Milk Powder Market Size, Share, Trends and Forecast by Product Type, Function, Application, and Region, 2026-2034

Global Milk Powder Market Size, Share, Trends & Forecast (2026-2034)

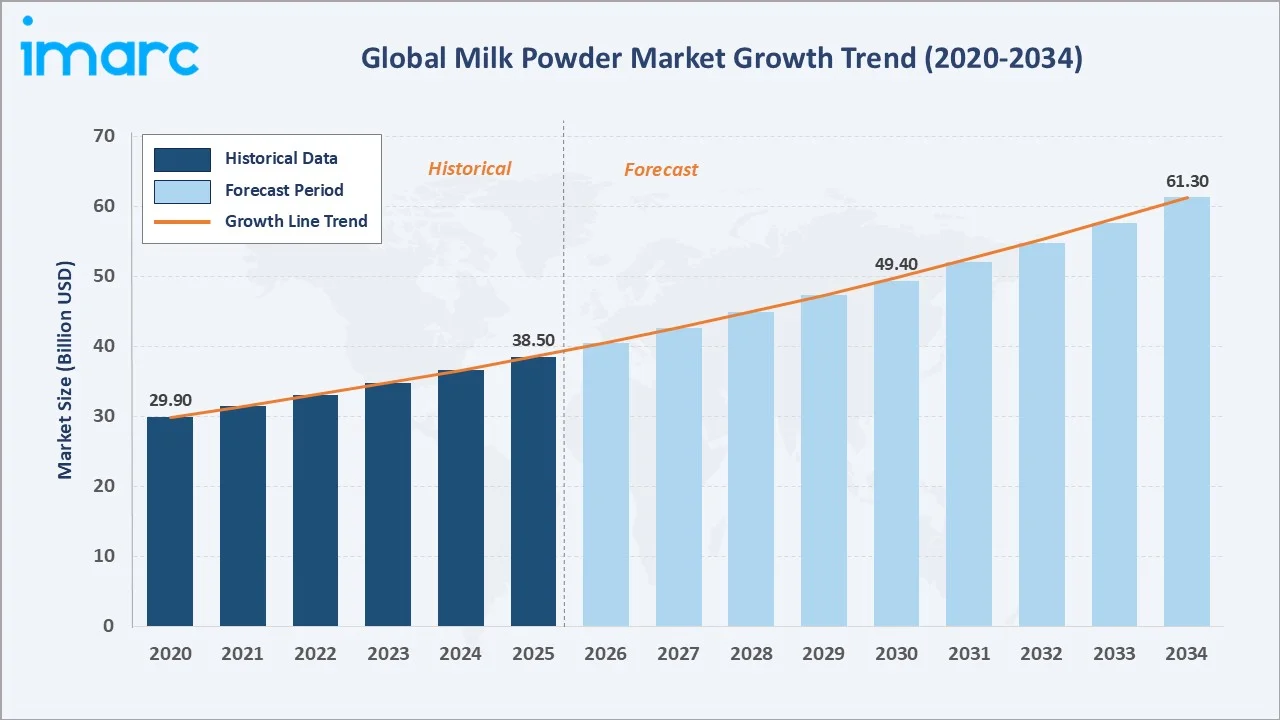

The global milk powder market size reached USD 38.5 Billion in 2025 and is projected to reach USD 61.3 Billion by 2034, exhibiting a CAGR of 5.15% during 2026-2034 Escalating demand driven by global population growth, expanding infant formula production, rising health consciousness, and broad-based food processing adoption are the primary forces fuelling milk powder market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 38.5 Billion |

