Military Laser Systems Market Size, Share, Trends and Forecast by Product Type, Technology, Application, End Use, and Region, 2026-2034

Military Laser Systems Market Size and Share:

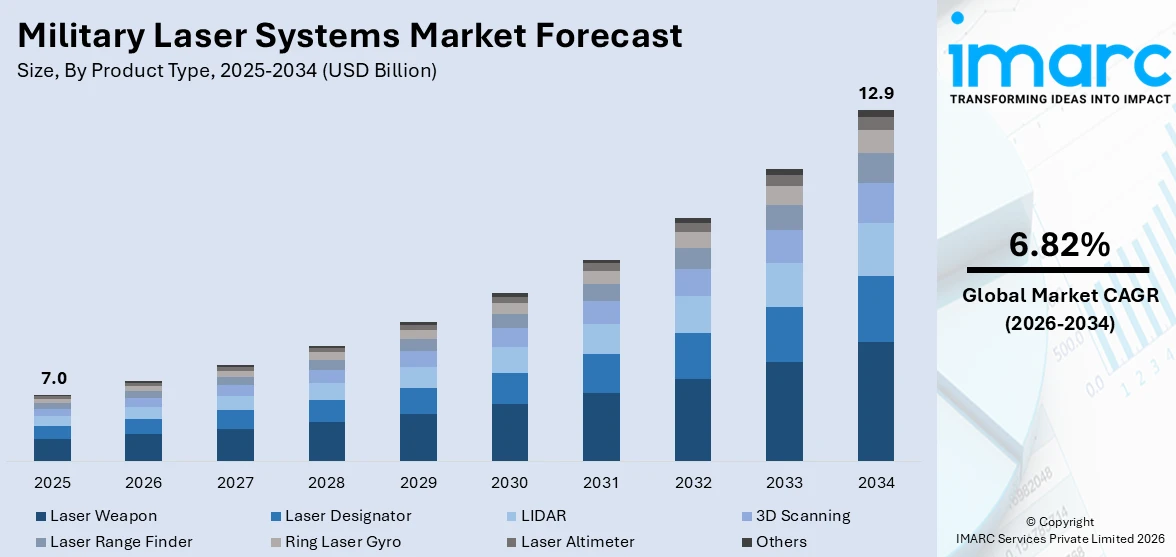

The global military laser systems market size was valued at USD 7.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 12.9 Billion by 2034, exhibiting a CAGR of 6.82% from 2026-2034. North America currently dominates the market, holding a market share of 37.8% in 2025. The dominance of the region is because of high defense spending, continuous research funding, and established defense contractors. Strong industrial base, frequent upgrades, and procurement programs also keep demand steady, ensuring ongoing development and deployment of cutting-edge laser-based defense solutions.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 7.0 Billion |

|

Market Forecast in 2034

|

USD 12.9 Billion |

| Market Growth Rate 2026-2034 | 6.82% |

Many nations are increasing military expenditure to enhance national safety and update their military capabilities. This boost allocates substantial resources to cutting-edge laser technologies that offer accurate targeting and reduced long-term expenses. Increased budgets allow for the acquisition of advanced laser systems and facilitate long-term research and development (R&D) for future military requirements. Additionally, contemporary combat requires weapons capable of accurately targeting enemies while minimizing collateral damage. Military laser systems fulfill this need by providing precise hits on threats such as drones and missiles. Precision minimizes accidental harm and boosts mission achievement, rendering these systems appealing investments for forces aiming to improve control in complicated combat scenarios. Besides this, advancements in laser optics, energy sources, and compact configurations are increasing the power, reliability, and versatility of laser systems. Enhanced beam quality, superior cooling systems, and modular parts facilitate simpler integration into aircraft, vessels, and ground vehicles, broadening their operational potential and motivating more defense organizations to embrace laser-driven technologies.

