Online Travel Market Size, Share, Trends and Forecast by Service Type, Platform, Mode of Booking, Age Group, and Region, 2026-2034

Global Online Travel Market Size, Share, Trends & Forecast (2026-2034)

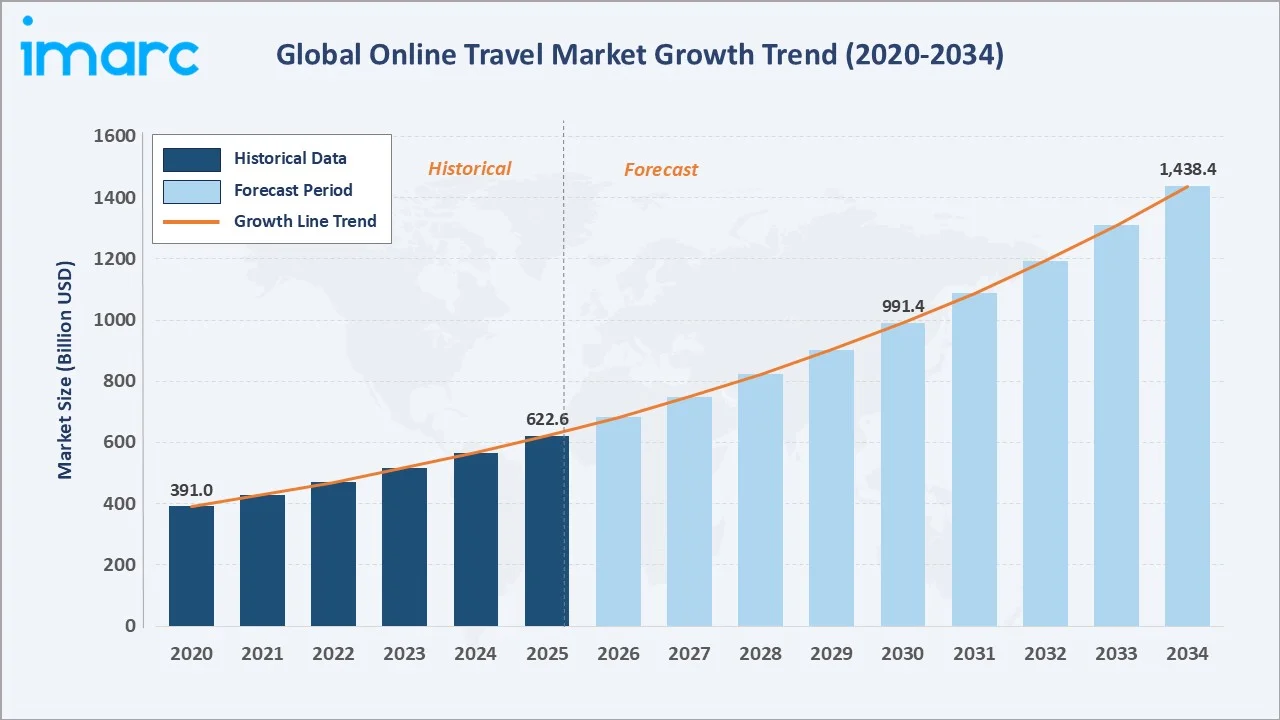

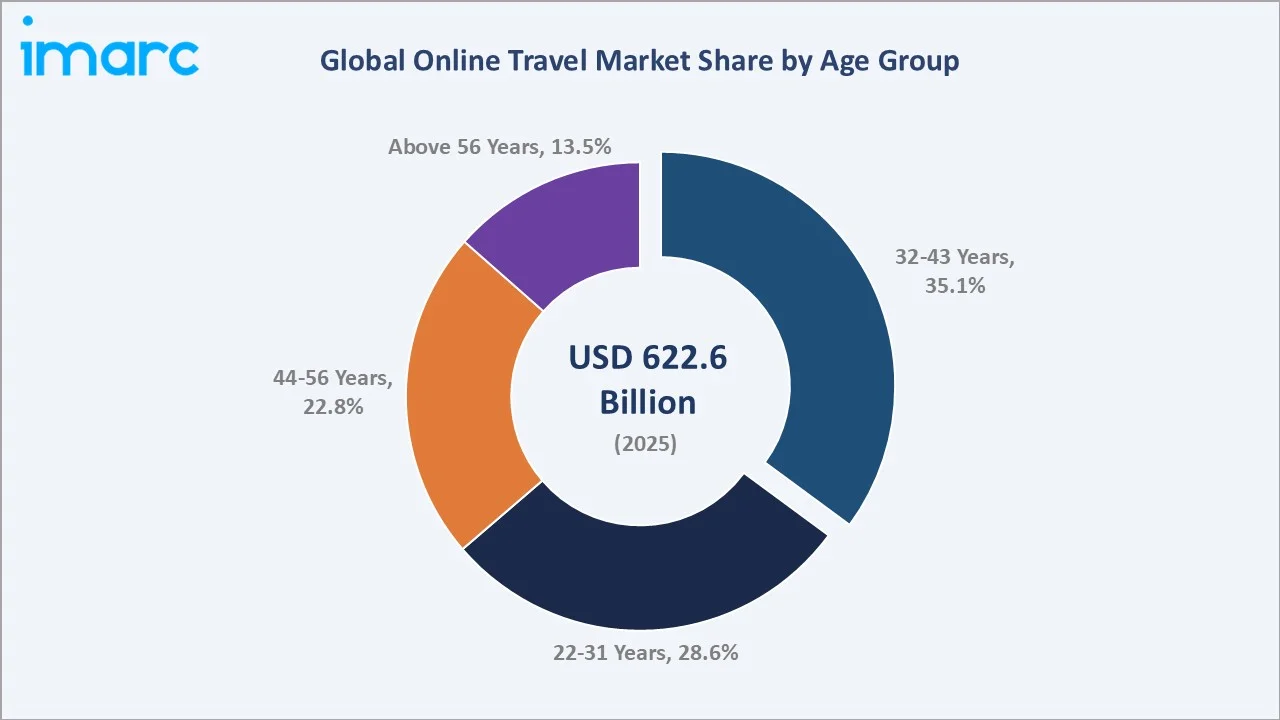

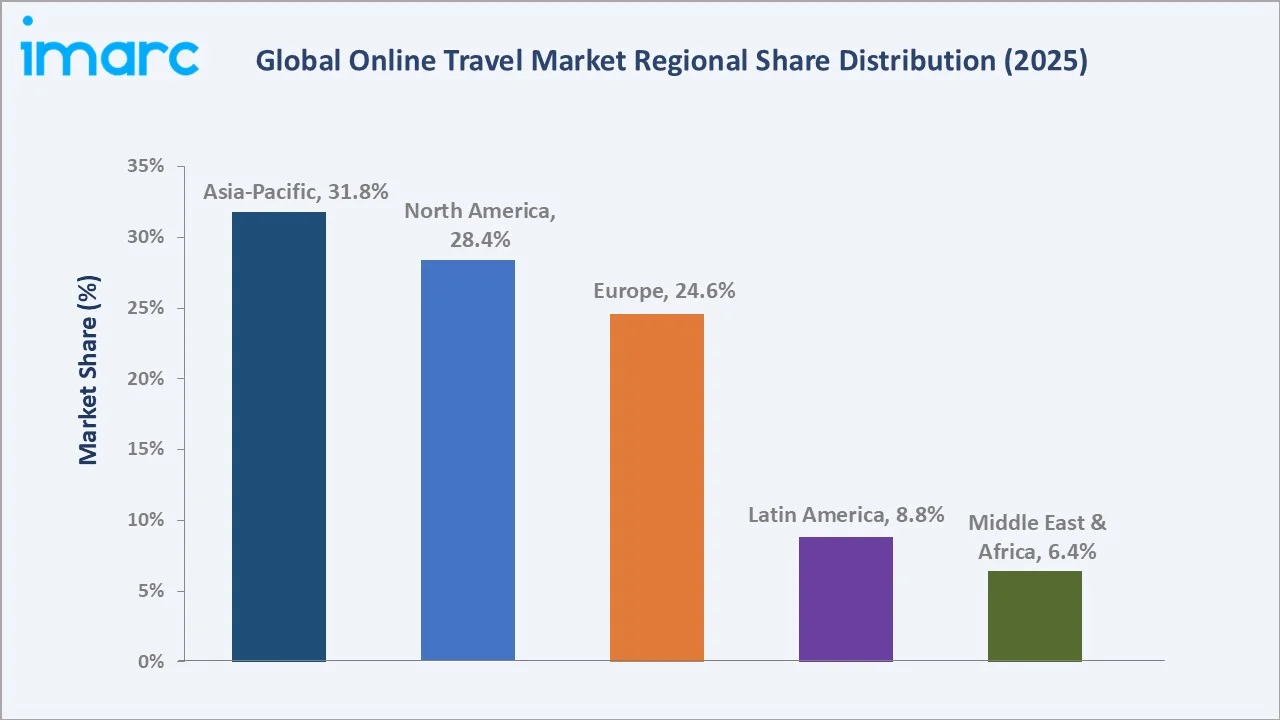

The global online travel market size was valued at USD 622.6 Billion in 2025 and is projected to reach USD 1,438.4 Billion by 2034, exhibiting a CAGR of 9.75% during the forecast period 2026-2034. Rising internet penetration, mobile app adoption, and AI-driven personalization are the primary growth engines. The 32-43 years age group leads with a 35.1% market share in 2025, while Desktop platforms command 67.3% of bookings. Asia-Pacific dominates regionally at 31.8%, driven by China, India, and Japan, followed by North America at 28.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 622.6 Billion |

|

Forecast Market Size (2034) |

USD 1,438.4 Billion |

|

CAGR (2026-2034) |

9.75% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (31.8% share, 2025) |

|

Fastest Growing Platform |

Mobile (CAGR ~13.5%) |

|

Leading Age Group |

32-43 Years (35.1%, 2025) |

|

Leading Platform |

Desktop (67.3%, 2025) |

The online travel market growth trajectory from 2020 through 2034 contrasts a consistent historical expansion base against a sustained forecast curve powered by digital adoption, AI integration, and rising global travel aspirations.

