Mobile Advertising Market Size, Share, Trends and Forecast by Segment and Region, 2026-2034

Mobile Advertising Market Size, Share, Trends & Forecast (2026-2034)

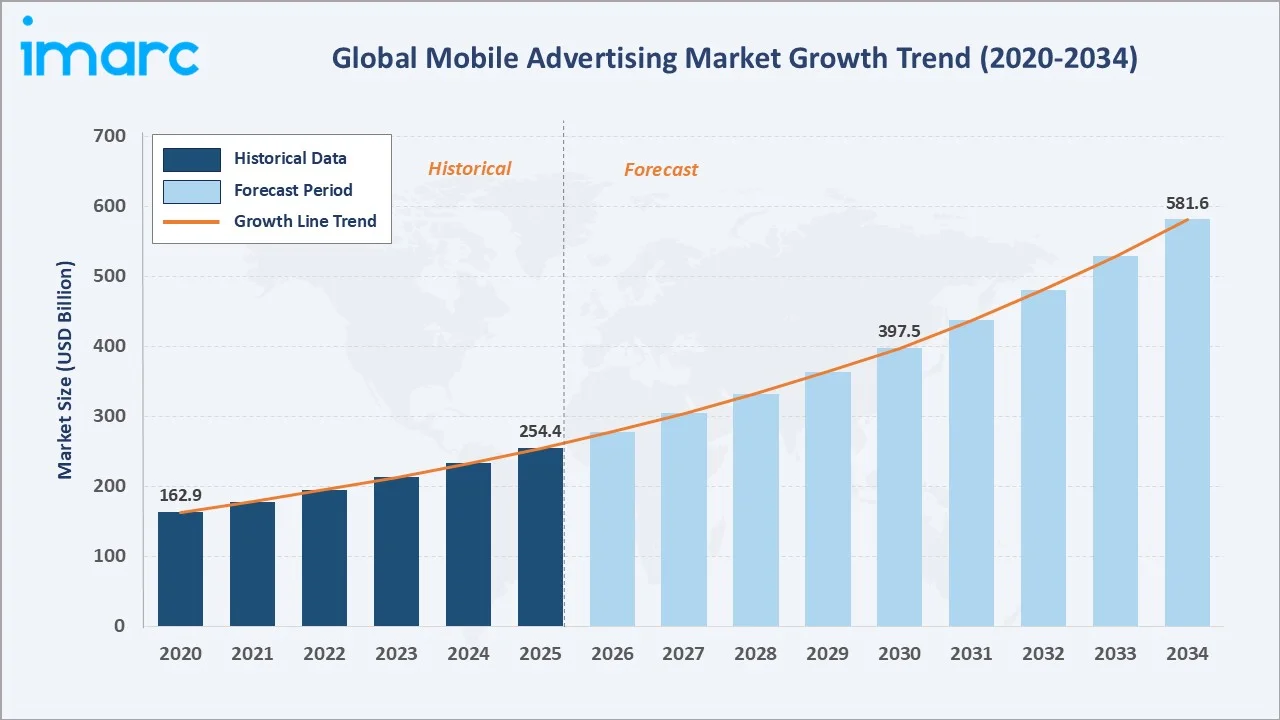

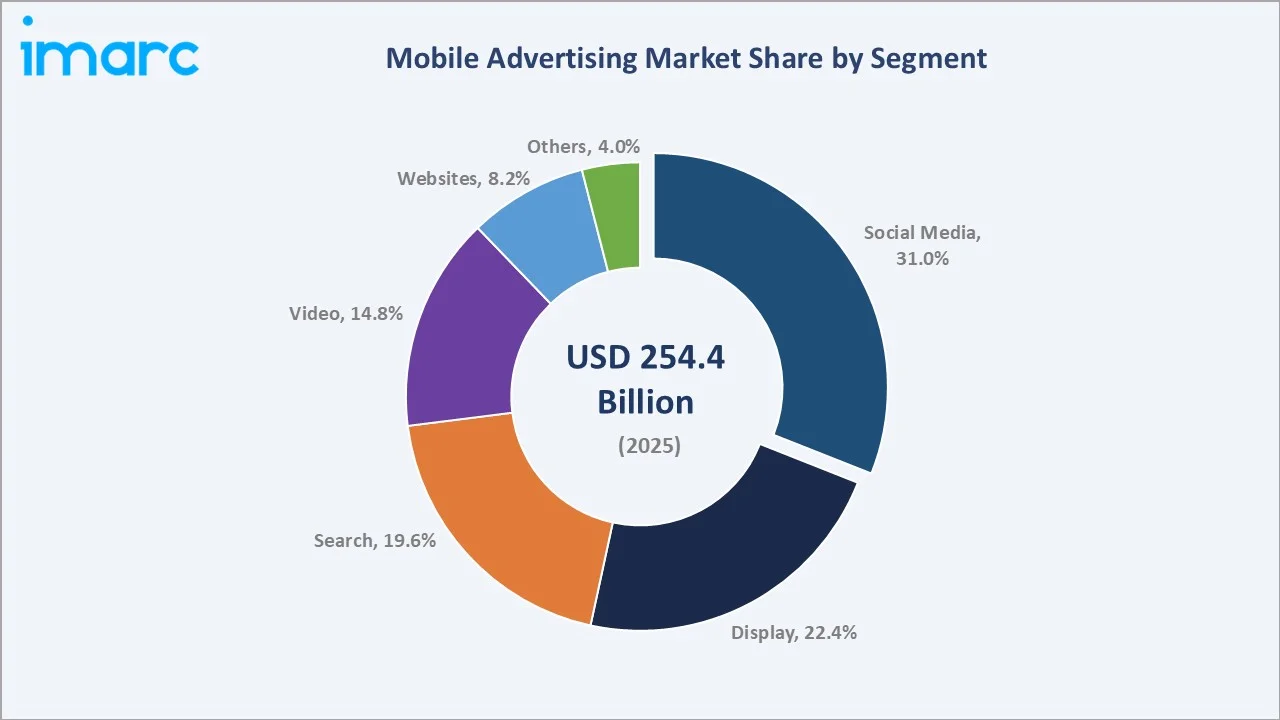

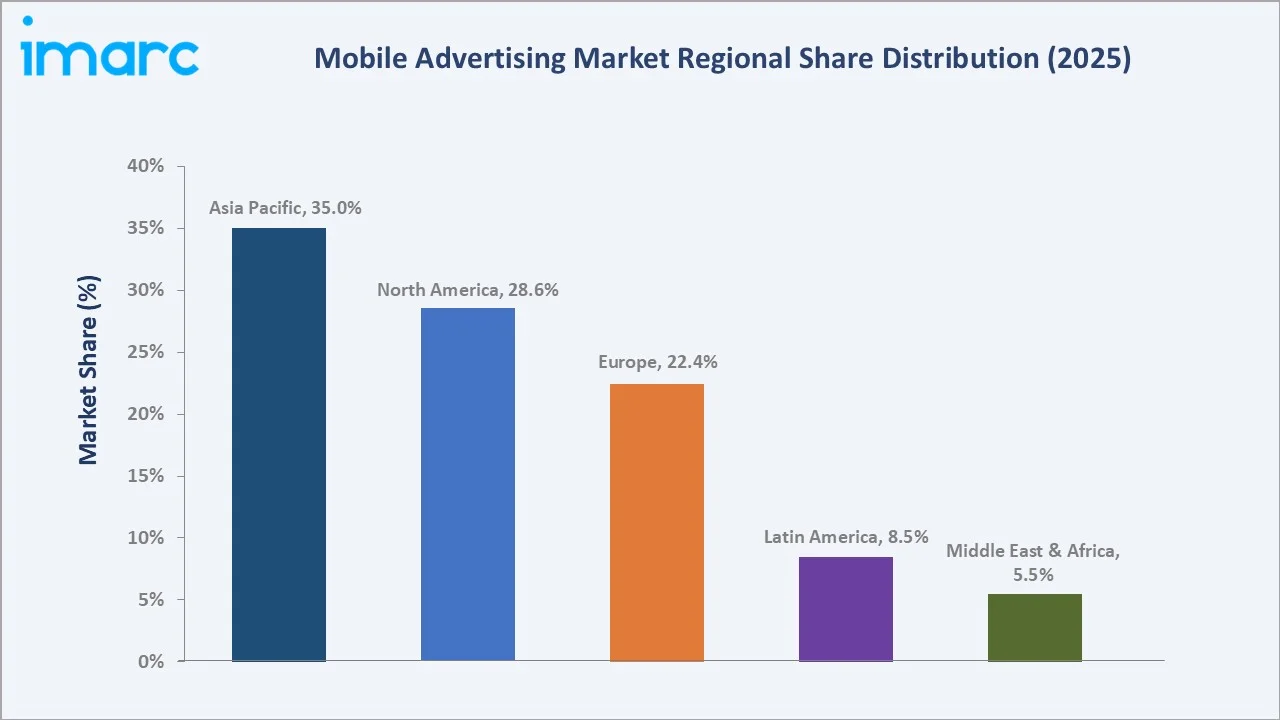

The global mobile advertising market reached USD 254.4 Billion in 2025 and is projected to reach USD 581.6 Billion by 2034, growing at a CAGR of 9.33% during 2026-2034. The market is driven by the increasing mobile phone penetration, with over 82% of individuals 10 years or older owning a mobile phone globally, growing mobile internet usage, and the demand for personalized, location-based advertising. Social media dominates segments at 31.0%. Asia Pacific leads regionally at 35.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 254.4 Billion |

|

Forecast Market Size (2034) |

USD 581.6 Billion |

|

CAGR (2026-2034) |

9.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Segment |

Social Media (31.0%, 2025) |

|

Leading Region |

Asia Pacific (35.0%, 2025) |

The market expanded from USD 162.9 Billion in 2020 to USD 254.4 Billion in 2025, anchored at USD 397.5 Billion in 2030, and forecast to reach USD 581.6 Billion by 2034. COVID-19 dramatically accelerated mobile screen time globally, and this consumption shift permanently elevated mobile advertising's share of total digital advertising, as advertisers reallocated TV and print budgets toward the screen where consumers now spend the majority of their media time.

