Mexico Vaccine Market Size, Share, Trends and Forecast by Product Type,Treatment Type, Technology, Route of Administration, Patient Type, Indication, Distribution Channel, End User, and Region, 2026-2034

Mexico Vaccine Market Size, Share, Trends & Forecast (2026-2034)

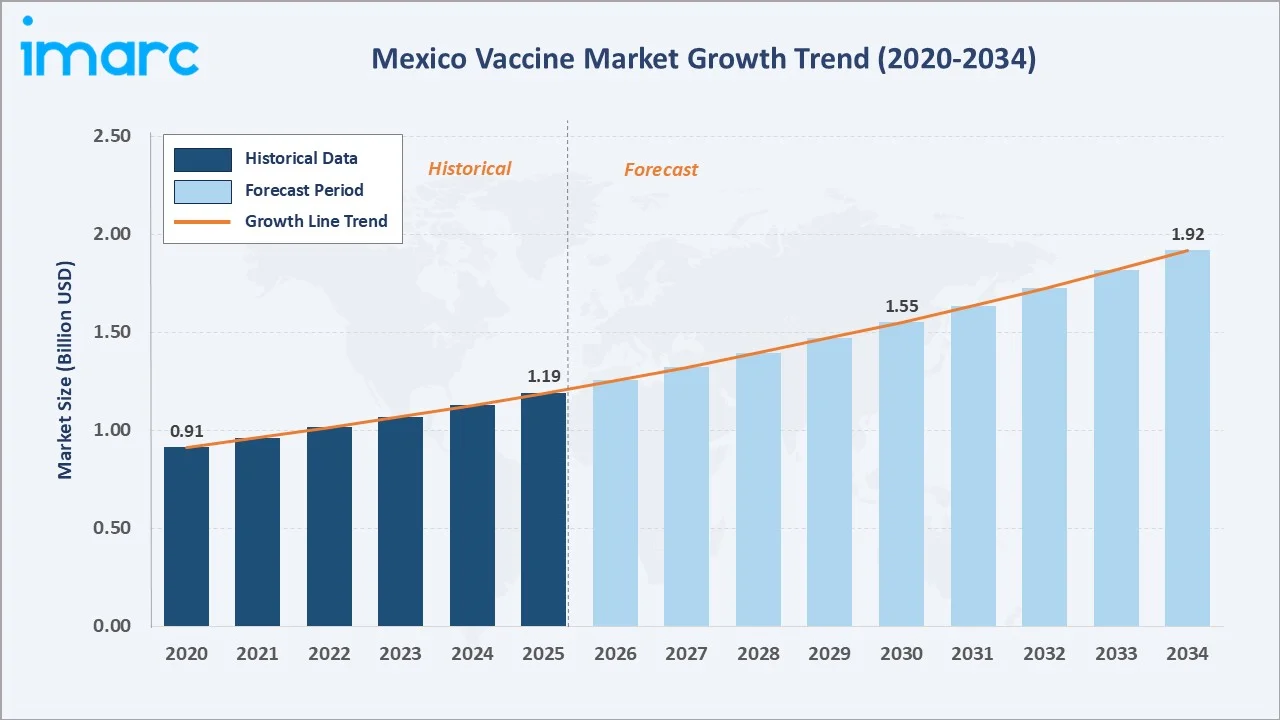

The Mexico vaccine market reached USD 1.19 Billion in 2025 and is projected to reach USD 1.92 Billion by 2034, growing at a CAGR of 5.45% during 2026-2034. The expansion of public immunization programs, rising incidences of vaccine-preventable diseases, and the adoption of advanced vaccine technologies, including mRNA and vector-based platforms, are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.19 Billion |

|

Forecast Market Size (2034) |

USD 1.92 Billion |

|

CAGR (2026-2034) |

5.45% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

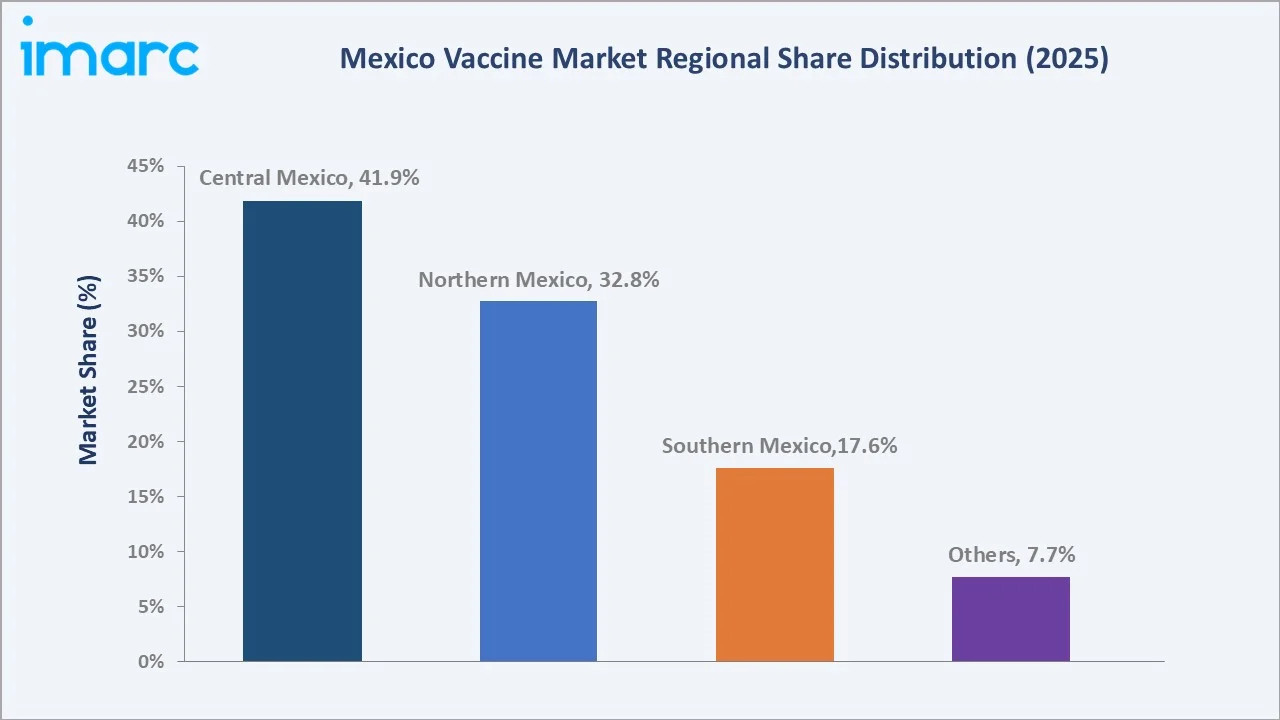

Central Mexico leads regionally with a 41.9% market share in 2025, anchored by Mexico City’s concentration of federal health institutions, IMSS and ISSSTE hospital networks, the CENAPRECE national immunization coordination center, and COFEPRIS regulatory headquarters that collectively drive the country’s vaccine procurement, distribution, and administration infrastructure. Multivalent vaccines command the product-type leadership at 58.4%, reflecting the National Vaccination Schedule’s systematic preference for combination vaccines that maximize immunization efficiency per visit.

