Metal Forging Market Size, Share, Trends and Forecast by Raw Material, Application, and Region, 2026-2034

Global Metal Forging Market Size, Share, Trends & Forecast (2026-2034)

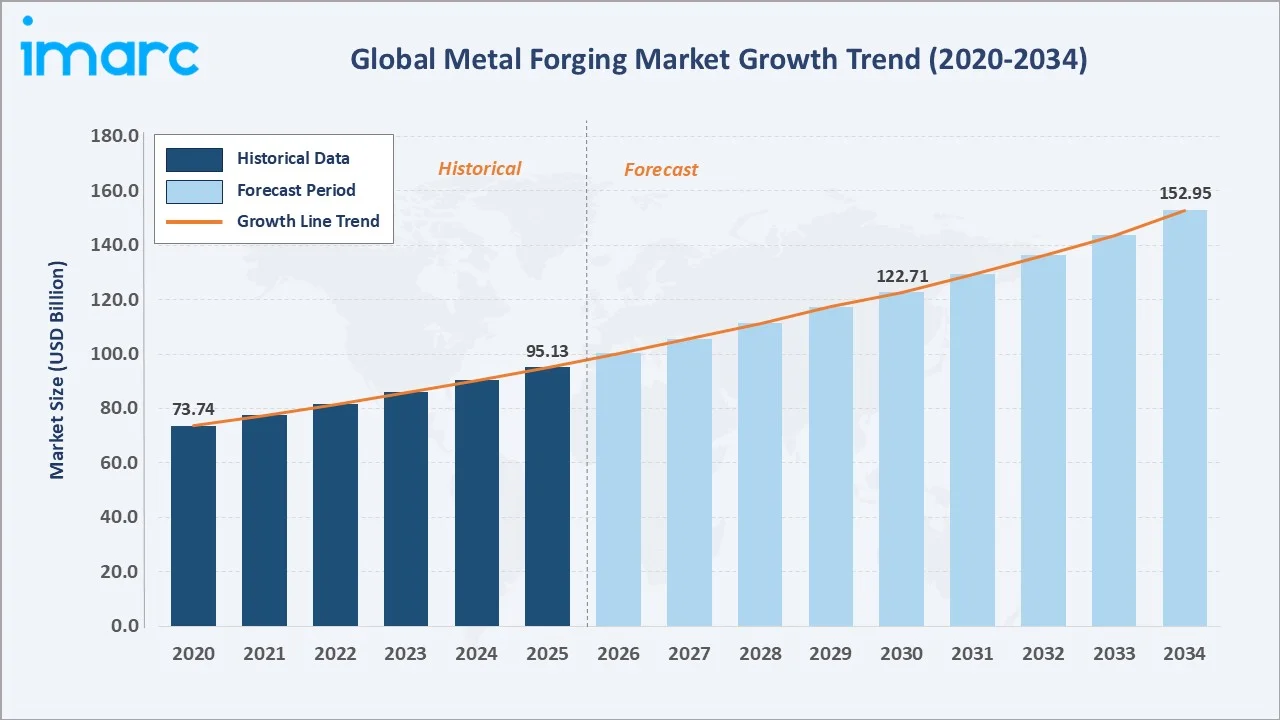

The global metal forging market size reached USD 95.13 Billion in 2025. It is projected to reach USD 152.95 Billion by 2034, at a CAGR of 5.22% during 2026-2034. Rising demand from the automotive and aerospace sectors, rapid industrialization across Asia Pacific, technological advancements in precision forging, and growing investments in infrastructure and renewable energy are the primary growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 95.13 Billion |

|

Forecast Market Size (2034) |

USD 152.95 Billion |

|

CAGR (2026-2034) |

5.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (42.3% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (~6.1% CAGR) |

|

Leading Raw Material |

Carbon Steel (38.4%, 2025) |

|

Leading Application |

Automotive (36.4%, 2025) |

The chart below illustrates the global metal forging market growth trajectory from 2020 through 2034, contrasting historical performance against a sustained forecast curve powered by automotive lightweighting, aerospace recovery, and infrastructure expansion across emerging economies.

