Mexico Factoring Market Size, Share, Trends and Forecast by Type, Organization Size, Application, and Region, 2026-2034

Mexico Factoring Market Summary:

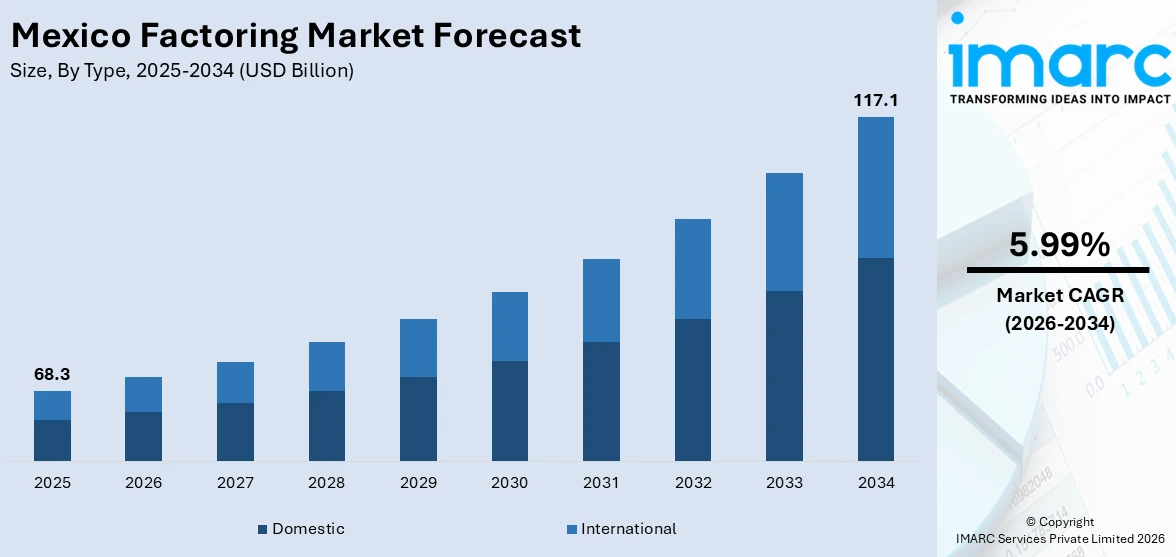

The Mexico factoring market size was valued at USD 68.3 Billion in 2025 and is projected to reach USD 117.1 Billion by 2034, growing at a compound annual growth rate of 5.99% from 2026-2034. The Mexico factoring market is experiencing robust expansion, driven by growing demand for working capital financing among small and medium enterprises, rapid adoption of digital platforms and fintech solutions, and expanding cross-border trade supported by USMCA trade provisions. Increasing awareness of alternative financing mechanisms, supportive regulatory developments, and rising nearshoring-driven manufacturing activity are collectively contributing to greater market penetration and strengthening the Mexico factoring market share.

To get more information on this market Request Sample

Key Takeaways and Insights:

- By Type: Domestic factoring dominates the market with a share of 83.2% in 2025, reflecting strong intra-national trade activity, an established financial intermediary network, and the preference of Mexican enterprises for local currency-denominated receivables financing.

- By Organization Size: Small and medium enterprises lead the market with a share of 72.5% in 2025, driven by the acute need for alternative financing channels given limited access to traditional bank credit and growing working capital requirements.