To get more information on this market, Request Sample

Mexico’s vaccine market is underpinned by three structural forces: the government’s sustained commitment to expanding universal immunization coverage across its 132 million population, growing collaborations between regulatory bodies and vaccine manufacturers facilitating technology transfer and local production investment, and the adoption of next-generation vaccine platforms that are broadening protection against previously difficult-to-vaccinate disease targets.

Executive Summary

The Mexico vaccine market is experiencing sustained expansion, driven by the convergence of public health imperatives, technological advancement in vaccine platforms, and strengthening government commitment to universal immunization as a public health and economic development priority. The market was valued at USD 1.19 Billion in 2025 and is forecast to reach USD 1.92 Billion by 2034, growing at a CAGR of 5.45%.

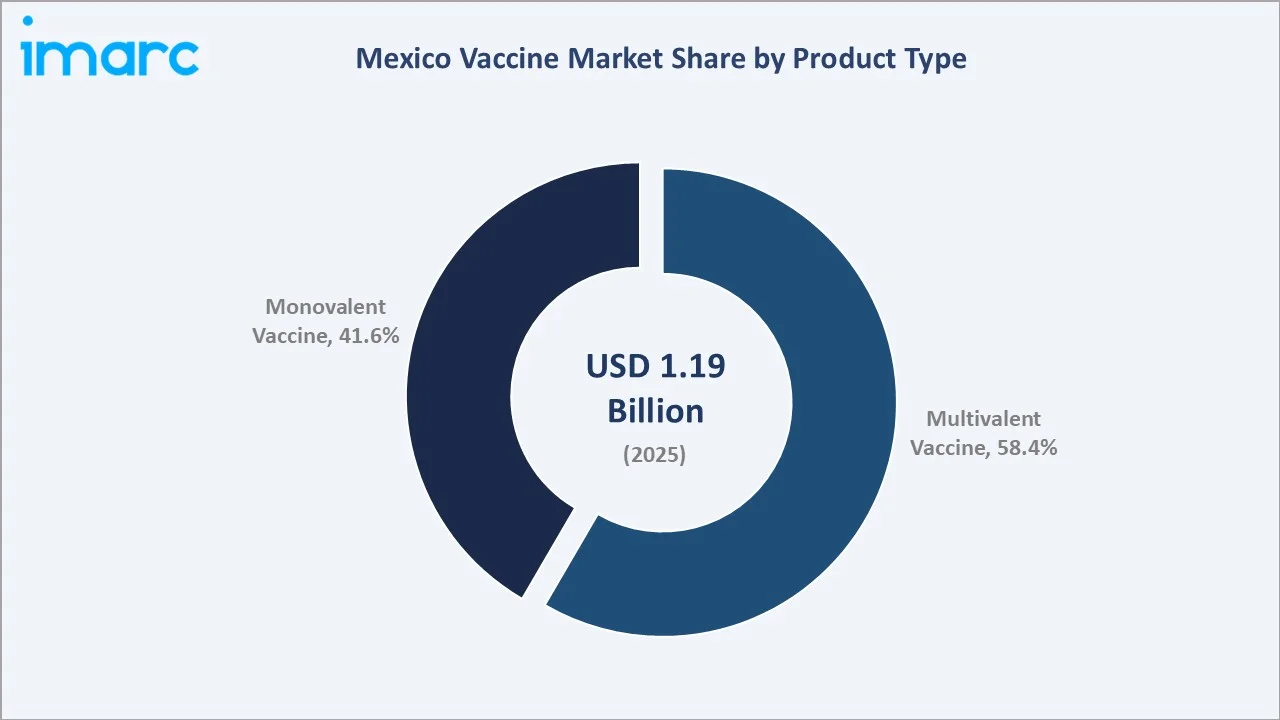

Multivalent vaccines lead the product-type segment with a 58.4% share in 2025, reflecting the national immunization program’s systematic use of combination vaccines that protect against multiple diseases through a single administration, improving coverage rates and reducing logistical burden on healthcare systems.

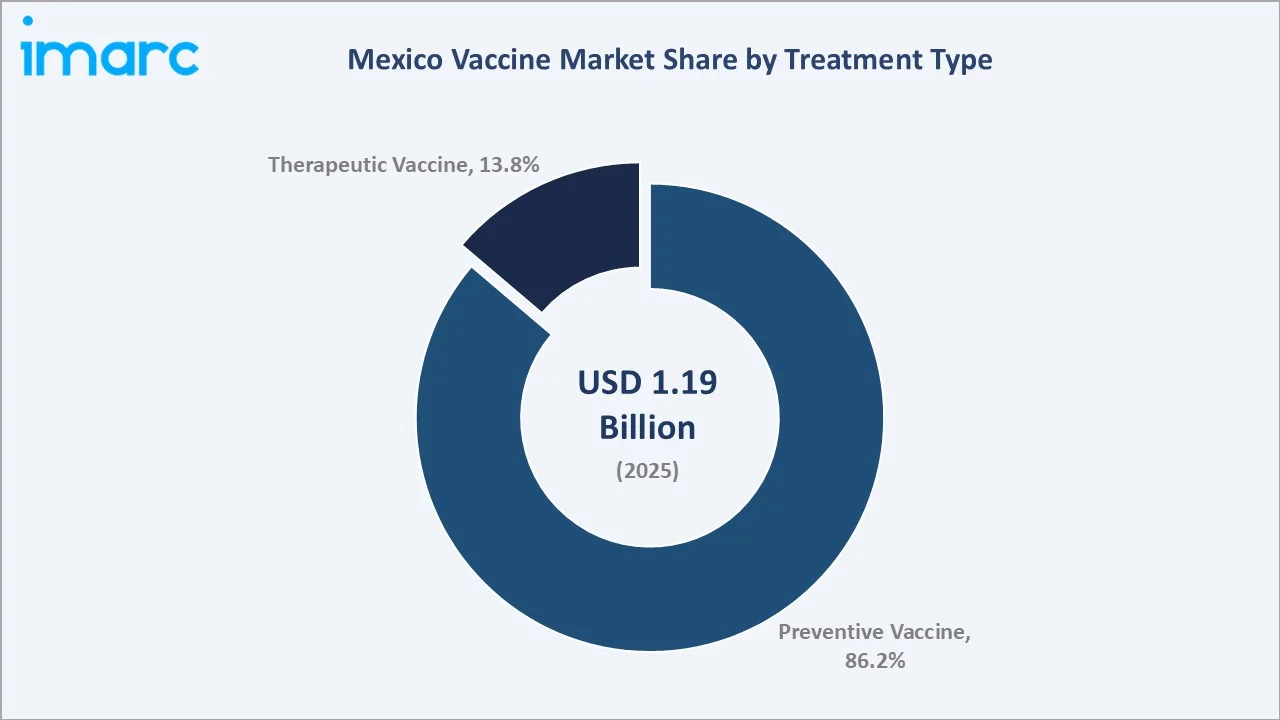

Monovalent vaccines at 41.6% serve critical applications in disease-specific campaigns, travel health, and emerging vaccine categories where single-antigen formulations provide targeted protection. Preventive vaccines dominate treatment type at 86.2%, underpinned by Mexico’s universal public vaccination mandate, while therapeutic vaccines at 13.8% represent the fastest-growing treatment type as cancer immunotherapy and HIV therapeutic vaccine research advances.

