Mexico Telehealth Market Size, Share, Trends and Forecast by Component, Communication Technology, Hosting Type, Application, End-User, and Region, 2026-2034

Mexico Telehealth Market Summary:

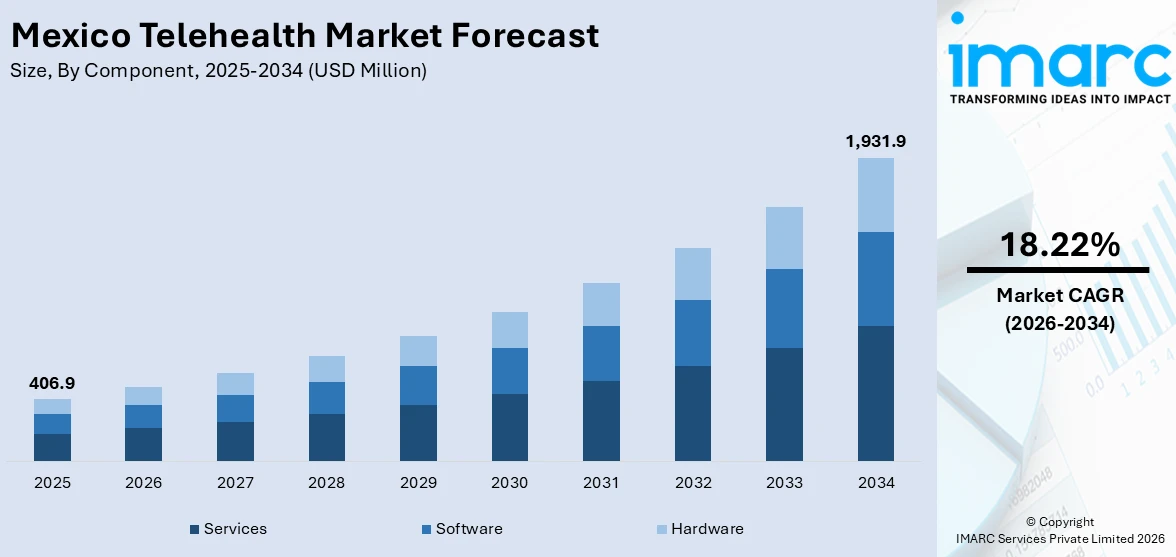

The Mexico telehealth market size was valued at USD 406.9 Million in 2025 and is projected to reach USD 1,931.9 Million by 2034, growing at a compound annual growth rate of 18.22% from 2026-2034.

The Mexico telehealth market is experiencing robust expansion driven by increasing digital health adoption, government-led healthcare modernization programs, and rising demand for accessible remote medical services across urban and rural populations. Growing internet connectivity, smartphone penetration, and supportive regulatory frameworks are accelerating virtual care integration into national healthcare delivery systems. Shifting patient preferences toward convenient consultation models and expanding telemedicine infrastructure are strengthening the Mexico telehealth market share.

Key Takeaways and Insights:

- By Component: Services dominate the market with a share of 38.5% in 2025, owing to the increasing outsourcing of telehealth platform management, technical support, and consulting activities by healthcare organizations seeking scalable virtual care delivery.

- By Communication Technology: Video conferencing leads the market with a share of 48.5% in 2025, driven by patient and provider preference for face-to-face virtual interactions that replicate in-person clinical consultations across specialties.

- By Hosting Type: Cloud-based and web-based exhibits a clear dominance in the market with 72.5% share in 2025, reflecting healthcare institutions' preference for scalable, cost-effective infrastructure that enables rapid deployment and remote accessibility.

