Microbiome Sequencing Services Market Size, Share, Trends and Forecast by Technology, Research Type, Laboratory Type, Application, End User, and Region, 2026-2034

Microbiome Sequencing Services Market Size, Share, Trends & Forecast (2026-2034)

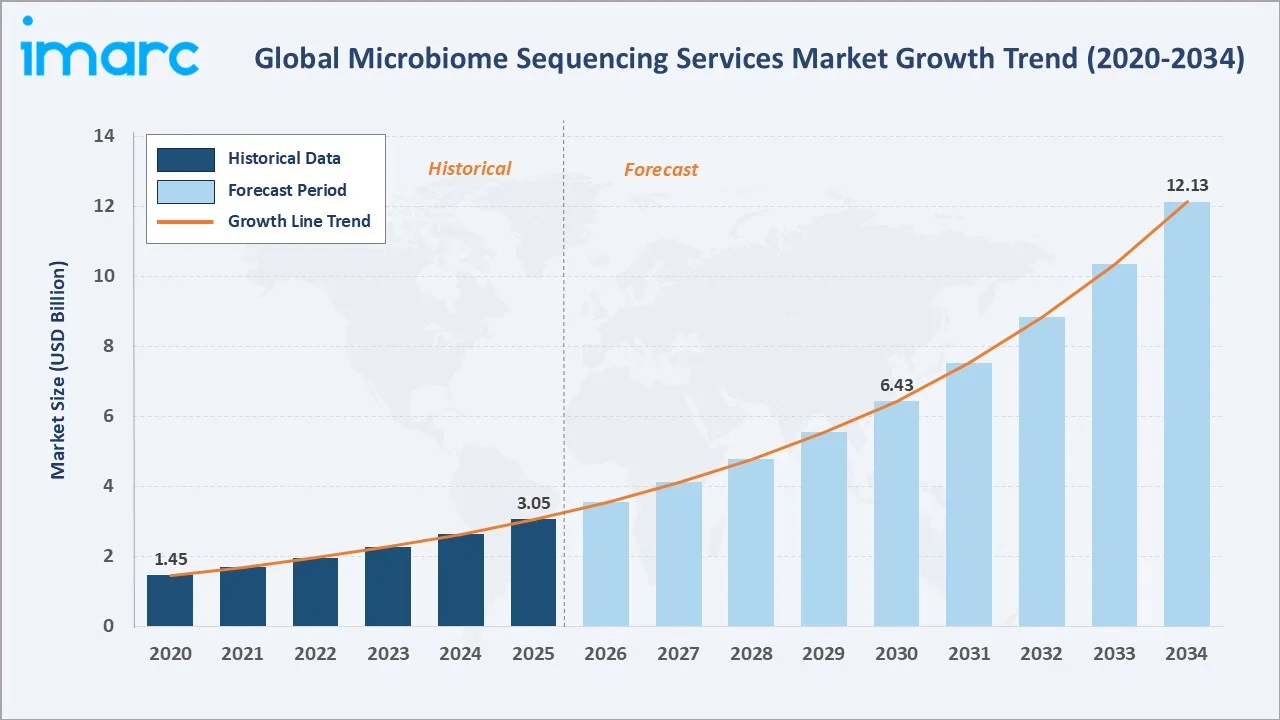

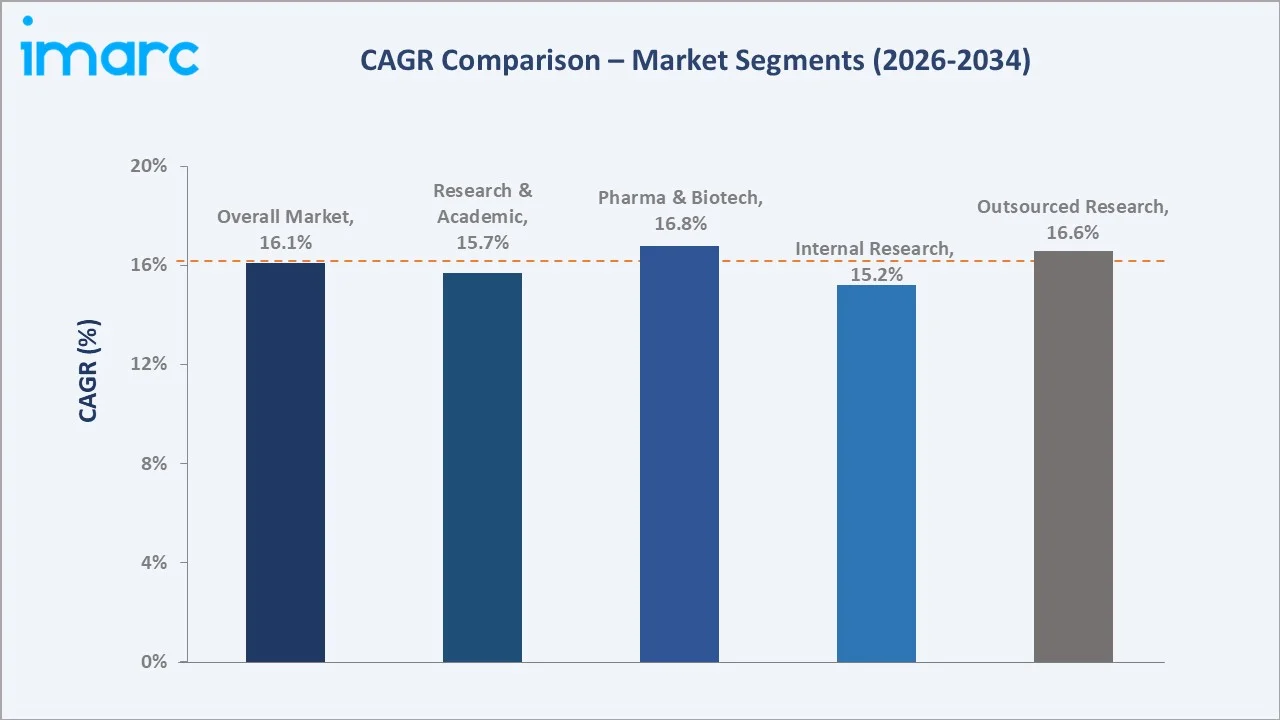

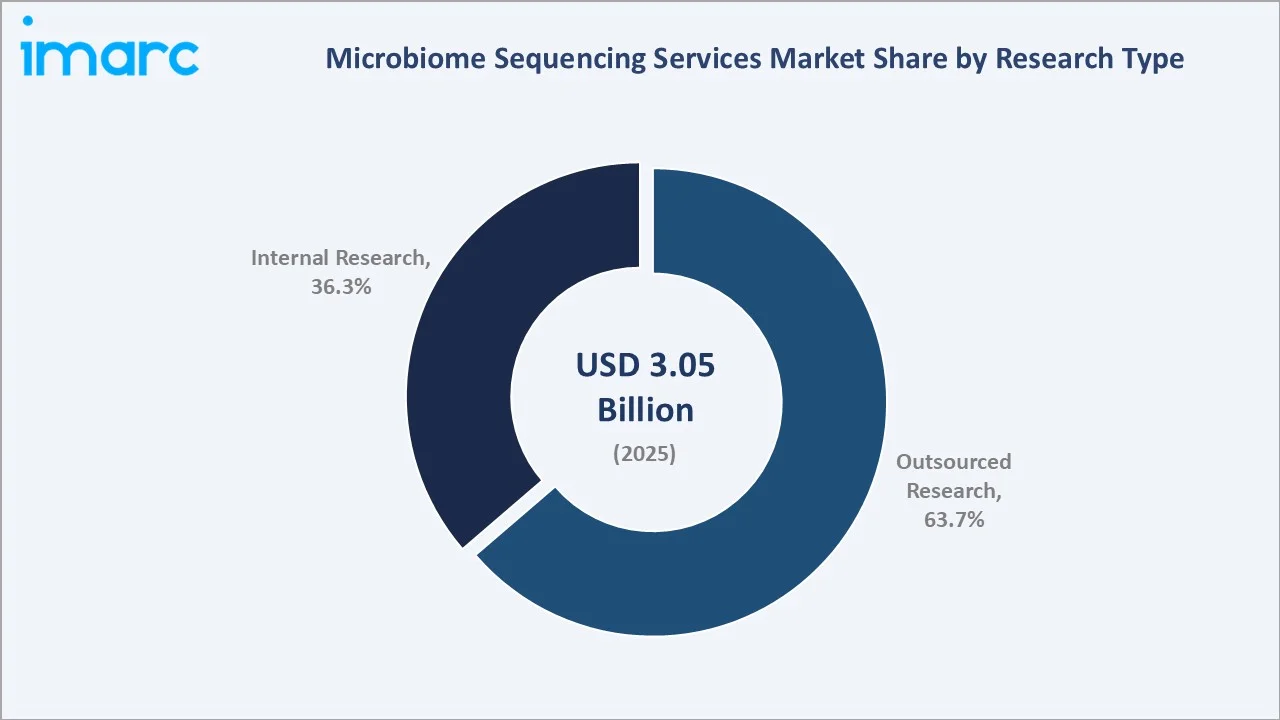

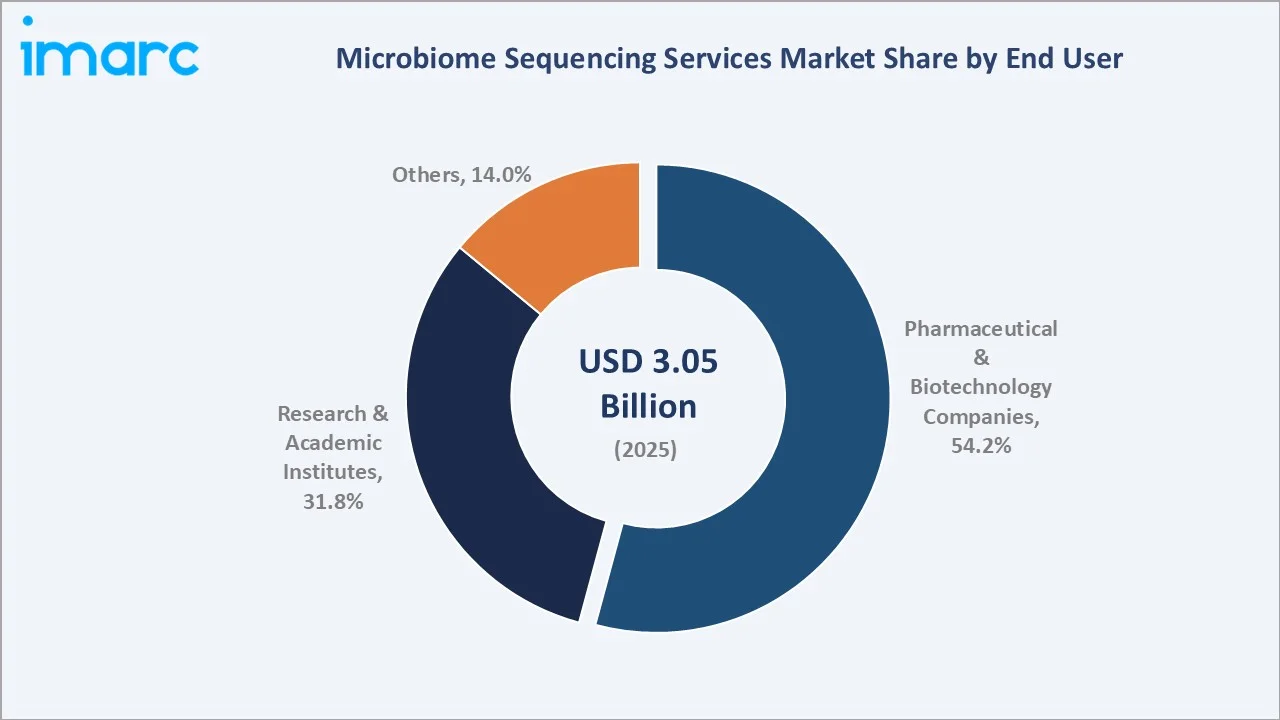

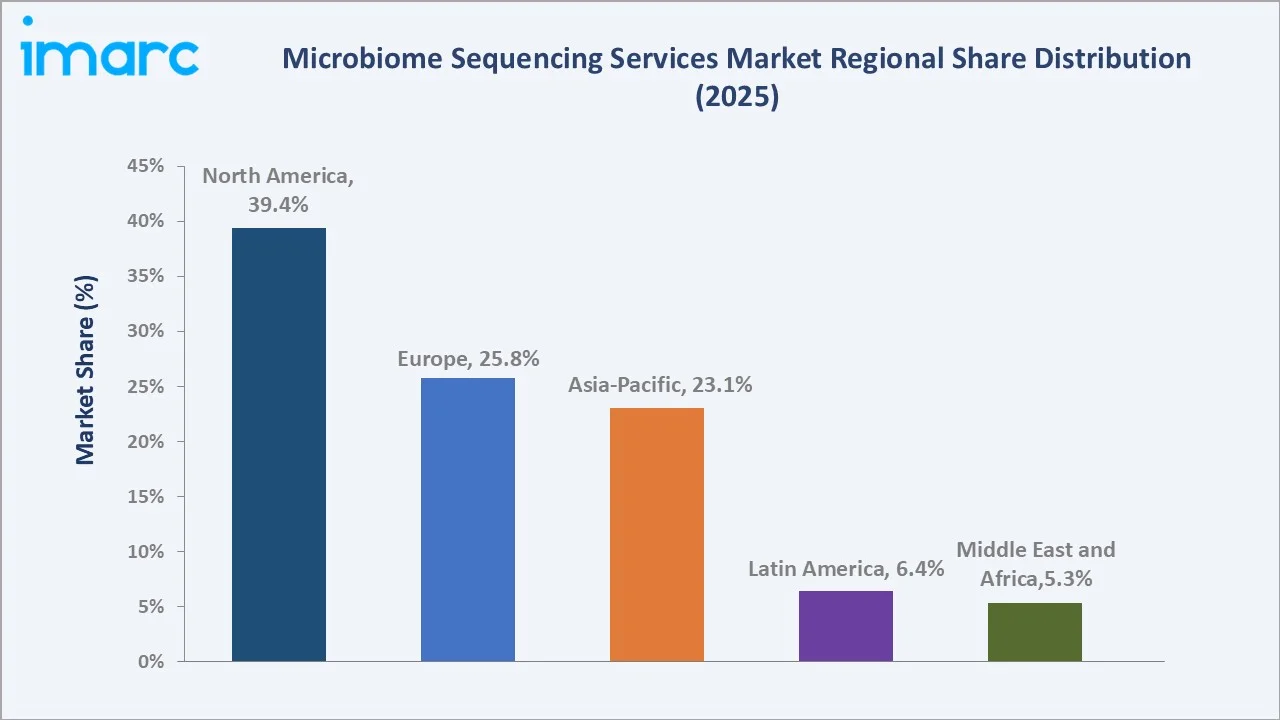

The global microbiome sequencing services market reached USD 3.05 Billion in 2025 and is projected to reach USD 12.13 Billion by 2034, growing at a CAGR of 16.09% during 2026-2034. The market is primarily driven by the increasing demand for precision medicine and personalized healthcare, coupled with the growing prevalence of chronic diseases and the need for microbiome-based diagnostics. Three in four American adults have at least one chronic condition, with over half living with two or more. Among adults aged 65 and older, over 90% have at least one chronic illness, while more than 75% of those aged 35-64 and 60% of adults aged 18-34 are affected. This high prevalence of chronic conditions is driving the microbiome sequencing services, as researchers and healthcare providers increasingly explore the role of the microbiome in disease development, progression, and personalized treatment strategies. Outsourced research dominates at 63.7%. Pharmaceutical and biotechnology companies lead end users at 54.2%. North America commands 39.4% of the global market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 3.05 Billion |

| Forecast Market Size (2034) | USD 12.13 Billion |

| CAGR (2026-2034) | 16.09% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Research Type | Outsourced Research (63.7%, 2025) |

| Dominant End User | Pharma & Biotech Companies (54.2%, 2025) |

| Leading Region | North America (39.4%, 2025) |

The market expanded from USD 1.45 Billion in 2020 to USD 3.05 Billion in 2025, anchored at USD 6.43 Billion in 2030, and forecast to reach USD 12.13 Billion by 2034. The rising FDA approvals marked a watershed moment for the microbiome sequencing services market, validating the microbiome drug development paradigm and catalyzing a new wave of pharmaceutical investment in microbiome programmes that generate systematic microbiome sequencing service demand for clinical trial biomarker analysis, pharmacodynamic monitoring, and companion diagnostic development.

