Non-Dairy Creamer Market Size, Share, Trends and Forecast by Origin, Type, Form, Nature, Sales Channel, and Region, 2026-2034

Non-Dairy Creamer Market Size and Share:

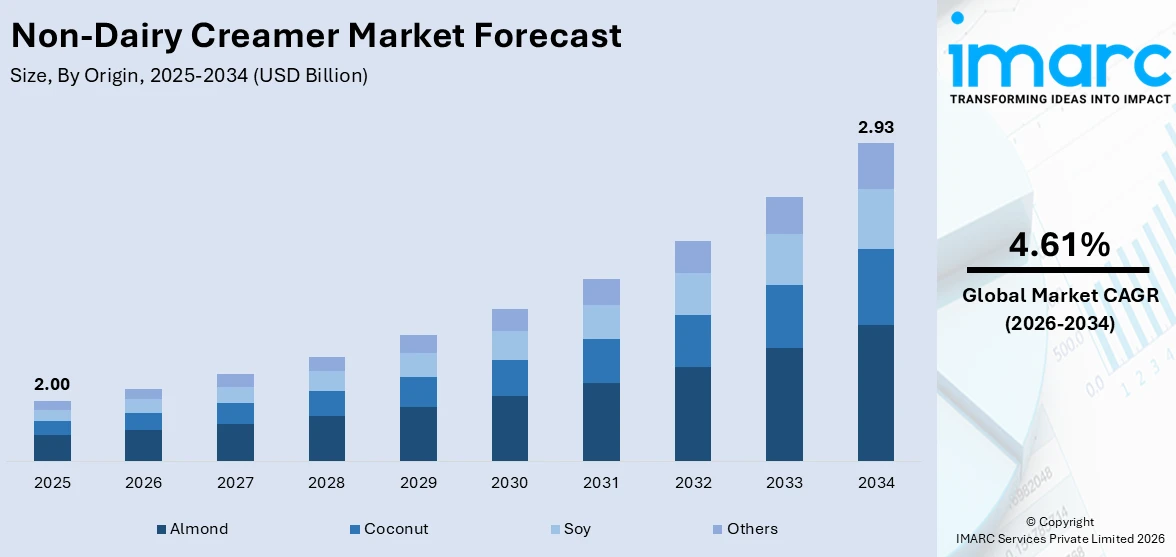

The global non-dairy creamer market size was valued at USD 2.00 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 2.93 Billion by 2034, exhibiting a CAGR of 4.61% from 2026-2034. North America currently dominates the market, holding a market share of 36% in 2025. The area benefits from a well-established coffee culture, high consumer awareness of plant-based and lactose-free dietary options, growing retail infrastructure for dairy substitutes, and robust demand from people looking to add cholesterol-free and low-fat beverages due to growing health consciousness, all contributing to the non-dairy creamer market share.

A confluence of lifestyle, health, and dietary factors is driving the worldwide non-dairy creamer industry and changing customer tastes in various geographical areas. There is a persistent need for dairy-free substitutes in food and beverage applications due to the rising incidence of lactose intolerance among a sizable segment of the adult population worldwide. Additionally, the market for plant-based creamers made from almond, soy, coconut, and oat sources is booming because to the rising popularity of vegan and flexitarian diets. Creamers are being consumed more often in both home and foodservice settings due to global coffee culture and rapid urbanization. Health-conscious consumers are drawn to innovative product formulations that include clean-label ingredients, sugar-free versions, and functional improvements like extra protein and vitamins. The wide availability of non-dairy creamers through supermarkets, online retail platforms, and specialty stores is further non-dairy creamer market growth across both developed and emerging economies.

The US has grown to be a sizable market for non-dairy creamers for a number of reasons. Because of the country's deeply embedded coffee culture, a significant portion of American people drink coffee daily, creamers are in high demand as a beverage adjunct. Customers are gravitating toward non-dairy alternatives that offer comparable flavor and texture without upsetting their digestive systems due to growing health consciousness, particularly because a significant section of the population is lactose intolerant. As plant-based diets gain popularity due to ethical and environmental concerns, almond, oat, and soy-based creamers are becoming more and more popular. Prominent manufacturers are also investing in state-of-the-art facilities and expanding their production capacity to meet the rising demand for innovative creamer products. The expansion of e-commerce platforms and modern retail channels has improved product accessibility and given consumers access to a wider variety of non-dairy creamer options.

