Menswear Market Size, Share, Trends and Forecast by Product Type, Season, Distribution Channel, and Region, 2026-2034

Menswear Market Size, Share, Trends & Forecast (2026-2034)

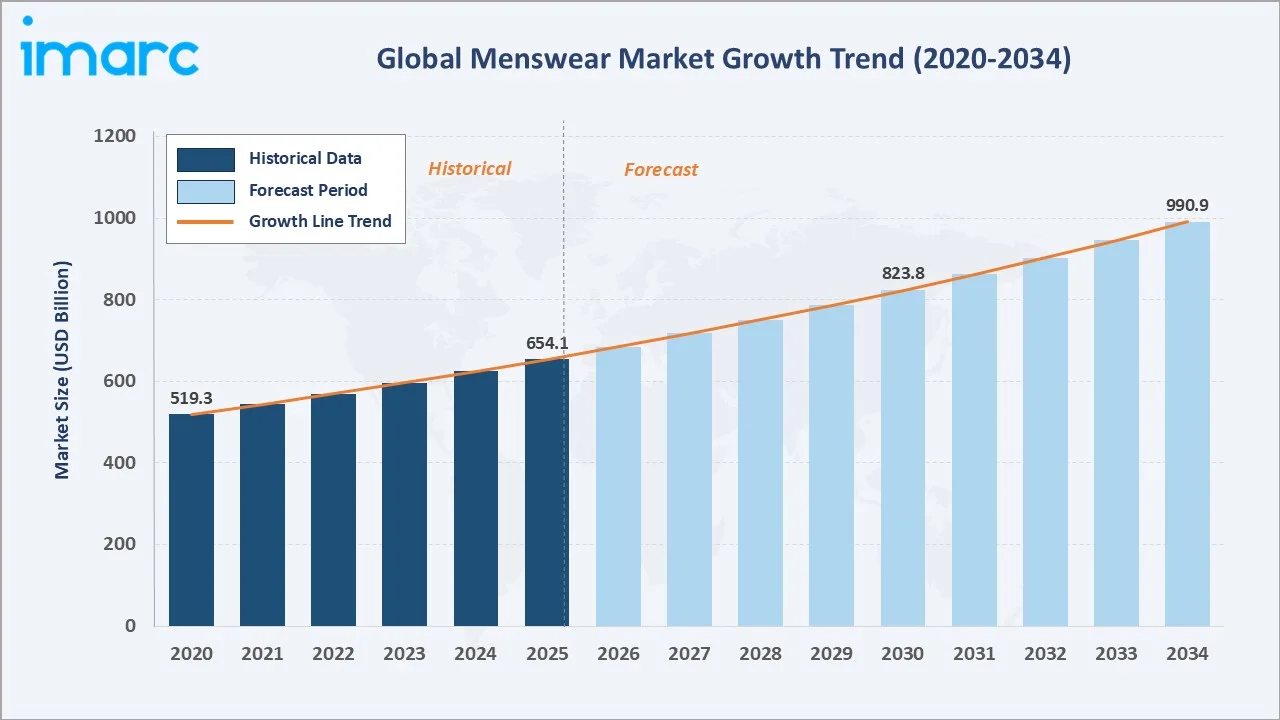

The global menswear market reached USD 654.1 Billion in 2025 and is projected to reach USD 990.9 Billion by 2034, growing at a CAGR of 4.72% during 2026-2034. Rising global male fashion consciousness, the proliferation of athleisure and lifestyle apparel, expanding e-commerce and DTC brand channels, and the premiumization of menswear across North America and the Asia Pacific are the primary catalysts driving sustained market expansion throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 654.1 Billion |

