Millet Market Size, Share, Trends and Forecast by Product Type, Application, Distribution Channel, and Region, 2026-2034

Millet Market Size, Share, Trends & Forecast (2026-2034)

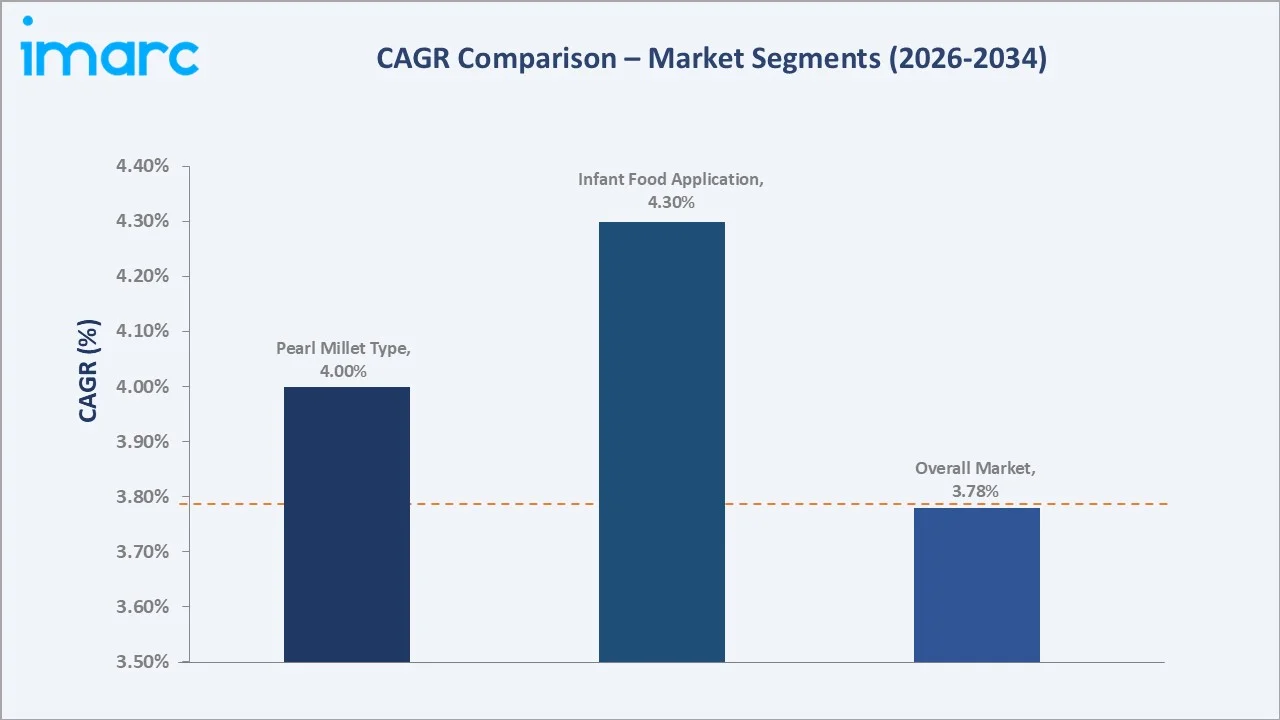

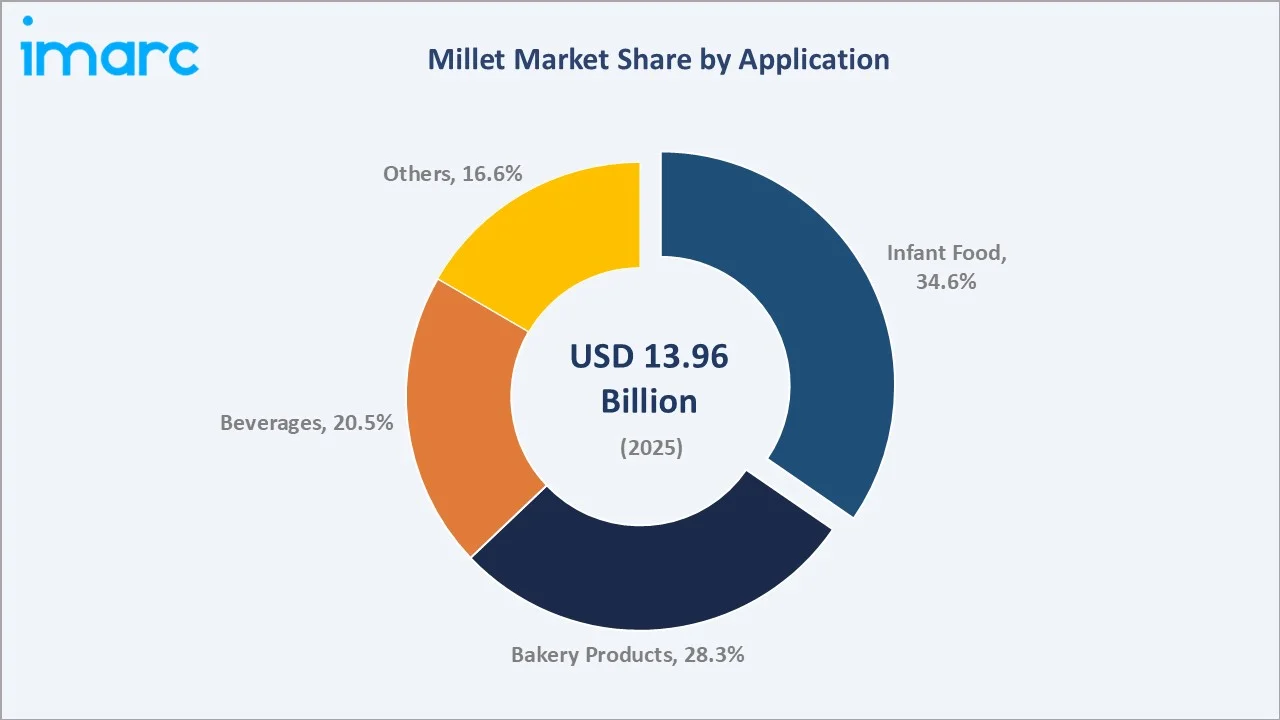

The global millet market reached USD 13.96 Billion in 2025 and is projected to reach USD 19.69 Billion by 2034, growing at a CAGR of 3.78% during 2026-2034. Market growth is driven by rising consumer demand for gluten-free and nutritionally dense grains, the landmark impact of the United Nations International Year of Millets (IYM) 2023, government agricultural promotion programs, and expanding commercial use in infant food, bakery products, and beverages.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.96 Billion |

