Multiple Myeloma Drugs Market Size, Share, Trends and Forecast by Therapy, Drug Type, End User, Distribution Channel, and Region, 2026-2034

Multiple Myeloma Drugs Market Size and Share:

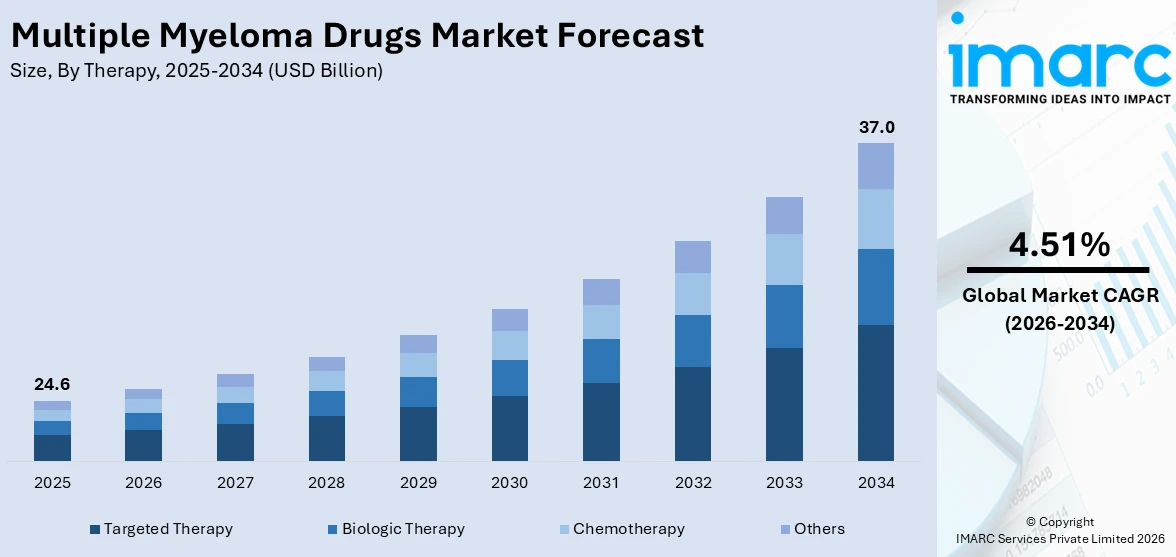

The global multiple myeloma drugs market size was valued at USD 24.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 37.0 Billion by 2034, exhibiting a CAGR of 4.51% during 2026-2034. North America currently dominates the market, holding a significant market share of over 40.7% in 2025. This dominance is driven by advanced healthcare infrastructure, high adoption of innovative therapies, and substantial investment in oncology research. The presence of key pharmaceutical companies and favorable reimbursement policies further fuel multiple myeloma drugs market share in the region.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 24.6 Billion |

|

Market Forecast in 2034

|

USD 37.0 Billion |

| Market Growth Rate 2026-2034 | 4.51% |

The market is propelled by an upsurge in precision medicine approaches and biomarker-driven treatment strategies. Increasing investments by pharmaceutical companies in novel drug discovery, including bispecific antibodies and next-generation proteasome inhibitors, are expanding therapeutic options. Enhanced clinical trial designs and adaptive regulatory pathways in global regions are accelerating time-to-market for innovative drugs. Moreover, improvements in diagnostic imaging and genomics have refined disease classification, enabling more personalized treatment regimens. The growing incorporation of digital health technologies to monitor patient response and improve adherence also plays a significant role. Strategic collaborations among biotech firms and research institutions further support ongoing therapeutic advancements.

To get more information on this market Request Sample

In the United States, the multiple myeloma drugs market growth is driven by robust federal funding for oncology research and the presence of an advanced healthcare infrastructure. The high adoption rate of breakthrough therapies, including CAR-T cell therapies and antibody-drug conjugates, is accelerating market penetration. The presence of major pharmaceutical players with strong commercialization capabilities supports rapid drug deployment. Additionally, favorable reimbursement frameworks through Medicare and private insurers improve access to costly treatments. An aging population and increasing life expectancy also contribute to rising disease incidence. For instance, in May 2025, a four-drug combination (DKRd) including daratumumab showed improved outcomes for newly diagnosed multiple myeloma patients in the ADVANCE trial. Compared to the standard KRd regimen, DKRd achieved higher MRD-negativity (59% vs. 36%) and better progression-free survival at nearly 33 months (86% vs. 79%), without significantly increased toxicity. These findings support DKRd as a potential new standard of care, enabling some patients to defer stem cell transplants and highlighting the importance of MRD-negativity in guiding treatment decisions.