Key players collectively supply the majority of Mexico’s vaccine requirements through a combination of IMSS/ISSSTE institutional procurement, government tender programs, and private market sales through hospital pharmacies and vaccination centers.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Multivalent Vaccine – 58.4% share (2025) |

|

Fastest Growing Product Type |

Monovalent Vaccine – ~5.2% CAGR (2026-2034) |

|

Largest Treatment Type |

Preventive Vaccine – 86.2% share (2025) |

|

Fastest Growing Treatment Type |

Therapeutic Vaccine – ~6.8% CAGR (2026-2034) |

|

Leading Region |

Central Mexico – 41.9% share (2025) |

|

Top Companies |

Sanofi, Pfizer Inc., GlaxoSmithKline plc, Merck & Co., Inc., Serum Institute of India Pvt. Ltd. |

Key Analytical Observations Supporting The Above Data:

- Multivalent vaccines account for 58.4% of Mexico’s vaccine market in 2025. The National Vaccination Schedule administered through IMSS, ISSSTE, and Secretaría de Salud mandates combination vaccines including hexavalent DTaP-IPV-HepB-Hib products, MMR, and pneumococcal conjugate vaccines for the pediatric population. Multivalent formulations are preferred in public health programs as they reduce the number of injections per child, improve compliance, decrease cold chain requirements, and lower per-dose administration costs.

- Preventive vaccines at 86.2% share (2025) dominate the treatment-type segment, reflecting the fundamental public health philosophy of vaccination as disease prevention rather than treatment. Mexico’s National Vaccination Schedule includes preventive vaccines for over 14 diseases, including tuberculosis, polio, hepatitis B, diphtheria-tetanus-pertussis, haemophilus influenzae type b, establishing preventive vaccination as the structural core of the nation’s immunization program.

- Therapeutic vaccines at 13.8% (2025) represent the fastest-growing treatment type (~6.8% CAGR through 2034), driven by advances in cancer immunotherapy and infectious disease therapeutic vaccine development. Mexico’s oncology sector, facing growing cancer burden from cervical cancer, hepatocellular carcinoma, and melanoma, represents a priority area where therapeutic vaccine approaches are gaining clinical and commercial traction.

- Central Mexico’s 41.9% share (2025) regional dominance reflects the concentration of healthcare infrastructure in the Mexico City metropolitan area and surrounding states. IMSS headquarters, ISSSTE central procurement, COFEPRIS regulatory operations, and CENAPRECE national immunization coordination are all based in or adjacent to Mexico City, creating a centralized ecosystem that drives vaccine procurement, distribution logistics, and cold chain management for the entire national system.

Mexico Vaccine Market Overview

The Mexico vaccine market encompasses biological preparations that stimulate the immune system to provide protection against infectious diseases and, increasingly, therapeutic applications in oncology and chronic disease management. Mexico’s vaccine ecosystem is structured around two parallel channels: the public immunization system administered through IMSS, ISSSTE, and Secretaría de Salud networks, which accounts for the majority of vaccine volume and is funded through federal and state government budgets; and the private market served through hospital pharmacies, private vaccination centers, and medical office channels.

The regulatory framework governing Mexico’s vaccine market is administered by COFEPRIS (Comisión Federal para la Protección contra Riesgos Sanitarios), which oversees vaccine market authorization, GMP manufacturing inspections, post-market pharmacovigilance, and import controls for biological products. Mexico’s adoption of ICH Good Manufacturing Practice guidelines and its accelerated review pathways for priority vaccines have progressively aligned the country’s regulatory environment with international standards, improving the speed-to-market for novel vaccines and reducing barriers to new product launches.

