Microgreens Market Size, Share, Trends and Forecast by Type, Farming Method, End Use, Distribution Channel, and Region, 2026-2034

Global Microgreens Market Size, Share, Trends & Forecast (2026-2034)

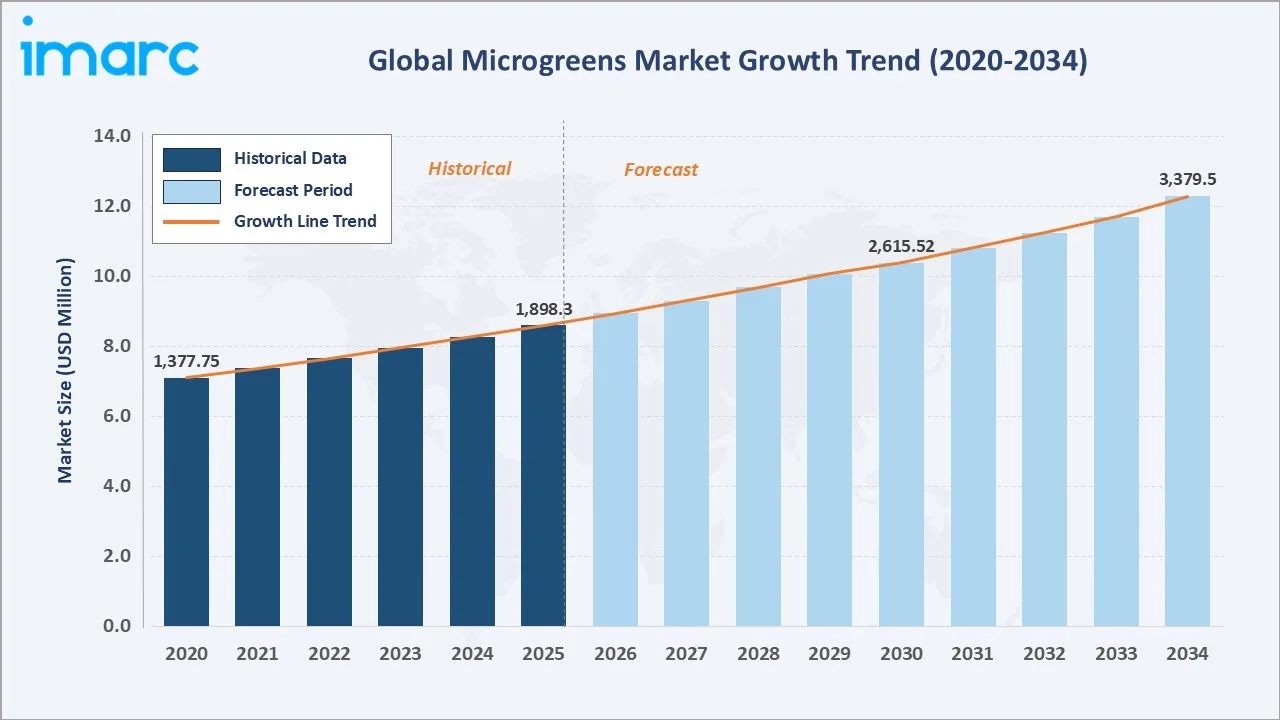

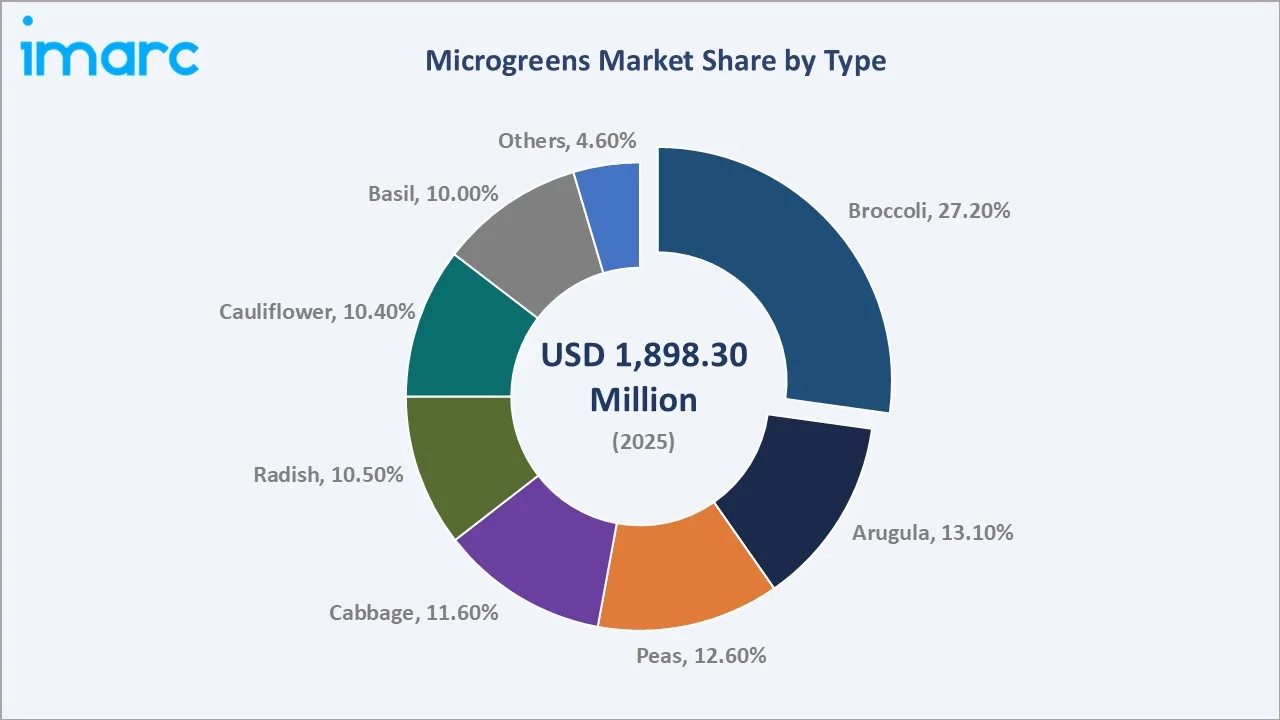

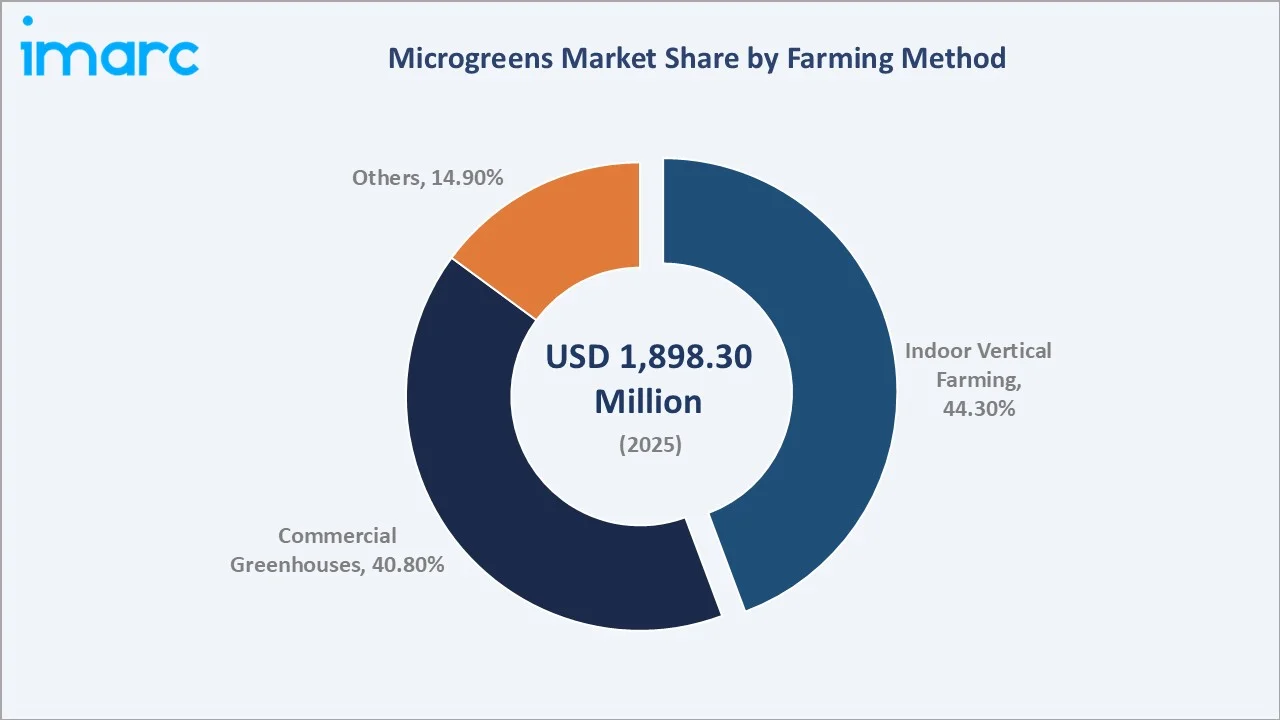

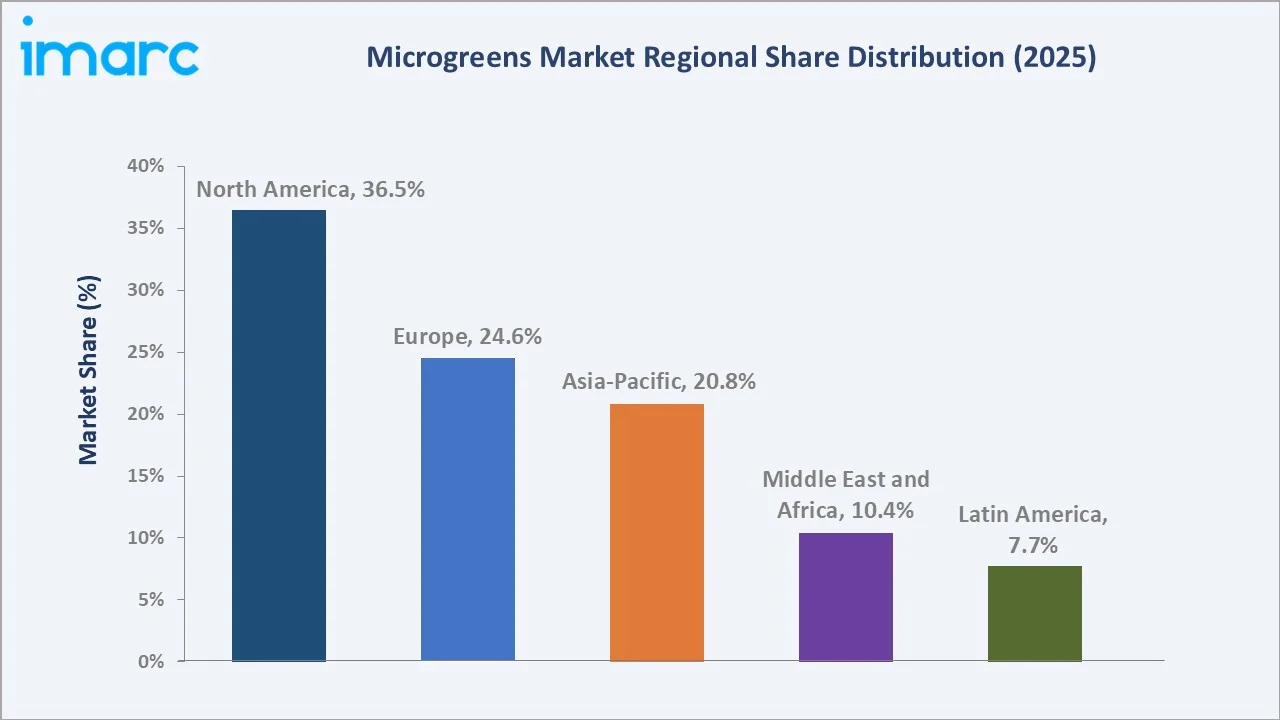

The global microgreens market size reached USD 1,898.30 Million in 2025 and is projected to reach USD 3,379.50 Million by 2034, exhibiting a CAGR of 6.62% during the forecast period 2026-2034. Rising health consciousness, expanding indoor vertical farming adoption, flourishing gourmet foodservice channels, and growing plant-based dietary trends are collectively fuelling microgreens market growth. According to the article published by ResearchGate, the online survey of 150 respondents aged 20–35 