Natural Food Colors Market Size, Share, Trends and Forecast by Product, Form, Application, and Region 2026-2034

Global Natural Food Colors Market Size, Share, Trends & Forecast (2026-2034)

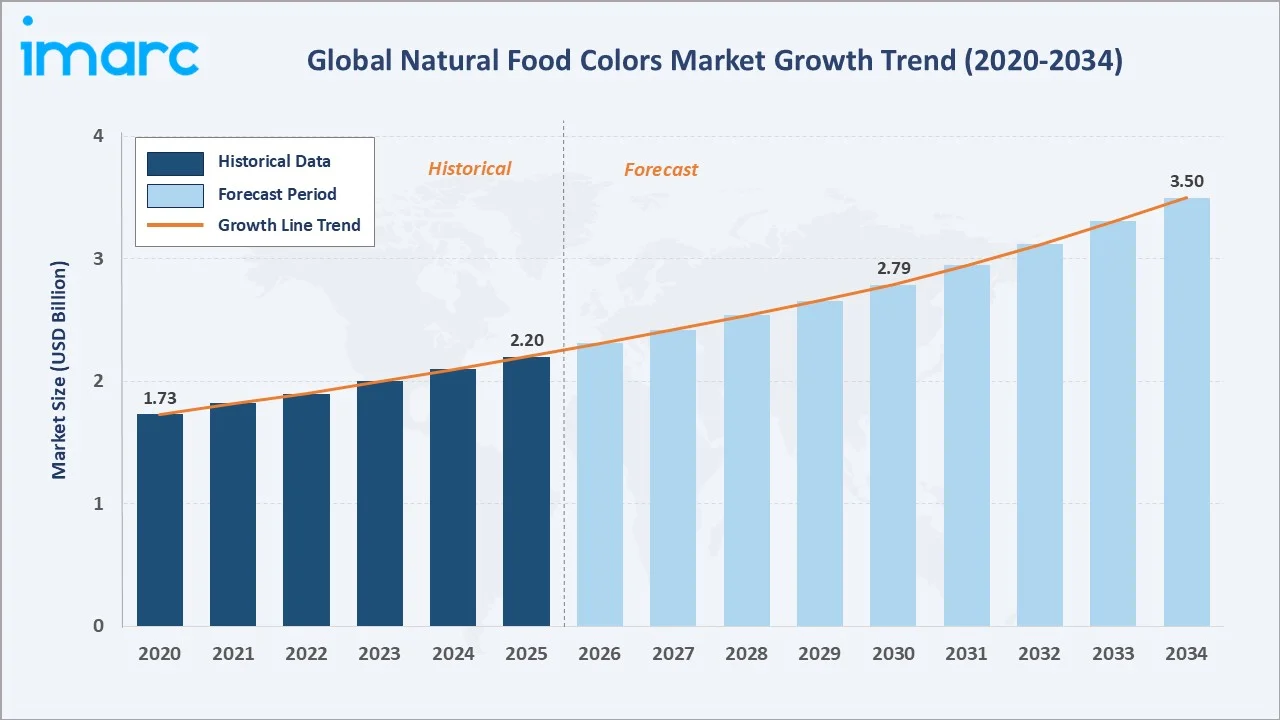

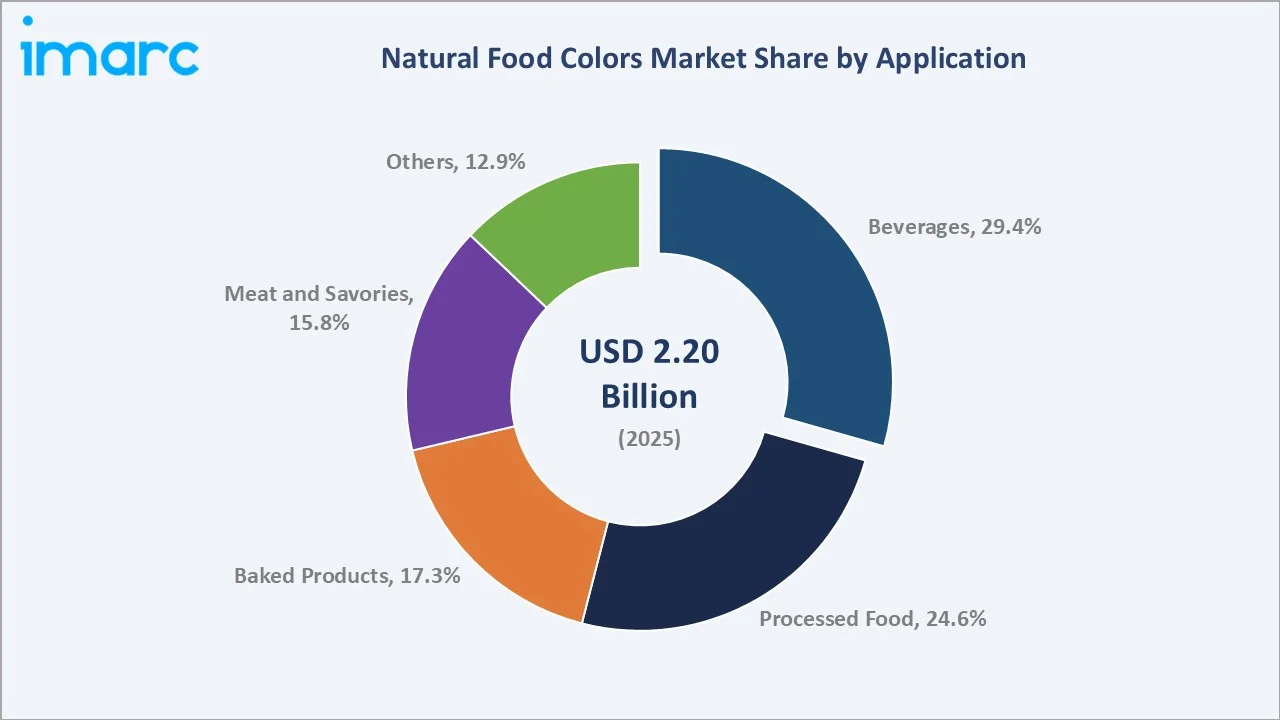

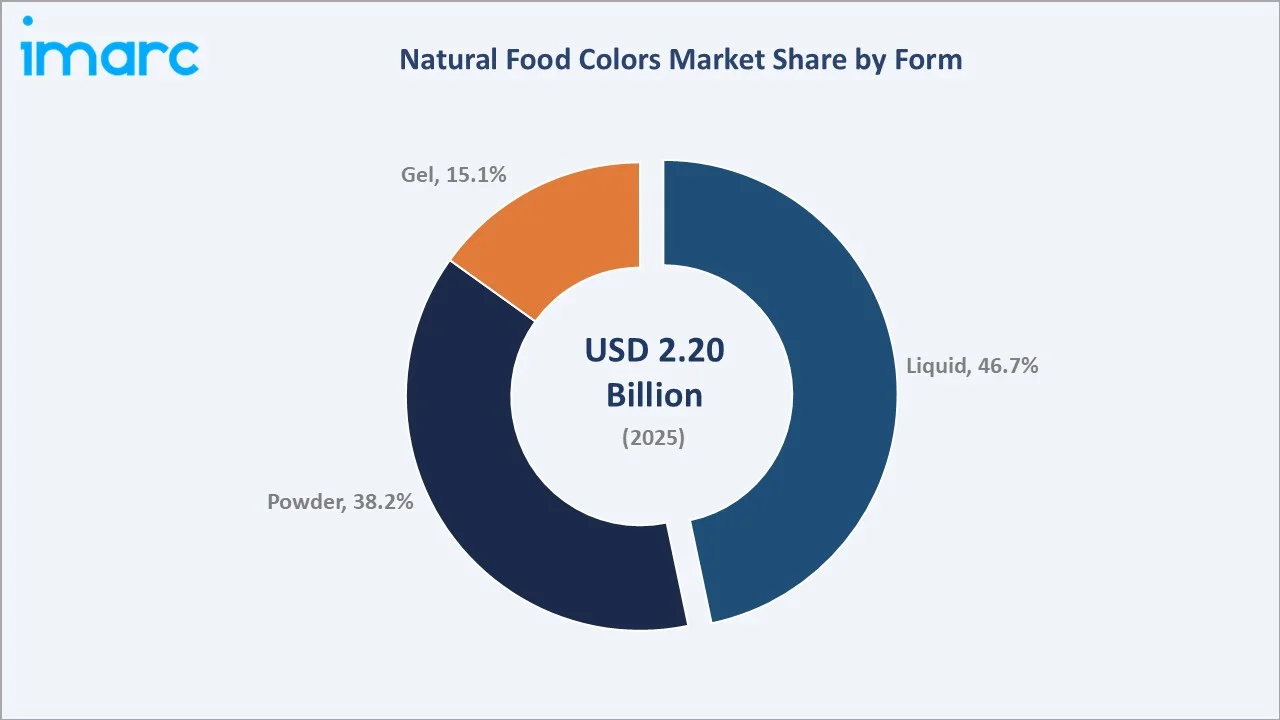

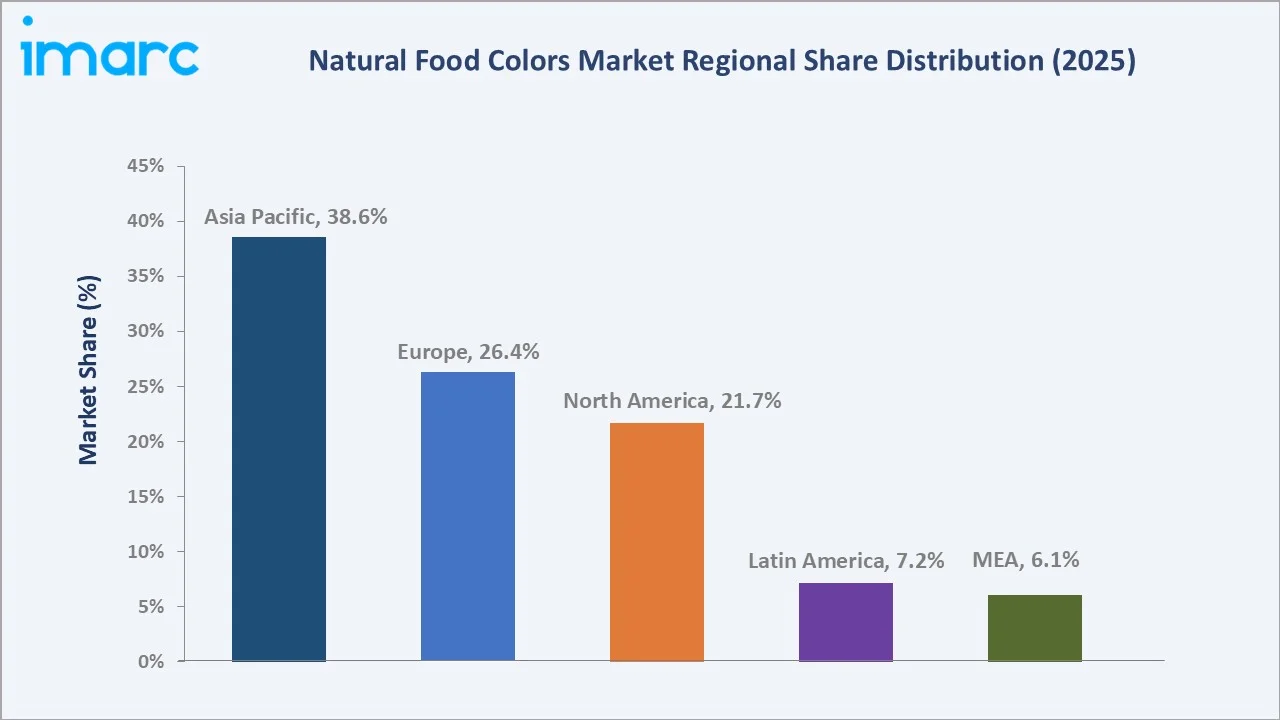

The global natural food colors market size was valued at USD 2.20 Billion in 2025 and is projected to reach USD 3.50 Billion by 2034, exhibiting a CAGR of 4.86% during the forecast period 2026-2034. Beverages lead application share at 29.4% in 2025, while Liquid dominates the form segment at 46.7%. Asia Pacific accounts for 38.6% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.20 Billion |

|

Forecast Market Size (2034) |

USD 3.50 Billion |

|

CAGR (2026-2034) |

4.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (38.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~5.6%) |

|

Leading Application |

Beverages (29.4%, 2025) |

|

Leading Form |

Liquid (46.7%, 2025) |

The global natural food colors market growth trajectory from 2020 through 2034 contrasts a steady historical expansion base against a sustained forecast curve powered by clean-label reformulation, regulatory restrictions on synthetic dyes, and rising plant-based food consumption.