To get more information on this market, Request Sample

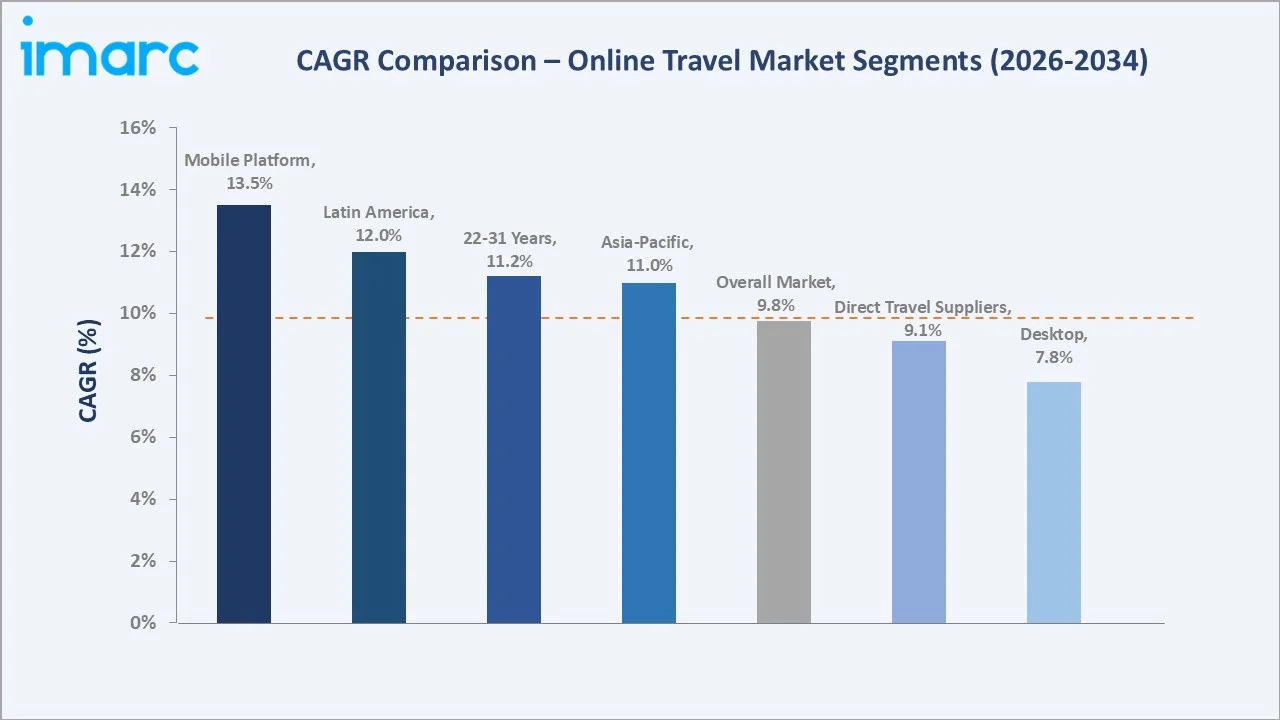

Segment-level CAGR comparisons highlighting Mobile platform and the 22-31 years age group as the two fastest-growing sub-categories within the global online travel industry through 2034.

Executive Summary

The global online travel market is undergoing a structural transformation fueled by the convergence of digital technologies, shifting consumer behavior, and rising global travel aspirations. Valued at USD 622.6 Billion in 2025, the market is forecast to reach USD 1,438.4 Billion by 2034 at a CAGR of 9.75%.

The 32-43 years age group commands 35.1% of market revenue in 2025, reflecting the dominance of high-income, digitally sophisticated consumers who drive both volume and premium booking value. Desktop platforms lead with 67.3% share, though Mobile is the fastest-growing channel, particularly across Asia-Pacific and Latin America. Direct Travel Suppliers hold 53.7% of the mode-of-booking share in 2025, while OTAs continue to grow through aggressive AI personalization and loyalty program investments.

Asia-Pacific leads regionally at 31.8%, driven by China's outbound travel rebound, India's expanding digital infrastructure, and Japan's technology-dense tourism ecosystem. North America follows at 28.4%, underpinned by high consumer digital maturity and the United States' dominant position, representing 86.30% of North American market revenue. Europe, at 24.6%, is increasingly influenced by sustainable travel preferences and rail-based alternatives to short-haul aviation.

Key Market Insights

|

Insight |

Data |

|

Largest Age Group |

32-43 Years – 35.1% share (2025) |

|

Leading Platform |

Desktop – 67.3% share (2025) |

|

Leading Region |

Asia-Pacific – 31.8% revenue share (2025) |

|

Second Region |

North America – 28.4% revenue share (2025) |

|

Fastest Growing Platform |

Mobile – ~13.5% CAGR (2026-2034) |

|

Top Companies |

Booking Holdings Inc., Expedia Group Inc., Airbnb Inc., Trip.com Group Limited, MakeMyTrip Pvt. Ltd. |