shows growing consumer acceptance of microgreens, with 100 respondents already aware of them and 64.6% expressing a liking of microgreens based on sensory evaluation. Broccoli leads the type segment with a 27.2% share in 2025, while indoor vertical farming commands a 44.3% farming method share. North America dominates regional revenue at 36.5% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,898.30 Million |

|

Forecast Market Size (2034) |

USD 3,379.50 Million |

|

CAGR (2026-2034) |

6.62% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~8.1%) |

|

Leading Type |

Broccoli (27.2%, 2025) |

|

Leading Farming Method |

Indoor Vertical Farming (44.3%, 2025) |

The global microgreens market growth trajectory from 2020 through 2034, showing a consistent historical expansion and an accelerating forecast underpinned by wellness food premiumization, agri-tech investment, and expanding chef and foodservice adoption globally.

To get more information on this market, Request Sample

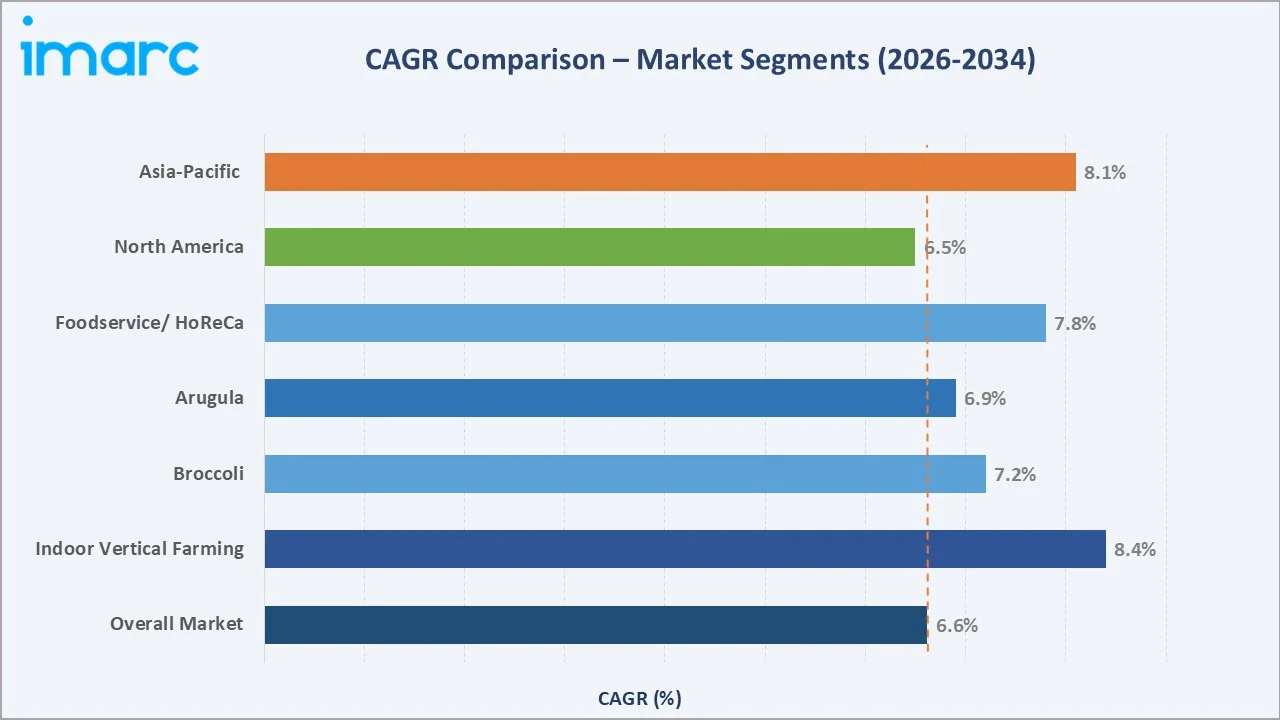

The CAGR trajectories across key type, farming method, and regional segments, with indoor vertical farming and Asia-Pacific emerging as the standout high-growth categories within the global microgreens industry analysis through 2034.

Executive Summary

The global microgreens market is experiencing consistent growth, shaped by a convergence of consumer health trends, agricultural technology innovation, and expanding culinary adoption. Valued at USD 1,898.30 Million in 2025, the market is set to reach USD 3,379.50 Million by 2034 at a CAGR of 6.62%. Microgreens harvested within 7-14 days of germination are documented to contain 4-40 times more nutrients than their mature counterparts.