To get more information on this market Request Sample

The United States plays a vital role in the market, fueled by its substantial defense spending, which promotes ongoing investment in cutting-edge weapon systems, such as lasers. Funding supports research, testing, and extensive implementation across all service branches. Robust financial support guarantees consistent advancement of high-energy laser initiatives focused on enhancing accuracy, lowering operational expenses, and preserving a technological advantage against potential dangers. Moreover, the swift introduction of advanced laser systems, featuring innovations in beam management, AI incorporation, and compact configurations, facilitates quicker development phases, enabling forces to address contemporary threats. In 2024, Fast Company announced that the US Army successfully deployed BlueHalo's 20-kilowatt Locust laser weapon system abroad, representing the initial combat application of laser weapons. Created to combat drones, the system employs advanced beam management and AI-driven targeting software ("Wisard") to achieve high accuracy with reduced power usage. Created in less than five years, it demonstrates a significant advancement in directed-energy technology.

Military Laser Systems Market Trends:

Rising Defense Budgets

Increasing investments focused on enhancing defense capabilities are positively influencing the market. Nations facing regional conflicts and escalating security risks persist in dedicating greater shares of their budgets to cutting-edge defense technologies, such as high-energy laser systems. Authorities view these systems as crucial for updating military forces and remaining ready for changing battle situations. Recent endorsements of substantial defense aid initiatives emphasize this dedication to enhancing military preparedness. In May 2024, for instance, officials throughout the United States approved a significant USD 15 billion military aid package for Israel, highlighting the value of strategic alliances and defense support. In addition, extra resources were allocated for artillery enhancements and the creation of advanced munitions, ensuring troops are supplied with state-of-the-art equipment. These funding trends are catalyzing the demand for cutting-edge laser-based solutions.

Growing Focus on Homeland Security

The increasing application of cutting-edge technologies to tackle homeland security issues and protect critical infrastructure is impelling the market growth. Defense forces and homeland security organizations are progressively depending on laser technologies to enhance their capacity to identify threats, oversee critical regions, and react swiftly to breaches. These systems provide great accuracy and quick implementation, which makes them ideal for activities such as monitoring, identifying threats, controlling borders, and neutralizing drones that might endanger national security. Their adaptability and effectiveness are making them crucial instruments for contemporary security tasks. In April 2024, Israel showed this dedication by implementing multi-tiered military laser systems aimed at protecting the country from severe harm during an Iranian strike that included more than 300 drones and ballistic missiles. These crucial steps and investments underscore how nations are adopting laser technology as an essential part of their larger plan to strengthen national defense and ensure security.

Increasing Collaborations

Collaborations are influencing the military laser systems market growth, as alliances facilitate quicker innovation and more efficient implementation of cutting-edge technologies. Top defense contractors, government agencies, and dedicated research organizations are merging their technological expertise, financial resources, and production abilities to meet the intricate demands of contemporary warfare. Collaborating allows them to customize laser systems to address changing operational needs, incorporate them with current platforms, and guarantee their reliable performance in various environments. Joint ventures and co-development initiatives also assist in sharing expenses and risks while accelerating innovation processes. Recent advancements underscore the extent to which countries are adopting this trend. In July 2024, South Korea's Defense Acquisition Program Administration (DAPA) declared the initiation of mass production for its Laser Air Defense Weapon Block-I, marking an important achievement due to the strong partnership between industry specialists and government strategists to enhance air defense and safeguard national airspace.

Military Laser Systems Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global military laser systems market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, technology, application, and end use.

Analysis by Product Type:

- Laser Designator

- LIDAR

- 3D Scanning

- Laser Weapon

- Laser Range Finder

- Ring Laser Gyro

- Laser Altimeter

- Others

Laser weapon holds 38.7% of the market share, due to its ability to satisfy increasing demands for accuracy, rapid response, and economical solutions in contemporary warfare. This system provides precise accuracy with limited unintended effects, making it appealing for operations that need targeted action against threats. Its capacity to swiftly engage various targets without requiring expensive ammunition restocking decreases operational costs and logistical difficulties. Defense forces focus on laser weapon to tackle drones, missiles, and small boats because of its adaptability and efficiency. Improvements in compact, high-energy laser technology enable use across various platforms, including ground vehicles, naval vessels, and aircraft. Ongoing studies, enhanced defense funding, and effective field trials strengthen its implementation. As dangers grow more advanced, the need for dependable, scalable laser weapon continues to be robust, maintaining its leading position in the market.