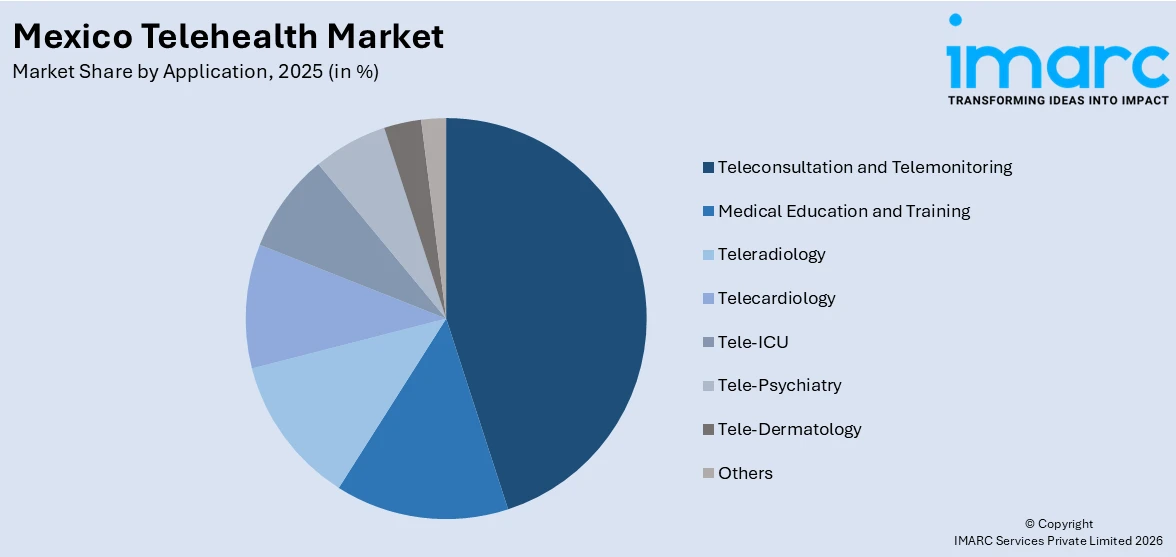

- By Application: Teleconsultation and telemonitoring represents the biggest segment with a market share of 42.5% in 2025, driven by growing patient demand for convenient primary care consultations and continuous chronic disease monitoring capabilities.

- By End-User: Providers is the largest segment with 42.5% share in 2025, driven by hospitals, clinics, and physician networks investing heavily in telehealth platforms to extend care reach and improve operational efficiency.

- By Region: Central Mexico dominates the market with 54.5% share in 2025, driven by the concentration of major healthcare facilities, digital infrastructure, and population density in Mexico City and surrounding metropolitan areas.

- Key Players: Key players drive the Mexico telehealth market by expanding digital health platforms, enhancing virtual care technologies, investing in interoperable systems, and forming strategic partnerships with healthcare providers to strengthen nationwide telemedicine adoption and improve patient outcomes across diverse populations.

To get more information on this market Request Sample

The Mexico telehealth market is advancing as healthcare institutions, government agencies, and technology providers collaborate to expand virtual care delivery across the nation. A major driver shaping this progress is the country's accelerating digital health transformation, supported by regulatory modernization and infrastructure investments. Policy encouragement through the national digital health strategy, expanding broadband connectivity in underserved regions, and rising patient acceptance of virtual consultations are contributing to a more favorable environment for telehealth adoption. The convergence of artificial intelligence integration, remote patient monitoring capabilities, and interoperable electronic health records is creating new opportunities for comprehensive virtual care ecosystems. Furthermore, increased private sector investment in telemedicine startups and established healthcare networks' digital transformation initiatives are strengthening market infrastructure and extending telehealth services to previously underserved communities across urban and rural Mexico.

Mexico Telehealth Market Trends:

Accelerating Integration of Artificial Intelligence in Virtual Care Platforms

Mexico's telehealth sector is increasingly incorporating artificial intelligence to enhance diagnostic accuracy, streamline clinical workflows, and personalize patient interactions. Healthcare providers are deploying AI-powered triage tools and symptom assessment chatbots to improve virtual consultation efficiency and reduce administrative burdens on medical staff. Natural language processing and machine learning algorithms are being embedded into telemedicine platforms to support preliminary assessments, automate clinical documentation, and enable intelligent patient routing. These innovations are strengthening care delivery quality, reducing consultation wait times, and supporting Mexico telehealth market growth.