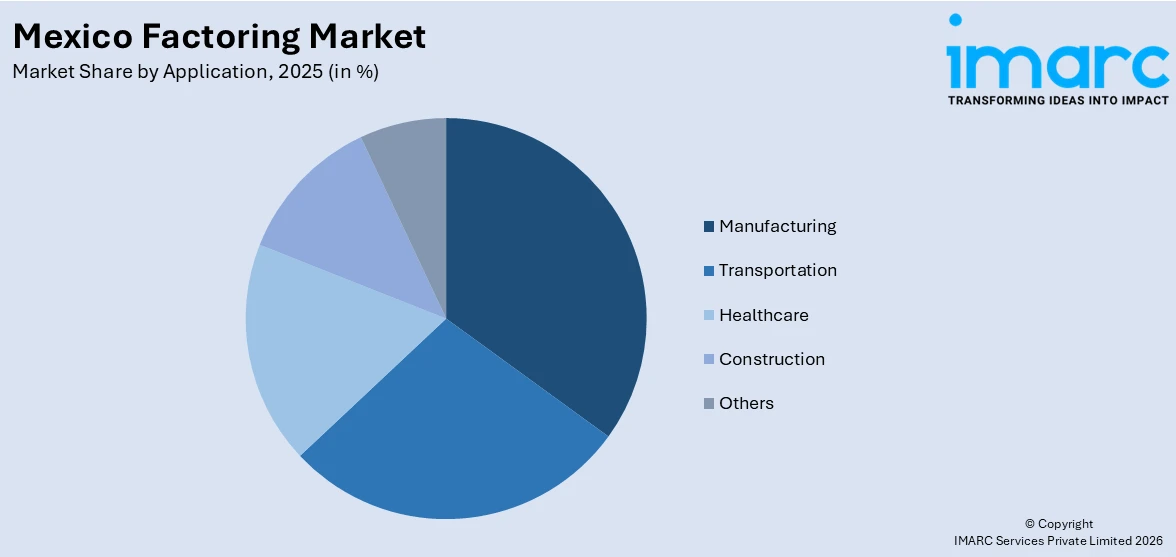

- By Application: Manufacturing prevails the market with a share of 30.5% in 2025, supported by nearshoring investments, expanding industrial activity, and the critical need for liquidity to manage complex and extended supply chains.

- By Region: Central Mexico comprises the largest region with a 52.8% share in 2025, driven by the high concentration of financial institutions, corporate headquarters, and industrial activity in Mexico City and surrounding states.

- Key Players: Key players drive the Mexico factoring market by expanding digital platforms, broadening service portfolios, and strengthening partnerships with financial institutions and fintechs. Their investments in automation, risk assessment technologies, and SME-focused financing programs are advancing market accessibility, boosting operational efficiency, and supporting wider adoption of factoring services across diverse industry sectors.

The Mexico factoring market is advancing robustly as diverse macroeconomic forces and structural improvements redefine access to working capital for enterprises of all sizes across the country. The financial ecosystem is undergoing transformative change, with fintech platforms expanding credit access to previously underserved segments, particularly SMEs operating in manufacturing, construction, and transportation. The surge in nearshoring activity has intensified demand for supply chain finance solutions, as manufacturers require agile liquidity tools to manage growing receivables effectively. Digital invoice verification, AI-powered credit scoring, and cloud-based factoring platforms are reducing approval timelines and broadening geographic reach beyond major metropolitan centers. Supportive regulation and increasing institutional interest from global financial organizations are further strengthening the ecosystem. As awareness continues to rise and digital infrastructure matures, the market is well-positioned for sustained long-term growth.

Mexico Factoring Market Trends:

Rise of Reverse Factoring and Supply Chain Finance

Mexico's factoring market is witnessing rapid expansion of reverse factoring, enabling large buyers to arrange early payments for suppliers through financial intermediaries. This model strengthens supplier relationships and improves financial stability across supply chains, proving particularly beneficial for SMEs with limited credit access. In August 2024, IFC and Citi launched a USD 500 Million facility in Mexico, the inaugural project of a USD 2 Billion global sustainable supply chain finance program, designed to expand SME access to finance and promote resilient, sustainable supplier networks, directly contributing to Mexico factoring market growth.

Digital Transformation and Fintech-Driven Platforms

Digital platforms and fintech solutions are redefining factoring in Mexico by automating invoice verification, credit assessment, and receivables management. AI-driven scoring models and cloud-based systems are reducing processing times and extending market access to underserved businesses beyond major cities. In March 2025, MercadoLibre announced plans to invest USD 3.4 Billion in technology and financial services in Mexico, accelerating the development of digital platforms that streamline receivables management and support a broader shift toward automated, AI-driven factoring and credit solutions for businesses across the country.

Growing SME Adoption Amid Financial Inclusion Push

Mexico's large underfinanced SME segment is increasingly turning to factoring as a viable working capital solution, as traditional banks serve only a fraction of the market. Fintech-backed factoring platforms are filling the financing gap with agile, technology-enabled services. According to the Asociación de Sociedades Financieras de Objeto Múltiple en México, 46.6% of SMEs have resorted to factoring due to lack of access to bank financing. Mexico surpassed 800 domestic fintech companies in 2024, with revenues growing by 31% year-on-year, reflecting strong infrastructure growth that is directly expanding factoring accessibility nationwide.

