Middle East Renewable Energy Market Size, Share, Trends, and Forecast by Type, End User, and Country, 2026-2034

Middle East Renewable Energy Market Size, Share, Trends & Forecast (2026-2034)

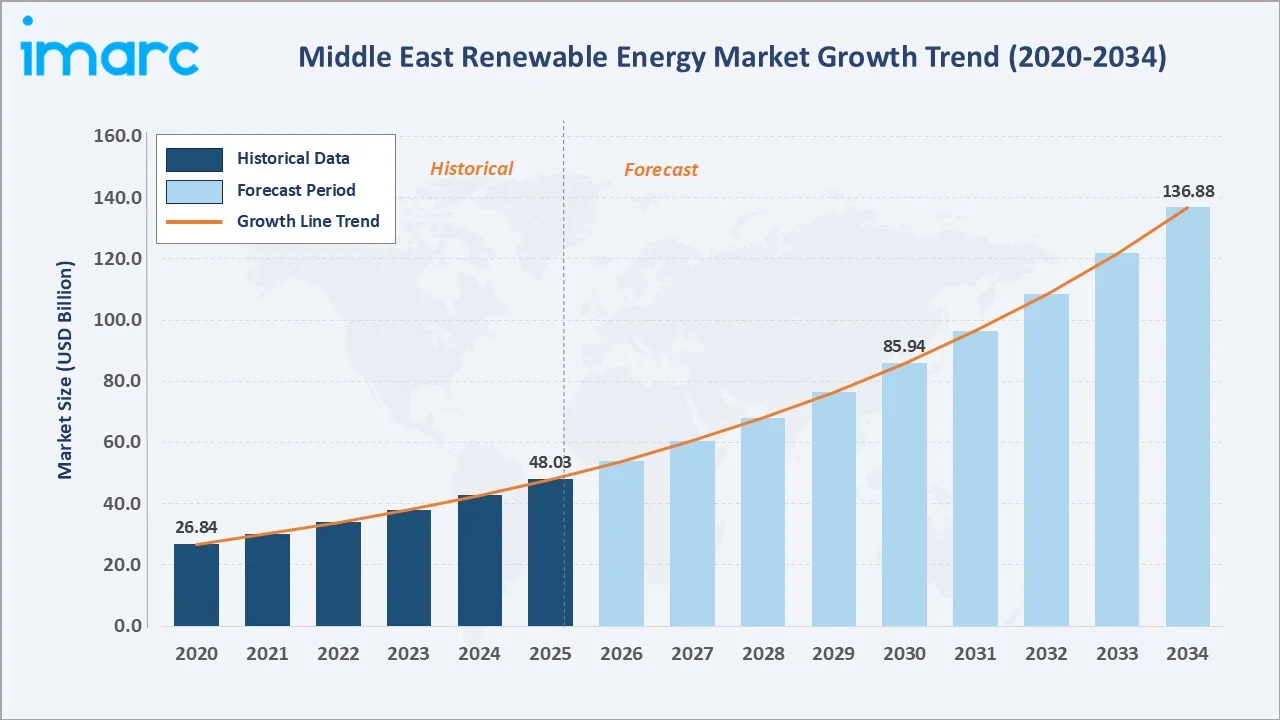

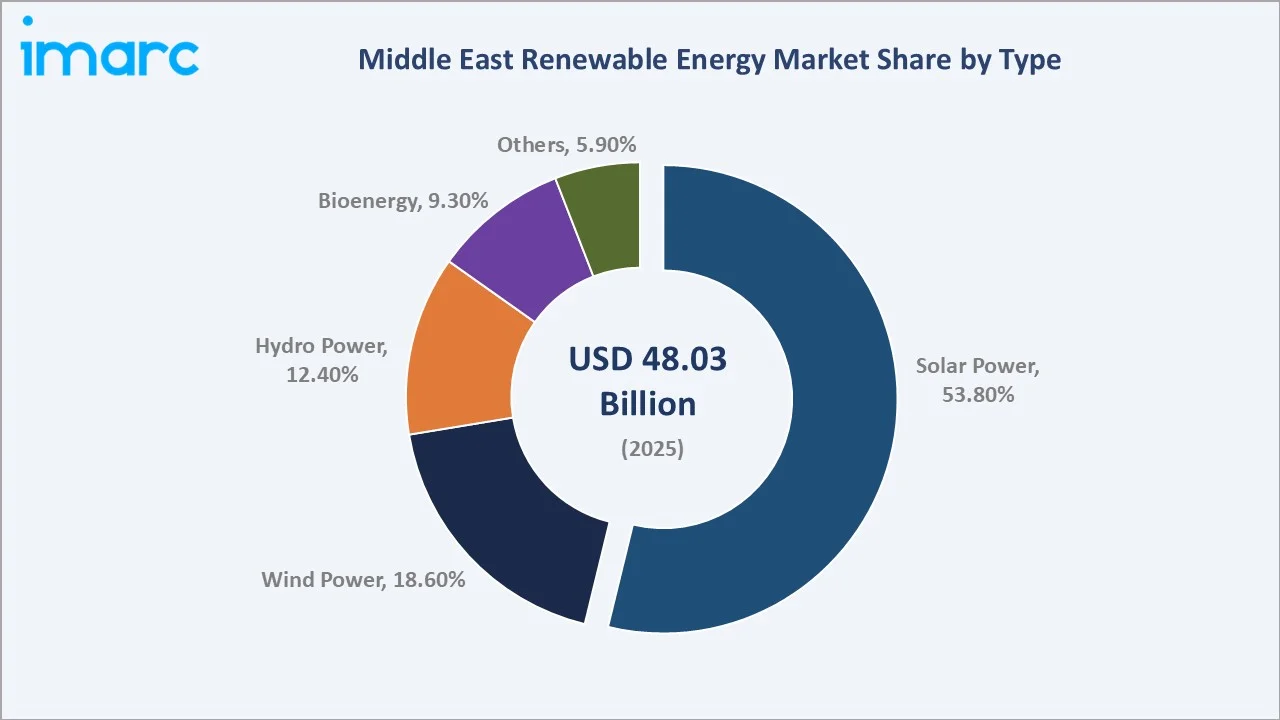

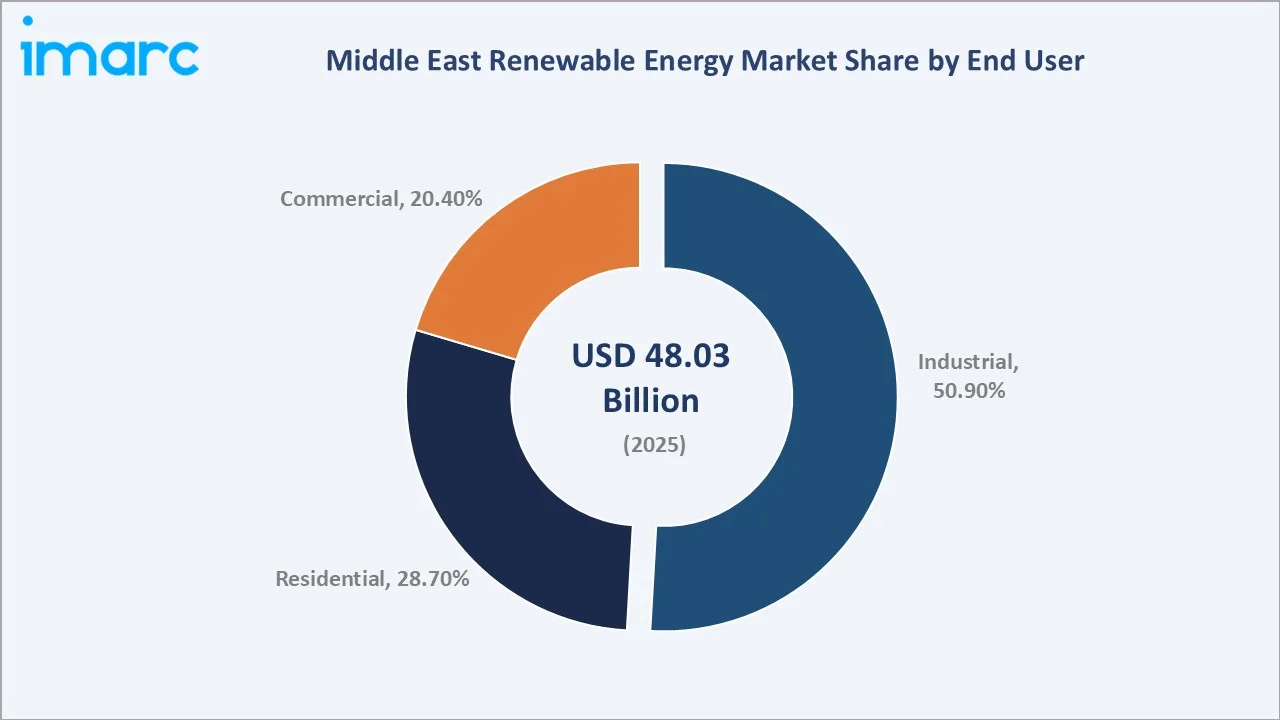

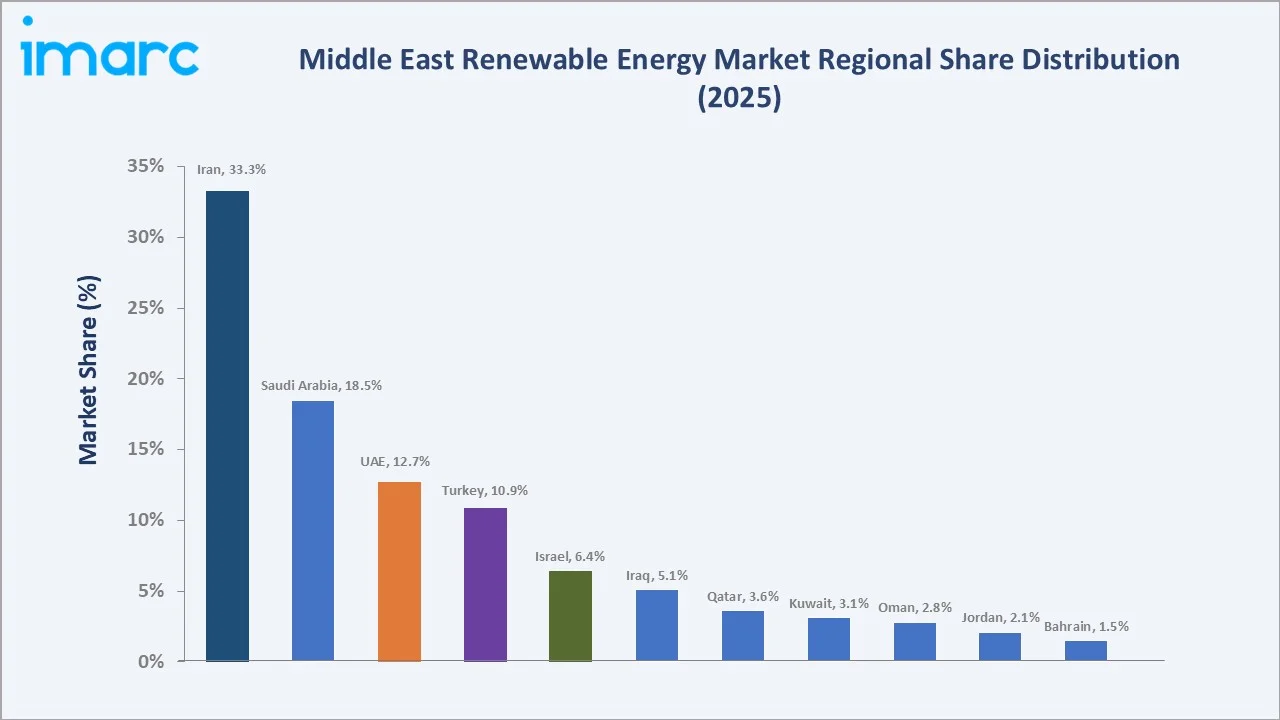

The Middle East renewable energy market was valued at USD 48.03 Billion in 2025 and is projected to reach USD 136.88 Billion by 2034, expanding at a CAGR of 12.34% during the forecast period (2026-2034). Growth is driven by ambitious national Vision programs such as Saudi Vision 2030, UAE Net Zero 2050, combined with record-low solar LCOE in the GCC region and accelerating green hydrogen export corridor development. Solar power dominates at 53.8% of the market share (2025), while the industrial end user leads at 50.9%. Iran holds the largest country share at 33.3%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 48.03 Billion |

|

Forecast Market Size (2034) |

USD 136.88 Billion |

|

CAGR (2026-2034) |

12.34% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Iran (33.3% share, 2025) |

|

Fastest Growing Country |

Saudi Arabia (CAGR ~18.5%) |

The Middle East renewable energy market expanded from USD 26.84 Billion in 2020 to USD 48.03 Billion in 2025, driven by rapid solar deployment, record-low power purchase agreement (PPA) tariffs, and unprecedented government capital commitments. The market is forecast to reach USD 85.94 Billion by 2030 before nearly tripling the 2020 baseline to reach USD 136.88 Billion by 2034.