To get more information on this market, Request Sample

Outsourced research grows fastest at ~16.6% CAGR as pharmaceutical companies increasingly commission external specialist microbiome sequencing CROs rather than building in-house sequencing infrastructure, driven by the capital-intensive nature of NGS platform maintenance, the bioinformatics expertise required for metagenomics analysis, and the cost advantages of scale that specialist service providers achieve. Pharmaceutical and biotechnology end users grow at ~16.8% CAGR through the exponential growth of microbiome clinical trial programmes requiring sequencing at every stage from discovery through Phase III.

Executive Summary

The global microbiome sequencing services market reached USD 3.05 Billion in 2025, representing the intersection of two major scientific and commercial forces: the maturation of the human microbiome as a validated therapeutic target through FDA-approved live biotherapeutic products, and the continuous democratization of next-generation sequencing technology that makes comprehensive microbiome profiling accessible to any research or pharmaceutical programme globally. The microbiome, the collective community of trillions of bacteria, archaea, fungi, viruses, and protists colonising the human body, has emerged over the past decade from scientific curiosity to an established pharmaceutical target class, with microbiome-gut-brain axis, microbiome-immune system crosstalk, and microbiome-drug metabolism interactions creating validated biological mechanisms linking microbiome composition to disease causation and therapeutic response. The market is projected to reach USD 12.13 Billion by 2034.

Outsourced research at 63.7% dominates the market structure, reflecting the pharmaceutical and academic research community's preference for commissioning specialist microbiome sequencing service providers rather than maintaining in-house NGS infrastructure. Pharmaceutical and biotechnology companies at 54.2% lead end-user demand through the systematic microbiome sequencing requirements of drug discovery, clinical biomarker development, companion diagnostic creation, and regulatory submission support that pharmaceutical microbiome programmes generate across the full drug development lifecycle. North America, at 39.4%, leads globally through the NIH microbiome research infrastructure, FDA-approved market validation, and the world's highest concentration of pharmaceutical microbiome drug development programmes.