|

Forecast Market Size (2034) |

USD 990.9 Billion |

|

CAGR (2026-2034) |

4.72% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

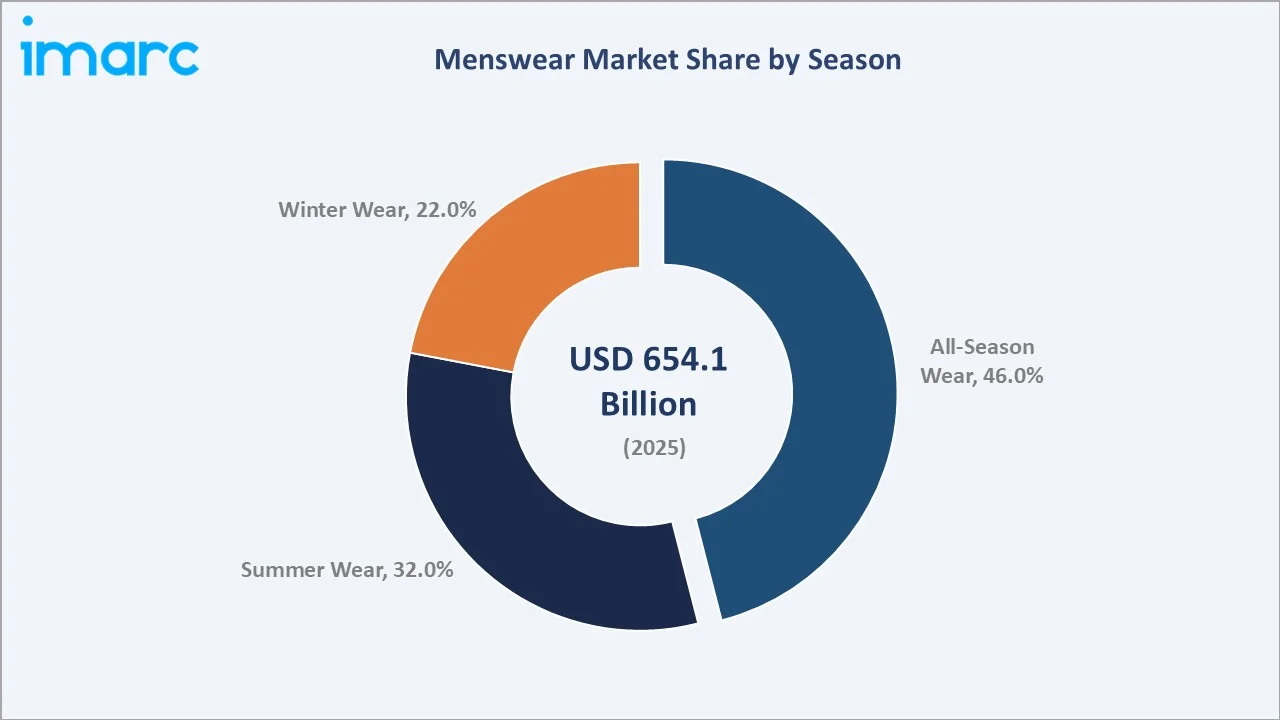

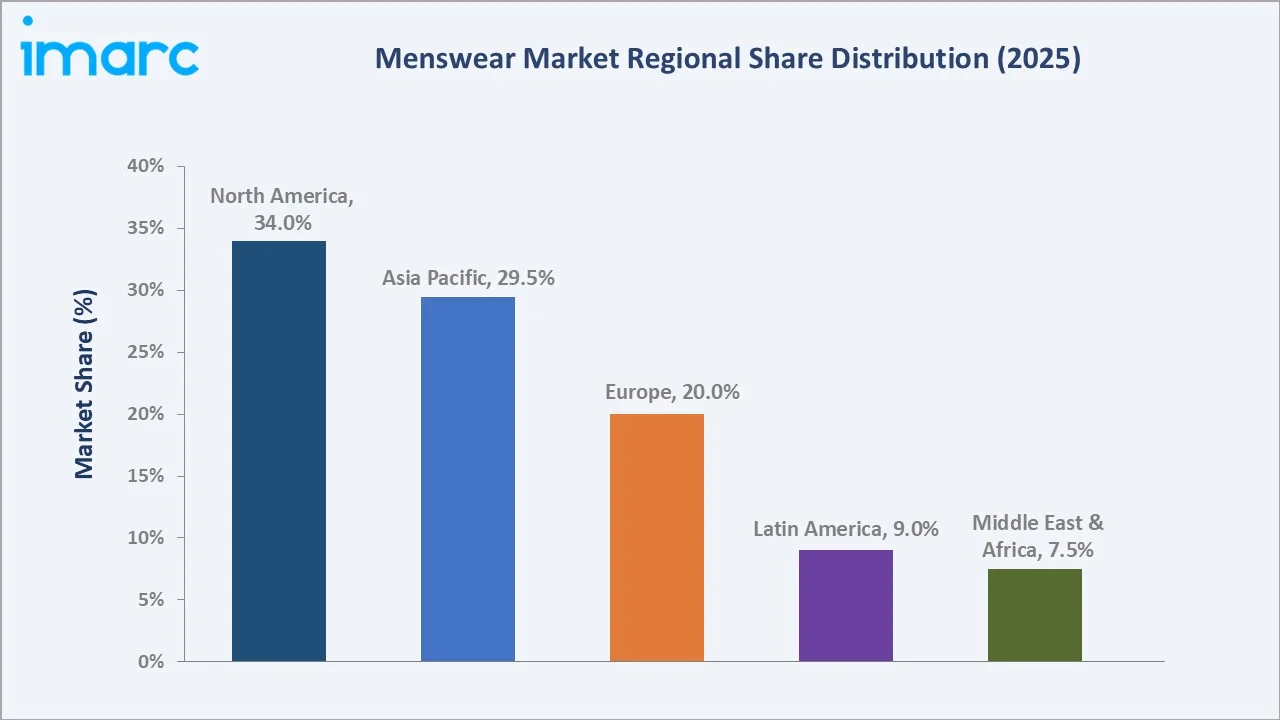

North America leads regionally with a 34.0% market share in 2025, anchored by the United States' premium athleisure and lifestyle menswear dominance. Shirts and t-shirts command the largest product type share at 32.5%, while all-season wear leads the season segment at 46.0%. Ethnic wear is the fastest-growing product type at ~6.3% CAGR, driven by surging demand from India, Southeast Asia, and the global South Asian diaspora market.