Market Dynamics

To evaluate market opportunities, Request Sample

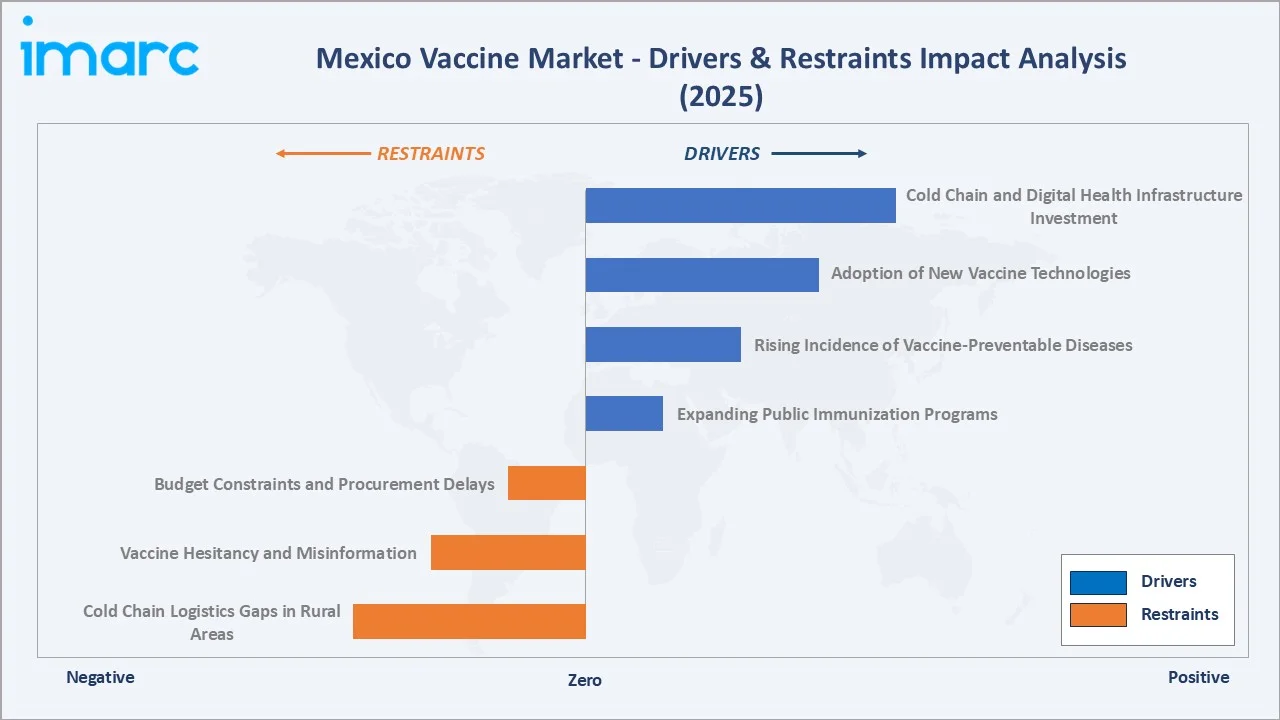

Market Drivers

- Expanding Public Immunization Programs: There is a sustained rise in the number of public immunization programs to enhance disease prevention across Mexico’s 132 million population. A significant focus on children who are more susceptible to infectious diseases drives consistent vaccine procurement, with approximately 2.0 million births annually requiring full pediatric schedule immunization.

- Rising Incidence of Vaccine-Preventable Diseases: Rising incidences of vaccine-preventable diseases are fueling urgency for comprehensive immunization coverage. This concern is also increasing public awareness, leading to higher vaccination rates in both public and private healthcare channels. Dengue virus circulation and HPV-related cervical cancer rates in Mexico create sustained clinical and public health demand for effective vaccination solutions, justifying continued investment in vaccine procurement and new product development by both government and private sector actors.

- Adoption of New Vaccine Technologies: The rising adoption of new vaccine technologies, such as messenger ribonucleic acid (mRNA) and vector-based vaccines, offers enhanced protection with fewer side effects compared to older vaccine platforms. Mexico’s regulatory framework has been progressively updated to accommodate accelerated evaluation of novel vaccine technologies, demonstrating faster-than-expected technology transfer.

- Cold Chain and Digital Health Infrastructure Investment: Growing collaborations between regulatory bodies, health organizations, and vaccine manufacturers are facilitating the development of advanced cold chain systems that are essential for the proper storage and distribution of vaccines. The rising employment of electronic health records (EHRs) and vaccination tracking systems is facilitating better monitoring of immunization rates and vaccine effectiveness, leading to more informed public health strategies and optimized vaccine stock management.

Market Restraints

- Cold Chain Logistics Gaps in Rural Areas: Despite significant infrastructure investment, Mexico’s rural and remote communities continue to face last-mile vaccine delivery challenges due to inadequate cold chain infrastructure, limited electricity access, and transportation logistics constraints. These gaps result in suboptimal vaccine coverage in precisely the communities most vulnerable to vaccine-preventable disease outbreaks, creating both public health risks and market penetration constraints for vaccine suppliers.

- Vaccine Hesitancy and Misinformation: Vaccine hesitancy, fueled by social media misinformation and residual mistrust from adverse event concerns, represents a growing challenge to Mexico’s immunization programs in urban and peri-urban populations. Post-COVID-19 pandemic, anti-vaccination sentiment has strengthened in certain demographic segments, complicating the achievement of herd immunity thresholds for diseases including measles and HPV, where coverage gaps have been identified.

- Budget Constraints and Procurement Delays: Government vaccine procurement in Mexico is conducted through complex multi-year tender processes that can experience delays due to budgetary constraints, administrative challenges, and supply chain disruptions. Funding limitations have occasionally resulted in temporary stock-outs of specific vaccines in public healthcare facilities, undermining vaccination schedule completion rates and creating uncertainty for vaccine manufacturers regarding demand predictability for public channel products.

Market Opportunities

- Adult Immunization Market Expansion: Mexico’s adult immunization market remains significantly underpenetrated relative to pediatric vaccination coverage. Influenza, pneumococcal, herpes zoster, meningococcal, and hepatitis vaccines for adult populations represent a structurally growing market opportunity as awareness of adult vaccine-preventable diseases increases, private health insurance coverage for adult vaccines expands, and occupational health programs at large Mexican enterprises incorporate adult immunization into employee health benefits packages.

- Therapeutic Oncology Vaccine Development: Mexico’s growing cancer burden, with cervical cancer, hepatocellular carcinoma, and melanoma representing significant public health challenges, creates demand for therapeutic vaccine approaches that complement or replace conventional chemotherapy and radiotherapy. International biopharmaceutical companies advancing cancer immunotherapy pipelines are progressively entering Mexico’s oncology treatment landscape, representing a high-value growth frontier for the therapeutic vaccine segment.

Market Challenges

- Post-Pandemic Routine Immunization Catch-Up: The COVID-19 pandemic disrupted routine childhood immunization programs globally, including in Mexico, creating cohorts of under-vaccinated children who require catch-up immunization. Reestablishing full National Vaccination Schedule coverage across multiple birth cohorts simultaneously creates logistical and budgetary pressure on the public health system, requiring prioritization of resources and targeted catch-up campaigns that compete with ongoing routine immunization program funding requirements.

- Biosimilar and Generic Vaccine Competition: As patents on established vaccine formulations expire, the entry of biosimilar and generic vaccine manufacturers intensifies price competition in public tender channels. While lower-cost alternative vaccines improve affordability for government procurement, they create margin pressure for established multinational vaccine manufacturers that compete on product quality and clinical data differentiation in price-sensitive tender environments.