To get more information on this market Request Sample

Non-Dairy Creamer Market Trends:

Rising Plant-Based Dietary Adoption

The market for non-dairy creamers is being significantly impacted by the growing trend toward plant-based diets as consumers search for alternatives to traditional dairy products. The primary drivers of this change include growing awareness of the environmental impacts of dairy farming, ethical concerns about animal suffering, and the purported health benefits of plant-derived ingredients. Non-dairy creamers made from almond, coconut, oat, and soy are gaining popularity as healthy substitutes with comparable flavor and smoothness. The emergence of veganism and flexitarianism, particularly among younger populations, is expanding the addressable consumer base beyond individuals with dietary restrictions. The rising proportion of people who identify as vegan or flexitarian in significant nations demonstrates a significant cultural shift in food consumption patterns. Manufacturers are being encouraged by this trend to expand their product lines with cutting-edge plant-based formulas that meet changing dietary requirements and palate preferences in international markets. The increasing use of plant-based creamers in well-known retail and restaurant channels is another indication of the ongoing momentum of this nutritional transition.

Expanding Global Coffee Culture

Non-dairy creamers are in high demand as a necessary beverage adjunct due to the quick spread of coffee culture in both developed and emerging nations. Personalized beverage customisation is being encouraged and consumption occasions are becoming more varied due to the growth of specialty coffee shops, home brewing equipment, and ready-to-drink coffee formats. Demand for high-end non-dairy choices is being driven by consumers' growing experimentation with flavored and functional creamers to emulate café-style experiences in household settings. The non-dairy creamer market outlook is further strengthened by the rising popularity of cold brew and iced coffee beverages that pair well with plant-based creamers offering superior solubility and blending properties. For instance, China's café market expanded by 58% in 2023, surpassing 50,000 stores and overtaking the United States as the world's largest branded coffee shop market. This global café expansion is directly contributing to higher creamer consumption, particularly in the Asia-Pacific region where coffee adoption among younger urban populations is accelerating at an unprecedented rate.

Clean-Label and Health-Conscious Formulations

The rising consumer preference for clean-label products with transparent ingredient lists is reshaping the non-dairy creamer market landscape. Health-conscious individuals are gravitating toward creamers formulated without artificial flavors, preservatives, hydrogenated oils, or excessive sugar content, driving manufacturers to invest in reformulation efforts. The demand for functional non-dairy creamers enriched with added protein, medium-chain triglyceride oils, probiotics, and essential vitamins is creating new premium product categories that command higher price points. This trend aligns with the broader non-dairy creamer market forecast indicating sustained growth in health-oriented product segments. For instance, in November 2025, Danone expanded its Too Good & Co. brand into the coffee creamer category, launching products with approximately 3 grams of sugar per serving compared to about 5 grams in leading competitors, targeting consumers who prioritize reduced sugar intake. Clean-label formulations are particularly resonating with millennials and Generation Z consumers who demonstrate strong willingness to pay premium prices for products that align with their health and wellness priorities across both retail and foodservice channels.

Non-Dairy Creamer Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global non-dairy creamer market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on origin, type, form, nature, and sales channel.

Analysis by Origin:

- Almond

- Coconut

- Soy

- Others

Almond holds 30% of the market share. Almond-based non-dairy creamers have gained popularity due to their smooth texture, subtly nutty flavor, and favorable nutritional profile, which includes less calories and no cholesterol. The increasing consumer demand for products made from almonds is partly due to the widespread perception that almonds are a premium, health-conscious ingredient that satisfies clean-label requirements. Almond creamers are particularly popular in North American and European markets, where they are easily available in flavored and unflavored variations through retail and foodservice channels. The versatility of almond creamers in hot and cold beverages and their suitability for specialty coffee preparations contribute to their ongoing appeal. In order to appeal to consumers seeking natural and minimally processed ingredients, leading producers are continuously expanding their almond-based creamer portfolios to include seasonal and organic alternatives. Online sales of almond creamers are expanding, increasing consumer accessibility and promoting repeat business from a range of demographic groups.

Analysis by Type:

- Low Fat NDC

- Medium Fat NDC

- High Fat NDC

Medium-fat NDC leads the market with a share of 42%. Medium-fat non-dairy creamers strike the perfect balance between creaminess and health-conscious composition, offering consumers a pleasing texture without the higher calorie content of full-fat variants. Because they often contain moderate levels of vegetable oils and emulsifiers, which give both hot and cold beverages a smooth mouthfeel and effective mixing, these products are a versatile choice for daily use. The non-dairy creamer market trends indicate that medium-fat formulations are preferred across commercial and household applications due to their consistent performance and balanced nutritional profile. Manufacturers are gradually introducing medium-fat versions with organic and plant-based ingredient bases to satisfy the increasing demand for cleaner formulations that combine functional benefits with sensory delight. This market niche benefits from its appeal to consumers seeking a balance between indulgence in a range of beverage categories and moderation in their diet.