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Research Type | Outsourced Research – 63.7% share (2025) |

| Dominant End User | Pharmaceutical & Biotechnology Companies – 54.2% market share (2025) |

| Leading Region | North America – 39.4% market share (2025) |

Key Analytical Observations Supporting The Above Data:

- Outsourced research at 63.7%: Outsourcing offers access to advanced technologies, expert analysis, and scalable resources, enabling faster and cost-effective research without the complexities of maintaining internal sequencing capabilities.

- Pharmaceutical and biotechnology companies at 54.2%: The pharmaceutical and biotechnology companies drive extensive research and development in drug discovery, personalized medicine, and microbiome-based therapeutics. Their reliance on high-throughput, specialized sequencing services to accelerate product development and clinical studies fuels consistent demand in this market.

- North America at 39.4%: North America dominates regionally due to advanced healthcare infrastructure, high research and development expenditure, and widespread adoption of next-generation sequencing technologies. The region’s strong presence of pharmaceutical, biotechnology, and academic research institutions further drives demand for microbiome sequencing services.

Microbiome Sequencing Services Market Overview

The global microbiome sequencing services market encompasses all contract sequencing, bioinformatics analysis, and data interpretation services applied to the characterization of microbial communities across human health, environmental, and other biological contexts using next-generation sequencing technologies.

The ecosystem integrates microbiome sequencing service providers, NGS instrument manufacturers, reagent and sample preparation companies, bioinformatics platform providers, and microbiome database curators. Macroeconomic factors include rising global healthcare expenditure, increased investment in life sciences research, and growing funding for precision medicine initiatives.