Multiple Myeloma Drugs Market Trends:

Rising Burden of Hematological Cancers Boosting Drug Demand

The increasing incidence of hematologic malignancies globally is significantly influencing the multiple myeloma drug market. In 2022, these cancers accounted for 6.6% of all diagnosed cancer cases and 7.2% of related deaths, underscoring the critical need for targeted therapies. As multiple myeloma stems largely from genetic abnormalities, its treatment requires a multidisciplinary approach involving immunomodulatory drugs, chemotherapy, radiation, and stem cell transplants. Platelet transfusions also play a role in managing side effects. With early detection improving, more patients are eligible for advanced treatments. Healthcare systems worldwide are under pressure to offer effective therapeutics, which is accelerating innovation and boosting investments in myeloma-specific drugs, thus contributing to the positive multiple myeloma drugs market outlook.

Technological Advancements Accelerating Treatment Innovations

Technological progress is transforming multiple myeloma treatment, particularly through innovations like microRNA-based therapies and nanomedicines. These platforms enable precision targeting of malignant cells while minimizing damage to healthy tissues. A prime example is Ardena’s nanomedicine facility in Oss, Netherlands, which secured GMP certification in November 2024 after a €20 million investment. This facility supports complex manufacturing of lipid and polymeric nanoparticles, delivery vehicles critical for transporting macromolecular agents to the bone marrow and triggering antitumor responses. Such innovations not only enhance treatment outcomes but also lower long-term healthcare costs by reducing complications. As pharmaceutical companies expand their nanotech capabilities, these developments are expected to play a vital role in driving the multiple myeloma drug market growth.

Increasing Biologic Therapy Adoption and Healthcare Spending

Growing awareness about biologic therapies is reshaping treatment preferences in the multiple myeloma landscape. These drugs leverage the immune system to recognize and eliminate cancer cells, offering a less invasive and often more effective alternative to conventional treatments. Patients are increasingly drawn to therapies that provide targeted mechanisms with fewer systemic side effects. Alongside this trend, rising global healthcare expenditures, reported at USD 9.8 Trillion in 2021, equating to 10.3% of global GDP, are enabling wider access to these advanced treatments. Combined with the pharmaceutical industry's expanding research budgets, biologic therapies are gaining traction across developed and emerging markets. This shift is expected to significantly contribute to the expansion of the multiple myeloma drug market in the coming years.

Multiple Myeloma Drugs Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global multiple myeloma drugs market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on therapy, drug type, end user, and distribution channel.

Analysis by Therapy:

- Targeted Therapy

- Biologic Therapy

- Chemotherapy

- Others

Targeted therapy plays a pivotal role in the multiple myeloma drug market by offering a precision-based approach that directly interferes with specific molecules responsible for cancer cell growth and survival. These therapies, such as proteasome inhibitors and histone deacetylase inhibitors, provide enhanced efficacy with fewer side effects compared to traditional treatments. The increasing understanding of the genetic and molecular mechanisms of multiple myeloma has led to the development of more selective drugs. Ongoing clinical trials and regulatory approvals are further accelerating adoption. Moreover, the ability of targeted therapy to be used in combination regimens is expanding its clinical utility, driving consistent growth in this segment globally.

Biologic therapy has gained significant prominence in the multiple myeloma drug market, largely due to its ability to harness the body’s immune system to combat cancer. Monoclonal antibodies, such as daratumumab and elotuzumab, have shown strong clinical success by targeting specific proteins on myeloma cells. The increasing acceptance of immunotherapy approaches and the growing demand for personalized medicine are key growth drivers for this segment. With rising awareness among healthcare providers and patients regarding the benefits of biologics, coupled with supportive reimbursement frameworks and expanding biologics pipelines, the segment is expected to experience sustained growth in both developed and emerging markets.

