Medical Simulation Market Size, Share, Trends and Forecast by Product and Services, Fidelity, End User, and Region, 2026-2034

Medical Simulation Market Size, Share, Trends & Forecast (2026-2034)

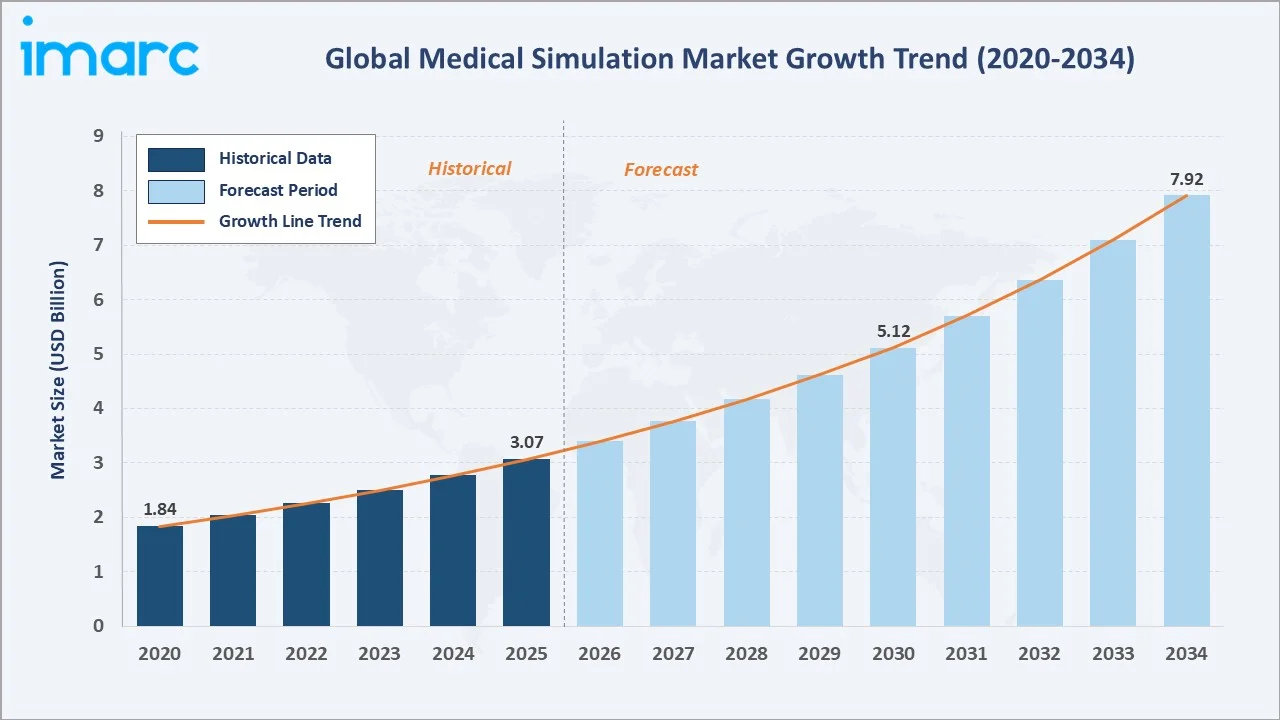

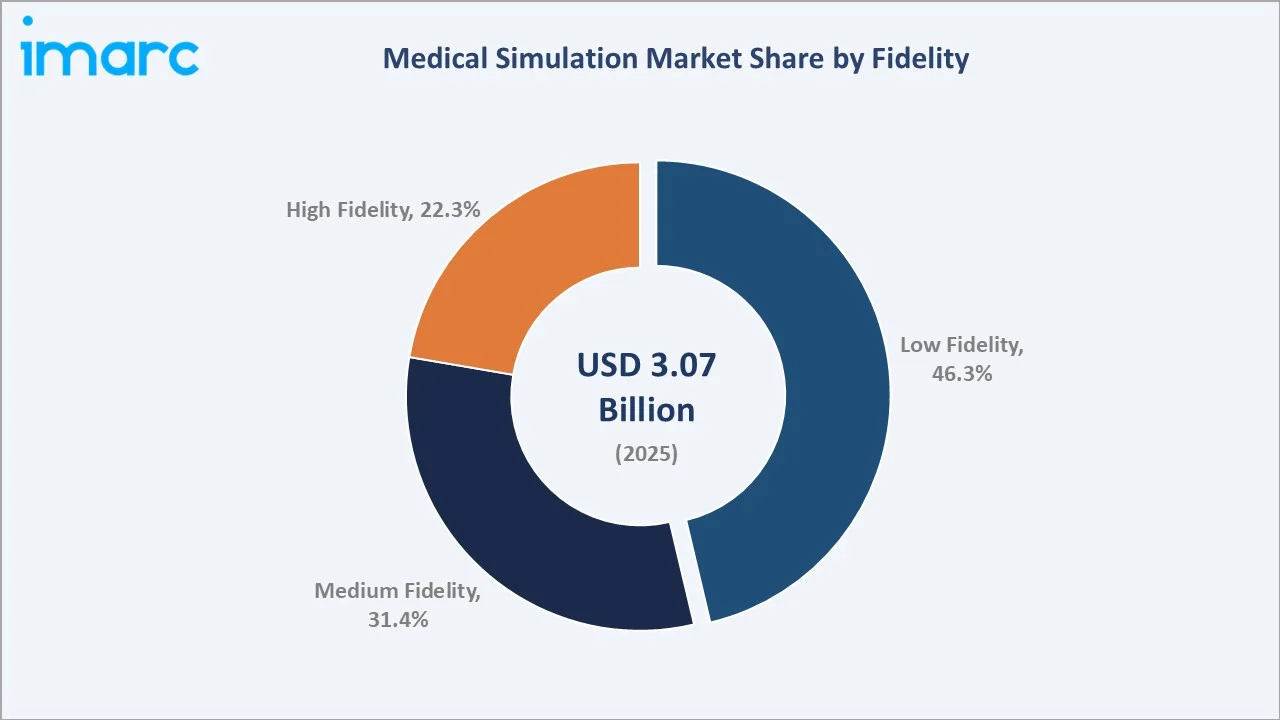

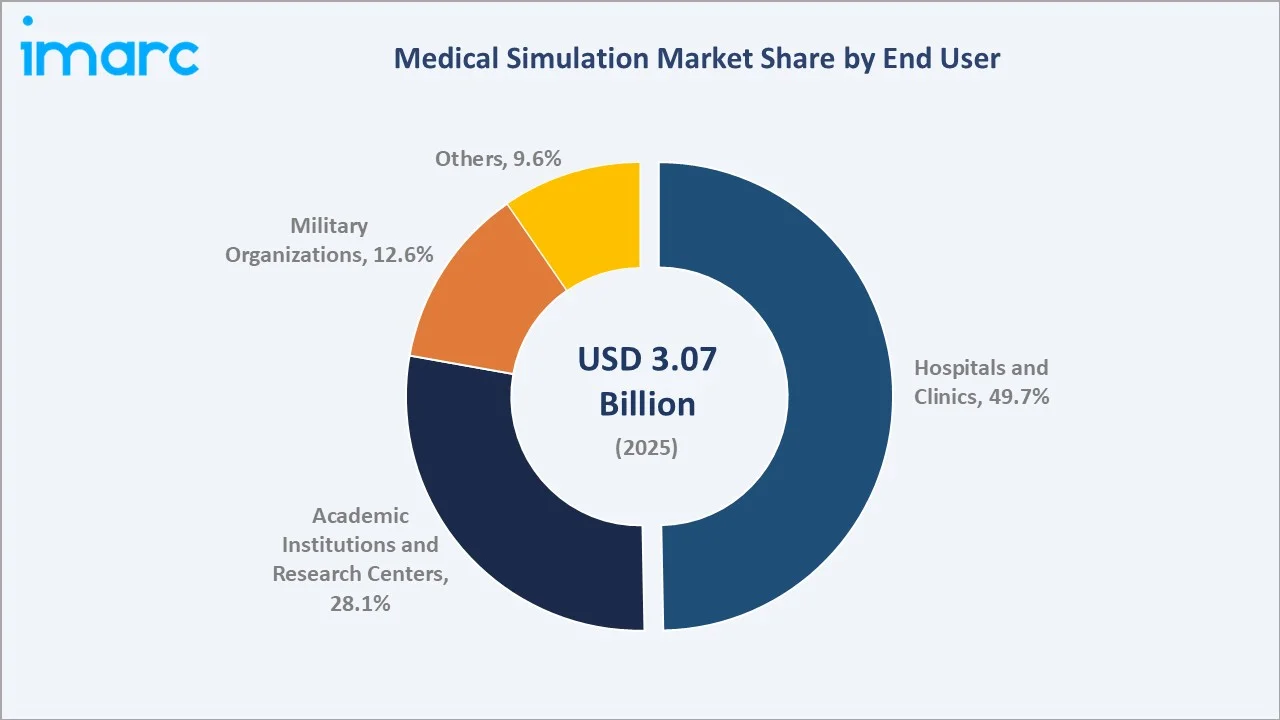

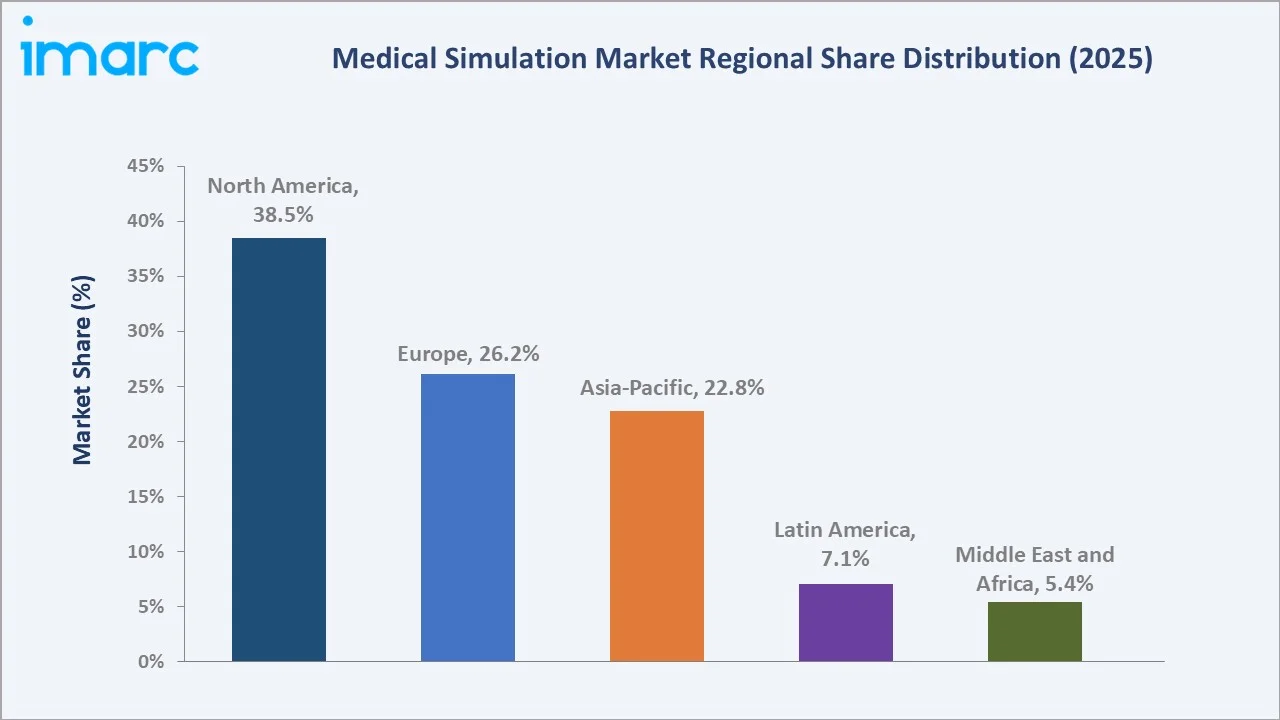

The global medical simulation market reached USD 3.07 Billion in 2025 and is projected to reach USD 7.92 Billion by 2034, growing at a CAGR of 10.77% during 2026-2034. The market is primarily driven by increasing demand for advanced medical training and education, the need to improve patient safety, and the growing adoption of simulation-based learning in healthcare institutions. A study published in the International Journal of Medical and Pharmaceutical Research reported that 80% of students enjoyed learning through simulation, while 78% found it intellectually engaging. Around 85% believed that Simulation-Based Learning (SBL) effectively facilitated learning of fundamental medical sciences, and 70% felt it adequately prepared them for real-world clinical scenarios. Low fidelity simulators dominate at 46.3%. Hospitals and clinics lead end-users at 49.7%. North America commands 38.5% of the global market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 3.07 Billion |

| Forecast Market Size (2034) | USD 7.92 Billion |

| CAGR (2026-2034) | 10.77% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Fidelity | Low Fidelity (46.3%, 2025) |

| Dominant End User | Hospitals and Clinics (49.7%, 2025) |

| Leading Region | North America (38.5%, 2025) |

The market expanded from USD 1.84 Billion in 2020 to USD 3.07 Billion in 2025, anchored at USD 5.12 Billion in 2030, and forecast to reach USD 7.92 Billion by 2034. COVID-19 acted as a defining accelerant for medical simulation. The pandemic's dual effect of disrupting traditional patient-contact medical training while simultaneously elevating awareness of healthcare system capacity and resilience needs created urgent demand for simulation-based alternatives to bedside learning. Virtual patient simulation platforms and remote simulation programmes demonstrated feasibility for remote clinical skills development, creating new institutional awareness of simulation technology, which sustained post-pandemic investment.