Market Dynamics

Market Drivers

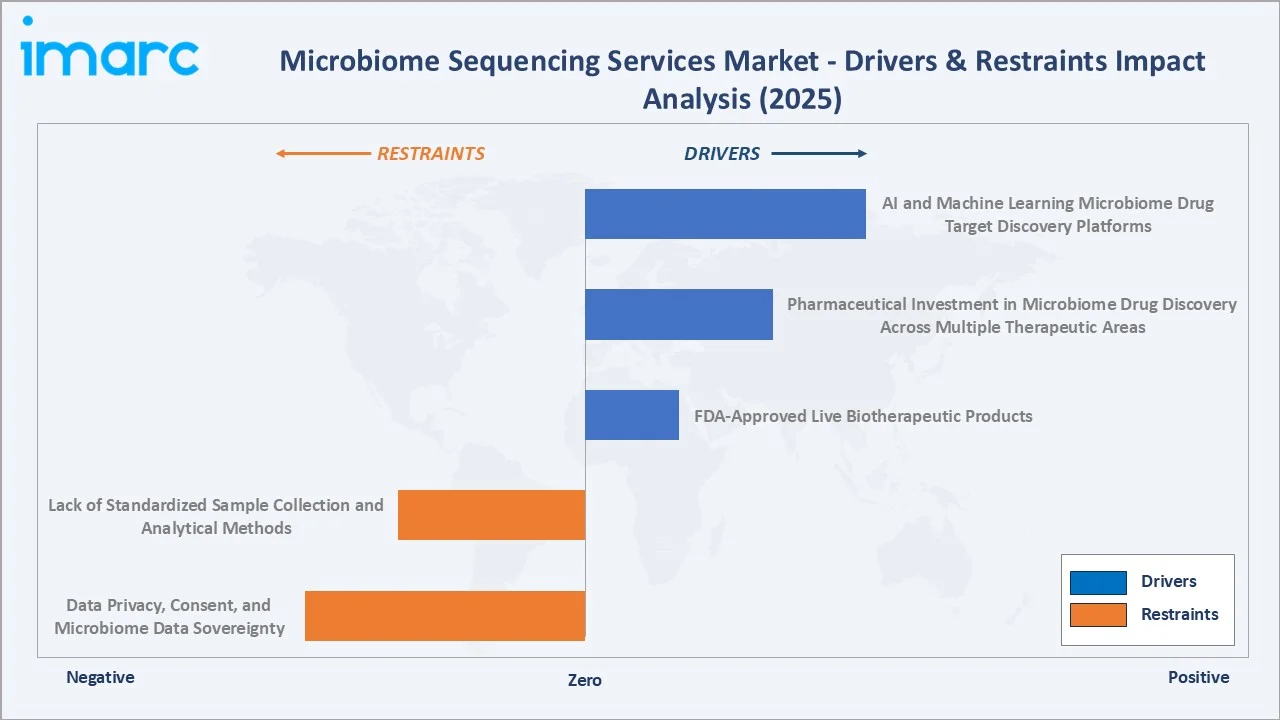

- FDA-Approved Live Biotherapeutic Products: FDA-approved live biotherapeutic products create demand for precise characterization and quality control of therapeutic microorganisms. Sequencing services are essential for ensuring product safety, potency, and regulatory compliance. Additionally, as more live biotherapeutics receive FDA approval, pharmaceutical and biotech companies increasingly rely on microbiome sequencing to develop, validate, and optimize these therapies, fueling market growth in research, clinical trials, and commercial production.

- Pharmaceutical Investment in Microbiome Drug Discovery Across Multiple Therapeutic Areas: Pharmaceutical investment in microbiome drug discovery across multiple therapeutic areas is increasing demand for high-throughput, accurate sequencing to identify microbial targets and biomarkers. In May 2026, Kanvas Biosciences secured $48 million in a Series A funding round co-led by existing investors DCVC and Lions Capital LLC, with participation from the Gates Foundation, ATHOS KG, Germin8, Ki Tua Fund, Pangaea Ventures, and others. Following a July 2024 round, this brings the company’s total funding to $78 million. The capital will support clinical trials for its lead immuno-oncology drug candidate, KAN-001, and advance commercial partnerships leveraging Kanvas’ spatial imaging and manufacturing platform for next-generation live biotherapeutic product (LBP) development. This investment exemplifies the pharmaceutical commitment to microbiome-based drug discovery across multiple therapeutic areas.

- AI and Machine Learning Microbiome Drug Target Discovery Platforms: AI and machine learning-driven microbiome drug target discovery platforms enable rapid analysis of complex microbial datasets to identify potential therapeutic targets. These platforms streamline the discovery process by predicting functional interactions, microbial pathways, and host-microbiome effects, reducing R&D timelines and costs. As a result, pharmaceutical and biotech companies increasingly rely on high-throughput sequencing services to generate the data required for AI-based analyses, fueling demand and growth in the microbiome sequencing services market.

Market Restraints

- Data Privacy, Consent, and Microbiome Data Sovereignty: Data privacy, consent, and microbiome data sovereignty impose strict regulatory and ethical requirements on data collection, storage, and sharing. Companies must navigate complex legal frameworks to protect personal microbiome information, which can slow research, limit cross-border collaborations, and increase compliance costs. These constraints create barriers to large-scale sequencing initiatives, reduce operational flexibility, and can delay market expansion despite growing demand for microbiome-based research and therapeutics.

- Lack of Standardized Sample Collection and Analytical Methods: The lack of standardized sample collection and analytical methods introduces variability and inconsistencies in data quality and reproducibility. Differences in collection protocols, storage conditions, and sequencing workflows can affect results, making it difficult to compare studies or validate findings. This challenges researchers and service providers, increases operational complexity, and slows the adoption of microbiome sequencing in clinical and commercial applications.

Market Opportunities

- Microbiome Companion Diagnostic Development: The development of microbiome companion diagnostics enabling personalized treatment strategies based on an individual’s microbial profile. Sequencing services are essential for identifying biomarkers, predicting patient response, and guiding therapy selection. As pharmaceutical and biotech companies invest in companion diagnostic programs, demand for high-precision, high-throughput microbiome sequencing grows, driving market expansion across research, clinical trials, and therapeutic applications.

- Long-Read Metagenomics and Strain-Level Microbiome Profiling: Long-read metagenomics and strain-level microbiome profiling provide highly detailed insights into microbial communities and individual strains. These technologies improve the accuracy of microbial identification, enable the discovery of rare or novel organisms, and support precision diagnostics and targeted therapeutics. As researchers and pharmaceutical companies increasingly seek strain-level resolution for disease association studies and live biotherapeutic development, demand for advanced sequencing services rises, driving market growth.

Market Challenges

- China Sequencing Service Provider Regulatory Scrutiny Creating Market Share Uncertainty in Western Markets: Regulatory scrutiny of China-based sequencing service providers is creating uncertainty regarding market share and service reliability for Western clients. Compliance concerns, data sovereignty issues, and differing quality standards can limit cross-border collaborations and slow the adoption of services from these providers. This regulatory ambiguity may force companies to seek alternative regional partners, increasing costs and operational complexity while constraining market growth.

- Clinical Validation and LDT Regulatory Requirements Creating Barriers for Microbiome Diagnostic Service Entry: Clinical validation and laboratory-developed test (LDT) regulatory requirements impose strict standards for accuracy, reproducibility, and compliance. Companies must invest significant time and resources to meet these requirements before entering the diagnostic space, which can delay product launches and increase operational costs. These regulatory hurdles create barriers for new entrants and slow the adoption of microbiome-based diagnostic services, limiting market growth despite increasing demand.