Chemotherapy continues to serve as a foundational component in the treatment of multiple myeloma, particularly in combination with other therapeutic classes. Although its prominence has somewhat declined with the emergence of targeted and biologic therapies, chemotherapy remains essential, especially in newly diagnosed or relapsed patients requiring rapid cytoreduction. The wide availability, proven efficacy, and cost-effectiveness of chemotherapeutic agents ensure their continued use. Advancements in formulation, including oral chemotherapies and supportive care options to manage side effects, have also contributed to maintaining its relevance. As part of combination regimens, chemotherapy enhances overall treatment outcomes, securing its ongoing role in the evolving multiple myeloma drug market.

Analysis by Drug Type:

- Immunomodulatory Drugs

- Proteasome Inhibitors

- Histone Deacetylase Inhibitors

- Monoclonal Antibody Drugs

- Steroids

- Others

Immunomodulatory drugs stand as the largest drug type in 2025, holding around 38.7% of the market. The immunomodulatory drugs segment dominates the multiple myeloma drug market due to its proven effectiveness in enhancing immune responses and directly targeting cancer cells. These drugs, such as lenalidomide and pomalidomide, have become foundational therapies for both newly diagnosed and relapsed patients, often used in combination with other treatments like corticosteroids and proteasome inhibitors. Their ability to modulate the tumor microenvironment, suppress abnormal plasma cells, and improve patient outcomes has led to widespread adoption. Additionally, ongoing clinical trials and regulatory approvals continue to expand their indications, reinforcing their central role in treatment protocols and sustaining their dominance in the multiple myeloma drug market.

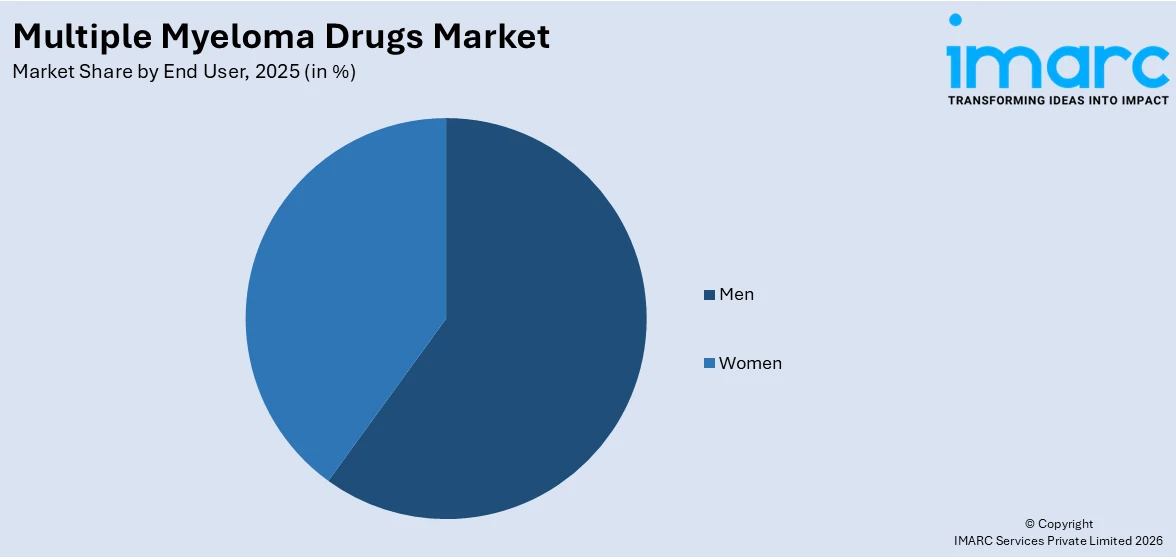

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Men

- Women

Men represent a significant segment in the multiple myeloma drug market, accounting for a higher prevalence rate compared to women. Epidemiological data indicate that men are more frequently diagnosed with multiple myeloma, which naturally drives greater demand for therapeutic interventions among this demographic. The higher incidence may be attributed to genetic, hormonal, and lifestyle factors, including greater exposure to environmental risk elements such as industrial chemicals and tobacco use. As a result, pharmaceutical companies and healthcare providers often prioritize this patient group in clinical trials and treatment planning. Increased health awareness, along with access to advanced diagnostics and treatment options, further supports the growth of this segment within the market.