Broccoli dominates the type segment at 27.2% in 2025, driven by its well-documented sulforaphane content, a compound studied for anti-inflammatory and anti-cancer properties by the Johns Hopkins School of Medicine. Arugula follows at 13.1% in 2025, popular in gourmet applications for its peppery flavour. Indoor vertical farming holds a commanding 44.3% farming method share in 2025.

North America leads regional demand at 36.5% in 2025, anchored by robust retail health food infrastructure and a deeply embedded farm-to-table restaurant culture. Key market participants include AeroFarms, Bright Farms, Little Leaf Farms, Gotham Greens, AppHarvest, Shenandoah Growers, and True Leaf Market.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Broccoli - 27.2% share (2025) |

|

Leading Farming Method |

Indoor Vertical Farming - 44.3% share (2025) |

|

Leading Region |

North America - 36.5% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific - CAGR ~8.1% (2026-2034) |

|

Top Companies |

AeroFarms, Bright Farms, Little Leaf Farms, Gotham Greens, AppHarvest |

Key Analytical Observations Supporting the Above Data:

- Broccoli leads with 27.2% of the microgreens type market in 2025. Broccoli microgreens contain 10-100 times more sulforaphane than mature broccoli heads, making them one of the most studied and nutritionally marketed microgreen varieties.

- Indoor vertical farming's 44.3% share in 2025 reflects a structural shift in how microgreens are produced.

- North America leads regional demand at 36.5% in 2025, driven by the US health food market. Whole Foods Market, Sprouts Farmers Market, and Direct-to-Consumer platforms like FreshDirect list microgreens prominently.

- Asia-Pacific's fastest-growing regional CAGR of ~8.1% through 2034reflects rising middle-class health consciousness in China, Japan, South Korea, and India.

Global Microgreens Market Overview

Microgreens are young vegetable greens harvested immediately after the first true leaves emerge, typically 7-14 days after germination. Distinct from sprouts (grown in water) and baby greens (older harvests), microgreens are grown in soil or hydroponic substrates under LED lighting in controlled environments.

They span species including brassicas (broccoli, cabbage, radish), herbs (basil, cilantro), legumes (peas), and leafy greens (arugula, sunflower). Applications extend across fresh produce retail, gourmet and fine-dining restaurant garnishing, smoothie and juice bars, hospital nutrition programmes, school meal plans, and food manufacturer ingredient supply.

Macroeconomic enablers, rising urbanization driving demand for locally grown fresh produce, the global plant-based food market, and climate resilience concerns are accelerating investment in controlled-environment agriculture as a food security strategy.

Market Dynamics

To evaluate market opportunities, Request Sample

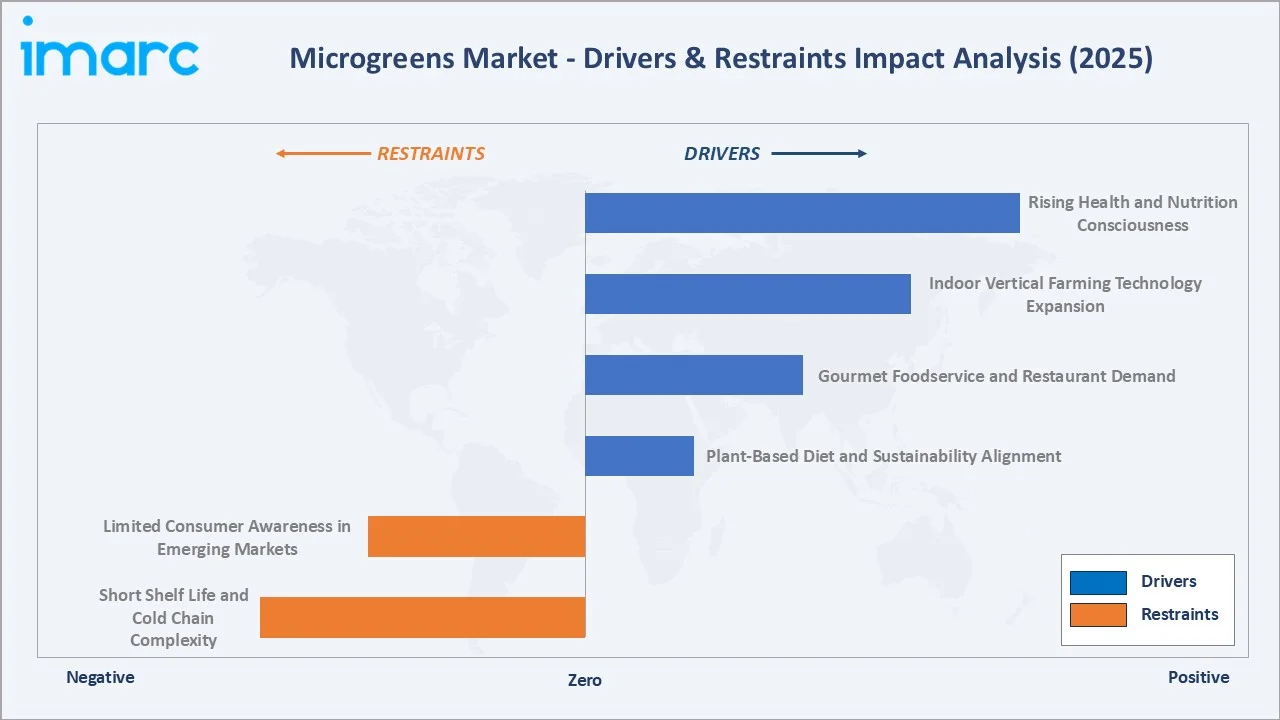

Market Drivers

- Rising Health and Nutrition Consciousness: The global wellness economy expanded by 7.9% between 2023 and 2024, reaching a record $6.8 trillion in 2024, and doubled in value since 2013. Microgreens are at the intersection of functional food, clean-label, and nutrient-density trends.

- Indoor Vertical Farming Technology Expansion: Companies like AeroFarms, Bowery Farming (Plenty) have deployed AI-driven grow systems that reduce production water use by 95%, eliminate pesticide requirements, and achieve crop cycles annually.

- Gourmet Foodservice and Restaurant Demand: Michelin-starred restaurants across New York, London, Tokyo, and Paris routinely feature microgreens as plating garnishes, salad bases, and flavour enhancers.

- Plant-Based Diet and Sustainability Alignment: Microgreens are naturally plant-based, require minimal land and water versus conventional crops, and align with USDA Dietary Guidelines for Americans (2020-2025), recommending greater vegetable and legume consumption.

Market Restraints

- Short Shelf Life and Cold Chain Complexity: Microgreens have a typical shelf life of 10-14 days post-harvest under refrigeration, versus 2-3 weeks for mature greens. This requires rapid farm-to-shelf logistics with consistent cold chain maintenance (34-38°F), creating distribution complexity and food waste risk.

- Limited Consumer Awareness in Emerging Markets: Despite strong growth trajectories, microgreens awareness in markets including India, Southeast Asia, and Latin America remains low outside urban premium consumer segments.

Market Opportunities

- Biofortified and Functional Microgreen Varieties: Research institutions, including Cornell University's AgriTech programme are developing microgreen varieties with enhanced levels of specific phytonutrients, selenium-enriched broccoli microgreens, high-anthocyanin purple basil, and omega-3-rich flaxseed microgreens.

- Direct-to-Consumer Subscription Services: Companies like Hamama (microgreen grow kits) and True Leaf Market report recurring subscriber growth, validating a DTC revenue model that bypasses traditional retail margin compression.

- Hospital, Healthcare, and Clinical Nutrition Channels: Clinical dietitians are increasingly incorporating microgreens into therapeutic nutrition programmes for immunocompromised patients, cancer recovery diets, and cardiovascular health management.

Market Challenges

- Food Safety and Contamination Risk: Microgreens' warm, humid growing environments create potential risk for Salmonella, E. coli, and Listeria contamination, similar to sprout food safety concerns.

- Energy Intensity of Indoor Farming: LED grow lights and HVAC systems for indoor vertical microgreen farms consume significant electrical energy.

Emerging Market Trends

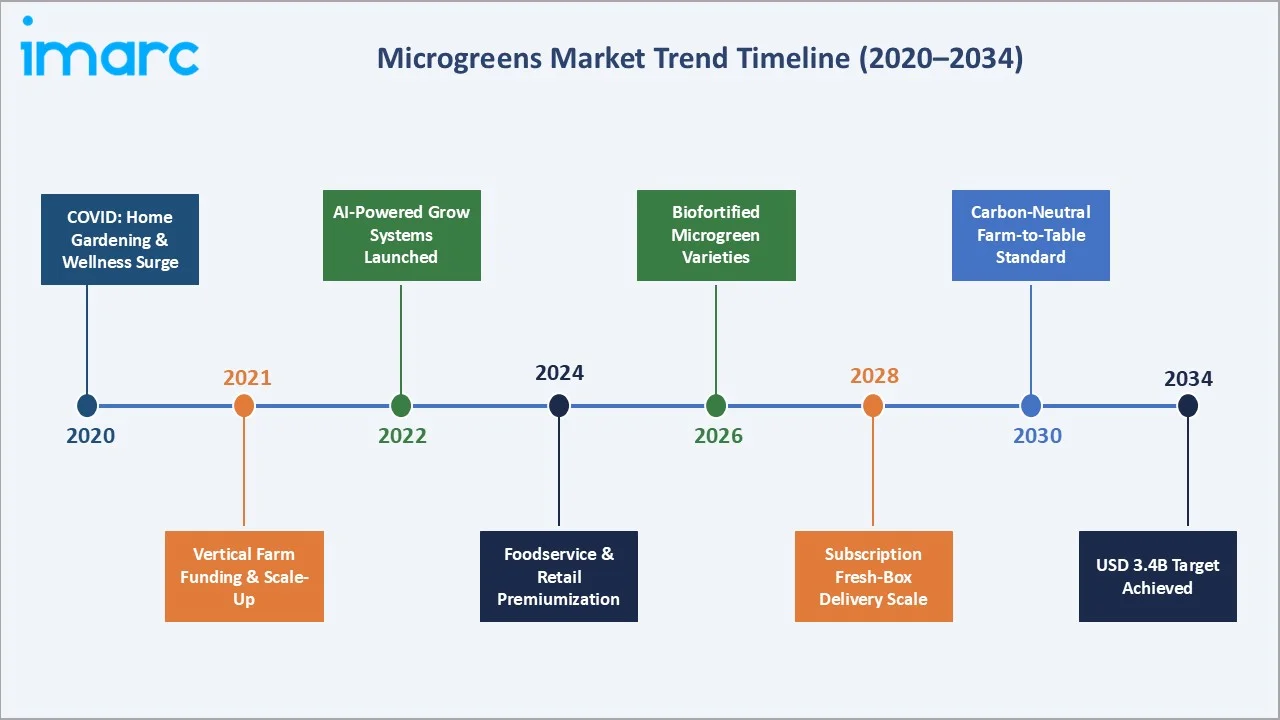

1. AI and IoT-Enabled Precision Indoor Farming

Vertical farm operators are deploying AI-driven climate management, computer vision crop monitoring, and IoT sensor networks to optimise microgreen yield, nutrient density, and energy efficiency simultaneously. Key components of Agriculture 4.0 include modern smart technologies such as robotics (including drones), big data, artificial intelligence, computer vision, 5G, cloud computing, the Internet of Things, and blockchain technology.