To get more information on this market, Request Sample

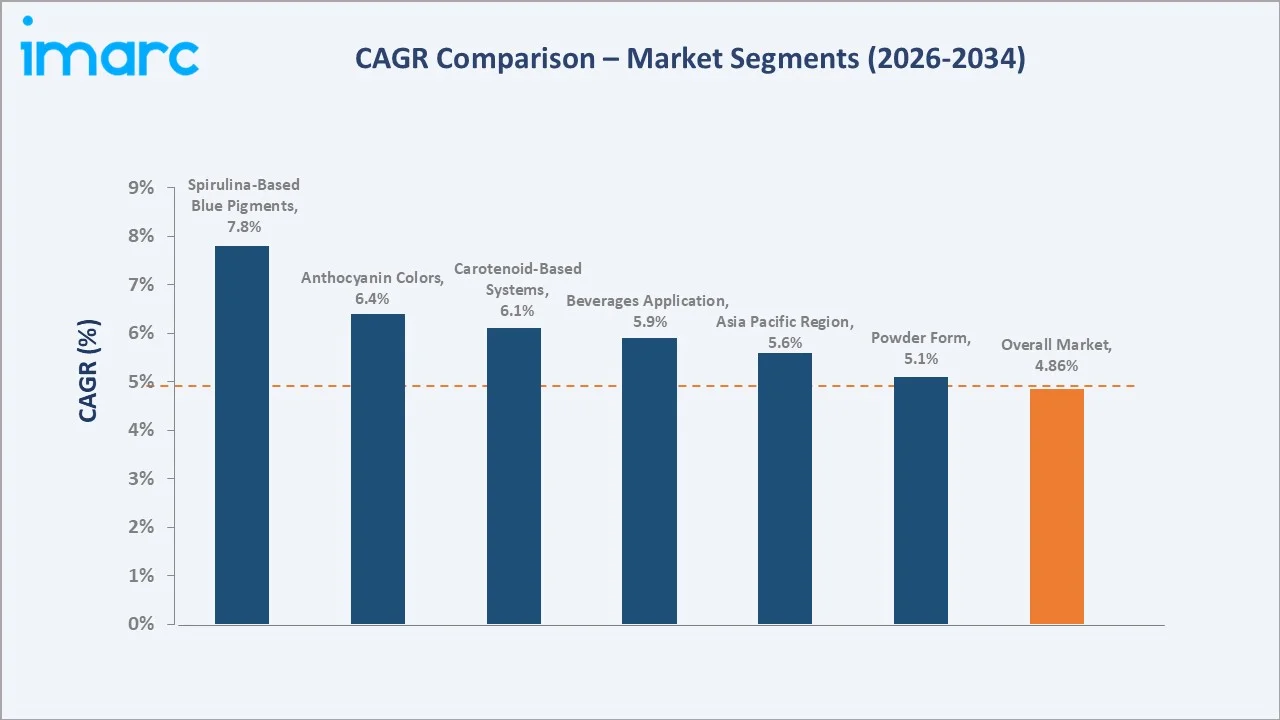

Segment-level CAGR comparison highlights spirulina-based blue pigments and anthocyanins as the two fastest-growing pigment sub-categories within the global natural food colors industry analysis through 2034.

Executive Summary

The global natural food colors market is undergoing a structural shift led by the convergence of health awareness, regulatory enforcement, and clean-label food innovation. Valued at USD 2.20 Billion in 2025, the market is forecast to reach USD 3.50 Billion by 2034 at a CAGR of 4.86%. The FDA's January 2025 revocation of Red Dye No. 3 authorisation for food and oral drugs, and the April 2025 HHS-FDA announcement of a phased industry withdrawal of petroleum-based FD&C synthetic dyes, have compressed the US reformulation timeline from a decade-long evolution to a two-to-three year transition cycle, with Kraft Heinz, General Mills, and Tyson Foods publicly committing to full natural-colour conversion by 2027-2028.

Beverages command the dominant application share at 29.4% in 2025, supported by the rapid growth of functional drinks, plant-based dairy, and reformulated carbonated beverages. Processed Food at 24.6% is the second-largest application. Liquid form dominates the form segment at 46.7% in 2025, driven by superior dispersion in beverage and dairy matrices and lower dosage requirements in high-throughput bottling operations, while Powder holds 38.2%, preferred in bakery and savoury dry-mix applications where shelf stability is critical.

Asia Pacific dominates with a 38.6% global revenue share in 2025, led by India's turmeric production base supplying approximately 75% of global curcumin volume, China's USD 1.2 trillion processed-food market, and rising ASEAN middle-class packaged food consumption. Europe holds 26.4% in 2025 and North America 21.7%, with Europe anchored by EFSA E-number labelling and mature clean-label retail, while North America is the fastest-repositioning region owing to 2025 federal action against synthetic dyes.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Beverages - 29.4% share (2025) |

|

Leading Form |

Liquid - 46.7% share (2025) |

|

Leading Region |

Asia Pacific - 38.6% revenue share (2025) |

|

Second Region |

Europe - 26.4% revenue share (2025) |

|

Top Companies |

ADM, Oterra A/S, Sensient Technologies Corporation, Givaudan, Döhler GmbH |

Key Analytical Observations Supporting the Above Data:

- Beverages' 29.4% dominance in 2025 reflects accelerated reformulation of soft drinks, plant-based milks, and functional beverages, where anthocyanin-based colourants have largely replaced synthetic reds across North American and European portfolios since 2024.

- Liquid form leads at 46.7% in 2025 due to superior dispersion stability in water-based matrices, lower dosage rates, and faster integration into high-throughput beverage bottling operations compared with powder and gel formats.

- Asia Pacific's 38.6% global dominance in 2025 reflects the region's dual role as the largest producer of raw botanical inputs such as turmeric, paprika, and annatto AND the fastest-growing consumer market for processed food and ready-to-drink beverages.

- Europe's 26.4% regional share in 2025 is underpinned by the EFSA E-number labelling framework that effectively mandates natural colour disclosure on packaged foods, combined with Germany, France, the UK, and Italy’s mature organic retail channels and consistent consumer willingness to pay a premium for clean-label formulations.

- The top five players: ADM, Oterra A/S, Sensient Technologies Corporation, Givaudan, and Döhler GmbH — collectively hold an estimated 45–50% global revenue share in 2025, with Givaudan’s acquisitions of Naturex (2018) and DDW (2021) accelerating consolidation around vertically integrated, bioscience-led natural colour platforms.

Global Natural Food Colors Market Overview

Natural food colors are pigments extracted from plants, microorganisms, minerals, or animal sources that impart colour to food and beverage formulations without petroleum-derived synthetic dyes. Core commercial pigments include curcumin (yellow), carotenoids (orange-red), anthocyanins (red-purple-blue), carmine (red), caramel (brown), copper chlorophyllin (green), and spirulina (blue-green).

Applications span the entire processed food and beverage value chain: beverages, confectionery, bakery, dairy, sauces, meat and savouries, pet food, and nutraceuticals. Natural colours hold regulatory approval across the major global food safety frameworks, including FDA, EFSA, FSSAI, and China GB standards, providing broad application access.