To get more information on this market, Request Sample

The global menswear market grew from USD 519.3 Billion in 2020 to USD 654.1 Billion in 2025, representing an absolute gain of USD 134.8 Billion. The post-COVID recovery accelerated in 2022–2024 as office return, social occasion dressing, and luxury splurge spending drove menswear above pre-pandemic trajectories. The market is projected to add a further USD 336.8 Billion by 2034, more than doubling the 2025-to-2034 incremental value versus the 2020-to-2025 growth quantum.

Executive Summary

The global menswear market is expanding at a 4.72% CAGR, driven by the convergence of fashion and function, the global rise of casual and athleisure dressing norms, and the emergence of digital-first DTC menswear brands. The market accounted for USD 654.1 Billion in 2025 and is forecast to reach USD 990.9 Billion by 2034

Shirts and t-shirts dominate at 32.5% in 2025, anchored by the universal appeal of casual tops across mass, premium, and luxury menswear tiers. Trousers at 21.0% and denims at 18.5% form the core wardrobe essentials segment. Ethnic wear at 15.0% is the fastest-growing product type at ~6.3% CAGR, driven by India's 1.4 billion domestic market and the 35.4 million Indian diaspora in the US, UK, Canada, and Gulf countries.

All-season wear leads seasonality at 46.0%, reflecting the growing preference for year-round versatile wardrobe pieces over climate-specific purchases. North America's 34.0% regional share is supported by the US's position as the world's largest single apparel market by value. Key players are accelerating the market's digital and sustainable transformation.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Shirts and T-Shirts – 32.5% share (2025) |

|

Fastest Growing Product Type |

Ethnic Wear – ~6.3% CAGR (2026-2034) |

|

Largest Season Segment |

All-Season Wear – 46.0% share (2025) |

|

Fastest Growing Season |

Summer Wear – ~5.8% CAGR (2026-2034) |

|

Leading Region |

North America – 34.0% share (2025) |

|

Top Companies |

NIKE, Inc., adidas AG, H & M Hennes & Mauritz GBC AB, Levi Strauss & Co., and Ralph Lauren Corporation |

Key Analytical Observations Supporting The Above Data:

- Shirts and t-shirts at 32.5% (2025) reflect the global casualization of male dress codes, from office smart-casual to social media streetwear influence. The graphic tee segment, led by Nike, H&M, and Zara, grew at 8%+ in 2024, driven by collaboration drops, brand licensing, and AI-generated custom print platforms.

- All-season wear at 46.0% (2025) reflects the structural shift toward capsule wardrobe purchasing with fewer, higher-quality, versatile pieces replacing large-volume seasonal fast fashion purchases. Levi's, Ralph Lauren Polo, and Uniqlo have built their menswear positioning around year-round essential items that transcend seasonal fashion cycles.

- North America at 34.0% (2025) is underpinned by the US's USD 154.5 Billion menswear market in 2025, with premium athleisure, luxury, and fast fashion all operating at significant scale in a single national retail ecosystem.

- Ethnic wear at ~6.3% CAGR represents the market's fastest-growing product category, driven by India's growing domestic fashion market, the global rise of occasion-led traditional dressing for weddings and festivals, and the normalization of fusion ethnic-western wear in corporate and social settings across South and Southeast Asia.

Menswear Market Overview

The global menswear market encompasses all apparel, accessories, and footwear designed for men, spanning mass-market fast fashion, mid-market lifestyle and casualwear, premium sportswear and athleisure, and luxury fashion. The market is served by over 50,000 brands globally across physical retail, e-commerce, and hybrid omni-channel distribution, with digital channels accounting for one-third of total menswear revenue in 2025 following accelerated e-commerce adoption during and after the COVID-19 pandemic.

The menswear market has undergone a structural transformation over the 2020–2025 period: the athleisure revolution elevated sportswear brands to fashion authority status, fast fashion shifted from pure price competition to sustainability positioning, and luxury menswear saw a steep post-COVID rebound, as experiences deferred during lockdowns were replaced by luxury goods spending.

Digitalization of the value chain, AI trend forecasting, 3D design prototyping, on-demand manufacturing, and social commerce are compressing design-to-retail cycles from 52 weeks to under 14 days for leading digital-native brands.