To get more information on this market, Request Sample

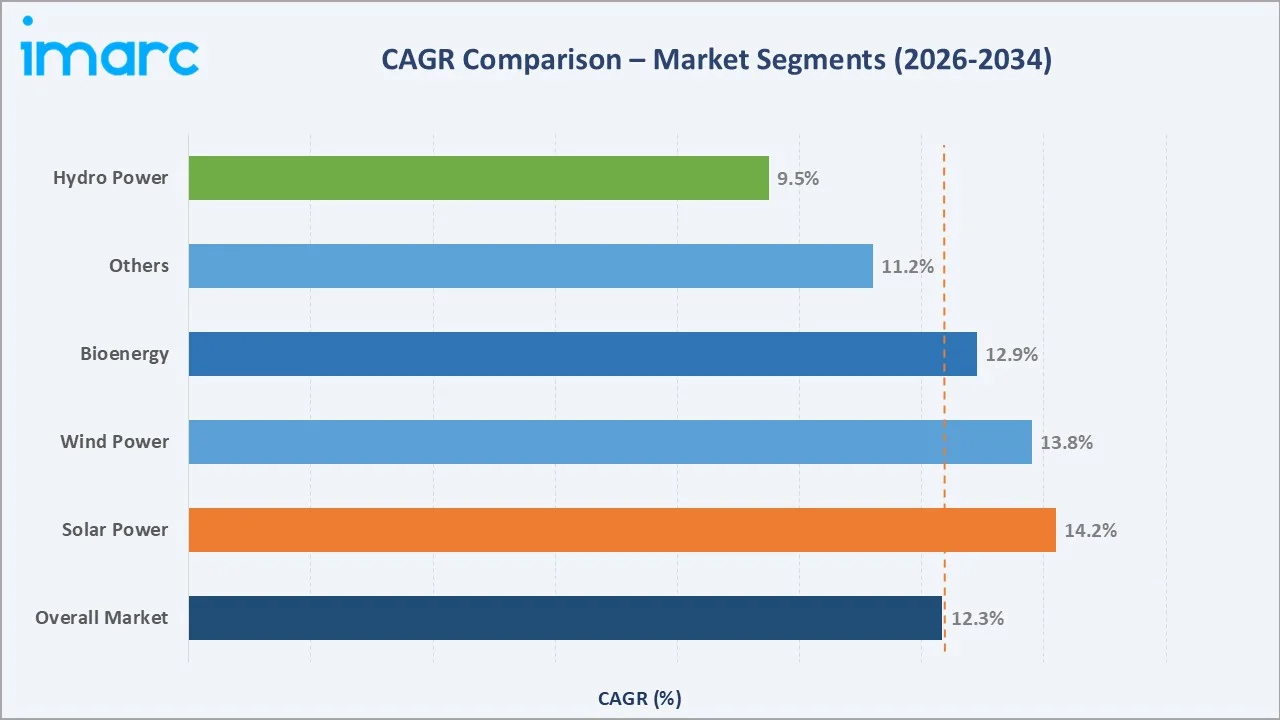

The CAGR across energy type segments with solar power leads at ~14.2% CAGR, leveraging irradiation levels across the Arabian Peninsula and world-record PPA prices in the UAE and Saudi Arabia. Wind power at ~13.8% CAGR benefits from Turkey’s extensive Aegean coast resource base, Saudi Arabia’s developing northwest wind corridor, and Oman’s Dhofar region potential through 2034.

Executive Summary

The Middle East renewable energy market is undergoing the most consequential energy transition in the region’s modern history. From USD 26.84 Billion in 2020, the market reached USD 48.03 Billion in 2025, driven by Gulf Cooperation Council (GCC) countries’ energy diversification mandates, post-COVID energy security imperatives, and the extraordinary competitive advantage the region holds in solar energy. The forecast to USD 136.88 Billion by 2034 represents a 2.85× market expansion from 2025 levels, anchored by the region’s sovereign wealth fund-backed investment programs, government-to-government energy partnerships, and the emerging green hydrogen export economy that requires massive dedicated renewable capacity.

Solar power dominates at 53.8% of market revenue (2025), reflecting the GCC’s extraordinary solar resource that delivers the world’s most competitive solar electricity costs. Wind power at 18.6% is growing rapidly in Turkey, and in the emerging offshore wind programs of the GCC and Red Sea corridor.

Iran’s 33.3% market share (2025) reflects the country’s large existing hydropower base and growing solar program, though sanctions-related financing constraints limit project execution pace relative to its resource potential. Saudi Arabia at 18.5% and UAE at 12.7% represent the most dynamic investment markets, with Vision 2030’s renewable energy target by 2030 and UAE’s Net Zero 2050 strategy.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Solar Power – 53.8% market share (2025) |

|

Leading End User |

Industrial – 50.9% market share (2025) |

|

Leading Country |

Iran – 33.3% market share (2025) |

|

Fastest Growing Country |

Saudi Arabia (CAGR ~18.5%) |

Key Analytical Observations Supporting The Above Data:

- Solar power dominates at 53.8% (2025): Solar power is the foundational driver of the Middle East renewable energy market, enabled by a unique combination of global solar irradiation leadership. By the end of 2024, a total of ten renewable energy projects were operational, including nine solar energy projects with a combined capacity of 6,151 megawatts and one wind energy project with a capacity of 400 megawatts in Saudi Arabia.