|

Forecast Market Size (2034) |

USD 61.3 Billion |

|

CAGR (2026-2034) |

5.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

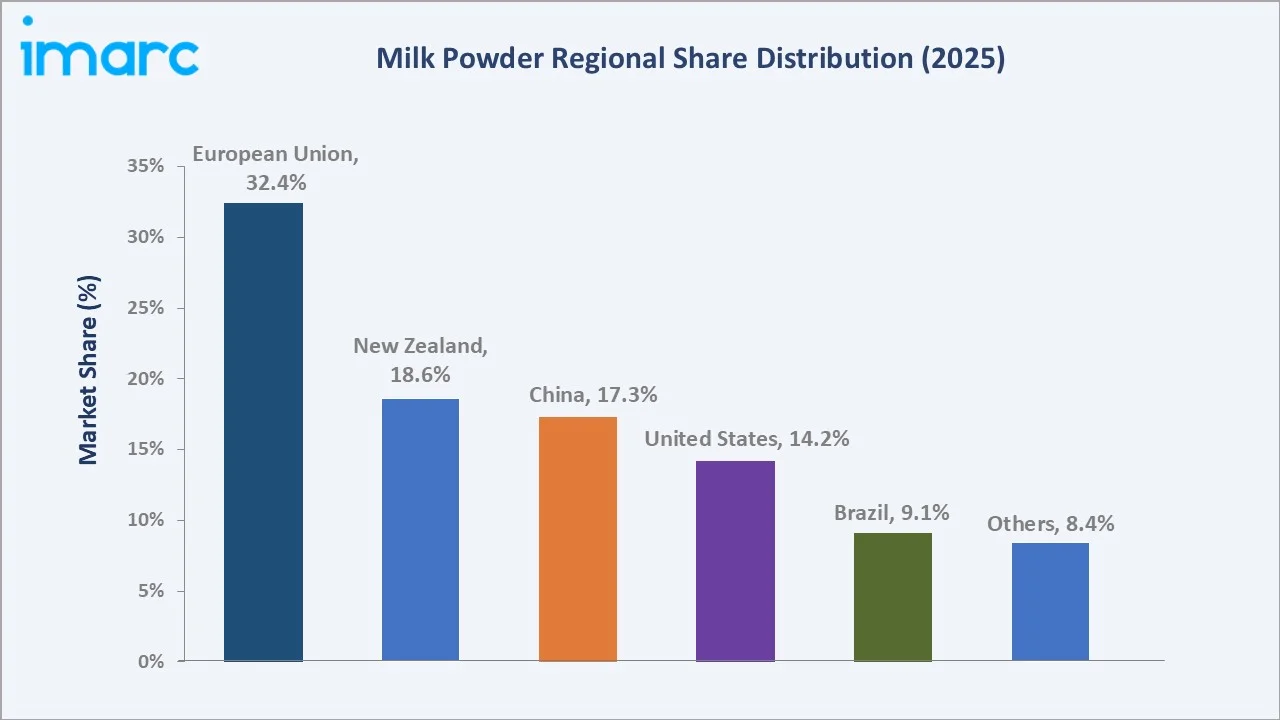

European Union (32.4% share, 2025) |

|

Fastest Growing Region |

China (17.3%, ~6.2% CAGR) |

|

Leading Product Type |

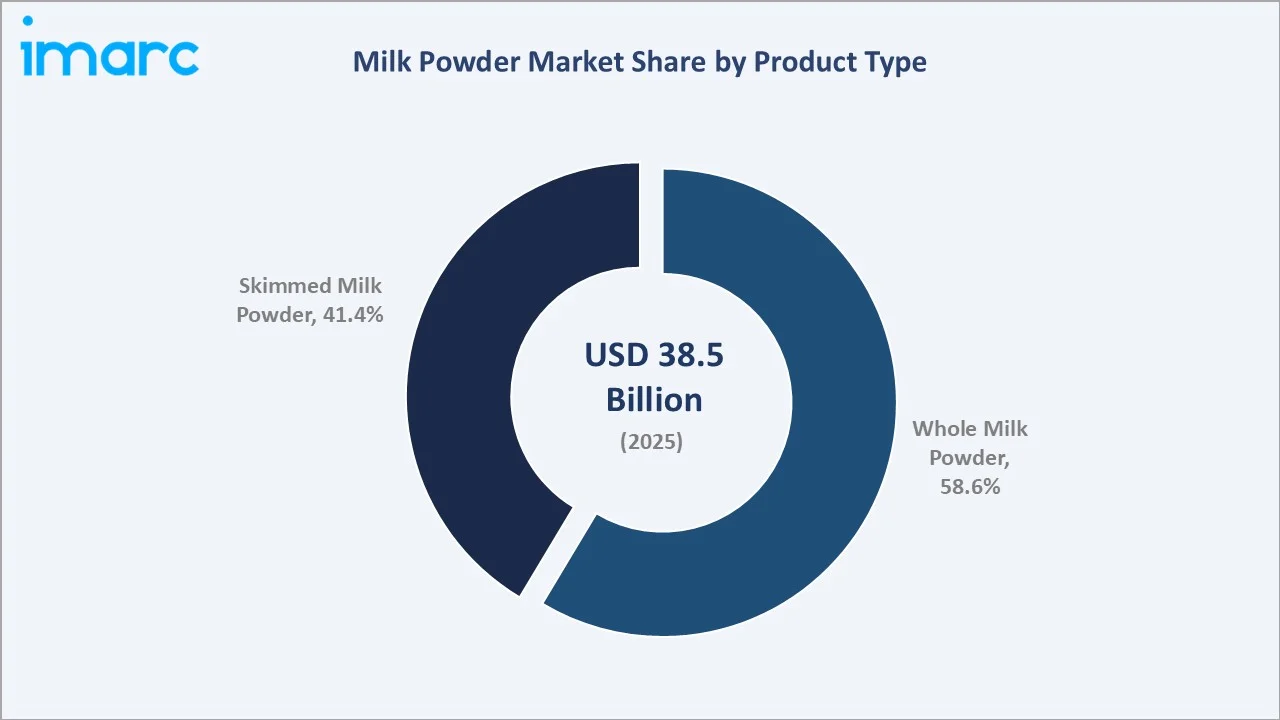

Whole Milk Powder – 58.6%, 2025 |

|

Leading Function |

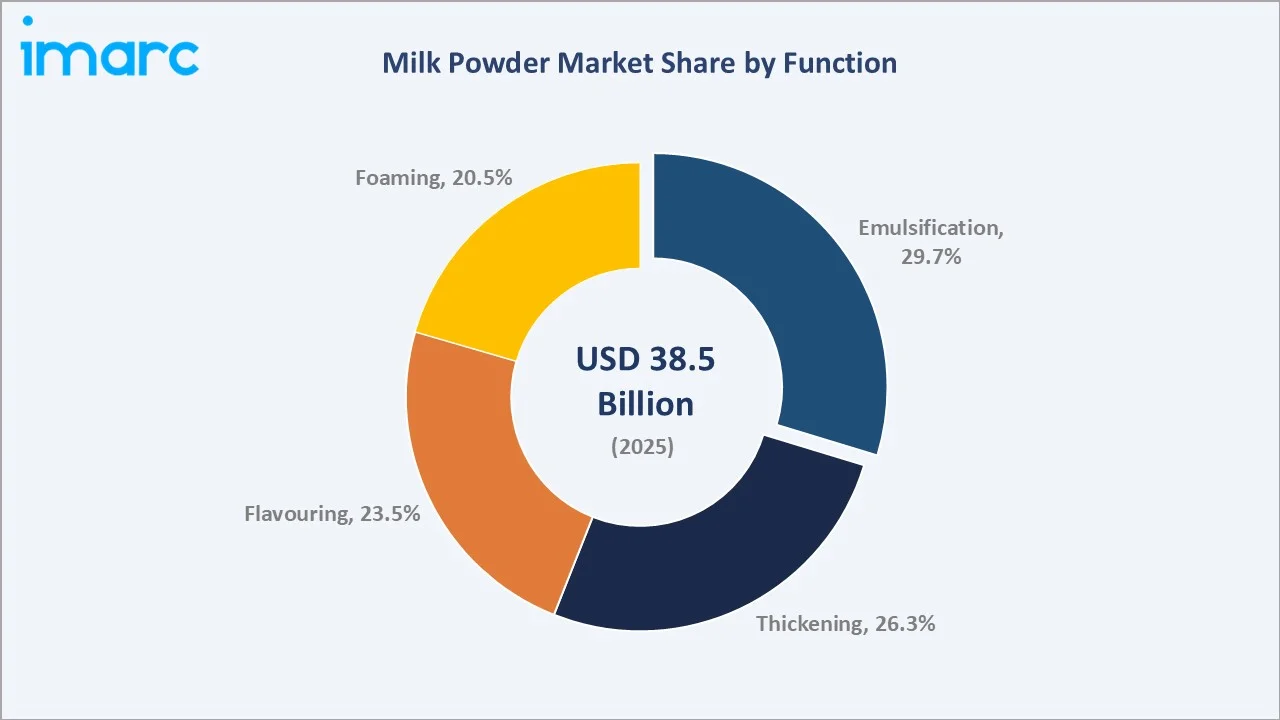

Emulsification – 29.7%, 2025 |

The global milk powder market growth trajectory from 2020 through 2034, contrasting historical expansion at USD 29.9 Billion in 2020 against a sustained forecast curve powered by urbanization, infant nutrition demand, and dairy technology adoption across developed and emerging markets.