To get more information on this market, Request Sample

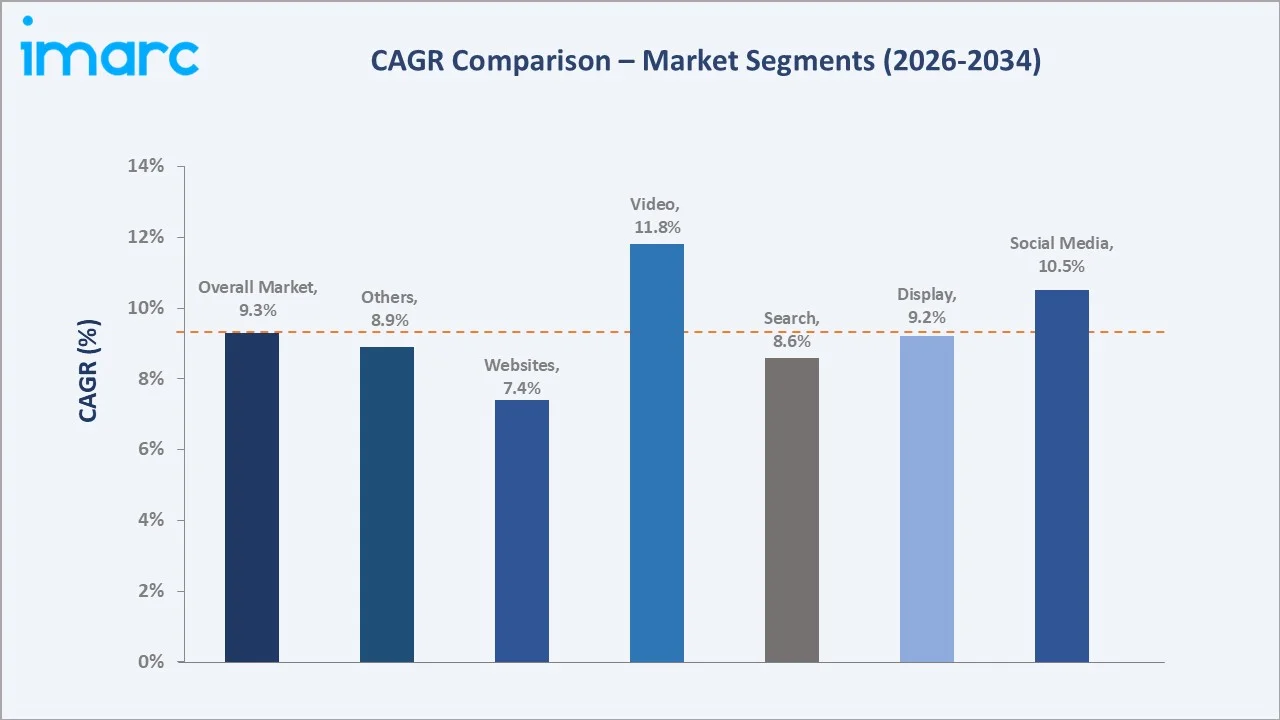

Video grows fastest at ~11.8% CAGR (2026-2034), driven by TikTok's active users consuming short-form video daily, YouTube shorts exceeding high daily views, and Instagram reels driving video ad spend migration from television. Social media at 31.0% is the dominant and second-fastest growing segment at ~10.5% CAGR.

Executive Summary

The global mobile advertising market reached USD 254.4 Billion in 2025, representing digital advertising spend and the world's largest advertising medium by revenue, surpassing television, print, and desktop digital combined. Mobile advertising has become the primary customer acquisition, retention, and revenue generation tool for the global digital economy, serving active advertisers globally ranging from Fortune 500 brand marketers to micro-SME performance advertisers. The market is projected to reach USD 581.6 Billion by 2034 at 9.33% CAGR.

Social media at 31.0% leads all segments through Meta's combined family of generating an opportunity in global advertising revenues. Video at 14.8% is growing fastest as Instagram’s unprecedented user engagement metrics attract brand advertising budgets previously allocated to broadcast television. Asia Pacific at 35.0% leads regionally through China's mobile advertising ecosystem and India's active mobile internet users, representing the world's fastest-growing mobile advertising market.

Key Market Insights

|

Insight |

Data |

|

Dominant Segment |

Social Media - 31.0% share (2025) |

|

Leading Region |

Asia Pacific - 35.0% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Social media at 31.0% driven by Meta's AI-powered mobile advertising ecosystem: Meta’s family of apps reached 3.98 billion monthly active users as of early 2025, an audience concentration enabling precision targeting at scale that no competitor can match.

- Asia Pacific at 35.0% dominated by China's mobile advertising super-apps and India's mobile-first digital economy: China's mobile advertising super-apps create a high revenue in domestic mobile advertising annually. India's internet user base crossed 950 million in 2025, representing the world's single largest growth market for mobile advertising.

Mobile Advertising Market Overview

The mobile advertising market encompasses all paid advertising formats delivered on mobile devices, including smartphones and tablets, across in-app environments, mobile web browsers, mobile search results, mobile video platforms, and messaging applications. The market serves active advertisers globally.