To get more information on this market, Request Sample

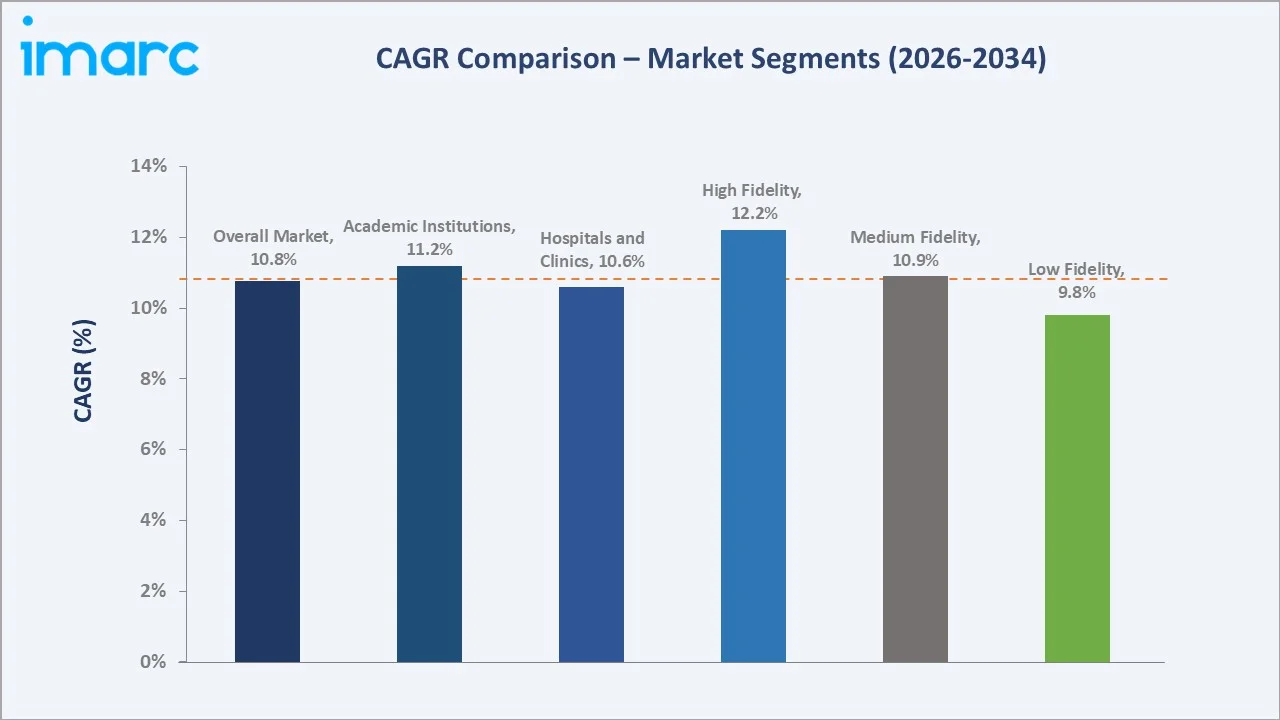

High fidelity simulation grows fastest at ~12.2% CAGR as VR/AR hardware cost reductions make immersive simulation accessible below the historically prohibitive threshold, and AI-driven adaptive learning platforms create competency-based simulation curricula that justify premium investment through measurable learning outcome improvements. Academic institutions grow at ~11.2% CAGR through national medical education simulation accreditation mandates, creating systematic institutional procurement demand.

Executive Summary

The global medical simulation market reached USD 3.07 Billion in 2025, representing the convergence of three global healthcare imperatives: patient safety requiring that clinical competence be demonstrated before patient contact; medical workforce capacity building demanding scalable training solutions for the world's projected shortfall of healthcare workers; and technological innovation enabling increasingly realistic virtual clinical environments that reduce or eliminate the gap between simulated and real-world clinical performance. Medical simulation encompasses the full spectrum of training tools from simple low-fidelity task trainers through medium-fidelity standardized patient models and screen-based simulation to high-fidelity patient simulators and fully immersive VR/AR simulation platforms.

Low fidelity simulators at 46.3% dominate through the breadth and accessibility of task trainers. Hospitals and clinics at 49.7% lead end-user demand through hospital-based simulation centres providing ongoing clinical skill maintenance, new procedure credentialing, and emergency response team training for employed clinical staff, creating recurring institutional procurement independent of academic calendar cycles. North America, at 38.5%, leads through the simulation mandate, the VA national programme, and the world's most commercially developed medical simulation procurement and innovation ecosystem.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Fidelity | Low Fidelity – 46.3% share (2025) |

| Dominant End User | Hospitals and Clinics – 49.7% market share (2025) |

| Leading Region | North America – 38.5% market share (2025) |

Key Analytical Observations Supporting The Above Data:

- Low fidelity at 46.3%: The low-fidelity simulators are cost-effective, easy to use, and widely accessible for teaching fundamental medical skills. Their simplicity allows institutions to train large numbers of students efficiently while providing essential hands-on practice without the complexity or expense of high-fidelity systems.

- Hospitals and clinics at 49.7%: The hospitals and clinics segment dominates the market because these institutions are the primary adopters of simulation-based training for healthcare professionals. Their focus on improving clinical skills, patient safety, and staff preparedness drives consistent demand for simulation equipment and programs.

- North America at 38.5%: North America dominates the market due to advanced healthcare infrastructure, high adoption of innovative training technologies, and strong investments in healthcare education. The presence of key simulation technology providers and regulatory support for clinical training further reinforces the region’s leading market position.

Medical Simulation Market Overview

The global medical simulation market encompasses the design, manufacture, distribution, and implementation of training tools and systems that replicate clinical scenarios, patient physiological states, and procedural anatomy to enable healthcare providers to develop, practise, and assess clinical skills without risk to actual patients. Market products range from simple low-fidelity procedural task trainers to medium-fidelity partial patient simulators and screen-based virtual patients, high-fidelity full-body electronic patient simulators, VR/AR immersive surgical simulation platforms, 3D-printed patient-specific anatomical models for surgical rehearsal, and AI-powered adaptive learning simulation systems.

The ecosystem integrates simulation product manufacturers, software and VR platform developers, distributors and system integrators, medical simulation training centres, medical education accreditation bodies whose standards drive institutional simulation investment, and research funders. Macroeconomic factors include rising healthcare expenditure, increasing government investment in medical education, and growing demand for skilled healthcare professionals.