To get more information on this market, Request Sample

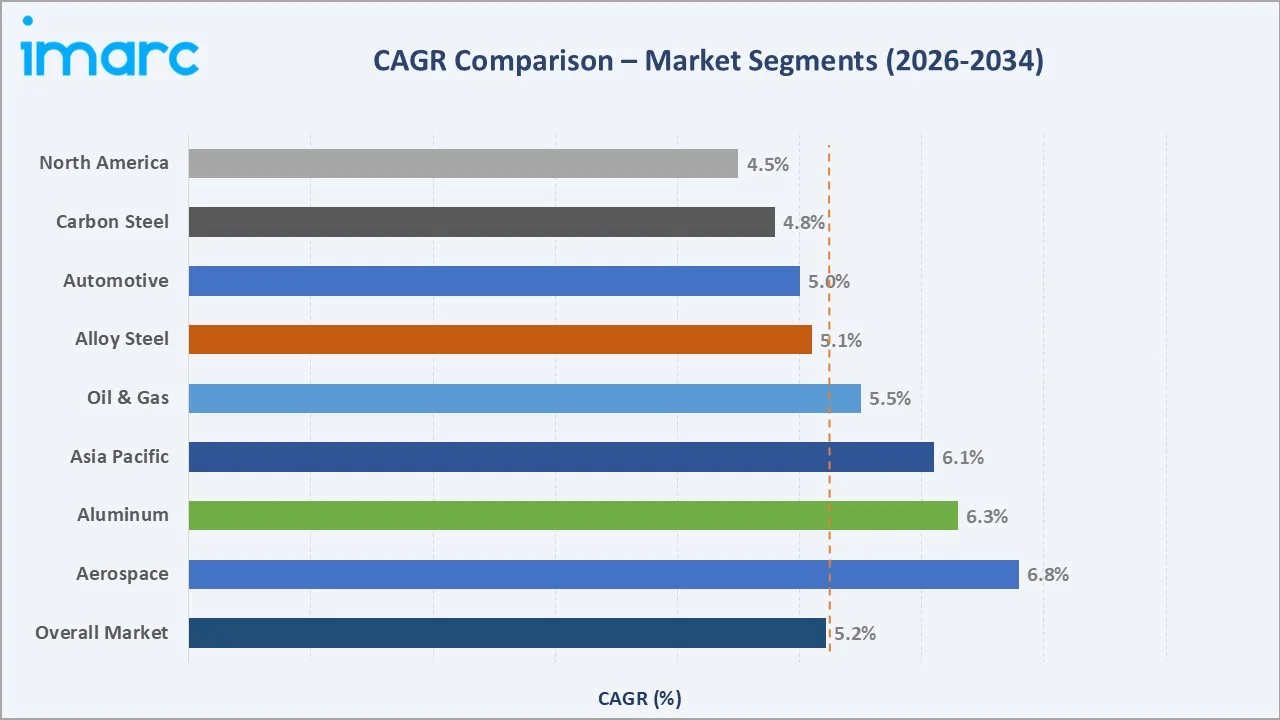

Segment-level CAGR comparisons highlight aluminum forging and aerospace application as the fastest-growing sub-categories within the global metal forging market forecast through 2034, both outpacing the overall market rate of 5.22%.

Executive Summary

The global metal forging market is undergoing sustained expansion. It is driven by rising end-use demand in automotive, aerospace, oil and gas, and infrastructure sectors. Valued at USD 95.13 Billion in 2025, the market is forecast to reach USD 152.95 Billion by 2034 at a CAGR of 5.22%.