The ecosystem integrates advertisers, ad technology platforms, ad exchanges and networks, mobile publishers, mobile measurement partners, and global smartphone end users, generating the mobile screen time that the advertising industry monetizes. Privacy regulation is fundamentally reshaping mobile advertising's targeting infrastructure, creating a multi-year industry transition from device ID-based tracking toward privacy-preserving alternatives, including contextual targeting, first-party data, and federated learning.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

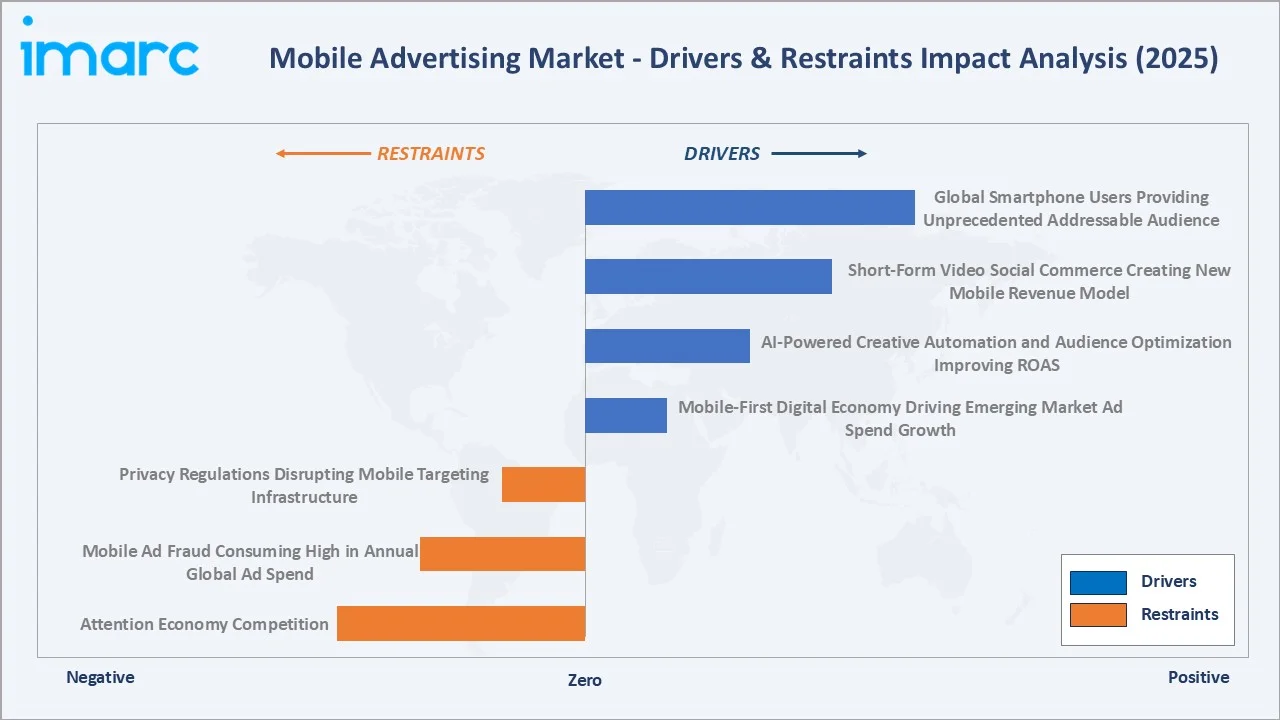

- Global Smartphone Users Providing Unprecedented Addressable Audience: There are over 7 billion smartphones in the world, with smartphones reaching high penetration in developed markets and growing at a high rate in emerging markets. Average global daily mobile screen time reached 4.8 hours in 2025, representing the world's largest single-medium audience by engaged time. This audience concentration provides mobile advertisers with inventory scale and frequency capability that no other advertising medium can match.

- Short-Form Video Social Commerce Creating New Mobile Revenue Model: Instagram Shopping's 130M monthly US shoppers, and YouTube Shopping's expanding product tagging capability collectively demonstrate that short-form video is transitioning from an entertainment medium to a commerce platform.

- AI-Powered Creative Automation and Audience Optimization Improving ROAS: Generative AI's integration into mobile advertising workflows is delivering measurable ROAS improvements of 15-30% versus manually managed campaigns. This ROAS improvement effect is self-reinforcing: improved returns attract additional ad spend, which generates more training data for AI optimization, further improving returns and attracting more spend.

Market Restraints

- Privacy Regulations Disrupting Mobile Targeting Infrastructure: GDPR enforcement against behavioral mobile advertising creates ongoing compliance costs and targeting restrictions for European mobile advertising.

- Mobile Ad Fraud Consuming High in Annual Global Ad Spend: App install fraud, where fraudsters claim credit for app installations through fake device ID spoofing, is estimated to affect most of the mobile app install campaign budgets. Major brands have disclosed pulling significant mobile advertising budgets following fraud investigations.