Market Dynamics

To evaluate market opportunities, Request Sample

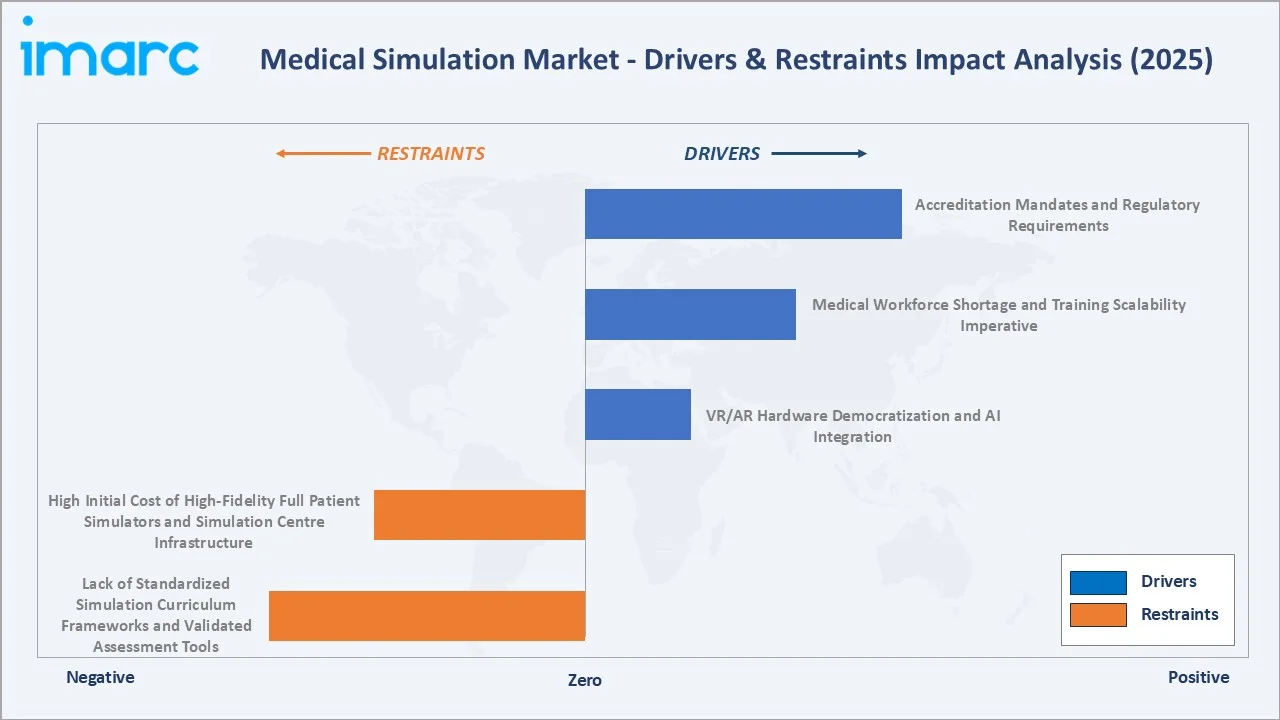

Market Drivers

- VR/AR Hardware Democratisation and AI Integration: The democratization of VR/AR hardware and integration of AI are making advanced training technologies more accessible and affordable. VR and AR platforms provide immersive, interactive learning experiences, while AI enhances realism through adaptive simulations, real-time feedback, and performance analytics. Together, these technologies improve learning outcomes, reduce training costs, and encourage broader adoption of simulation-based education across medical institutions worldwide.

- Medical Workforce Shortage and Training Scalability Imperative: The shortage of healthcare professionals, coupled with the need to train large numbers of practitioners efficiently, is driving the medical simulation market. Simulation-based learning allows scalable, repeatable, and risk-free training, enabling institutions to upskill students and staff rapidly. This approach addresses workforce gaps, improves clinical competency, and enhances patient safety, making simulation technologies increasingly essential in medical education worldwide. Health systems in Africa are expected to face a shortfall of 600,000 healthcare workers by 2030 due to limited absorptive capacity. This growing workforce gap underscores the need for scalable training solutions, making simulation-based learning essential.

- Accreditation Mandates and Regulatory Requirements: Accreditation mandates and regulatory requirements require healthcare institutions to provide standardized, competency-based training for medical students and professionals. Compliance with bodies such as the WHO and national licensing boards compels hospitals, universities, and clinics to adopt simulation-based learning to ensure clinical competency, patient safety, and adherence to quality standards, thereby boosting demand for simulation technologies.

Market Restraints

- High Initial Cost of High-Fidelity Full Patient Simulators and Simulation Centre Infrastructure: The high initial cost of high-fidelity full patient simulators and the infrastructure required for simulation centers limits accessibility, especially for smaller hospitals and educational institutions. The significant investment in equipment, software, and facility setup can delay adoption, reduce return on investment, and create budgetary constraints, slowing overall market growth despite the recognized educational benefits of advanced simulation technologies.

- Lack of Standardized Simulation Curriculum Frameworks and Validated Assessment Tools: The absence of standardized simulation curriculum frameworks and validated assessment tools creates inconsistency in training quality and learning outcomes across institutions. Without universally accepted guidelines and reliable evaluation methods, healthcare educators face challenges in measuring competency, ensuring accreditation compliance, and justifying investment in simulation technologies, which limits widespread adoption and market growth.

Market Opportunities

- AI-Driven Adaptive Simulation Platforms Creating Next-Generation Personalised Medical Education: AI-driven adaptive simulation platforms enabling personalized, next-generation medical education. These platforms adjust training scenarios in real time based on individual learner performance, offering targeted feedback and adaptive difficulty levels. This personalization enhances skill acquisition, accelerates competency development, and supports more efficient, effective training programs, driving adoption of advanced simulation technologies across medical institutions.

- Surgical Robot Training Simulation Creating Premium High-Fidelity Simulation Category with Device Manufacturer Investment: Surgical robot training simulation creating a premium high-fidelity category. Device manufacturers are investing in these specialized simulators to train surgeons on robotic platforms, ensuring safe and efficient skill development. This drives demand for advanced, realistic simulation technologies, enhances surgeon competency with expensive robotic systems, and opens new revenue streams for both simulation providers and medical device companies.

Market Challenges

- Technology Obsolescence Cycle Creating Continuous Capital Investment Requirement for Simulation Centres: The rapid technology obsolescence cycle in medical simulation creates a continuous capital investment requirement for simulation centers, posing a market challenge. Institutions must regularly upgrade simulators, software, and supporting infrastructure to maintain training relevance and comply with evolving clinical standards. These frequent upgrades increase operational costs, strain budgets, and can slow adoption in smaller hospitals and educational institutions, limiting overall market growth.

- Regulatory Classification Uncertainty for VR and AI-Enabled Simulation Devices Affecting Market Entry Timelines: Regulatory classification uncertainty for VR and AI-enabled simulation devices is creating delays in market entry and adoption. Ambiguity around whether these technologies are considered medical devices or educational tools affects approval timelines, compliance requirements, and reimbursement eligibility. This uncertainty increases development risk, slows commercialization, and can deter investment in advanced simulation platforms despite their growing clinical and educational potential.