- Industrial end users lead at 50.9% (2025): Middle East industrial energy demand is dominated by desalination plants, oil & gas processing, and petrochemical industries that collectively consume high national electricity in GCC countries.

- Iran leads at 33.3% (2025): Iran’s large hydropower base represents the largest existing renewable energy asset base in the Middle East. The country’s 10 GW solar pipeline is primarily to reduce domestic gas consumption and reduce grid losses.

- Saudi Arabia fastest growing at ~18.5% CAGR: As of the end of 2024, the total investment volume in renewable energy projects reached approximately SAR 19.839 Billion in Saudi Arabia. This rising investments accelerating the market growth.

Middle East Renewable Energy Market Overview

The Middle East renewable energy market encompasses the generation, transmission, distribution, and commercialization of electricity and energy from renewable sources, including solar photovoltaic (PV), concentrated solar power (CSP), wind (onshore and offshore), hydropower, and bioenergy across countries spanning the Arabian Peninsula, Levant, and Turkey.

Applications span utility-scale solar parks and wind farms supplying national grids, dedicated industrial power for desalination and petrochemical complexes, commercial and residential distributed solar, and the emerging green hydrogen production sector. Macroeconomic influences include oil price cycles, global clean energy investment flows, bilateral energy partnerships between GCC states and European/Asian trading partners, and the sovereign wealth fund capital committed to clean energy.

Market Dynamics

To evaluate market opportunities, Request Sample

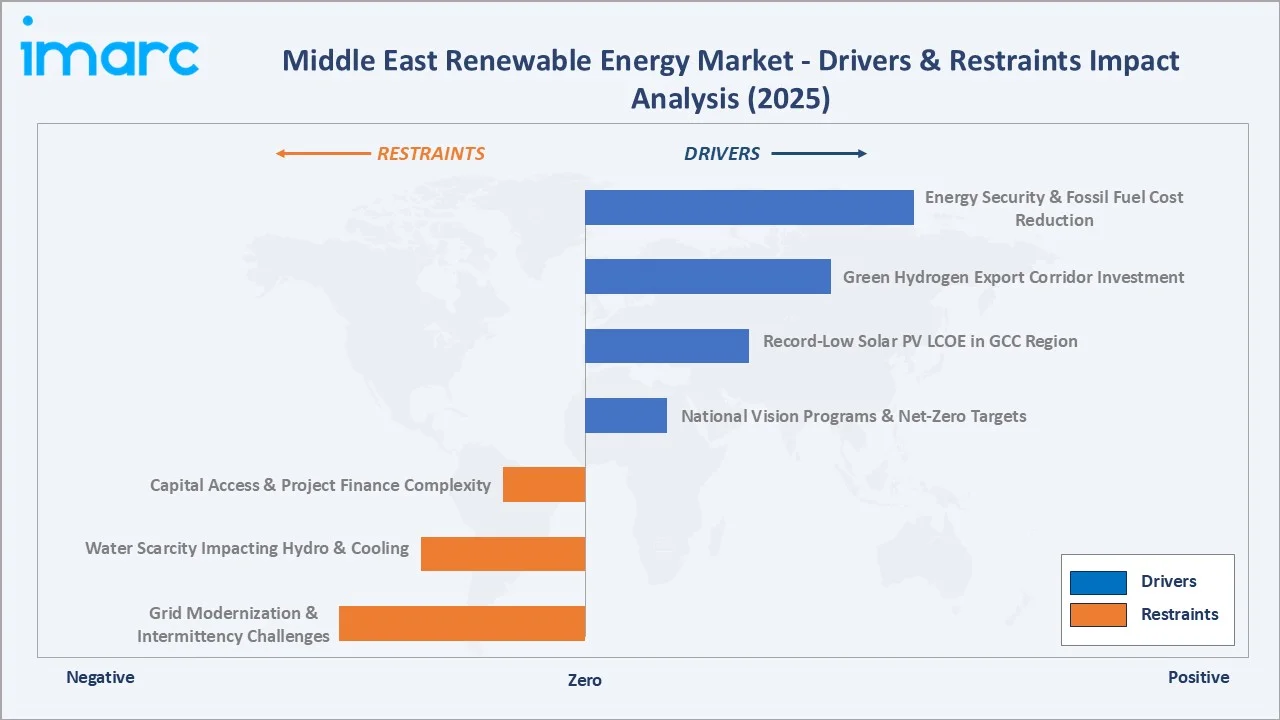

Market Drivers

- National Vision Programs and Net-Zero Mandates: Saudi Arabia aims to generate at least 50% of its electricity from renewable sources by 2030, with a total capacity of 130 gigawatts (GW). Of this, 58.7 GW is projected to come from solar energy and 40 GW from wind energy. UAE’s Net Zero 2050 strategy commits 600 Billion dirhams ($163 Billion) in renewable energy investment.

- Record-Low Solar LCOE Driving Project Economics: The GCC region repeatedly achieved the world’s lowest solar LCOE bids. These extraordinary price levels reflect the GCC’s combination of world-class solar irradiance, zero land costs, low-cost sovereign debt financing, and competitive international EPC contracts.

- Green Hydrogen Export Economy Development: The Middle East is positioning itself as the world’s largest green hydrogen production region, with Saudi Arabia, UAE, Oman, and Jordan collectively targeting low-carbon hydrogen production. Each MT of green hydrogen requires renewable electricity, creating a massive captive renewable energy demand that is additional to grid electricity requirements.

Market Restraints

- Grid Modernization and Intermittency Challenge: The GCC’s electricity grid infrastructure was designed for centralized fossil fuel generation with predictable dispatch patterns. Integrating variable solar and wind generation requires high grid modernization investment that cannot keep pace with the speed of renewable capacity additions.

- Water Scarcity and Environmental Constraints: Concentrated Solar Power (CSP) and some wind turbine designs require cooling water or dust management water that is extremely scarce in the GCC. Climate change projections indicate increasing dust storm frequency and intensity.

- Capital Access and Project Finance Complexity for Non-GCC Countries: While GCC countries benefit from sovereign wealth fund financing that eliminates conventional project finance risk, countries including Iraq, Jordan, and Iran face acute capital access constraints.