Market Opportunities

- Connected TV / Mobile Cross-Screen Advertising Creating New Measurement Frameworks: The convergence of streaming video consumption is creating cross-screen advertising opportunities where mobile data enhances CTV (Connected Television) targeting, and CTV completion rates validate mobile audience modeling.

- Generative AI Ad Creative Enabling Personalization at Scale: Large Language Models and image generation AI integrated into advertising workflow platforms are enabling automatic generation of thousands of ad creative variations personalized to different audiences, contexts, and geographies.

Market Challenges

- Attention Economy Competition Reducing Mobile Ad Engagement Rates: Average mobile banner click-through rates declined as mobile users developed effective ad avoidance behavior and ad blocking penetration reached high levels in some European markets. This engagement decline is forcing advertisers toward higher-cost but higher-engagement formats that command 3-8x higher CPMs than banner display. The fundamental challenge of earning attention in a mobile environment with daily brand impressions per user requires continuous creative innovation and format experimentation.

- App Store Policy Restrictions Limiting Mobile Advertising Measurement and Attribution: The measurement restriction reduces advertisers' confidence in ROAS calculations for iOS campaigns, compressing iOS campaign investment and shifting mobile advertising budgets toward Android platforms with less restrictive tracking policies, creating a bifurcated mobile advertising measurement environment.

Emerging Market Trends

1. Generative AI Transforming Mobile Creative Production and Campaign Optimization

Generative AI is transforming mobile advertising by enabling faster, more personalized creative production and real‑time campaign optimization. It helps brands automatically generate tailored ad content at scale and refine targeting and performance, improving engagement and advertising efficiency across mobile platforms.

2. Mobile Social Commerce Eroding the E-Commerce Purchase Funnel

Mobile social commerce is reshaping the e‑commerce purchase funnel by enabling users to discover and buy products directly within social apps. This blurs the traditional path from browsing to purchase, making social engagement a critical touchpoint in mobile advertising and driving higher conversions through integrated shopping experiences.

3. Cookieless Identity Solutions Racing to Replace Third-Party Mobile Identifiers

Cookieless identity solutions are rapidly emerging as alternatives to third‑party mobile identifiers, enabling marketers to track and target users while maintaining privacy compliance. These solutions support effective audience measurement and personalization in a landscape where traditional identifiers are being phased out.

4. In-App Bidding and First-Party Data Reshaping Mobile Publisher Monetization

In-app bidding (IAB), where multiple demand sources compete simultaneously for each impression through a real-time auction within the publisher's app, has replaced the waterfall monetization model for premium mobile publishers. In‑app bidding and first‑party data also enable publishers to maximize revenue through real‑time competition for ad impressions and deeper audience insights. This trend allows publishers to better leverage their own customer data for more effective targeting and higher yield, reducing reliance on traditional ad networks.