Market Dynamics

To evaluate market opportunities, Request Sample

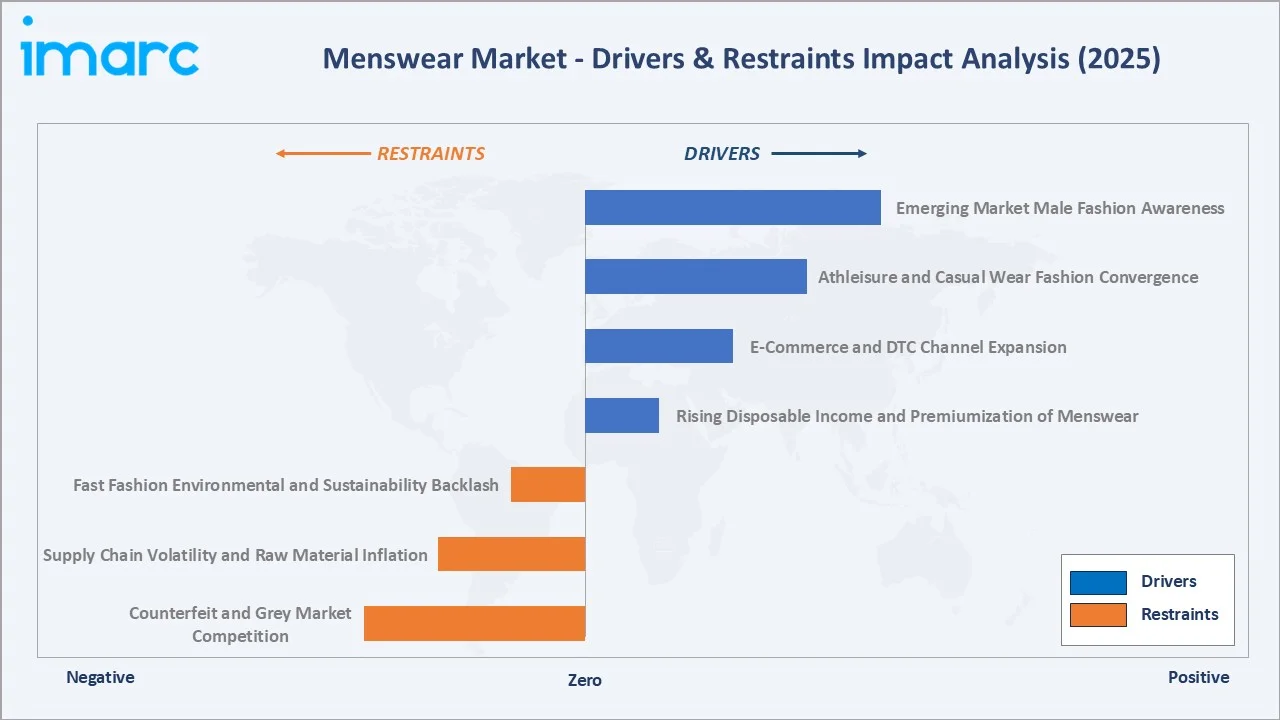

Market Drivers

- Rising Disposable Income and Premiumization of Menswear: By 2030, the global middle-class population is projected to reach 5.4 billion, with total spending estimated at USD 63 trillion. This is creating first-time premium menswear buyers who are bypassing the mass market and entering mid-premium directly through mobile commerce.

- E-Commerce and DTC Channel Expansion: Nike Direct crossed 42% of total global revenue in FY2025; Levi Strauss & Co.’s e-commerce business has grown from 5% of total net revenue in 2019 to 10% in 2024. Together, these shifts are repositioning menswear from a physical retail-dependent to a digital-first category.

- Athleisure and Casual Wear Fashion Convergence: The permanent shift to hybrid work post-COVID has normalized casual wear in professional settings, structurally expanding the addressable market for sportswear-influenced menswear.

- Emerging Market Male Fashion Awareness: India's male consumer is rapidly upgrading from unbranded commodity apparel to branded fashion. Vedant Fashions Limited’s IPO (owner of Manyavar brand), Fabindia's ethnic menswear expansion, and the rapid scaling of Myntra's dedicated menswear categories are creating a USD 18+ Billion domestic branded menswear opportunity by 2030.

Market Restraints

- Fast Fashion Environmental and Sustainability Backlash: EU's Ecodesign for Sustainable Products Regulation (ESPR) entering force from 2026 mandates minimum recycled content, repairability scoring, and digital product passports for all apparel sold in Europe.

- Supply Chain Volatility and Raw Material Inflation: Cotton prices fluctuated around 28% between 2022 and 2024, driven by weather-related crop failures in Pakistan and India. Synthetic fiber costs linked to petrochemical price cycles added further volatility.

- Counterfeit and Grey Market Competition: The global counterfeit apparel market is estimated at USD 450+ Billion annually, with luxury and premium menswear brands most heavily targeted. Social media platforms amplify counterfeit reach through influencer promotions, eroding brand trust and forcing USD 2+ Billion in annual anti-counterfeiting investment by major players.

Market Opportunities

- Sustainable and Circular Menswear Innovation: The global second-hand and resale apparel market is projected to reach USD 350 Billion by 2027, with menswear representing 40%+ of resale volume. Brands including Patagonia, Levi's, and Nike are building first-party resale channels that extend customer lifetime value and capture sustainability-motivated consumers aged 25–40.