To get more information on this market, Request Sample

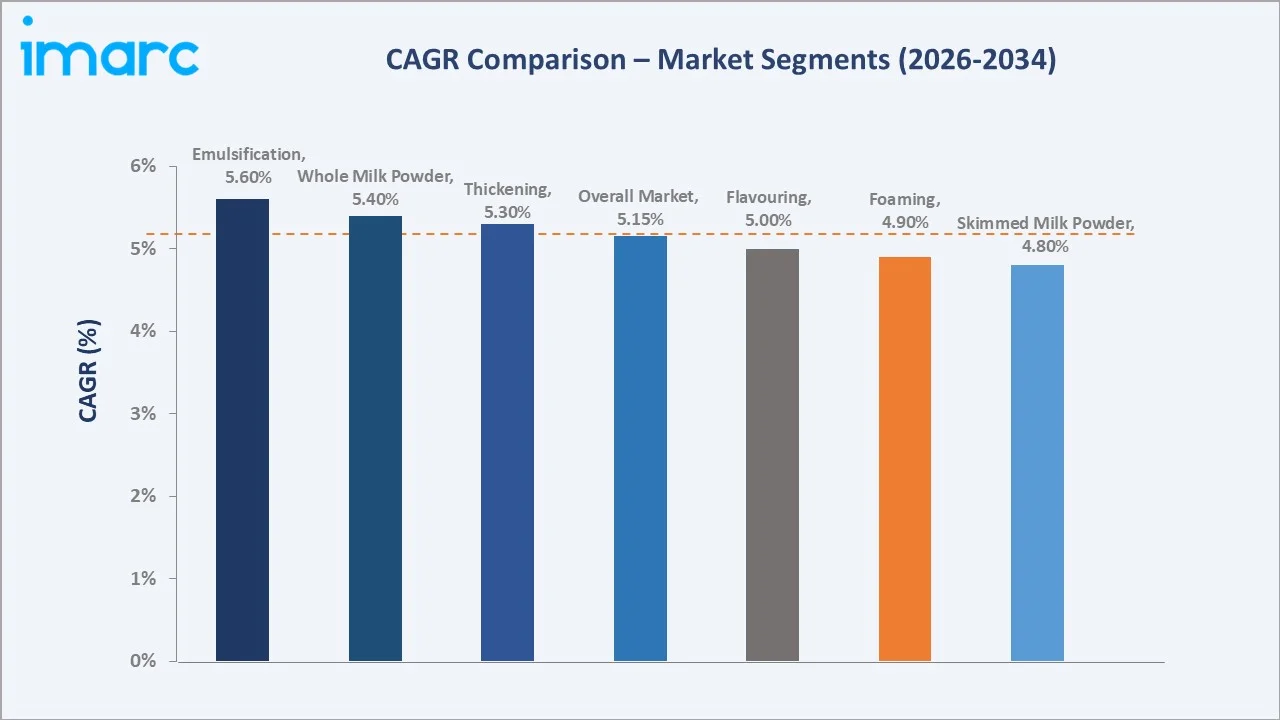

Segment-level CAGR comparisons highlighting emulsification and whole milk powder as the fastest-growing sub-categories within the global milk powder market forecast through 2034.

Executive Summary

The global milk powder market is undergoing steady structural expansion, underpinned by population growth, urbanization, and the rising integration of dairy-derived ingredients across diverse food processing and nutrition applications. Valued at USD 38.5 Billion in 2025, the market is forecast to reach USD 61.3 Billion by 2034, advancing at a CAGR of 5.15%. Between 2020 and 2025, the market grew from USD 29.9 Billion – reflecting a compound annual expansion of approximately 5.2% during the historical period – with sustained momentum expected through 2030 at an estimated market size of USD 49.4 Billion.

Whole Milk Powder commands 58.6% of global revenue in 2025, driven by its extensive use in confectionery, bakery products, and recombined dairy. Skimmed Milk Powder accounts for the remaining 41.4%, supported by its functional importance in infant formula and low-fat dietary products. From a functional standpoint, emulsification is the leading application at 29.7%, followed by thickening at 26.3%, flavouring at 23.5%, and foaming at 20.5%.

The European Union dominates global supply with a 32.4% share in 2025, reflecting its status as the world's largest dairy exporting bloc. New Zealand holds 18.6%, underpinned by Fonterra's export infrastructure. China accounts for 17.3%, driven by domestic consumption and government-supported dairy programs. The milk powder market outlook remains strongly positive through 2034, as emerging market consumers increasingly adopt dairy-based nutrition and food manufacturers scale specialty milk powder utilisation across value-added product categories.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Whole Milk Powder – 58.6% share (2025) |

|

Second Product Type |

Skimmed Milk Powder – 41.4% share (2025) |

|

Largest Function |

Emulsification – 29.7% share (2025) |

|

Second Function |

Thickening – 26.3% share (2025) |

|

Leading Region |

European Union – 32.4% revenue share (2025) |

|

Fastest Growing Region |

China – 17.3% share; ~6.2% CAGR (2026-2034) |

|

Top Companies |

Nestlé, Danone, FrieslandCampina, Lactalis, Arla Foods amba, Saputo Inc., GCMMF |

|

Market Opportunity |

Infant formula sector is projected to drive a significant share of total demand by 2034 |

Key Analytical Observations Supporting the Above Data:

- Whole Milk Powder at 58.6%: Whole Milk Powder's 58.6% dominance in 2025 reflects its broad functional versatility across confectionery, chocolate manufacturing, and bakery sectors. Global confectionery production continues to expand, with WMP serving as a critical input for chocolate coatings and milk-based fillings.

- Skimmed Milk Powder at 41.4%: Skimmed Milk Powder at 41.4% is anchored by infant formula demand. The global infant formula market remains large and continues to expand, driven by steady per-capita consumption growth in emerging economies.

- Emulsification at 29.7%: Emulsification's 29.7% leading functional share reflects milk powder's critical role in processed food manufacturing – stabilising oil-in-water emulsions in products including cream liqueurs, soups, sauces, and ready-to-drink beverages across global FMCG supply chains.

- EU's 32.4% Regional Leadership: The European Union's 32.4% global production share is sustained by robust export infrastructure, Common Agricultural Policy (CAP) dairy support mechanisms.

- China at 17.3%: China at 17.3% of global consumption reflects the government's domestic dairy development strategy. The Ministry of Agriculture and Rural Affairs targets a national raw milk output of 41 million metric tons by 2025, reducing import dependency for standard commodity powders.