Analysis by Technology:

- Fiber Laser

- Solid-State Laser

- Chemical Laser

- CO2 Laser

- Semiconductor Laser

- Others

Solid-state laser dominates the market owing to its excellent energy efficiency, small form factor, and dependable operation in tough combat environments. It produces strong, concentrated beams through solid gain materials, enabling integration into numerous platforms without added weight or cooling needs. Its design facilitates scalability, allowing defense contractors to create more powerful systems for emerging applications, such as missile defense or counter-drone strategies. Solid-state technology is also gaining from years of commercial and defense research, enhancing beam quality, durability, and cost efficiency. Military forces favor this technology due to its established effectiveness and its ability to adjust to changing mission requirements. Continuous improvements aid in minimizing size and power requirements while enhancing output, providing operators a benefit in accurate strikes. This blend of advanced development, operational adaptability, and real-world application ensures that solid-state laser remains at the forefront of military laser technology.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

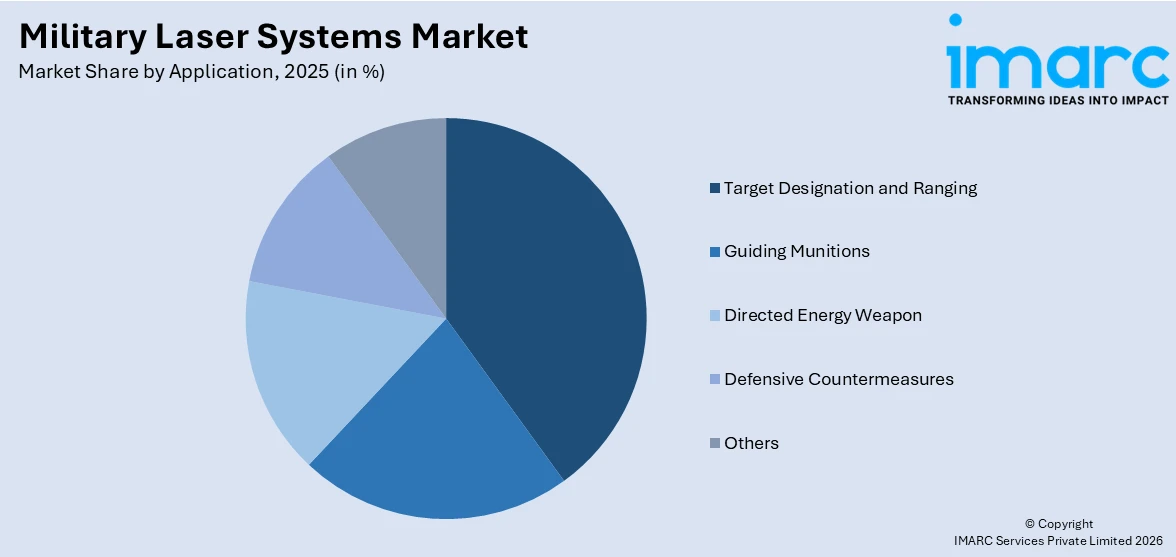

- Target Designation and Ranging

- Guiding Munitions

- Directed Energy Weapon

- Defensive Countermeasures

- Others

Target designation and ranging hold the biggest market share, as they are essential for improving accuracy and efficacy in combat situations. These systems allow forces to precisely identify, mark, and monitor targets over different distances, enhancing the effectiveness of guided munitions and reducing the likelihood of collateral damage. Their dependability in extreme conditions makes them essential for contemporary combat missions, where situational awareness and rapid response are crucial. Ongoing enhancements to range, targeting speed, and compatibility with other sensor systems maintain their relevance for emerging platforms and mission profiles. Defense initiatives continuously designate resources to enhance laser-based targeting and measurement instruments, recognizing their importance in joint strikes and surveillance. Increasing deployment of drones and sophisticated ground vehicles extends their accessibility further. Their proven effectiveness, along with technological advancements, maintains their leading status in the market.