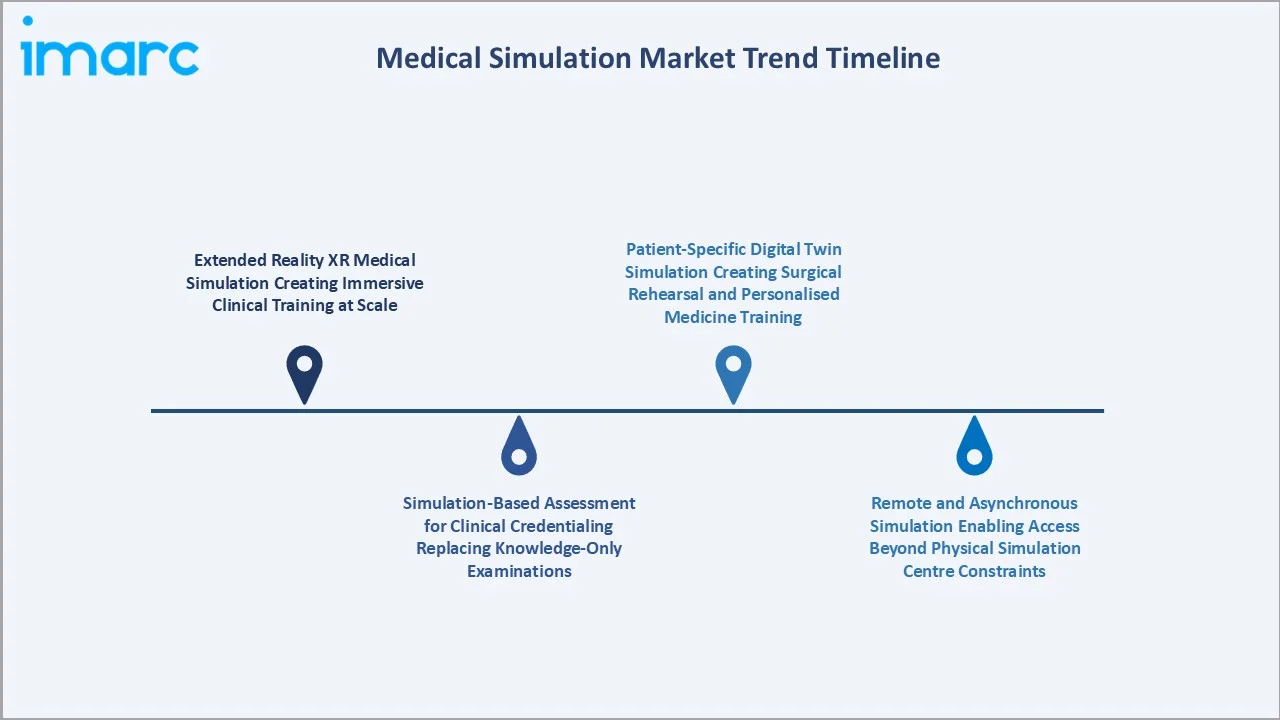

Emerging Market Trends

1. Extended Reality XR Medical Simulation Creating Immersive Clinical Training at Scale

Extended Reality (XR) medical simulation enabling immersive, interactive clinical training at scale. XR technologies, encompassing virtual reality (VR), augmented reality (AR), and mixed reality (MR), allow learners to practice procedures in realistic, risk-free environments. This enhances skill retention, standardizes training across institutions, and supports scalable education for large numbers of medical professionals, driving adoption of advanced simulation solutions in healthcare. In October 2025, Healthtech BR launched its flagship product, GaveaXR Medical Center. GaveaXR is an Extended Reality (XR) platform that provides safe, repeatable, and scalable clinical training, addressing the global need for diverse, high-quality, cost-effective, and efficient medical education.

2. Simulation-Based Assessment for Clinical Credentialing Replacing Knowledge-Only Examinations

Simulation-based assessment for clinical credentialing shifts evaluation from traditional knowledge-only exams to practical, skills-based testing. These assessments allow clinicians to demonstrate real-world competency in a controlled, risk-free environment. By providing objective performance data, simulation-based credentialing enhances patient safety, standardizes evaluation, and encourages broader adoption of advanced simulation technologies in medical education and professional certification programs.

3. Remote and Asynchronous Simulation Enabling Simulation Access Beyond Physical Simulation Centre Constraints

Remote and asynchronous simulation extends access to training beyond the constraints of physical simulation centers. Learners can engage in clinical scenarios at their own pace and location, enabling flexible, scalable, and cost-effective education. This approach supports broader participation, continuous skill development, and operational efficiency, driving wider adoption of simulation technologies across healthcare institutions globally.

4. Patient-Specific Digital Twin Simulation Creating Surgical Rehearsal and Personalised Medicine Training

Patient-specific digital twin simulation enabling surgical rehearsal and personalized medicine training. These simulations create virtual replicas of individual patients’ anatomy and physiology, allowing clinicians to practice complex procedures and tailor treatments to unique patient characteristics. This approach improves surgical precision, reduces operative risk, enhances personalized care, and drives adoption of advanced, patient-centered simulation technologies in healthcare education and practice.