2. Retail Premiumization and Private-Label Microgreen Lines

Major grocery retailers are responding to microgreen demand by developing branded private-label lines. Whole Foods Market's 365 Everyday Value label, Trader Joe's seasonal microgreen offerings, and Marks & Spencer's Living Herb range in the UK reflect retailer investment in fresh microgreen category ownership.

3. Microgreens in Processed Food and Ingredient Applications

Beyond fresh produce, microgreens are emerging as functional ingredients in cold-pressed juices, smoothie pods, dried supplement blends, and baby food formulations.

4. Vertical Farm Consolidation and Strategic Partnerships

Following the capital market normalization post-2021 venture boom, the vertical farming industry is consolidating. AeroFarms completed Chapter 11 restructuring in 2023 and emerged under new ownership focused on profitability.

5. Subscription Growing Kits Democratising Home Production

Consumer microgreen growing kits, supplying seeds, growing medium, trays, and care instructions for home cultivation, are one of the market's fastest-growing segments. This trend extends the microgreen market beyond professional growing into consumer participation, building awareness and long-term purchase loyalty for fresh retail products.

Industry Value Chain Analysis

The microgreens industry value chain spans six stages from seed and input supply to end consumption. Each stage carries distinct margin profiles, technology requirements, and regulatory compliance obligations.

|

Stage |

Key Players / Examples |

|

Seed & Input Supply |

Johnny's Selected Seeds, True Leaf Market, High Mowing Organic Seeds, Premier Tech Horticulture (substrates) |

|

Cultivation & Farming |

AeroFarms, Bright Farms, Gotham Greens, Little Leaf Farms, Shenandoah Growers, AppHarvest |

|

Processing & Packaging |

Fresh Innovations LLC, Taylor Farms, Ready Pac Produce – washing, packing, clamshell/bag packaging |

|

Cold Chain & Logistics |

Lineage Logistics, Preferred Freezer (cold storage); cold truck carriers maintaining 34-38°F transit |

|

Retail & Distribution |

Whole Foods Market, Sprouts Farmers Market, Instacart, FreshDirect, Amazon Fresh, specialty grocers |

|

End Users |

Restaurant chefs, home consumers, juice bars, hospital nutrition programmes, food manufacturers |

Seed suppliers and indoor farming technology vendors capture the highest intellectual property value in the microgreen value chain, as proprietary seed varieties and automated grow system patents provide durable competitive advantages. Retail and direct-to-consumer channels capture significant margin, often 40-60% gross margin on packaged microgreens versus 15-25% for bulk foodservice supply.

Technology Landscape in the Microgreens Industry

LED Grow Light Optimization

Spectrally tuned LED grow lighting is the foundational technology for indoor microgreen farming. Full-spectrum LED arrays from Fluence (Signify), Gavita (ScottsMiracle-Gro), and Heliospectra enable precise light spectrum customization that modulates flavour compound development, anthocyanin production, and growth rate.

Hydroponic and Aeroponic Growing Media

While traditional soil-based growing media remain common, hydroponic (nutrient solution in inert substrate) and aeroponic (nutrient mist directly to roots) systems are gaining adoption for commercial microgreen production.

AI-Driven Crop Management and Yield Prediction

Machine learning platforms integrating camera-based crop imaging, IoT climate sensors, and growth-model algorithms are enabling yield prediction accuracy within 5% and automated anomaly detection for disease or nutrient deficiency.

Sustainable Packaging and Extended Shelf-Life Technologies

Modified atmosphere packaging (MAP) extends microgreen shelf life to 15 days, materially reducing distribution constraints and food waste. Biodegradable and compostable packaging from cornstarch-based biopolymers is growing in adoption among premium microgreen brands targeting eco-conscious consumers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Broccoli |

27.2% |

2025 |

|

Farming Method |

Indoor Vertical Farming |

44.3% |

2025 |

|

End Use |

Commercial |

🔒 |

2025 |

|

Distribution Channel |

Retail Stores |

42.6% |

2025 |

|

Region |

North America |

36.5% |

2025 |

By Type

Broccoli dominates the microgreens type segment at 27.2% in 2025, driven by its exceptional scientific credibility as a health food. Johns Hopkins University research demonstrating that 3-day-old broccoli sprouts harbor 20 to 50 times more sulforaphane potential than adult broccoli has generated sustained media coverage and dietitian endorsement. This scientific legitimacy justifies premium retail pricing, making broccoli microgreens the highest-revenue per unit type in most retail formats.

To access detailed market analysis, Request Sample

Arugula, with 13.1% in 2025, is the second-largest type by revenue, valued for its distinctive peppery flavour profile and versatility across both gourmet garnishing and everyday salad applications. Peas (12.6%) are gaining significant momentum in plant-based and high-protein diet applications. Radish microgreens (10.5%) are widely used in Asian cuisine and growing strongly in Asia-Pacific markets. The Others category (4.6%) includes sunflower, amaranth, wheatgrass, and cilantro microgreens, which are seeing niche but rapid growth in juice bar and functional food ingredient applications.

By Farming Method

Indoor vertical farming commands the majority of farming method share at 44.3% in 2025, a decisive structural shift from the greenhouse-dominant landscape. The vertical farms use up to 95% less water per kilogram of produce compared to conventional soil farming.

Commercial greenhouses with 40.8% in 2025 offer a cost-effective intermediate, providing climate protection and extended growing seasons with lower capital cost than full indoor vertical farms. Greenhouse-grown microgreens benefit from natural sunlight supplementation that reduces LED energy costs, making this method competitive for large-volume commodity microgreen production (peas, sunflower, radish) where per-unit value is lower than premium varieties. Others (14.9%) includes field-grown seasonal microgreens in temperate climates and the rapidly growing consumer home-growing kit segment.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.5% |

Health food retail maturity; farm-to-table restaurant culture; strong CEA investment ecosystem |

|

Europe |

24.6% |

Organic food premiumization; UK/Germany indoor farm investment; EU Farm-to-Fork strategy |

|

Asia-Pacific |

20.8% |

Rising urban health consciousness; Japan functional food culture; India & China emerging demand |

|

Middle East and Africa |

10.4% |

Year-round CEA viability; UAE/Saudi food security investment; soilless farming adoption |

|

Latin America |

7.7% |

Brazil organic food growth; Mexico urban farming projects; regional wellness food expansion |

North America leads with 36.5% of the global microgreens market in 2025. The United States accounts for the lion's share, driven by the health food retail market and significant venture-backed indoor farming infrastructure concentrated in New Jersey, California, and Virginia. In 2024, U.S. Agriculture Secretary Tom Vilsack announced that the U.S. Department of Agriculture allocated more than $270 million through cooperative agreements with state agriculture departments to enhance resilience in the mid-tier food supply chain and support stronger local and regional food systems, supporting small and mid-size microgreen producers.

Asia-Pacific, with 20.8% in 2025, is the fastest-growing region. In 2024, Japan’s food processing sector recorded a 3.9% rise in output value, reaching a total of $174 billion. India's urban organic food market is growing at 25-30% annually in major metros, creating emerging demand.

Competitive Landscape

The global microgreens market is moderately fragmented, with a small number of technology-forward indoor farming companies competing nationally and internationally alongside a large base of regional greenhouse operators and artisan urban farms.

|

Company Name |

Key Brand / Platform |

Market Position |

Strategic Focus |

|

AeroFarms |

AeroFarms Microgreens |

Leader |

Aeroponic vertical farming; national retail & foodservice |

|

2BFresh |

2BFresh Microgreens |

Emerging |

Premium fresh-cut microgreens; local distribution; chef-focused supply |

|

80 Acres Farms |

Infinite Acres / 80 Acres Farms |

Leader |

Indoor vertical farming; AI & automation; retail partnerships |

|

Badia Farms |

Badia Microgreens |

Challenger |

UAE-based indoor farming; premium hospitality supply; controlled environment agriculture |

|

Farm.One Inc. |

Farm.One |

Emerging |

Hyper-local indoor farms; direct chef supply; urban agriculture model |

|

Farmbox Greens (Charlie's Produce) |

Farmbox Greens |

Challenger |

Retail-ready microgreens; West Coast distribution; foodservice partnerships |

|

Fresh Origins |

Fresh Origins Microgreens |

Leader |

Culinary microgreens; strong chef network; premium garnish segment |

|

GoodLeaf Farms (True Leaf) |

GoodLeaf Farms |

Challenger |

Vertical farming; pesticide-free greens; Canadian retail expansion |

|

Greeneration |

Greeneration Microgreens |

Emerging |

Sustainable microgreens; local farming; eco-friendly production |

|

Ibiza Microgreens |

Ibiza Microgreens |

Emerging |

Boutique microgreens supplier; hospitality & premium retail focus |

The competitive positioning of key global microgreens market participants across market presence and strategic investment dimensions in 2025.

Key Company Profiles

AeroFarms

AeroFarms is a US-based commercial-scale indoor vertical farming company headquartered in Newark, New Jersey. Founded in 2004, AeroFarms pioneered the commercial aeroponic growing system that delivers nutrients directly to plant roots via fine mist, claiming 95% water use reduction and 390x higher productivity per square foot versus field farming.

- Product Portfolio: AeroFarms produces a range of packaged microgreens, including broccoli, arugula, kale, super mix, wasabi mustard, micro rainbow mix.

- Recent Developments: In October 2026, AeroFarms announced new third-party research validating the extraordinary nutritional value of the company’s Micro Broccoli.

- Strategic Focus: AeroFarms is refocusing its strategy on operational profitability, reduction of per-unit energy costs through LED efficiency investments, and licensing its aeroponic technology to international partners in water-scarce markets including the Middle East and Southeast Asia.

80 Acres Farms

80 Acres Farms is a leading U.S. indoor farming company specializing in fully automated vertical farming systems. It operates multiple large-scale indoor farms and is closely linked with its technology arm, Infinite Acres.

- Product Portfolio: Offers microgreens, such as broccoli, arugula, micro-topia, super punch.

- Recent Developments: In January 2026, 80 Acres Farms expanded the availability of its microgreens to additional grocery stores across the United States, further advancing its nationwide growth and deepening partnerships with retail distributors.

- Strategic Focus: Heavy investment in AI-driven growing systems, robotics, and scalable indoor farming infrastructure to achieve consistent quality and national distribution.

Fresh Origins

Fresh Origins is a California-based company recognized as a global leader in gourmet microgreens and edible flowers, primarily serving the culinary industry.

- Product Portfolio: Specializes in microgreens, petite greens, edible flowers, and specialty garnishes tailored for fine dining.

- Recent Developments: In July 2024, Fresh Origins reported rising consumer demand for its Micro Cilantro and Micro Rainbow Mix products.

- Strategic Focus: Focuses on innovation in flavor, color, and texture, positioning itself as a premium brand for chefs rather than mass retail markets.