Women constitute an essential and growing segment in the multiple myeloma drug market, supported by rising awareness and improving access to healthcare. Though the prevalence of multiple myeloma is relatively lower among women compared to men, the market demand from this group is expanding due to early diagnosis and increasing participation in screening programs. Advances in gender-specific research and the growing focus on tailoring therapies to address women’s physiological responses contribute to better treatment outcomes. Additionally, supportive care services and educational initiatives have improved adherence to treatment regimens among female patients, fueling continued market growth in this segment.

Analysis by Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Hospital pharmacies lead the market with around 57.0% of market share in 2025. The hospital pharmacies segment dominates the multiple myeloma drug market due to the complex nature of treatment regimens and the need for specialized administration and monitoring. Multiple myeloma therapies often involve intravenous drugs, combination treatments, and biologics that require hospital-grade infrastructure and professional supervision. Hospitals serve as primary points for cancer diagnosis, staging, and early treatment, making them central to drug dispensing and patient management. Furthermore, hospital pharmacies maintain a broader inventory of high-cost and high-risk oncology drugs, ensuring immediate access for patients undergoing intensive therapies. This central role in comprehensive cancer care reinforces their dominance in the multiple myeloma drug market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 40.7%. North America dominates the multiple myeloma drug market due to its advanced healthcare infrastructure, high healthcare spending, and robust presence of leading pharmaceutical companies engaged in oncology research. The region benefits from early adoption of innovative therapies, strong regulatory support from agencies like the FDA, and widespread access to cutting-edge treatments. A high prevalence of multiple myeloma, combined with increased awareness and early diagnosis, contributes to the growing demand for targeted and biologic therapies. Additionally, favorable reimbursement policies and significant investment in clinical trials further strengthen North America’s leadership in this space, ensuring its continued prominence in the multiple myeloma drug market. For instance, in June 2024, AbbVie begun its Phase III CERVINO trial for ABBV-383, a bispecific T-cell engager targeting BCMA and CD3, in patients with relapsed/refractory multiple myeloma. The global, randomized trial will enroll 380 patients who have had at least two prior therapies but not BCMA-targeted ones. Participants will receive ABBV-383 or standard available therapies. The primary endpoints are progression-free survival and overall response rate, with secondary measures including survival and disease symptom changes. ABBV-383 is dosed monthly to simplify treatment.

Key Regional Takeaways:

United States Multiple Myeloma Drugs Market Analysis

In 2025, the United States held a market share of over 86.8% in North America. The United States multiple myeloma drug market is primarily driven by the rising incidence of the disease, supported by improved diagnostic techniques that enable earlier detection and intervention. In 2025, the American Cancer Society projected approximately 36,110 new cases of multiple myeloma in the U.S. (20,030 in men, 16,080 in women) and about 12,030 related deaths (6,540 in men, 5,490 in women). In accordance with this, robust advancements in immunotherapy and precision medicine are fostering the development of novel drug classes and combination regimens, thereby impelling the market. The growing presence of a robust clinical trial pipeline, pushed by industry-academic collaborations, is further propelling market growth. Similarly, the growing awareness among healthcare providers and patients regarding early treatment options is enhancing adoption rates. Additionally, the market is benefiting from strategic mergers, acquisitions, and partnerships that strengthen research capabilities and expand portfolios. Apart from this, continued investments in biomarker-driven research and personalized medicine are driving targeted drug development and market expansion.

Europe Multiple Myeloma Drugs Market Analysis

The multiple myeloma drug market in Europe is experiencing growth due to the region’s aging population, which elevates the prevalence of hematologic cancers requiring advanced treatments. It has been reported that Europe’s median age is projected to rise by 5.5 years, from 44.7 in 2024 to 50.2 in 2100, with the share of people aged 80 and above expected to grow from 6.1% to 15.3%. In line with this, continued improvements in healthcare infrastructure across Europe are enhancing market accessibility. Similarly, the expansion of national cancer control programs, which promote earlier detection and the establishment of structured care pathways, is fostering market expansion. The increase in government funding dedicated to research on rare and complex diseases is driving pharmaceutical innovation. Additionally, the increasing acceptance of biosimilars is reducing treatment costs and expanding patient access to these therapies. Furthermore, the growing integration of digital health tools and electronic medical records, which improves personalized treatment planning and monitoring, is stimulating market appeal. Besides this, cross-border healthcare collaboration within the EU is strengthening knowledge exchange and accelerating the adoption of advanced multiple myeloma therapies across member states.