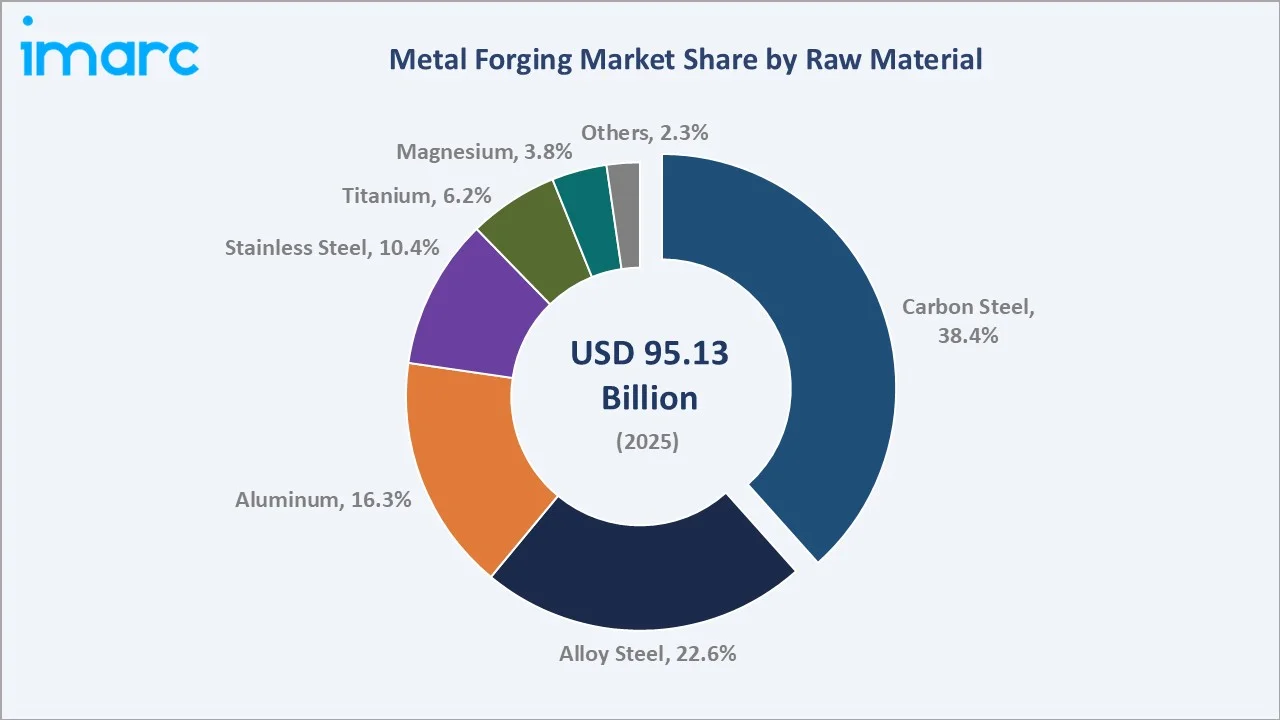

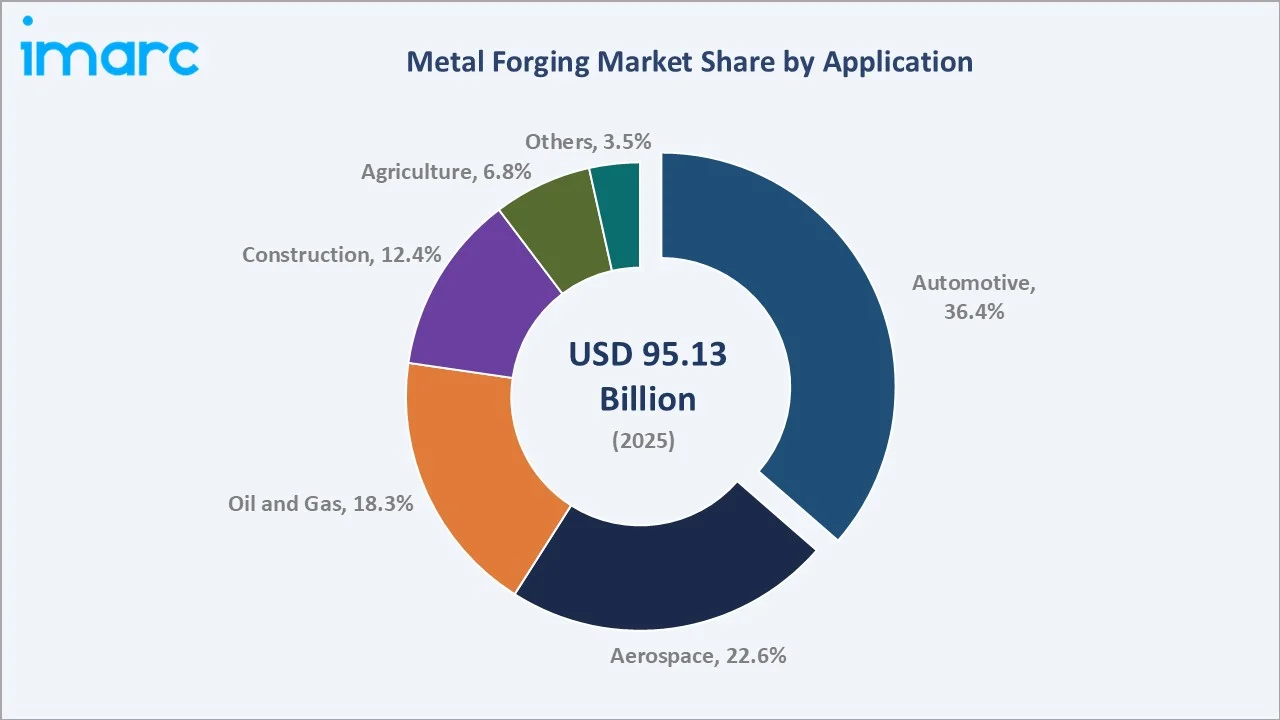

Carbon steel retained the dominant raw material position at 38.4% share in 2025, supported by its cost-competitiveness and broad application range. Alloy steel follows at 22.6%, while aluminum – the fastest-growing material at ~6.3% CAGR – accounted for 16.3% share. The automotive application segment leads at 36.4%, reflecting the sector's reliance on forged components for structural and powertrain parts. Aerospace commands 22.6% share, accelerating on the back of commercial aviation fleet expansion and defense procurement uptick observed globally in 2024–2025.

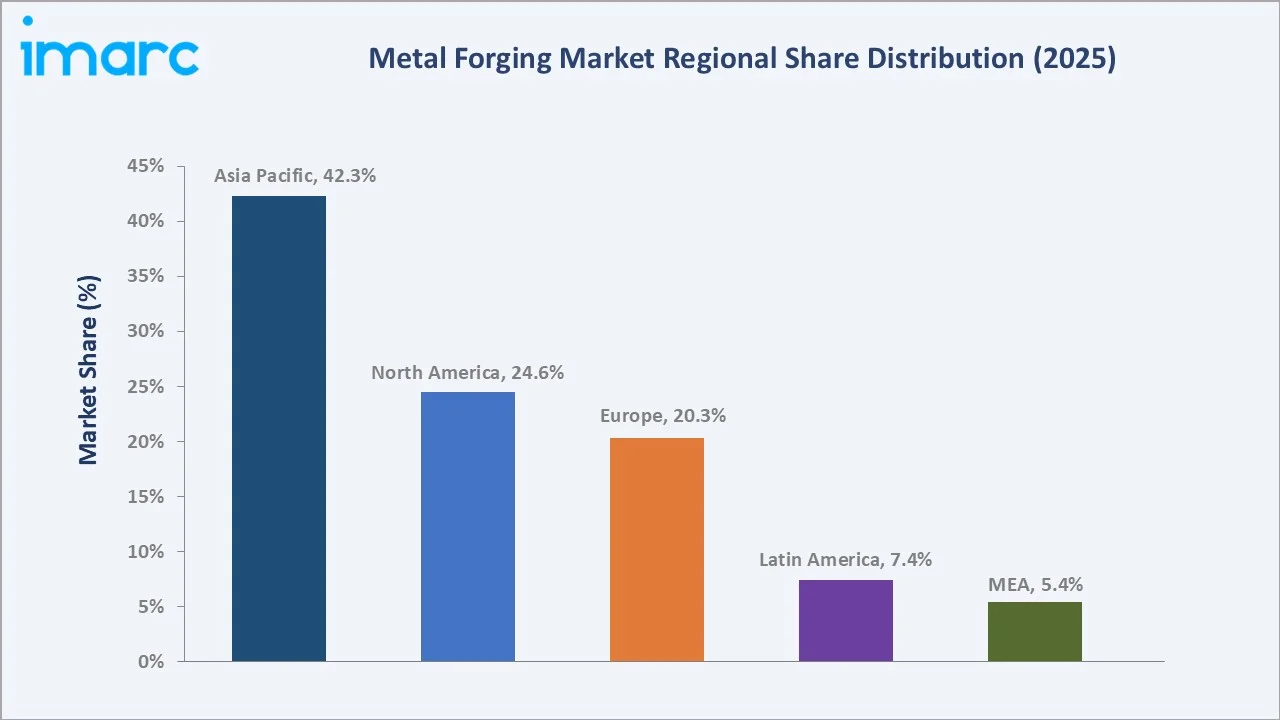

Asia Pacific dominates with 42.3% global revenue share, led by China's massive industrial base and India's manufacturing growth. North America follows at 24.6%, anchored by U.S. aerospace OEM demand. The metal forging market outlook remains positive as electrification of mobility, decarbonization of industrial processes, and infrastructure investment converge to sustain structural demand for high-performance forged components through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Raw Material |

Carbon Steel – 38.4% share (2025) |

|

Second Raw Material |

Alloy Steel – 22.6% share (22025) |

|

Leading Application |

Automotive – 36.4% share (2025) |

|

Second Application |

Aerospace – 22.6% share (2025) |

|

Leading Region |

Asia Pacific – 42.3% revenue share (2025) |

|

Top Companies |

Bharat Forge, Precision Castparts Corp, Thyssenkrupp AG, Nippon Steel Corporation, Arconic, Larsen & Toubro Limited, ELLWOOD Group Inc, Scot Forge Company |

|

Market Opportunity |

EV lightweighting driving aluminum forging at ~6.3% CAGR (2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Carbon Steel's 38.4% dominance in 2025 reflects its entrenched position in automotive powertrain, construction equipment, and oil & gas pressure vessel applications, where cost and availability are critical procurement criteria.