Market Opportunities

- Battery Energy Storage for Grid Stability: The rapid scaling of intermittent solar generation requires proportional investment in grid-scale battery energy storage systems (BESS). DEWA patented a cost-effective, environmentally friendly method to enhance battery performance, supporting its energy storage projects at the Mohammed bin Rashid Al Maktoum Solar Park, including a Tesla lithium-ion solution and a sodium-sulfur pilot project.

- Cross-Border Renewable Energy Trading: The GCCIA (Gulf Cooperation Council Interconnection Authority) grid, connecting Saudi Arabia, UAE, Bahrain, Kuwait, Qatar, and Oman, represents a unique infrastructure enabling renewable energy trading that no other emerging market region possesses.

Market Challenges

- Local Content and Saudization Requirements: Saudi Arabia’s Vision Realization Office mandates local content for REPDO projects, covering module manufacturing, steel, cabling, and O&M services. Saudi Arabia’s Sudair solar project boosted its solar capacity to 2.2 GW, with a target of 40 GW by 2030. To achieve its ambitious plan, Saudi Arabia must install an average of 5.5 GW of new solar capacity per year.

- Technology Adaptation for Extreme Heat and Dust: Standard solar panel and wind turbine designs lose rated efficiency in the ambient temperatures characteristic of Gulf summer conditions. Tracker system failure rates are 3–4× higher in sand-prone environments.

Emerging Market Trends

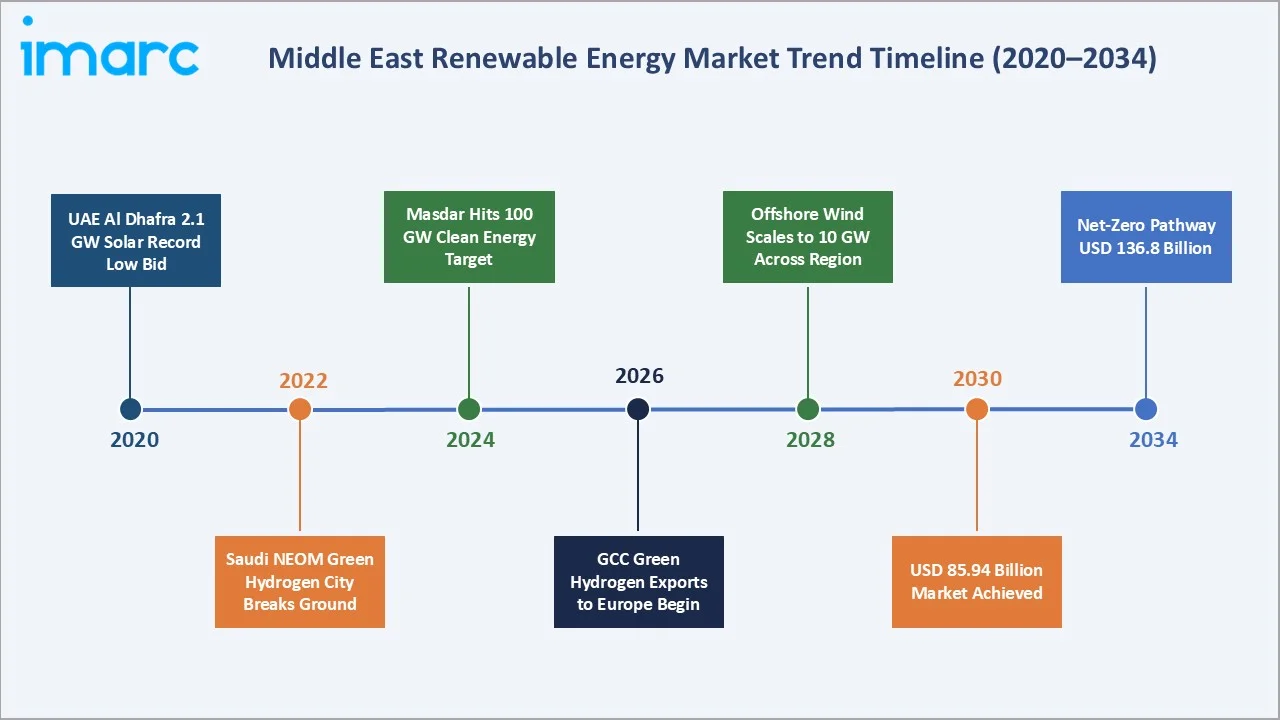

1. Giga-Scale Solar Projects Setting Global Records

The Middle East is the epicenter of the world’s largest solar project development. Saudi Arabia’s Al Shuaibah Phases 1 and 2 is one of the largest solar plants with a total capacity of 2631 MW. The competitive advantage of giga-scale in the GCC, where land is free, solar irradiance is exceptional, and sovereign financing eliminates risk premiums, is creating project economics that reshape global solar LCOE benchmarks.

2. Green Hydrogen and Ammonia Export Industry Emergence

NEOM Green Hydrogen Company (NGHC) secured financial closure for the world’s largest green hydrogen production facility, with a total investment of USD 8.4 Billion, after signing financial agreements with 23 local, regional, and international banks and investment firms. The Arab Hydrogen Vision frames green hydrogen as the second hydrocarbon export economy, replacing oil revenues, with European energy security concerns post-Ukraine creating long-term offtake certainty for GCC producers.

3. Distributed Solar and Prosumer Markets Emerging

Historically absent from the Middle East due to subsidized electricity tariffs, distributed rooftop solar is gaining traction as GCC governments reduce electricity subsidies and introduce net metering programs.