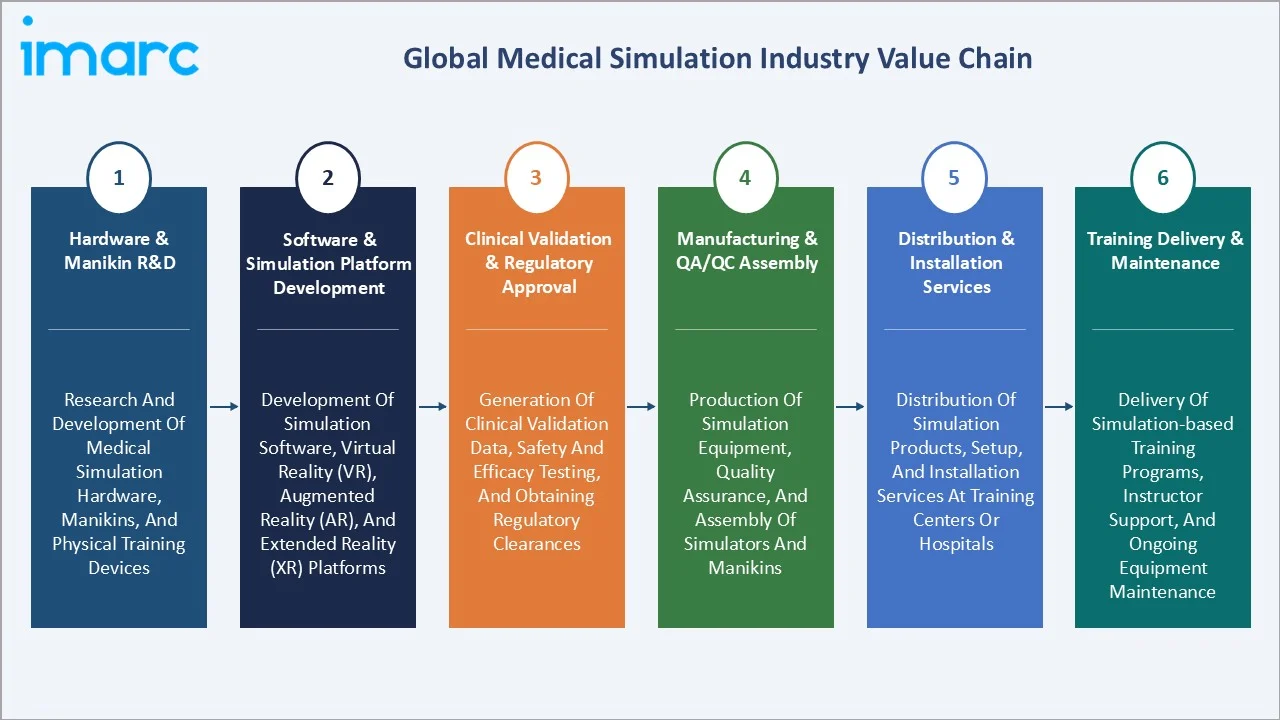

Industry Value Chain Analysis

The medical simulation value chain integrates hardware and manikin R&D, software and simulation platform development, clinical validation and regulatory approval, manufacturing and QA/QC, distribution and installation services, and training delivery and maintenance. The value chain's commercial structure is characterised by the complexity of integrating physical hardware with software simulation platforms and clinical validity evidence that together create defensible commercial products with meaningful barriers to replication.

| Stage | Key Participants |

|---|---|

| Hardware & Manikin R&D | Research and development of medical simulation hardware, manikins, and physical training devices |

| Software & Simulation Platform Development | Development of simulation software, virtual reality (VR), augmented reality (AR), and extended reality (XR) platforms |

| Clinical Validation & Regulatory Approval | Generation of clinical validation data, safety and efficacy testing, and obtaining regulatory clearances |

| Manufacturing & QA/QC Assembly | Production of simulation equipment, quality assurance, and assembly of simulators and manikins |

| Distribution & Installation Services | Distribution of simulation products, setup, and installation services at training centers or hospitals |

| Training Delivery & Maintenance | Delivery of simulation-based training programs, instructor support, and ongoing equipment maintenance |

The training delivery and maintenance tier represents the value chain's most strategically important recurring revenue component, with simulation maintenance contracts, software update subscriptions, consumable replacement, and faculty development programmes creating multi-year revenue streams beyond initial equipment sale.

Technology Landscape in the Medical Simulation Industry

Physical Manikin and Task Trainer Technology

Physical manikin and task trainer technology provide hands-on, tactile training tools that replicate human anatomy and clinical procedures. These technologies allow learners to practice skills such as intubation, catheterization, and CPR in realistic, risk-free environments. In September 2024, PRESTAN introduced the PRESTAN Female Manikin. The new female manikin marks a major advancement in CPR education, addressing the significant difference in cardiac arrest survival rates between men and women. By enhancing muscle memory, procedural accuracy, and learner confidence, manikins and task trainers form the foundation of simulation-based education, complementing digital and VR-based platforms in the industry’s technology landscape.

Virtual Reality and Extended Reality Simulation

Virtual Reality (VR) and Extended Reality (XR) simulations are providing fully immersive and interactive training environments. These platforms enable realistic clinical scenario replication, allowing learners to practice procedures safely and repeatedly without patient risk. VR/XR enhances engagement, supports remote and scalable training, and integrates with AI for adaptive learning, positioning these technologies as critical drivers of innovation in medical education.

AI and Machine Learning in Simulation Assessment

AI and machine learning are enabling intelligent assessment of learner performance. These technologies analyze actions, decision-making, and procedural accuracy in real time, providing personalized feedback and adaptive learning paths. By improving evaluation objectivity, identifying skill gaps, and enhancing training efficiency, AI-driven assessment tools are driving innovation and increasing the effectiveness of simulation-based medical education.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product and Services |

🔒 |

🔒 |

2025 |

|

Fidelity |

Low Fidelity |

46.3% |

2025 |

|

End User |

Hospitals and Clinics |

49.7% |

2025 |

|

Region |

North America |

38.5% |

2025 |

By Fidelity

Low fidelity simulators lead at 46.3% market share (2025). Low fidelity encompasses all task trainers, CPR training manikins, basic anatomical models, standardized patient programmes, and screen-based virtual patient case libraries.

To access detailed market analysis, Request Sample

Medium fidelity at 31.4% encompasses partial task simulators with anatomical realism, screen-based simulation platforms, and standardized patient training programmes. High fidelity at 22.3% grows fastest at ~12.2% CAGR through full patient simulators, procedural VR/AR simulation, and AI-adaptive simulation platforms that collectively represent the market's premium and highest-growth technology tier.

By End User

Hospitals and clinics lead at 49.7% market share (2025). Hospital simulation centres provide ongoing clinical credentialing, procedure-specific new technology training, emergency response team training, and new employee clinical orientation programmes, creating year-round simulation utilisation above academic calendar-constrained medical school programmes.

Academic institutions at 28.1% grow fastest at ~11.2% CAGR through medical school, nursing school, and paramedic programme simulation curriculum integration driven by accreditation requirements. Military organisations at 12.6% sustain investment through combat casualty care and surgical skill maintenance simulation programmes. Others at 9.6% includes pharmaceutical company procedural training simulation, medical device company sales force simulation training, and ambulatory surgical centre simulation programmes.

Regional Market Insights

| Region | Share (2025) | Key Medical Simulation Market Drivers & Characteristics |

|---|---|---|

| North America | 38.5% | Driven by advanced healthcare infrastructure, widespread adoption of simulation-based training, and strong R&D investment |

| Europe | 26.2% | Driven by established medical education programs, regulatory support, and high adoption of simulation technologies |

| Asia-Pacific | 22.8% | Supported by increasing healthcare investments, rising demand for skilled medical professionals, and expansion of training facilities |

| Latin America | 7.1% | Fueled by improving medical education infrastructure, increasing simulation adoption, and growing awareness of patient safety and training efficacy |

| Middle East and Africa | 5.4% | Driven by healthcare modernization initiatives, rising medical education programs, and increasing demand for clinical training solutions |

North America, at 38.5%, leads through simulation mandate, the VA national programme, and the world's highest density of education institutes. Europe, at 26.2%, reflects simulation mandate, Northern European simulation manufacturer concentration, and EU simulation research funding.

Asia Pacific, at 22.8%, is the fastest-growing region through the China clinical skills centre mandate, India clinical laboratory requirement, and Japan-Australia premium simulation markets. Latin America, at 7.1%, reflects Brazil's large medical education sector and growing accreditation standard enforcement. MEA, at 5.4%, encompasses GCC premium simulation investment and Africa institutional training development.