- Alloy Steel's 22.6% share is driven by rising demand for high-strength, heat-treated forgings in heavy equipment, defense, and power generation sectors requiring superior mechanical properties.

- Aluminum forging at 16.3% share is growing at ~6.3% CAGR, the fastest among raw materials, as EV manufacturers mandate lightweight components to extend battery range without structural compromise.

- Asia Pacific's 42.3% global dominance is primarily anchored by China's role as the world's largest auto manufacturer, producing over 30 million vehicles annually, with forged components integral to driveshaft, wheel hub, and crankshaft production.

- Automotive's 36.4% application share reflects the sector's structural dependency on forged parts – connecting rods, crankshafts, steering knuckles, and wheel hubs – across ICE and EV platforms.

- Aerospace commands 22.6% share with components such as landing gear, turbine discs, and engine mounts demanding ultra-tight tolerances and certification standards met only through precision forging processes.

Global Metal Forging Market Overview

Metal forging is a manufacturing process in which metal is shaped using compressive forces applied through dies, presses, or hammering. The process produces components with superior strength, grain structure, and mechanical integrity compared to casting or machining from stock.

The global market encompasses open-die forging, closed-die (impression-die) forging, ring rolling, isothermal forging, and cold forging, serving a diverse spectrum of industries including automotive, aerospace, oil and gas, construction, agriculture, and defense.

The industry operates at the intersection of raw material supply chains, advanced manufacturing technology, and high-specification end-use demand. Macroeconomic influences include infrastructure investment cycles, defense budget allocations, automotive production volumes, and global energy sector capital expenditure. Structural shifts toward electrification, lightweighting, and precision engineering are redefining process innovation. Automation, digital twin integration, and AI-driven quality control are transforming how forgings are designed and produced at scale.

Market Dynamics

To evaluate market opportunities, Request Sample

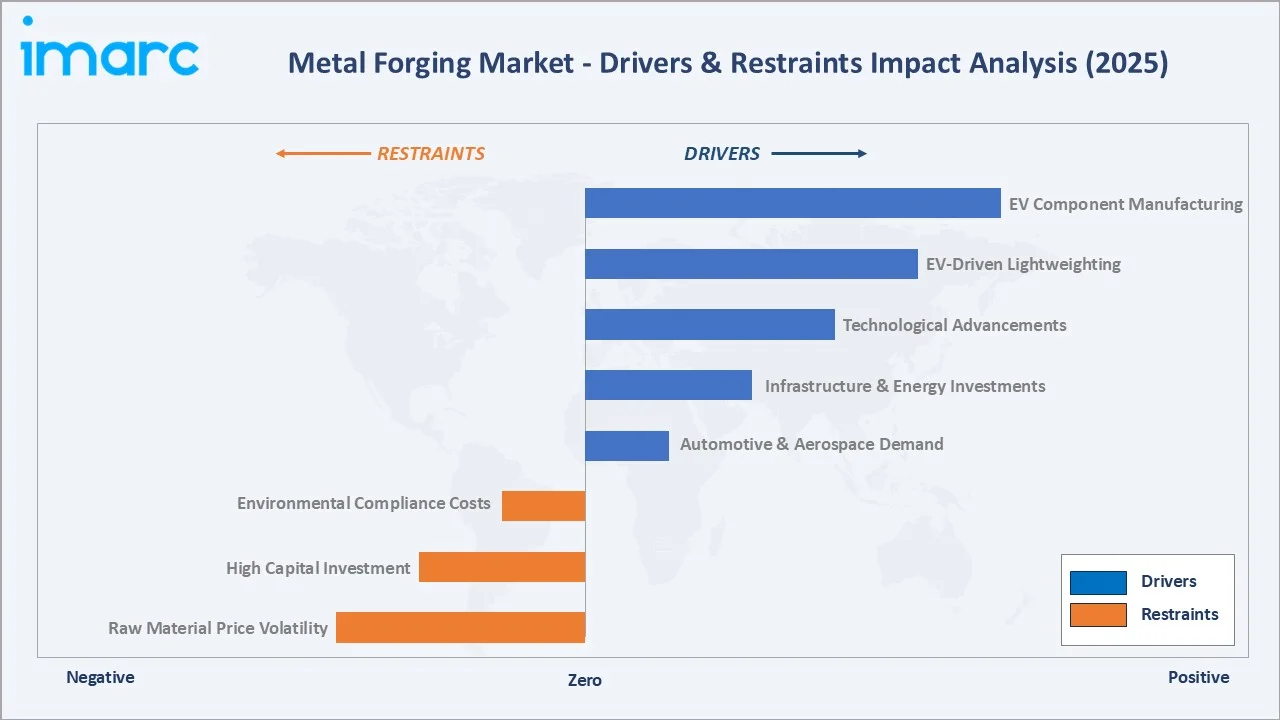

Market Drivers

- Automotive & Aerospace Demand: Structural components in both sectors require forged parts for their unmatched strength-to-weight ratio. The global commercial aircraft fleet is expected to double by 2041 per Boeing's forecast, sustaining long-term aerospace forging orders.

- Infrastructure & Energy Investments: Global infrastructure investment needs are projected to reach USD 94 trillion cumulatively by 2040, implying annual spending levels exceeding USD 3.5 – 4.0 trillion. Forged components are integral to construction equipment, power turbines, pipelines, and wind energy nacelles, creating multi-year procurement cycles for forging manufacturers.

- Technological Advancements: Closed-die precision forging, isothermal forging, and computer-aided die design are enhancing material utilization and dimensional precision. Automation in forging cells is shortening cycle times, strengthening the competitive edge of high-volume producers.

- EV-Driven Lightweighting: Electric vehicle production requires lighter, stronger components to maximize battery range. Demand for aluminum and titanium forging is increasing in line with EV chassis, suspension, and structural battery enclosure needs, growing at a notable pace through 2034.

Market Restraints

- Raw Material Price Volatility: Steel scrap, aluminum, and titanium sponge prices experience substantial commodity cycle volatility. In 2024, global scrap steel prices swung sharply, putting pressure on forging manufacturer margins, especially for small and mid-size operators with limited risk management capabilities.