- AI-Powered Personalization and On-Demand Manufacturing: AI-driven personalization platforms are increasing basket conversion by 25–35% for menswear by serving hyper-relevant product recommendations based on body measurement, style history, and social media fashion signals. On-demand manufacturing platform reduces unsold inventory waste by 40% versus seasonal buying models.

Market Challenges

- Brand Loyalty Fragmentation and Gen-Z Menswear Values: Gen-Z male consumers demonstrate 3x lower brand loyalty than millennials, as a survey suggests that over 50% of Gen Z consumers would switch brands if an alternative offered better quality or a lower price. The rise of micro-brands on TikTok, Instagram, and YouTube is fragmenting market share from established players, requiring continuous brand investment to maintain relevance.

- Sizing Standardization and Returns Costs: In 2026, the average e‑commerce return rate is projected at 20–21%, which is approximately 2–3 times higher than the 5–8.9% return rate typical for brick-and-mortar stores. Return processing costs are estimated at USD 15–25 per order, representing a USD 40+ Billion annual industry cost burden that constrains digital channel profitability.

Emerging Market Trends

1. Luxury Menswear Casualization and Streetwear Integration

Luxury houses, including Kering, LVMH, and Burberry, are incorporating streetwear aesthetics, oversized silhouettes, logo typography, and sneaker-first dressing into mainline seasonal collections. The global luxury menswear market exceeded USD 28 Billion in 2025, driven by the generational broadening of the luxury customer base and China's domestic luxury recovery.

2. Ethnic Wear Premiumization and Global Diaspora Demand

India's branded ethnic menswear market, led by Manyavar (Vedant Fashions), Fabindia, and Twamev, is growing at 14% annually, with wedding occasion wear driving average ticket sizes of INR 8,000–25,000. Globally, the South Asian diaspora across the US, UK, UAE, and Canada generates USD 3+ Billion annually in ethnic menswear imports, creating a premium export opportunity for Indian brands.

3. Sustainable Denim and Circularity Innovation

In September 2025, Kering’s Material Innovation Lab (MIL) presented S|STYLE 2025, Denim Lab, a sustainable fashion initiative showcased at Milan Fashion Week that brings together emerging designers to reinterpret denim using innovative, low‑impact materials and water‑saving technologies. Aligned with Kering’s water strategy and sustainability goals, the project highlights advanced dyeing, washing, and finishing techniques that drastically reduce water use and harmful chemicals in denim production.

4. AI-Driven Virtual Try-On and Digital Fashion

In June 2026, Google launched an AI‑powered virtual try‑on feature in Singapore that lets online shoppers upload a full‑length photo to see how clothing and shoes would look on them before purchase. The tool, available through Google Search, Shopping, and Images, aims to make fashion e‑commerce more interactive and confidence‑boosting for consumers.