Macroeconomic enablers include 6-8% annual global processed-food category growth, over 70% of US grocery shoppers actively reading ingredient lists for synthetic additives, the 2025 US federal action against FD&C synthetic dyes, and expanding middle-class packaged food consumption across Asia Pacific and Latin America through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

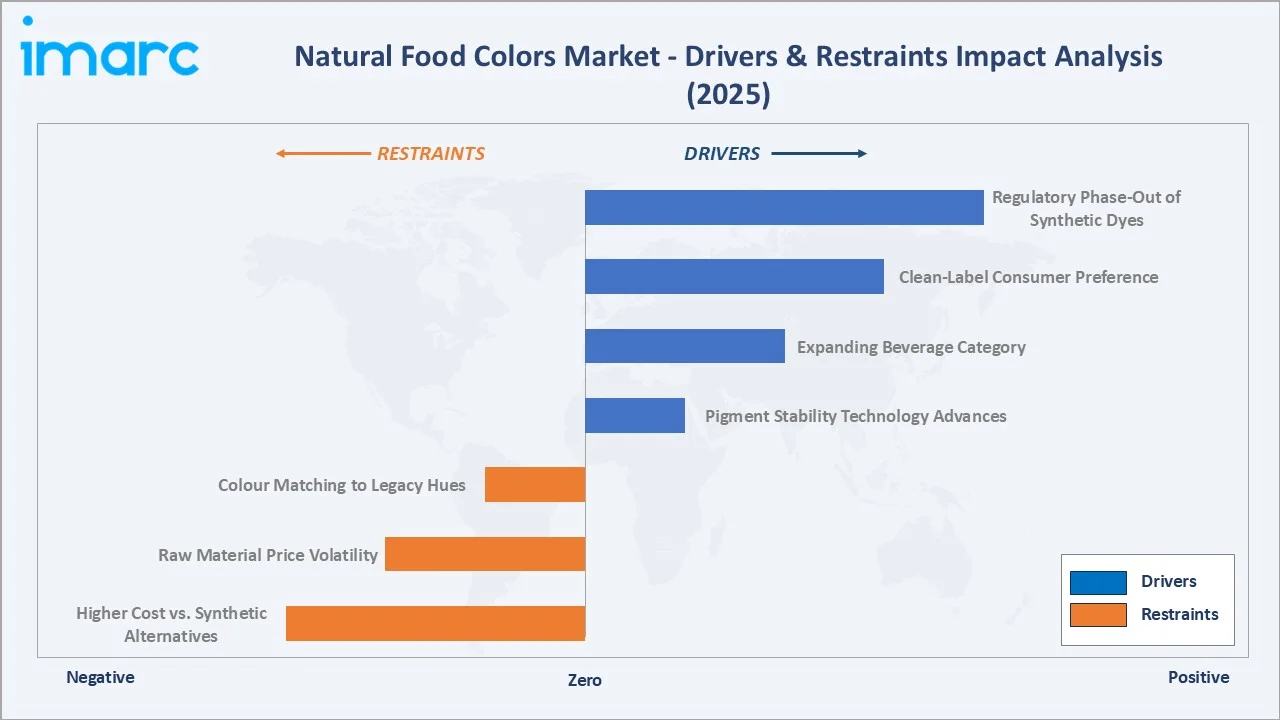

Market Drivers

- Regulatory Phase-Out of Synthetic Dyes: The FDA's January 2025 revocation of Red Dye No. 3 for food and oral drugs, followed by the April 2025 HHS-FDA announcement of a phased industry withdrawal of petroleum-based FD&C synthetic dyes, is the single largest structural catalyst for the natural food colors market. Kraft Heinz, General Mills, and Tyson Foods have publicly committed to full reformulation by the end of 2027.

- Clean-Label and Plant-Based Consumer Preference: Clean-label positioning is now a mainstream purchase criterion rather than a premium niche. Industry surveys in 2025 show over 70% of US grocery shoppers actively check ingredient lists for synthetic additives, and private-label retailers, including Whole Foods 365 and Trader Joe's, require natural colouring in their own-brand formulations.

- Expanding Beverage and Functional-Drink Category: The global functional beverage market is expanding, led by energy drinks, plant-based dairy, and protein-enhanced beverages. Each new functional SKU launched in 2024-2025 typically specifies a naturally-derived colour system, creating structural volume growth for beverage-grade natural colourants.

- Advances in Pigment Stability Technology: Microencapsulation and emulsion-based delivery systems have sharply improved the heat, pH, and light stability of natural pigments, narrowing the performance gap with synthetic dyes. New spirulina-derived blue extracts approved by the FDA in 2025 now provide stable blue hues in yogurt, ice cream, and beverages.

Market Restraints

- Higher Cost vs. Synthetic Alternatives: Natural colourants typically cost 3-10 times more per unit of colour strength than synthetic FD&C dyes. The cost gap remains a barrier in price-sensitive private-label and developing-market product lines, particularly in confectionery and snack categories with thin margins.

- Raw Material Price Volatility and Supply Concentration: Key inputs such as turmeric, paprika, and annatto are sourced from concentrated agricultural regions, exposing manufacturers to weather, disease, and geopolitical supply disruption risks.

Market Opportunities

- Reformulation of Confectionery and Bakery Portfolios: The confectionery and bakery reformulation cycle triggered by the 2025 US regulatory action represents a multi-year demand surge. Mars, Hershey, Mondelez, and Ferrero have announced reformulation programmes targeting full natural-colour conversion by 2027-2028.

- Emerging Novel-Source Pigments: Microalgae-derived spirulina blue, gardenia blue, red cabbage extract, and butterfly pea flower are creating new colour-strength and stability options at competitive price points. Spirulina blue FDA approval for expanded applications in May 2025 has accelerated the reformulation of blue and green products previously dependent on synthetic dyes.

- Clean-Label Expansion in Dairy and Plant-Based Products: Plant-based milk, yogurt alternatives, and functional dairy represent a fast-growing application where natural colour systems are specified from product inception.

Market Challenges

- Colour Matching to Legacy Synthetic Hues: Consumer acceptance of reformulated products requires a close visual match to legacy synthetic-dye versions. Matching the vivid reds of Red 40 or the bright yellows of Yellow 5 with plant-derived alternatives is technically difficult and often requires multi-pigment blends that raise formulation cost.

- Regulatory Fragmentation Across Jurisdictions: Natural colour approvals vary across FDA, EFSA, FSSAI, China GB, and ANVISA frameworks, requiring multi-jurisdiction dossier preparation and sometimes separate product formulations. Carmine and copper chlorophyllin face specific restrictions in kosher, halal, and religious-dietary contexts.