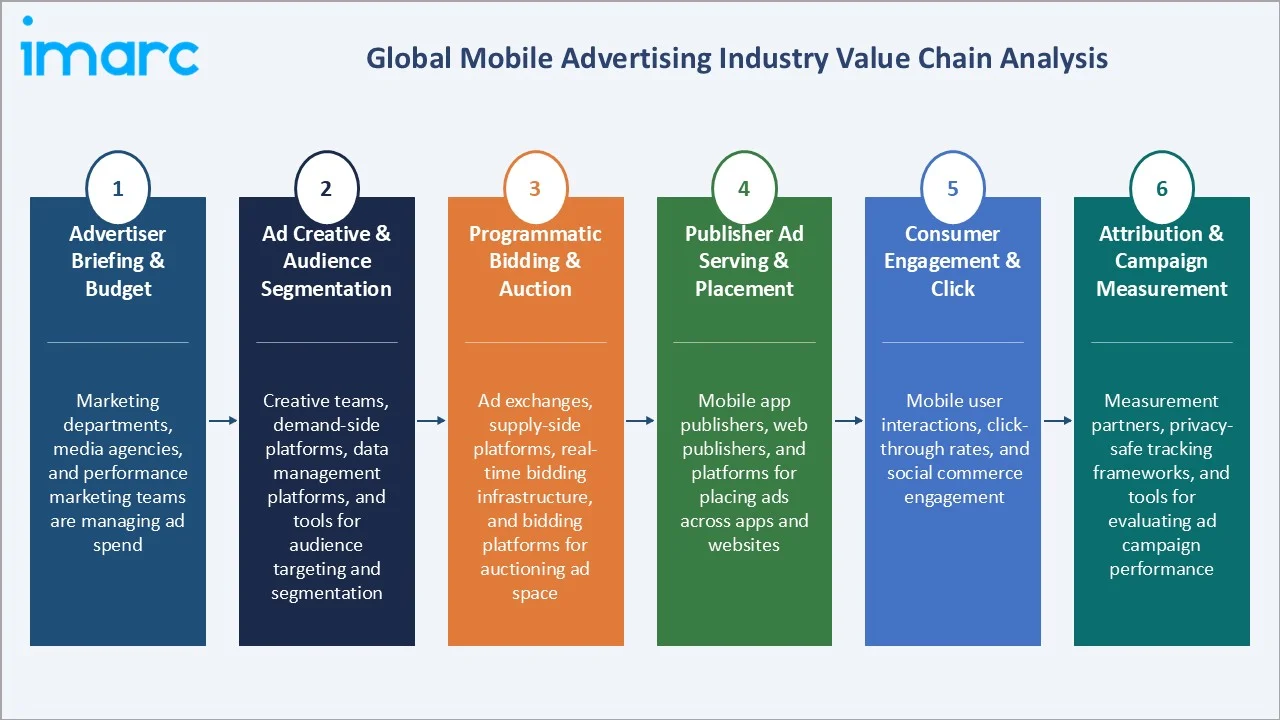

Industry Value Chain Analysis

The mobile advertising value chain integrates advertiser demand through agencies and brand-direct teams, ad technology platforms, programmatic exchanges and ad networks, mobile publisher inventory, consumer engagement, and performance measurement through mobile measurement partners. Platform intermediaries capture 60-70% gross margins on mobile advertising revenues while open programmatic ecosystem players earn 15-25% technology fees on transaction value.

|

Stage |

Key Participants |

|

Advertiser Briefing & Budget |

Marketing departments, media agencies, and performance marketing teams are managing ad spend. |

|

Ad Creative & Audience Segmentation |

Creative teams, demand-side platforms, data management platforms, and tools for audience targeting and segmentation. |

|

Programmatic Bidding & Auction |

Ad exchanges, supply-side platforms, real-time bidding infrastructure, and bidding platforms for auctioning ad space. |

|

Publisher Ad Serving & Placement |

Mobile app publishers, web publishers, and platforms for placing ads across apps and websites. |

|

Consumer Engagement & Click |

Mobile user interactions, click-through rates, and social commerce engagement. |

|

Attribution & Campaign Measurement |

Measurement partners, privacy-safe tracking frameworks, and tools for evaluating ad campaign performance. |

The mobile measurement and attribution tier has become the most strategically critical and contested value chain tier as privacy regulations fragment mobile identity. MMPs that successfully develop privacy-preserving attribution methodologies command premium positioning as the measurability infrastructure that justifies continuing advertiser investment in mobile advertising despite tracking restrictions.

Technology Landscape in the Mobile Advertising Industry

Programmatic Real-Time Bidding Infrastructure

Programmatic real-time bidding (RTB) infrastructure enabling advertisers to bid for ad impressions in real-time. This technology streamlines the ad-buying process, ensuring optimal targeting, cost-efficiency, and speed. It facilitates automated, data-driven decisions for ad placements, allowing advertisers to reach the right audience at the right moment, enhancing overall campaign performance and maximizing return on investment.

AI and Machine Learning in Campaign Optimization

AI and machine learning are transforming the mobile advertising industry by enabling advanced campaign optimization. These technologies analyze vast amounts of consumer data in real time, predicting behaviors, and automating decisions to personalize ad content, targeting, and bidding strategies. By continuously learning from user interactions and campaign performance, AI and machine learning enhance ad effectiveness, improve ROI, and ensure more efficient use of advertising budgets.

Privacy-Preserving Advertising Technologies

Privacy-preserving advertising technologies are reshaping the mobile advertising industry by enabling targeted ad campaigns while safeguarding user privacy. These technologies, such as data anonymization, consent management, and privacy-focused tracking, ensure compliance with regulations like GDPR and CCPA. They allow advertisers to gather valuable insights without compromising user trust, maintaining data security, and offering a transparent, privacy-respecting environment, which is crucial in a post-cookie world.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Segment |

Social Media |

31% |

2025 |

|

Region |

Asia Pacific |

35% |

2025 |

By Segment

Social media leads at 31.0% market share (2025). Meta's family of apps, such as Facebook, Instagram, WhatsApp, and Messenger, collectively generate the majority of social media mobile advertising revenue globally. As of early 2025, Meta’s suite of apps boasts 3.98 billion monthly active users, with Facebook accounting for approximately 3.07 billion monthly active users in 2025. WhatsApp has surpassed 3.3 billion active users globally in 2025, while Instagram has reached 2 billion monthly active users in 2025. In 2024, Meta generated annual revenue of $164.5 billion, with more than 80% of its monthly users engaging with its products on a daily basis.

To access detailed market analysis, Request Sample

Display at 22.4% includes mobile banner, rich media, interstitial, and native advertising across in-app and mobile web environments. Search at 19.6% is dominated by search ads on mobile. Video at 14.8% grows fastest at ~11.8% CAGR through YouTube Shorts and Instagram Reels. Websites at 8.2% covers mobile web display and native advertising. Others at 4.0% includes SMS/MMS advertising, push notifications, in-game advertising, and podcast mobile advertising.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Asia Pacific |

35.0% |

Strong mobile internet adoption, rapid growth in mobile advertising, and integration of mobile advertising with e-commerce and payments. |

|

North America |

28.6% |

High mobile internet usage, leading mobile advertisers, and significant growth in mobile commerce and mobile payments. |

|

Europe |

22.4% |

Strict privacy regulations are driving local mobile advertising, with key growth from large publishers and regional compliance requirements. |

|

Latin America |

8.5% |

Increased mobile internet penetration and mobile advertising growth, particularly in markets with strong social media engagement. |

|

Middle East & Africa |

5.5% |

Rising mobile internet usage and mobile advertising expansion, with a focus on social media and mobile commerce. |

Asia Pacific's 35.0% lead reflects the region's mobile-first digital economy, where smartphones are the primary, often only, internet access device for billions of consumers. China's domestic mobile advertising market is the world's largest single national mobile advertising market. India's emerging market scale positions India as the decade's most significant mobile advertising growth market.