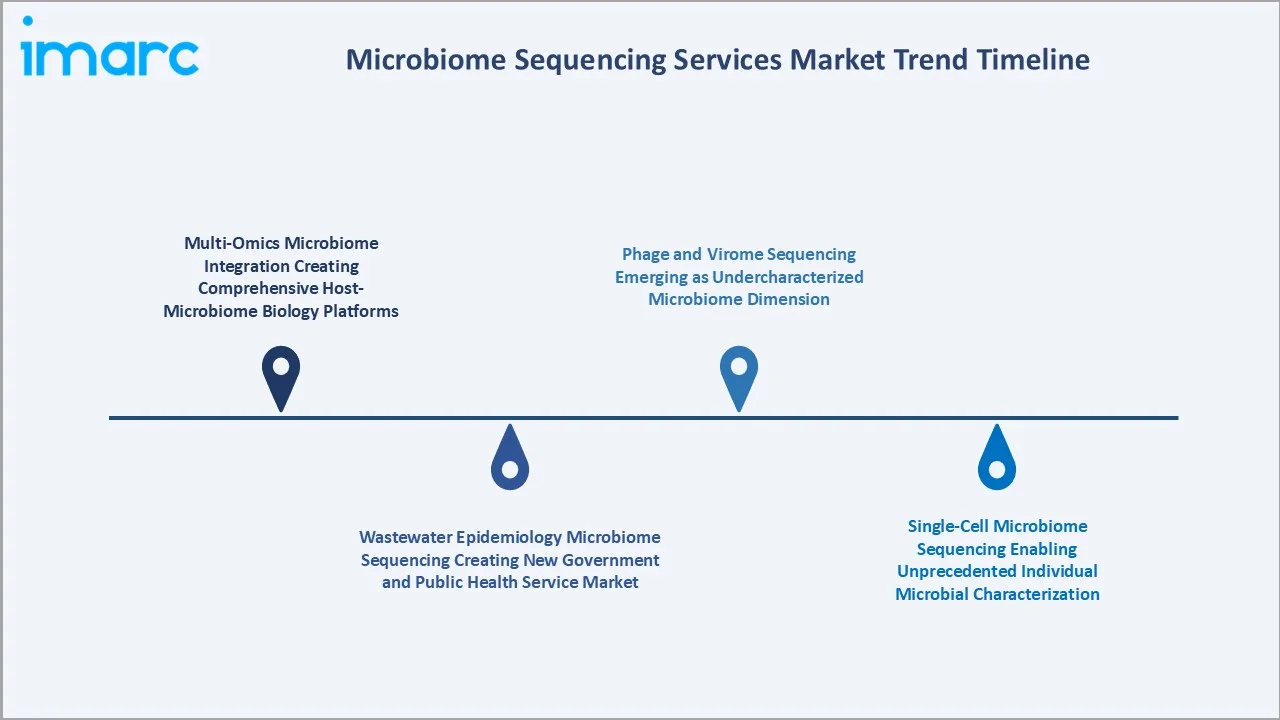

Emerging Market Trends

1. Multi-Omics Microbiome Integration Creating Comprehensive Host-Microbiome Biology Platforms

Integration of multi-omics microbiome data creates comprehensive platforms that combine genomic, transcriptomic, proteomic, and metabolomic information. In April 2025, Metabolon launched a microbiome research solution that integrates a new microbiome panel with metagenomics sequencing and multi-omics bioinformatics tools, providing a comprehensive platform for analyzing host-microbiome interactions. By providing a holistic view of host-microbiome biology, it enhances understanding of disease mechanisms, facilitates biomarker discovery, and drives demand for advanced sequencing services, reinforcing the growth of the microbiome sequencing services market.

2. Wastewater Epidemiology Microbiome Sequencing Creating New Government and Public Health Service Market

Wastewater epidemiology using microbiome sequencing enables governments and public health agencies to monitor community health in real time. By analyzing microbial and pathogen profiles in sewage, authorities can detect outbreaks, track antimicrobial resistance, and assess population-level exposure to chemicals or infectious agents. This approach creates a new market for microbiome sequencing services in public health surveillance, policy planning, and environmental monitoring, driving demand for high-throughput, accurate sequencing technologies.

3. Single-Cell Microbiome Sequencing Enabling Unprecedented Individual Microbial Characterization

Single-cell microbiome sequencing enables highly detailed characterization of individual microbial cells within complex communities. This technology allows researchers to study microbial diversity, function, and interactions at unprecedented resolution, revealing rare or previously undetectable species. By providing precise insights into microbial behavior and host interactions, single-cell approaches drive demand for advanced sequencing services, supporting innovation in diagnostics, therapeutics, and personalized medicine.

4. Phage and Virome Sequencing Emerging as Undercharacterized Microbiome Dimension

Phage and virome sequencing focusing on the largely undercharacterized viral component of the microbiome. This approach enables researchers to study bacteriophages, viruses, and their interactions with bacterial communities, shedding light on microbial ecology, disease mechanisms, and therapeutic potential. By uncovering these previously overlooked dimensions, phage and virome sequencing expand research capabilities and drive demand for specialized microbiome sequencing services.