Market Concentration Analysis

The global microgreens market is moderately fragmented. The top 5 organized commercial-scale operators collectively account for approximately 18-25% of total global market revenue in 2025, with the remaining 75-82% distributed across regional greenhouse operators, artisan urban farms, home kit sellers, and emerging market producers.

The fragmented market structure reflects microgreens' geographic perishability constraint; the 10-15 day shelf life effectively limits each producer to a regional distribution radius, preventing any single operator from dominating national or global share. This fragmentation is both a market characteristic and a consolidation opportunity: operators that solve shelf-life extension through MAP technology or freeze-drying can expand geographically and capture disproportionate market share.

Investment & Growth Opportunities

Fastest-Growing Segments

Indoor vertical farming at ~8.4% CAGR through 2034 is the highest-growth operational sub-segment. Biofortified microgreen varieties, currently at research-to-commercial stage, represent the next premium product innovation tier, targeting clinical nutrition and pharmaceutical-adjacent positioning at USD 15-25 per ounce price points.

Emerging Markets

Middle East and Africa (10.4%, 2025) is growing at ~7.5% CAGR, above the global average, driven by Gulf state food security investment. UAE's National Food Security Strategy 2051 and Saudi Arabia's Vision 2030 both identify CEA as a priority technology for reducing the region's food import dependence.

Venture & Investment Trends

Global agri-tech venture investment in controlled-environment agriculture, with microgreen and leafy green producers among the primary beneficiaries. Direct-to-consumer microgreen kit companies attracted significant seed and Series A investment in 2023-2024, Back to the Roots secured USD 15 Million in Series D funding in 2023.

Future Market Outlook (2026-2034)

The global microgreens market forecast projects expansion from USD 1,898.30 Million in 2025 to USD 3,379.50 Million by 2034 at a CAGR of 6.62%, nearly doubling in value over the forecast period. The market's growth trajectory is underpinned by structural health food demand trends, technology cost curves in indoor farming, and expanding global fresh food retail infrastructure.

Bioprinting and precision fermentation technologies may enable microgreen-derived phytonutrient production without the growing process by 2030-2034, a potential disruption to traditional cultivation-based supply chains. Shorter term, CRISPR-enabled crop variety development for microgreens, targeting higher nutrient density, longer shelf life (10-14 days), and pathogen resistance, is expected to produce commercial varieties from 2027-2030, improving the economics of indoor microgreen production significantly.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews with indoor farm operators, commercial greenhouse managers, specialty produce buyers at major retail chains, foodservice purchasing directors, and investment professionals active in the agri-tech sector. Primary insights validated market sizing, type and farming method segmentation splits, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include USDA Agricultural Research Service microgreen nutrient studies (2012, 2021), AgFunder Annual AgriFood Tech Investment Report (2023-2024), Nutrition Business Journal Natural/Organic Sector Report (2024), FAO Global Food Systems data, EU Farm-to-Fork Strategy documentation, USDA LAMP programme data, and trade publications including The Packer, Produce Business, and Controlled Environment Agriculture magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Microgreens Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Broccoli, Cabbage, Cauliflower, Arugula, Peas, Basil, Radish, Others |

| Farming Methods Covered | Indoor Vertical Farming, Commercial Greenhouses, Others |

| End Uses Covered | Residential, Commercial |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Retail Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AeroFarms, 2BFresh, 80 Acres Farms, Badia Farms, Farm.One Inc., Farmbox Greens (Charlie's Produce), Fresh Origins, GoodLeaf Farms (True Leaf), Greeneration, Ibiza Microgreens, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecast, and dynamics of the microgreens market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global microgreens market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the microgreens industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Microgreens Market Report

The global microgreens market reached USD 1,898.30 Million in 2025.

The market is projected to reach USD 3,379.50 Million by 2034, growing at a CAGR of 6.62% during 2026-2034, driven by indoor farming technology, foodservice demand, and expanding consumer health consciousness.

Broccoli leads with a 27.2% type share in 2025, underpinned by documented sulforaphane content, up to 100 times higher than mature broccoli, driving strong demand from health-focused retail consumers.

Indoor vertical farming dominates with a 44.3% share in 2025, enabling year-round production with 95% water savings versus field farming and 26+ annual crop cycles from the same footprint.

North America leads with a 36.5% revenue share in 2025, driven by the USD 200 Billion US health food retail market, strong farm-to-table restaurant culture, and robust venture-backed indoor farming infrastructure.

Asia-Pacific is the fastest-growing region at ~8.1% CAGR through 2034, driven by Japan's functional food market, South Korea's Smart Farm programme, and rising urban health consciousness in China and India.

Key drivers include documented 4-40x higher nutrient density versus mature crops (USDA, 2012), indoor vertical farming adoption, gourmet foodservice demand (global USD 3.9 Trillion market), and plant-based diet alignment.

Leading companies include 2BFresh, 80 Acres Farms, AeroFarms, Badia Farms, Farm.One Inc., Farmbox Greens (Charlie's Produce), Fresh Origins, GoodLeaf Farms (True Leaf), Greeneration, Ibiza Microgreens, Living Earth Farm, Metro Microgreens, The Chef's Garden Inc., etc.

USDA Agricultural Research Service research (2012) found microgreens contain 4-40 times more nutrients than mature counterparts, including vitamins C, E, K, and beta-carotene, supporting strong premium pricing in health food channels.

Microgreens typically last 10-15 days post-harvest under refrigeration, requiring rapid farm-to-shelf cold chain logistics at 34-38°F. Modified atmosphere packaging can extend shelf life to 10-14 days, improving distribution economics.

Indoor vertical farming enables year-round production, eliminates weather risk, reduces water use by 95%, and allows nutrient density optimization via controlled light spectrum, driving its 44.3% market share and ~8.4% CAGR through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)