OLED Materials Market Report by Type (Substrates, Encapsulation, Anode, Hole Injection Layer (HIL), Hole Transport Layer (HTL), Electron Transport Layer (ETL), Emissive Layer (EML), Cathode), Application (Display, Lighting), End Use (Residential Products, Commercial Products, Industrial Products), and Region 2026-2034

Global OLED Materials Market:

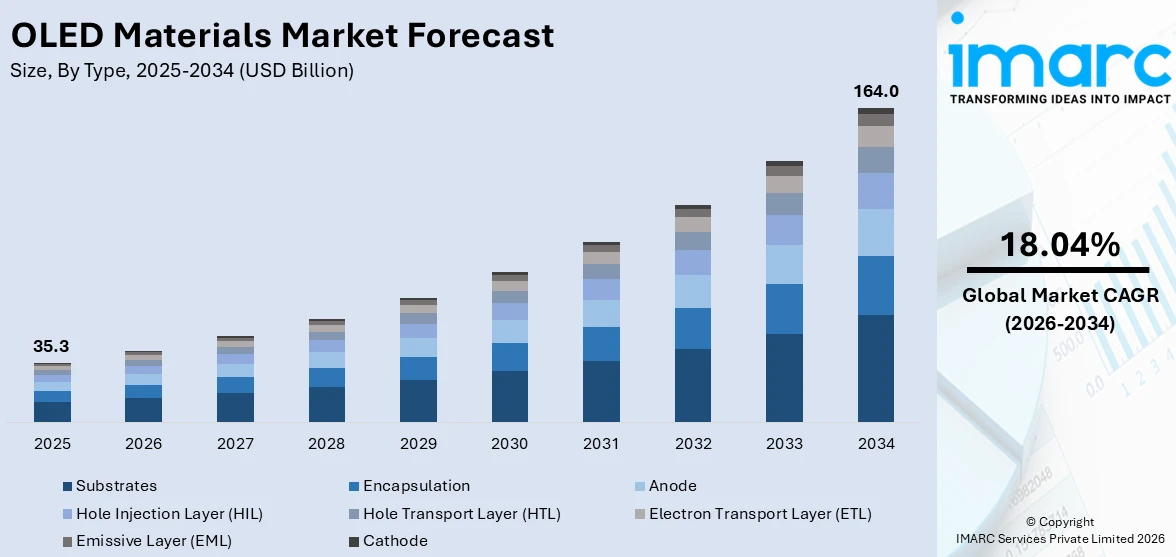

The global OLED materials market size reached USD 35.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 164.0 Billion by 2034, exhibiting a growth rate (CAGR) of 18.04% during 2026-2034. At present, Asia Pacific represents the largest region owing to the increase in the uptake of consumer electronic devices like curved televisions and premium smartphones. The increasing demand for flexible and foldable display technologies, along with the increasing adoption of consumer electronics, is primarily driving the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 35.3 Billion |

|

Market Forecast in 2034

|

USD 164.0 Billion |

| Market Growth Rate 2026-2034 | 18.04% |

OLED Materials Market Analysis:

- Major Market Drivers: The growing usage of superior image quality, energy efficiency, and flexible design capabilities is one of the significant factors driving the growth of the market. Additionally, the escalating adoption of consumer electronic devices, such as smartphones, laptops, televisions, etc., on account of the elevating levels of lifestyles and the inflating spending capacities, is also contributing to the market growth.

- Key Market Trends: Continuous innovations in OLED materials to achieve higher resolution, better color reproduction, and longer lifespan are creating a positive outlook for the overall market. Moreover, they offer reduced power consumption, lower carbon footprint, and recyclability, which is further catalyzing the market.

- Competitive Landscape: Some of the leading companies operating in the global market include DuPont de Nemours Inc., Heraeus Holding GmbH, Hodogaya Chemical Co. Ltd., Idemitsu Kosan Co. Ltd., LG Chem Ltd., Merck KGaA, Samsung SDI Co. Ltd., Sumitomo Chemical Co. Ltd., Tokyo Chemical Industry Co. Ltd., and Universal Display Corporation, among many others.

