Mexico Portable Power Tools Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

Mexico Portable Power Tools Market Size, Share, Trends & Forecast (2026-2034)

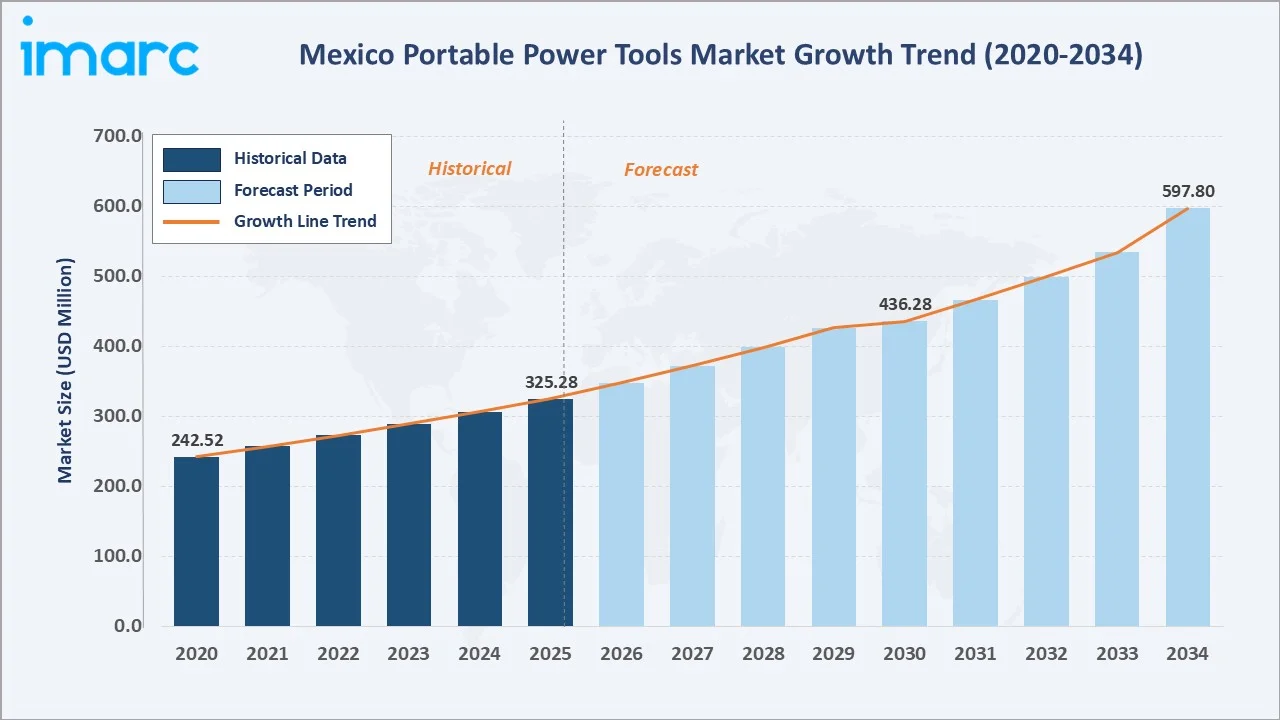

The Mexico portable power tools market reached USD 325.28 Million in 2025 and is projected to reach USD 597.80 Million by 2034, growing at a CAGR of 6.05% during 2026-2034. Robust construction activity, automotive sector expansion, nearshoring-driven industrial investment, and the accelerating shift toward cordless lithium-ion battery-powered tools are the primary growth drivers of the Mexico portable power tools market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 325.28 Million |

|

Forecast Market Size (2034) |

USD 597.80 Million |

|

CAGR (2026-2034) |

6.05% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Central Mexico – 46.3% share (2025) |

|

Fastest Growing Region |

Northern Mexico |

To get more information on this market, Request Sample

Central Mexico dominates, holding a 46.3% share in 2025, anchored by Mexico City's dense urban construction activity and the industrial belt of the Bajío corridor spanning Guanajuato, Querétaro, and Aguascalientes. Cordless tools account for 64.2% of the product segment owing to breakthroughs in lithium-ion battery technology and growing preference across both professional contractors and DIY consumers.

With applications spanning construction, automotive, industrial manufacturing, and consumer DIY, the market is expected to expand sustainably through 2034, supported by robust infrastructure pipelines, favorable demographics, and accelerating adoption of smart, IoT-integrated tools across commercial segments.

Executive Summary

Mexico portable power tools market is on a sustained growth trajectory, driven by construction sector expansion, nearshoring-driven industrial investment, and the accelerating transition to cordless battery-powered tools. The market reached USD 325.28 Million in 2025 and is forecast to reach USD 597.80 Million by 2034, reflecting a CAGR of 6.05% over the forecast period.

Central Mexico leads geographically with 46.3% of the 2025 national market, anchored by Mexico City's construction ecosystem and the Bajío industrial corridor. Northern Mexico is the fastest-growing cluster, gaining momentum from automotive cluster expansion and rapid establishment of nearshoring manufacturing parks in Nuevo León, Chihuahua, and Coahuila.