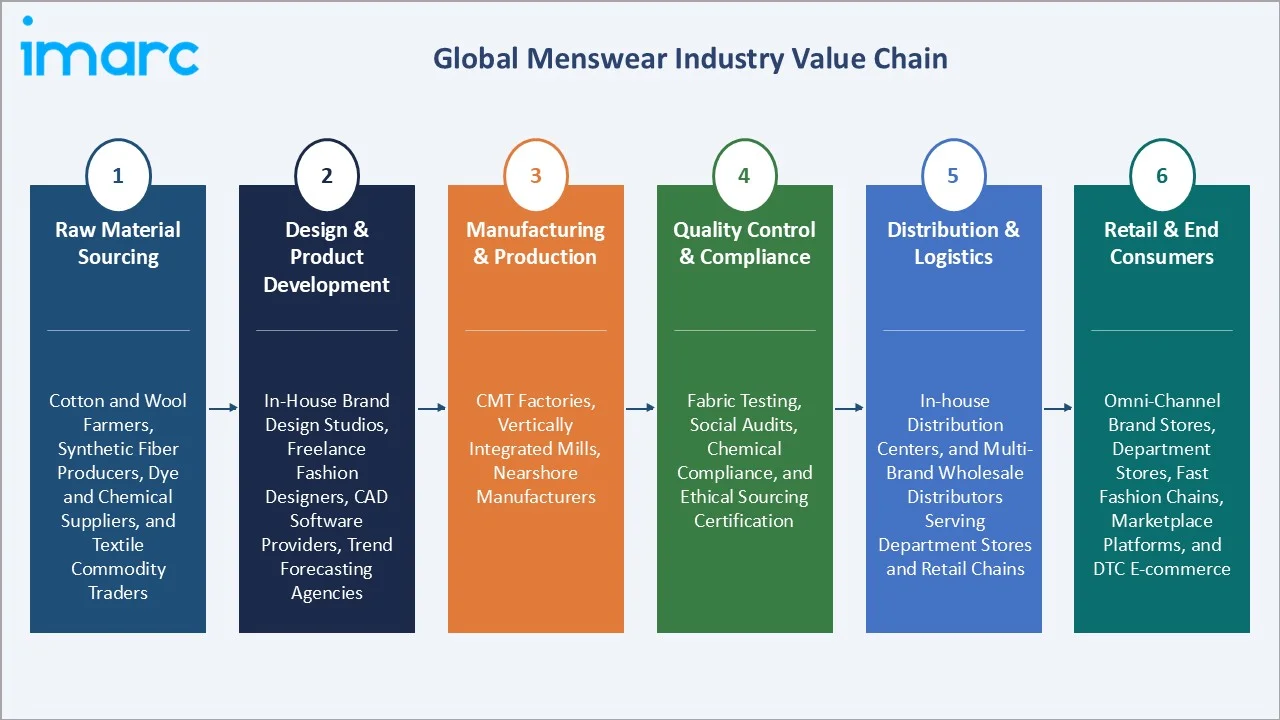

Industry Value Chain Analysis

The global menswear value chain is a globally distributed, multi-tier ecosystem spanning fiber and fabric production in Asia and Africa, design and brand development headquartered in Europe and North America, manufacturing concentrated in South and Southeast Asia, and multi-channel retail serving consumers across 180+ markets.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Cotton and wool farmers, synthetic fiber producers, dye and chemical suppliers, and textile commodity traders |

|

Design & Product Development |

In-house brand design studios, freelance fashion designers, CAD software providers, trend forecasting agencies |

|

Manufacturing & Production |

CMT factories, vertically integrated mills, nearshore manufacturers |

|

Quality Control & Compliance |

Fabric testing, social audits, chemical compliance, and ethical sourcing certification |

|

Distribution & Logistics |

in-house distribution centers, and multi-brand wholesale distributors serving department stores and retail chains |

|

Retail & End Consumers |

Omni-channel brand stores, department stores, fast fashion chains, marketplace platforms, and DTC e-commerce |

Technology Landscape in the Menswear Industry

AI-Powered Design and Trend Forecasting

WGSN and Trendalytics deploy AI-driven trend prediction models that analyze 500 million+ social media data points daily to forecast menswear color, silhouette, and product category trends 18–24 months in advance. Major brands, including Adidas and H&M, have integrated AI trend intelligence into their seasonal buying and private label design processes, reducing trend miss rates by 20–30% and markdown frequencies by 15%.

Sustainable Materials and Textile Innovation

Regenerative cotton, lyocell, and recycled polyester derived from plastic bottles are transitioning from niche to mainstream menswear materials. Bolt Threads' Mylo mushroom leather and Modern Meadow's bioleather, while pre-commercial, represent the frontier of post-petroleum material development that will reshape menswear premium accessories by 2030.

Omni-Channel and Social Commerce Technology

TikTok Shop included 13,430 stores for menswear & underwear in 2023, with Nike, Adidas, and Levi's all running brand storefronts. Instagram Shopping's checkout feature processes 2 million+ menswear transactions monthly in the US alone. Shopify's Shop Pay and Klarna's BNPL penetration at 35%+ of menswear e-commerce transactions are reducing purchase friction and extending average order values, particularly in the 18–35 male demographic that indexes highest for buy-now-pay-later adoption.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Shirts & T-Shirts |

32.5% |

2025 |

|

Season |

All-Season Wear |

46.0% |

2025 |

|

Distribution Channel |

Exclusive Stores |

🔒 |

2025 |

|

Region |

North America |

34.0% |

2025 |

By Product Type

Shirts and t-shirts command a 32.5% share in 2025, making them the largest and most versatile menswear category globally. The category spans mass-market basics, mid-premium lifestyle, performance athletic, and luxury, serving the complete male income and lifestyle spectrum.

To access detailed market analysis, Request Sample

Trousers at 21.0% encompass formal trousers, chinos, joggers, and technical performance pants. Denims at 18.5% represent a structurally stable category with ongoing premiumization. Ethnic Wear at 15.0% is the fastest-growing category at ~6.3% CAGR, driven by India's Tier-2 city branded occasion wear demand.

By Season

All-season wear leads at 46.0% in 2025. The category's dominance reflects the global shift toward versatile wardrobe essentials; the capsule wardrobe movement positions year-round basics as the highest-value-per-wear menswear investment. Polo shirts, Oxford button-downs, slim chinos, and the five-pocket jean are quintessential all-season menswear items purchased for year-round utility.

Summer wear at 32.0% is the fastest-growing season segment at ~5.8% CAGR, driven by climate change extending effective summer seasons in both Northern and Southern hemispheres, resort and travel wear recovery post-COVID, and the proliferation of summer-first street style cultures across Southeast Asia, India, and Latin America. Winter wear at 22.0% remains stable, driven by outerwear luxury with Moncler and Canada Goose representing the premium end of a structurally defensive category.

Regional Market Insights

North America's market leadership (34.0%, 2025) is anchored by the United States, the world's largest national menswear market at approximately USD 154.5 Billion in 2025. The US market combines the world's highest per-capita menswear spend with the deepest DTC brand ecosystems, most developed e-commerce infrastructure, and the broadest spread from mass-market to ultra-luxury within a single national consumer base.