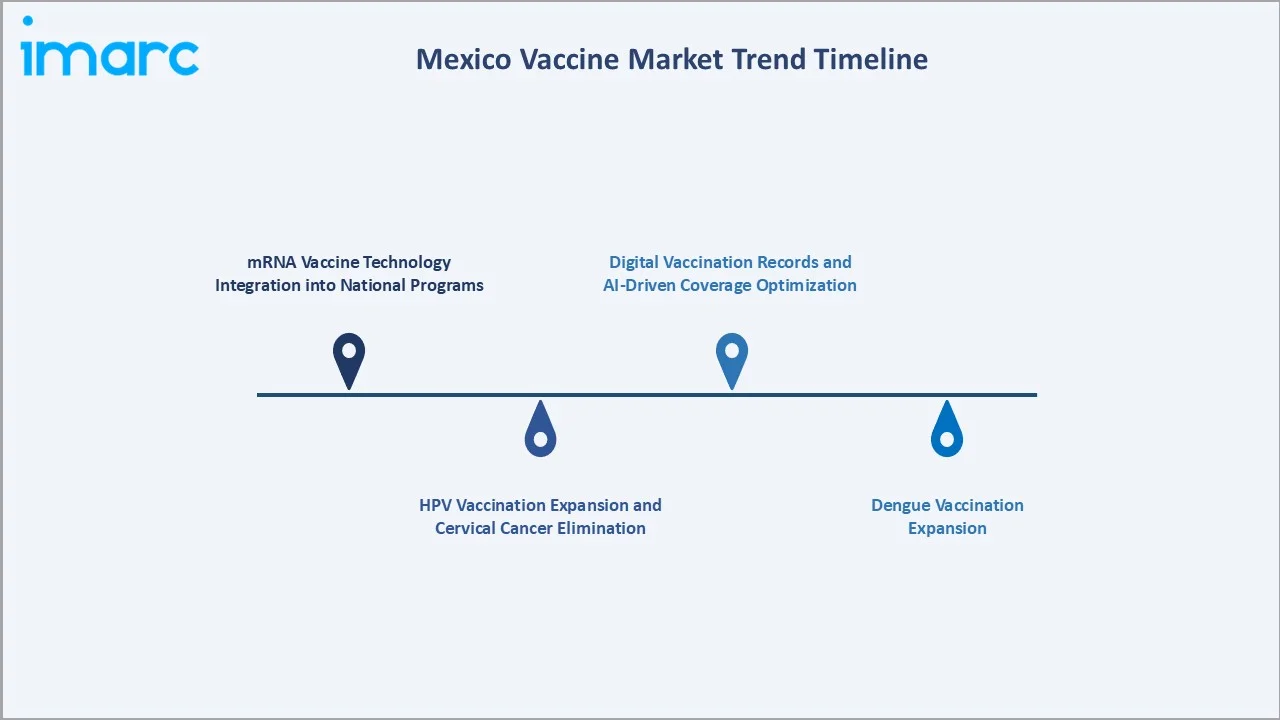

Emerging Market Trends

1. mRNA Vaccine Technology Integration into National Programs

The successful deployment of mRNA-based COVID-19 vaccines in Mexico established the country’s regulatory, cold chain, and healthcare system capacity to handle next-generation vaccine platforms. This experience is creating a foundation for future mRNA vaccine applications beyond COVID-19, including seasonal influenza vaccines with broader antigenic coverage, respiratory syncytial virus (RSV) vaccines for elderly populations, and investigational mRNA-based cancer immunotherapy products.

2. HPV Vaccination Expansion and Cervical Cancer Elimination

Mexico has committed to the WHO’s global strategy to eliminate cervical cancer by 2030, requiring 90% HPV vaccination coverage in girls aged 9–14, 70% cervical cancer screening coverage for women aged 35 and 50, and 90% access to treatment for pre-cancer and invasive cancer. HPV vaccine programs in Mexico have historically faced coverage challenges in rural states with high cervical cancer incidence. The government is accelerating school-based HPV vaccination programs using Merck’s Gardasil 9, targeting the 9–14 age cohort through coordinated health and education sector campaigns.

3. Dengue Vaccination Expansion

Mexico bears one of Latin America’s heaviest dengue virus burdens, with endemic transmission across tropical and subtropical regions including Chiapas, Guerrero, Oaxaca, Veracruz, and Yucatan. Sanofi’s Dengvaxia and Takeda’s QDENGA (TAK-003) dengue vaccines represent expanding market opportunities in Mexico’s dengue-endemic regions, particularly following the completion of COFEPRIS registration processes and the government’s evaluation of dengue vaccine inclusion in regional immunization programs.

4. Digital Vaccination Records and AI-Driven Coverage Optimization

The implementation of the Cartilla Nacional de Vacunación in digital format, integrated with IMSS and Secretaría de Salud patient records, enables automated identification of under-vaccinated individuals for targeted outreach campaigns. AI-driven analytics applied to vaccination coverage data are enabling health authorities to predict geographic areas at risk of disease outbreaks due to coverage gaps, optimize vaccine stock distribution to prevent stock-outs, and personalize public health communication for vaccine-hesitant population segments.

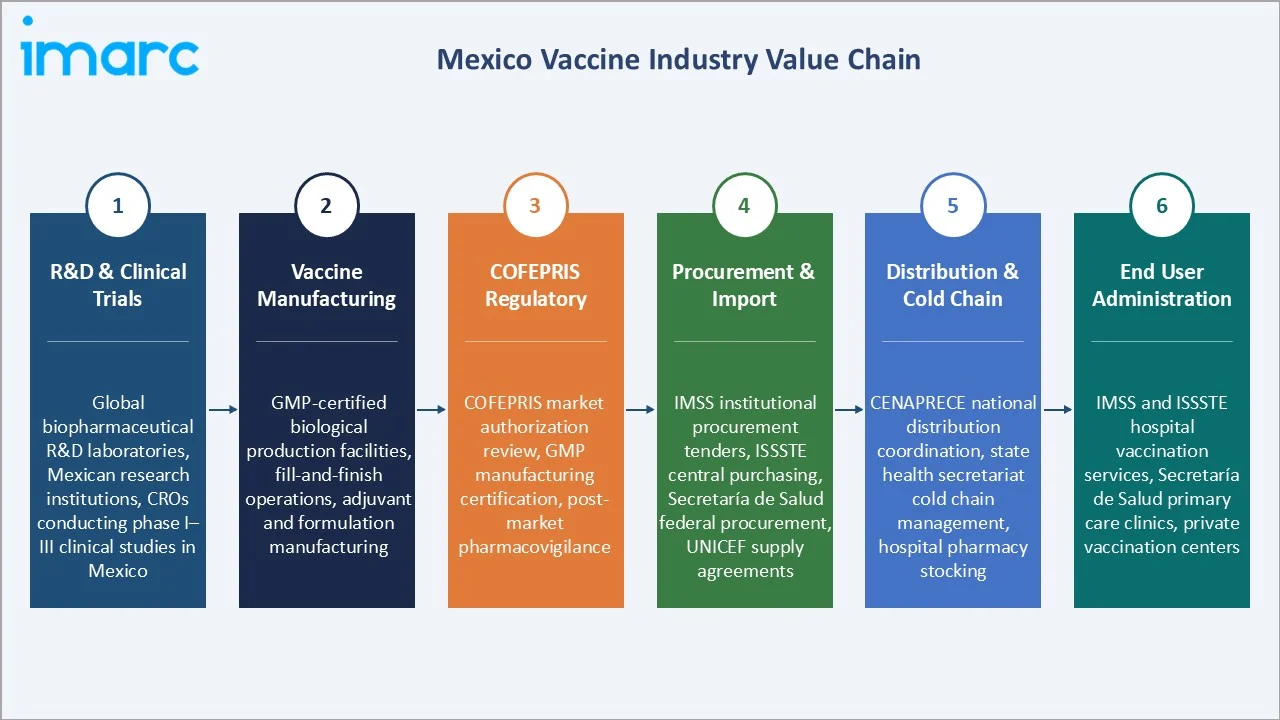

Industry Value Chain Analysis

Mexico’s vaccine value chain spans global R&D and clinical development through final patient administration, with each stage involving specialized institutions whose capabilities directly influence vaccine availability, quality, affordability, and public health impact.