Analysis by End Use:

- Defense

- Homeland Security

Defense represents the largest segment, accounting a share of 73.7%, because global armed forces emphasize cutting-edge directed energy technologies to sustain tactical dominance. Laser systems fulfill essential defense requirements such as target neutralization, surveillance, and threat deterrence with unparalleled accuracy and rapidity. Authorities continuously allocate funds to enhance armaments, emphasizing the incorporation of lasers for purposes like intercepting missiles and countering drones. Demand in the sector is driven by the need for advanced battlefield capabilities and the capacity to address asymmetric threats efficiently. Defense contracts frequently encompass long-term obligations for research, testing, and implementation, fostering consistent growth. Solid collaborations between military organizations and private firms guarantee ongoing advancement of resilient, operational systems. Services for training, maintenance, and system integration combined with these technologies enhance value and secure ongoing contracts. This consistent investment and emphasis on national security reinforce defense as the leading application segment for military laser systems.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, holding a share of 37.8% market share, because of robust defense budgets, a well-established defense industrial base, and consistent government support for advanced weapon initiatives. For instance, in 2024, the US Department of Defense released its FY 2025 budget request of $849.8 billion. The budget prioritized defending the US, strengthening alliances, modernizing forces, and investing in people, technology, and readiness. Besides this, the area advantages from established defense companies and research organizations that collaborate with military divisions to create advanced laser systems for precise targeting, missile defense, and counter-drone activities. Ongoing modernization efforts sustain high demand, as military forces seek to preserve a technological advantage and address new challenges. Collaborative efforts between private firms and government entities enhance the speed of testing, prototyping, and implementation. Moreover, supportive policies and ongoing funding in directed energy research guarantee ongoing innovation. The existence of several major contractors enhances competition and technological advancement, establishing North America as a center for advanced military laser technologies.

Key Regional Takeaways:

United States Military Laser Systems Market Analysis

The laser systems market for the US military accounted for 84.90%. It is mainly propelled by ongoing defense modernization efforts and rising investments in directed energy technologies to address emerging threats. In April 2025, US military service committees recommended a USD 150 Billion increase in defense funding, bringing the total expenditure above USD 1 Trillion. The strategy allocates USD 25 Billion for the Golden Dome missile defense program, emphasizing satellites and interceptors. In line with this, increasing apprehensions regarding unmanned aerial vehicles and hypersonic missile threats are driving the need for high-accuracy laser-based defensive systems. The ongoing progress in solid-state and fiber laser technologies, improving system efficiency and deployment adaptability across air, land, and naval platforms, is contributing to the market growth. Moreover, effective cooperation between the Department of Defense and prominent domestic defense contractors is accelerating the creation and testing of operational prototypes, thus increasing the market demand. The growing emphasis on accurate targeting with limited collateral damage is enhancing interest in laser technologies for intricate urban missions. Moreover, the proliferation of portable, vehicle-mounted, and shipborne laser systems, which enhance multi-domain mission preparedness, is impelling the market growth.

Europe Military Laser Systems Market Analysis

The European market is seeing growth attributed to heightened regional security issues and a rise in defense expenditure among NATO partners. In alignment with this, the escalating danger from drones and hybrid warfare strategies is leading to the implementation of advanced counter-UAS laser technologies. The increasing funding for cross-border collaborative defense initiatives by the EU is enhancing research and development processes and driving market expansion. In May 2025, the European Commission revealed EUR 910 million from the 2024 European Defence Fund to address capability gaps, enhance EU-Ukraine defense collaboration, and promote disruptive technologies, thus extending Europe’s defense innovation and preparedness objectives. Furthermore, the swift implementation of laser technologies on naval vessels to improve maritime surveillance and defense is boosting the market adoption. The continuous improvements in laser range-finding and precise targeting, which enhance strike accuracy for both air and ground forces, are supporting the market growth. Additionally, the growing modernization of air defense systems with directed energy elements, allowing quicker reactions to intricate aerial dangers, is driving product sales. In addition to this, favorable procurement policies and financial incentives are promoting the deployment of advanced military laser systems throughout the continent.