- Geographical Trends: According to the report, Asia-Pacific currently dominates the global market, owing to the escalating demand for curved televisions and premium smartphones. The widespread sales of passenger vehicles are also acting as significant growth-inducing factors.

- Challenges and Opportunities: One of the challenges hindering the market is the high manufacturing costs and competition from other display technologies. Opportunities lie in advancing material efficiency and enhancing environmental sustainability through innovative manufacturing processes.

To get more information on this market Request Sample

OLED Materials Market Trends:

Growing Use of OLED Displays in Smartphones and TVs

The market for OLED materials is growing as producers are increasingly incorporating OLED displays into smartphones, high-end TVs, and wearable technology. Phone producers are continually looking for thinner, lighter, and more power-efficient screens to satisfy consumer demand for slim, high-performance devices. OLED technology is offering benefits like higher color fidelity, improved contrast ratios, and the possibility to produce flexible and foldable displays that cannot be achieved using conventional LCDs. TV makers are also equipping their higher-end products with OLED panels to meet the demand from the high-end market segment that puts a premium on superior image quality as well as design stylings. With growing demand for enhanced visual experiences, the need for high-quality OLED material is rising, motivating suppliers to invest in developing the business and increasing capacity. The IMARC Group predicts that the global smartphone market is expected to attain 1,998.2 Million Units by 2033.

Growing Investments in Future-Proof Flexible and Foldable Displays

Substantial investments in flexible and foldable display technology are driving the OLED materials market. Big-name electronics companies are investing heavily continuously in research and development to commercialize innovative form factors that increase user convenience and design flexibility. Flexible OLED panels are helping device manufacturers bring new categories like foldable smartphones, rollable TVs, and curved monitors to market. For instance, in 2025, Samsung announced its plans of launching its seventh generation of foldable phones. These innovations are driving increasing demand for specialized OLED materials that preserve performance while providing mechanical flexibility. Firms are pursuing the development of novel organic compounds, substrates, and encapsulation technologies to overcome the challenges related to durability and manufacturing yield. With increased competition in the high-end user electronics market, the demand for innovative flexible displays is continuously driving the market for high-performance OLED materials globally.

OLED Material Efficiency and Lifespan Technological Advances

Ongoing technological innovation is having an important role in driving the market. Research organizations and material suppliers are heavily investing in the creation of OLED compounds that provide improved brightness, color persistence, and operating life. OLED panels have a history of being disadvantaged by shorter operating life and image retention, particularly with blue-emitting materials. New developments are overcoming these limitations through the design of new emissive materials and host-dopant systems that enhance the endurance and efficiency of OLED panels. These advancements are allowing for broader deployment in use cases that require long life in operation, like TVs and commercial digital signage. As material science continues to evolve, manufacturers are streamlining production processes to boost yield and minimize defects, further decreasing costs and bringing OLED displays within reach. This cycle of innovation is supporting the market growth by ensuring OLED technology keeps pace with novel display competitors. LG Electronics (LG) revealed its 2025 OLED evo collection, showcasing a variety of cutting-edge TV models, featuring the world's first genuine wireless OLED evo M5 and OLED evo G5 variants. At the heart of the newest OLED evo models lies LG's α (Alpha) 11 AI processor Gen21, delivering unmatched OLED picture quality characterized by perfect blacks, outstanding brightness, and sophisticated processing features. Fueled by AI-enabled personalization, the LG OLED evo delivers a bespoke experience designed for every user and exemplifies the peak of OLED advancement for enhanced home entertainment.

OLED Materials Market Growth Drivers:

Increasing Demand for Energy-Efficient and Green Display Solutions

Both individuals and manufacturers are focusing on energy efficiency and sustainability, which is driving the demand for OLED materials. OLED technology has the advantage of consuming less power than conventional display technologies such as LCD since it does not need a backlight and can control each pixel's illumination individually. This aspect is making devices perform more efficiently with batteries and have smaller energy footprints. More and more brands are promoting OLED screens as sustainable solutions that comply with global sustainability objectives and regulatory demands to reduce carbon emissions. Suppliers are concentrating on producing OLED materials that not only provide high performance but also prolong the life span of panels, hence cutting electronic waste. Governments and green groups are promoting the use of cleaner technologies, which is driving the OLED materials market as companies react to changing regulatory environments and demands for environment friendly electronics.

Widening Use of OLED Technology Across Consumer Electronics

OLED materials sector is becoming diversified as more producers are making use of OLED technology across conventional consumer electronics. Automakers are making use of OLED panels for sophisticated infotainment systems, instrument clusters, and interior light solutions, taking advantage of OLED's design freedom and better display quality. The lighting sector is investigating OLED panels for architectural and decor lighting applications because they can create diffuse, uniform lighting with innovative form factors. The wearable tech business is also incorporating OLED displays in smartwatches, fitness trackers, and AR devices to offer lightweight and highly colorful screens. This growing variety of applications creates demand for novel material formulations that address diverse requirements in terms of performance, longevity, and aesthetics.

More Collaborations and Strategic Alliances Between Industry Actors

The OLED materials market is experiencing a rise in strategic alliances and collaborations between material suppliers, display firms, and technology firms. These collaborations are encouraging collaborative development initiatives to drive material innovation faster, streamline supply chains, and lower production costs. Firms are sharing resources to address technical hurdles related to scalability and yield improvement of future OLED panels. Strategic partnerships are also assisting companies in procuring long-term supply contracts with top display makers, guaranteeing reliable demand for high-quality OLED materials. Intellectual property sharing and licensing contracts are driving quicker commercialization of proprietary materials technologies. Through collaboration, industry participants are reinforcing their competitive standings and forging synergies driving market development. This cooperation trend is driving the market, prompting ongoing improvements in material performance, and facilitating widespread adoption of OLED technology globally.

Global OLED Materials Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global OLED materials market report, along with forecasts at the global, regional, and country levels from 2026-2034. Our report has categorized the market based on type, application, and end use.

Breakup by Type:

- Substrates

- Encapsulation

- Anode

- Hole Injection Layer (HIL)

- Hole Transport Layer (HTL)

- Electron Transport Layer (ETL)

- Emissive Layer (EML)

- Cathode

Substrates hold the majority of the total market share

The OLED materials market report has provided a detailed breakup and analysis of the market based on the type. This includes substrates, encapsulation, anode, hole injection layer (HIL), hole transport layer (HTL), electron transport layer (ETL), emissive layer (EML), and cathode. According to the report, substrates represented the largest market segmentation.

Substrates are crucial in the market as they serve as the foundation upon which OLED layers are deposited to form displays or lighting panels. Demand for substrates stems from their role in determining the performance and durability of OLED devices. Glass substrates are commonly used due to their transparency, thermal stability, and smooth surface, ideal for high-resolution displays. Flexible plastic substrates are gaining traction for their ability to enable bendable and rollable OLED displays, catering to the growing demand for flexible electronics. As OLED technology advances, the demand for versatile and high-quality substrates continues to grow to meet diverse application needs.

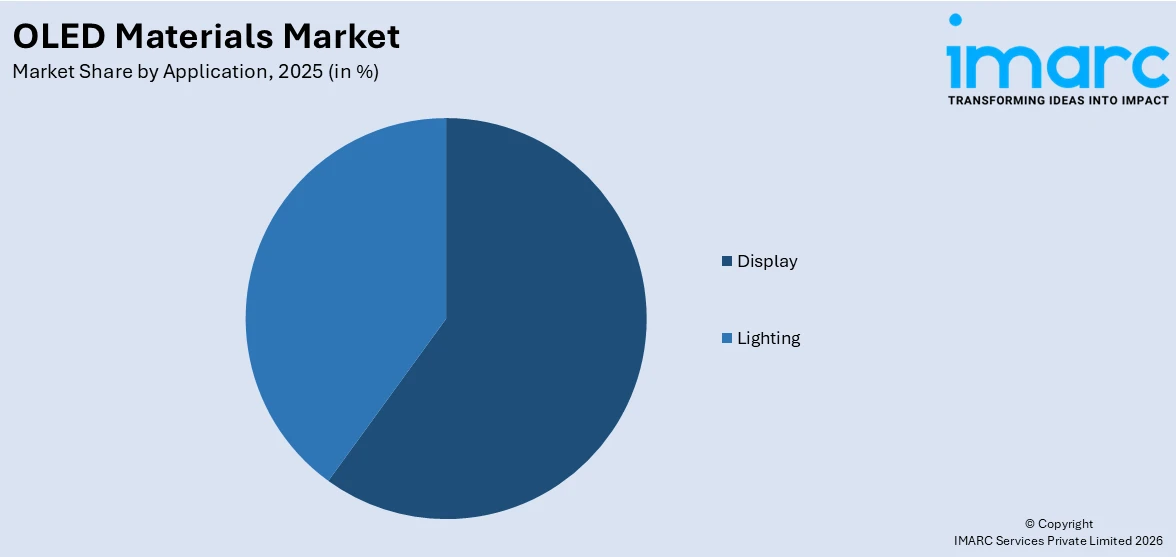

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Display

- Television and Monitors

- Smartphones

- Notebooks and Tablets

- Automotive

- Others

- Lighting

Display currently exhibits a clear dominance in the market

The OLED materials market report research report has provided a detailed breakup and analysis of the market based on the application. This includes display (television and monitors, smartphones, notebooks and tablets, automotive, and others) and lighting. According to the report, display represented the largest market segmentation.

Their unique advantages drive the demand for OLED materials in displays over traditional LCD technology. They enable displays with superior image quality, including vibrant colors, deep blacks, and wide viewing angles. They offer flexibility in design, allowing for curved or foldable screens in smartphones and tablets. OLED displays also consume less power, contributing to longer battery life in portable devices. As consumer electronics continue to demand thinner, lighter, and more energy-efficient displays, OLED materials play a crucial role in meeting these requirements and enhancing the overall user experience.

Breakup by End Use:

- Residential Products

- Commercial Products

- Industrial Products

Residential products account for the largest market share

The report has provided a detailed breakup and analysis of the market based on the end use. This includes residential products, commercial products, and industrial products. According to the report, residential products represented the largest market segmentation.

The growth of the segment can be attributed to the rising demand for consumer electronics and lighting fixtures within homes. OLED materials are employed in manufacturing televisions, where they enable ultra-thin screens with vibrant colors, high contrast ratios, and energy efficiency. Furthermore, a significant rise in demand for OLED TVs in the residential sector is offering lucrative growth opportunities to the overall market. For instance, Samsung's OLED TV lineup recorded about 1.01 million units sold in 2023, capturing a market share of 22.7%.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific currently dominates the global market

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia-Pacific accounted for the largest market share.

The economies of major Asia Pacific countries like India and China are growing, leading to an increase in the uptake of consumer electronic devices like curved televisions and premium smartphones. Thus driving the OLED materials market in the region. Moreover, the OLED materials market forecast by IMARC indicates that Chinese companies are moving quickly to set up large-scale production bases to churn out OLEDs. For instance, BOE is constructing a production plant for smaller OLEDs in the southwestern Chinese city of Chongqing. The OLED production line is the largest for a single factory in China, producing 115 million panels annually. Also, the Tech giant Apple Inc. is investing in developing its foldable phone and has planned to start the assembly plant in India for premium iPhones. The commencement of this plant will make its phones available at cheaper rates. Hence, the demand will drive the growth of the OLED market in the region.

Competitive Landscape:

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major market companies have also been provided. Some of the key players in the market include:

- DuPont de Nemours Inc.

- Heraeus Holding GmbH

- Hodogaya Chemical Co. Ltd.

- Idemitsu Kosan Co. Ltd.

- LG Chem Ltd.

- Merck KGaA

- Samsung SDI Co. Ltd.

- Sumitomo Chemical Co. Ltd.

- Tokyo Chemical Industry Co. Ltd.

- Universal Display Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Global OLED Materials Market News:

- June 2025: South Korea's Dongjin Semichem has licensed out its OLED material patents to industry leaders like Germany's Merck and Japan's Idemitsu Kosan, underscoring its technological strength and robust patent base.

- June 2025: OLEDWorks GmbH, a fully owned German subsidiary of OLEDWorks LLC (Rochester, NY, USA), has been awarded an investment grant from the joint task "Improvement of Regional Economic Structure" to double its OLED production facility in Aachen. The project, called "OLEDWorks Production Capacity Extension 0.5 (CE05)", is aimed at doubling the firm's capacity for the production of organic light-emitting diodes (OLEDs) for application in the automotive sector.

- June 2025: China's BOE will deliver a total of 45 million iPhone OLED units in 2025 with the potential to double that if needed by Apple.

- May 2025: Solus Advanced Materials revealed on May 28 that its green phosphorescent host with differentiated features and proprietary intellectual property (IP) has finally gained approval from customers after years of research and development (R&D) and is now in the preparation phase for large-scale production.

- February 2025: OLEDWorks, the worldwide frontrunner in multi-stack organic light-emitting diode (OLED) technology, revealed a strategic investment from Japan Display Inc. (JDI). OLEDWorks and JDI intend to create a top-tier advanced display facility in the United States by utilizing JDI’s cutting-edge display technology and manufacturing expertise along with OLEDWorks’ established U.S. presence, multi-stack OLED technology, and manufacturing and product skills.

- May 2024: Apple launched iPad Pros with dual-layer OLED displays and M4 chipsets.

- March 2024: Xiaomi announced a strategic partnership with Lumilan, an OLED materials provider, to develop new materials for smartphone display applications.

- January 2024: ASUS introduced the Zenbook 14 OLED with Intel Core Ultra processor as the latest addition to the Zenbook Classic series in India.

Global OLED Materials Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Substrates, Encapsulation, Anode, Hole Injection Layer (HIL), Hole Transport Layer (HTL), Electron Transport Layer (ETL), Emissive Layer (EML), Cathode |

| Applications Covered |

|

| End Uses Covered | Residential Products, Commercial Products, Industrial Products |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | DuPont de Nemours Inc., Heraeus Holding GmbH, Hodogaya Chemical Co. Ltd., Idemitsu Kosan Co. Ltd., LG Chem Ltd., Merck KGaA, Samsung SDI Co. Ltd., Sumitomo Chemical Co. Ltd., Tokyo Chemical Industry Co. Ltd., Universal Display Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the OLED materials market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global OLED materials market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the OLED materials industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the OLED Materials Market Report

The global OLED materials market was valued at USD 35.3 Billion in 2025.

We expect the global OLED materials market to exhibit a CAGR of 18.04% during 2026-2034.

The rising adoption of wireless devices to maintain connectivity in remote areas without the need for long cable wires is primarily driving the global OLED materials market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary halt in numerous production activities for OLED materials.

Based on the type, the global OLED materials market can be segmented into substrates, encapsulation, anode, Hole Injection Layer (HIL), Hole Transport Layer (HTL), Electron Transport Layer (ETL), Emissive Layer (EML), and cathode. Currently, substrates hold the majority of the total market share.

Based on the application, the global OLED materials market has been divided into display and lighting. According to OLED materials market outlook by IMARC, display currently exhibits a clear dominance in the market.

Based on the end use, the global OLED materials market can be categorized into residential products, commercial products, and industrial products. Currently, residential products account for the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global OLED materials market include DuPont de Nemours Inc., Heraeus Holding GmbH, Hodogaya Chemical Co. Ltd., Idemitsu Kosan Co. Ltd., LG Chem Ltd., Merck KGaA, Samsung SDI Co. Ltd., Sumitomo Chemical Co. Ltd., Tokyo Chemical Industry Co. Ltd., and Universal Display Corporation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)