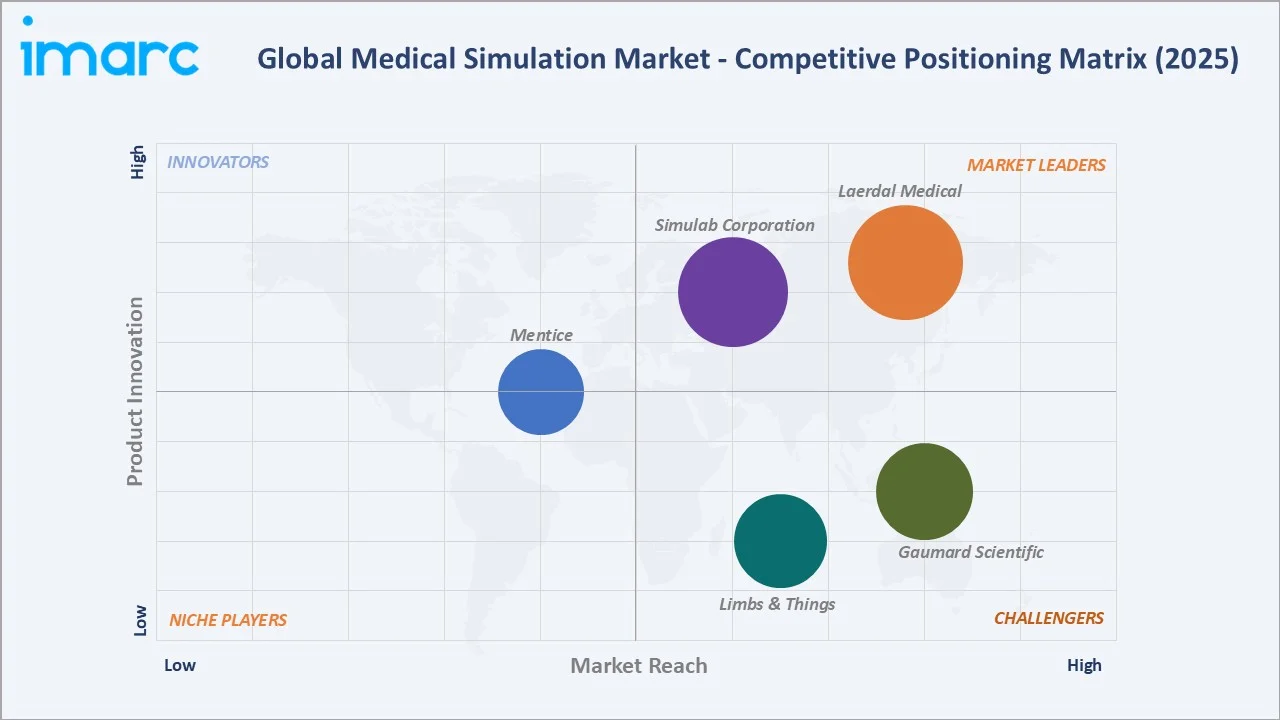

Competitive Landscape

The global medical simulation competitive landscape is characterised by moderate concentration at the premium segment level and high fragmentation in the task trainer and low-fidelity segment. The concentration reflects the substantial R&D investment, clinical validation evidence generation, and global sales and service infrastructure required to compete in the premium high-fidelity and procedural VR simulation segments versus the lower barriers of task trainer manufacturing.

| Company Name | Key Products | Market Position | Core Strength |

|---|---|---|---|

| Laerdal Medical | Little Anne, Little Anne QCPR, Little Baby QCPR, Mini Anne, Mini Anne Plus, SimMan Critical Care, SimMan 3G PLUS, SimMan Essential, SimMan Trauma | Market Leader | Laerdal Medical is a global leader in medical simulation, focusing on improving patient safety and healthcare outcomes through high-fidelity manikins, virtual, and scenario-based training |

| Simulab Corporation | TraumaMan Surgical Simulator, CentraLineMan Pro System, PacerMan System | Market Leader | Simulab Corporation is a leading provider of medical simulation technology, specializing in developing highly realistic, affordable soft-tissue procedural task trainers and anatomical models |

| Gaumard Scientific | HAL S1060, SUSIE S2400, HAL S5301 | Strong Challenger | Gaumard Scientific is a pioneer in healthcare simulation, designing and manufacturing high-fidelity patient simulators, task trainers, and specialized training solutions for healthcare education |

| Limbs & Things | Birthing Simulator PROMPT Flex - Standard (Light Skin Tone), Infant Hip Examination Trainer, Clean Bleed Mat – Blood and Fluid Loss Simulator, Nickie Medical Training Dolls | Strong Challenger | Limbs & Things is a leading global manufacturer of anatomically accurate medical task trainers and simulators |

| Mentice | VIST G7 and G7+, VIST TEE Trainer, VIST G7 Go | Established Player | Mentice is a global leader in simulation solutions for image-guided interventional therapies, providing high-fidelity virtual reality (VR) hardware and software to train clinicians, improve patient outcomes, and validate medical devices |

The competitive boundary between medical device companies and medical simulation companies is blurring. This cross-sector competitive entry creates both partnership opportunities and competitive threats.

Key Company Profiles

Laerdal Medical

Laerdal Medical is a globally recognized leader in medical simulation and healthcare training solutions, dedicated to improving patient outcomes through realistic practice and skills development. The company’s portfolio includes a wide range of simulation products, from basic manikins and task trainers to advanced high‑fidelity patient simulators, designed for use in nursing, emergency care, and clinical education.

- Key Products: Little Anne, Little Anne QCPR, Little Baby QCPR, Mini Anne, Mini Anne Plus, SimMan Critical Care, SimMan 3G PLUS, SimMan Essential, SimMan Trauma.

- Recent Developments: In January 2024, Laerdal Medical introduced the MamaAnne Maternal Simulator, designed to replicate the entire maternal labor and delivery process, from initial assessment through postnatal care. The simulator allows multi-professional birthing teams to practice obstetric emergencies, addressing major causes of maternal mortality such as postpartum hemorrhage, hypertensive disorders, sepsis, and obstructed labor, while emphasizing respectful care, normal birth practices, and effective communication in the delivery room.

- Strategic Focus: Developing realistic, evidence-based training solutions that enhance clinical skills, improve patient safety, and support competency-based healthcare education globally.

Simulab Corporation

Simulab Corporation is a medical simulation company specializing in high‑fidelity surgical and procedural training models. The company focuses on creating realistic, hands‑on simulators that help healthcare professionals refine critical skills in trauma, surgical airway management, central line placement, and other invasive procedures.

- Key Products: TraumaMan Surgical Simulator, CentraLineMan Pro System, PacerMan System.

- Recent Developments: In February 2026, Simulab Corporation launched the TraumaMan System Ultrasound Module, which expands ultrasound-enabled training capabilities within its flagship trauma training platform.

- Strategic Focus: Providing high-fidelity, hands-on procedural training models that enhance clinical skills and improve real-world patient outcomes.

Market Concentration Analysis

The medical simulation market is moderately concentrated at the premium segment level, with Laerdal Medical, Simulab Corporation, Gaumard Scientific, and Limbs & Things together accounting for approximately 40-50% of total market revenue, with the remainder distributed among smaller specialist simulation companies targeting specific procedure types, clinical specialties, or geographic markets. Market concentration is higher in the high-fidelity patient simulator category and lower in the task trainer and low-fidelity segment.