- High Capital Investment: Setting up a modern closed-die forging facility demands substantial investment, varying with capacity and automation. This high capital requirement restricts market entry and pushes smaller players toward niche or regional markets with constrained pricing power.

- Environmental Compliance Costs: Forging operations consume large amounts of energy and generate substantial CO2 emissions. Stricter EU and U.S. EPA regulations on industrial carbon intensity are raising compliance costs, impacting the cost structures of high-volume manufacturers.

Market Opportunities

- EV Component Manufacturing: The global electric vehicle fleet is projected to exceed 145 million units by 2030. Each EV uses significantly fewer forged parts than an ICE vehicle, but the value per part is considerably higher due to lightweighting and precision demands, creating revenue growth opportunities for specialized forgers.

- Defense Sector Expansion: Global defense budgets exceeded USD 2.63 Trillion in 2025. Military aviation, naval shipbuilding, and armored vehicle programs require certified, high-alloy precision forgings – a segment commanding premium margins and offering multi-year contracted revenue streams for qualified suppliers.

- Emerging Market Industrialization: India's Production-Linked Incentive (PLI) scheme for advanced manufacturing and Southeast Asia's growing automotive assembly base are creating greenfield demand centers for forged components, particularly in mid-range automotive and agricultural equipment categories.

Market Challenges

- Skilled Workforce Shortage: Precision forging and die-design expertise demands a decade or more of specialized training. In North America and Europe, aging workforces and a limited vocational pipeline are creating capacity constraints at premium forging facilities, posing potential delivery risks for OEM customers.

- Competition from Alternative Processes: Advanced casting, metal additive manufacturing, and composite structures are increasingly viable for low-volume or complex geometries, directly competing with forging in aerospace and medical device segments where design flexibility outweighs volume economics.

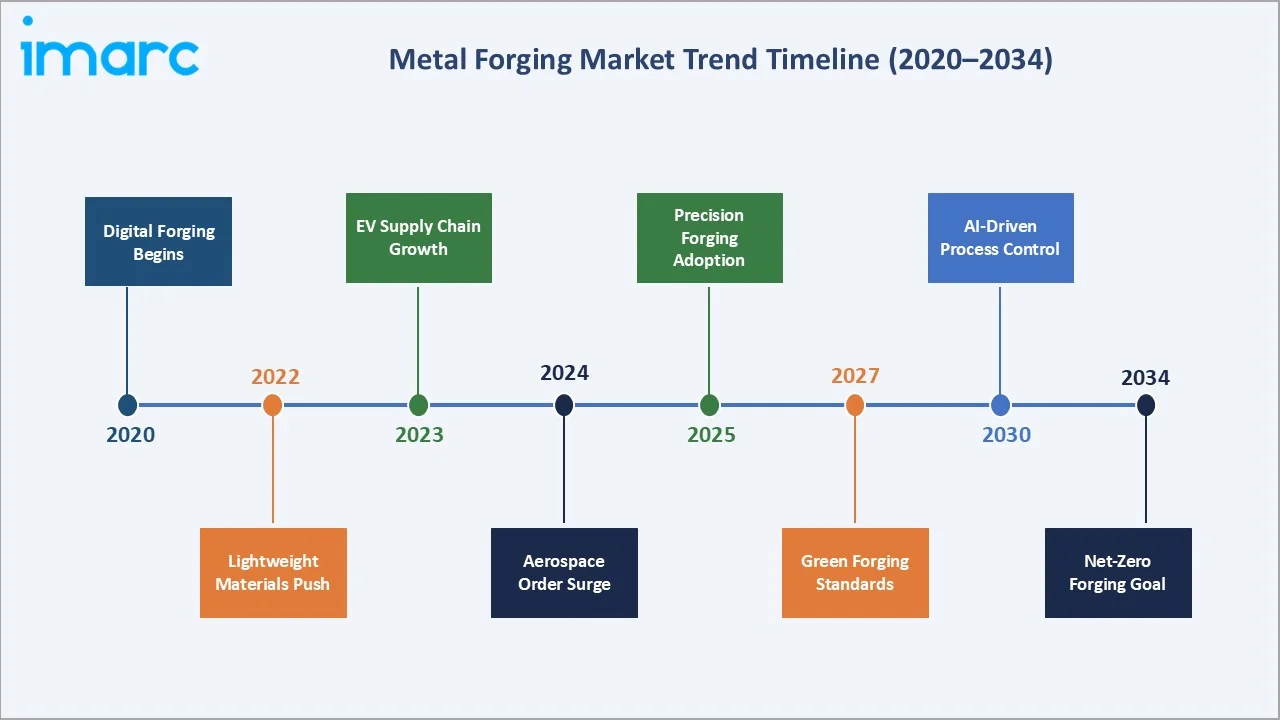

Emerging Market Trends

1. Electric Vehicle Lightweighting Demand

EV platforms demand significantly lighter structural components compared to ICE vehicles. Aluminum and titanium forging requirements are rising to meet these specifications, with EV-focused forging contracts becoming a rapidly growing revenue segment for major suppliers.

2. Automation and Smart Forging Integration

Robotic forging cells, servo-controlled hydraulic presses, and real-time SPC (Statistical Process Control) are becoming standard in Tier-1 forging facilities. Automation reduces human error, improves repeatability, and enables 24/7 production cycles. Smart forging lines using IoT sensors generate data that feeds predictive maintenance algorithms, reducing downtime by an estimated 18–24% in leading facilities.

3. Titanium and Specialty Alloy Adoption

Titanium forging is expanding its presence in aerospace, medical implant, and high-performance automotive applications. Its strength-to-weight advantage and biocompatibility make it essential for specific segment requirements. Nickel and cobalt superalloy forgings are likewise crucial for jet engine hot-section components subjected to extreme thermal conditions.

4. Nearshoring and Supply Chain Resilience

Post-pandemic supply chain disruptions have accelerated OEM reshoring strategies. Automotive and aerospace OEMs in North America and Europe are increasingly sourcing from local or near-regional forging suppliers to shorten lead times and mitigate geopolitical risks, driving forging capacity investment in the U.S., Mexico, Poland, and India.