- Infant Formula Opportunity: The global milk powder market opportunity in infant formula is projected to drive 28–32% of total revenue by 2034, supported by WHO-aligned fortification standards and the continued expansion of premium infant nutrition brands in China, Southeast Asia, and Sub-Saharan Africa.

Global Milk Powder Market Overview

Milk powder is a dehydrated dairy derivative produced by evaporating liquid milk to a stable solid form. The global market encompasses Whole Milk Powder, Skimmed Milk Powder, buttermilk powder, whey powder, and specialty fortified variants. These products serve critical roles in infant formula, confectionery, bakery products, sports nutrition, dry beverage mixes, fermented dairy, and meat processing applications worldwide.

The industry operates at the intersection of agricultural commodity cycles, consumer nutrition trends, food industry sourcing strategies, and international trade policy. Key macroeconomic influences include dairy herd productivity improvements, global milk surplus and deficit dynamics, fluctuating feed costs, and trade agreements governing export competitiveness between major dairy blocs including the EU, New Zealand, Australia, and the United States.

Technological investments in spray drying efficiency and membrane filtration are further enhancing product quality and production economics, supporting milk powder industry analysis as a forward-growing segment within the broader dairy complex.

Market Dynamics

To evaluate market opportunities, Request Sample

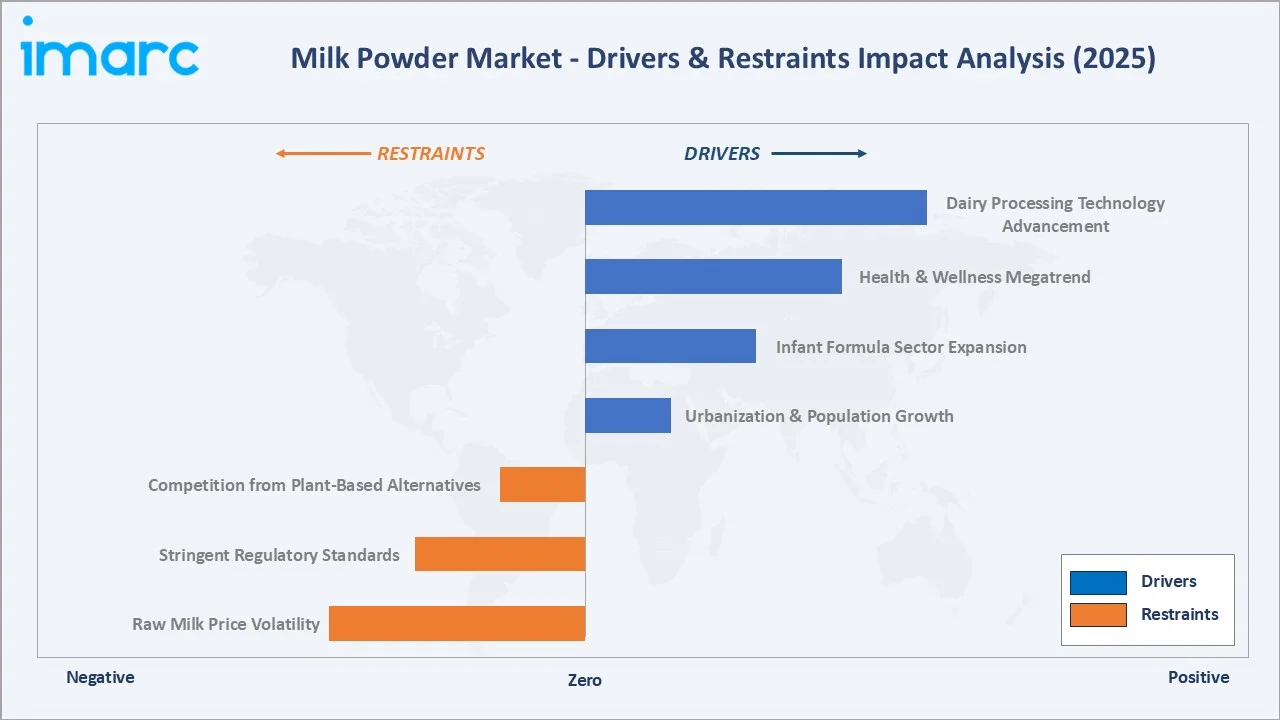

Market Drivers

- Urbanization and Population Growth: Global population reached 8.2 billion in 2024 and is projected to approach 9.6 billion by 2050. Urbanization is accelerating, particularly in Sub-Saharan Africa and South Asia, where urban household formation directly increases demand for shelf-stable, convenient dairy products including milk powder.

- Infant Formula Sector Expansion: The global infant formula market remains a major value segment, with milk powder particularly SMP serving as a key protein source in standard and follow-on formulations. Strict regulatory standards governing composition continue to underpin stable SMP demand within infant nutrition supply chains.

- Health and Wellness Megatrend: Health and wellness product innovations incorporating fortified milk powder are increasing, including high-protein formulations for sports nutrition and micronutrient-enriched blends for maternal health. Growing consumer preference for functional dairy is expanding demand for specialty milk powder variants.

- Dairy Processing Technology Advancement: Advances in spray drying, agglomeration, and instant powder technology have significantly improved the reconstitution speed, solubility, and shelf life of commercial milk powders. Membrane filtration systems are enabling precise protein standardisation, supporting premium product quality at competitive production costs.

Market Restraints

- Raw Milk Price Volatility: Global raw milk prices exhibit cyclical volatility driven by weather patterns, feed cost fluctuations, and herd health events. Price swings in global dairy benchmarks have directly compressed processor margins during periods of elevated input costs.

- Stringent Regulatory Standards: Milk powder exports face complex regulatory requirements including phytosanitary standards, labelling compliance, and infant formula-specific composition mandates across major import markets including China (GB 19644), the EU, and the United States.

- Competition from Plant-Based Alternatives: Growing consumer adoption of plant-based milk alternatives is moderating growth in certain retail dairy channels, particularly in Western Europe and North America.

Market Opportunities

- Emerging Market Demand Penetration: China’s dairy policy aims to reduce import dependence over time, while still supporting sustained demand for milk powder during the transition due to lower per-capita consumption levels. India’s dairy cooperative sector is expanding processing and spray-drying capacity, creating opportunities for technology partnerships and capability upgrades.

- Sports and Functional Nutrition Expansion: The global sports nutrition market surpassed USD 53.3 Billion in 2024. Milk-derived proteins – including caseins and lactoferrin – are increasingly incorporated into performance nutrition blends, generating demand for specialty high-protein powder fractions.