|

Stage |

Key Players |

|

R&D & Clinical Trials |

Global biopharmaceutical R&D laboratories, Mexican research institutions, CROs conducting phase I–III clinical studies in Mexico |

|

Vaccine Manufacturing |

GMP-certified biological production facilities, fill-and-finish operations, adjuvant and formulation manufacturing |

|

COFEPRIS Regulatory |

COFEPRIS market authorization review, GMP manufacturing certification, post-market pharmacovigilance |

|

Procurement & Import |

IMSS institutional procurement tenders, ISSSTE central purchasing, Secretaría de Salud federal procurement, UNICEF supply agreements |

|

Distribution & Cold Chain |

CENAPRECE national distribution coordination, state health secretariat cold chain management, hospital pharmacy stocking |

|

End User Administration |

IMSS and ISSSTE hospital vaccination services, Secretaría de Salud primary care clinics, private vaccination centers |

Technology Landscape in the Mexico Vaccine Industry

Traditional Vaccine Platforms in Mexico's Immunization Program

Live-attenuated vaccines including oral polio vaccine (OPV), measles-mumps-rubella (MMR), varicella, and rotavirus are administered in pediatric programs under IMSS and Secretaría de Salud supervision, offering robust and durable immunity through single or limited doses. Inactivated vaccines including hepatitis A and B, influenza, and inactivated polio serve adults and high-risk populations. Toxoid vaccines including tetanus-diphtheria (Td) and combined DTP formulations protect against bacterial toxin-mediated diseases and are among the highest-volume products in Mexico’s public procurement system.

Conjugate Vaccine Technology

Conjugate vaccines, which link polysaccharide antigens to carrier proteins to enhance immunogenicity in infants and young children, represent a critical technology category in Mexico’s pediatric immunization program. Pneumococcal conjugate vaccines, Haemophilus influenzae type b (Hib) conjugate vaccines, and meningococcal conjugate vaccines are integral components of Mexico’s infant vaccination schedule. These higher-value products command premium pricing relative to traditional vaccine platforms and represent a growing share of vaccine market revenue as the National Vaccination Schedule progressively incorporates newer conjugate formulations with broader serotype coverage.

Recombinant Protein and mRNA Vaccine Platforms

Recombinant protein vaccines, produced through genetic engineering techniques that express target antigens in yeast, bacterial, or mammalian cell systems, underpin several of Mexico’s most strategically important vaccine programs. Merck’s Gardasil 9 and Sanofi Pasteur’s recombinant influenza vaccines exemplify this platform. The COVID-19 pandemic established mRNA vaccine technology in Mexico’s regulatory framework and healthcare provider infrastructure, creating a validated pathway for future mRNA-based vaccines against influenza, RSV, and investigational cancer immunotherapy applications.

Adjuvant Technology and Formulation Innovation

The increasing utilization of adjuvants in vaccines to improve the immune response, particularly for diseases that are more prevalent in Mexico’s diverse population, is enhancing the efficacy of vaccines and optimizing immunization campaigns. GSK’s AS01 adjuvant system, incorporated in the Shingrix herpes zoster vaccine, represents a clinically validated adjuvant technology that substantially elevates immune response compared to alum-adjuvanted or unadjuvanted formulations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Multivalent Vaccine |

58.4% |

2025 |

|

Treatment Type |

Preventive Vaccine |

86.2% |

2025 |

|

Technology |

🔒 |

🔒 |

2025 |

|

Route of Administration |

🔒 |

🔒 |

2025 |

|

Patient Type |

🔒 |

🔒 |

2025 |

|

Indication |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

41.9% |

2025 |

By Product Type

Multivalent vaccines dominate with a 58.4% share in 2025. This segment encompasses combination vaccines that protect against two or more diseases through a single formulation, including hexavalent DTaP-IPV-HepB-Hib pediatric vaccines, MMR, MMRV, and quadrivalent/nonavalent HPV vaccines. The National Vaccination Schedule’s systematic preference for combination vaccines reflects their public health advantages: fewer injections per visit, reduced cold chain requirements, improved vaccination schedule adherence, and lower per-disease protection cost that enables broader disease coverage within constrained government healthcare budgets.

To access detailed market analysis, Request Sample

Monovalent vaccines at 41.6% serve critical applications where single-antigen formulations are clinically appropriate or epidemiologically necessary, including BCG, hepatitis A, hepatitis B standalone, cholera, rabies, typhoid, Japanese encephalitis, and standalone influenza formulations for specific population segments. Monovalent products also include emerging vaccine categories such as dengue, RSV, and investigational therapeutic vaccines where single-antigen precision targeting is the clinical development approach.

By Treatment Type

Preventive vaccines dominate with a commanding 86.2% share in 2025. This segment encompasses all vaccines administered to healthy individuals to prevent future infectious disease, forming the core of Mexico’s National Vaccination Schedule. The preventive vaccine segment’s dominance reflects the public health priority of disease prevention over treatment, the large target population of all Mexican infants, children, adolescents, and adults eligible for scheduled preventive vaccines, and the established procurement and distribution infrastructure built around delivering preventive vaccines at scale.

Therapeutic vaccines at 13.8% share (2025) represent the fastest-growing treatment type at approximately 6.8% CAGR through 2034. This emerging category includes cancer immunotherapy vaccines (including therapeutic HPV vaccines for existing HPV-related pre-cancers and cancers), HIV therapeutic vaccine candidates in clinical development, and investigational vaccines targeting chronic diseases and autoimmune conditions.

Regional Market Insights

Central Mexico’s market leadership (41.9%, 2025) reflects the concentration of Mexico’s healthcare infrastructure, government procurement operations, and private healthcare market in the Mexico City metropolitan area and adjacent states. Federal healthcare institutions, including IMSS headquarters, ISSSTE central operations, and COFEPRIS, administer the majority of national vaccine procurement decisions and clinical regulatory approvals that shape the entire market.