The market concentration is declining through the forecast period as VR-native simulation entrants create new high-fidelity simulation revenue outside the established manikin-based simulation company revenue base. Medical device manufacturer entry into simulation through acquisition and organic development is creating a parallel simulation market funded by device company balance sheets rather than standalone simulation company revenues, reducing the traditional simulation company market share denominator as device company simulation revenues grow within the total market.

Investment & Growth Opportunities

Highest Growth Segments

High fidelity simulation (~12.2% CAGR), academic institutions (~11.2% CAGR), Asia Pacific regional market (~12-13% CAGR), VR/AR simulation platform (~25-30% CAGR from growing base), AI-adaptive simulation (~30-40% CAGR from near-zero commercial base), robotic surgery simulation (~20-25% CAGR linked to robotic system installed base growth), and patient-specific digital twin simulation (~20-30% CAGR per-procedure model recurring revenue) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

The simulation-based credentialing market represents the highest-value emerging commercial opportunity. Simulation products used for formal competency assessment in licensing and board certification programmes command premium pricing, recurring per-assessment revenue models, and defensible commercial positions through regulatory clearance that commodity simulation products cannot match.

Investment Themes

- VR simulation platform development for procedural medicine specialties creating device-independent high-fidelity simulation at democratised price points: VR simulation platforms targeting procedural medicine specialties without adequate simulation coverage represent USD 50-500 Million total addressable markets per specialty where high-fidelity physical simulators cost USD 50,000-200,000 per unit.

- Medical simulation subscription and outcome-based business model transformation creating recurring revenue from one-time hardware sales: The transition from transactional simulation hardware sales toward subscription-based simulation services creates a more predictable revenue model aligned with institutional budget planning cycles.

Future Market Outlook (2026-2034)

The global medical simulation market is projected to grow from USD 3.07 Billion in 2025 to USD 7.92 Billion by 2034, delivering a 10.77% CAGR over the forecast period. The market's anchor value of USD 5.12 Billion in 2030 represents a medical simulation industry at a critical commercial inflection point. VR simulation has achieved mainstream clinical validity, AI-adaptive simulation is entering commercial deployment at scale, simulation-based clinical credentialing is progressively replacing knowledge-only examinations, and Asia Pacific medical education expansion is creating the fastest institutional growth in simulation centre establishment of any region in history. These concurrent transitions create a market dynamic where both technology upgrade-driven replacement demand and new institutional establishment demand are simultaneously accelerating through 2030.

Three structural forces define medical simulation market growth through 2034 with confidence. The patient safety imperative is irreversible. Every accreditation standard update incorporating new simulation requirements, every new training requirement, and every new nursing training standard incorporating simulation creates mandatory procurement demand that compounds the baseline simulation market growth. The technology cost curve is consistently declining, VR headset prices falling, AI inference costs declining 75%+ per token annually with GPU scaling, and 3D printing costs reducing 20-30% annually create the economic conditions where simulation fidelity accessible to mid-range budget institutions, continuously improves, expanding the market's addressable institutional customer base as previously cost-prohibitive high-fidelity simulation becomes accessible to community hospitals, rural training programmes, and medical schools.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Chief Technology Officers; Clinical Simulation Directors; simulation standards committee members and clinical skills training standard reviewers; Military medical simulation programme directors; Medical simulation faculty; and Asia Pacific simulation programme leads.

Secondary Research

Secondary research encompassed Society for Simulation in Healthcare Survey of Simulation Programs 2024; Accreditation Data System simulation programme requirement analysis; simulation development fund programme reports; WHO Global Health Workforce Alliance healthcare workforce projections 2030; individual company annual reports and investor presentations; International Meeting on Simulation in Healthcare 2025 proceedings abstracts; Simulation in Healthcare journal systematic review publications; Medical Education journal simulation education research meta-analyses. Over 60 secondary sources reviewed.

Forecasting Models

- Market revenue forecasts were developed using an institutional bottom-up model: (i) simulation centre count by region and institutional type multiplied by average annual simulation procurement budget per institution type; (ii) end-user segment product mix modelling; (iii) technology adoption curve modelling for VR and AI simulation market share growth versus traditional manikin simulation.

Medical Simulation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product and Services Covered | Model-based Simulation, Surgical Simulation, Ultrasound Simulation, Web-based Simulation, Simulation Training Services |

| Fidelities Covered | Low Fidelity, Medium Fidelity, High Fidelity |

| End Users Covered | Hospitals and Clinics, Academic Institutions and Research Centers, Military Organizations, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Laerdal Medical, Simulab Corporation, Gaumard Scientific, Limbs & Things, Mentice, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the medical simulation market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global medical simulation market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the medical simulation industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Medical Simulation Market Report

The global medical simulation market reached USD 3.07 Billion in 2025, driven by low fidelity task trainer broad institutional adoption, growing hospital and clinic simulation centre investment for clinical credentialing, international accreditation body simulation mandates creating non-discretionary institutional procurement, VR and AI simulation technology integration creating new high-fidelity simulation market segments, and Asia Pacific medical education expansion creating new institutional simulation centre establishment demand at an unprecedented scale.

The market grows at 10.77% CAGR during 2026-2034, reaching USD 7.92 Billion by 2034. Growth reflects high fidelity VR/AR simulation democratisation, academic institution accreditation-mandated simulation investment, Asia Pacific medical education simulation centre establishment, AI-adaptive simulation commercial deployment, robotic surgery simulation growth linked to robotic system installed base, and patient-specific digital twin simulation per-procedure revenue model expansion.

Low fidelity leads at 46.3% through the universal accessibility of task trainers at low price points, enabling adoption at every healthcare training institution globally.

Hospitals and clinics lead at 49.7% through hospital simulation centre investment for clinical staff credentialing, new procedure training, and emergency team response simulation.

North America leads at 38.5% through the world's most developed medical simulation infrastructure, the VA national simulation programme, higher education institutes, and the highest concentration of medical simulation manufacturers and innovation.

Leading companies include Laerdal Medical, Simulab Corporation, Gaumard Scientific, Limbs & Things, and Mentice, among others.

The market is projected to reach approximately USD 5.12 Billion by 2030, with VR simulation achieving mainstream adoption, AI-adaptive simulation entering commercial scale deployment at academic medical centres, Asia Pacific new simulation centre establishments at peak mandate implementation, robotic surgery simulation growth, and simulation-based clinical credentialing achieving formal accreditation board recognition in additional specialties.

Low fidelity simulation encompasses basic task trainers providing isolated procedural skill practice without integrated physiological response, venipuncture arms, IV cannulation trainers, suture pads, airway management heads, and catheterization models. Medium fidelity includes partial body simulators with some physiological realism (birthing simulators, CPR manikins with AED integration, screen-based virtual patient cases) and standardized patient programmes. High fidelity encompasses full-body electronic patient simulators with comprehensive cardiorespiratory, pharmacological, and neurological physiological modelling, procedural VR/AR simulation, and AI-adaptive simulation platforms providing immersive, realistic simulation experiences approximating real clinical encounters.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)