Asia Pacific Military Laser Systems Market Analysis

The Asia Pacific region is mainly influenced by rising territorial conflicts that are boosting the demand for advanced defense technologies. Moreover, increasing defense expenditures in countries like China, India, and South Korea are fueling significant investments in laser weapon initiatives. In May 2025, India’s defense budget is projected to increase by INR 50,000 Crore because of Operation Sindoor, elevating total spending beyond INR 7 Lakh Crore to support R&D and weapon acquisitions amid rising tensions with Pakistan. Furthermore, robust governmental efforts to foster indigenous defense production and boost regional technological independence and capability are strengthening the market growth. The growing network of research facilities and defense innovation centers in the area is speeding up the advancement of sophisticated directed energy technologies. Moreover, the swift adoption of laser technologies for counter-drone measures tackling emerging aerial threats in urban and strategic areas is positively influencing the market. In addition, boosting involvement in multinational military drills and strategic partnerships is enhancing technology transfer, standardization, and interoperability, fostering an optimistic market perspective.

Latin America Military Laser Systems Market Analysis

In Latin America, the market for military laser systems is expanding because of rising investments in border security and anti-drug initiatives. In 2024, Colombia's Army acquired seven new facilities, worth approximately USD 3.8 million, from the U.S. INL, enhancing counternarcotics efforts in Norte de Santander and Antioquia, aiding more than 450 personnel tackling organized crime and transnational dangers. Moreover, increasing collaboration with international defense tech companies, which improves local access to advanced directed energy technologies, is offering a favorable military laser systems market outlook. The continuous implementation of modernization initiatives for the military is leading to the incorporation of precision laser systems on land and sea platforms. Additionally, rising defense budgets in Brazil and Colombia, along with fostering domestic laser technology advancement, are broadening the market offerings.

Middle East and Africa Military Laser Systems Market Analysis

Investments in advanced border surveillance and air defense technologies are greatly influencing the market in the Middle East and Africa. In February 2025, the UAE finalized a USD 1 Billion agreement with local company Calidus for a new ground-to-ground missile system, enhancing its domestic air defense capabilities and representing the biggest contract unveiled at IDEX 2025. Moreover, the growing incorporation of laser technologies into current missile defense initiatives to improve targeting accuracy and operational efficiency is propelling the market growth. The cooperative defense alliances with top international tech companies are speeding up the exchange of technical knowledge and enabling the quicker rollout of contemporary laser solutions. Additionally, the rise of local manufacturing and defense technology parks is bolstering domestic production and innovation in directed energy weapons, consequently enhancing product sales.

Competitive Landscape:

Major participants in the market are prioritizing the growth of their portfolios via innovative research, collaborations, and defense agreements. They make significant investments in compact, high-power laser modules designed for integration into land, air, and naval platforms. Numerous individuals are partnering with military units to evaluate prototypes in authentic combat situations, guaranteeing dependability and versatility. Enhancements to current systems continue to be a focus, stressing the importance of boosting beam strength, distance, and precision in tracking. Businesses are pursuing export chances and enduring supply agreements with partner countries to expand their influence. In December 2024, MBDA Italia and Leonardo signed an MoU to develop naval laser weapons for the Italian Navy. The partnership aimed to produce “light” and “high-end” Fire Units for current and next-generation ships, backed by an initial EUR 80 Million budget under Italy’s Defense Planning Document.