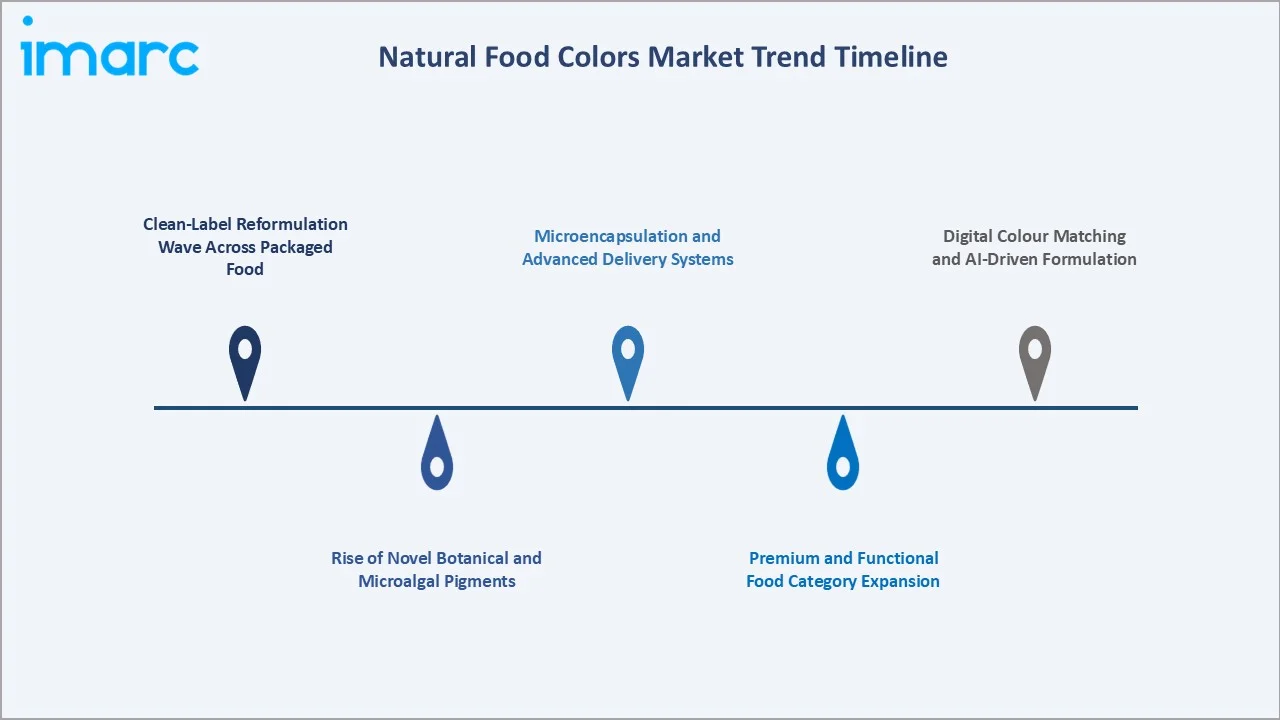

Emerging Market Trends

1. Clean-Label Reformulation Wave Across Packaged Food

Major food manufacturers are executing multi-year reformulation programmes to replace synthetic FD&C dyes with natural alternatives. Kraft Heinz, General Mills, Mars Wrigley, Hershey, and PepsiCo have publicly committed to phase out synthetic colours from their US portfolios by 2027-2028, creating a structural demand tailwind for natural pigment producers.

2. Rise of Novel Botanical and Microalgal Pigments

Spirulina blue, butterfly pea flower extract, gardenia blue, and red cabbage anthocyanins are emerging as next-generation natural colour sources. The FDA's May 2025 expanded approval for spirulina extract in cereals, chips, and snack bar coatings has unlocked reformulation pathways in product categories previously dependent on synthetic blue and green dyes.

3. Microencapsulation and Advanced Delivery Systems

Microencapsulation, liposomal carriers, and emulsion-based delivery platforms are improving the heat, pH, and light stability of natural pigments. These technologies narrow the performance gap versus synthetic dyes, enabling natural colour use in thermally processed, acidic, and light-exposed product formats previously considered incompatible.

4. Premium and Functional Food Category Expansion

Functional beverages, plant-based dairy, protein snacks, and nutraceuticals specify natural colour systems from product inception rather than as reformulation additions. This segment consistently supports premium pricing, enabling natural colour producers to offset higher unit costs through value-based product positioning.

5. Digital Colour Matching and AI-Driven Formulation

Manufacturers are deploying AI-based colour matching software and digital pigment libraries to accelerate natural colour formulation development. This reduces the time and cost of matching legacy synthetic-dye hues, enabling faster reformulation cycles across global food manufacturer portfolios.

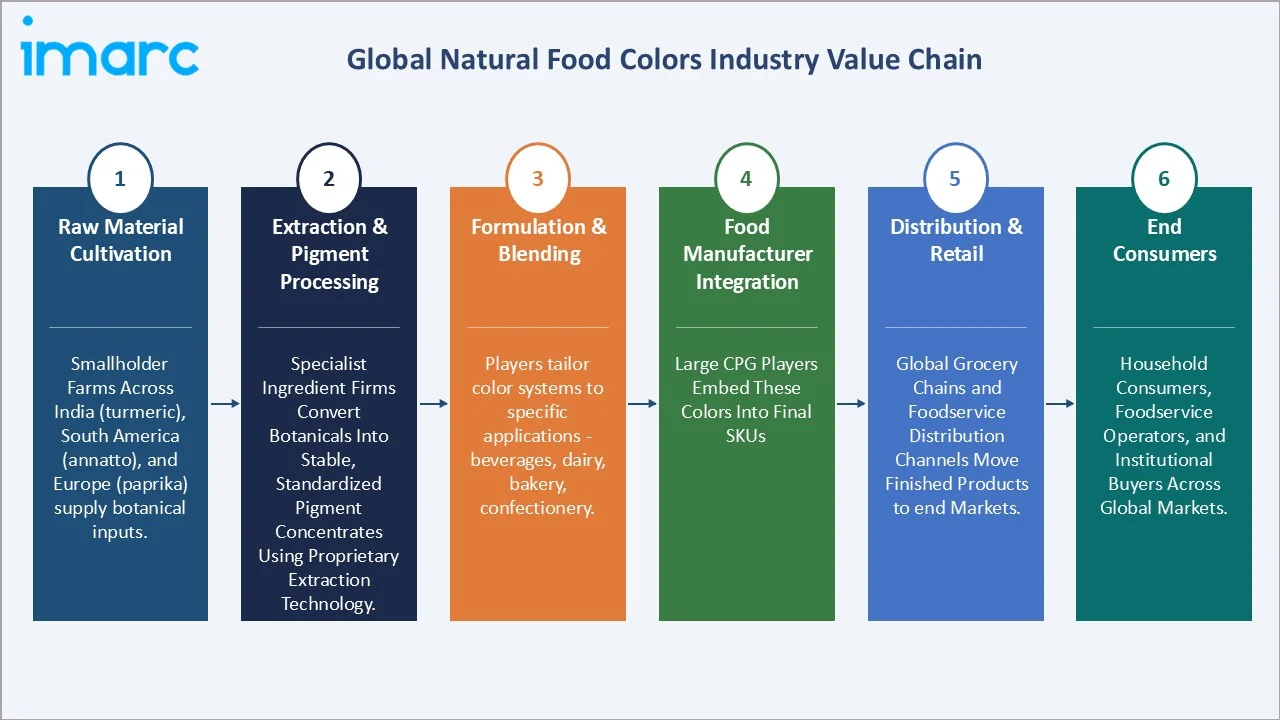

Industry Value Chain Analysis

The natural food colors value chain spans six integrated stages from agricultural raw-material cultivation through end-consumer packaged food delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Raw Material Cultivation |