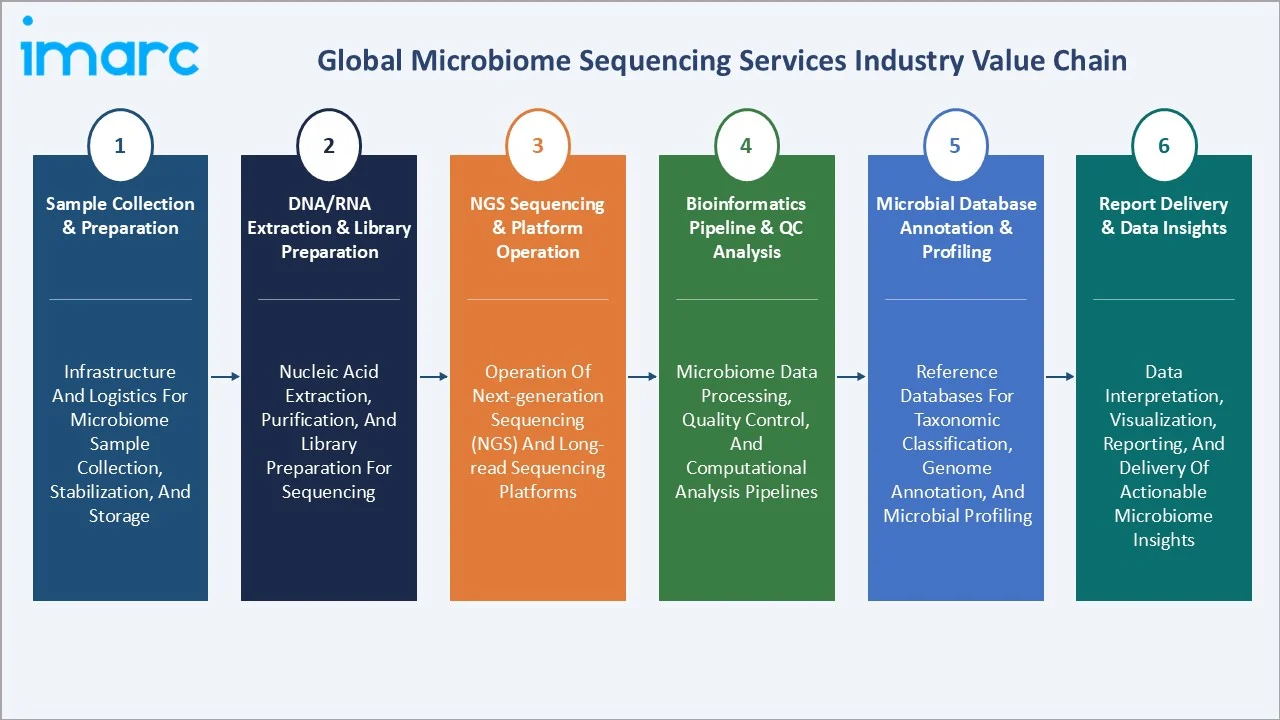

Industry Value Chain Analysis

The microbiome sequencing services value chain integrates sample collection and preparation, DNA/RNA extraction and library preparation, NGS sequencing and platform operation, bioinformatics pipeline and QC analysis, microbial database annotation and profiling, and report delivery and data insights.

| Stage | Key Participants |

|---|---|

| Sample Collection & Preparation | Infrastructure and logistics for microbiome sample collection, stabilization, and storage |

| DNA/RNA Extraction & Library Preparation | Nucleic acid extraction, purification, and library preparation for sequencing |

| NGS Sequencing & Platform Operation | Operation of next-generation sequencing (NGS) and long-read sequencing platforms |

| Bioinformatics Pipeline & QC Analysis | Microbiome data processing, quality control, and computational analysis pipelines |

| Microbial Database Annotation & Profiling | Reference databases for taxonomic classification, genome annotation, and microbial profiling |

| Report Delivery & Data Insights | Data interpretation, visualization, reporting, and delivery of actionable microbiome insights |

The bioinformatics pipeline and annotation tier is the value chain's highest-margin and most differentiated commercial tier. The sample collection and preparation tier is experiencing significant commercial innovation.

Technology Landscape in the Microbiome Sequencing Services Industry

Short-Read NGS Technology

Short-read next-generation sequencing (NGS) technology provides high-throughput, accurate, and cost-effective profiling of microbial communities. Its ability to rapidly sequence millions of DNA fragments allows comprehensive analysis of microbial diversity and abundance. This technology forms the backbone of many microbiome research and clinical studies, supporting large-scale projects, enabling comparative analyses, and driving the expansion of sequencing service offerings in both research and healthcare applications.

Long-Read Sequencing Technology

Long-read sequencing technology enables the assembly of complete microbial genomes and the resolution of complex genomic regions that short-read methods cannot accurately capture. This technology allows for strain-level identification, detection of structural variations, and improved characterization of microbial communities. In July 2025, Qiagen introduced its new QIAseq xHYB Long Read Panels, a set of target enrichment solutions designed to facilitate long-read sequencing of genomically complex regions. By providing deeper and more precise insights into microbial diversity and function, long-read sequencing supports advanced research, therapeutic development, and high-resolution microbiome analysis, driving innovation and differentiation in sequencing service offerings.

Targeted Microbiome Amplicon Sequencing

Targeted microbiome amplicon sequencing focusing on specific marker genes, such as 16S rRNA, to efficiently profile microbial communities. This approach allows for cost-effective, high-throughput analysis of microbial diversity, composition, and relative abundance. By providing precise, targeted insights with faster turnaround times, amplicon sequencing supports large-scale studies, biomarker discovery, and clinical research, making it a cornerstone technology in microbiome analysis services.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

🔒 |

🔒 |

2025 |

|

Research Type |

Outsourced Research |

63.7% |

2025 |

|

Laboratory Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

Pharmaceutical and Biotechnology Companies |

54.2% |

2025 |

|

Region |

North America |

39.4% |

2025 |

By Research Type

Outsourced research leads at 63.7% market share (2025). Outsourced research encompasses all microbiome sequencing services contracted to external providers, full-service genomics companies, specialist microbiome sequencing CROs, clinical reference laboratories, and bioinformatics-only services. The outsourced segment's commercial dominance reflects pharmaceutical industry CRO model adoption for all non-proprietary technical services and academic institution dependency on shared sequencing core facilities and external specialist service providers.

To access detailed market analysis, Request Sample

Internal research at 36.3% encompasses microbiome sequencing performed on internally owned NGS instruments by organizational staff scientists at pharmaceutical companies, major academic institutions, and national genomics centres.

By End User

Pharmaceutical and biotechnology companies lead at 54.2% (2025). Pharma and biotech end users generate the highest revenue per project engagement. The pharmaceutical end user segment is growing fastest at ~16.8% CAGR through new microbiome drug programme initiations, broader pharmaceutical industry microbiome biomarker adoption across immunology, oncology, neurology, and metabolic disease therapeutic areas, and growing regulatory requirements for microbiome characterization in clinical development.

Research and academic institutes at 31.8% generate high volume but lower per-project revenue compared to pharmaceutical end users. Others at 14.0% includes clinical diagnostic microbiome testing, food safety microbiome QC, environmental monitoring, and direct-to-consumer microbiome health testing, collectively representing the broadening application landscape beyond traditional research.

Regional Market Insights

| Region | Share (2025) | Key Microbiome Sequencing Services Market Drivers & Characteristics |

|---|---|---|

| North America | 39.4% | Driven by advanced research infrastructure, high R&D investment, and widespread adoption of next-generation sequencing technologies |

| Europe | 25.8% | Supported by established pharmaceutical and biotech sectors, regulatory support, and growing microbiome research initiatives |

| Asia-Pacific | 23.1% | Driven by expanding healthcare research, increasing investment in biotechnology, and rising awareness of microbiome-based therapeutics |

| Latin America | 6.4% | Fueled by improving research infrastructure and emerging microbiome-focused studies |

| Middle East and Africa | 5.3% | The MEA market is the smallest by share but is experiencing above-average growth due to developing healthcare research capabilities and rising government support for biotechnology |

North America, at 39.4%, leads through NIH microbiome research infrastructure, FDA-approved market validation, and the world's highest pharmaceutical microbiome drug development concentration. Europe, at 25.8%, reflects European funding and European microbiome academic excellence.

Asia Pacific, at 23.1%, is the fastest-growing region through competitive cost structure and China, Japan, and Australia's growing microbiome research programmes. Latin America, at 6.4%, reflects Brazil's genomics excellence and distinctive microbiome cohort research value. MEA, at 5.3%, encompasses the regional institutes' microbiome excellence and Saudi Vision 2030 medical investment.