Expansion of Remote Patient Monitoring for Chronic Disease Management

Remote patient monitoring is gaining significant traction in Mexico as healthcare systems prioritize continuous care for chronic conditions including diabetes, hypertension, and cardiovascular disease. Connected medical devices and wearable health trackers are enabling real-time data transmission between patients and providers, facilitating proactive clinical interventions. Integration of glucometers, blood pressure cuffs, and pulse oximeters with telehealth platforms is allowing physicians to track patient vitals remotely and adjust treatment plans accordingly. This shift toward preventive care models is reducing hospital readmissions and improving long-term health outcomes across the country.

Growing Adoption of Telepsychiatry and Mental Health Platforms

Digital mental health services are emerging as a critical component of Mexico's telehealth landscape, addressing the nation's significant gap in psychiatric care accessibility. Telepsychiatry platforms are connecting patients in underserved areas with licensed mental health professionals through secure video consultations and asynchronous messaging tools. Growing societal awareness around psychological wellbeing, combined with persistent shortages of psychiatrists in rural and semi-urban regions, is accelerating demand for virtual therapy and counseling services. These platforms are reducing stigma-related barriers and enabling confidential, convenient access to behavioral health support nationwide.

Market Outlook 2026-2034:

Mexico's telehealth market is poised for sustained expansion, supported by continued government investment in digital health infrastructure, growing institutional adoption of virtual care models, and increasing patient comfort with remote medical consultations. The market generated a revenue of USD 406.9 Million in 2025 and is projected to reach a revenue of USD 1,931.9 Million by 2034, growing at a compound annual growth rate of 18.22% from 2026-2034. With only 77% of Mexico's population currently having access to healthcare coverage and the country allocating just 5.7% of GDP to healthcare costs, telehealth represents a cost-effective solution for bridging persistent access gaps. Expanding broadband connectivity across rural and semi-urban regions, coupled with rising chronic disease prevalence, is expected to drive higher demand for remote consultation and monitoring services. The integration of artificial intelligence, machine learning, and interoperable health information systems is anticipated to further enhance virtual care capabilities. Increasing private sector investment in telehealth startups, strategic partnerships between technology firms and healthcare networks, and evolving regulatory frameworks supporting cross-state telemedicine practice are expected to create a more competitive, mature, and accessible digital healthcare landscape across Mexico.

Mexico Telehealth Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Services |

38.5% |

|

Communication Technology |

Video Conferencing |

48.5% |

|

Hosting Type |

Cloud-Based and Web-Based |

72.5% |

|

Application |

Teleconsultation and Telemonitoring |

42.5% |

|

End-User |

Providers |

42.5% |

|

Region |

Central Mexico |

54.5% |

Component Insights:

- Software

- Hardware

- Services

Services dominate with a market share of 38.5% of the total Mexico telehealth market in 2025.

The services segment encompasses telehealth platform management, technical support, consulting, integration services, and managed care solutions that enable healthcare organizations to deploy and maintain virtual care infrastructure. Healthcare providers in Mexico are increasingly outsourcing telehealth operations to specialized service providers, allowing them to focus on clinical delivery while ensuring platform reliability and regulatory compliance. The growing complexity of digital health ecosystems, including multi-system integration requirements and cybersecurity needs, is driving sustained demand for professional telehealth services across both public and private healthcare institutions nationwide.

The expanding scope of telehealth services extends beyond basic platform maintenance to include workflow optimization, clinical training, data analytics, and regulatory advisory support tailored to Mexico's evolving digital health landscape. Healthcare organizations are seeking end-to-end service partnerships that address interoperability consulting, platform customization, and ongoing performance monitoring to ensure seamless virtual care delivery. Rising demand for managed telehealth solutions that integrate with existing hospital information systems and electronic health records is further reinforcing the segment's leading position within the broader market.

Communication Technology Insights:

- Video Conferencing

- mHealth Solutions

- Others

Video conferencing leads with a share of 48.5% of the total Mexico telehealth market in 2025.

Video conferencing technology serves as the primary communication channel for real-time clinical consultations between patients and healthcare providers in Mexico. The technology enables face-to-face interactions that closely replicate in-person visits, supporting diagnostic assessments, treatment planning, and specialist referrals. Healthcare institutions are integrating high-definition video capabilities with electronic health records and diagnostic peripherals to create comprehensive virtual examination environments. The growing preference for synchronous communication in clinical settings is reinforcing video conferencing as the foundational technology underpinning telehealth service delivery across Mexico.

For instance, according to a 2024 Doctoralia survey, 68% of Mexican patients prefer video and telephone consultations for follow-up appointments, citing convenience, reduced travel costs, and faster access to specialists, highlighting the critical role of video-based telehealth infrastructure in meeting patient expectations. Enhanced bandwidth availability and mobile-optimized video platforms are further expanding the reach of synchronous telehealth consultations across metropolitan and regional healthcare networks, with urban centers like Mexico City, Guadalajara, and Monterrey leading in user adoption.

Hosting Type Insights:

- Cloud-Based and Web-Based

- On-Premises

Cloud-based and web-based exhibits a clear dominance with a 72.5% of the total Mexico telehealth market in 2025.

Cloud-based and web-based hosting solutions are the preferred infrastructure model for telehealth deployment in Mexico, offering healthcare organizations scalable, cost-effective, and rapidly deployable virtual care platforms. These solutions eliminate the need for significant upfront capital investment in physical servers and IT infrastructure, enabling smaller clinics and regional hospitals to adopt telehealth capabilities. The flexibility of cloud architectures supports seamless system updates, multi-location access, and integration with third-party health applications, making them particularly attractive for Mexico's diverse and geographically dispersed healthcare landscape.

The adoption of cloud-hosted telehealth platforms is further supported by improving data sovereignty frameworks and healthcare-specific compliance configurations that address patient privacy and security requirements. Healthcare institutions benefit from reduced infrastructure maintenance burdens, automatic software updates, and elastic computing resources that accommodate fluctuating patient consultation volumes. The increasing availability of multi-tenant cloud environments with built-in encryption, access controls, and audit trail capabilities is accelerating adoption among both public and private healthcare organizations seeking reliable, secure, and regulation-compliant telehealth hosting environments across the country.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Teleconsultation and Telemonitoring

- Medical Education and Training

- Teleradiology

- Telecardiology

- Tele-ICU

- Tele-Psychiatry

- Tele-Dermatology

- Others

Teleconsultation and telemonitoring represents the leading segment with a 42.5% of the total Mexico telehealth market in 2025.

Teleconsultation and telemonitoring applications form the core of Mexico's telehealth ecosystem, enabling real-time virtual clinical encounters and continuous remote monitoring of patient health parameters. These applications address critical healthcare accessibility challenges by connecting patients in underserved and rural areas with physicians and specialists through secure digital platforms. The rising prevalence of chronic conditions including diabetes, hypertension, and obesity across Mexico is driving significant demand for continuous remote monitoring solutions that enable proactive care management and early intervention capabilities within integrated health delivery frameworks.

The integration of teleconsultation with telemonitoring functionalities is creating unified care delivery workflows that combine synchronous clinical interactions with asynchronous patient data tracking. Connected wearable devices and digital health peripherals are enabling clinicians to track patient vitals continuously, supporting personalized treatment adjustments and reducing unnecessary emergency department visits. Growing institutional reliance on virtual consultation models for primary care delivery, specialist referrals, and post-discharge follow-up is reinforcing the segment's dominance as healthcare organizations increasingly embed these applications into routine clinical operations across the national healthcare system.

End-User Insights:

- Providers

- Patients

- Payers

- Others

Providers account for the highest revenue share of 42.5% of the total Mexico telehealth market in 2025.

Healthcare providers including hospitals, clinics, physician networks, and integrated health systems represent the largest end-user segment in Mexico's telehealth market. Providers are investing substantially in telehealth platforms to extend their clinical reach, optimize appointment scheduling, reduce patient no-show rates, and improve operational efficiency across care delivery workflows. The shift toward value-based care models is incentivizing providers to adopt virtual consultation and remote monitoring capabilities that enhance patient outcomes while managing costs. Public health institutions are also accelerating telemedicine adoption as part of national healthcare modernization initiatives.