geographically dispersed and commoditized, relying on smallholder farms across emerging markets — turmeric (India), paprika (Spain, Peru), annatto (Peru, Kenya), and spirulina (China, USA) |

|

Extraction & Pigment Processing |

Specialist ingredient firms convert botanicals into stable, standardized pigments, with high R&D intensity and proprietary IP creating strong entry barriers and premium margins. |

|

Formulation & Blending |

players tailor color systems to specific applications — beverages, dairy, bakery, confectionery — where pH stability, heat resistance, and shelf life drive formulation complexity, making this a technical-services-heavy segment. |

|

Food Manufacturer Integration |

Food manufacturer integration sees large CPG players embed these colors into finished products, with clean-label reformulation and removal of synthetic dyes driving sustained demand growth. |

|

Distribution & Retail |

operates on scale and shelf economics, with global grocery chains and foodservice distributors exerting consistent pricing pressure upstream while controlling consumer access. |

|

End Consumers |

Household consumers, foodservice operators, and institutional buyers |

Extraction and pigment-processing firms capture the highest strategic value in the natural food colors chain, combining proprietary extraction technology, application expertise, and long-standing food manufacturer relationships. Vertical integration from cultivation through blending, pursued by Chr. Hansen and Döhler provide margin insulation against raw-material volatility.

Technology Landscape in the Natural Food Colors Industry

The natural food colors industry is being reshaped by four converging technology frontiers that are narrowing the historical performance gap with synthetic dyes. Advances in stability, biotechnology, extraction, and digital formulation are enabling clean-label reformulation at unprecedented speed and scale across global food and beverage portfolios.

Microencapsulation and Advanced Delivery Systems

Spray drying, liposomal carriers, and nano-emulsion systems have materially improved the heat, light, and pH stability of anthocyanins, carotenoids, and curcumin-based pigments. In 2025, multiple suppliers commercialised nano-emulsion delivery platforms that reduce pigment dosage by 20–30% while extending shelf stability in acidic beverage matrices, narrowing the durability gap with synthetic FD&C dyes.

Precision Fermentation and Biotechnology-Derived Pigments

Precision fermentation has emerged as the most disruptive technology frontier, enabling microbial production of beta-carotene, phycocyanin, and anthocyanin analogues without reliance on agricultural supply chains. Startups such as Michroma and Phytolon, alongside established players including Chr. Hansen and dsm-firmenich, are scaling fermentation-derived natural reds, blues, and yellows that offer consistent quality, year-round supply security, and substantially lower land and water footprints than traditional botanical sourcing.

Green Extraction and Purification Technologies

Supercritical CO2 extraction, pulsed electric field processing, and membrane filtration are progressively replacing traditional solvent-based pigment recovery, delivering higher purity, cleaner regulatory profiles, and solvent-free label claims. These processes also improve pigment yields from botanical feedstocks such as paprika, turmeric, and spirulina by 15–25%, reducing raw-material intensity and strengthening the sustainability narrative of clean-label natural colour systems.

AI-Driven Colour Matching and Digital Formulation

AI-powered colour-matching platforms and digital pigment libraries now enable formulators to replicate target synthetic-dye shades within precise Delta-E tolerance ranges. These tools compress reformulation cycles from months to weeks, accelerate application-specific pigment selection across diverse food matrices, and are becoming a decisive competitive capability for ingredient suppliers supporting global CPG clean-label transition programmes.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Anthocyanin | 🔒 | 2025 |

| Form | Liquid | 46.7% | 2025 |

| Application | Beverages | 29.4% | 2025 |

| Region | Asia Pacific | 38.6% | 2025 |

By Application

Beverages command a 29.4% share in 2025, reflecting the category's central position in the clean-label reformulation wave. Functional beverages, plant-based dairy alternatives, sports and energy drinks, and reformulated carbonated soft drinks are the primary volume drivers. Anthocyanin and carotenoid-based colour systems have largely replaced synthetic reds, oranges, and yellows across North America and Europe.

To access detailed market analysis, Request Sample

Processed Food at 24.6% in 2025 is anchored by confectionery, snacks, sauces, and ready-to-eat meal reformulation. Mars, Hershey, Mondelez, and General Mills are executing multi-year reformulation programmes targeting synthetic dye elimination from US portfolios by 2027-2028. Baked Products holds 17.3% share, centred on dry-mix powdered formats for biscuits, pastries, and fillings where heat-stability is critical. Meat and Savories at 15.8% is driven by the replacement of synthetic red dyes with carmine, annatto, and paprika-based systems, while Others at 12.9% covers dairy, pet food, nutraceutical capsules, and frozen desserts.

By Form

Liquid form dominates at 46.7% in 2025, driven by superior dispersion in water-based beverage, dairy, and sauce matrices, lower dosage requirements, and faster integration into high-throughput bottling and mixing operations. Liquid formats are the format of choice for beverage manufacturers where line speed and homogeneity are critical operational criteria.

Powder form holds 38.2% in 2025, preferred in bakery, dry-mix, confectionery, and savoury snack applications where shelf stability, long storage life, and dry-ingredient compatibility are priorities. Powder formats also travel and store more efficiently, making them attractive for regional distribution across the Asia Pacific and Latin America. Gel form at 15.1% serves premium confectionery, pastry glazes, and artisanal bakery decoration, where controlled viscosity and colour intensity are required for high-end product aesthetics.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

38.6% |

India turmeric/paprika base, China processed-food growth, ASEAN middle-class spending |

|

Europe |

26.4% |

EFSA clean-label rules, E-number labelling, premium food retail, and organic category growth |

|

North America |

21.7% |

2025 FDA synthetic dye phase-out, clean-label consumer shift, retailer private-label mandates |

|

Latin America |

7.2% |

Brazil/Mexico processed-food expansion, annatto production, beverage reformulation |

|

Middle East & Africa |

6.1% |

GCC premium packaged food, halal-certified natural pigments, dairy reformulation |

Asia Pacific commands a 38.6% global revenue share in 2025, the dominant regional position. India is the world's largest producer of turmeric, supplying approximately 75% of global curcumin volume, alongside substantial paprika and annatto cultivation.

Europe at 26.4% in 2025 is shaped by EFSA's E-number labelling framework, which effectively mandates natural colour disclosure on all packaged foods. Germany, France, the United Kingdom, and Italy lead regional demand, supported by mature organic food retail channels and strong consumer willingness to pay a premium for clean-label products.