Northern Mexico at 32.8% represents the country’s most commercially active private vaccine market, driven by the large industrial workforce employed in maquiladora manufacturing operations that participate in occupational health vaccination programs for influenza, hepatitis B, and tetanus. Monterrey’s private hospital sector and high-income professional population generate significant demand for travel vaccines, premium influenza formulations, and adult vaccination services not covered under public programs.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Central Mexico |

41.9% |

IMSS and ISSSTE headquarters driving procurement volume; COFEPRIS regulatory operations; highest private healthcare density; largest adult immunization private market |

|

Northern Mexico |

32.8% |

Industrial workforce occupational health vaccination programs; cross-border healthcare access creating private vaccine demand; high-income consumer base for private vaccination services |

|

Southern Mexico |

17.6% |

Highest burden of tropical vaccine-preventable diseases; federal health program expansion; growing tourism sector creating travel vaccine demand |

|

Others |

7.7% |

Secondary markets with improving healthcare infrastructure; federal immunization program expansion into rural communities; growing private vaccination center network in secondary cities |

Competitive Landscape

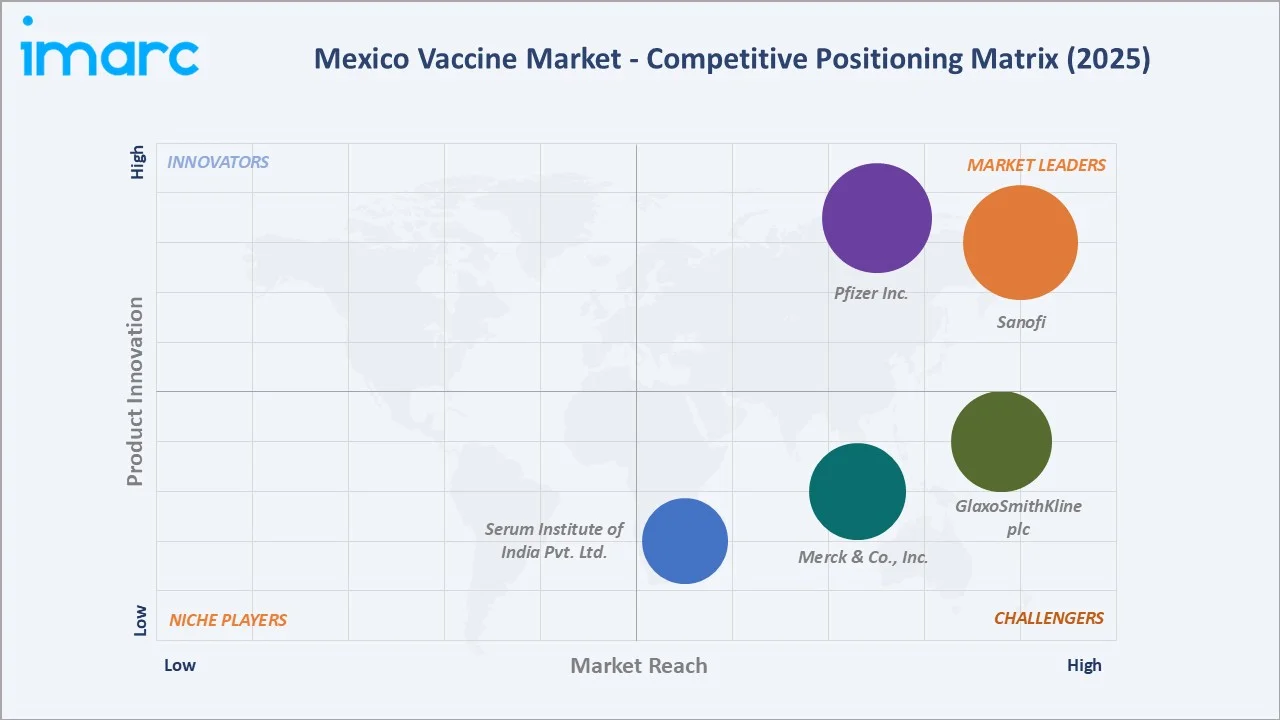

Mexico’s vaccine market is dominated by global multinational biopharmaceutical companies that supply both public institutional procurement channels and private healthcare markets. The competitive landscape is characterized by a small number of global leaders holding the majority of value share through high-technology products, with emerging competition from cost-competitive producers from India and China in price-sensitive public tender segments.

|

Company Name |

Key Vaccines |

Market Position |

Core Strength |

|

Sanofi |

Dengvaxia, Fluzone, MenQuadfi, YF-VAX, among others |

Market Leader |

Dengue vaccine pioneer; influenza portfolio breadth; pediatric combination vaccines; IMSS supply relationships |

|

Pfizer Inc. |

Abrysvo, Prevnar, Comirnaty, among others |

Market Leader |

PCV market leadership; mRNA platform; COVID-19 vaccine infrastructure; pneumococcal innovation pipeline |

|

GlaxoSmithKline plc |

Shingrix, Infanrix, Rotarix, Arexvy, among others |

Strong Challenger |

Herpes zoster vaccine leadership; HPV vaccine portfolio; rotavirus; adjuvant system technology |

|

Merck & Co., Inc. |

Gardasil, Gardasil 9, ProQuad, RotaTeq, VAQTA, among others |

Strong Challenger |

Nonavalent HPV vaccine leadership; pediatric MMR combinations; hepatitis A; clinical oncology pipeline |

|

Serum Institute of India Pvt. Ltd. |

COVISHIELD, COVOVAX, RABIVAX-S, HEXASIIL |

Challenger |

Low-cost biosimilar and generic vaccine supply; public tender competitiveness; large-scale production capacity |

Global multinationals leverage their clinical data differentiation, GMP-certified manufacturing quality standards, and long-term IMSS and ISSSTE supplier relationships to maintain value leadership in institutional procurement. Cost-competitive producers from developing countries are gaining share in price-sensitive tender categories where bioequivalence to established vaccines is well-documented, and procurement criteria emphasize unit cost minimization.

Key Company Profiles

Sanofi

Sanofi is one of the world’s largest vaccine manufacturers and holds a leading position in Mexico’s vaccine market through Sanofi Pasteur, its dedicated vaccines division. The company’s portfolio is particularly strong in influenza vaccines, dengue vaccination, and pediatric combination products.

- Product Portfolio: Dengvaxia (dengue vaccine), Fluzone (seasonal influenza), MenQuadfi, Imovax, and investigational next-generation RSV vaccine candidates.

- Recent Developments: In January 2026, Sanofi reported Q4 2025 net sales of EUR 11,303 million, up 13.3% at CER, while FY 2025 net sales reached EUR 43,626 million, up 9.9% at CER. However, vaccine sales stood at EUR 2,039 million in Q4 2025, down 2.5% at CER, and EUR 7,936 million for FY 2025, down 1.2% at CER.

- Strategic Focus: Dengue vaccine market development in endemic regions; next-generation mRNA influenza vaccine pipeline; pediatric combination vaccine volume in public procurement; RSV vaccine development for elderly and maternal immunization.

Pfizer Inc.

Pfizer Inc. is one of the global vaccine leaders and holds a dominant position in Mexico’s pneumococcal and COVID-19 vaccine segments through its vaccines, oncology, and retrovirology division.

- Product Portfolio: Prevnar 13 and Prevnar 20 (pneumococcal conjugate), Comirnaty (COVID-19 mRNA vaccine), Trumenba (meningococcal B), and mRNA-based pipeline products.

- Recent Developments: In July 2025, Pfizer announced plans to use its Toluca, México state facility to revive vaccine awareness in Mexico and strengthen its role as a key vaccine supplier across Latin America. The site labels, packages, stores, and distributes vaccines and other products to 10 Latin American markets, while supporting Pfizer’s upcoming 20-valent pneumococcal vaccine rollout.