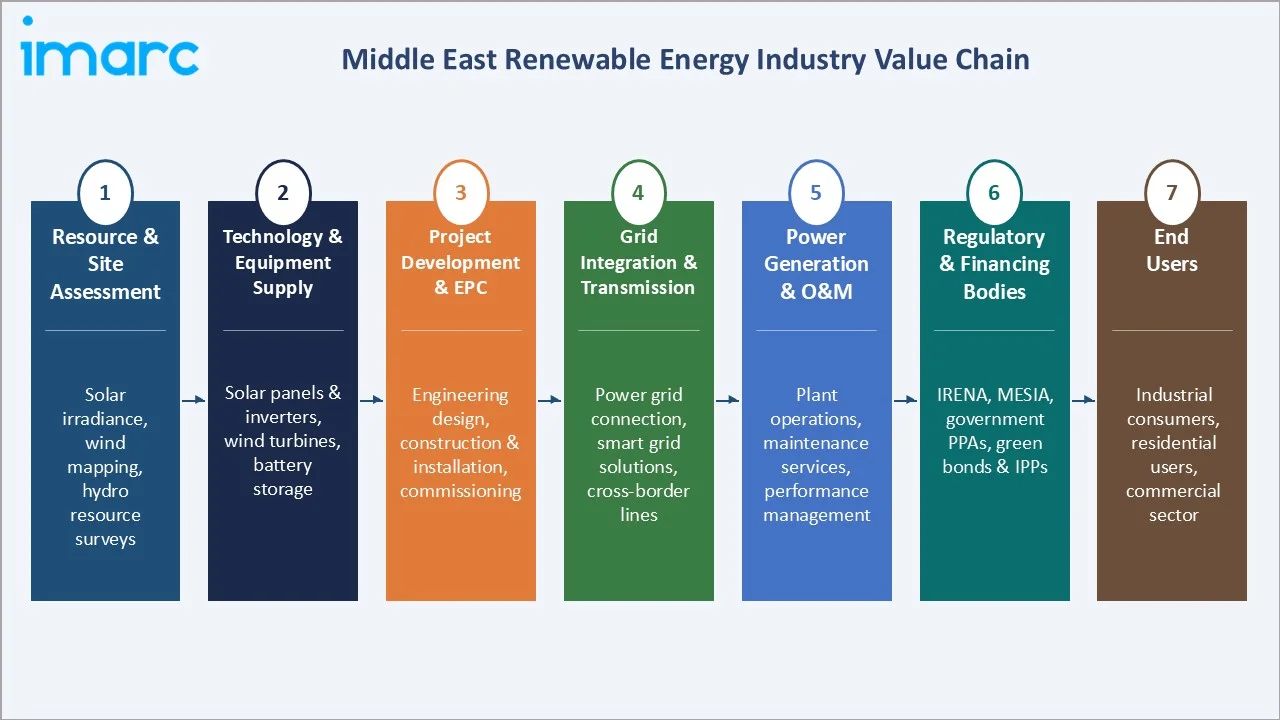

Industry Value Chain Analysis

The Middle East renewable energy value chain spans upstream equipment supply through project development, construction, grid integration, and final energy delivery to end-use consumers, with a unique regional characteristic of sovereign wealth fund participation at every stage of the chain.

|

Stage |

Key Participants |

|

Raw Materials & Components |

Solar wafers, wind turbine components, steel towers, inverters, battery cells |

|

Grid Transmission & Integration |

National grid operators, HVDC transmission, BESS grid stabilization |

|

Technology & O&M Services |

TotalEnergies Services, predictive maintenance platforms, drone inspection services |

|

Energy Trading & Commercialization |

DEWA, CSPF Saudi Arabia; regional power exchange under GCCIA; corporate PPA markets for C&I buyers; green certificate markets |

|

End-Use Consumers |

Industrial (desalination, oil & gas, mining), residential rooftop solar, commercial & institutional buildings, hydrogen production facilities |

The project development and finance stage is unique in the Middle East context: sovereign wealth funds provide equity capital directly at 5–6% cost, eliminating the 12–18% commercial equity return requirement that inflates project costs in other emerging markets. This structural financing advantage, unique to GCC-backed projects globally, is the primary reason for the world-record LCOE bids from ACWA Power and Masdar, and creates a competitive advantage that is near-impossible to replicate outside the region.

Technology Landscape in the Middle East Renewable Energy Industry

Bifacial and High-Efficiency Solar PV Technology

The Middle East’s flat, high-albedo (reflective) desert terrain makes bifacial solar panels, which capture reflected light from the rear cell surface, particularly effective, adding additional energy yield versus monofacial panels.

Concentrated Solar Power for 24/7 Generation

CSP with integrated molten salt thermal energy storage enables 24/7 solar power dispatch without battery storage, critically important for base-load industrial applications in the Middle East where 24/7 desalination and oil & gas operations cannot tolerate intermittency.

Green Hydrogen Electrolysis and Power-to-X

Proton Exchange Membrane (PEM) and Alkaline electrolysers are the two dominant technologies for green hydrogen production from renewable electricity. Air Products awarded thyssenkrupp Uhde Chlorine Engineers a contract to provide a 2-gigawatt electrolysis plant for one of the largest green hydrogen projects globally at NEOM in Saudi Arabia.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Solar Power |

53.8% |

2025 |

|

End User |

Industrial |

50.9% |

2025 |

|

Country |

Iran |

33.3% |

2025 |

By Type

Solar power dominates at 53.8% of market revenue (2025). The category spans utility-scale solar PV parks, distributed rooftop solar, concentrated solar power (CSP) with thermal storage, and floating solar on reservoirs. GCC countries are deploying the world’s largest utility-scale solar projects, with Saudi Arabia’s REPDO program. By the end of 2024, the total investment in renewable energy projects amounted to around SAR 19.839 Billion, with SAR 18.264 Billion dedicated to solar energy.

To access detailed market analysis, Request Sample

Wind power at 18.6% is growing rapidly in GCC countries. Hydropower at 12.4% is primarily concentrated in Turkey and Iran’s existing dam infrastructure. Bioenergy at 9.3% encompasses municipal solid waste-to-energy (MSW) projects that are strategically prioritized in UAE and Saudi Arabia for simultaneous waste management and power generation. The Others category at 5.9% includes geothermal, tidal, and wave energy pilot projects.

By End User

Industrial end users dominate at 50.9% market share (2025). This reflects the energy-intensive nature of the Middle East’s industrial base: oil and gas upstream operations, petrochemical refinery complexes, aluminum smelters, and the emerging green hydrogen production facilities.

Residential end users at 28.7% are growing at ~14.2% CAGR, the fastest of all end user segments. The removal of electricity subsidies in Saudi Arabia, the UAE’s Smart Dubai initiative, and Israel’s mandatory solar for new buildings are driving residential adoption of distributed solar. Commercial end users at 20.4% include hotels, shopping malls, offices, and airports implementing solar and energy efficiency investments to meet corporate sustainability commitments and reduce electricity costs as subsidy reforms continue.