5. Green Forging and Decarbonization

EU's Carbon Border Adjustment Mechanism (CBAM) and voluntary net-zero commitments from automotive OEMs are pressuring forge shops to reduce Scope 1 and 2 emissions. Electric induction heating, hydrogen-based furnace trials, and renewable energy procurement are the primary decarbonization strategies being deployed across leading European forging groups.

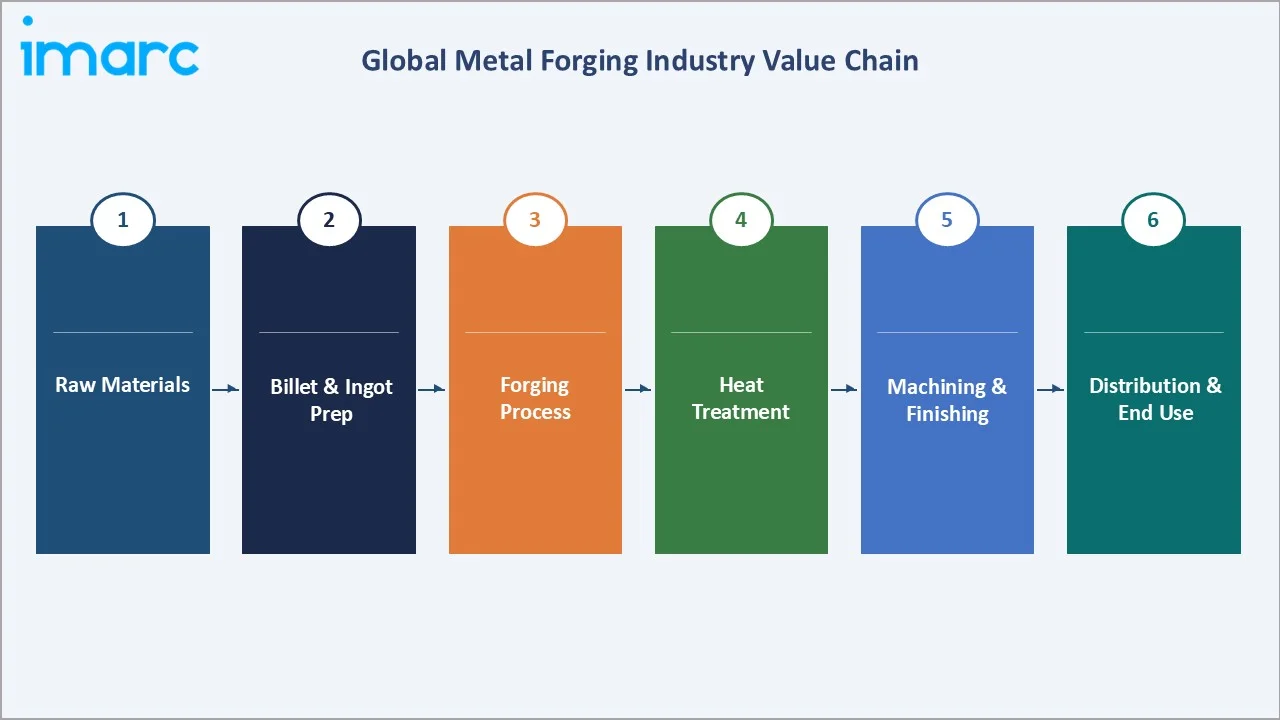

Industry Value Chain Analysis

The global metal forging industry value chain spans six integrated stages, from raw material extraction to end-user delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall metal forging market analysis.

|

Value Chain Stage |

Description |

|

Raw Materials |

Iron ore, bauxite, scrap steel, titanium sponge; primary suppliers are concentrated in China, Australia, Russia, and Brazil |

|

Billet & Ingot Preparation |

Steel and aluminum smelters producing billets and ingots for forging processes |

|

Forging Process |

Open-die, closed-die, ring-rolling operations used to shape metal components |

|

Heat Treatment & Finishing |

Annealing, quenching, tempering, shot blasting; typically performed in-house by OEMs or specialized vendors |

|

Machining & Quality Control |

CNC machining, non-destructive testing (NDT), surface treatment to ensure component precision and reliability |

|

Distribution & End Users |

Tier-1 automotive suppliers, aerospace OEMs, oil & gas operators, and construction contractors |

OEM forging manufacturers hold the highest strategic value by integrating raw material inputs, advanced tooling, and precision process technology into certified, customer-specific components. Distribution is primarily direct-to-OEM for Tier-1 automotive and aerospace customers, while distributors serve smaller industrial and aftermarket segments.

Technology Landscape in the Metal Forging Industry

Precision and Isothermal Forging

Precision closed-die forging creates near-net-shape components that reduce the need for post-forging machining. Isothermal forging, performed at elevated die temperatures matching the workpiece, is essential for titanium and nickel superalloy parts in jet engines. These techniques decrease material waste and lower the cost per part in high-value aerospace programs.

Automation and Robotics

Robotic handling systems, servo-electric presses, and automated die-change systems are being deployed across high-volume forging lines. Automation improves output consistency and supports JIT delivery requirements from automotive OEMs.

Digital Twin and IoT Integration

Digital twin models of forging dies and process parameters allow engineers to simulate material flow, temperature distribution, and die wear before physical tooling is cut. IoT-enabled press monitoring captures real-time force, speed, and temperature data, enabling predictive maintenance and reducing unplanned downtime. Simulation-led die design helps achieve significant reductions in tooling cost.

Advanced Materials Processing

Hydrogen-assisted sintering and electric arc furnace steel production are being integrated into upstream processes to lower the carbon footprint of raw material inputs. PVD surface treatment of dies is extending tool life in high-cycle forging environments. Powder metallurgy combined with hot isostatic pressing (HIP) is enabling complex near-net-shape titanium components for aerospace at scale.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Raw Material |

Carbon Steel |

38.4% |

2025 |

|

Application |

Automotive |

36.4% |

2025 |

|

Region |

Asia Pacific |

42.3% |

2025 |

By Raw Material

To access detailed market analysis, Request Sample

Carbon steel leads the global metal forging market raw material segmentation with a 38.4% share in 2025. Its dominance is driven by cost-effectiveness, widespread availability, and broad applicability across automotive powertrain components, construction machinery, and oil and gas pressure equipment.