The report provides a comprehensive analysis of the competitive landscape in the military laser systems market with detailed profiles of all major companies, including:

- BAE Systems PLC

- Coherent Inc.

- Elbit Systems Ltd.

- Lockheed Martin Corporation

- MKS Instruments Inc.

- Northrop Grumman Corporation

- Rafael Advanced Defense Systems Limited

- Raytheon Technologies Corporation

- Thales Group

- The Boeing Company

Latest News and Developments:

- June 2025: Zen Technologies secured its 54th Indian and 82nd global patent for a laser-based military training system. The patented long-pass optical filter integrates visible and infrared lasers for more realistic simulators. This follows Zen’s recent entry into the UAV segment with TISA Aerospace.

- May 2025: NUBURU announced its planned acquisition of TEKNE, an electronic warfare and cyber defense specialist, aiming to increase revenue to USD 50 Million. Pending approvals, the deal will merge TEKNE’s advanced vehicle protection and jammer technologies with NUBURU’s blue laser innovations for a new Defense & Security hub.

- March 2025: HII’s Mission Technologies division secured a contract to develop a High-Energy Laser weapon system for the U.S. Army. The open architecture HEL prototype will counter Groups 1–3 drones, support fixed-site or vehicle defense, and aims for rapid deployment, interoperability, and scalable upgrades.

- November 2024: Israel announced plans to deploy its new Iron Beam laser defense system within a year. Developed with Rafael and Elbit, Iron Beam uses high-power lasers to counter missiles, drones, and rockets, offering a cost-effective complement to Iron Dome but facing weather-related limitations.

- October 2024: Rafael Advanced Defense Systems announced it will showcase its latest laser weapons, air defense, and precision strike systems at AUSA 2024. Highlights include the IRON BEAM, SPIKE missile family, and new ICEBREAKER cruise missile, reinforcing Rafael’s commitment to US defense collaboration and innovation.

Military Laser Systems Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Laser Designator, LIDAR, 3D Scanning, Laser Weapon, Laser Range Finder, Ring Laser Gyro, Laser Altimeter, Others |

| Technologies Covered | Fiber Laser, Solid- State Laser, Chemical Laser, CO2 Laser, Semiconductor Laser, Others |

| Applications Covered | Target Designation and Ranging, Guiding Munitions, Directed Energy Weapon, Defensive Countermeasures, Others |

| End Uses Covered | Defense, Homeland Security |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Brazil, Mexico |

| Companies Covered | BAE Systems PLC, Coherent Inc., Elbit Systems Ltd., Lockheed Martin Corporation, MKS Instruments Inc., Northrop Grumman Corporation, Rafael Advanced Defense Systems Limited, Raytheon Technologies Corporation, Thales Group, The Boeing Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the military laser systems market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global military laser systems market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the military laser systems industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Military Laser Systems Market Report

The military laser systems market was valued at USD 7.0 Billion in 2025.

The military laser systems market is projected to exhibit a CAGR of 6.82% during 2026-2034, reaching a value of USD 12.9 Billion by 2034.

Rising defense budgets, demand for precision targeting, and advancements in directed energy technology are driving the military laser systems market. Forces seek systems that enhance accuracy, reduce collateral damage, and counter emerging threats like drones. Integration of lasers in modern platforms aligns with the push for cost-effective, efficient, and adaptable solutions to meet current and future combat needs is bolstering the market growth.

North America currently dominates the military laser systems market, accounting for a share of 37.8%. The dominance of the region is because of high defense spending, continuous research funding, and established defense contractors. Strong industrial base, frequent upgrades, and procurement programs keep demand steady, ensuring ongoing development and deployment of cutting-edge laser-based defense solutions.

Some of the major players in the military laser systems market include BAE Systems PLC, Coherent Inc., Elbit Systems Ltd., Lockheed Martin Corporation, MKS Instruments Inc., Northrop Grumman Corporation, Rafael Advanced Defense Systems Limited, Raytheon Technologies Corporation, Thales Group, The Boeing Company, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)