Asia Pacific at 29.5% (2025) is the fastest-growing region, with China's luxury menswear recovery, India's first-generation branded apparel market, and Southeast Asia's young male demographic collectively projecting the region to surpass North America's share by 2031.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.0% |

Highest per-capita menswear spending globally, US premium and athleisure dominance, strong DTC brand ecosystems, Canada and Mexico growing middle-class fashion adoption |

|

Asia Pacific |

29.5% |

China's premiumization and luxury menswear expansion, growing urbanization driving ethnic and western wear convergence, Southeast Asia's fast-growing young male consumer base |

|

Europe |

20.0% |

Western Europe's luxury heritage brand strength, the UK and Germany's sustainable fashion regulation driving circular menswear |

|

Latin America |

9.0% |

Brazil's domestic fast fashion market growth, Mexico's cross-border trade with the US fashion ecosystem, rising middle-class male fashion consciousness |

|

Middle East & Africa |

7.5% |

GCC luxury menswear demand from high-net-worth consumers, Dubai's status as a fashion retail hub, African emerging market urbanization driving mid-market demand |

Europe at 20.0% sustains its luxury heritage and sustainable fashion regulatory leadership. Latin America (9.0%) and Middle East & Africa (7.5%) represent the highest upside geographies as urbanization and digital commerce accelerate branded menswear penetration.

Competitive Landscape

The global menswear market is highly fragmented at the brand level but moderately concentrated by revenue, with the top brands (Nike, Adidas, H&M, Inditex/Zara) controlling approximately 18–22% of total global menswear revenue.

|

Company Name |

Key Brands / Products |

Market Position |

Core Strength |

|

|

ACG, Jordan, Kobe, Nike, Nike Pro, Nike Sportswear |

Market Leader |

One of the world’s largest sportswear brands, DTC ecosystem leadership, AI-powered personalization |

|

|

Adidas Originals, Y-3, Adidas Performance, Adidas Sportswear, TERREX, Five Ten |

Market Leader |

Strong sportswear and lifestyle convergence, Yeezy brand legacy management |

|

|

H&M Man, COS Men, Weekday Men |

Strong Challenger |

Multi-brand strategy targeting mass and premium menswear, H&M Looop garment recycling innovation |

|

|

Levi’s, Beyond Yoga, Signature |

Strong Challenger |

The global denim reference brand, with a long heritage driving premium and customization strategy; Project F.L.X. laser finishing reducing water use |

|

|

Polo, Purple Label, RRL, Chaps, RLX, Pink Pony |

Challenger |

American luxury lifestyle brand with menswear at its core, strong department store and mono-brand distribution |

The mass market is contested by H&M, Zara, Uniqlo, and Primark, while the luxury segment is anchored by Kering, LVMH, and Prada Group.

Key Company Profiles

NIKE, Inc.

NIKE, Inc. is one of the world's largest athletic footwear and apparel companies. Nike's menswear strategy centers on performance-to-lifestyle product architecture, DTC digital ecosystem dominance, and cultural authority through sports, music, and digital creator collaborations.

- Product Portfolio: Nike performance shirts and shorts, Nike casualwear, Jordan lifestyle apparel, ACG outdoor wear, Nike Sportswear (NSW) streetwear, Nike Pro, and Kobe.

- Recent Developments: In June 2026, Jacquemus teamed up with NIKE, Inc. and the French Football Federation to launch a special lifestyle and pre‑match collection tied to the France national team ahead of the 2026 FIFA World Cup, blending high fashion with football culture.

- Strategic Focus: Nike By You mass customization scaling; Move to Zero sustainability program targeting 50% recycled polyester in all menswear; SNKRS cultural drops driving Gen-Z engagement and brand heat.

adidas AG

adidas AG offers menswear through its three-division strategy spanning Performance, Originals, and Sportswear, with premium Y-3 Yohji Yamamoto as a collaboration line.

- Product Portfolio: Adidas Originals (Stan Smith, Samba, Gazelle apparel), adidas performance wear, adidas TERREX outdoor, adidas Sportswear casual collection, premium Y-3 Yohji Yamamoto menswear collaboration, and Five Ten

- Recent Developments: In November 2024, adidas AG launched an exclusive “BelliGold” Originals collection in collaboration with Jude Bellingham, featuring premium Gazelle sneakers and an Originals clothing line inspired by retro football culture and modern elegance.

- Strategic Focus: Originals brand heat restoration post-Yeezy; Speedfactory on-demand manufacturing.

Market Concentration Analysis

The global menswear market is highly fragmented, with the top brands (Nike, Adidas, H&M, Inditex/Zara) controlling approximately 18-22% of total global menswear revenue. The luxury tier (Kering, LVMH, and Prada Group) holds 8–10% of total revenue at disproportionately higher margins, while the mass-market tier (H&M, Zara, Uniqlo, and Primark) commands high volumes at thin margins.