By Application

Automotive dominates the global metal forging application segmentation at 36.4% share in 2025. Forged components – crankshafts, connecting rods, steering knuckles, wheel hubs, and suspension arms – are integral to both ICE and EV vehicle architectures.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

42.3% |

China & India auto/infra boom, ASEAN industrialization, Make in India push |

|

North America |

24.6% |

U.S. aerospace OEM demand, defense procurement, reshoring of supply chains |

|

Europe |

20.3% |

Automotive lightweighting, aerospace supply chain, EV transition requirements |

|

Latin America |

7.4% |

Brazil industrial sector, oil & gas upstream expansion, agri-equipment demand |

|

Middle East & Africa |

5.4% |

GCC infrastructure projects, Vision 2030, growing energy sector investments |

Asia Pacific commands 42.3% of global metal forging revenue in 2025 – the largest regional share by a significant margin. China is the single most critical national market, combining the world's largest automotive production base with massive infrastructure capital expenditure.

North America holds 24.6% share, anchored by U.S. aerospace defense procurement, reshoring of automotive forging supply chains, and robust oil and gas capital expenditure in Texas and the Permian Basin. Europe accounts for 20.3% of global revenue. Germany, France, and the UK represent the core demand centers, supported by Tier-1 automotive OEMs and aerospace supply chain partners to Airbus and Rolls-Royce.

Competitive Landscape

|

Company Name |

Key Brand / Division |

Market Position |

Core Strength |

|

Bharat Forge |

BFL |

Leader |

Scale in automotive forging, global MNC clients, EV component strategy |

|

Precision Castparts Corp. |

Precision Castparts Corp. (PCC) |

Leader |

Aerospace-grade components, titanium forging, FAA-certified supply |

|

Thyssenkrupp AG |

thyssenkrupp Forged Tech |

Leader |

European automotive, high-strength steel, green steel transition |

|

Nippon Steel Corporation |

Nippon Steel & Sumikin Precision Forge, Inc. (NSPF) |

Leader |

Japan & Asia Pacific, special steels, advanced heat treatment |

|

Arconic |

Arconic |

Challenger |

Aluminum & titanium forging, aerospace and defense focus |

|

Larsen & Toubro Limited |

L&T Heavy Engineering |

Challenger |

India market leadership, nuclear and defense forgings |

|

ELLWOOD Group Inc |

Ellwood |

Emerging |

North American mid-market, oil & gas and mining applications |

|

Scot Forge Company |

Scot Forge |

Emerging |

Custom open-die forgings, agile operations, North American niche |

The global metal forging market's competitive landscape is moderately fragmented. Global OEM-focused players such as Bharat Forge, Precision Castparts Corp, Thyssenkrupp AG, Nippon Steel Corporation, Arconic, Larsen & Toubro Limited, ELLWOOD Group Inc, Scot Forge Company compete alongside regional specialists and high-volume Asian manufacturers.

Key Company Profiles

Bharat Forge

Bharat Forge Ltd. is one of the world's largest forging companies, headquartered in Pune, India. Founded in 1960, it operates 18 manufacturing plants across India, Germany, Sweden, and North America with a total installed capacity exceeding 716,500 metric tons per annum.

- Product & Platform Portfolio: Bharat Forge's product range spans powertrain components (crankshafts, connecting rods), chassis and suspension forgings, aerospace structural parts, oil and gas pressure components, and defense forgings. It serves global Tier-1 automotive OEMs including Daimler, PACCAR, Volvo, and Cummins.

- Recent Developments: In 2025, Bharat Forge Ltd. and Liebherr announced a strategic collaboration to establish a state-of-the-art manufacturing facility in Pune, India. The facility will feature advanced forging and machining technologies, including a ring mill, to produce high-precision landing gear components, supporting global aerospace industry demand.

- Strategic Focus: Bharat Forge's strategy centers on diversification from traditional automotive forging into aerospace, defense, and EV components. Its technology partnerships with global Tier-1 suppliers and investment in aluminum and titanium forging capabilities position it as a leading player in next-generation mobility supply chains.

Precision Castparts Corp.

Precision Castparts Corp. founded in 1947 and headquartered in Portland, is a global leader in the manufacture of complex metal components and products for critical industries such as aerospace, industrial gas turbines, defense, power generation, and general industry.

- Product & Platform Portfolio: Company offers forged products, investment castings, and engineered components used in critical aerospace and industrial applications.

- Recent Developments: In 2026, Precision Castparts Corp restarted its acquisition trajectory of UK‑based Morvern Group. The move strengthens PCC’s position in turbine casting capabilities and expands its footprint in the European aerospace and defense supply chains.

- Strategic Focus: Leverages conglomerate strength and capital allocation to support precision forging businesses that serve high‑growth segments like aerospace and energy.

Arconic

Arconic is a U.S.‑based engineering and manufacturing company specializing in lightweight metals solutions, especially aluminum and advanced forged products for aerospace, automotive, and industrial markets.

- Product & Platform Portfolio: Covers engineered aluminum products, advanced alloys, and precision components that support performance and weight reduction in high‑value industries.

- Recent Developments: In 2025, Arconic Corporation has commissioned a $57.5 million expansion at its Davenport Works plant in Iowa, effectively doubling domestic High Purity Aluminum (HPA) production for aerospace and defense applications, supporting forged and advanced aluminum components.

- Strategic Focus: Focuses on sustainable materials, innovation in metal processing technologies, and serving high‑growth aerospace and transportation segments.

Market Concentration Analysis

The global metal forging market exhibits moderate fragmentation. The top five players – Bharat Forge, Precision Castparts Corp., Thyssenkrupp AG, Nippon Steel Corporation, and Arconic– collectively account for an estimated 18–25% of global market revenue in 2025. The remaining share is distributed across a large number of regional manufacturers in China, India, Germany, Japan, and North America, many of which serve domestic automotive and construction equipment markets.