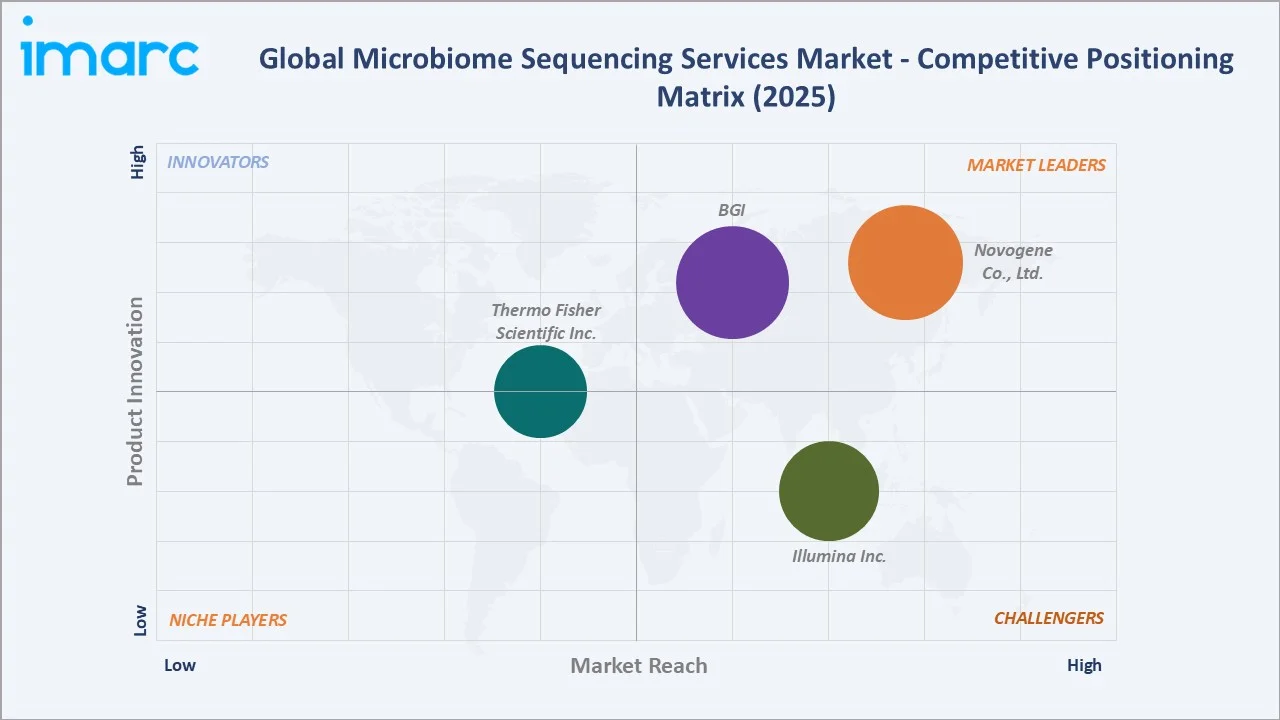

Competitive Landscape

The microbiome sequencing services market's competitive landscape is structured across three tiers: volume-based commodity sequencing providers, technology platform companies enabling the service ecosystem, and specialist analytics and clinical service providers. The competitive dynamics are being disrupted by the convergence of decreasing sequencing cost and increasing analytical complexity.

| Company Name | Key Services | Market Position | Core Strength |

|---|---|---|---|

| Novogene Co., Ltd. | 16S/18S/ITS Amplicon Sequencing, Shotgun Metagenomic Sequencing | Market Leader | Novogene Co., Ltd. is playing a key role in microbiome research by offering comprehensive, high-throughput, and cost-effective sequencing solutions |

| BGI | 16S/18S/ITS Sequencing, Metagenomic Sequencing | Market Leader | BGI acts as a major global provider of microbiome sequencing services, leveraging proprietary high-throughput sequencing technologies (DNBSEQ) to map microbial communities for academic, clinical, and environmental research |

| Illumina Inc. | Shotgun metagenomic sequencing, 16S rRNA sequencing, Microbial metatranscriptomics | Challenger | Illumina, Inc. is serving as the industry standard for microbiome research. They provide end-to-end sequencing solutions for 16S rRNA, metagenomics, and metatranscriptomics |

| Thermo Fisher Scientific Inc. | Shotgun metagenomic sequencing, 16S rRNA sequencing | Established Player | Thermo Fisher Scientific Inc. provides end-to-end microbiome sequencing solutions for fast, scalable metagenomic analysis |

The competitive boundary between the microbiome sequencing service market and the pharmaceutical tools and technology market is blurring through strategic partnerships.

Key Company Profiles

Novogene Co., Ltd.

Novogene Co., Ltd. is a leading global provider of genomic and bioinformatics services, with strong capabilities in high‑throughput sequencing and microbiome analysis. Leveraging robust next‑generation sequencing (NGS) infrastructure, advanced bioinformatics pipelines, and deep expertise in microbial genomics, Novogene delivers comprehensive microbiome sequencing solutions to academic institutions, pharmaceutical and biotechnology companies, and clinical research organizations.

- Key Services: 16S/18S/ITS Amplicon Sequencing, Shotgun Metagenomic Sequencing.

- Recent Developments: In June 2025, Novogene launched Novogene Korea Limited, a fully owned subsidiary based in Seoul. This strategic move strengthens Novogene’s long-term collaboration with Korea’s biomedical and biotech industries, demonstrating its commitment to providing rapid, high-quality, and cost-effective multi-omics services tailored to local research needs.

- Strategic Focus: Delivering high-throughput, cost-effective, and multi-omics sequencing solutions to accelerate research, biomarker discovery, and therapeutic development globally.

BGI

BGI is one of the world’s largest genomics organizations and a key player in the microbiome sequencing services market. With cutting‑edge sequencing platforms, comprehensive bioinformatics capabilities, and global service networks, BGI offers a wide range of microbiome sequencing solutions.

- Key Services: 16S/18S/ITS Sequencing, Metagenomic Sequencing.

- Recent Developments: In March 2026, BGI Genomics launched SIROmics, an AI-powered localized platform for high-throughput genetic testing that integrates laboratory automation with AI-assisted data analysis and reporting.

- Strategic Focus: Expanding global access to high-precision, scalable sequencing technologies that support multi-omics research and enable actionable insights for healthcare and biotechnology applications.

Market Concentration Analysis

The microbiome sequencing services market is moderately concentrated with a clear duopoly at the volume service tier and more fragmented in the analytics, clinical, and specialty service tiers. Market concentration reflects the capital intensity of NGS service operations. The concentration is declining through the forecast period as most of the platforms create equipment cost reduction that enables new entrants to establish competitive sequencing operations at lower capital thresholds. The regulatory scrutiny dynamic is actively reshaping market concentration in Western markets.

