Online Grocery Market Size, Share, Trends and Forecast by Product Type, Business Model, Platform, Purchase Type, and Region, 2026-2034

Online Grocery Market Size, Share, Trends & Forecast (2026-2034)

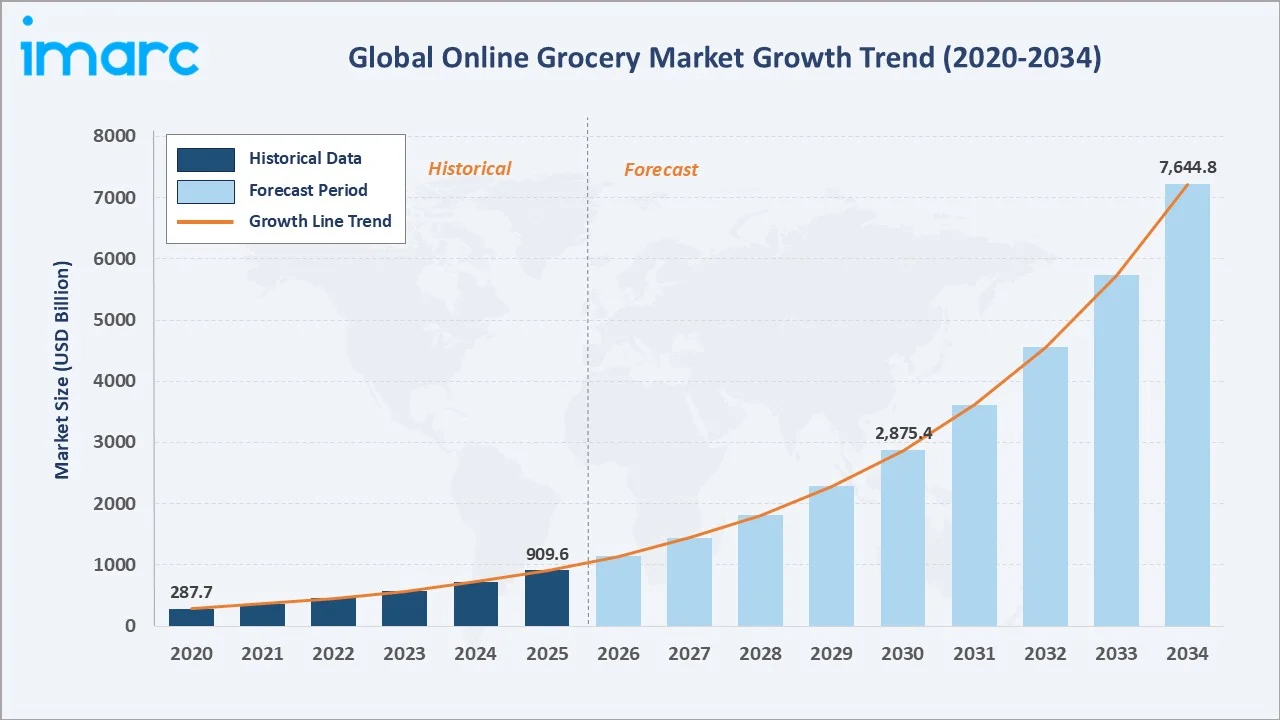

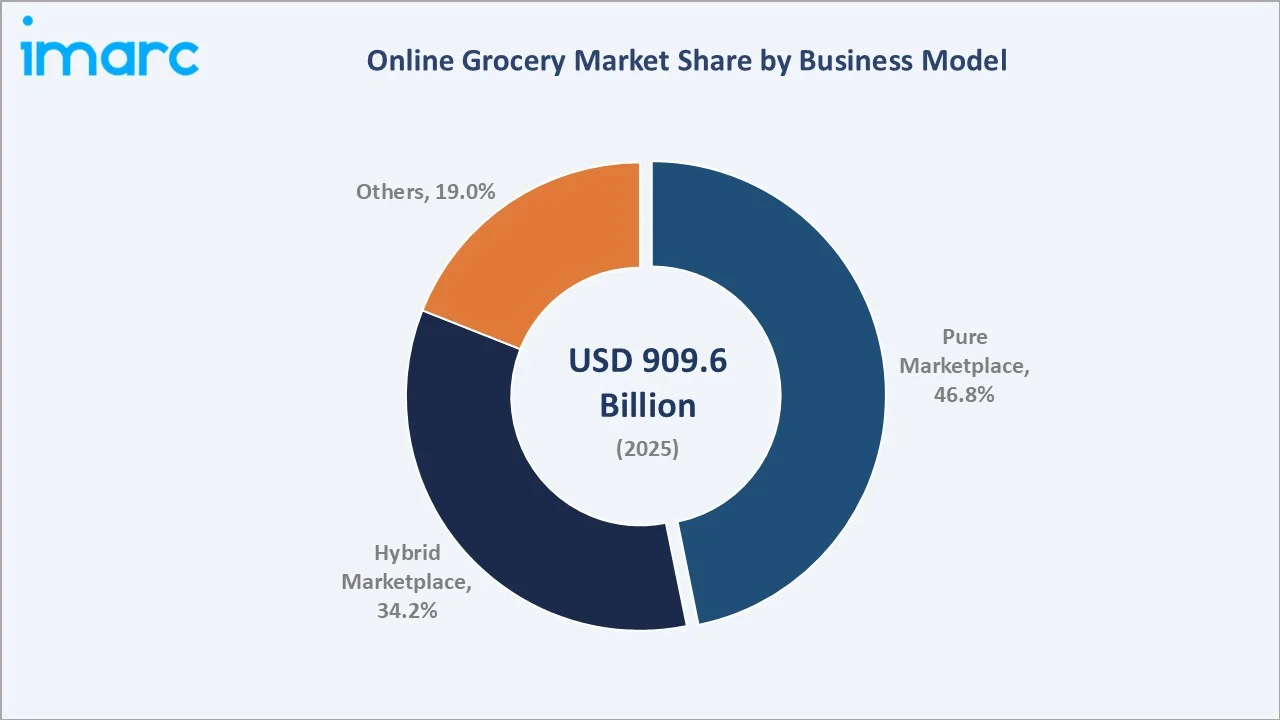

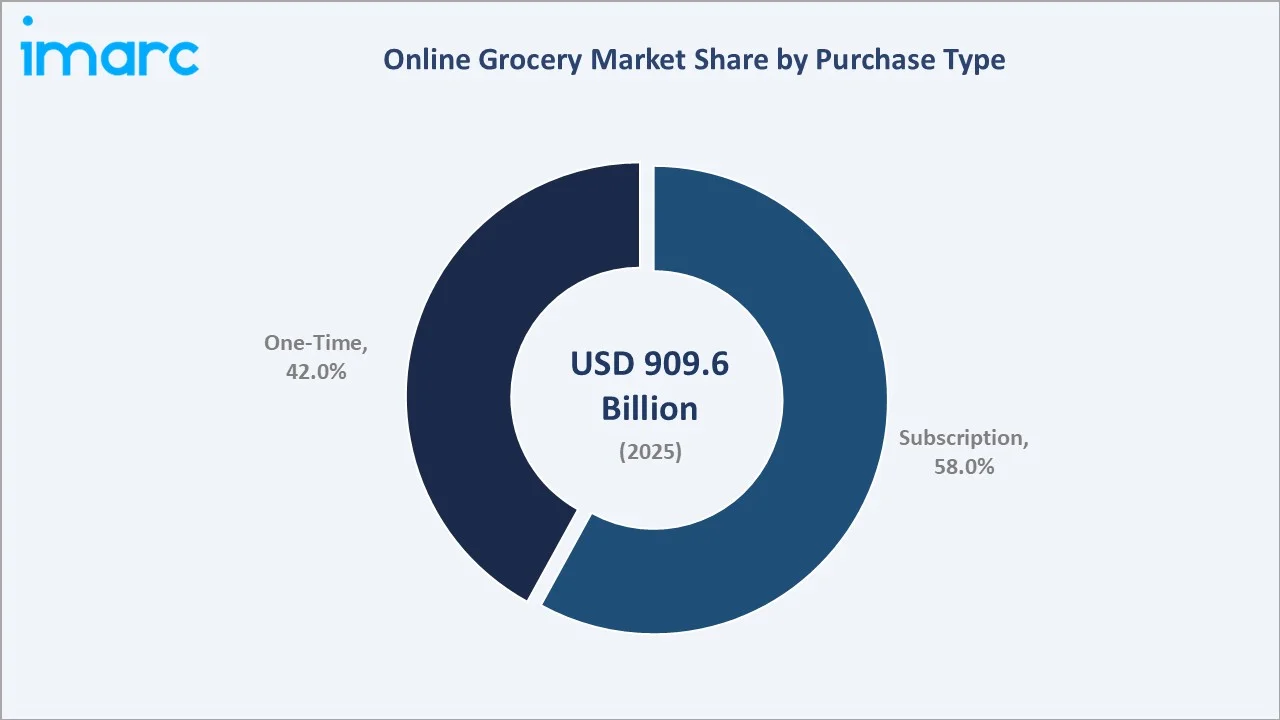

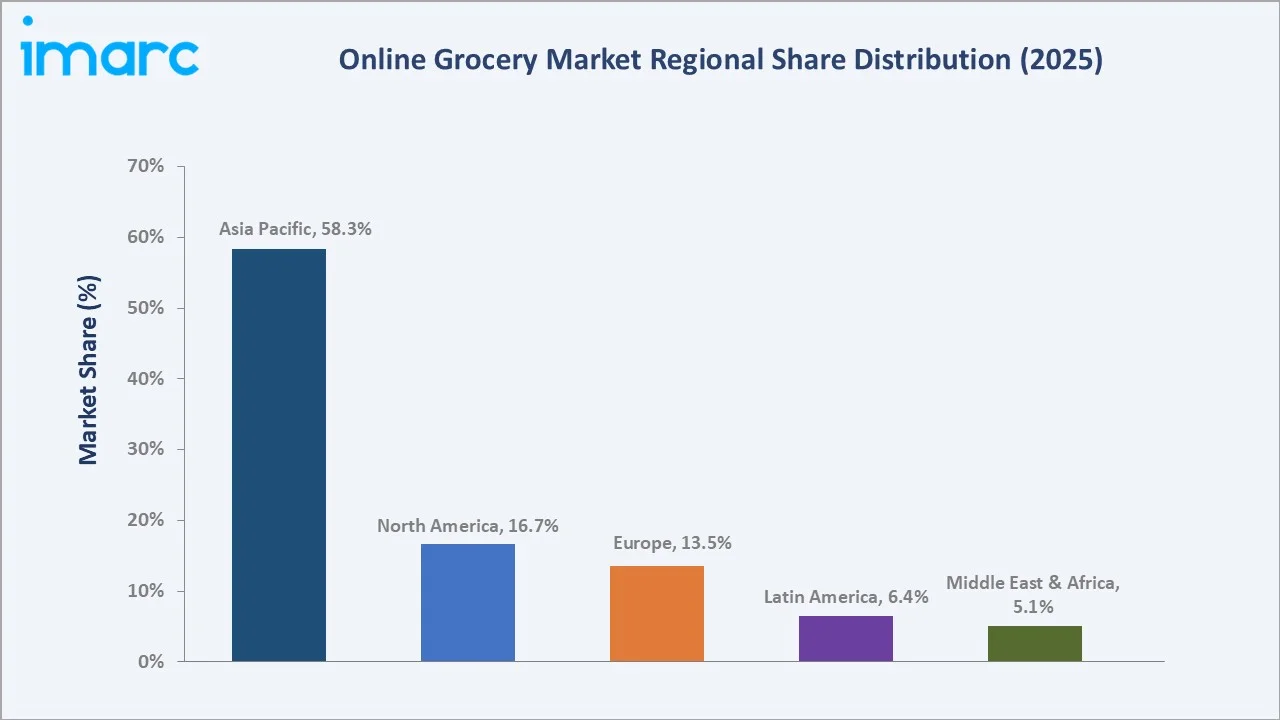

The global online grocery market reached USD 909.6 Billion in 2025 and is projected to reach USD 7,644.8 Billion by 2034, growing at a CAGR of 25.88% during 2026-2034. By the end of 2025, online grocery purchasing had expanded to 61% of households across the United States, while online channels accounted for 19% of total grocery expenditure during December 2025. This rising consumer shift toward digital grocery shopping is driving the online grocery market by increasing demand for convenient home delivery, quick commerce services, personalized shopping experiences, and omnichannel retail strategies among grocery retailers. Pure marketplace dominates at 46.8%. Subscription purchase type leads at 58.0%. Asia Pacific commands 58.3% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 909.6 Billion |

|

Forecast Market Size (2034) |

USD 7,644.8 Billion |

|

CAGR (2026-2034) |

25.88% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Business Model |

Pure Marketplace (46.8%, 2025) |

|

Dominant Purchase Type |

Subscription (58.0%, 2025) |

|

Leading Region |

Asia Pacific (58.3%, 2025) |

The market expanded from USD 287.7 Billion in 2020 to USD 909.6 Billion in 2025, anchored at USD 2,875.4 Billion in 2030, and forecast to reach USD 7,644.8 Billion by 2034. COVID-19 was the catalytic event that permanently accelerated online grocery adoption globally. Lockdowns, social distancing, and the convenience of home delivery created first-time online grocery shoppers among demographics that had previously resisted digital grocery. The post-COVID retention of grocery shopping behavior has been substantially higher than anticipated.

To get more information on this market, Request Sample

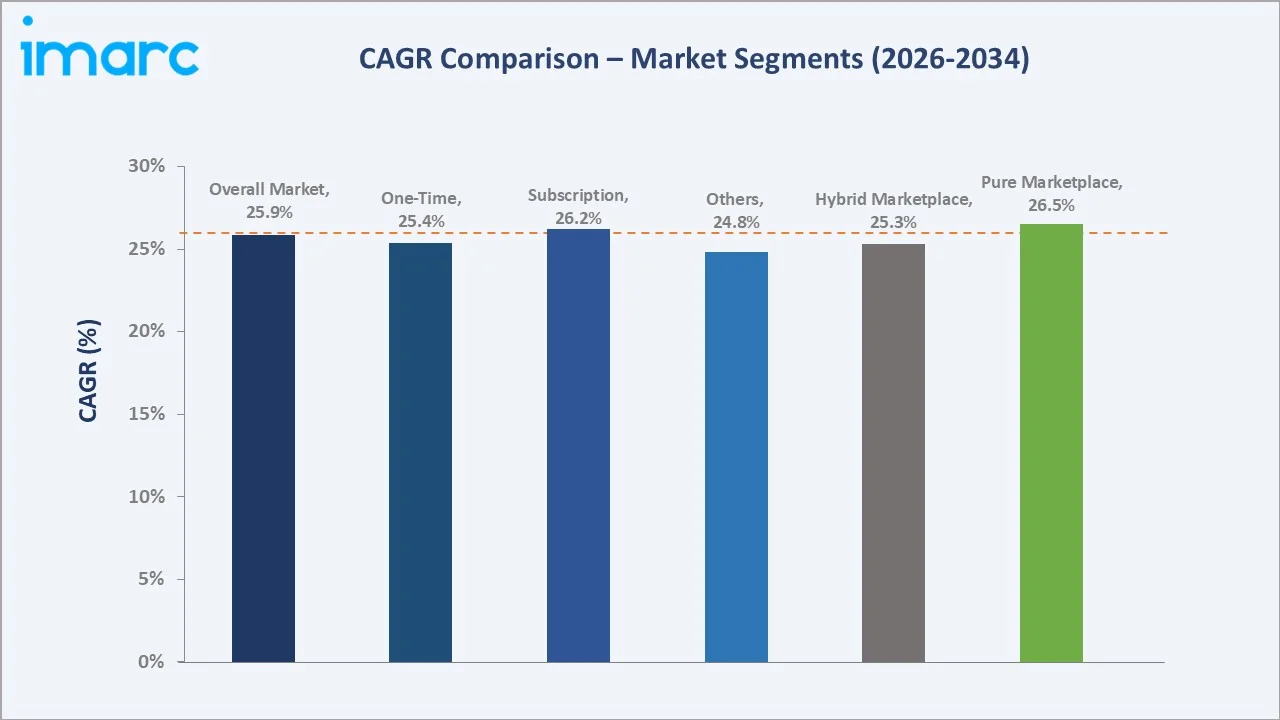

Pure marketplace grows fastest at ~26.5% CAGR as open marketplace platforms leverage existing massive consumer bases and logistics infrastructure to scale grocery assortment with minimal incremental capital. Subscription purchase type grows at ~26.2% CAGR as Amazon, Walmart, BigBasket, and regional equivalents create grocery habit-forming subscription relationships that sustain household retention with significantly lower customer acquisition cost than transactional one-time purchase models.

Executive Summary

The global online grocery market reached USD 909.6 Billion in 2025, representing the world's most rapidly growing major consumer segment. Grocery represents 30-40% of all household consumer spending globally, and the digitization of this massive consumption category at 25.88% CAGR creates wealth creation, consumer value, and supply chain transformation at a scale that few industry transitions in history have matched. The market's expansion from USD 287.7 Billion (2020) to USD 909.6 Billion (2025) validates that COVID-19 created not a temporary e-commerce spike but a permanent structural shift in how humans buy groceries. The market is projected to reach USD 7,644.8 Billion by 2034.

Pure marketplace at 46.8% dominates through Amazon, Flipkart Grocery, and regional equivalents' ability to leverage their existing massive marketplace ecosystems for grocery acquisition at near-zero incremental cost versus the greenfield customer acquisition investments required by dedicated online grocery startups. Subscription purchase type at 58.0% reflects the grocery category's inherent repeat purchase nature. Asia Pacific at 58.3% leads globally.

Key Market Insights

|

Insight |

Data |

|

Dominant Business Model |

Pure Marketplace - 46.8% share (2025) |

|

Dominant Purchase Type |

Subscription - 58.0% market share (2025) |

|

Leading Region |

Asia Pacific - 58.3% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Pure Marketplace at 46.8% reflecting the commercial power of leveraging existing mega-platform ecosystems for grocery category expansion without incremental customer acquisition cost: Pure Marketplace platforms' market dominance is structurally sustained by network effects that dedicated grocery players cannot replicate, Amazon already has Prime membership relationships that include payment credentials, delivery address, and behavioral data, enabling Amazon Fresh to acquire grocery customers by adding a category benefit to existing Prime rather than building independent grocery customer acquisition from zero.

- Subscription at 58.0% reflecting the grocery category's structural alignment with subscription economics: Subscription purchase type's 58.0% market dominance reflects that grocery is inherently a subscription behavior even without explicit subscription programs; online grocery subscription formalization simply adds delivery benefit incentives to naturally recurring grocery purchasing.

- Asia Pacific at 58.3% reflecting the region's structural advantages in online grocery: Asia Pacific's 58.3% market share reflects demographic, geographic, and behavioral advantages that make the region uniquely suited to online grocery penetration at speed and scale. China's tier-1 and tier-2 city residential compounds create delivery density economics that make 10-30 minute delivery economically viable at delivery fee structures, making online grocery cost-competitive with physical grocery shopping, including transportation cost.

Online Grocery Market Overview

The global online grocery market encompasses all retail grocery transactions completed through digital channels - e-commerce platforms, supermarket digital channels, quick commerce platforms, and social commerce channels. The market includes all grocery product categories purchased online: fresh produce (fruits, vegetables, dairy, meat, fish), packaged groceries (FMCG branded goods, private label), beverages (soft drinks, juices, bottled water), household care (cleaning products), personal care, and baby care products. The market encompasses various delivery models: same-day/express delivery, Q-commerce, scheduled slot delivery, click-and-collect BOPIS (Buy Online Pick In Store), and subscription box delivery.

The ecosystem integrates FMCG brands and fresh food suppliers, digital platform and app developers, warehouse management and dark store operators, last-mile delivery infrastructure, digital payment providers, and end consumers ranging from urban millennials to suburban families and senior citizens with varying delivery speed and quality requirements.

Market Dynamics

To evaluate market opportunities, Request Sample

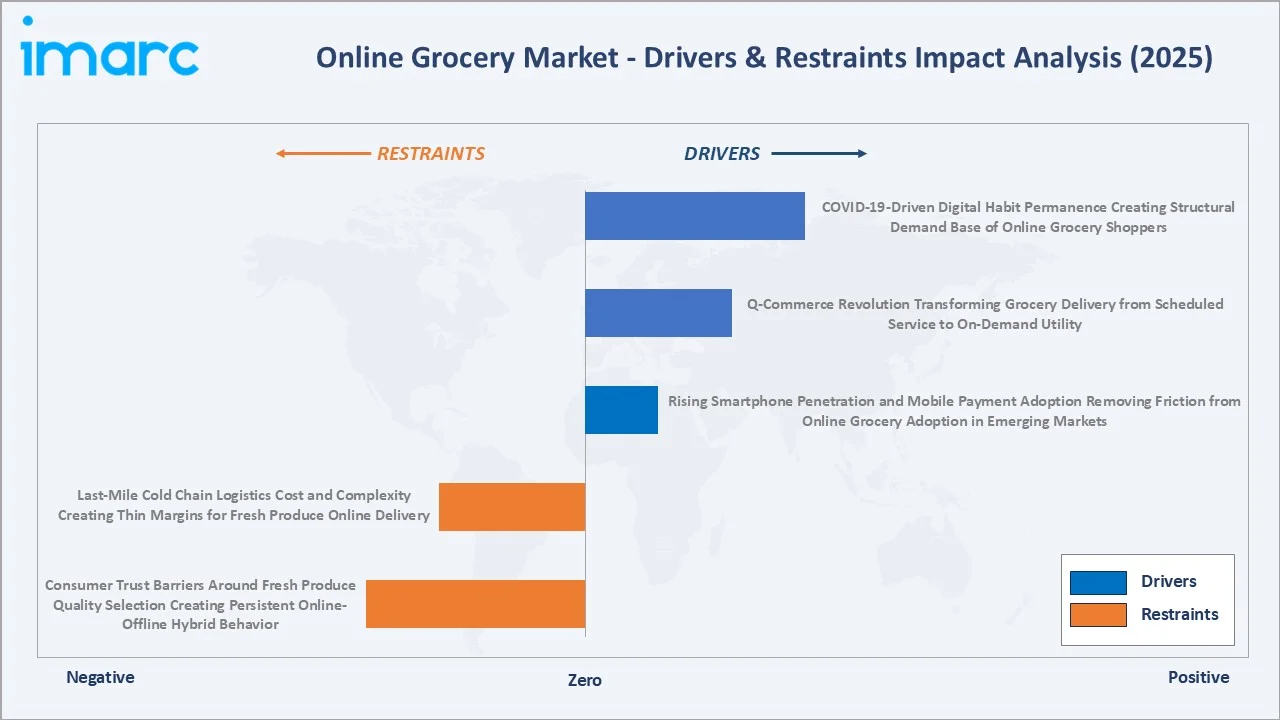

Market Drivers

- COVID-19-Driven Digital Habit Permanence Creating Structural Demand Base of Online Grocery Shoppers: The COVID-19 pandemic created the largest single behavioral adoption event in digital commerce history. During the pandemic, 42% of the US population purchased their groceries online at least once a week. Global lockdowns and physical store restrictions in 2020-2021 forced hundreds of millions of consumers to try online grocery shopping for the first time, including demographics that had previously been resistant to e-commerce for grocery. This installed user base now compounds organically as word-of-mouth, platform marketing, and generational demographics add new online grocery users annually without extraordinary acquisition investment.

- Q-Commerce Revolution Transforming Grocery Delivery from Scheduled Service to On-Demand Utility: Quick commerce has fundamentally changed the value proposition of online grocery delivery from a scheduled weekly shop to an instant-gratification on-demand utility comparable to tap water availability. Blinkit's 10-minute delivery in India, Zepto's 10-minute dark store network, collectively demonstrate that Q-commerce is viable as a commercial model at operating density.

- Rising Smartphone Penetration and Mobile Payment Adoption Removing Friction from Online Grocery Adoption in Emerging Markets: Globally, 82 per cent of individuals 10 years or older own a mobile phone. This rising smartphone penetration and growing adoption of mobile payment platforms are accelerating online grocery adoption in emerging markets by making digital shopping more accessible, convenient, and seamless for consumers. Improved internet connectivity, app-based grocery platforms, and secure digital payment systems are reducing transaction barriers and encouraging higher frequency of online grocery purchases, particularly in urban and semi-urban areas.

Market Restraints

- Last-Mile Cold Chain Logistics Cost and Complexity Creating Thin Margins for Fresh Produce Online Delivery: Fresh produce (fruits, vegetables, dairy, meat, fish) represents 35-45% of grocery basket value and consumer interest in online grocery, but fresh produce online delivery requires cold chain logistics that adds USD 2-5 per delivery in incremental logistics cost versus ambient grocery delivery. Cold chain complexity increases product spoilage and customer dissatisfaction if temperature management is compromised in transit.

- Consumer Trust Barriers Around Fresh Produce Quality Selection Creating Persistent Online-Offline Hybrid Behavior: Consumer trust in fresh produce quality remains the single most cited barrier to exclusive online grocery adoption globally. The inability to physically select individual produce items creates quality uncertainty for online orders, where a trained store associate or algorithm makes the selection on the consumer's behalf.

Market Opportunities

- Tier-2 and Tier-3 City Online Grocery Expansion Representing the Next Consumer Opportunity: The majority of global online grocery growth investment in 2020-2025 has concentrated in tier-1 metropolitan areas where logistics density economics are favorable. However, tier-2 and tier-3 cities globally represent 50-60% of total grocery spending and remain substantially under-penetrated by online channels.

- AI-Predicted Grocery Replenishment Automating Routine Household Restocking: AI-predicted grocery replenishment enables platforms to automate routine household purchases based on consumer behavior, usage patterns, and purchasing history. This technology improves customer convenience, increases repeat purchases, and strengthens subscription-based grocery delivery models while helping retailers enhance inventory planning and customer retention.

Market Challenges

- Profitability at Scale Remaining Elusive for Dedicated Online Grocery Platforms Despite Revenue Growth: Despite 25.88% CAGR and USD 909.6 Billion market scale, dedicated online grocery operators' profitability remains challenging. The pattern across global online grocery startups is revenue scale without profitability at delivered food margins of 18-25% against picking, packaging, and last-mile delivery costs that can consume 20-35% of order value, leaving negative contribution margin on small basket orders.

- Supply Chain Complexity and Food Safety Compliance Creating Operational Challenges at Scale: Online grocery's supply chain is among the most operationally complex in all of e-commerce - managing perishable inventory, maintaining cold chain from supplier to dark store to consumer doorstep, handling product weight variability, coordinating with assortments requiring daily availability updates, and ensuring food safety compliance across distributed dark store networks where food safety audit frequency and rigor varies. Any food safety incident creates reputational and regulatory exposure that is disproportionately damaging for online grocery platforms.

Emerging Market Trends

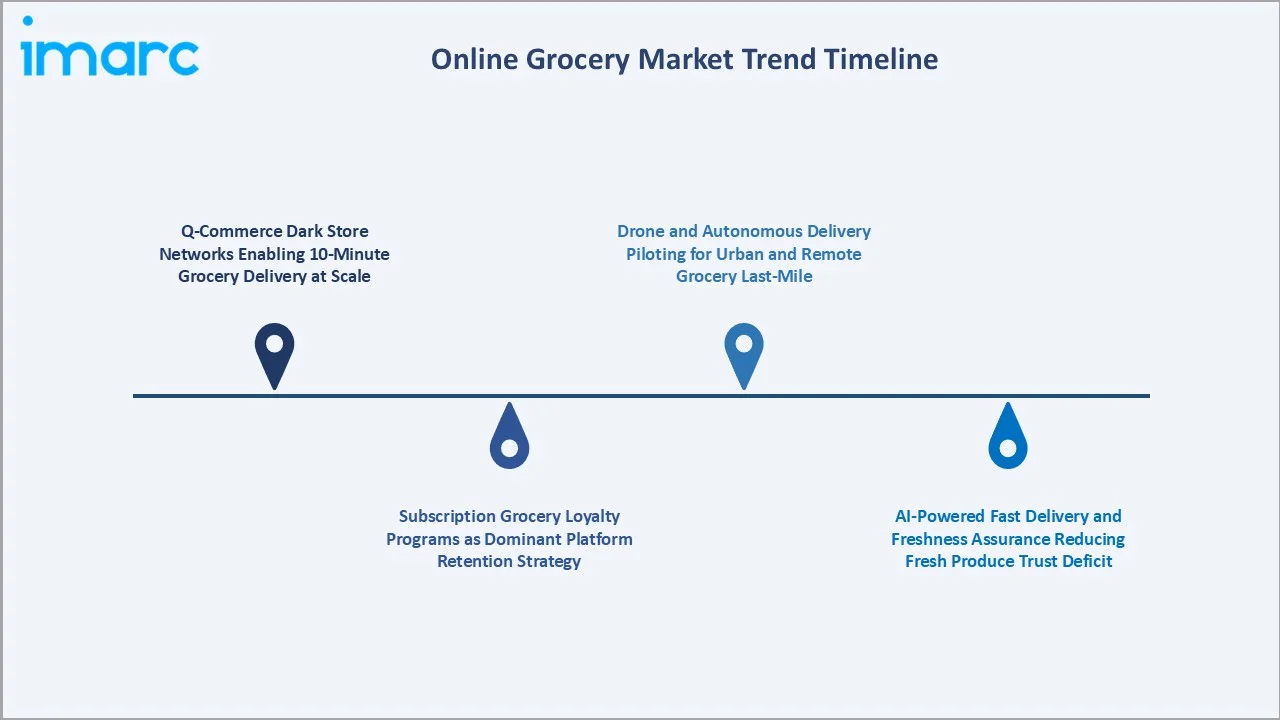

1. Q-Commerce Dark Store Networks Enabling 10-Minute Grocery Delivery at Scale

Q-commerce dark store networks enable ultra-fast grocery deliveries within 10 to 15 minutes across densely populated urban areas. Retailers are increasingly establishing localized micro-fulfillment centers and AI-driven inventory systems to improve order processing speed and delivery efficiency. This model is enhancing consumer convenience for urgent and small-basket purchases while intensifying competition among online grocery and quick-commerce platforms. Growing urbanization and rising demand for instant delivery services are further accelerating the adoption of dark store-based grocery operations.

2. Subscription Grocery Loyalty Programs as Dominant Platform Retention Strategy

Subscription grocery loyalty programs are emerging as retailers focus on strengthening customer retention and increasing repeat purchase frequency. The best grocery loyalty program examples include Kroger’s Boost, LuLu happiness program, Albertsons for U, and Amazon Prime. Companies are offering benefits such as free delivery, exclusive discounts, priority delivery slots, and personalized promotions to encourage long-term platform engagement. These programs also help online grocery providers improve customer lifetime value and generate predictable recurring revenue streams. Increasing competition among digital grocery platforms is further accelerating the adoption of subscription-based loyalty strategies.

3. AI-Powered Fast Delivery and Freshness Assurance Reducing Fresh Produce Online Trust Deficit

AI-powered fast delivery and freshness assurance help retailers improve consumer trust in fast delivery and fresh produce, dairy, meat, and bakery products. Companies are increasingly using AI-based quality inspection, predictive shelf-life analytics, and smart inventory monitoring systems to maintain product freshness and reduce spoilage. In December 2025, Albertsons Companies, Inc. introduced a new AI-powered shopping assistant as part of its digital transformation strategy, aiming to reduce average online grocery shopping time from 46 minutes to just four minutes. These technologies enhance transparency, improve customer satisfaction, and minimize return rates for perishable items. Growing consumer expectations for high-quality fresh groceries are further driving the adoption of AI-enabled freshness management solutions.

4. Drone and Autonomous Delivery Piloting for Urban and Remote Grocery Last-Mile

Drone and autonomous delivery piloting is emerging as retailers seek faster, more efficient, and cost-effective last-mile delivery solutions for urban and remote locations. Companies are testing autonomous robots, self-driving delivery vehicles, and drone-based delivery systems to reduce delivery times, optimize logistics costs, and improve service coverage in hard-to-reach areas. These technologies also help address labor shortages and rising operational expenses in traditional delivery networks. Increasing investments in smart logistics and regulatory support for autonomous mobility are further accelerating market adoption.

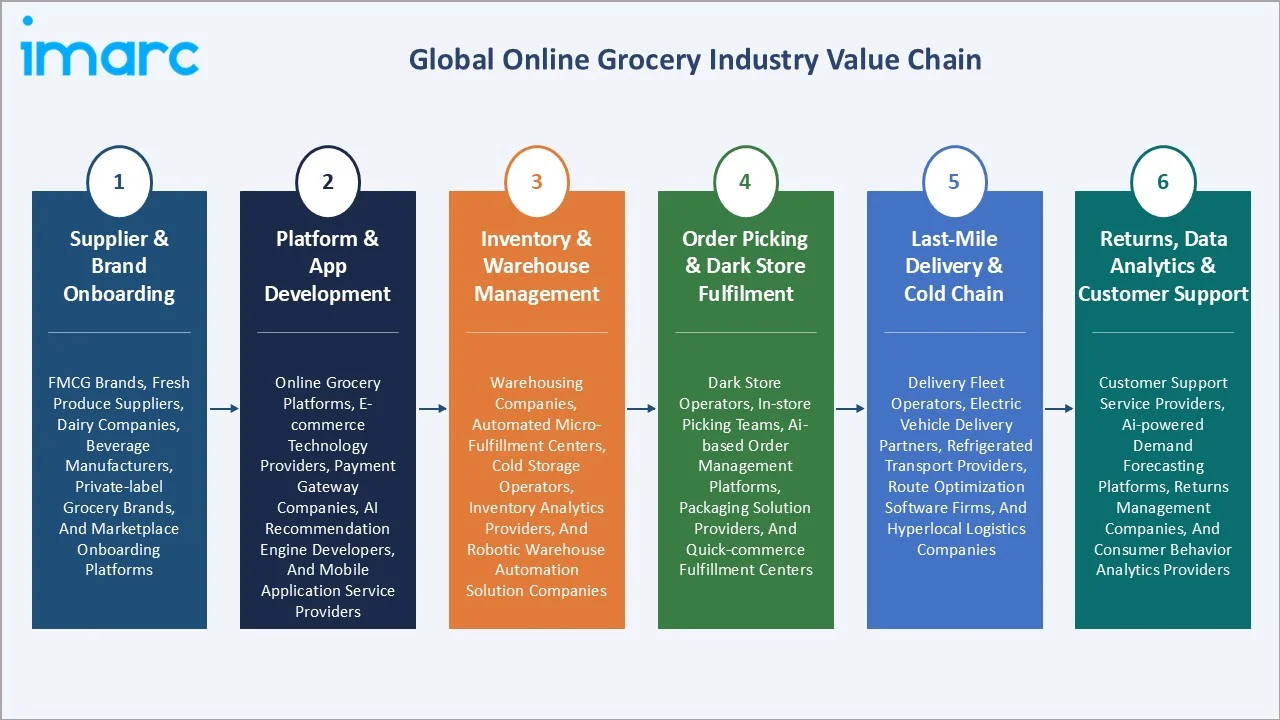

Industry Value Chain Analysis

The global online grocery value chain integrates supplier and brand onboarding, platform and app development, inventory and warehouse management, order picking and dark store fulfilment, last-mile delivery and cold chain, and returns management with CRM and data analytics.

|

Stage |

Key Participants |

|

Supplier & Brand Onboarding |

FMCG brands, fresh produce suppliers, dairy companies, beverage manufacturers, private-label grocery brands, and marketplace onboarding platforms. |

|

Platform & App Development |

Online grocery platforms, e-commerce technology providers, payment gateway companies, AI recommendation engine developers, and mobile application service providers. |

|

Inventory & Warehouse Management |

Warehousing companies, automated micro-fulfillment centers, cold storage operators, inventory analytics providers, and robotic warehouse automation solution companies. |

|

Order Picking & Dark Store Fulfilment |

Dark store operators, in-store picking teams, AI-based order management platforms, packaging solution providers, and quick-commerce fulfillment centers. |

|

Last-Mile Delivery & Cold Chain |

Delivery fleet operators, electric vehicle delivery partners, refrigerated transport providers, route optimization software firms, and hyperlocal logistics companies. |

|

Returns, Data Analytics & Customer Support |

Customer support service providers, AI-powered demand forecasting platforms, returns management companies, and consumer behavior analytics providers. |

The returns, CRM, and data analytics tier has become increasingly commercially valuable as online grocery platforms recognize that first-party grocery purchase data is among the most commercially valuable consumer data available. This data monetization opportunity is progressively transforming online grocery platforms from thin-margin grocery retailers to high-margin data and advertising businesses where grocery revenue partially subsidizes the data asset creation.

Technology Landscape in the Online Grocery Industry

Automated Micro-Fulfilment and Robotic Picking

Automated micro-fulfillment and robotic picking technologies are enabling faster order processing, higher picking accuracy, and improved warehouse efficiency. Retailers are increasingly deploying AI-driven robotics, automated storage systems, and smart inventory management solutions to support rapid grocery fulfillment and quick-commerce operations. These technologies help reduce labor dependency, lower operational costs, and improve delivery speed for high-frequency online grocery orders. Growing demand for same-day and ultra-fast grocery delivery is further accelerating the adoption of automated fulfillment infrastructure.

AI Demand Forecasting and Inventory Optimization

AI demand forecasting and inventory optimization are enabling retailers to predict consumer purchasing patterns and manage stock levels more efficiently. Advanced AI algorithms analyze historical sales, seasonal trends, weather conditions, and customer behavior to reduce stockouts, minimize food waste, and improve inventory turnover. In November 2025, Instacart introduced Instacart AI Solutions, a new enterprise-focused platform designed to help grocery retailers strengthen competitiveness in an AI-driven retail environment. These capabilities help retailers improve inventory forecasting, reduce operational inefficiencies, and enhance customer shopping experiences across online and physical stores.

Last-Mile Delivery Technology and Route Optimization

Last-mile delivery technology and route optimization enable faster, more efficient, and cost-effective order deliveries. Companies are increasingly using AI-powered route planning, GPS tracking, predictive traffic analytics, and dynamic dispatch systems to reduce delivery times and improve fleet utilization. These technologies help optimize fuel consumption, enhance cold-chain reliability for perishable products, and improve customer satisfaction through accurate delivery tracking. Growing demand for same-day and ultra-fast grocery delivery is further accelerating investments in smart logistics technologies.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Business Model |

Pure Marketplace |

46.8% |

2025 |

|

Platform |

🔒 |

🔒 |

2025 |

|

Purchase Type |

Subscription |

58.0% |

2025 |

|

Region |

Asia Pacific |

58.3% |

2025 |

By Business Model

Pure marketplace leads at 46.8% market share (2025). Pure marketplace platforms operate as digital intermediaries connecting grocery suppliers and brands directly to consumers without owning physical grocery stores as primary assets. Pure marketplace's commercial model advantages: near-zero incremental cost to add grocery category to existing consumer base, massive scale economics from shared logistics infrastructure, advertising monetization of product placement, and supplier/brand competition lowering prices for consumers while sustaining platform economics through fee structures.

To access detailed market analysis, Request Sample

The hybrid marketplace at 34.2% represents physical grocery retailers building digital channels alongside physical stores. Others at 19.0% includes pure-play online grocery retailers with proprietary fulfilment, Q-commerce dark store operators, meal kit subscription services, and social commerce grocery models.

By Purchase Type

Subscription leads at 58.0% market share (2025). Subscription encompasses Amazon Prime grocery benefits, Walmart, BigBasket Daily, and Chinese platforms' member-exclusive pricing and delivery programs. Subscription's commercial case is unambiguous: subscribers have 3-4x higher annual spend, 60% lower churn rate, and 40% lower cost of retention versus non-subscribers across all major online grocery platforms.

One-time purchase at 42.0% represents single transaction grocery purchases without an ongoing membership commitment. One-time purchase is the acquisition channel through which consumers first experience online grocery before converting to a subscription, making one-time purchase a commercial investment, a subscriber acquisition cost embedded in the one-time purchase revenue category.

Regional Market Insights

|

Region |

Share (2025) |

Key Online Grocery Market Drivers & Characteristics |

|

Asia Pacific |

58.3% |

Driven by high smartphone penetration, rapid urbanization, strong quick-commerce adoption, and expanding digital payment ecosystems. |

|

North America |

16.7% |

Characterized by advanced e-commerce infrastructure, widespread subscription-based grocery delivery services, and strong investments in AI-driven fulfillment and last-mile delivery technologies. |

|

Europe |

13.5% |

Driven by growing consumer demand for convenience, strong adoption of automated warehouse technologies, and increasing focus on sustainable grocery delivery and cold-chain logistics solutions. |

|

Latin America |

6.4% |

Expanding steadily due to rising internet accessibility, increasing smartphone usage, and growing investments in hyperlocal delivery and digital retail platforms across urban areas. |

|

Middle East and Africa |

5.1% |

Witnessing rapid growth supported by rising digital commerce adoption, expanding quick-commerce platforms, improving logistics infrastructure, and a young tech-savvy consumer population. |

Asia Pacific's 58.3% dominance is structurally driven by China's online grocery economy, representing the world's most advanced grocery digitization experiment at scale, combined with India's fastest-growing online grocery market, and Southeast Asia's rapidly digitizing grocery commerce. The region's multi-billion-consumer scale, mobile-first commerce behavior, and dense urban geography collectively create online grocery market dynamics that North America and Europe cannot replicate at equivalent growth velocity.

North America, at 16.7%, is defined by Amazon Prime's grocery integration, Walmart's omnichannel scale, and Kroger's data-driven digital grocery as the three dominant competitive forces. Europe, at 13.5%, features Ocado's global platform technology leadership, the UK's highest online grocery penetration in the Western world, and Q-commerce's rapid adoption in major European cities. Latin America, at 6.4%, is growing through super-app grocery and marketplace expansion. The Middle East and Africa, at 5.1%, is the fastest-growing region with GCC tech adoption and Africa's mobile-money-enabled grocery commerce is emerging.

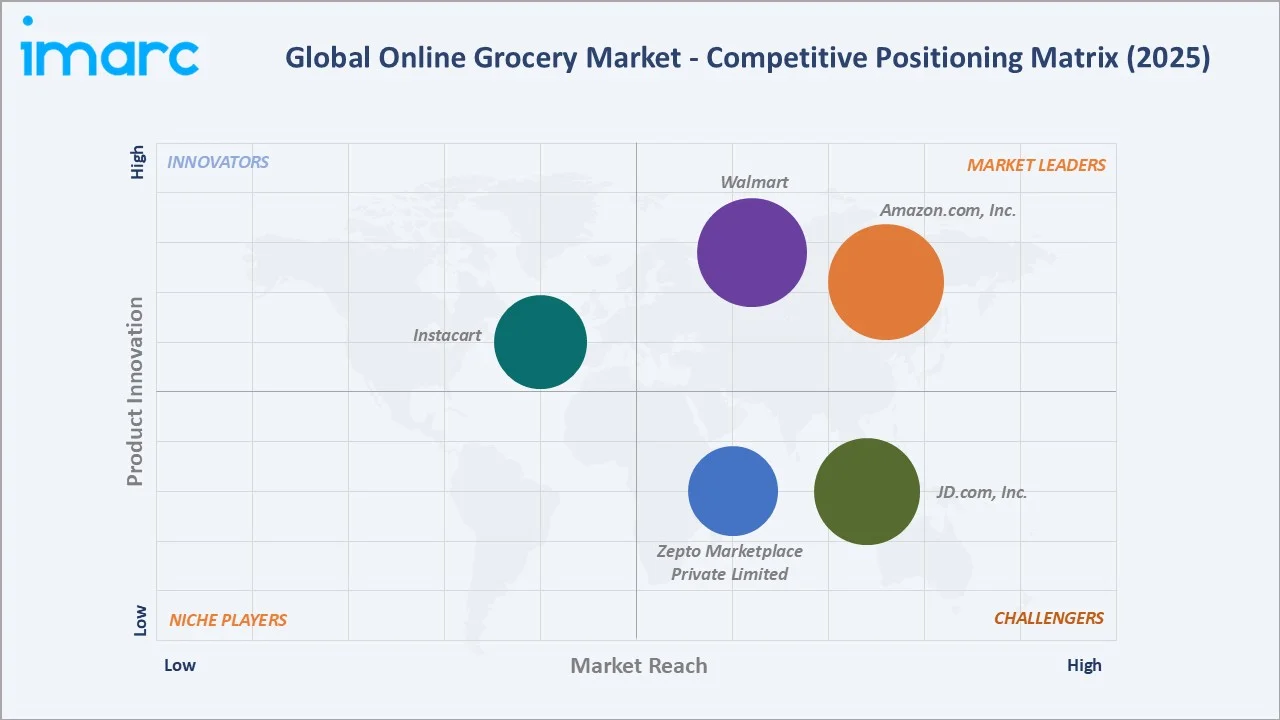

Competitive Landscape

The global online grocery competitive landscape features a distinctive three-tier structure: global mega-platforms leveraging existing multi-billion-consumer ecosystems for grocery expansion; regional grocery technology leaders with specialized grocery platforms or operational capabilities; and market-specific specialists serving specific countries or regional markets with locally-optimized models.

|

Company Name |

Delivery Platform |

Market Position |

Core Strength |

|

Amazon.com, Inc. |

Amazon Fresh, Amazon Now |

Market Leader |

Amazon offers an extensive online grocery service, primarily through Amazon Fresh. |

|

JD.com, Inc. |

JD Retail, JD Now |

Strong Challenger |

JD.com, also known as JINGDONG, is a leading supply chain-based technology and service provider. |

|

Walmart |

Walmart, Walmart+, Walmart InHome |

Market Leader |

Walmart is a people-led, tech-powered omnichannel retailer dedicated to helping people save money and live better. |

|

Instacart |

Instacart |

Established Player |

A decade ago, Instacart introduced a new model for online grocery shopping and convenient home delivery. |

|

Zepto Marketplace Private Limited |

Zepto |

Challenger |

Zepto is strengthening its online grocery position through ultra-fast delivery and AI-enabled quick-commerce logistics. |

The competitive landscape's defining dynamic of 2024-2026 is the profitability reckoning; the era of unlimited venture capital funding for market share acquisition, regardless of unit economics, is ending, and online grocery platforms are consolidating and rationalizing geographic presence to focus on profitable markets at density. The survivors of this consolidation phase will have materially stronger competitive positions as the reduced competitive field increases per-market pricing power and reduces customer acquisition spending arms races.

Key Company Profiles

Amazon.com, Inc.

Amazon is the world's most commercially significant online grocery operator, leveraging its global membership base, cloud infrastructure, and fulfilment network to build the grocery category's most integrated digital-physical ecosystem.

- Delivery Platform: Amazon Fresh, Amazon Now.

- Recent Developments: In March 2026, Amazon launched its Amazon Now service in Brazil, introducing 15-minute delivery for groceries and essential products.

- Strategic Focus: Focused on expanding ultra-fast grocery delivery, AI-driven fulfillment capabilities, and subscription-based convenience services to strengthen its position in the online grocery market.

Walmart

Walmart is the world's largest grocery retailer, operating with high annual grocery revenue across its operations, with an accelerating digital grocery transformation that represents the world's most commercially consequential online grocery growth story.

- Delivery Platform: Walmart.

- Recent Developments: In December 2025, Walmart partnered with Pinterest to pilot a shoppable recipe feature that enables consumers to convert food inspiration content into grocery shopping lists. The integration allows users to add recipe ingredients directly to their Walmart online cart, view live pricing, substitute products, and choose preferred pickup or delivery locations through the Walmart app or website.

- Strategic Focus: Focused on strengthening its omnichannel grocery ecosystem through AI-enabled shopping experiences, rapid fulfillment services, and integrated pickup and delivery solutions.

Market Concentration Analysis

The global online grocery market is highly concentrated at the regional level and moderately concentrated at the global level. China alone represents approximately 45-50% of the global online grocery market, with JD.com and other regional players collectively holding 70-75% of the Chinese online grocery market share. Within the US market, Amazon Fresh, Walmart Grocery, and Instacart collectively represent approximately 75-80% of US online grocery GMV. This high regional concentration within relatively open national markets reflects the winner-takes-most dynamics of marketplace platforms combined with the logistics density economics of grocery delivery.

Global market concentration is more fragmented due to the region-specific nature of grocery retail. No single global online grocery company approaches the 20% global market share that global tech leaders in other categories achieve, reflecting both grocery's inherently local supply chain and the regulatory and cultural barriers to international grocery expansion.

Investment & Growth Opportunities

Highest Growth Segments

Pure marketplace model (~26.5% CAGR), subscription purchase type (~26.2% CAGR), Q-commerce dark store operations (30-40% CAGR for the sub-30-minute delivery sub-segment), AI grocery personalization technology (~40-50% CAGR for AI-enabled grocery recommendation and demand forecasting tools), and retail media advertising revenue from FMCG brands targeting online grocery shoppers (20-25% CAGR from high base) represent the global online grocery market's highest-growth investment vectors through 2034.

Emerging Investment Opportunities

The B2B institutional online grocery market represents an underleveraged opportunity that online grocery platforms have largely ignored in favor of a B2C consumer focus. An institution-focused online grocery platform providing consolidated ordering, spend analytics, dietary requirement management, and automated replenishment for cafeterias of daily meals could achieve USD 1-5 Million annual contract value per institutional client with multi-year switching costs that create durable recurring revenue.

Investment Themes

- Dark store network expansion in tier-2 and tier-3 cities for Q-commerce penetration: Each dark store in a tier-2 Indian, Southeast Asian, or Latin American city requires USD 0.5-1.5 Million initial capex (fit-out, refrigeration, technology, initial inventory) and achieves payback at 1,500-2,000 daily orders.

- Retail media advertising platform development for online grocery: Online grocery advertising is the fastest-growing digital advertising segment globally because grocery purchase data is the most comprehensive consumer behavioral dataset available, and advertising at the point of grocery purchase intent achieves purchase attribution rates of 25-40% versus 0.5-2% for typical display advertising.

Future Market Outlook (2026-2034)

The global online grocery market is projected to grow from USD 909.6 Billion in 2025 to USD 7,644.8 Billion by 2034, delivering a 25.88% CAGR over the forecast period. The market's anchor value of USD 2,875.4 Billion in 2030 represents a global online grocery industry where online grocery penetration of total grocery retail has grown. Three structural forces define global online grocery market growth through 2034 with high confidence. Consumer habit formation permanence: the consumers who adopted online grocery through 2020-2025 will each compound their online grocery spend as follows: trust in fresh produce quality improves through AI freshness assurance; convenience benefits deepen through AI personalization eliminating browse-and-select friction; and subscription loyalty reduces switching cost annually.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Head of E-Commerce; VP of Product Management; dark store operations directors; digital grocery strategy directors; fresh produce supply chain managers; and consumer behavior research leaders.

Secondary Research

Secondary research encompassed Global Online Retailing 2025 database; Nielsen IQ Connected Commerce Survey 2025; Amazon 10-K annual report; JD.com Annual Report; Instacart annual report; McKinsey Global Institute Digital India Report 2024; KPMG China Online Grocery Market Analysis 2025; BCG Retail Media Advertising Market Sizing 2024; Logistics annual reports. Over 75 secondary sources reviewed.

Forecasting Models

Market GMV forecasts were developed using top-down regional grocery retail market size multiplied by regional online grocery penetration rate forecasts calibrated against historical penetration curves. Bottom-up models by business model type. Key inputs include smartphone penetration and mobile payment adoption by country, urbanization rates, income elasticity of online grocery adoption, cold chain logistics infrastructure availability, regulatory food delivery framework, and competitive dynamics by region.

Online Grocery Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Vegetables and Fruits, Dairy Products, Staples and Cooking Essentials, Snacks, Meat and Seafood, Others |

| Business Models Covered | Pure Marketplace, Hybrid Marketplace, Others |

| Platforms Covered | App-based, Web-based |

| Purchase Types Covered | One-time, Subscription |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amazon.com, Inc., JD.com, Inc., Walmart, Instacart, Zepto Marketplace Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the online grocery market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global online grocery market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the online grocery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Online Grocery Market Report

The global online grocery market reached USD 909.6 Billion in 2025, driven by COVID-19's permanent behavioral shift to digital grocery shopping among online grocery users globally, Q-commerce dark store expansion enabling 10-30 minute delivery in major cities, AI-personalized grocery recommendation increasing conversion and basket size, subscription loyalty programs sustaining repeat purchase frequency, and Asia Pacific's extraordinary scale from China's online grocery economy.

The market grows at 25.88% CAGR during 2026-2034, reaching USD 7,644.8 Billion by 2034, among the highest CAGRs of any major consumer market globally. The exceptional CAGR reflects the compound of structural digitization, COVID-driven installed user base, Q-commerce service quality improvements driving urban household adoption acceleration, and Asia Pacific's billion-consumer scale markets growing at above-average rates.

Pure marketplace leads at 46.8% through Amazon, JD.com, and others, leveraging existing massive consumer ecosystems for grocery expansion at near-zero incremental customer acquisition cost. Pure Marketplace also grows fastest at ~26.5% CAGR as mega-platform network effects compound.

Subscription leads at 58.0% as grocery's inherent weekly repurchase frequency aligns naturally with subscription economics. Subscription customers spend 3-4x more annually, churn 60% less frequently, and cost 40% less to retain versus one-time purchase customers across Amazon Prime, Instacart, Walmart, and others. Subscription also grows fastest at ~26.2% CAGR as online grocery platforms universally prioritize subscription conversion as their highest-LTV commercial strategy.

Asia Pacific leads at 58.3% through China's online grocery economy, India's 35-40% annual growth, and Southeast Asia's grocery expansion. Asia Pacific's dominance reflects mobile-first consumer behavior, dense urban delivery economics, and high addressable consumers.

Leading companies include Amazon.com, Inc., JD.com, Inc., Walmart, Instacart, and Zepto Marketplace Private Limited, among others.

The market is projected to reach approximately USD 2,875.4 Billion by 2030, representing online grocery penetration growth. Q-commerce achieves mainstream status in tier-1 cities globally, Amazon/Walmart each build USD 1 Trillion+ total grocery businesses, and top scaled platforms achieve EBITDA positive operations through advertising revenue, private label margin, and subscription efficiency improvements.

Q-commerce (Quick commerce) refers to grocery and convenience delivery completed within 10-30 minutes using hyperlocal dark store networks positioned within 1-2 km of the consumer. Q-commerce transforms online grocery from a planned weekly shop to an on-demand impulse utility, capturing forgetting occasions, recipe last-minute needs, and convenience occasions that physical stores historically captured exclusively, fundamentally expanding online grocery's total addressable basket capture.

COVID-19 created the largest single behavioral adoption event in digital commerce history, and global lockdowns forced consumers to try online grocery shopping for the first time.

Three priority opportunities: dark store network expansion for Q-commerce in tier-2 cities; retail media advertising platform development for online grocery platforms with active users; and AI predictive grocery replenishment technology creating user experience differentiation and basket size improvement that sustains platform loyalty in the competitive consumer-choice environment of mature online grocery markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)