Market Outlook 2026-2034:

The Mexico factoring market is poised for sustained expansion throughout the forecast period, supported by the convergence of structural economic forces, digital innovation, and shifting enterprise financing preferences. As SMEs continue to seek agile alternatives to traditional banking credit, factoring services are expected to deepen their penetration across manufacturing, transportation, healthcare, and construction sectors. The ongoing nearshoring boom, underpinned by favorable USMCA trade provisions and Mexico's proximity to the United States market, is creating a steady pipeline of new manufacturing enterprises with growing receivables and limited credit access. Accelerating digitalization—encompassing AI-based credit scoring, automated invoice processing, and cloud-based receivables management—is lowering operational costs for factoring providers while shortening onboarding timelines for clients. Regulatory frameworks are evolving to accommodate e-invoice financing and new forms of supply chain finance, further legitimizing the market. With financial inclusion expanding and institutional investment rising, Mexico's factoring market is firmly positioned to deliver robust long-term returns. The market generated a revenue of USD 68.3 Billion in 2025 and is projected to reach a revenue of USD 117.1 Billion by 2034, growing at a compound annual growth rate of 5.99% from 2026-2034.

Mexico Factoring Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Domestic |

83.2% |

|

Organization Size |

Small and Medium Enterprises |

72.5% |

|

Application |

Manufacturing |

30.5% |

|

Region |

Central Mexico |

52.8% |

Type Insights:

- International

- Domestic

Domestic factoring dominates the market with a share of 83.2% of the total Mexico factoring market in 2025.

Domestic factoring commands the overwhelming majority of Mexico's factoring market, reflecting the depth and scale of intra-national trade activity and the entrenched preference of Mexican businesses for financing solutions denominated in local currency. The domestic segment benefits from a well-established network of financial intermediaries, including banks, multi-purpose financial companies, and fintech platforms specializing in the processing and discounting of domestic invoices. Businesses engaged in manufacturing, retail, and services routinely utilize domestic factoring to bridge the gap between invoice issuance and payment receipt, enabling them to maintain operational continuity and fund working capital requirements without resorting to traditional bank credit facilities.

The dominance of the domestic segment is further underpinned by Mexico's expanding e-invoicing infrastructure, which mandates digital invoice issuance for a broad range of commercial transactions. This regulatory requirement has dramatically increased the volume of verifiable and standardized invoices, lowering risk and administrative burden for factoring providers. As digital platforms become more adept at processing domestic invoices using automated tools and AI-powered credit scoring, the efficiency and accessibility of domestic factoring services continue to improve. Industries ranging from construction and transportation to healthcare and light manufacturing are increasingly integrating domestic factoring into their treasury management strategies, further consolidating the segment's leadership position.

Organization Size Insights:

- Small and Medium Enterprises

- Large Enterprises

Small and medium enterprises lead the market with a share of 72.5% of the total mexico factoring market in 2025.

Small and medium enterprises constitute the primary user base of factoring services in Mexico, driven by the structural challenges they face in accessing formal credit from traditional banking institutions. Unlike large corporations with established credit histories and collateral assets, SMEs frequently encounter financing gaps that disrupt cash flow and constrain growth. Factoring provides these businesses with a practical solution by converting outstanding receivables into immediate working capital, enabling them to meet payroll obligations, fund inventory replenishment, and invest in operational improvements without the delays and complexity of conventional loan applications. The fintech revolution in Mexico has been particularly transformative for this segment, with digital platforms dramatically reducing onboarding times and minimum invoice requirements.

Mexico's SME sector is experiencing a parallel trend of increasing formalization, driven by mandatory e-invoicing and expanded digital payment infrastructure. As more SMEs issue standardized electronic invoices, their receivables portfolios become more transparent and easier to assess for factoring providers, reducing transaction costs and enabling greater risk segmentation. The government's continued focus on financial inclusion, supported by fintech-friendly regulatory frameworks and international development programs, is expected to deepen SME penetration in the factoring market over the forecast period. Platforms that combine factoring with additional financial management tools, such as cash flow analytics and payroll integration, are gaining traction among SME clients seeking holistic financial solutions.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Transportation

- Healthcare

- Construction

- Manufacturing

- Others

Manufacturing exhibits a clear dominance with a 30.5% share of the total Mexico factoring market in 2025.