North America, at 21.7% in 2025, is the most rapidly repositioning regional market. The January 2025 FDA revocation of Red Dye No. 3, followed by the April 2025 HHS-FDA phased industry withdrawal of petroleum-based synthetic dyes, has compressed the reformulation timeline for US food manufacturers from a decade-long evolution to a two-to-three-year transition. Retailer private-label mandates from Walmart, Kroger, and Costco have added further momentum.

Latin America, at 7.2% in 2025, is anchored by Brazil's USD 80+ Billion processed food industry and Mexico's beverage manufacturing base. Peru and Colombia are leading annatto producers. Middle East & Africa at 6.1% is led by GCC premium packaged-food growth and expanding halal-certified natural pigment supply chains serving regional dairy and beverage manufacturers.

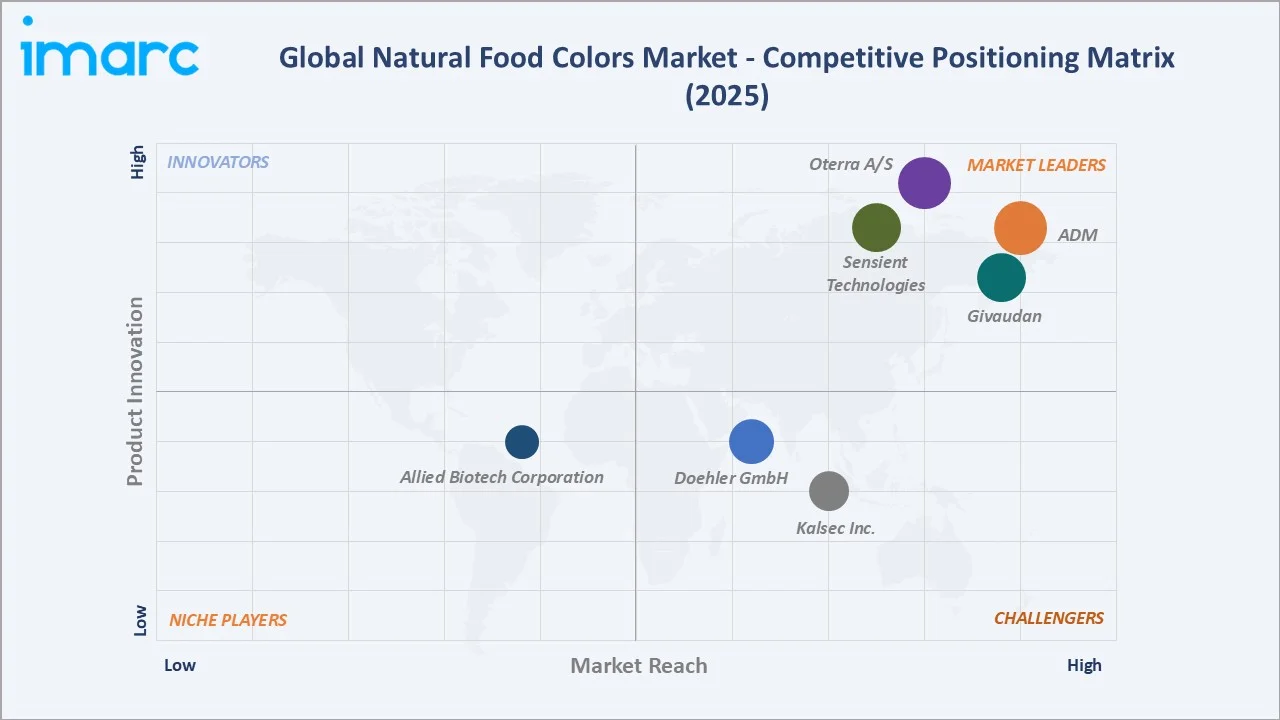

Competitive Landscape

|

Company Name |

Key Brand / Offerings |

Market Position |

Core Strength |

|

ADM |

ADM Colors from Nature |

Leader |

Scale, integrated supply, broad pigment portfolio |

|

Oterra A/S |

FruitMax |

Leader |

Bioscience-led pigments, carmine, and beetroot expertise |

|

Sensient Technologies Corporation |

Sensient Colors |

Leader |

Application-specific formulation, beverage/confectionery |

|

Givaudan |

Givaudan Sense Colours |

Leader |

Botanical extract expertise, premium clean-label focus |

|

Döhler GmbH |

Döhler Natural Colors |

Challenger |

Beverage integration, fruit-derived pigment systems |

|

Kalsec Inc. |

Durabrite |

Challenger |

Paprika/annatto extraction, stability technology |

|

Allied Biotech Corporation |

Altratene β-Carotene |

Emerging |

Carotenoid production, Asia Pacific supply base |

The natural food colors competitive landscape is characterised by a small group of global ingredient suppliers with integrated botanical extraction capabilities, alongside regional specialists in single-pigment categories and emerging biotechnology-driven novel-source suppliers. Givaudan's acquisitions of Naturex (2018) and DDW (2021) have sharpened the industry's consolidation trajectory around scaled, vertically integrated natural ingredient platforms.

Key Company Profiles

ADM

ADM (Archer Daniels Midland Company) is a global ingredient supplier with a broad natural food colors portfolio serving beverage, confectionery, bakery, and dairy manufacturers across more than 170 countries.

- Product & Platform Portfolio: ADM Colours from Nature range covering carotenoid oranges and yellows, anthocyanin reds and purples, caramel colours, curcumin-based systems, and application-specific colour solutions for beverage, bakery, and dairy manufacturers.

- Recent Developments: In October 2023, ADM announced its outlook on the flavor and color trends that will drive product innovation in 2024. With unapologetic abandon for self-expression coupled with individual wellness goals top-of-mind for consumers across regions, ADM has identified four trends that illustrate evolving consumer behaviors and will inspire memorable moments.

- Strategic Focus: ADM's strategy centres on integrated nutrition solutions where natural colours are paired with flavour, protein, and botanical-extract offerings, enabling full clean-label formulation partnerships with global and regional food manufacturers.

Sensient Technologies Corporation

Sensient is a specialist in natural and synthetic colours with deep application-formulation capabilities across beverage, confectionery, bakery, and savoury categories, operating extraction and formulation facilities across North America, Europe, and the Asia Pacific.

- Product & Platform Portfolio: Sensient Colors' natural range covering anthocyanins, carotenoids, caramel, curcumin, spirulina, and proprietary multi-pigment blends engineered for specific application matrices.

- Recent Developments: In March 2026, Sensient Food Colors, a division of Sensient Technologies, commenced a major expansion at its largest natural color plant in St. Louis, Missouri.

- Strategic Focus: Sensient's strategy emphasises application-specific colour formulation, rapid reformulation support for food manufacturers, and technical-service-led customer relationships across global beverage and confectionery accounts.

Givaudan

Givaudan S.A. is a Swiss multinational manufacturer of flavours, fragrances, and active cosmetic ingredients.