North America's 28.6% generates the world's highest average CPMs, reflecting premium US and Canadian consumer purchasing power and the world's most competitive auction dynamics among active US mobile advertisers. Europe's 22.4% is characterized by stringent GDPR privacy compliance that has created first-party data advantages for large publishers while disadvantaging the open programmatic ecosystem.

Competitive Landscape

The mobile advertising market is highly concentrated at the platform revenue level. Meta and Amazon together capture approximately 50%+ of global mobile advertising revenues, with ByteDance (TikTok) rapidly approaching 10% global share. This duopoly-to-triopoly structure at the top contrasts with the long tail of thousands of mobile ad networks, DSPs, SSPs, and measurement platforms competing for the remaining 40% of market revenues in the open programmatic ecosystem.

|

Company Name |

Platform |

Market Position |

Core Strength |

|

Meta |

Facebook Ads, Instagram Ads |

Market Leader |

Billions of people use Meta apps to connect with people and explore topics they care about. The Meta ads can show up as customers explore their Facebook Feed, watch Instagram Reels or check their Messenger inbox. |

|

ByteDance |

TikTok Ads |

Strong Challenger |

People can explore and engage with a range of products and services, including TikTok, CapCut, TikTok Shop, Lark, Pico, and Mobile Legends |

|

Amazon.com, Inc. |

Amazon Ads |

Strong Challenger |

By using Amazon Ads solutions like Sponsored Brands, the business has the opportunity to connect with audiences by delivering a quality mobile advertising experience. |

|

Apple Inc. |

Apple Ads |

Established Player |

Apple Ads purposefully integrates advertising into Apple experiences. Over 850 million people visit the App Store every week. |

The competitive landscape is bifurcated between walled garden platforms that own first-party user data, operate closed auction ecosystems, and control both buy-side and sell-side with opaque measurement, and the open programmatic ecosystem operating on shared infrastructure with transparent auction mechanics but fragmenting identity graphs post-ATT and cookie deprecation.

Key Company Profiles

Meta

Meta is the world's largest mobile advertising company by mobile-attributed revenue. Meta's competitive moat is structural with daily active people across Facebook, Instagram, WhatsApp, and Messenger creating an advertising inventory scale and audience targeting precision that no competitor can replicate.

- Platforms: Facebook Ads, Instagram Ads.

- Recent Developments: Meta generated US$56.3 billion in revenue for the 2026 March quarter, marking a 33% increase compared to the previous year, as the social media leader leveraged AI to enhance its advertising business.

- Strategic Focus: WhatsApp monetization scaling through business messaging and Click-to-WhatsApp advertising in emerging markets.

ByteDance

ByteDance is the world's fastest-growing digital advertising company, with a TikTok advertising platform at a comparable revenue scale.

- Platforms: TikTok Ads

- Recent Developments: In April 2026, TikTok broadened its collaborations with Integral Ad Science and Zefr to extend campaign measurement and safety tools to marketers across more ad formats on the platform.

- Strategic Focus: TikTok Shop social commerce integration monetizing purchase intent within video content.

Market Concentration Analysis

The mobile advertising market exhibits extreme concentration at the platform level. Meta and Amazon together generate approximately 50-55% of total global mobile advertising revenues from their walled garden ecosystems, an extraordinary duopoly for a USD 254.4 Billion market. Adding ByteDance (TikTok, ~9%) and Apple (~2%), the top 4 platforms capture approximately 70-75% of total global mobile advertising revenues. This concentration significantly exceeds other major media industries, even broadcast television's most concentrated markets, which feature less concentrated advertiser spend among top networks.

The open programmatic ecosystem competes for the remaining 25-30% of global mobile advertising revenue on open internet publishers. This ecosystem faces increasing structural pressures: privacy regulations fragmenting targeting identity, walled garden platforms improving relative ROAS through AI optimization, and supply chain transparency concerns limiting premium brand advertiser investment in open programmatic channels. Despite these headwinds, the open internet's total addressable advertising market is growing as total mobile advertising grows, sustaining absolute revenue growth for leading independent ad tech companies.

Investment & Growth Opportunities

Fastest Growing Segments

Video advertising (~11.8% CAGR), social media advertising (~10.5% CAGR), AI-generated creative automation (~25%+ CAGR in platform adoption), mobile commerce advertising (~15%+ CAGR), and AR/immersive mobile advertising (~20%+ CAGR from a small base) represent the global mobile advertising market's highest-growth investment vectors through 2034. Video's ~11.8% CAGR reflects the fundamental shift of video entertainment consumption from television to smartphone and the corresponding migration of brand advertising budgets from TV to mobile video.