The market is bifurcated across two competitive tiers. At the premium OEM tier, consolidation is occurring around aerospace certification, EV-specific material capability (aluminum, titanium), and automation investments. Simultaneously, Asia Pacific – particularly Chinese manufacturers – is generating competitive challengers targeting international export markets with cost-competitive offerings in carbon and alloy steel forgings.

Market concentration is expected to increase modestly through 2034 as EV supply chain consolidation, certification barriers in aerospace, and capital intensity drive smaller players toward merger or exit. Strategic acquisitions, joint ventures with OEMs, and technology licensing are expected to be the primary consolidation mechanisms over the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Aluminum forging represents the highest-growth raw material opportunity, driven by demand for lightweighting in electric vehicles and aerospace. Aerospace is the fastest-growing end-use segment. Titanium forging for aerospace and medical implants commands premium margins above carbon steel equivalents, offering significant revenue potential for specialized operators.

Emerging Market Expansion

India represents the highest-potential emerging market for forging capacity investment, driven by domestic automotive and defense demand, PLI scheme incentives, and cost-competitive labor for semi-skilled operations. Vietnam, Thailand, and Indonesia are emerging as secondary investment targets as Japanese and Korean automotive OEMs relocate assembly and supply chain operations to ASEAN economies.

Venture and Strategic Investment Trends

Private equity and strategic capital is targeting mid-tier forging operators with established OEM relationships but underinvested automation infrastructure. Key investment themes include: (1) aluminum and titanium forging capacity for EV and aerospace, (2) automation and digitalization to improve yield and throughput efficiency, (3) green forging – electric induction furnaces and hydrogen heating systems reducing carbon intensity, and (4) defense-focused forge shops with existing government certifications and long-cycle contract visibility.

Future Market Outlook (2026-2034)

The global metal forging market forecast projects steady and sustained value expansion from USD 95.13 Billion in 2025 to USD 152.95 Billion by 2034 at a CAGR of 5.22%. Asia Pacific will retain and extend regional leadership while North America and Europe sustain premium value growth through aerospace procurement, defense spending, and EV transition-related component upgrades.

Three structural shifts will define the metal forging market through 2034. First, EV lightweighting mandates will fundamentally alter raw material demand, accelerating the shift from carbon and alloy steel toward aluminum and titanium, and requiring forgers to invest in new die technologies, heating systems, and material handling capabilities.

Aerospace fleet expansion, with major manufacturers targeting high annual deliveries through 2030, will sustain long-term demand for certified precision forgings with extended lead times from design freeze to first article inspection. Additionally, digital transformation of forging operations—via automation, IoT monitoring, and AI-driven quality control—will differentiate cost leaders from margin-constrained commodity operators, accelerating mid-tier consolidation.

Manufacturers that strategically invest in material diversification, automation, sustainability compliance, and OEM partnership deepening will be best positioned to capture outsize revenue growth as the global metal forging market transitions through its next decade of structural evolution.

Research Methodology

Primary Research

Primary research involved structured interviews with C-level executives, procurement directors, plant managers, and product engineers at forging manufacturers, automotive OEMs, aerospace prime contractors, and industrial end users. Approximately 180+ primary respondents contributed data to validate segment sizing, growth rates, and competitive positioning assessments presented in this report.

Secondary Research

Secondary research drew on data from national steel and metals associations (World Steel Association, European Steel Association), aerospace industry bodies (IATA, AIA), automotive production databases (IHS Markit, MarkLines), regulatory filings, annual reports, trade publications, and government industrial statistics from China NBS, India MoSPI, U.S. Census Bureau, and Eurostat.

Forecasting Models

Market size forecasting employed a hybrid bottom-up and top-down approach, calibrated against macroeconomic indicators including industrial production indices, automotive production forecasts, aerospace delivery schedules, and infrastructure investment pipelines. Regression-based CAGR modeling was cross-validated against company revenue trajectories and end-use demand elasticity analysis. All forecasts carry a 90% confidence interval validated through triangulation across three independent data streams.

Metal Forging Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Raw Materials Covered | Carbon Steel, Alloy Steel, Aluminum, Magnesium, Stainless Steel, Titanium, Others |

| Applications Covered | Automotive, Aerospace, Oil and Gas, Construction, Agriculture, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bharat Forge, Precision Castparts Corp., Thyssenkrupp AG, Nippon Steel Corporation, Arconic, Larsen & Toubro Limited, ELLWOOD Group Inc, Scot Forge Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the metal forging market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global metal forging market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the metal forging industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Metal Forging Market Report

The global metal forging market size reached USD 95.13 Billion in 2025 and is projected to grow at a CAGR of 5.22% through 2034.

The market is projected to reach USD 152.95 Billion by 2034, driven by automotive, aerospace, and infrastructure demand from 2026 onward.

Asia Pacific leads with 42.3% revenue share in 2025, with China and India as the primary demand centers for forged components.

Growth is fueled by rising aerospace and automotive demand, infrastructure investment, EV lightweighting, and precision forging technology adoption.

Carbon steel dominates with a 38.4% share in 2025, due to its cost-effectiveness and wide applicability across industrial end users.

Aerospace is the fastest-growing application at an estimated ~6.8% CAGR, driven by commercial aviation recovery and defense procurement.

Key players include Bharat Forge, Precision Castparts Corp., Thyssenkrupp AG, Nippon Steel Corporation, Arconic, Larsen & Toubro Limited, ELLWOOD Group Inc, Scot Forge Company.

Aluminum forging is growing at ~6.3% CAGR due to EV lightweighting mandates; it held a 16.3% share of the raw material segment in 2025.

Automotive is the largest application segment at 36.4% share in 2025, with EV transition fueling demand for high-strength, lightweight forgings.

Core challenges include raw material price volatility, high capital investment requirements, skilled workforce shortages, and stringent environmental norms.

North America holds 24.6% of global metal forging revenue in 2025, anchored by U.S. aerospace OEM procurement and defense sector demand.

Automation, IoT-enabled monitoring, precision closed-die forging, and AI-driven quality control are reshaping efficiency and output quality across the industry.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)