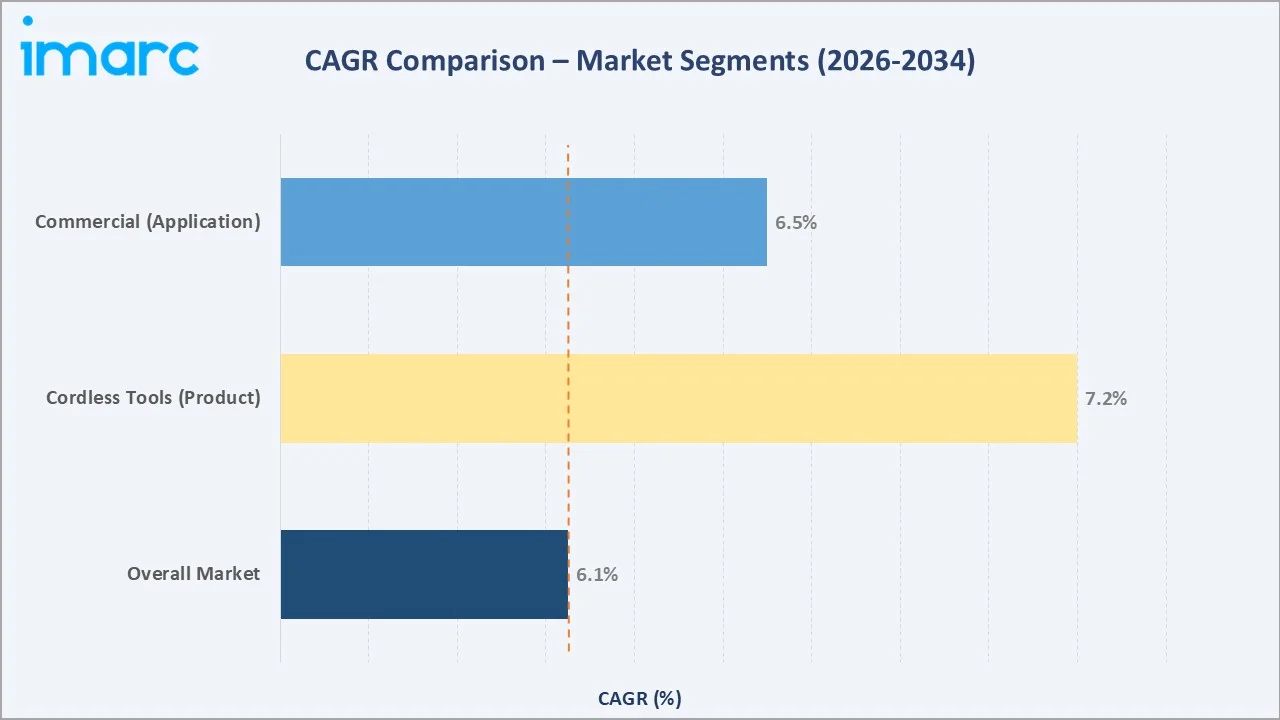

Cordless tools dominate the product segment at 64.2%, supported by brushless motor advances and expanding multi-voltage battery platforms that reduce total tool ownership costs. Commercial applications lead with 57.6% of the 2025 market, fueled by contractor activity, automotive manufacturing, and energy infrastructure projects. The consumer segment at 42.4% is expanding through e-commerce channels and a growing DIY culture.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product) |

Cordless Tools – 64.2% share (2025) |

|

Largest Segment (Application) |

Commercial – 57.6% share (2025) |

|

Leading Region |

Central Mexico – 46.3% revenue share (2025) |

|

Fastest Growing Region |

Northern Mexico (nearshoring + automotive growth) |

|

Top Companies |

Stanley Black & Decker, Inc., Robert Bosch GmbH, Makita Corporation, Techtronic Industries Co. Ltd., and Hilti Corporation |

|

Market Opportunity |

Cordless segment projected to exceed USD 380 Million by 2034 on Li-ion battery advances. |

Key Analytical Observations Supporting The Above Data:

- Cordless Tools account for 64.2% of the Mexico portable power tools market in 2025, preferred across construction, automotive repair, and DIY applications for superior portability and rapidly improving battery performance.

- Commercial is the dominant application at 57.6% (2025), fueled by contractor activity, nearshoring industrial construction, and automotive assembly and maintenance demand across Mexico's key manufacturing states.

- Central Mexico holds 46.3% of the national market in 2025, driven by construction activity in the Mexico City metropolitan area and the manufacturing density of the Bajío economic corridor.

- Northern Mexico is the fastest-growing regional market, driven by automotive cluster expansion and rapid buildout of manufacturing facilities in Nuevo León, Chihuahua, and Coahuila.

- Adoption of IoT-integrated smart power tools with predictive maintenance and Bluetooth connectivity is gaining traction in Mexico's industrial sector, representing an emerging premium growth segment through 2034.