Emerging Market Opportunities

India represents the single largest mobile advertising growth opportunity through 2034, with active mobile internet users growth, GDP per capita doubling, and e-commerce penetration expanding from 5% to 15%+ of retail, creating the demand base in annual Indian mobile advertising by 2034.

Investment Themes

- Privacy-preserving identity infrastructure: Companies providing privacy-compliant identity graphs, clean room analytics, and modeled conversion measurement will capture high annual platform revenues by 2030 as the industry completes its identity transition.

- AI creative automation for SME mobile advertisers: Generative AI democratizing high-quality mobile video ad creation for SME advertisers, currently limited to static image ads by cost and production capability, represents an annual addressable market expansion. Platforms and SaaS tools enabling SMEs to create TikTok-quality video ad content from product URLs and text prompts will capture the long tail of mobile advertising budget currently underinvested due to creative production limitations.

Future Market Outlook (2026-2034)

The global mobile advertising market is projected to grow from USD 254.4 Billion in 2025 to USD 581.6 Billion by 2034, delivering a 9.33% CAGR over the forecast period. The market's anchor value of USD 397.5 Billion in 2030 represents a mobile advertising landscape where AI-automated campaign management has become universal and social commerce has made mobile advertising the primary customer acquisition channel for both direct-to-consumer brands and brick-and-mortar retailers digitizing their customer relationships.

Three structural forces define the mobile advertising market's growth trajectory with exceptional certainty through 2034: the continued migration of global media consumption time toward mobile devices creating a perpetually expanding attention inventory that advertisers must purchase to reach any demographic below 50 years of age; the maturation of mobile social commerce as a primary retail channel, where every commercial transaction originates with mobile advertising exposure; and the democratization of AI-powered advertising optimization.

Research Methodology

Primary Research

Primary research comprised structured interviews with 75+ industry stakeholders (2025), including digital marketing VPs from Fortune 500 consumer goods brands (FMCG, retail, travel, financial services); global media agency mobile strategy leads; mobile advertising platform product managers from Meta, TikTok, and Amazon Advertising; mobile measurement specialists; independent mobile ad tech executives; and app developer monetization leads from major mobile gaming studios.

Secondary Research

Secondary research encompassed GSMA Mobile Economy Report 2025, App Annie/data.ai State of Mobile 2025 Report, eMarketer/Insider Intelligence Worldwide Digital Advertising 2025, IAB Internet Advertising Revenue Report 2024, IDC Digital Advertising Technologies 2025, company investor presentations and earnings calls, EU DMA enforcement proceedings documentation, GDPR enforcement tracker (IAPP), and Apple ATT impact studies. Over 130 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using top-down digital advertising share models calibrated against GSMA mobile penetration projections, eMarketer digital advertising baseline, and platform-specific revenue trajectory models for Meta, TikTok, Amazon, and the open programmatic ecosystem. Key inputs include global smartphone penetration forecasts by region (GSMA 2025-2034), mobile commerce GMV projections, TikTok growth trajectory modeling, privacy regulation impact coefficients on targeting efficiency, AI advertising automation adoption curves, and emerging market digital advertising GDP correlation models for India, Southeast Asia, Africa, and Latin America growth scenarios.

Mobile Advertising Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Search, Display, Video, Social Media, Websites, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Meta, ByteDance, Amazon.com Inc., Apple Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the mobile advertising market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global mobile advertising market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the mobile advertising industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mobile Advertising Market Report

The global mobile advertising market reached USD 254.4 Billion in 2025, driven by global smartphone users, Meta and Amazon commanding 50%+ market share, TikTok reaching high in advertising revenues, and mobile representing most of all global digital advertising spend.

The market grows at 9.33% CAGR during 2026-2034, reaching USD 581.6 Billion by 2034, driven by short-form video social commerce, AI-powered campaign automation, privacy-preserving identity infrastructure maturation, and Asia Pacific mobile internet user growth.

Social media leads at 31.0% through Meta's family of apps (Facebook, Instagram, WhatsApp), generating high advertising revenues.

Asia Pacific leads at 35.0%, anchored by China's domestic mobile advertising market, India's active mobile internet users’ growth, and Southeast Asia's super-app ecosystem generating premium intent-data advertising.

Leading companies include Meta, ByteDance, Amazon.com Inc., and Apple Inc., among others.

The market reaches approximately USD 397.5 Billion by 2030, with AI-automated campaigns managing the majority of global budgets, social commerce processing, India emerging as the world's third-largest national mobile advertising market, and privacy-preserving identity infrastructure completing its deployment.

TikTok's growth in advertising revenues is the fastest revenue scale-up in digital advertising history. TikTok’s user engagement demonstrates social commerce integration that is compelling brand advertisers to reallocate TV toward TikTok's mobile video ecosystem.

China's domestic mobile ad revenues, India's growing mobile user base, Southeast Asia's super-app ecosystem with rich first-party commerce data, South Korea's mobile gaming advertising, and Japan's LINE platform collectively generate the region's 35.0% global mobile advertising share.

Mobile programmatic is transitioning from device ID to UID2, contextual targeting, probabilistic modeling, and first-party data clean rooms, enabling privacy-safe audience activation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade