover, the region boasts a large pool of skilled and trained professionals in engineering, science, and technology fields. This skilled workforce includes engineers, scientists, and technicians with expertise in medical device design, development, and manufacturing. The availability of such talent accelerates the outsourcing process and ensures high-quality products.

Competitive Landscape:

The competitive landscape of the medical device outsourcing market is highly dynamic with numerous companies offering a wide range of outsourcing services to medical device manufacturers. Nowadays, key players are expanding their service portfolios to provide a comprehensive range of outsourcing solutions. They are diversifying their offerings to include contract manufacturing, product design and development, regulatory support, post-market services, packaging, and logistics. Companies are also engaging in mergers, acquisitions, and strategic partnerships to expand their geographical presence and technical capabilities. They are also investing heavily in advanced manufacturing technologies such as automation, robotics, 3D printing, and data analytics to improve production efficiency, reduce costs, and offer faster turnaround times to medical device manufacturers.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Celestica Inc. (Onex Corporation)

- Charles River Laboratories International Inc.

- Flex Ltd.

- Freyr Inc.

- Heraeus Holding GmbH

- ICON plc

- Integer Holdings Corporation

- IQVIA Inc.

- Plexus Corp.

- Sanmina Corporation

- TE Connectivity

- West Pharmaceutical Services Inc.

Recent Developments:

- Flex Ltd. launched "Healthcare Solutions," a comprehensive suite of medical device design, engineering, and manufacturing services. The offering includes rapid prototyping, miniaturization expertise, and end-to-end solutions to support medical device companies throughout the product lifecycle.

- Celestica acquired PCI Limited, a provider of design and manufacturing services for medical and other industries. This acquisition strengthened Celestica's presence in the medical device outsourcing market and expanded its offerings in the Asia Pacific region.

- Celestica Inc. acquired Atrenne Integrated Solutions, a provider of electronic manufacturing and design services for the aerospace, defense, and other industries. This acquisition enhanced Celestica's capabilities in serving the medical device market.

Medical Device Outsourcing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Services Covered | Regulatory Consulting, Product Design and Development, Product Testing and Sterilization, Product Implementation, Product Upgrade, Product Maintenance |

| Therapeutics Covered | Cardiology, Diagnostic Imaging, Orthopedic, IVD, Ophthalmic, General and Plastic Surgery, Drug Delivery, Dental, Endoscopy, Diabetes Care |

| Classes Covered | Class I, Class II, Class III |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Celestica Inc. (Onex Corporation), Charles River Laboratories International Inc., Flex Ltd., Freyr Inc., Heraeus Holding GmbH, ICON plc, Integer Holdings Corporation, IQVIA Inc., Plexus Corp., Sanmina Corporation, TE Connectivity and West Pharmaceutical Services Inc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the medical device outsourcing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global medical device outsourcing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the medical device outsourcing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Medical Device Outsourcing Market Report

The global medical device outsourcing market was valued at USD 146.9 Billion in 2025.

We expect the global medical device outsourcing market to exhibit a CAGR of 7.40% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic has led to the increasing adoption of medical device outsourcing for package testing validation and sterilization validation of the antigen testing kits for the coronavirus infection.

The increasing demand for medical device outsourcing services over traditional approaches, as they offer enhances efficiency, improves product quality, minimized business risks, etc., is primarily driving the global medical device outsourcing market.

Based on the service, the global medical device outsourcing market can be categorized into regulatory consulting, product design and development, product testing and sterilization, product implementation, product upgrade, and product maintenance. Currently, product design and development exhibits clear dominance in the market.

Based on the therapeutics, the global medical device outsourcing market has been segmented into cardiology, diagnostic imaging, orthopedic, IVD, ophthalmic, general and plastic surgery, drug delivery, dental, endoscopy, and diabetes care. Among these, cardiology currently holds the largest market share.

Based on the application, the global medical device outsourcing market can be bifurcated into class I, class II, and class III. Currently, class II accounts for the majority of the total market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global medical device outsourcing market include Celestica Inc. (Onex Corporation), Charles River Laboratories International Inc., Flex Ltd., Freyr Inc., Heraeus Holding GmbH, ICON plc, Integer Holdings Corporation, IQVIA Inc., Plexus Corp., Sanmina Corporation, TE Connectivity, and West Pharmaceutical Services Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)