- Product & Platform Portfolio: Pink to red shades (oil and water soluble, oil dispersible), Yellow to orange shades (oil and water soluble, water dispersible), Yellow to brown shades (water soluble), Green shades (oil and water soluble), Black.

- Recent Developments: In April 2024, Givaudan Sense Colour rolled out a series of new natural color solutions in line with market demands, including a phycocyanin-rich natural blue hue similar to spirulina, its Endure Red Beet, which can be a suitable replacement for carmine, and a range of anthocyanins.

- Strategic Focus: Givaudan centres on premium organic and clean-label positioning, sustainability-certified sourcing, and a broader flavour and fragrance customer portfolio.

Market Concentration Analysis

The global natural food colors market exhibits moderate concentration among the top natural ingredient suppliers, with ADM, Oterra A/S, Sensient Technologies Corporation, Givaudan, and Döhler GmbH collectively accounting for approximately 40-48% of global market revenue in 2025.

The market is experiencing a bifurcated structural dynamic. At the premium ingredient tier, consolidation is accelerating: Givaudan's acquisitions of Naturex in 2018 and DDW in 2021, combined with Novonesis's 2025 merger of Novozymes and Chr. Hansen has created scaled platforms that smaller regional specialists struggle to match on R&D, regulatory dossier depth, and global customer account coverage.

Simultaneously, the lower tier of the market is fragmenting with novel-source suppliers. Spirulina, butterfly pea, and gardenia blue producers in Asia Pacific and North America are entering the industry with differentiated pigment chemistries, creating pockets of specialist competition that established suppliers address through acquisition, licensing, or strategic partnership.

Investment & Growth Opportunities

Fastest-Growing Segments

Spirulina-derived blue is the highest-growth pigment category at ~7.8% CAGR through 2034, driven by the FDA's May 2025 expanded approval and reformulation of blue and green products previously dependent on synthetic Blue 1 and Blue 2. Anthocyanins are growing at ~6.4% CAGR, enabled by beverage and dairy reformulation demand across North America and Europe.

Emerging Market Expansion

India, China, Brazil, and Indonesia represent the highest-potential emerging geographies through 2034. Rising middle-class spending on branded packaged food, retailer-led clean-label mandates, and growing regulatory alignment with FDA and EFSA frameworks are expanding the addressable market size at a 6-8% annual pace. Precision-fermentation pigments represent the highest-potential revenue model shift in natural food colors' history.

Venture & Private Investment Trends

Notable transactions include Givaudan's continued bolt-on acquisitions of natural ingredient platforms, PAI Partners' investments in botanical extract specialists, and multiple venture rounds in microalgal and precision-fermentation pigment start-ups, including Phytolon, Michroma, and Debut Biotech, reflecting the rising strategic value of fermentation-derived colour molecules at commercial scale.

Future Market Outlook (2026-2034)

The global natural food colors market forecast projects steady value expansion from USD 2.20 Billion in 2025 to USD 3.50 Billion by 2034 at a CAGR of 4.86%, driven by regulatory phase-out of synthetic dyes, sustained clean-label consumer demand, and ongoing reformulation of packaged food portfolios across all major consumer markets through the forecast period.

Three technology discontinuities are most likely to reshape the industry through 2034. Precision fermentation of natural pigments, enabling microbial production of anthocyanins, carotenoids, and novel colour molecules at lower cost and without agricultural supply volatility, is expected to reach commercial scale by 2028-2030. Advanced microencapsulation and lipid-based delivery systems will continue narrowing the stability gap versus synthetic dyes.

By 2034, the natural food colors industry is forecast to have completed its transition from a specialty clean-label niche to the mainstream colour specification across global packaged food and beverage portfolios. Synthetic FD&C dyes are expected to retain only a minority position in limited-use industrial and non-food applications, with natural pigments dominating food and beverage colour demand across all major geographies.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews conducted in 2024-2025 with natural food colors industry stakeholders, including product-development directors at major ingredient suppliers, R&D and procurement leads at global food and beverage manufacturers, regulatory specialists at the FDA and EFSA, and trade association representatives. Primary insights validated market sizing, segmentation estimates, regulatory timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include FDA regulatory publications, EFSA scientific opinions, FSSAI approvals, USDA agricultural data, industry association reports (Natural Food Colours Association, International Food Additives Council), company annual reports, investor presentations, and trade publications, including Food Navigator, Just Food, and Food Business News clean-label coverage.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models, incorporating processed food and beverage category growth, regulatory timeline mapping, pigment-type mix shifts, and regional consumption evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for regulatory, supply, and consumer-adoption uncertainty.

Natural Food Colors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Curcumin, Carotenoids, Anthocyanins, Carmine, Caramel, Copper Chlorophyllin, Others |

| Forms Covered | Liquid, Powder, Gel |

| Applications Covered | Processed Food, Meat and Savories, Beverages, Baked Products, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | ADM, Oterra A/S, Sensient Technologies Corporation, Givaudan, Döhler GmbH, Kalsec Inc., Allied Biotech Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the natural food colors market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global natural food colors market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the natural food colors industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Natural Food Colors Market Report

The global natural food colors market was valued at USD 2.20 Billion in 2025, driven by clean-label reformulation, the FDA's synthetic dye phase-out, and rising beverage category demand.

The market is projected to reach USD 3.50 Billion by 2034, growing at a CAGR of 4.86% during 2026-2034, led by regulatory action on synthetic dyes and accelerating clean-label adoption across US and European packaged food portfolios.

Beverages lead with a 29.4% share in 2025, driven by functional drinks, plant-based dairy reformulation, and the replacement of synthetic red and orange dyes in soft drinks and sports beverages.

Liquid form leads with a 46.7% share in 2025, owing to superior dispersion in beverage and dairy matrices, lower dosage requirements, and faster integration into high-throughput bottling operations.

Asia Pacific leads with a 38.6% share in 2025, driven by India's turmeric production, China's processed-food expansion, and growing middle-class packaged food spending across ASEAN economies.

Key drivers include the 2025 FDA phase-out of FD&C synthetic dyes, over 70% of consumers checking ingredient labels, functional beverage category expansion, and microencapsulation stability advances.

Spirulina-derived blue and carotenoid-based colours are the fastest-growing pigment categories, driven by the FDA's May 2025 expanded approval and beverage and confectionery reformulation programmes.

Leading companies include ADM, Oterra A/S, Sensient Technologies Corporation, Givaudan, Döhler GmbH, Kalsec Inc., and Allied Biotech Corporation.

The FDA's January 2025 revocation of Red Dye No. 3 and April 2025 industry phase-out of FD&C dyes has compressed US reformulation from a decade to a two-to-three-year transition cycle.

Clean-label consumer preference is now mainstream, with over 70% of US grocery shoppers checking ingredient lists and retailers such as Walmart and Kroger mandating natural colours in private-label portfolios.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)