|

Forecast Market Size (2034) |

USD 19.69 Billion |

|

CAGR (2026-2034) |

3.78% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

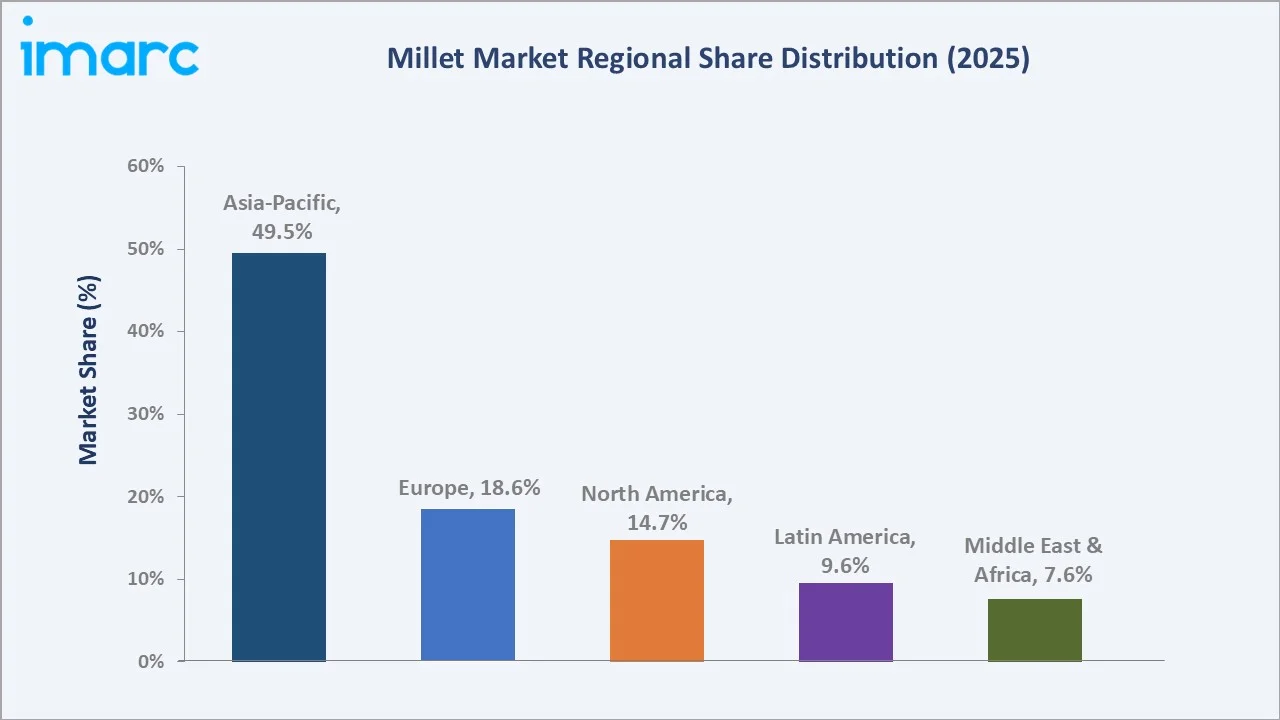

Asia-Pacific's commanding 49.5% share reflects the region's dual role as both the world's largest millet producer and consumer, with India accounting for approximately 40% of global production and China, Nigeria, and Ethiopia collectively adding substantial volume. Pearl millet's 46.3% type dominance reflects its broad adaptability to arid and semi-arid growing conditions, wide deployment as both a food crop and animal feed, and its strong demand profile in Sub-Saharan Africa and South Asia.

To get more information on this market, Request Sample

The market's 3.78% CAGR is supported by structural demand drivers, including millet's nutritional advantages over mainstream cereals, its drought and heat tolerance that positions it as a climate-resilient crop of growing strategic importance, and a sustained wave of government and international organization-backed promotion that has elevated millet's global consumer profile since the IYM 2023 campaign.

Executive Summary

The global millet market is on a consistent growth trajectory, transitioning from its traditional role as a subsistence staple in South Asia and Sub-Saharan Africa to a globally recognized functional food ingredient with established commercial applications across infant food, bakery, beverage, and snack categories. From USD 13.96 Billion in 2025, the market will reach USD 19.69 Billion by 2034, generating USD 5.73 Billion in incremental value at a 3.78% CAGR.

Pearl millet leads the type segment at 46.3%, driven by its extremely broad cultivation range and its dual role as a food and feed crop. Infant food leads the application segment at 34.6%, where millet's iron, zinc, and calcium content and its hypoallergenic profile make it an increasingly preferred weaning food ingredient, particularly in African and Asian markets where millet-based infant porridges are a cultural staple.

Key players, including Archer Daniels Midland Company, Cargill, Incorporated, BrettYoung, and Ernst Conservation Seeds, span the full millet value chain from seed development and production through grain processing, distribution, and food product ingredient supply.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Pearl Millet – 46.3% share (2025) |

|

Fastest Growing Type |

Finger Millet – driven by superfood positioning in developed markets |

|

Largest Application |

Infant Food – 34.6% share (2025) |

|

Fastest Growing Application |

Infant Food – ~4.30% CAGR (nutrition-led demand) |

| Leading Region | Asia-Pacific – 49.5% share (2025) |

|

Top Companies |

Archer Daniels Midland Company, Cargill, Incorporated, BrettYoung, and Ernst Conservation Seeds |

Key Analytical Observations:

- Pearl millet at 46.3% (2025) dominates the type segment due to its exceptional adaptability to arid, semi-arid, and low-fertility soils across Sub-Saharan Africa, South Asia, and the US Great Plains. Its high energy density, rich iron and zinc content, and lower anti-nutritional factor profile versus sorghum make it the preferred millet variety for food-grade commercial processing.

- Infant food applications lead at 34.6% (2025) because millet's nutritional profile, high iron (3.3–14.8 mg/100g in finger millet), calcium (344 mg/100g), dietary fiber, and essential amino acids directly address the micronutrient deficiencies prevalent in infant populations across developing markets.

- Bakery products at 28.3% (2025), where millet flour is gaining shelf space in gluten-free bread, cookie, and cracker formulations as consumers seek grain-free and whole-grain alternatives to wheat-based products.

- Beverages at 20.5% (2025) represent a growing and commercially innovative application segment, encompassing traditional fermented millet beverages dominant in West Africa, kombucha-style probiotic millet drinks gaining traction in premium health food channels, and craft beer brewers using millet as a gluten-free malt alternative for the growing gluten-sensitive consumer segment.

Millet Market Overview

Millets are a diverse group of small-seeded annual cereal grasses cultivated across arid and semi-arid regions globally. Primary species include pearl millet, finger millet, proso millet, foxtail millet, and barnyard millet. In 2023, global millet production reached 90.5 million metric tons (MMT), making it the world's fifth most important cereal crop group after wheat, rice, maize, and sorghum.

The International Year of Millets (IYM) campaign engaged more than 138 million users through social media and facilitated over 100 events across 35 countries. It effectively raised awareness of millets’ contribution to food security, climate resilience, and improved nutrition. The IYM 2023 momentum is sustaining ongoing market development through residual awareness, established food service relationships, and expanded retail distribution channels.

Market Dynamics

To evaluate market opportunities, Request Sample

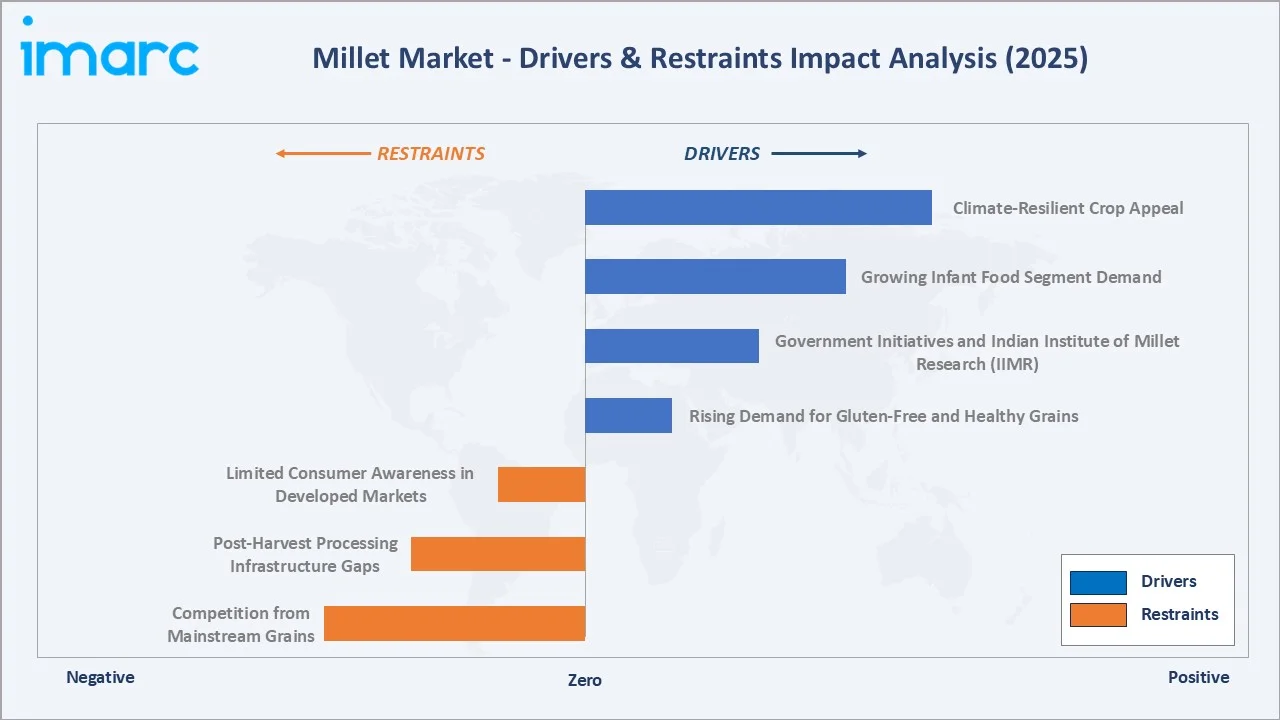

Market Drivers

- Rising Demand for Gluten-Free and Healthy Grains: The global gluten-free products market reached a value of USD 23.6 Billion in 2025, growing at 8%+ annually as coeliac disease diagnosis rates increase and non-coeliac gluten sensitivity gains mainstream consumer awareness.

- Government Initiatives and Indian Institute of Millet Research (IIMR): The UN's designation of 2023 as the International Indian Institute of Millet Research in Hyderabad established over 500 millet start-ups, aggregating INR 1,000 crore in funding rounds, leading to high consumption demand in the country.

- Growing Infant Food Segment Demand: The global baby food and infant formula market is projected to reach USD 89.0 Billion by 2034, with millet-based infant cereals representing a rapidly growing sub-segment. Millet's high calcium content (finger millet at 344 mg/100g versus 28 mg/100g in rice) supports infant bone development, and its iron content addresses iron-deficiency anaemia prevalent among infants.

- Climate-Resilient Crop Appeal: Millets are highly resilient to high temperatures and drought-prone conditions, requiring only around 350 mm of water compared with approximately 1,200 mm required for rice. Over 20 countries have incorporated millet production expansion into their national climate adaptation agricultural strategies, with incentivized cultivation programs providing guaranteed floor prices and subsidized inputs to millet farmers.

Market Restraints

- Limited Consumer Awareness in Developed Markets: Despite the IYM 2023 awareness boost, millet remains an unfamiliar grain to a majority of consumers in North America, Western Europe, and East Asia. Consumer purchase intent surveys indicate that 65–70% of US and EU consumers have never purchased a millet product.

- Post-Harvest Processing Infrastructure Gaps: Traditional millet dehulling and milling is a time-intensive manual process that has historically constrained commercial-scale millet flour and grain supply. Modern roller mill and attrition mill processing of millet is technically challenging due to the grain's small size, hard seed coat, and variable moisture content.

- Competition from Mainstream Grains: Rice and wheat, with their established supply chains, consumer familiarity, subsidized pricing in many developing markets, and superior processing characteristics, create persistent competitive headwinds for millet market expansion.

Market Opportunities

- Millet-Based Functional Food and Nutraceutical Products: High-value millet extract products, millet protein concentrates, millet bran antioxidant extracts, beta-glucan-rich millet fractions, and fortified millet composites are emerging as premium ingredients for sports nutrition, gut health, and cardiovascular wellness product formulations.

- E-Commerce and Direct-to-Consumer Millet Brand Development: Digital-native millet brand companies are building direct consumer relationships through e-commerce channels that bypass traditional grocery retail barriers, enabling higher margin capture and faster product iteration.

Market Challenges

- Standardization of Millet Product Quality and Grading: Unlike rice and wheat, which have established international quality grading standards, millet lacks widely adopted global grading systems covering varietal purity, mycotoxin levels, moisture content, and nutrient profile specifications.

- Short Shelf Life and Storage Challenges: Millet grain and flour have shorter shelf lives than rice and wheat due to their higher fat content and susceptibility to lipid oxidation. Millet flour becomes rancid within 30–60 days of milling at ambient temperatures, requiring either refrigerated storage or immediate use after milling.

Emerging Market Trends

.webp)

1. Ramoji Group Sabala Millets Launch

In November 2024, India's Ramoji Group launched the Sabala Millets brand, comprising 45 millet-based products positioned around preservative-free, nutrient-rich formulations. The launch included millet-based ready-to-cook products, health bars, and snacks, targeting India's health-conscious urban middle class through modern retail and e-commerce channels. This launch represents the entry of large-scale Indian conglomerates into the millet value-added product category.

2. Jammu and Kashmir Agriculture Millet Initiative

In February 2023, the Jammu and Kashmir government launched a three-year initiative to revive traditional millet cultivation across 8,000 hectares and double productivity from 10 to 20 quintals per hectare. The project includes subsidized seeds, support for processing units and millet restaurants, and efforts to promote climate-resilient crops and farmer entrepreneurship.

3. Millet Inclusion in Institutional Food Programs

Multiple state governments in India have mandated millet inclusion in school mid-day meal programs, Integrated Child Development Services (ICDS) supplementary nutrition, and the Public Distribution System (PDS) covering 800 million beneficiaries. Rajasthan, Karnataka, Odisha, and Telangana have introduced millet-based recipes in their school meal menus, creating structured government procurement demand.

4. Premium Millet Craft Beer and Functional Beverage Market

Great State Aleworks’ Millet Beer Project explores the use of locally grown millets, such as bajra and jowar, in Indian craft beer while creating demand for climate-resilient crops. In 2024, the brewery committed to using at least 5,000 kg of millet annually, sourcing directly from small farmers in drought-prone regions and sharing its brewing knowledge through an open-source handbook.

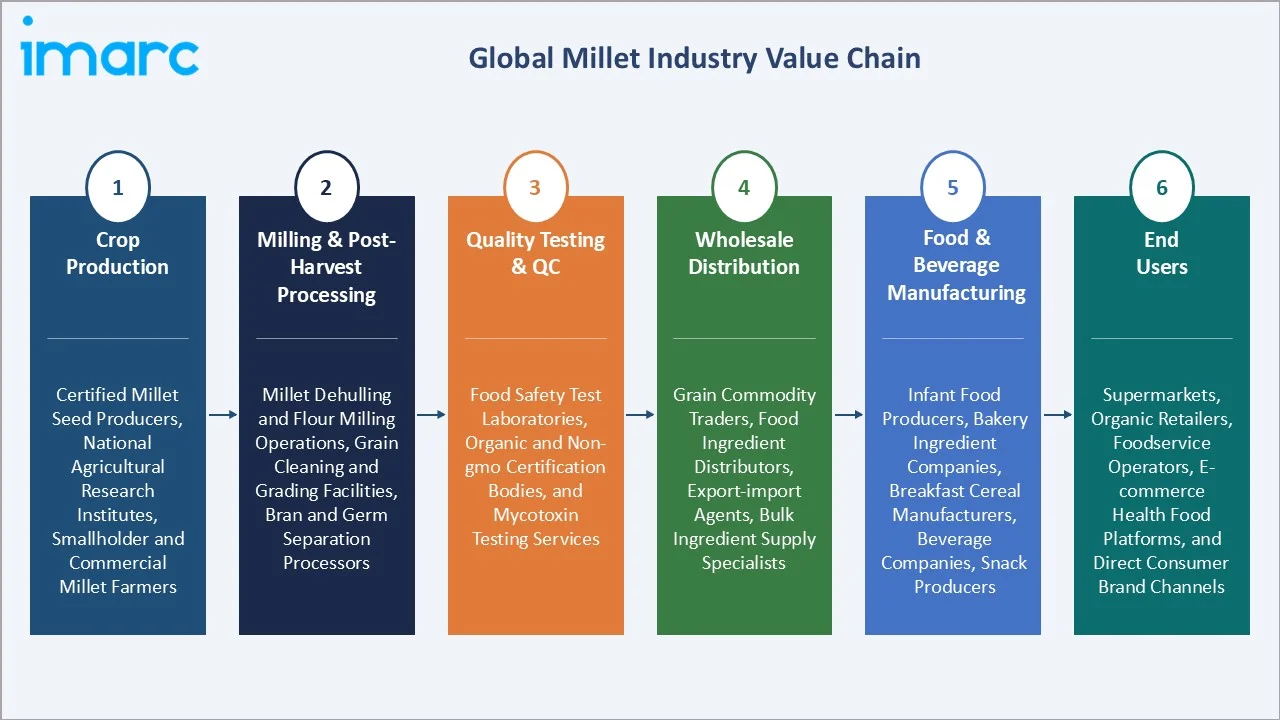

Industry Value Chain Analysis

The millet value chain spans certified seed development through farm production, post-harvest processing, food ingredient supply, and end-consumer product delivery, with the growing importance of quality certification and traceability at each stage.

|

Stage |

Key Players / Examples |

|

Crop Production |

Certified millet seed producers, national agricultural research institutes, smallholder and commercial millet farmers |

|

Milling & Post-Harvest Processing |

Millet dehulling and flour milling operations, grain cleaning and grading facilities, bran and germ separation processors |

|

Quality Testing & QC |

Food safety test laboratories, organic and non-GMO certification bodies, and mycotoxin testing services |

|

Wholesale Distribution |

Grain commodity traders, food ingredient distributors, export-import agents, bulk ingredient supply specialists |

| Food & Beverage Manufacturing | Infant food producers, bakery ingredient companies, breakfast cereal manufacturers, beverage companies, snack producers |

|

End Users |

Supermarkets, organic retailers, foodservice operators, e-commerce health food platforms, and direct consumer brand channels |

Technology Landscape in the Millet Industry

Millet Seed Technology and Hybrid Varieties

In January 2026, ICRISAT and ICAR developed RHB 273, the world’s first three-way pearl millet hybrid, combining high yield, drought tolerance, disease resistance, and improved fodder quality. Released for India’s dryland zones in Rajasthan, Gujarat, and Haryana, the hybrid produced about 2,230 kg/ha, achieving a 13–27% yield advantage over regional varieties.

Millet Processing and Milling Innovation

Modern millet processing addresses traditional limitations through purpose-designed abrasive dehullers, reduced-gap roller mills, and pin mills for fine flour. Jet milling and air classification fractionate flour into protein-rich and starch-rich streams. Germination and fermentation pre-processing reduce anti-nutritional factors by 40–80%, improving mineral bioavailability in infant food formulations.

Digital Supply Chain and Traceability

Blockchain traceability platforms are emerging for premium organic millet supply chains, enabling farm-to-shelf origin verification. Digital procurement platforms, including DeHaat, Ninjacart, and AgriBazaar, link Indian smallholder millet farmers directly to food company buyers, improving price discovery and reducing intermediary cost layers.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Pearl Millet | 46.3% | 2025 |

| Application | Infant Food | 34.6% | 2025 |

| Distribution Channel | Traditional Grocery Stores | 🔒 | 2025 |

| Region | Asia-Pacific | 49.5% | 2025 |

By Product Type

Pearl millet leads at 46.3% in 2025. It is the primary millet species cultivated and consumed across India's Rajasthan, Gujarat, and Haryana states and across West Africa's Sahelian belt, where it is the primary caloric source for hundreds of millions of people.

To access detailed market analysis, Request Sample

Finger millet at 24.7% in 2025 is the nutritionally densest millet species, with exceptionally high calcium, iron, and amino acid leucine content, making it the preferred millet variety for infant food and health food product formulations. Proso millet at 16.8% serves primarily the North American and Eastern European birdseed and organic grain market, with growing use in craft brewing and organic breakfast cereals.

By Application

Infant food leads at 34.6% in 2025. The application benefits from millet's superior micronutrient profile for infant nutrition, cultural embeddedness of millet porridges as first foods in South Asia and Sub-Saharan Africa, and the WHO's recommendation of millet-based complementary foods for weaning from 6 months.

Bakery products at 28.3% in 2025, with gluten-free bread, muffin, cracker, and cookie formulations incorporating millet flour as a nutritionally superior alternative to rice flour. Beverages at 20.5% span traditional fermented drinks in Africa to premium craft beer and health drinks in developed markets.

Regional Market Insights

Asia-Pacific dominates the global millet market with a 49.5% share in 2025. India anchors the region as the world's largest millet producer and consumer, with millet forming a dietary staple across multiple states and the government's active Millets Mission driving both production expansion and commercial product development.

Europe's 18.6% share reflects Germany and France's mature gluten-free food markets and the rapid growth of organic grain channels that have made millet a premium shelf staple in natural and organic retailers. The Middle East & Africa region at 7.6% represents significant volume given Africa's role as a major millet production and consumption region, with Nigeria, Niger, and Burkina Faso among the world's top millet-producing countries.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

49.5% |

India's dominant production and consumption, Japan and South Korea's health food demand, and China's growing foxtail and proso millet cultivation. |

|

Europe |

18.6% |

Gluten-free product demand in Germany, the UK, and France, craft beer millet adoption, and premium health food retail channel expansion. |

| North America | 14.7% | US gluten-free consumer demand, proso millet birdseed and organic grain market, craft brewing millet usage, and specialty health food retailer distribution growth. |

|

Latin America |

9.6% |

Brazil's growing demand for alternative grains, animal feed usage, and the emerging millet-based food product market is driven by health-conscious urban consumers. |

|

Middle East and Africa |

7.6% |

Traditional pearl and finger millet staple consumption in West and East Africa, infant food institutional demand, and millet production expansion in Nigeria, Niger, and Ethiopia. |

Competitive Landscape

The global millet market is fragmented, with no single company holding a dominant market position across all geographies and value chain stages. Archer Daniels Midland Company and Cargill, Incorporated are the most globally present players through their grain trading and processing operations.

| Company | Brand / Division | Market Position | Key Strength |

|---|---|---|---|

| Archer Daniels Midland Company | HarvestEdge | Market Leader | Millet procurement and distribution; ingredient supply to food manufacturers globally |

| Cargill, Incorporated | Cargill | Market Leader | Grain trading and processing infrastructure; food-grade millet supply; animal feed millet distribution |

| BrettYoung | BrettYoung | Challenger | North American proso millet and foxtail millet seed supply; certified organic seed varieties; prairie region expertise |

| Ernst Conservation Seeds | Ernst Conservation Seeds | Challenger | Specialized native and warm-season millet seed varieties; U.S. conservation and wildlife habitat planting markets |

Market participants are increasingly investing in millet-based product innovation, improved crop varieties, sustainable sourcing, and partnerships with farmers to capitalize on rising demand for nutritious, gluten-free, and climate-resilient food products.

Key Company Profiles

Archer Daniels Midland Company

Archer Daniels Midland Company is a global leader in agricultural commodity processing and food ingredient supply. ADM's millet operations encompass procurement from global production regions, grain processing, and supply of millet grain and flour ingredients to commercial food manufacturers.

- Product Portfolio: Millet grain procurement and trading, millet flour and grain ingredients for food manufacturers, and millet-based animal feed ingredient supply.

- Strategic Focus: Alternative and ancient grain ingredient portfolio expansion, food-grade millet procurement and supply chain development, nutritional ingredient product line broadening, and sustainability-linked grain sourcing programs.

Cargill, Incorporated

Cargill, Incorporated, is the world's largest privately held agricultural company with extensive grain trading, processing, and food ingredient operations. Cargill's millet market presence spans grain trading from Indian and African production origins through to food ingredient and animal feed supply.

- Product Portfolio: Millet grain trading and logistics, millet-based animal feed ingredients, food-grade millet supply for bakery and cereal ingredient customers, and specialty grain procurement services for food manufacturers.

- Recent Developments: In March 2025, at AAHAR 2025, Cargill, Incorporated showcased millet cookies among its chef-curated bakery applications, demonstrating the potential of millets in innovative, consumer-focused food products.

- Strategic Focus: Agricultural commodity chain efficiency improvement, sustainable sourcing certification for specialty grains, Indian and African millet supply base development, and food manufacturer ingredient supply partnership growth.

Market Concentration Analysis

The millet market is highly fragmented at the production level, with millions of smallholder farmers across India, Nigeria, Niger, and other producing countries holding no individual market power.

At the processing and commercial ingredient level, ADM and Cargill provide the largest global trading and ingredient supply capacities, but millet represents a small fraction of their overall grain portfolios. The seed segment is more concentrated, with Bayer and national research institutes dominating the improved hybrid seed supply.

Investment & Growth Opportunities

Fastest Growing Segments

Infant food millet applications (~4.30% CAGR), functional food and nutraceutical millet extracts (~8%+ CAGR), and gluten-free bakery millet flour are the highest-growth investment vectors through 2034, collectively representing a combined incremental addressable market of approximately USD 3 Billion by 2034.

Emerging Market Expansion

The European Union's Farm-to-Fork Strategy promotes diversification away from wheat and barley monocultures, with millet identified as a resilient alternative suitable for Mediterranean and Eastern European agricultural regions. The EU's Horizon Europe research program is funding millet variety development, processing optimization, and consumer acceptance studies across six member states.

Venture and Institutional Investment Trends

- Impact investment funds, including AgDevCo and Acumen, are funding millet processing capacity in Sub-Saharan Africa, building food-grade flour milling and quality certification infrastructure to enable commercial export of African millet grain to European food manufacturers.

- The Gates Foundation and World Food Program are co-investing in millet crop improvement, post-harvest technology, and market linkage programs across Nigeria, Senegal, and Ethiopia, creating structured institutional demand and supply chain development support.

Future Market Outlook (2026-2034)

The global millet market will reach USD 19.69 Billion by 2034 from USD 13.96 Billion in 2025, adding USD 5.73 Billion at a 3.78% CAGR. The market's trajectory will be shaped by the sustained conversion of IYM 2023 awareness into commercial product development, growing gluten-free and whole grain consumer demand in developed markets, and expanding institutional and government-driven demand in developing markets through school meals, public distribution, and food security programs.

Infant food will extend its market leadership as child nutrition programs expand access to millet-based weaning foods across Africa and South Asia. Bakery and beverage applications will grow fastest in North America and Europe, driven by premium health food positioning. Asia-Pacific will retain its dominant share, while the Middle East & Africa region will grow its share as processing infrastructure develops and commercial food manufacturing expands.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including millet farmers, grain traders, food ingredient buyers, infant food manufacturers, and retail food buyers across Asia-Pacific, Europe, North America, and Africa. Expert input validated market sizing, application adoption trends, and regional market dynamics.

Secondary Research

Secondary research encompassed FAO cereal crop statistics, ICRISAT millet production data, national agriculture ministry reports, IYM 2023 impact assessments, company annual reports, and trade publications, including Cereal Foods World, Food & Beverage Technology, and World Grain.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting, incorporating global millet production volumes, price per ton trajectories, food-grade value-add processing penetration rates, regional consumption growth assumptions, and government program volume commitments. A base-case CAGR of 3.78% reflects validated consensus from industry expert interviews and publicly disclosed government millet procurement targets.

Millet Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Pearl Millet, Finger Millet, Proso Millet, Others |

| Applications Covered | Infant Food, Bakery Products, Beverages, Others |

| Distribution Channels Covered | Supermarket and Hypermarkets, Traditional Grocery Stores, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Archer Daniels Midland Company, Cargill, Incorporated, BrettYoung, Ernst Conservation Seeds, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the millet market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global millet market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the millet industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Millet Market Report

The market reached USD 13.96 Billion in 2025 and is projected to reach USD 19.69 Billion by 2034 at a 3.78% CAGR.

Asia-Pacific leads with a 49.5% share in 2025, anchored by India's dominant production and consumption and government Millets Mission programs.

Pearl millet leads at 46.3% in 2025, the most widely cultivated millet species globally, and a primary staple cereal in South Asia and Sub-Saharan Africa.

Infant food leads at 34.6% in 2025, leveraging millet's superior mineral profile for infant nutrition and the cultural tradition of millet porridges as weaning foods.

Archer Daniels Midland Company, Cargill, Incorporated, BrettYoung, and Ernst Conservation Seeds are some of the leading players in the market.

IYM 2023 generated over 2 Billion media impressions, triggered 40+ country-level policy actions, and catalyzed a wave of new millet product launches across infant food, bakery, and beverages globally.

Limited consumer awareness in developed markets, post-harvest processing infrastructure gaps, and competition from mainstream grains are key challenges.

Infant food is growing fastest at approximately 4.30% CAGR, driven by nutrition-led demand and institutional government programs across Africa and South Asia.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)