Analysis by Form:

- Powdered

- Liquid

Powdered dominates the market, with a share of 62%. Because of its long shelf life, portability, affordability, and simplicity of storage without the need for refrigeration, powdered non-dairy creamers continue to have a dominant market position. These goods are especially popular in developing nations where consumers value portability and cost and cold chain infrastructure may be scarce. Powdered forms are commonly used in foodservice operations, vending machines, office settings, and institutional settings where bulk dispensing capabilities and uniform quality are critical. Modern powdered creamers' dissolving qualities have been greatly enhanced by sophisticated spray-drying technologies and emulsification procedures that guarantee seamless beverage blending. Their firmly established place in the worldwide market is demonstrated by the broad use of powdered non-dairy creamers in both developed and developing nations' retail and commercial distribution channels. Manufacturers continue to enhance product quality through improved solubility and flavor consistency, ensuring that powdered formats remain a preferred choice for consumers and businesses seeking reliable, shelf-stable, and economically viable creamer solutions.

Analysis by Nature:

- Organic

- Conventional

Conventional represents the leading segment, with a market share of 70%. Traditional non-dairy creamers dominate the market primarily due to their affordable prices, wide availability, and established distribution networks that ensure accessibility through a range of worldwide retail and foodservice channels. These products, which are produced using standard vegetable oils, corn syrup solids, and emulsifiers, offer a consistent flavor and texture at reasonable costs, making them accessible to a broad spectrum of customers. Because of economies of scale in production and raw material sourcing, conventional formulations enable manufacturers to maintain cheaper retail price when compared to organic alternatives. Their dominant position is further reinforced by the fact that traditional non-dairy creamers are widely used in emerging nations in the Middle East, Asia-Pacific, and Latin America, where consumers are still heavily influenced by price. The continued preference for standardized unflavored formulations in everyday beverage consumption is another indication of the strength of traditional versions. Manufacturers continue to increase manufacturing efficiencies and expand distribution partnerships in order to maintain the competitive pricing advantage that underpins this segment's market leadership.

Analysis by Sales Channel:

Access the comprehensive market breakdown Request Sample

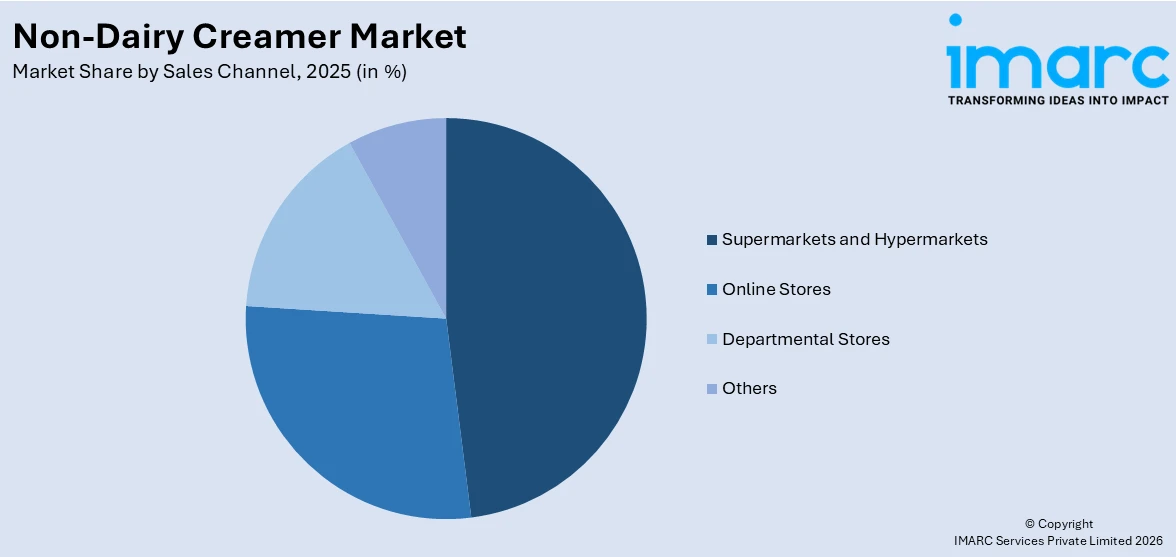

- Supermarkets and Hypermarkets

- Online Stores

- Departmental Stores

- Others

Supermarkets and hypermarkets hold 48% of the market share. Because of their large product selections, easy shopping experiences, and capacity to provide competitive prices through bulk purchase agreements, supermarkets and hypermarkets are the main distribution channels for non-dairy creamers. These retail formats enable customers to make well-informed purchasing decisions by giving them the chance to compare several brands, flavors, and formulations in a single visit. In contemporary retail settings, the amount of shelf space devoted to dairy substitutes has increased dramatically in recent years, reflecting both customer demand and retailers' dedication to carrying plant-based product categories. Promotional events, in-store sampling, and private-label products that increase consumer interaction with non-dairy creamers are also advantageous for supermarkets and hypermarkets. This distribution route is being further strengthened by the growing cooperation between producers of non-dairy creamers and big-box stores to launch limited-edition product lines and seasonal products. Mainstream consumers are being encouraged to try new goods by the deliberate placement of non-dairy creamers next to traditional dairy products in store aisles.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 36% of the share, enjoys the leading position in the market. The region's dominance is a result of high rates of lactose intolerance among different demographic groups, a deeply ingrained coffee-drinking culture, and a robust retail infrastructure that ensures wide product availability across supermarkets, convenience stores, and online platforms. The US, as the primary regional demand generator, benefits from continuous product innovation resulting from large manufacturers' expenditures in new flavors, practical ingredients, and eco-friendly packaging. Canadian consumers are adopting non-dairy alternatives as part of broader health and wellness trends that highlight plant-based nutritional options. The increasing number of specialty coffee shops in the region and the expanding popularity of at-home brewing are driving up demand for non-dairy creamers that replicate café-quality beverage experiences. North America's robust e-commerce infrastructure is supporting the company's sustained dominance in the worldwide sector while also giving consumers more access to a range of non-dairy creamer brands and formulas.

Key Regional Takeaways:

United States Non-Dairy Creamer Market Analysis

The United States is the largest national market for non-dairy creamers because of the country's massive coffee consumption, shifting dietary preferences, and sophisticated retail environment that accommodates a wide range of product offers. The growing prevalence of lactose intolerance in a significant section of the population is the main factor driving the demand for dairy-free creamer alternatives. Manufacturers are expanding their product lines to include almond, oat, coconut, and soy-based formulations in response to American consumers' increasing demand for clean-label products with reduced sugar content and plant-based ingredients. Premium non-dairy creamer products are in high demand due to the increase in at-home coffee preparation, especially among younger generations who consider personalized home-brewed beverages to be an inexpensive daily luxury. Thanks to the expansion of e-commerce platforms, consumers can now locate and purchase specialty and niche creamer brands, thus enhancing product accessibility. Customers' increasing desire to add a choice of flavored and functional creamer options to their coffee cups is reinforcing the United States' position as the world's largest national market for non-dairy creamers.

Europe Non-Dairy Creamer Market Analysis

The market for non-dairy creamers in Europe is expanding rapidly due to factors like growing awareness of lactose intolerance, the growing popularity of vegan and flexitarian diets, and supportive laws that promote the production and consumption of plant-based foods. The availability and diversity of dairy-free creamer products are expanding significantly across retail and foodservice channels in key regions like Germany, the UK, and France. Organic, clean-label, and sustainably sourced products are highly preferred by the European customer base, which motivates producers to invest in high-end formulations that meet these demands. The need for barista-grade non-dairy creamers that consistently produce frothing and blending performance is being further heightened by the growing café culture in Western and Northern European nations. The market is being further stimulated by government programs in several European countries that support the development of plant-based foods and increase consumer awareness. A wider cultural trend toward plant-forward dietary patterns is reflected in the region's increasing incorporation of non-dairy creamers into mainstream retail shelves and restaurant menus.

Asia-Pacific Non-Dairy Creamer Market Analysis

The Asia-Pacific region represents a high-growth market for non-dairy creamers, propelled by rapid urbanization, expanding coffee culture, rising disposable incomes, and the high prevalence of lactose intolerance across the population. Countries including China, India, Japan, South Korea, and Indonesia are witnessing increasing adoption of coffee as a lifestyle beverage, driving demand for creamers across institutional, foodservice, and retail channels. The powdered non-dairy creamer segment maintains particular strength in this region due to favorable pricing, extended shelf stability, and compatibility with local beverage preparation methods including instant coffee and tea applications. For instance, India's coffee exports more than doubled over the past decade, reaching USD 1.8 billion in the fiscal year 2024 according to the Ministry of External Affairs, reflecting the expanding domestic and export-oriented coffee ecosystem that supports associated product categories.