- Strategic Focus: PCV20 adoption in Mexico’s National Vaccination Schedule; mRNA vaccine platform lifecycle management beyond COVID-19; adult immunization market development; investigational vaccine pipeline for emerging infectious diseases.

Market Concentration Analysis

Mexico’s vaccine market exhibits moderate-to-high concentration, with the leading five multinationals collectively holding an estimated 65–70% of market value in 2025. This concentration reflects the high technical and regulatory barriers to vaccine development, the premium pricing of proprietary next-generation vaccine formulations, and the established institutional supply relationships that create switching costs in public procurement channels.

Market dynamics are evolving with the entry of cost-competitive producers from India and China that are challenging established suppliers in public tender segments. Government preferences for vaccine supply diversification to reduce single-supplier dependency, combined with the growing quality certification of alternative producers under WHO prequalification programs, are creating conditions for a gradual share shift in price-sensitive product categories.

Investment & Growth Opportunities

Fastest Growing Segments

Therapeutic vaccines (~6.8% CAGR) represent the highest-growth investment vector through 2034, driven by cancer immunotherapy pipeline maturation and the progressive expansion of Mexico’s oncology treatment center infrastructure. The therapeutic vaccine segment is projected to reach approximately USD 300–350 Million by 2030, representing a high-value niche that commands significant pricing premiums over traditional preventive vaccines.

Emerging Market Expansion

Southern Mexico’s 17.6% market share significantly understates its growth potential relative to its disease burden profile. The region’s high dengue, typhoid, hepatitis A, and rabies disease burden creates structural demand for vaccines that is currently underserved by public program coverage and private market access. Investment in cold chain infrastructure, healthcare worker training, and private vaccination centers in Oaxaca, Chiapas, Veracruz, and Yucatán state capitals could unlock substantial incremental market growth through 2034.

Venture and Institutional Investment Trends

- Mexico’s government has articulated strategic interest in developing domestic vaccine manufacturing capability through joint ventures with international companies, offering fiscal incentives for investment in GMP-certified biological manufacturing facilities that would reduce import dependency and improve pandemic preparedness.

- COFEPRIS’s progressive alignment with ICH regulatory standards is attracting increased interest from global clinical-stage vaccine companies seeking to include Mexican sites in late-stage clinical trials, creating economic activity and potentially accelerating market access for approved products.

Future Market Outlook (2026-2034)

Mexico’s vaccine market is positioned for sustained, above-average healthcare sector growth through 2034. From a base of USD 1.19 Billion in 2025, the market is projected to reach USD 1.92 Billion by 2034, representing total incremental value creation of USD 0.73 Billion at a CAGR of 5.45%. This growth reflects expanding adult immunization programs, the progressive uptake of next-generation vaccine formulations that command premium pricing, and the gradual emergence of therapeutic vaccines as a commercially significant market category.

The market composition will evolve significantly by 2034. Therapeutic vaccines are projected to grow from 13.8% to approximately 18–20% of total treatment-type market value as cancer immunotherapy advances. Multivalent vaccine dominance is expected to be sustained above 55% as next-generation combination products integrate additional antigens, while mRNA-based preventive vaccines for influenza and RSV may capture 8–12% of volume in their respective categories by 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including vaccine medical affairs and commercial executives at multinational companies, IMSS and ISSSTE procurement officials, COFEPRIS regulatory scientists, private vaccination center medical directors, infectious disease specialists, and public health policy advisors across Mexico’s major healthcare markets.

Secondary Research

Secondary research encompassed COFEPRIS market authorization databases, IMSS and Secretaría de Salud immunization program publications, CENAPRECE vaccination coverage data, PAHO and WHO country vaccination reports, vaccine company annual reports, and epidemiological publications covering Mexico’s vaccine-preventable disease burden from 2020 to 2025.

Forecasting Models

Market size estimations were derived from top-down and bottom-up forecasting incorporating immunization program budget projections, private market spend models, new product launch impact assessment, and vendor revenue data. A base-case CAGR of 5.45% reflects consensus estimates validated against government healthcare expenditure trends, IMSS tender volumes, and IMARC market tracking from 2020 to 2025.

Mexico Vaccine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Multivalent Vaccine, Monovalent Vaccine |

| Treatment Types Covered | Preventive Vaccine, Therapeutic Vaccine |

| Technologies Covered | Conjugate Vaccines, Inactivated and Subunit Vaccines, Live Attenuated Vaccines, Recombinant Vaccines, Toxoid Vaccines, Others |

| Route of Administrations Covered | Intramuscular and Subcutaneous Administration, Oral Administration, Others |

| Patient Types Covered | Pediatric, Adult |

| Indications Covered |

|

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Institutional Sales, Others |

| End Users Covered | Hospitals, Clinics, Vaccination Centers, Academic and Research Institutes, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Comapnies Covered | Sanofi, Pfizer Inc., GlaxoSmithKline plc, Merck & Co. Inc., Serum Institute of India Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico vaccine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico vaccine market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico vaccine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Vaccine Market Report

The Mexico vaccine market reached USD 1.19 Billion in 2025 and is projected to reach USD 1.92 Billion by 2034, growing at a CAGR of 5.45% during 2026-2034.

Multivalent vaccines lead with a 58.4% market share in 2025, driven by the National Vaccination Schedule’s systematic preference for combination vaccines that protect against multiple diseases through a single administration, improving vaccination coverage rates and reducing logistical burden in public immunization programs.

Preventive vaccines dominate with an 86.2% market share in 2025, reflecting the public health priority of disease prevention through the national immunization system and representing the core mission of Mexico’s universal vaccination programs administered through IMSS, ISSSTE, and Secretaría de Salud networks.

Central Mexico leads with a 41.9% share in 2025, anchored by the concentration of federal health institutions (IMSS, ISSSTE, COFEPRIS) in Mexico City, the country’s largest private healthcare market, and the administrative infrastructure that coordinates national vaccine procurement and distribution policy.

Some of the leading companies include Sanofi, Pfizer Inc., GlaxoSmithKline plc, Merck & Co., Inc., and Serum Institute of India Pvt. Ltd. Global multinationals collectively hold approximately 65–70% of market value through their high-technology vaccine portfolios and established institutional supply relationships.

Therapeutic vaccine growth is driven by the maturation of global cancer immunotherapy pipelines, Mexico’s high cervical cancer burden from HPV, the growing incidence of hepatocellular carcinoma, and investment in oncology treatment infrastructure.

Key challenges include cold chain logistics gaps limiting vaccine delivery to rural and remote communities, vaccine hesitancy amplified by social media misinformation particularly following the COVID-19 pandemic, government procurement budget constraints, and administrative delays creating stock-out risks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)