Regional Market Insights

|

Country |

Share (2025) |

Key Initiatives & Drivers |

|

Iran |

33.3% |

Largest renewable base by existing hydro, solar expansion under National Energy Master Plan |

|

Saudi Arabia |

18.5% |

Vision 2030 targets renewables by 2030, NEOM city renewable |

|

United Arab Emirates |

12.7% |

UAE Net Zero 2050, Barakah nuclear (clean energy base) |

|

Turkey |

10.9% |

Largest renewable market by installed capacity in region, Turkish private sector investment |

|

Israel |

6.4% |

Israeli Electricity Authority 30% renewables by 2030, rooftop solar mandate for new buildings |

|

Iraq |

5.1% |

World Bank and USAID-backed solar for national grid stabilization, persistent grid infrastructure challenges |

|

Qatar |

3.6% |

FIFA World Cup 2022 solar legacy, hydrogen electrolyser linked to solar |

|

Kuwait |

3.1% |

Shagaya Renewable Energy Park 2 GW, KIPIC (Kuwait Integrated Petroleum Industries) solar for refinery |

|

Oman |

2.8% |

Oman Vision 2040, Manah I & II solar |

|

Jordan |

2.1% |

Jordan Energy Strategy 31% renewables by 2030, Jordan Electric Power Company grid upgrade |

|

Bahrain |

1.5% |

Al Dur offshore solar plans, Bahrain Vision 2030, limited land resources |

Iran’s 33.3% market dominance (2025) primarily reflects its large existing hydropower base rather than new clean energy investment. However, the pace of new renewable energy development in Iran is constrained by U.S. and EU sanctions that prevent access to SWIFT banking for project financing, European and American equipment supply chains, and export credit guarantee programs from OECD countries, forcing reliance on Chinese and domestic equipment suppliers at higher cost.

Saudi Arabia’s 18.5% share (2025) is growing fastest because it starts from a relatively small base despite enormous potential. The REPDO program is transforming the market growth. The total number of operated renewable energy projects reached 10, nine of which were solar energy projects with a combined capacity of 6,151 megawatts, in addition to one wind energy project with a total capacity of 400 megawatts by 2024 in Saudi Arabia.

Competitive Landscape

The Middle East renewable energy market is moderately concentrated at the utility-scale developer tier, developing approximately 45–50% of announced GCC renewable capacity.

|

Company Name |

Key Divisions / Platform |

Market Position |

Core Strength |

|

Acwa |

Concentrated Solar Power (CSP), Photovoltaic (PV) Power, Wind Power |

Dominant Market Leader |

ACWA has a portfolio of 109 projects totalling 94 GW of installed capacity, 52 GW of which comes from renewable sources |

|

Masdar |

Solar, Wind, Geothermal and Waste-to-Energy Projects |

Market Leader |

Masdar's operational, under construction and advanced pipeline capacity grew from 20GW to 51GW between 2022 and the end of 2024. |

|

TotalEnergies |

Solar Power Projects and Wind Power Projects |

Established |

TotalEnergies operates extensively across the Middle East in solar and wind, although the claim of having the "largest" footprint among European supermajors in the Middle East. |

|

Dubai Electricity & Water Authority (DEWA) |

Mohammed bin Rashid Al Maktoum Solar Park |

State Champion |

DEWA has implemented a pilot Green Hydrogen Project at the Mohammed bin Rashid Al Maktoum Solar Park, the first project of its kind in the MENA region to produce green hydrogen using solar energy |

The market’s unique characteristic is the central role of sovereign entities that combine commercial objectives with national policy mandates, creating competitive dynamics that differ fundamentally from commercial renewable energy markets in Europe or North America.

Key Company Profiles

Acwa

Acwa is Saudi Arabia’s and the broader Middle East’s most powerful renewable energy developer, investor, and operator, with 50+ GW of renewable capacity under development or operation across the Middle East, Africa, and Central Asia.

- Portfolio: Concentrated Solar Power (CSP), Photovoltaic (PV) Power, Wind Power.

- Recent Developments: In February 2026, Türkiye and ACWA Power are set to formalise the second phase of their 5 GW renewable energy collaboration during the UN climate summit COP31.

- Strategic Focus: Become the world’s largest renewable energy company by capacity by 2030; green hydrogen as next growth platform; international expansion leveraging Saudi government relationships; battery storage integration alongside solar and wind assets; capital recycling through project sell-downs to institutional investors.

Masdar

Masdar is Abu Dhabi’s sovereign clean energy champion. Founded in 2006, Masdar operates the world’s most technologically advanced clean energy research city (Masdar City) alongside a global clean energy portfolio.

- Portfolio: Solar, Wind, Geothermal and Waste-to-Energy Projects.

- Recent Developments: In January 2026, Masdar’s capacity reached 65GW, two-thirds of the way to the company’s 100GW 2030 target.

- Strategic Focus: Accelerate from 30 GW to 100 GW by 2030 through acquisitions and greenfield development; offshore wind as a key growth platform leveraging Mubadala’s global infrastructure relationships; green hydrogen electrolysis integration; position as UAE’s primary vehicle for clean energy diplomacy and international partnerships.

Dubai Electricity & Water Authority (DEWA)

DEWA is Dubai’s vertically integrated state utility and the most technologically advanced electricity distribution company in the Middle East.

- Portfolio: Mohammed bin Rashid Al Maktoum Solar Park

- Recent Developments: In January 2026, DEWA’s projects strengthened the UAE’s leading role in the transition to clean and renewable energy.

- Strategic Focus: Achieve Dubai Clean Energy Strategy 2050 target of 100% clean energy by 2050; Mohammed bin Rashid Al Maktoum Solar Park as global renewable energy showcase; Smart Grid as foundation for EV integration and demand response; Green Hydrogen scaling from pilot to 100 MW by 2030; digital utility leadership through AI-powered grid management and customer services.

Market Concentration Analysis

The Middle East renewable energy market is moderately concentrated in the GCC sub-market and highly fragmented across the broader 11-country region. In Saudi Arabia, Acwa dominates with approximately 35–40% of total renewable capacity under development or operation, reflecting its PIF ownership that aligns commercial and national energy security objectives. UAE’s market is shared between Masdar and DEWA as the three primary developers, collectively controlling approximately 80% of UAE renewable capacity.