Provider-led digital health transformation is reshaping clinical workflows through the integration of telehealth capabilities into existing hospital management systems and electronic health records, enabling seamless transitions between virtual and in-person care modalities. Healthcare networks are deploying multi-specialty teleconsultation platforms that facilitate coordinated care delivery, specialist referral management, and interdisciplinary clinical collaboration across geographically distributed facilities. The increasing focus on operational efficiency, patient engagement optimization, and clinical outcome measurement is further strengthening provider commitment to virtual care delivery models and reinforcing the segment's leading position within the market.

Regional Insights:

- Northern Mexico

- Central Mexico

- Southern Mexico

- Others

Central Mexico holds the largest share at 54.5% of the total Mexico telehealth market in 2025.

Central Mexico dominates the national telehealth landscape, anchored by Mexico City's concentration of major public and private healthcare institutions, advanced digital infrastructure, and high population density. The region benefits from superior broadband connectivity, a robust network of tertiary care hospitals, and proximity to technology hubs that facilitate rapid adoption of telemedicine platforms. The metropolitan area's well-established healthcare ecosystem and institutional capacity provide a strong foundation for integrating virtual care solutions into existing clinical workflows, positioning the region as the leading market for telehealth services.

The region's leadership position is further reinforced by the presence of leading private hospital groups, pharmaceutical companies, and health technology startups headquartered in the metropolitan area. Central Mexico's healthcare workforce density and institutional capacity support higher volumes of specialist teleconsultations, medical education programs, and remote monitoring initiatives compared to other regions. The convergence of academic medical centers, research institutions, and digital health incubators fosters continuous innovation and early adoption of emerging telehealth technologies, establishing the region as the primary hub for virtual care advancement across the country.

Market Dynamics:

Growth Drivers:

Why is the Mexico Telehealth Market Growing?

Government-Led Digital Health Modernization and Regulatory Support

Mexico's federal government is playing a pivotal role in driving telehealth adoption through comprehensive digital health strategies, regulatory modernization, and targeted infrastructure investments. The establishment of supportive legal frameworks for telemedicine practice, including guidelines for virtual prescriptions and cross-state consultations, is creating a more conducive environment for healthcare providers to deliver remote services. These regulatory advancements are complemented by substantial public investment in digital health infrastructure, including broadband expansion in underserved communities and the deployment of integrated health information systems. Government programs supporting telehealth capacity building, provider training, and technology procurement are further accelerating the digital transformation of Mexico's healthcare system. The progressive integration of telemedicine into public health insurance schemes and national development plans is broadening service reach and reducing institutional resistance. Standardized protocols for virtual consultations across federally funded healthcare facilities are establishing minimum technical requirements and patient data protection standards, fostering greater confidence among institutions and patients in virtual care delivery models.

Rising Chronic Disease Prevalence Driving Demand for Remote Monitoring

Mexico faces one of the highest chronic disease burdens in Latin America, with diabetes, hypertension, obesity, and cardiovascular conditions affecting a substantial proportion of the adult population. This epidemiological profile is generating significant demand for continuous remote patient monitoring and teleconsultation services that enable proactive chronic disease management and reduce the strain on physical healthcare facilities. The growing recognition that effective chronic disease management requires continuous patient engagement beyond periodic clinic visits is driving healthcare institutions to invest in telemonitoring platforms. Connected medical devices, wearable sensors, and digital health applications are enabling real-time vital sign tracking and timely clinical interventions, reducing emergency hospitalizations and improving long-term patient outcomes across the national healthcare system. The convergence of aging population demographics, sedentary lifestyle prevalence, and dietary patterns contributing to metabolic conditions is further amplifying the need for scalable virtual care solutions that support longitudinal patient management and preventive health interventions across diverse geographic regions.

Expanding Digital Infrastructure and Internet Connectivity

The rapid expansion of broadband internet access and mobile network coverage across Mexico is creating the foundational infrastructure necessary for widespread telehealth adoption. Improvements in connectivity are reaching previously underserved rural and semi-urban populations, enabling access to virtual healthcare services for communities historically limited by geographic barriers. This expanding digital footprint is particularly significant for telehealth adoption, as reliable internet connectivity is a prerequisite for video-based consultations, remote patient monitoring, and electronic health record integration. The growing availability of affordable smartphones and mobile data plans is further democratizing access to digital health applications, enabling patients across socioeconomic segments to engage with virtual care platforms and participate in telehealth programs offered by both public and private healthcare providers. Public-private partnerships focused on extending cellular coverage, deploying satellite internet solutions, and modernizing telecommunications infrastructure in remote areas are progressively narrowing the digital divide and creating new opportunities for telehealth service expansion across the country.