Latin America Non-Dairy Creamer Market Analysis

Due to the region's long-standing coffee consumption customs, rising health consciousness, and growing urbanization, the non-dairy creamer industry in Latin America is growing gradually. The two main demand hubs where consumers are progressively adding dairy substitutes to their regular beverage routines are Brazil and Mexico. The region's market is developing steadily thanks to the growing influence of global dietary trends toward plant-based and dairy-free products as well as the expanding modern retail infrastructure. Supermarkets, hypermarkets, and online retail channels are increasing the availability of non-dairy creamers, which is improving product accessibility and promoting trial uptake among health-conscious consumers looking for reasonably priced dairy-free beverage additions.

Middle East and Africa Non-Dairy Creamer Market Analysis

Growing urbanization, growing coffee culture, and growing consumer awareness of dairy-free products are all driving the non-dairy creamer market in the Middle East and Africa. One important demand channel in the area is the foodservice industry, specifically quick-service restaurants and coffee shops. Demand for creamer products is being driven by the growth of regional and worldwide coffee chains in major cities, which is generating new occasions for consumption. The region's acceptance of non-dairy creamer products is being gradually aided by growing young populations, changing dietary choices, and developing sophisticated retail infrastructure.

Competitive Landscape:

Both well-known global firms and niche dairy substitute businesses are present in the competitive non-dairy creamer market, pursuing strategies focused on product innovation, taste diversification, and geographic expansion. In order to develop formulations that closely mimic the flavor, texture, and functionality of conventional dairy creamers while incorporating health-focused features like reduced sugar, added protein, and clean-label ingredients, leading manufacturers are making large investments in research and development. Companies are strengthening their distribution networks and reaching new customer segments through strategic acquisitions, alliances with coffee chains, and partnerships with foodservice providers. The plant-based sector is seeing more rivalry as manufacturers set themselves apart with new ingredient bases including lentil, pea protein, and unique nut blends. As customers show a rising preference for environmentally concerned firms, sustainability measures such as recyclable packaging, materials sourced responsibly, and decreased environmental footprints are increasingly affecting competitive positioning.

The report provides a comprehensive analysis of the competitive landscape in the non-dairy creamer market with detailed profiles of all major companies, including:

- Balchem Corporation

- Califia Farms LLC

- Compact Industries Inc.

- Custom Food Group

- Danone S.A.

- Frusela UAB

- Laird Superfood

- Nestlé S.A.

- nutpods

- Rich Products Corporation

- TreeHouse Foods Inc.

- Viceroy Holland B.V.

Latest News and Developments:

- In January 2025, Violife, owned by Flora Food Group, launched its Supreme Sweet Cream lentil-based coffee creamers at select Walmart stores across the United States. The dairy-free range debuted in three flavors: Boldly Original, Tempting Vanilla, and Seductive Caramel, featuring a breakthrough lentil protein formula designed to prevent separation and curdling in both hot and iced beverages.

Non-Dairy Creamer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Origins Covered | Almond, Coconut, Soy, Others |

| Types Covered | Low Fat NDC, Medium Fat NDC, High Fat NDC |

| Forms Covered | Powdered, Liquid |

| Natures Covered | Organic, Conventional |

| Sales Channels Covered | Supermarkets and Hypermarkets, Online Stores, Departmental Stores, Others |

| Region Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Balchem Corporation, Califia Farms LLC, Compact Industries Inc., Custom Food Group, Danone S.A., Frusela UAB, Laird Superfood, Nestlé S.A., nutpods, Rich Products Corporation, TreeHouse Foods Inc., Viceroy Holland B.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the non-dairy creamer market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global non-dairy creamer market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the non-dairy creamer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Non-Dairy Creamer Market Report

The non-dairy creamer market was valued at USD 2.00 Billion in 2025.

The non-dairy creamer market is projected to exhibit a CAGR of 4.61% during 2026-2034, reaching a value of USD 2.93 Billion by 2034.

The non-dairy creamer market is primarily driven by the rising prevalence of lactose intolerance affecting approximately 68% of the global population, growing adoption of vegan and flexitarian diets, expanding coffee culture worldwide, increasing consumer preference for clean-label and health-conscious formulations, and the expanding availability of diverse plant-based creamer options through modern retail and e-commerce channels.

North America currently dominates the non-dairy creamer market, accounting for a share of 36%. The region benefits from deeply entrenched coffee consumption culture, high consumer awareness of dairy-free alternatives, continuous product innovation by major manufacturers, and robust retail infrastructure.

Some of the major players in the non-dairy creamer market include Balchem Corporation, Califia Farms LLC, Compact Industries Inc., Custom Food Group, Danone S.A., Frusela UAB, Laird Superfood, Nestlé S.A., nutpods, Rich Products Corporation, TreeHouse Foods Inc., Viceroy Holland B.V., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)