Manufacturing represents the largest application segment in Mexico's factoring market, underpinned by the sector's capital intensity, extended payment cycles, and the need for consistent working capital to sustain production operations. Manufacturers typically deal with large corporate buyers and government entities that impose lengthy payment terms, creating substantial receivables that tie up cash for extended periods. Factoring allows manufacturers to convert these outstanding invoices into immediate liquidity, enabling them to procure raw materials, service equipment, and meet labor costs without disruption. Mexico's position as a nearshoring hub for automotive, electronics, aerospace, and consumer goods production has significantly expanded the pool of manufacturers seeking factoring solutions.

The manufacturing sector's continued integration into North American supply chains, driven by USMCA trade provisions and sustained foreign direct investment, is creating a sustained pipeline of enterprises with growing receivables and limited credit access. Suppliers in tiered manufacturing ecosystems, particularly mid-tier and lower-tier companies providing components to large assembly operations, are among the most active users of factoring services. Reverse factoring programs sponsored by large original equipment manufacturers and international development institutions are further embedding factoring within manufacturing value chains. As Mexico's industrial base diversifies into advanced technology sectors, the demand for sophisticated receivables financing is expected to expand substantially within this segment.

Regional Insights:

- Northern Mexico

- Central Mexico

- Southern Mexico

- Others

Central Mexico represents the leading segment with a 52.8% share of the total Mexico factoring market in 2025.

Central Mexico's commanding position in the factoring market is driven by its status as the country's preeminent economic, financial, and commercial hub. Mexico City and surrounding states host the highest concentration of financial institutions, corporate headquarters, and business services firms, creating a dense and active receivables ecosystem. Sophisticated financial infrastructure, widespread digital payment adoption, and high commercial transaction volumes collectively support the region's dominance across diverse factoring applications and industry sectors.

The region also benefits from significant industrial activity in surrounding states such as Estado de México, Querétaro, and Guanajuato, which generate substantial receivables through complex supply chains. Proximity to federal regulatory bodies and financial oversight institutions facilitates compliance and access to institutional financing programs. The ongoing expansion of fintech platforms and e-commerce logistics infrastructure within the Central Mexico region is further stimulating demand for agile, digitally enabled factoring services.

Market Dynamics:

Growth Drivers:

Why is the Mexico Factoring Market Growing?

Expanding SME Base and Working Capital Demand

Mexico's vast SME landscape is the primary engine of factoring demand, as millions of businesses face persistent cash flow constraints due to extended payment cycles and limited bank credit access. Small and medium enterprises represent the economic backbone of the country, contributing significantly to employment and output, yet many operate outside formal financial networks. Factoring provides an immediate, collateral-free liquidity mechanism that directly addresses the working capital gap experienced during periods of high receivables. The growing formalization of Mexico's economy, supported by e-invoicing mandates and digital record-keeping requirements, is enabling factoring providers to more accurately assess the creditworthiness of smaller clients, reducing risk and lowering borrowing costs. This expanding formal invoice base creates fertile conditions for factoring growth. In September 2024, MercadoLibre's fintech arm, Mercado Pago, secured a USD 250 Million financing arrangement with JPMorgan to enhance its credit offerings in Mexico, enabling expanded financing for SMEs and individuals and demonstrating strong institutional commitment to financing Mexico's underserved enterprise segment.

Nearshoring-Driven Manufacturing Expansion

Mexico's emergence as a premier nearshoring destination for global manufacturers has generated significant demand for factoring services within the manufacturing sector. The relocation of production activities closer to North American consumer markets, driven by supply chain disruptions, rising Asia-Pacific trade costs, and the competitive advantages of USMCA, has created a large new cohort of manufacturers with extensive receivables and limited credit access. These enterprises, particularly mid-tier suppliers, require agile factoring solutions to maintain operational cash flow between production and payment receipt. The sustained momentum of nearshoring across automotive, electronics, and aerospace sectors is continuously expanding the pool of manufacturers engaged in complex, multi-tiered supply chains, driving heightened demand for factoring and supply chain finance services. As Mexico solidifies its position as a critical link in North American production networks, the need for efficient receivables financing instruments is expected to deepen considerably across diverse industrial corridors and supplier ecosystems throughout the forecast period.

Regulatory Support and Digital Financial Infrastructure

Mexico's regulatory evolution is creating a more enabling environment for factoring and supply chain finance. E-invoicing requirements, open banking frameworks, and the legal strengthening of accounts receivable financing are reducing transactional risk and increasing transparency across the market. Regulatory bodies are implementing enhanced internal control frameworks and improved fraud prevention measures that build confidence in financial transactions, encouraging broader participation from both traditional institutions and fintech providers. Mexico's expanding digital payments ecosystem provides a robust backbone supporting faster settlement, automated reconciliation, and more efficient invoice discounting for factoring providers across the country. As regulatory clarity continues to improve and digital financial infrastructure matures, factoring companies are better positioned to scale operations, onboard new clients efficiently, and offer more competitive pricing, collectively reinforcing the market's long-term growth trajectory throughout the forecast period

Market Restraints:

What Challenges the Mexico Factoring Market is Facing?

Limited Market Awareness Among Small Enterprises

Despite the growth of factoring, awareness remains limited among a large segment of Mexican businesses, particularly in rural and informal sectors. Encuesta Nacional de Financiamiento de las Empresas data indicates that only a small percentage of companies actively use factoring, with the majority unfamiliar with the financial instrument. This informational gap suppresses demand and prevents many eligible SMEs from benefiting from factoring, hindering the broader development of the market and slowing financial inclusion efforts across underserved regions and industry segments.

Regulatory Complexity and Compliance Burdens

The evolving regulatory landscape for factoring in Mexico introduces compliance requirements that can burden both providers and clients. Obligations such as Know Your Customer protocols, anti-money laundering procedures, and tax compliance add administrative costs and slow onboarding processes. For smaller factoring providers, meeting these requirements demands significant investment in compliance infrastructure and legal expertise. These burdens constrain operational agility, limit provider scalability, and can discourage new entrants, ultimately restricting market expansion and competitive diversity within the industry.

Credit Risk and Concentration in Traditional Sectors

The concentration of factoring activity in limited sectors and geographies introduces credit concentration risks for providers. Factoring companies operating primarily within manufacturing or large buyer ecosystems are exposed to sector-specific downturns, delayed payments from large corporates, and the financial vulnerabilities of SME clients. Managing default risk without robust credit scoring infrastructure remains challenging for smaller institutions, limiting their capacity to expand portfolios, serve higher-risk clients, and scale operations across new industry verticals and geographic regions.

Competitive Landscape:

The Mexico factoring market features a diverse mix of commercial banks, non-banking financial companies, and rapidly growing fintech platforms competing for market share. Established financial institutions leverage their balance sheet strength, regulatory credibility, and established client relationships, while fintech providers differentiate through technology-driven onboarding, digital processing, and agile credit assessment models. Competition is intensifying as global institutions enter the market through supply chain finance programs. Service innovation, digital platform investment, and expanding SME-focused offerings are the primary competitive differentiators shaping market dynamics.

Mexico Factoring Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | International, Domestic |

| Organization Sizes Covered | Small and Medium Enterprises, Large Enterprises |

| Applications Covered | Transportation, Healthcare, Construction, Manufacturing, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Mexico Factoring Market Report

The Mexico factoring market size was valued at USD 68.3 Billion in 2025.

The Mexico factoring market is expected to grow at a compound annual growth rate of 5.99% from 2026-2034 to reach USD 117.1 Billion by 2034.

Domestic factoring dominated the market with a share of 83.2%, reflecting strong intra-national trade activity, an established financial intermediary network, and the prevalent preference of Mexican enterprises for local currency-denominated receivables financing instruments.

Key factors driving the Mexico factoring market include growing SME demand for working capital, nearshoring-driven manufacturing expansion, rapid fintech and digital platform adoption, expanding e-invoicing infrastructure, supportive regulatory frameworks, and rising institutional investment in supply chain finance solutions.

Major challenges include limited market awareness among SMEs, regulatory complexity and compliance burdens, credit risk concentration in traditional sectors, insufficient financial literacy, and barriers to digital adoption among smaller enterprises operating in informal or rural segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)