Market Restraints:

What Challenges the Mexico Telehealth Market is Facing?

Digital Literacy and Technology Adoption Barriers Among Underserved Populations

Despite expanding internet connectivity, significant portions of Mexico's population, particularly elderly individuals and rural communities, face challenges in effectively utilizing digital health platforms due to limited digital literacy and technology familiarity. The complexity of telehealth applications, language barriers among indigenous populations, and insufficient patient education programs hinder adoption. These factors create disparities in virtual care accessibility, limiting the market's potential to serve the populations that would benefit most from remote healthcare services.

Data Privacy and Cybersecurity Concerns in Healthcare Digitization

The increasing digitization of healthcare services raises significant concerns regarding patient data privacy, cybersecurity vulnerabilities, and regulatory compliance across Mexico's telehealth ecosystem. Healthcare institutions face challenges in implementing robust data protection frameworks that comply with evolving national regulations while maintaining seamless virtual care delivery. The risk of data breaches, unauthorized access to sensitive medical records, and insufficient cybersecurity infrastructure among smaller healthcare providers create trust barriers that can slow institutional and patient adoption of telehealth platforms.

Fragmented Healthcare System and Interoperability Challenges

Mexico's healthcare system operates through multiple distinct institutions including the Social Security Institute, public health facilities, and private providers, creating significant fragmentation in digital health infrastructure. The lack of standardized interoperability protocols among different telehealth platforms, electronic health record systems, and institutional networks limits seamless data exchange and continuity of care across providers. This fragmentation complicates the development of integrated telehealth ecosystems and increases implementation costs for healthcare organizations seeking comprehensive virtual care solutions.

Competitive Landscape:

The Mexico telehealth market is becoming increasingly competitive as healthcare technology providers, established hospital networks, and emerging digital health startups expand their virtual care capabilities across the country. Companies are focusing on developing comprehensive platform solutions that integrate video consultations, remote monitoring, digital prescriptions, and electronic health record interoperability to deliver seamless patient experiences. Competition is driven by investments in artificial intelligence capabilities, multilingual interface development, and regulatory compliance features tailored to Mexico's evolving digital health framework. Strategic partnerships between technology firms and healthcare institutions are fostering innovation, accelerating platform adoption, and improving clinical workflow integration. As a result, market players are continually refining their strategies to capture market share and capitalize on the country's accelerating shift toward digital healthcare delivery.

Mexico Telehealth Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Hardware, Others |

| Communication Technologies Covered | Video Conferencing, mHealth Solutions, Others |

| Hosting Types Covered | Cloud-Based and Web-Based, On-Premises |

| Applications Covered | Teleconsultation and Telemonitoring, Medical Education Training, Teleradiology, Telecardiology, Tele-ICU, Tele-Psychiatry, Tele-Dermatology, Others |

| End-Users Covered | Providers, Patients, Payers, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Mexico Telehealth Market Report

The Mexico telehealth market size was valued at USD 406.9 Million in 2025.

The Mexico telehealth market is expected to grow at a compound annual growth rate of 18.22% from 2026-2034 to reach USD 1,931.9 Million by 2034.

Services dominated the market with a share of 38.5%, driven by increasing healthcare provider reliance on outsourced platform management, technical support, and integration services for deploying scalable telehealth solutions.

Key factors driving the Mexico telehealth market include government-led digital health modernization, rising chronic disease prevalence, expanding internet connectivity, growing provider and patient acceptance of virtual care, and increasing investment in health technology innovation.

Major challenges include digital literacy barriers among underserved populations, data privacy and cybersecurity concerns in healthcare digitization, fragmented healthcare system interoperability, uneven infrastructure development across regions, and evolving regulatory compliance requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)