Investment & Growth Opportunities

Highest Growth Segments

Pharmaceutical and biotech end users (~16.8% CAGR), outsourced research (~16.6% CAGR), Asia Pacific regional market (~17-18% CAGR), clinical microbiome diagnostics (potentially 25-30% CAGR from growing base), AI-powered microbiome analytics (~30-40% CAGR from small base), long-read metagenomics premium service (~20-25% CAGR), multi-omics microbiome integration (~20% CAGR), wastewater epidemiology microbiome (~25% CAGR), and microbiome companion diagnostic mandated sequencing (potential step-change revenue on CDx approvals) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Regulatory-grade microbiome sequencing service platform development for pharmaceutical LBP companion diagnostic programmes represents the most commercially defensible investment opportunity.

Investment Themes

- Microbiome CDx service platform development for LBP drug companion diagnostics, creating a mandatory regulated sequencing market: The development of FDA-approved or FDA-cleared microbiome companion diagnostics for LBP therapeutics and future LBP drug approvals creates a mandatory sequencing market where every prescribed patient requires a regulated microbiome CDx test.

- AI microbiome drug target discovery platform services creating premium pharmaceutical analytics above sequencing commodity economics: Investment in AI microbiome analytics platforms that integrate metagenomics, metatranscriptomics, metabolomics, and clinical outcomes data to identify microbiome drug targets, predict microbiome-drug interactions, and discover microbiome biomarkers creates a premium pharmaceutical analytics tier.

Future Market Outlook (2026-2034)

The global microbiome sequencing services market is projected to grow from USD 3.05 Billion in 2025 to USD 12.13 Billion by 2034, delivering a 16.09% CAGR over the forecast period. The market's anchor value of USD 6.43 Billion in 2030 represents a microbiome sequencing services industry at its most commercially transformative inflection. Multiple additional LBP drug FDA approvals are anticipated in the 2026-2030 period for indications including graft-versus-host disease, inflammatory bowel disease, autism spectrum disorder gut-brain axis, and immuno-oncology microbiome adjuvants, each creating companion diagnostic development sequencing demand and post-approval mandatory CDx sequencing at commercial patient scale. These CDx-triggered mandatory sequencing markets will transform the industry's revenue model from discretionary research spending to regulated diagnostic necessity.

Three structural forces define the microbiome sequencing services market growth through 2034 with confidence. The pharmaceutical microbiome pipeline is entering its most commercially productive phase. The NGS cost curve continues declining predictably, each new generation of sequencing platform delivering 3-5x cost reduction versus the previous generation, creating new accessibility thresholds that expand the microbiome sequencing addressable market to institutions and applications previously excluded by cost. The microbiome science evidence base is compounding, each landmark publication linking specific microbiome features to disease outcomes creates new pharmaceutical drug discovery programmes that generate sustained sequencing service demand, and the rate of high-impact microbiome publication is accelerating as the field matures.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Chief Scientific Officers; Microbiome Programme Directors; NIH National Human Genome Research Institute microbiome research programme officers; regulatory reviewers; microbiome guideline working group; Bioinformatics Directors; Clinical Microbiome Laboratory Directors; and pharmaceutical microbiome biomarker leaders.

Secondary Research

Secondary research encompassed data publications; Live Biotherapeutic Products draft; Regulatory guidelines on quality, safety and efficacy requirements for live biotherapeutic products; company annual reports; Microbiome journal landmark publication meta-analysis; clinicaltrials.gov microbiome therapeutics clinical trial registry analysis; microbiome drug pipeline analysis. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a demand-side bottom-up model: (i) pharmaceutical microbiome sequencing demand; (ii) academic microbiome sequencing demand; (iii) emerging CDx and clinical diagnostic market modelling using LBP approval timeline projections and CDx market penetration assumptions. CAGR validated against microbiome tool and services forecast and sequencing market growth trajectories from investor guidance.

Microbiome Sequencing Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Sequencing By Synthesis (SBS), Sequencing by Ligation (SBL), Pyrosequencing, Sanger Sequencing, Others |

| Research Types Covered | Outsourced Research, Internal Research |

| Laboratory Types Covered | Dry Labs, Wet Labs |

| Applications Covered | Shotgun Sequencing, Targeted Gene Sequencing, RNA Sequencing, Whole Genome Sequencing, Others |

| End Users Covered | Pharmaceutical and Biotechnology Companies, Research and Academic Institutes, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Novogene Co., Ltd., BGI, Illumina Inc., Thermo Fisher Scientific Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the microbiome sequencing services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global microbiome sequencing services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the microbiome sequencing services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Microbiome Sequencing Services Market Report

The global microbiome sequencing services market reached USD 3.05 Billion in 2025, driven by surging pharmaceutical microbiome drug discovery investment, the FDA approvals creating commercial LBP market validation motivating new pharmaceutical programme initiations, government microbiome research funding sustaining academic sequencing demand, continuous NGS cost reduction expanding accessible applications, and Asia Pacific service provider expansion, democratizing global microbiome research access.

The market grows at 16.09% CAGR during 2026-2034, reaching USD 12.13 Billion by 2034. Growth reflects pharmaceutical microbiome drug pipeline expansion, NGS cost reduction expanding accessible applications, AI microbiome drug target discovery platforms generating premium analytics service demand, clinical microbiome diagnostic adoption in gastroenterology and oncology, wastewater epidemiology institutionalization, and Asia Pacific pharmaceutical CRO outsourcing growth.

Outsourced research leads at 63.7% through pharmaceutical and academic preference for specialist microbiome CRO services over capital-intensive in-house NGS infrastructure, driven by scale cost advantages, specialist bioinformatics expertise, and project-based demand that does not justify dedicated platform investment. Outsourced research also grows fastest at ~16.6% CAGR, reflecting pharmaceutical industry CRO adoption trends extending to microbiome sequencing.

Pharmaceutical and biotechnology companies lead at 54.2% and grow fastest at ~16.8% CAGR through LBP clinical trial microbiome sequencing requirements, pharmaceutical microbiome biomarker programmes across immuno-oncology, IBD, and neuroscience therapeutic areas, and growing regulatory requirements for microbiome characterization in LBP development.

North America leads at 39.4% through FDA-approved LBP market validation, the world's highest pharmaceutical microbiome programme concentration, and US academic microbiome research excellence.

Leading companies include Novogene Co., Ltd., BGI, Illumina Inc., and Thermo Fisher Scientific Inc., among others.

The market is projected to reach approximately USD 6.43 Billion by 2030, with multiple additional LBP FDA approvals anticipated, creating companion diagnostic development sequencing demand, long-read metagenomics achieving cost parity with short-read metagenomics at scale service providers, wastewater epidemiology microbiome sequencing growth, AI microbiome analytics platforms achieving pharmaceutical partnership validation, and clinical microbiome diagnostics beginning insurance reimbursement for specific indications in major healthcare systems.

Three priority opportunities: microbiome companion diagnostic service platform for LBP drug programmes; AI microbiome drug target discovery platform services for pharmaceutical analytics; and Western market sequencing infrastructure to capture BGI regulatory risk-driven market share transfer.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)