- Sustainability-Led Product Differentiation: Sustainable packaging mandates and consumer preference for climate-responsible brands are creating opportunities for dairy manufacturers to differentiate through recyclable packaging formats and reduced-carbon production claims. The EU Farm to Fork Strategy sets binding targets for dairy sector emissions reductions through 2030.

Market Challenges

- Supply Chain and Logistics Complexity: Rising global logistics costs and port congestion, particularly in key trade corridors between New Zealand and Asia Pacific markets, are elevating delivered costs for imported milk powder and complicating just-in-time supply chain management for FMCG manufacturers.

- Food Safety and Contamination Risk: Food safety incidents involving contamination or adulteration of dairy ingredients have historically triggered rapid regulatory responses, import bans, and severe brand damage. Maintaining quality certification compliance across global production and distribution networks is a persistent operational challenge.

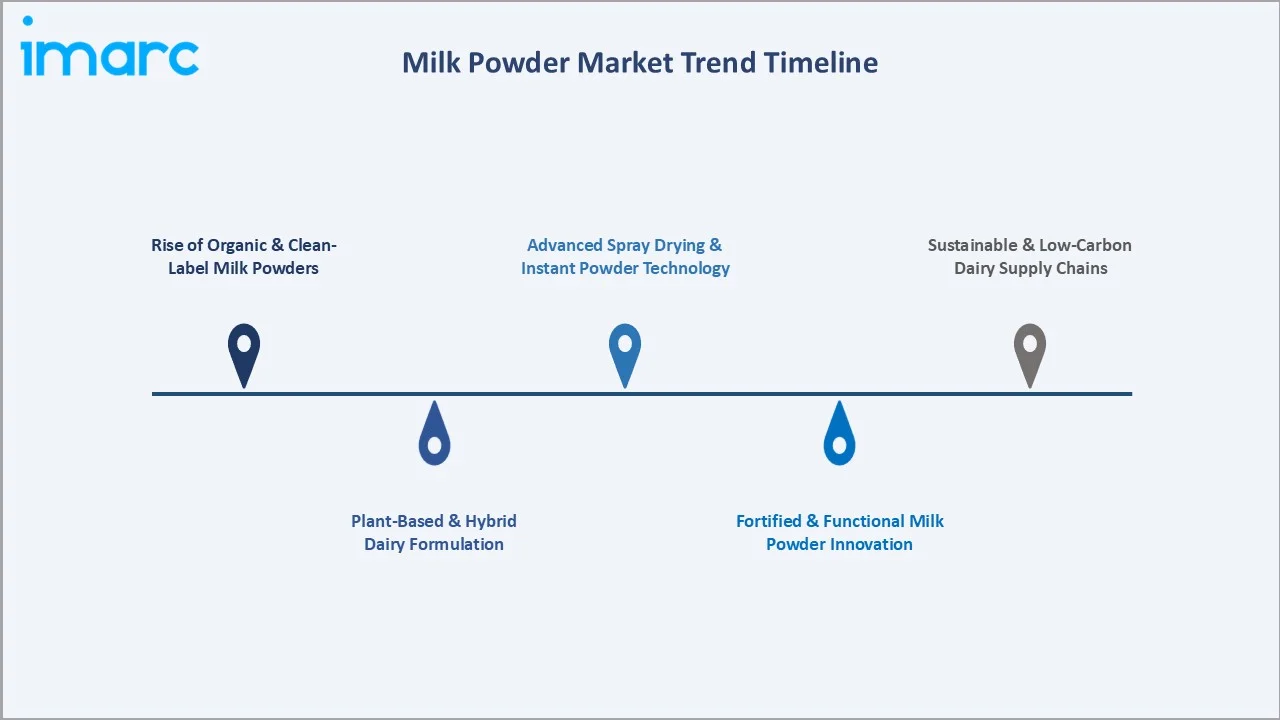

Emerging Market Trends

1. Rise of Organic and Clean-Label Milk Powders

Consumer demand for transparent, minimally processed dairy is increasing. Organic milk powder is commanding significant price premiums over conventional grades in key retail markets. This trend is encouraging global dairy cooperatives to expand certified organic supply chains.

2. Plant-Based and Hybrid Dairy Formulation

Food manufacturers are increasingly adopting hybrid formulations that combine conventional milk powder with plant-based proteins to balance nutrition, cost, and sustainability goals. These blended dairy systems are gaining traction in bakery and confectionery applications, supporting broader market diversification beyond traditional commodity formats.

3. Fortified and Functional Milk Powder Innovation

Launches of fortified milk powder products enriched with iron, zinc, vitamin D, and omega-3 have increased globally, driven by rising focus on maternal, child, and elderly nutrition. Government-supported supplementation programs in emerging markets are strengthening institutional demand, while aging populations in developed Asian economies are supporting uptake of premium nutrition-focused dairy products.

4. Advanced Spray Drying and Instant Powder Technology

Next-generation spray dryers incorporating fluid bed agglomeration and pressure nozzle systems are enabling the production of instant-dissolving milk powders with enhanced dispersibility. These products command premiums in foodservice and food manufacturing markets due to reduced reconstitution time, lower clumping, and improved emulsification performance.

5. Sustainable and Low-Carbon Dairy Supply Chains

Leading exporters including Arla, and FrieslandCampina have set net-zero emission targets for dairy operations within the 2030-2050 range. Carbon-footprint labelling on milk powder products is becoming a standard feature in European retail channels. Life-cycle assessment tools are increasingly embedded in procurement decisions by multinational food manufacturers sourcing bulk milk powder globally.