Market consolidation is driven by platform aggregation: Amazon Fashion's menswear marketplace handles 2,500+ menswear brands on a single platform, Myntra in India hosts 6,000+ menswear brands, and Zalando in Europe aggregates 4,500+ menswear brands, creating winner-takes-most platform dynamics that favor digitally capable brands with strong data analytics, fast replenishment, and high customer review scores.

Investment & Growth Opportunities

Fastest Growing Segments

Ethnic wear (~6.3% CAGR), summer wear (~5.8% CAGR), denims (~5.1% CAGR), and services including styling subscriptions and resale (~8% CAGR) represent the highest-return investment vectors through 2034. Together, these segments address an incremental market of approximately USD 280+ Billion by 2034, above 2025 levels.

Emerging Market Expansion

Asia Pacific's 29.5% regional share conceals the highest absolute growth opportunity: India's menswear market is projected to reach USD 65 Billion by 2030 at 12% CAGR, the fastest-growing major national menswear market globally. Southeast Asia's collective menswear market of USD 18 Billion in 2025 is growing at 8.5% CAGR, with Vietnam, Indonesia, and Thailand each hosting 30+ million male consumers in the 20–40 primary menswear buying cohort.

Investment and M&A Trends

- Menswear DTC platforms attracted USD 4.2 Billion in venture capital in 2023–2025, with India-focused brands receiving INR 1,000+ crore in PE investment. Global menswear resale platforms collectively raised USD 800+ Million in 2023–2025.

- Sustainability-linked fashion technology attracted USD 2.8 Billion in global investment in 2024, including Bolt Threads and Modern Meadow circular textile platform technologies that will reshape premium menswear material architecture by 2030.

Future Market Outlook (2026-2034)

The global menswear market will expand from USD 654.1 Billion in 2025 to USD 990.9 Billion by 2034 at a 4.72% CAGR. Shirts and t-shirts will retain product type leadership, but ethnic wear and functional activewear will gain significant share. Asia Pacific will overtake North America as the largest regional market by revenue between 2030 and 2032, driven by India's domestic brand market maturation and China's luxury menswear recovery.

By 2034, the menswear industry will be characterized by three convergent structural shifts: AI-personalized on-demand manufacturing reducing global unsold inventory waste by 35–50%, blockchain-enabled product authentication creating premium authentication premiums for luxury brands, and circular economy models representing 15–20% of total menswear value.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 100 industry participants in 2024–2025, including brand directors, category buyers, supply chain managers, sustainability officers, and retail analysts across the US, UK, Germany, India, China, and Japan.

Secondary Research

Secondary research covered Euromonitor International global apparel databases, Statista consumer survey data, McKinsey Global Fashion Index 2025, Business of Fashion annual reports, Brand Finance Global 500, and company annual reports and investor presentations for all key players.

Forecasting Models

Market size estimations used bottom-up forecasting incorporating per-capita apparel expenditure trends, male consumer population growth projections, category penetration benchmarks, and DTC digital channel migration rates. A 4.72% CAGR reflects consensus cross-validated against Euromonitor's menswear category forecast and IMARC's primary expert panel.

Menswear Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Trousers, Denims, Shirts and T-Shirts, Ethnic Wear, Others |

| Seasons Covered | Summer Wear, Winter Wear, All-Season Wear |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Exclusive Stores, Multi-Brand Retail Outlets, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | NIKE Inc., adidas AG, H & M Hennes & Mauritz GBC AB, Levi Strauss & Co., Ralph Lauren Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the menswear market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global menswear market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the menswear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Menswear Market Report

The market reached USD 654.1 Billion in 2025 and is forecast to reach USD 990.9 Billion by 2034 at a 4.72% CAGR.

Shirts and t-shirts lead at 32.5% in 2025, reflecting the universal appeal of casual and performance tops across all income tiers and geographies in the global menswear market.

All-season wear leads at 46.0% in 2025, reflecting the global shift toward versatile capsule wardrobe essentials that transcend seasonal fashion cycles and deliver higher value-per-wear.

North America leads at 34.0% in 2025, anchored by the United States, the world's largest national menswear market, with the highest per-capita menswear spend and deepest DTC brand ecosystem globally.

Some of the key players in the market include NIKE, Inc., adidas AG, H & M Hennes & Mauritz GBC AB, Levi Strauss & Co., and Ralph Lauren Corporation.

Ethnic Wear is the fastest-growing product type at ~6.3% CAGR, driven by India's domestic occasion wear market, the global South Asian diaspora's branded ethnic apparel demand, and the broader global trend toward cultural authenticity in fashion expression.

Rising global male fashion consciousness, e-commerce and DTC channel proliferation, athleisure and casualwear convergence, emerging market middle-class expansion, AI-personalized shopping, and ethnic wear premiumization are the primary market catalysts.

Fast fashion sustainability regulation, supply chain volatility, cotton price inflation, counterfeit competition, Gen-Z brand loyalty fragmentation, high e-commerce return rates, and sizing standardization complexity are the primary challenges constraining market profitability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)