Asia Pacific Multiple Myeloma Drugs Market Analysis

The Asia Pacific market is largely driven by rising healthcare spending in emerging economies, which strengthens access to advanced oncology therapies. An industry report projected that India’s healthcare spending will increase from 3.3% to 5% of GDP by 2030. Furthermore, rapid urbanization and changing lifestyles are increasing cancer prevalence, thereby strengthening market demand. The strong government initiatives to raise awareness of rare diseases and improve patient registries, which support early diagnosis and timely care, are bolstering market development. Additionally, strategic collaborations between regional biotech companies and global pharmaceutical firms are accelerating the transfer of technology and innovative drug development. The expansion of specialized cancer treatment centers and the growth of medical tourism infrastructure are attracting patients seeking advanced therapies. As such, India’s medical tourism sector is expected to grow at a double-digit rate of 14–15% following the recent relaxation of visa rules outlined in the Union Budget 2025–26. Moreover, broader reimbursement coverage and regulatory reforms across key Asia-Pacific countries are facilitating the faster approval and availability of cutting-edge multiple myeloma treatments, thereby providing an impetus to the market.

Latin America Multiple Myeloma Drugs Market Analysis

In Latin America, the multiple myeloma drug market is growing due to the steady improvement of healthcare systems and greater public funding for oncology services across the region. Accordingly, by March 2025, Brazil’s radiotherapy expansion plan, with Varian, added 92 linacs and nine HDR afterloaders, reducing wait times and enabling advanced treatments. The initiative now treats an estimated 55,000 cancer patients annually, expanding access nationwide. In addition to this, rising awareness initiatives and patient advocacy programs are encouraging earlier diagnosis and improved treatment uptake. The increasing presence of multinational pharmaceutical companies, through the formation of strategic partnerships and expansion of distribution channels, is bolstering market development. Furthermore, wider participation in international clinical trials is fostering scientific exchange and supporting faster access to advanced multiple myeloma therapies, thereby creating lucrative market opportunities.

Middle East and Africa Multiple Myeloma Drugs Market Analysis

The market in the Middle East and Africa is significantly influenced by rising healthcare expenditure and strong government initiatives to modernize oncology care. Industry analysis indicates that the UAE’s healthcare spending ranks among the highest per capita globally, at approximately USD 1,200. The sector generates over USD 4.63 Billion in annual revenue and comprises 75 insurers, which provide more than 12,000 policies. Similarly, the continual development of regional cancer centers is expanding access to specialized diagnostics and advanced treatment options for multiple myeloma. Furthermore, increasing collaborations between local healthcare systems and global pharmaceutical companies are enhancing the market reach. Similarly, the growth of public-private partnerships and focused investments in training medical professionals is strengthening the oncology workforce, ensuring that patients receive high-quality, up-to-date care and improving overall treatment outcomes.

Competitive Landscape:

The competitive landscape of the multiple myeloma drug market is characterized by intense R&D activity, strategic collaborations, and continuous drug innovation. Leading players are focusing on expanding their product pipelines through the development of advanced biologics, immunotherapies, and targeted treatments. For instance, in June 2025, Glenmark’s subsidiary, Ichnos Glenmark Innovation (IGI), reported promising early trial results for its cancer drug ISB 2001, targeting relapsed/refractory multiple myeloma. The novel trispecific antibody therapy showed a 79% overall response rate (ORR) among heavily pretreated patients, with 30% achieving complete or near-complete response. Six of eight patients tested negative for minimal residual disease. The trial, presented at ASCO 2025, showed manageable side effects and is moving into dose expansion to determine optimal dosing for broader testing. Regulatory approvals and fast-track designations are accelerating the launch of novel therapeutics, while mergers and licensing agreements are enhancing global reach and capabilities. Companies are increasingly investing in technologies such as CAR-T cell therapies and nanomedicine-based delivery systems to gain a competitive edge. With rising competition and robust clinical pipelines, the multiple myeloma drugs market forecast projects sustained innovation and market expansion through 2033, driven by unmet medical needs and a growing patient population worldwide.

The report provides a comprehensive analysis of the competitive landscape in the multiple myeloma drug market with detailed profiles of all major companies, including:

- Amgen Inc.

- Bristol Myers Squibb

- Daiichi Sankyo Co., Ltd.

- Sanofi-Aventis Groupe (Genzyme Corporation)

- Johnson & Johnson Services, Inc.