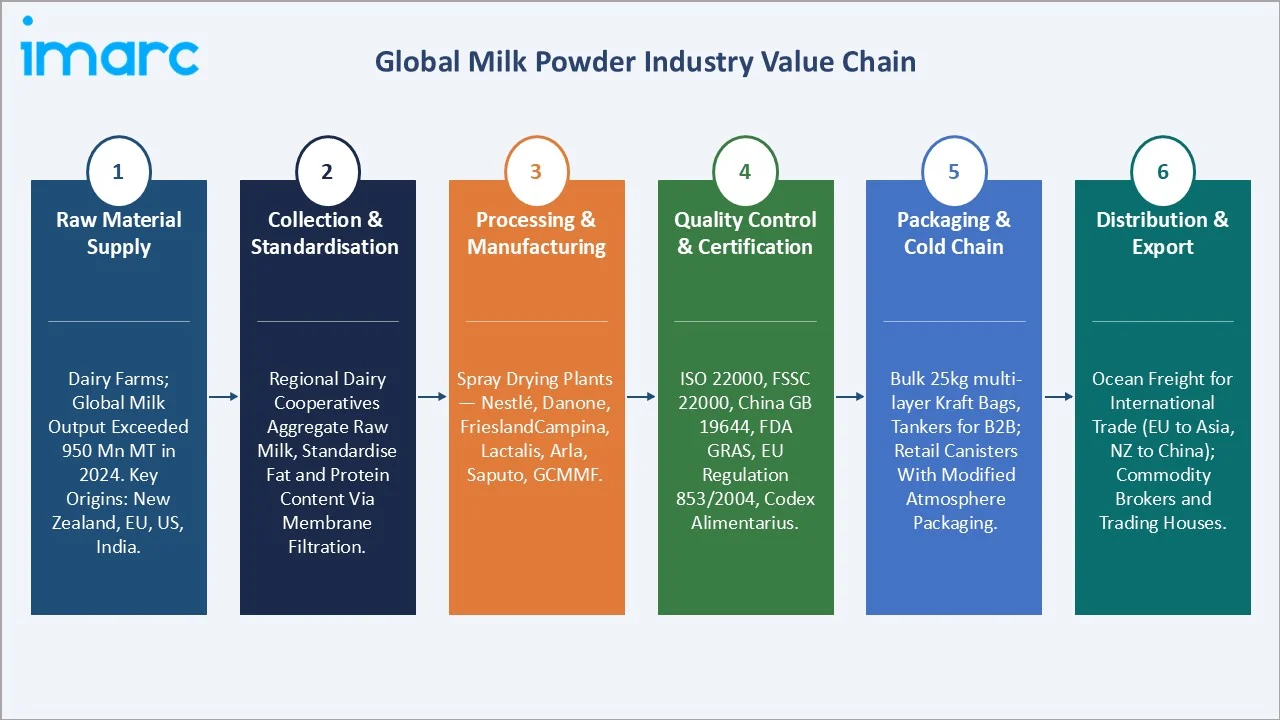

Industry Value Chain Analysis

The global milk powder industry value chain spans five integrated stages from raw milk collection through end-consumer delivery. Each stage presents distinct competitive dynamics and technology investment requirements relevant to the overall milk powder industry analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Material Supply |

Dairy farms – global milk output exceeded 950 million metric tons in 2024. New Zealand, EU member states, US, and India are the dominant supply origins. Herd productivity, feed costs, and climate variability are key input factors. |

|

Collection & Standardisation |

Regional dairy cooperatives aggregate raw milk, standardise fat and protein content via separation and membrane filtration, ensuring consistent input quality for downstream spray dryers. |

|

Processing & Manufacturing |

Spray drying plants – operated by global OEMs including Nestlé, Danone, FrieslandCampina, Lactalis, Arla Foods amba, Saputo Inc., GCMMF– convert liquid concentrates into commercial WMP, SMP, and specialty powder grades. |

|

Quality Control & Certification |

ISO 22000, FSSC 22000, and market-specific approvals (China GB 19644, FDA GRAS, EU Regulation 853/2004) ensure compliance. Infant formula powders require additional auditing under Codex Alimentarius and national pharmaceutical frameworks. |

|

Packaging & Cold Chain |

Bulk packaging in 25 kg multi-layer Kraft bags and bulk tankers for B2B markets; consumer retail formats in 400 g to 2.5 kg canisters with modified atmosphere packaging (MAP) for extended shelf life. |

|

Distribution & Export |

Ocean freight is the primary mode for international trade (EU to Asia, NZ to China). Specialist commodity brokers, global trading houses (Louis Dreyfus, Olam), and direct retail distribution for branded consumer products. |

|

End Users |

Infant formula producers, confectionery & chocolate OEMs, bakery manufacturers, sports nutrition brands, institutional food services, and household consumers across 150+ countries. |

Global milk powder OEMs hold the highest strategic value – integrating commodity sourcing, advanced processing technology, and quality certification into turnkey product solutions. Meanwhile, digital trade platforms and direct-to-manufacturer procurement models are progressively shortening traditional distribution layers in industrial B2B channels.

Technology Landscape in the Milk Powder Industry

Spray Drying and Agglomeration Technology

Multi-stage spray drying with integrated fluid bed systems remains the dominant production technology, enabling tighter control over particle size, bulk density, and moisture content in milk powder manufacturing. Advances in modern installations have improved thermal efficiency, while leading equipment manufacturers continue to support global capacity expansion across key dairy-producing regions.

Membrane Filtration and Protein Standardisation

Ultrafiltration (UF) and microfiltration (MF) membrane systems enable precise adjustment of fat-to-protein ratios prior to drying, ensuring consistent batch quality and supporting customised product specifications for infant formula and sports nutrition customers. Membrane-based separation is also enabling the commercial production of specialty fractions including native whey and micellar casein powders.

Instant Powder and Lecithinisation

Lecithin coating applied during the final drying stage enhances the wettability and dispersibility of whole milk powder, enabling instant-grade products for consumer and foodservice use. The instant WMP segment is emerging as a key premium category, driven by rising global demand for convenience-oriented dairy formats.

Smart Manufacturing and IoT Integration

Industry 4.0 technologies are increasingly embedded in large-scale dairy drying operations. Real-time sensors monitoring inlet air temperature, outlet moisture content, and particle size enable automated process control, reducing energy consumption and improving first-pass quality yields.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Whole Milk Powder | 58.6% | 2025 |

| Function | Emulsification | 29.7% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | European Union | 32.4% | 2025 |

By Product Type

To access detailed market analysis, Request Sample

Whole Milk Powder leads the global milk powder market with a 58.6% share in 2025. WMP contains approximately 26% fat content, making it the preferred ingredient in confectionery, chocolate manufacturing, bakery, and recombined dairy applications. The global chocolate market grew by 7.4% in value, relies heavily on WMP as a primary functional input, sustaining structural volume demand. WMP is also the dominant format for household consumption in developing markets including China, Brazil, and Southeast Asia, where it serves as a cost-effective, shelf-stable substitute for fresh dairy products.

By Function

Emulsification represents the largest functional application at 29.7% in 2025. Milk powder phospholipids – particularly in WMP – are highly effective natural emulsifiers in processed food systems, stabilising fat-water interfaces in cream soups, sauces, and dairy-based beverages. The global food processing market value at USD 10 Trillion in value in 2025, creating an enormous and consistent demand base for emulsification-grade milk powder ingredients across multinational FMCG supply chains.

Regional Market Insights

|

Region / Country |

Share (2025) |

Key Growth Drivers |

|

European Union |

32.4% |

CAP dairy support, world-class export infrastructure, sustainability regulations, Arla & FrieslandCampina leadership |

|

New Zealand |

18.6% |

Fonterra co-operative model, pasture-fed quality premium, Asia Pacific export orientation |

|

China |

17.3% |

Infant formula regulation, domestic dairy development strategy, rising per-capita dairy consumption |

|

United States |

14.2% |

USDA dairy support programs, strong food processing sector, specialty and organic milk powder demand |

|

Brazil |

9.1% |

Regional dairy production expansion, growing domestic food processing, Latam export base |

|

Others |

8.4% |

Australia, India, Argentina, Ukraine – emerging export capacity and growing domestic consumption |

The European Union commands a 32.4% share of global milk powder revenue in 2025 – the largest of any single market bloc. EU dairy export competitiveness is reinforced by subsidised production support under the Common Agricultural Policy (CAP), rigorous quality standards, and the global reputational premium attached to European dairy brands. Germany, France, the Netherlands, and Ireland are the primary production hubs.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Nestlé |

NIDO, Nestlé Carnation |

Leader |

Global distribution, infant nutrition, premium brand equity |

|

Danone |

Aptamil, Cow & Gate |

Leader |

Infant formula leadership, medical nutrition, R&D depth |

|

FrieslandCampina |

Dutch Lady |

Leader |

EU and Asia Pacific dual-strength, cooperative model |

|

Lactalis |

Président, Lactel |

Leader |

European dairy scale, diversified portfolio, export reach |

|

Arla Foods amba |

Arla, Dano |

Challenger |

Organic dairy credentials, EU + Middle East network |

|

Saputo Inc. |

Saputo |

Challenger |

North America and Oceania dairy processing scale |

|

GCMMF |

Amul |

Emerging |

India domestic market leadership, cooperative strength |

The global milk powder market's competitive landscape reflects moderate concentration at the premium and infant formula tiers, with significant fragmentation in commodity WMP and SMP trade. The remainder is distributed across cooperative exporters, national dairy boards, and a large number of regional processors in the EU, Oceania, and emerging markets.

Key Company Profiles

Nestlé

Nestlé is a global food and beverage company headquartered in Switzerland, with a strong presence across packaged foods, beverages, and nutrition products. It operates in numerous countries worldwide and holds a leading position in categories such as infant nutrition, dairy, coffee, and health science.

- Product & Platform Portfolio: Nestlé's milk powder portfolio includes NIDO fortified whole milk powder, Nestlé Carnation evaporated and condensed milk products, and the Cerelac and Nan infant formula brands which utilise premium SMP as a primary ingredient. The NAN Pro and NAN Supreme ranges represent the company's premium infant formula tier globally.

- Recent Developments: In 2025, Nestlé is positioning its NAN Sinergity infant formula as a key growth driver, focusing on premium and science-based nutrition solutions. The product combines advanced milk-derived ingredients such as human milk oligosaccharides (HMOs) and probiotics, supporting the trend toward high-value, functional milk powder formulations. Its global rollout reflects increasing demand for premium infant nutrition products.

- Strategic Focus: Nestlé's strategy centres on premiumising its infant and maternal nutrition portfolio, expanding in high-growth emerging markets (India, Sub-Saharan Africa, Southeast Asia), and transitioning its dairy supply chain towards certified sustainable and regenerative sourcing standards by 2030.

FrieslandCampina

FrieslandCampina is a global dairy cooperative headquartered in the Netherlands, engaged in the production and distribution of a wide range of dairy-based nutrition products. The company operates across consumer dairy, infant nutrition, and specialized ingredients, serving markets in Europe, Asia, Africa, and the Americas.

- Product & Platform Portfolio: FrieslandCampina’s milk powder portfolio includes consumer brands such as Friso infant formula, Dutch Lady and Peak milk powders, and Rainbow dairy products. Its ingredients division, FrieslandCampina Ingredients, supplies high-quality skim milk powder (SMP), Whole Milk Powder, and specialized dairy ingredients including whey proteins, lactoferrin, and HMOs for infant nutrition and functional food applications..

- Recent Developments: In 2026, FrieslandCampina outlined its 2026 strategic priorities focused on improving cost efficiency, strengthening its ingredients and nutrition portfolio, and expanding higher-value dairy segments. The company is increasing emphasis on protein-rich and functional milk powder ingredients, while optimizing operations and integrating recent acquisitions to enhance profitability and global competitiveness.

- Strategic Focus: FrieslandCampina’s strategy focuses on premiumisation of infant and performance nutrition, expanding in high-growth markets such as China, Southeast Asia, and Africa, and enhancing sustainability across its dairy value chain. The cooperative is also prioritising carbon footprint reduction, responsible sourcing, and innovation in value-added dairy ingredients to support long-term growth.

Danone

Danone is a global food and beverage company headquartered in France, with a strong focus on health-oriented and nutrition-based products. The company operates across essential dairy, plant-based alternatives, infant nutrition, and specialized medical nutrition, serving consumers in markets worldwide.

- Product & Platform Portfolio: Danone's milk powder-intensive brands include Aptamil, Nutricia, Cow & Gate, and Milupa in infant formula; and Fortimel and Fortisip in medical nutrition. The Aptamil brand holds market leadership in the premium infant formula segment across the United Kingdom, Germany, and several key Asia Pacific markets including Hong Kong and Singapore.

- Recent Developments: In 2022, Danone reorganised its China dairy portfolio by exiting its longstanding partnership with China Mengniu Dairy. The company divested its stakes in Yashili International and Inner Mongolia Dairy to Mengniu, while simultaneously re-acquiring full ownership of Dumex Baby Food Co. Ltd - the Chinese infant milk formula manufacturer it had originally sold to Yashili in 2016. The restructuring reflected Danone's strategic refocus on directly controlled, premium infant nutrition assets in China.

- Strategic Focus: Danone's infant nutrition strategy focuses on premiumising its portfolio toward human milk oligosaccharide (HMO)-enriched formula and personalised nutrition offerings, while deepening its regulatory and scientific relationships with healthcare professionals in key markets including China, Indonesia, and Brazil.

Market Concentration Analysis

The global milk powder market exhibits a dual structure: moderate concentration at the branded and infant formula premium tier, coexisting with high fragmentation at the commodity WMP and SMP trading level. The top five players – Nestlé, Danone, FrieslandCampina, Lactalis, and Arla Foods amba, – collectively represent an estimated 35-42% of branded/value-added milk powder market revenue in 2025. Commodity milk powder trading, by contrast, is served by numerous national dairy cooperatives, regional processors, and specialist exporters.

The infant formula sub-segment within the broader milk powder market is among the most concentrated in global food production. Regulatory barriers to entry – including China's SAMR infant formula registration requirements – are sustaining this concentration at the premium tier.

Consolidation trends are apparent in cooperative mergers and cross-border acquisitions. FrieslandCampina's ongoing transformation programme indicate a broader industry shift toward fewer but higher-value production assets.

Investment & Growth Opportunities

Fastest-Growing Segments

Fortified and specialty milk powders including high-protein, organic, and HMO-enriched variants represent the premium growth tier, driven by rising demand for functional and value-added nutrition. Instant milk powder is also expanding steadily, supported by foodservice and convenience-led consumption. The foaming application segment is emerging as the fastest-growing functional category, driven by premiumisation trends in coffee and dessert applications.

Emerging Market Expansion

Sub-Saharan Africa represents a high-potential emerging market for milk powder demand, driven by strong population growth and the role of milk powder in affordable nutrition. Southeast Asia’s rising middle class is supporting premiumisation toward branded WMP and fortified variants. In India, the dairy cooperative sector is expanding spray-drying capacity, with new facilities being commissioned to meet growing domestic consumption.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the specialty nutrition landscape, with increased private equity interest in premium infant formula brands across Asia driven by strong margins and regulatory barriers. Corporate R&D is increasingly focused on bioactive milk components such as lactoferrin, immunoglobulins, and MFGM, which command significant premiums over standard milk powders. These developments are reinforcing the shift toward high-value, science-based dairy ingredients.

Future Market Outlook (2026-2034

The global milk powder market forecast projects steady value expansion from USD 38.5 Billion in 2025 to USD 61.3 Billion by 2034, at a CAGR of 5.15%. An intermediate milestone of USD 49.4 Billion is projected for 2030, reflecting consistent compound growth across both commodity and value-added product categories.

The European Union is expected to maintain its leadership in global milk powder exports, while New Zealand may face increasing competitive pressure from emerging dairy producers. China’s domestic dairy expansion is likely to moderate whole milk powder imports, while sustaining demand for skim milk powder in infant nutrition. The United States is positioned to expand its export presence, particularly in premium and organic specialty segments.

Technological advancements in the milk powder market include precision fermentation-derived dairy proteins, which are expected to complement conventional SMP in select functional applications, and AI-driven spray drying optimisation that enhances energy efficiency and yield. Core growth drivers—such as population expansion, infant nutrition demand, and processed food industry growth—remain strong, supporting long-term value creation across the industry.

Research Methodology

Primary Research

Primary research for this report involved structured interviews with more than 150 stakeholders across the global milk powder value chain, including dairy farm cooperative managers, milk powder plant operators, infant formula procurement specialists, retail category managers, and trade policy experts in the EU, New Zealand, China, and the United States. Survey instruments captured quantitative demand data, pricing expectations, and forward product development priorities.

Secondary Research

Secondary data sources include the FAO Dairy Price Index, USDA Foreign Agricultural Service dairy trade statistics, EU Commission agricultural market reports, GlobalDairyTrade Holdings Limited (GDT) auction historical data, Codex Alimentarius Commission standards documentation, individual company annual reports and earnings releases, trade journals including Dairy Industries International and Food Business News, and academic and patent literature on dairy processing technology.

Forecasting Models

Market estimates use a bottom-up segmentation model validated by a top-down macroeconomic overlay. Demand forecasts integrate population and urbanisation projections (UN World Urbanisation Prospects 2024), FAO commodity price scenarios, infant formula market demand modelling, and food processing industry output trend analysis. CAGR projections are derived from a weighted average of segment-level growth scenarios adjusted for regulatory, technological, and trade policy risk factors.

Milk Powder Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Whole Milk Powder, Skimmed Milk Powder |

| Functions Covered | Emulsification, Foaming, Flavouring, Thickening |

| Applications Covered | Infant formula, Confectionery, Sports and Nutrition Foods, Bakery Products, Dry Mixes, Fermented Milk Products, Meat Products, Others |

| Regions Covered | European Union, New Zealand, China, United States, Brazil, Others |

| Companies Covered | Nestlé, Danone, FrieslandCampina, Lactalis, Arla Foods amba, Saputo Inc., GCMMF., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the milk powder market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global milk powder market.

- The study maps the leading, as well as the fastest growing, markets in the region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the milk powder industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Milk Powder Market Report

The global milk powder market size reached USD 38.5 Billion in 2025. It is projected to reach USD 61.3 Billion by 2034, growing at a CAGR of 5.15% during 2026-2034.

The market is projected to grow at a CAGR of 5.15% from 2026 to 2034, expanding from USD 38.5 Billion in 2025 to USD 61.3 Billion.

Whole Milk Powder dominates with 58.6% of global revenue in 2025, driven by extensive confectionery, bakery, and household consumption applications worldwide.

The European Union leads with 32.4% of global market share in 2025, supported by robust export infrastructure, CAP dairy support, and leading brands like Arla and FrieslandCampina.

Key drivers include global population growth and urbanization, expanding infant formula demand, rising health and wellness awareness, growth in confectionery and bakery industries, and advancements in dairy spray drying technology.

Major applications include infant formula, confectionery and chocolate, bakery products, sports nutrition, dry beverage mixes, fermented dairy products, and meat product processing across global food manufacturing.

Emulsification represents the largest functional application at 29.7% of global revenue in 2025, followed by thickening (26.3%), flavouring (23.5%), and foaming (20.5%).

Leading companies include Nestlé, Danone, FrieslandCampina, Lactalis, Arla Foods amba, Saputo Inc., and GCMMF.

The global milk powder market is projected to reach USD 49.4 Billion by 2030, representing a compound expansion of approximately 5.15% per year from the 2025.

Key challenges include raw milk price volatility impacting processor margins, stringent food safety and infant formula regulatory standards, supply chain complexity across global trade routes, and competition from plant-based dairy alternatives.

Fortified and specialty milk powders, including organic, high-protein, and HMO-enriched variants, are the fastest-growing premium tier, advancing at estimated CAGRs of 7-9% through 2034 globally.

Key trends include the rise of organic and clean-label powders, plant-based hybrid formulations, bioactive protein fractions (lactoferrin, MFGM), sustainability-led supply chains, and infant formula premiumization in Asia Pacific and Africa.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)