Mexico Portable Power Tools Market Overview

Portable power tools are electrically or battery-operated devices engineered to perform drilling, fastening, sawing, cutting, grinding, and material-removal tasks with far greater efficiency than manual alternatives. Originally developed for industrial use, their application has expanded to encompass residential DIY, automotive repair, commercial construction, and light manufacturing.

Macroeconomic factors, including Mexico's construction pipeline, automotive sector output, nearshoring-driven foreign direct investment, and rising consumer spending on home improvement, are the primary growth catalysts of the Mexico portable power tools market forecast. Mexico's strategic position as a key manufacturing hub under USMCA, combined with strong demographic fundamentals and rapid e-commerce expansion, positions it as Latin America's most dynamic portable power tools market.

Market Dynamics

To evaluate market opportunities, Request Sample

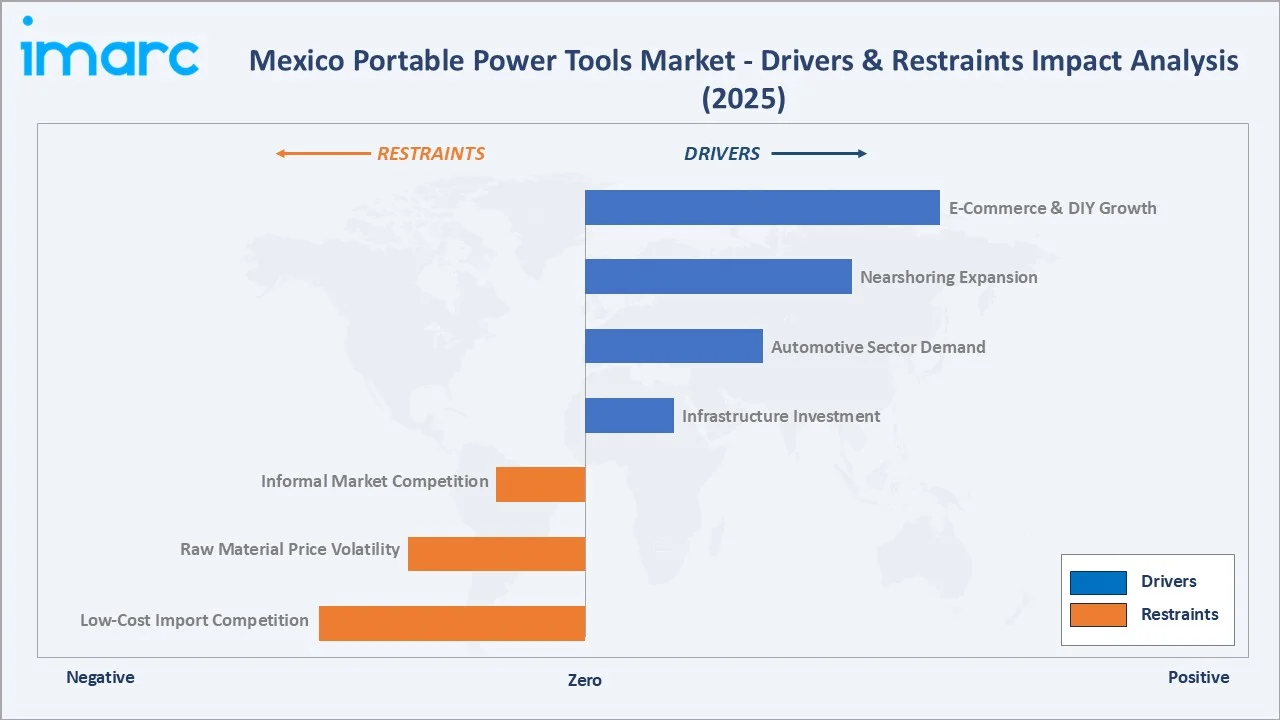

Market Drivers

- Infrastructure Investment: Mexico's government allocated approximately USD 22.3 Billion in 2025 toward 51 energy and infrastructure projects by 2030 under CFE, generating sustained demand for high-performance portable power tools across civil construction and electrical installation.

- Automotive Sector Demand: In December 2025, Mexico's light vehicle production totaled 243,961 units, reflecting an 8.45% annual growth, or 19,018 more vehicles than in December 2024. Automotive OEMs and aftermarket repair centers are intensive consumers of precision fastening, drilling, and impact tools.

- Nearshoring Expansion: The nearshoring wave has accelerated new factory establishment across northern and central Mexico, driving tool demand across construction, fit-out, and ongoing equipment maintenance phases of every new facility.

- E-Commerce and DIY Culture Growth: Mexico's e-commerce market is projected to reach USD 70.4 billion by 2027, driven by better connectivity, improved financial inclusion, optimized logistics, and growing digital literacy. It is expected to facilitate consumer-grade tool purchasing and accelerate the DIY segment's expansion into Tier-2 and Tier-3 cities.

These drivers reinforce a self-sustaining growth cycle, infrastructure spending drives commercial tool demand, which stimulates local distribution investment, which in turn broadens consumer market accessibility across Mexico.

Market Restraints

- Low-Cost Import Competition: Price-sensitive consumer segments face competition from Chinese-manufactured low-cost tools that undercut established brand pricing, constraining premium brand penetration in regional and rural markets.

- Raw Material and Battery Cost Volatility: Lithium carbonate and copper price fluctuations directly impact cordless tool manufacturing costs, creating periodic retail price instability and margin compression across the supply chain.

- Informal Market Competition: The Mexico portable power tools market faces significant competition from the informal market, where unbranded or low-cost counterfeit products are sold at a fraction of the price of established brands.

Market Opportunities

- Smart Tool Integration: IoT-embedded power tools with Bluetooth connectivity, real-time performance monitoring, and anti-theft geolocation are gaining traction in Mexico's professional segment, commanding premium price points and growing at approximately 18% CAGR through 2034.

- Tier-2 and Tier-3 City Expansion: Secondary cities, including San Luis Potosí, Querétaro, and Mérida, are experiencing accelerating construction and residential development, representing significant incremental distribution opportunities for both professional and consumer tool segments.

Market Challenges

- Informal Market Competition: A significant informal-channel market, supplied through grey-market imports and unbranded tools, captures substantial consumer-segment volume in price-sensitive regions, limiting formal market revenue measurement and brand loyalty development.

- After-Sales Service Network Gaps: Extending certified service infrastructure into southern Mexico and rural areas remains challenging for global brands, creating warranty and support gaps that reduce purchase confidence in lower-penetration regions.

Emerging Market Trends

1. Accelerating Transition from Corded to Cordless Tools

Brushless motor technology has accelerated adoption by delivering 20–30% greater energy efficiency and significantly longer motor lifespans. In Mexico's automotive assembly plants in Nuevo León and Sonora, major OEMs have mandated the transition to cordless fastening tools for ergonomic and safety compliance. The cordless tools segment is projected to grow at approximately 7.2% CAGR through 2034.

2. Rise of Smart and IoT-Integrated Power Tools

In Mexico's nearshoring industrial parks in Coahuila and Querétaro, multinational manufacturers are specifying smart tool compliance as part of factory operational standards. Smart power tool adoption among industrial professionals in Latin America grew approximately 28% year-on-year in 2024, with Mexico representing the region's largest share of uptake.

3. E-Commerce and Omnichannel Distribution Expansion

Platforms such as MercadoLibre, Amazon Mexico, and brand-direct online stores are becoming primary purchase channels, accounting for a growing share of overall market volume. Manufacturers are responding by investing in omnichannel strategies combining online product listings, virtual demonstrations, and same-day delivery supported by urban micro-warehouses.

4. Ergonomics, Safety Innovation, and Regulatory Compliance

Tool manufacturers are increasingly prioritizing ergonomic design features, reduced vibration, anti-kickback mechanisms, and lightweight composite housings in response to growing occupational health awareness among Mexican contractors. NOM (Norma Oficial Mexicana) safety standards for power tools are evolving, raising entry barriers for lower-quality imports and consolidating market share toward established brands.

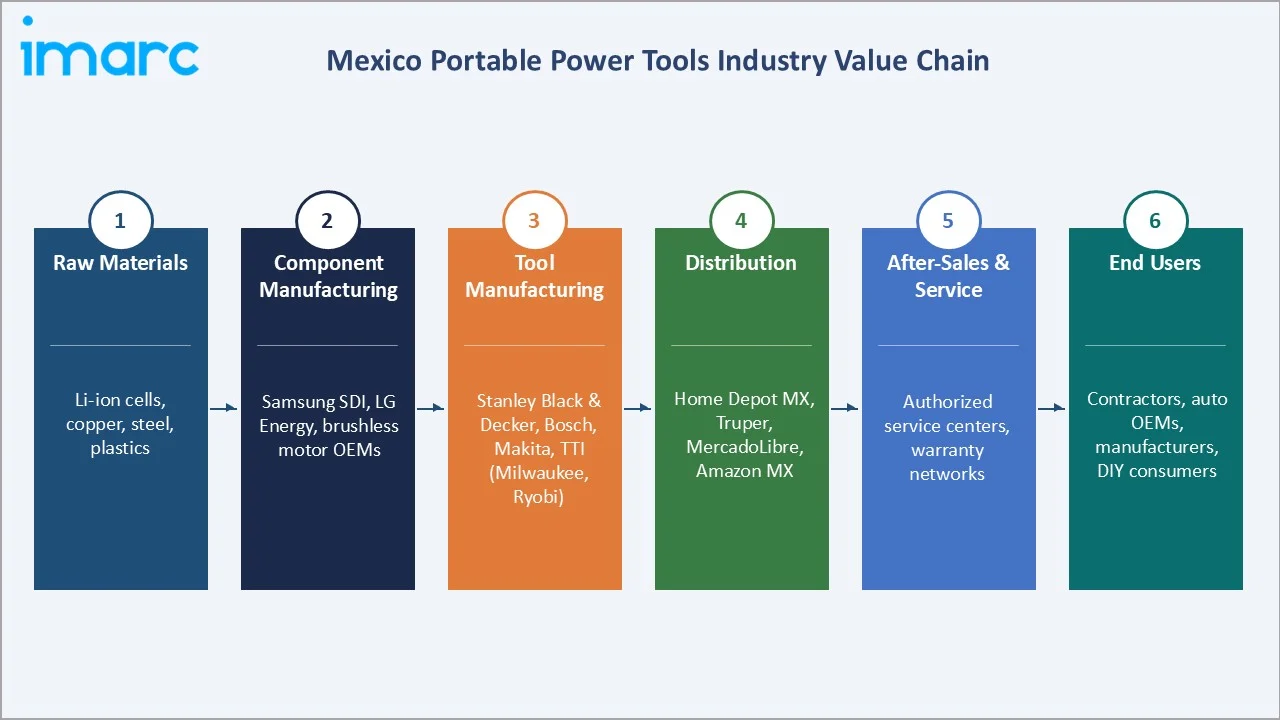

Industry Value Chain Analysis

The Mexico portable power tools value chain spans raw material supply through end-user deployment, with each stage contributing to the final product's performance, cost, and availability.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Lithium carbonate, copper, steel, and engineering-grade plastics from global commodity markets |

|

Component Manufacturing |

Li-ion cell producers (Samsung SDI, LG Energy Solution, CATL); brushless motor OEMs |

|

Tool Manufacturing |

Stanley Black & Decker, Inc., Robert Bosch GmbH, Makita Corporation, Techtronic Industries Co., Ltd., and Hilti Corporation. |

|

Distribution |

Authorized distributors, hardware retail chains (Home Depot Mexico), e-commerce (MercadoLibre, Amazon Mexico) |

|

After-Sales & Service |

Authorized service centres, manufacturer warranty networks, and independent repair shops |

|

End Users |

Construction contractors, automotive OEMs and repair shops, industrial manufacturers, and DIY consumers |

Technology Landscape in Mexico Portable Power Tools Industry

Brushless Motor Technology

Brushless motors, which eliminate mechanical brushes in favor of electronic commutation, have become the defining technology differentiator in the portable power tools sector. In Mexico's commercial segment, brushless tools are now the default specification for professional contractors due to 50–70% longer motor life, lower heat generation, and higher torque-to-weight ratios.

Lithium-Ion Battery Advances

Advances in lithium-ion cell chemistry, including higher energy-density NMC and LFP formulations, are steadily increasing cordless tool runtime and reducing charge times. Mexico's cordless market has benefited from declining battery pack costs, which fell approximately 15-20% between 2022 and 2025. Multi-ampere-hour platforms (5Ah, 8Ah, and 12Ah) are expanding the range of heavy-duty applications addressable without corded alternatives.

Smart Tool Integration

Global tool manufacturers have introduced connected ecosystems with companion mobile applications enabling fleet managers to monitor tool status, schedule maintenance, and verify compliance across multiple project sites. In Mexico's expanding nearshoring industrial parks, smart tool adoption is accelerating as multinational tenants import their global operational standards.

Ergonomics and Safety Innovation

Ergonomic innovation, including vibration-dampening handle systems, one-handed operation features, and automatic kickback brakes, is becoming a key competitive differentiator in Mexico's professional segment. Anti-vibration technology reduces occupational health risks associated with hand-arm vibration syndrome (HAVS), gaining regulatory attention in Mexico's industrial workforce management frameworks.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Cordless Tools |

64.2% |

2025 |

|

Application |

Commercial |

57.6% |

2025 |

|

Region |

Central Mexico |

46.3% |

2025 |

By Product

To access detailed market analysis, Request Sample

Cordless Tools dominate the Mexico portable power tools market with a 64.2% share in 2025. This dominance reflects the sweeping adoption of lithium-ion battery technology across professional and consumer applications, driven by steadily improving performance parity with corded alternatives. Multi-voltage battery ecosystems, where a single battery platform powers drills, saws, grinders, and impact drivers, have become a key purchase driver for commercial contractors seeking operational efficiency.

Corded Tools retain a 35.8% share, valued at approximately USD 116.5 Million, favored in high-duty-cycle applications such as concrete grinding, rebar cutting, and heavy timber sawing, where continuous power without battery replacement is essential. In Mexico's large-scale infrastructure and industrial construction projects, corded angle grinders and rotary hammers remain indispensable.

By Application

Commercial applications lead the Mexico portable power tools market with a 57.6% share in 2025. This dominance is underpinned by pervasive tool use across construction, automotive manufacturing, nearshoring industrial facilities, and energy infrastructure projects. In 2024, Mexico's automotive industry manufactured 3.99 million light vehicles, marking a 5.6% annual increase, which drives persistent, high-volume demand for precision fastening, drilling, and impact tools.

The consumer segment commands 42.4% of the market, expanding rapidly on the back of growing internet and smartphone penetration (61.5% of the population as of 2024), a rising urban middle class, and increased DIY media content across social platforms. Mexico's e-commerce market is projected to reach USD 70.4 billion by 2027, and has substantially reduced barriers to consumer tool purchasing, particularly for entry-level and mid-range cordless tool sets available through MercadoLibre and Amazon Mexico.

Regional Market Insights

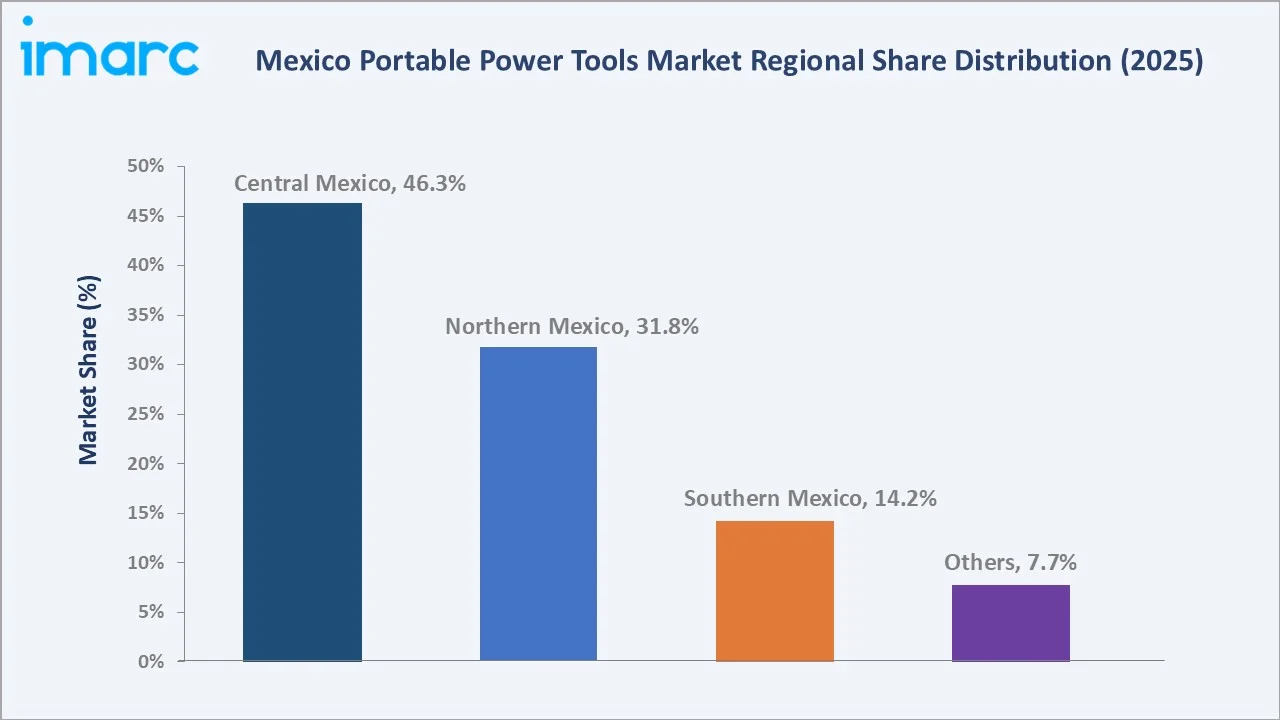

Central Mexico's market leadership (46.3%, 2025) reflects decades of industrial and construction activity concentrated in and around Mexico City, the State of Mexico, and the Bajío corridor. The region hosts the highest density of construction contractors, commercial builders, and light manufacturing SMEs in the country, all of which are intensive consumers of portable power tools.

|

Region |

Share (2025) |

Key Growth Drivers |

Key Industries |

Growth Outlook |

|

Central Mexico |

46.3% |

Urban construction, industrial corridors, Bajío manufacturing |

Construction, manufacturing, commercial services |

Stable, high volume |

|

Northern Mexico |

31.8% |

Automotive clusters, nearshoring parks, border trade |

Automotive, aerospace, electronics |

Fastest growing |

|

Southern Mexico |

14.2% |

Tren Maya, Dos Bocas refinery, tourism resort construction |

Tourism, energy, and public infrastructure |

Emerging growth |

|

Others |

7.7% |

Agricultural processing, regional residential construction |

Agriculture, regional commerce |

Steady, low base |

Northern Mexico, representing 31.8% of the 2025 national market, is the highest-growth regional cluster. The region encompasses key automotive production states, Nuevo León, Chihuahua, Coahuila, and Sonora, and the nearshoring investment wave is driving rapid buildout of industrial parks, warehousing, and supporting infrastructure, each requiring extensive portable power tool deployment during construction and fit-out phases.

Competitive Landscape

Mexico portable power tools market exhibits a moderately concentrated competitive structure. The top five global manufacturers, Stanley Black & Decker, Inc., Robert Bosch GmbH, Makita Corporation, Techtronic Industries Co. Ltd., and Hilti Corporation, collectively hold an estimated 55–65% of the formal market revenue in 2025. Regional importers, private-label distributors, and informal-channel operators account for the balance, particularly in consumer and mid-market segments.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Stanley Black & Decker, Inc. |

DEWALT, Stanley, Black+Decker |

Market Leader |

Widest portfolio; dominant DeWalt contractor brand; strong retail presence across Home Depot Mexico |

|

Robert Bosch GmbH |

Bosch Professional, Bosch DIY |

Market Leader |

Engineering precision; market-leading SDS rotary hammer systems; strong commercial penetration |

|

Makita Corporation |

Makita |

Strong Challenger |

Industry-leading LXT cordless battery platform; strongly favored by professional contractors |

|

Techtronic Industries Co. Ltd. |

Milwaukee, Ryobi, AEG |

Strong Challenger |

Milwaukee's professional dominance; Ryobi's consumer segment leadership via e-commerce channels |

|

Hilti Corporation |

Hilti |

Niche Leader |

Premium professional-grade tools; fleet management services; construction and industrial focus |

Key Company Profiles

Stanley Black & Decker, Inc.

Stanley Black & Decker, headquartered in New Britain, Connecticut, USA, is the world's largest tool and storage company. Its DeWalt brand is the dominant professional-grade portable power tool brand in Mexico, distributed through Home Depot Mexico, authorized distributors, and e-commerce channels.

- Product Portfolio: DeWalt 20V MAX and FLEXVOLT cordless platforms; Stanley FatMax hand tools; Black+Decker consumer cordless tools.

- Recent Developments: In November 2025, Stanley Black & Decker announced the move of production of its cordless products from China to Mexico.

- Strategic Focus: Professional contractor segment leadership; battery platform ecosystem expansion; Latin America distribution network investment.

Robert Bosch GmbH

Robert Bosch GmbH, headquartered in Gerlingen, Germany, operates the Bosch Professional and Bosch DIY brands across Mexico. Bosch's SDS-plus and SDS-max rotary hammer systems are among the most specified tools in Mexico's construction sector.

- Product Portfolio: Bosch Professional 18V cordless systems; SDS-plus and SDS-max rotary hammers; angle grinders and jigsaws.

- Recent Developments: In April 2025, Bosch Power Tools introduced the Bulldog Xtreme8 SDS-plus concrete drill bit with 8-cutter technology, delivering extended service life in rebar-intensive concrete — highly relevant to Mexico's infrastructure projects.

- Strategic Focus: Premium professional segment expansion; connectivity and smart tool ecosystem development; service network investment in Mexico.

Makita Corporation

Makita Corporation, headquartered in Anjo, Japan, is recognized for its LXT 18V and 40V MAX XGT battery platforms. The company has a strong presence in Mexico's professional contractor segment, particularly in construction, woodworking, and automotive service.

- Product Portfolio: 18V LXT and 40V MAX XGT cordless platforms; angle grinders, circular saws, rotary hammers, and multi-tools.

- Recent Developments: Makita expanded its 40V max XGT availability in Latin America in 2025, targeting heavy-duty professional applications in construction and infrastructure.

- Strategic Focus: High-performance cordless platform leadership; professional contractor loyalty programs; Latin America distribution expansion.

Techtronic Industries Co. Ltd.

Techtronic Industries, headquartered in Hong Kong, operates the Milwaukee Tool, Ryobi, and AEG brands. Milwaukee Tool's M18 FUEL platform has achieved significant penetration among professional contractors in Mexico's industrial and construction sectors.

- Product Portfolio: Milwaukee M18 FUEL professional platform; Ryobi ONE+ consumer 18V system; AEG commercial tools.

- Recent Developments: Milwaukee Tools inaugurated a new USD 83 million factory in Torreón, Mexico.

- Strategic Focus: Milwaukee professional dominance; Ryobi consumer e-commerce growth; service infrastructure investment across key Mexican cities.

Market Concentration Analysis

Mexico's portable power tools market exhibits moderate-to-high concentration at the formal branded segment level, with the top five players accounting for an estimated 55–65% of formal market revenue in 2025. A significant informal market segment, supplied through grey-market imports and unbranded Chinese-manufactured tools, captures additional volume in consumer and small contractor segments, particularly outside major urban centers.

Consolidation activity is driven by the need for extensive after-sales service networks, brand-certified contractor training programs, and compliance with evolving NOM safety standards that create barriers to entry for smaller operators. Mid-tier competitors face growing pressure to maintain competitive battery platform ecosystems, further concentrating market share toward established global brands with sufficient R&D investment capacity.

Investment & Growth Opportunities

Fastest Growing Segments

Cordless tools (est. ~7.2% CAGR), smart and IoT-connected tools (~18% niche CAGR), and professional-grade multi-tool kits (~9% CAGR) represent the highest-growth investment vectors through 2034. Together, these niches address a total addressable incremental opportunity of approximately USD 200 Million by 2034.

Emerging Market Expansion

Southern Mexico and the Pacific Coast corridor represent significant incremental growth opportunities, underpinned by Tren Maya-associated construction, tourism resort development, and improving distribution infrastructure. Entry via joint ventures with local hardware distributors and alignment with federal infrastructure procurement channels are the preferred market-entry strategies.

Venture and Institutional Investment Trends

- Investment themes include lithium-ion battery assembly localization in Mexico, brushless motor manufacturing partnerships, and development of Mexico-specific tool-leasing models for small contractors unable to invest in full tool fleets outright.

- E-commerce and digital retail investment represents a key growth lever, with MercadoLibre and Amazon Mexico providing scalable distribution reach across all 32 Mexican states without the fixed cost of physical retail network expansion.

- Nearshoring-aligned positioning — serving the multinational manufacturers establishing facilities in northern Mexico — represents an institutional B2B growth opportunity requiring investment in fleet management services, calibration support, and enterprise purchasing agreements.

Future Market Outlook (2026-2034)

The Mexico portable power tools market is forecast to reach USD 597.80 Million by 2034 at a CAGR of 6.05%, representing one of Latin America's most dynamic industrial tool markets. The market is expected to evolve from a volume-driven growth phase toward value-driven premium segment expansion, supported by smart tool adoption, battery platform ecosystem lock-in, and growing after-sales service revenues.

Structural growth catalysts, construction pipeline execution, automotive sector resilience, nearshoring investment continuation, and consumer spending growth are expected to underpin demand across both commercial and consumer segments through 2034. Smart tool integration will transition from a premium differentiator to a standard commercial specification, particularly in industrial and construction segments.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including portable power tool distributors, construction contractors, automotive OEMs, hardware retailers, and end consumers across Central, Northern, and Southern Mexico.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, regulatory filings (NOM standards, COFEPRIS), industry databases, trade publications, and publicly available financial data. Key sources include INEGI industrial production data, CNET distributor reports, and CONUEE energy efficiency documentation. Over 180 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators (GDP growth, construction output, FDI inflows), sector-specific demand drivers, and historical market evolution. The base-case CAGR of 6.05% reflects consensus analyst estimates validated against manufacturer revenue growth rates.

Mexico Portable Power Tools Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Cordless Tools, Corded Tools |

| Applications Covered | Commercial, Consumer |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Stanley Black & Decker, Inc., Robert Bosch GmbH, Makita Corporation, Techtronic Industries Co. Ltd., Hilti Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico portable power tools market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico portable power tools market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico portable power tools industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Portable Power Tools Market Report

The Mexico portable power tools market accounted for USD 325.28 Million in 2025, representing sustained expansion driven by construction sector activity, automotive manufacturing demand, and the growing adoption of cordless tool platforms.

The Mexico portable power tools market is expected to grow at a CAGR of 6.05% during the forecast period from 2026-2034, supported by consistent demand from commercial construction, automotive, industrial nearshoring, and expanding consumer DIY segments.

The Mexico portable power tools market is projected to reach USD 597.80 Million by 2034. This growth reflects robust structural demand from construction, automotive, and industrial manufacturing sectors, complemented by the rising consumer DIY market.

Central Mexico leads the market with a 46.3% revenue share in 2025, driven by an established construction ecosystem, high manufacturing density in the Bajío industrial corridor, and the dense commercial and residential activity surrounding Mexico City, the State of Mexico, and Aguascalientes.

Northern Mexico is the fastest-growing regional cluster, accounting for 31.8% of the 2025 market. The region benefits from Mexico's automotive production concentration in Nuevo León, Chihuahua, and Coahuila, as well as the rapid buildout of nearshoring industrial parks driven by U.S.–China trade realignment and USMCA incentives.

Cordless Tools dominate with a 64.2% share of the product market in 2025, valued at approximately USD 208.8 Million. Adoption is driven by advances in lithium-ion battery chemistry, the expansion of brushless motor technology, and multi-voltage platform ecosystems that allow a single battery to power multiple tools, reducing total contractor ownership costs.

The Commercial application segment holds the largest share at 57.6% in 2025 (approx. USD 187.4 Million), driven by construction contractors, automotive OEMs, and repair workshops, nearshoring industrial facilities, and energy infrastructure projects. The segment benefits from high tool utilization rates, repeat purchase cycles, and growing demand for professional-grade cordless platforms.

Key players include Stanley Black & Decker, Inc., Robert Bosch GmbH, Makita Corporation, Techtronic Industries Co., Ltd., and Hilti Corporation. These five brands collectively hold an estimated 55–65% of the formal market revenue in 2025.

The major growth drivers include robust construction sector expansion fueled by government infrastructure investment, strong automotive manufacturing and aftermarket demand, nearshoring-driven industrial facility buildout across northern Mexico, growing adoption of cordless lithium-ion battery platforms, and rapid e-commerce expansion enabling consumer DIY tool purchasing across Tier-2 and Tier-3 cities.

Significant opportunities exist in cordless tool ecosystem expansion, smart and IoT-connected tool adoption, e-commerce distribution channel investment, after-sales service network development in secondary cities, southern Mexico infrastructure project alignment, and nearshoring-aligned B2B fleet management services targeting multinational manufacturers establishing facilities across northern Mexico.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)