- Merck & Co., Inc.

- Novartis International AG

- Pfizer Inc.

- PHARMA MAR, S.A.

- Takeda Pharmaceutical Company Limited

- Teva Pharmaceutical Industries Ltd.

Latest News and Developments:

- June 2025: The EMA’s CHMP gave a positive opinion for DARZALEX (daratumumab) SC as monotherapy for adults with high-risk smouldering multiple myeloma, supported by Phase 3 AQUILA results showing it may delay progression and extend survival, marking a first treatment option for this group.

- April 2025: Amneal and Shilpa launched BORUZU, the first ready-to-use subcutaneous or IV bortezomib in the U.S., streamlining preparation for multiple myeloma and mantle cell lymphoma treatment. This marks Amneal’s fourth 505(b)(2) injectable launch in a year, aiming to boost pharmacy efficiency and patient access.

- March 2025: Bristol Myers Squibb bought 2seventy bio for USD 286 Million, gaining full ownership of the multiple myeloma cell therapy Abecma. The deal secures operational control amid competition from Carvykti and upcoming rival anito-cel, as 2seventy had already divested its other cell therapy programs.

- January 2025: The FDA approved daratumumab (Darzalex Faspro) and isatuximab (Sarclisa) with VRd for newly diagnosed multiple myeloma patients, expanding first-line options. Daratumumab was approved for transplant-eligible patients; isatuximab for those ineligibles. Both improved progression-free survival and MRD negativity, offering longer remissions and better outcomes.

- January 2025: China’s NMPA approved Sarclisa with pomalidomide and dexamethasone for adults with relapsed or refractory multiple myeloma. The approval, based on ICARIA-MM and IsaFiRsT studies, showed improved survival and response rates. Sarclisa is now included in top Chinese treatment guidelines for this patient group.

- November 2024: Roche agreed to buy Poseida Therapeutics for up to USD 1.5 Billion, expanding its cell therapy pipeline. Poseida’s lead asset, P-BCMA-ALLO1, targets relapsed/refractory multiple myeloma with FDA designations. The deal strengthens Roche’s position in off-the-shelf CAR-T therapies for multiple myeloma and other diseases.

Multiple Myeloma Drugs Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Therapies Covered | Targeted Therapy, Biologic Therapy, Chemotherapy, Others |

| Drug Types Covered | Immunomodulatory Drugs, Proteasome Inhibitors, Histone Deacetylase Inhibitors, Monoclonal Antibody Drugs, Steroids, Others |

| End-Users Covered | Men, Women |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amgen Inc., Bristol Myers Squibb, Daiichi Sankyo Co., Ltd., Sanofi-Aventis Groupe (Genzyme Corporation), Johnson & Johnson Services, Inc., Merck & Co., Inc., Novartis International AG, Pfizer Inc., PHARMA MAR, S.A., Takeda Pharmaceutical Company Limited., and Teva Pharmaceutical Industries Ltd. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the multiple myeloma drug market from 2020-2034.

- The multiple myeloma drug market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the multiple myeloma drug industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Multiple Myeloma Drugs Market Report

The multiple myeloma drug market was valued at USD 24.6 Billion in 2025.

The multiple myeloma drug market is projected to exhibit a CAGR of 4.51% during 2026-2034, reaching a value of USD 37.0 Billion by 2034.

Key factors driving the multiple myeloma drug market include rising incidence rates, expanding elderly population, and increased awareness leading to early diagnosis. Advances in targeted therapies and immunotherapies (like CAR-T and monoclonal antibodies), alongside favorable regulatory approvals and strong R&D pipelines, further fuel market growth.

North America currently dominates the military laser systems market, accounting for a share of 40.7%. The dominance of the region is due to advanced defense infrastructure, substantial R&D investments, and the presence of major defense contractors. The region’s strategic focus on modernizing weapon systems and integrating laser technologies in combat operations further reinforces its leading position in the market.

Some of the major players in the multiple myeloma drug market include Amgen Inc., Bristol Myers Squibb, Daiichi Sankyo Co., Ltd., Sanofi-Aventis Groupe (Genzyme Corporation), Johnson & Johnson Services, Inc., Merck & Co., Inc., Novartis International AG, Pfizer Inc., PHARMA MAR, S.A., Takeda Pharmaceutical Company Limited., Teva Pharmaceutical Industries Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)