The broader Middle East market is significantly more fragmented, with Turkey hosting independent power producers and Israel supporting licensed renewable developers. Iran’s market is dominated by domestic state-related entities and Chinese partners operating under sanctions constraints. This two-tier concentration structure, highly concentrated in sovereign-dominated GCC markets, highly fragmented in market-driven non-GCC countries, creates distinct competitive dynamics across the region.

Investment & Growth Opportunities

Fastest Growing Segments

Solar power (CAGR ~14.2%), residential end users (CAGR ~14.2%), and green hydrogen-linked renewable projects (CAGR ~35–40% from near-zero base) represent the three highest-growth investment vectors. Battery energy storage (CAGR ~25–30%) and offshore wind represent the two highest-risk/highest-reward emerging segments.

Emerging Investment Markets

Iraq’s World Bank-backed renewable program, Jordan’s cross-border electricity export potential, and Oman’s green hydrogen and offshore wind corridor collectively create investment opportunities in non-GCC markets that have received limited attention from institutional investors relative to Saudi Arabia and the UAE.

Venture and Institutional Investment Trends

Middle East sovereign wealth funds invested in global clean energy, with Mubadala’s Masdar, ACWA Power, and QIA’s clean energy fund as the primary vehicles. International institutional investors are all expanding their Middle East renewable allocations.

- Key investment themes: GCC utility-scale solar development rights, green hydrogen electrolysis infrastructure, grid-scale BESS in Saudi Arabia and UAE, Turkey wind portfolio M&A, and distributed solar networks in liberalising GCC electricity markets.

- Export credit and multilateral financing: JBIC (Japan), Euler Hermes (Germany), and UKEF (UK) are all providing export credit for equipment supply to GCC renewable projects, effectively subsidizing European and Japanese equipment manufacturers’ competitiveness against Chinese alternatives in the world’s fastest-growing solar market.

Future Market Outlook (2026-2034)

The Middle East renewable energy market is positioned for transformational, sustained high-growth expansion through 2034. From USD 48.03 Billion in 2025, the market is forecast to reach USD 136.88 Billion by 2034, at a 12.34% CAGR. This growth is structurally anchored by three interlocking imperatives that are simultaneously driving renewable investment at scale: Vision program policy mandates with GDP-sized investment commitments; the commercial imperative of replacing expensive subsidized gas and oil generation with world’s-cheapest solar electricity; and the strategic ambition to build a second energy export economy based on green hydrogen for post-oil revenues.

Between 2026 and 2030, the dominant market transformation will be Saudi Arabia’s extraordinary acceleration to a targeted 130 GW by 2030. The 2030–2034 period will be defined by the green hydrogen export economy reaching commercial maturity. Saudi Arabia’s NEOM, Oman’s Duqm, and UAE’s ICAD green hydrogen facilities will collectively be shipping green ammonia and liquid hydrogen to European and Asian buyers.

Research Methodology

Primary Research

Primary research encompassed structured interviews with 130+ industry stakeholders in 2025, including renewable energy project developers, GCC energy ministry officials, sovereign wealth fund energy investment teams, EPC contractors operating in the region, project finance bankers at regional and international banks, and renewable energy equipment suppliers. Geographic coverage included Saudi Arabia, UAE, Turkey, Jordan, Israel, and Qatar. Primary insights validated country-level market sizing, investment pipeline assessments, and technology adoption timelines.

Secondary Research

Secondary research encompassed IRENA (International Renewable Energy Agency) regional data, World Bank and IFC project documentation, GCCIA electricity statistics, DEWA and SEC annual reports, REPDO project awards data, IEA Middle East energy outlooks, project finance databases, company investor presentations, and renewable energy media. Over 260 secondary sources were reviewed and synthesized.

Forecasting Models

Market forecasts were developed using a bottom-up country capacity pipeline aggregation alidated against top-down methodology. Key inputs include REPDO auction schedules, UAE IWP program timelines, Turkey YEKDEM extension decisions, bilateral green hydrogen offtake volumes, and sovereign wealth fund annual renewable investment commitments.

Middle East Renewable Energy Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Hydro Power, Wind Power, Solar Power, Bioenergy, Others |

| End Users Covered | Industrial, Residential, Commercial |

| Countries Covered | Saudi Arabia, Turkey, Israel, United Arab Emirates, Iran, Iraq, Qatar, Kuwait, Oman, Jordan, Bahrain, Others |

| Companies Covered | Acwa, Masdar, TotalEnergies, Dubai Electricity & Water Authority (DEWA), etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Middle East renewable energy market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Middle East renewable energy market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Middle East renewable energy industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Middle East Renewable Energy Market Report

The Middle East renewable energy market was valued at USD 48.03 Billion in 2025 and is projected to reach USD 136.88 Billion by 2034, growing at a CAGR of 12.34%.

Iran leads with 33.3% share (2025), primarily due to its large existing hydropower base. Saudi Arabia is the fastest-growing country, driven by REPDO auctions and NEOM green hydrogen investments.

Solar power dominates with 53.8% share (2025), reflecting the GCC region’s world-class solar irradiance and record-low LCOE bids for utility-scale solar parks.

Industrial end users lead with 50.9% share (2025), dominated by desalination, oil & gas processing, and petrochemical complexes. NEOM will become the world’s largest single industrial renewable energy consumer.

UAE’s Al Dhafra Solar Park achieved the world record lowest solar LCOE of USD 0.0131/kWh in 2020, surpassing all global benchmarks and reflecting the GCC’s exceptional solar resource and financing advantage.

Key participants include Acwa, Masdar, TotalEnergies, and Dubai Electricity & Water Authority (DEWA).

Key trends include giga-scale solar record-breaking projects, green hydrogen export economy development, sovereign wealth fund clean energy platforms, Turkey’s cross-border power exports, and distributed rooftop solar market emergence.

The region targets green hydrogen by 2050, requiring 100–150 GW of dedicated renewables. NEOM’s Helios project is the world’s largest single green hydrogen facility.

Key challenges include grid modernization for high-variable-renewable penetration, water scarcity for cooling and dust management, capital access constraints for non-GCC countries, and local content manufacturing gaps.

Top opportunities include GCC utility-scale solar, green hydrogen electrolysis, grid-scale BESS, Turkey wind M&A, Iraq and Jordan frontier markets, and offshore wind in the Red Sea and Arabian Gulf.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)