Key Analytical Observations Supporting The Above Data:

- 32-43 Years' 35.1% dominance reflects high disposable income, strong digital literacy, and active engagement with premium travel products and loyalty programs across OTA and direct booking platforms.

- Desktop's 67.3% share in 2025 is driven by the preference for desktop interfaces when managing high-value, complex, multi-destination bookings and corporate travel arrangements.

- Asia-Pacific's 31.8% global dominance reflects China's post-reopening outbound travel surge, India's 650+ million smartphone users, and the proliferation of mobile-first super-app travel ecosystems.

- Mobile platform CAGR of ~13.5% through 2034 is the highest sub-segment growth rate, driven by app-exclusive deals, integrated digital wallets, and AI-powered on-the-go booking capabilities.

- Direct Travel Suppliers' 53.7% mode-of-booking share reflects travelers' preference for personalized loyalty benefits, direct pricing control, and exclusive package customization unavailable via OTAs.

- Over 80% of global travelers completed bookings entirely online in 2025, signaling the near-complete digital transformation of the travel purchase journey.

Global Online Travel Market Overview

Online travel refers to the end-to-end planning, discovery, and booking of travel services—including flights, hotels, vacation packages, car rentals, and experiences—via digital platforms such as OTA websites, mobile applications, direct supplier portals, and emerging AI-powered booking agents. The ecosystem encompasses individual leisure travelers, corporate travel managers, travel agencies, and group planners.

Macroeconomic enablers include rising global internet penetration, rapid smartphone adoption, expanding digital payment infrastructure, and the surging disposable income of emerging market middle classes, particularly across Asia-Pacific and Latin America.

Market Dynamics

To evaluate market opportunities, Request Sample

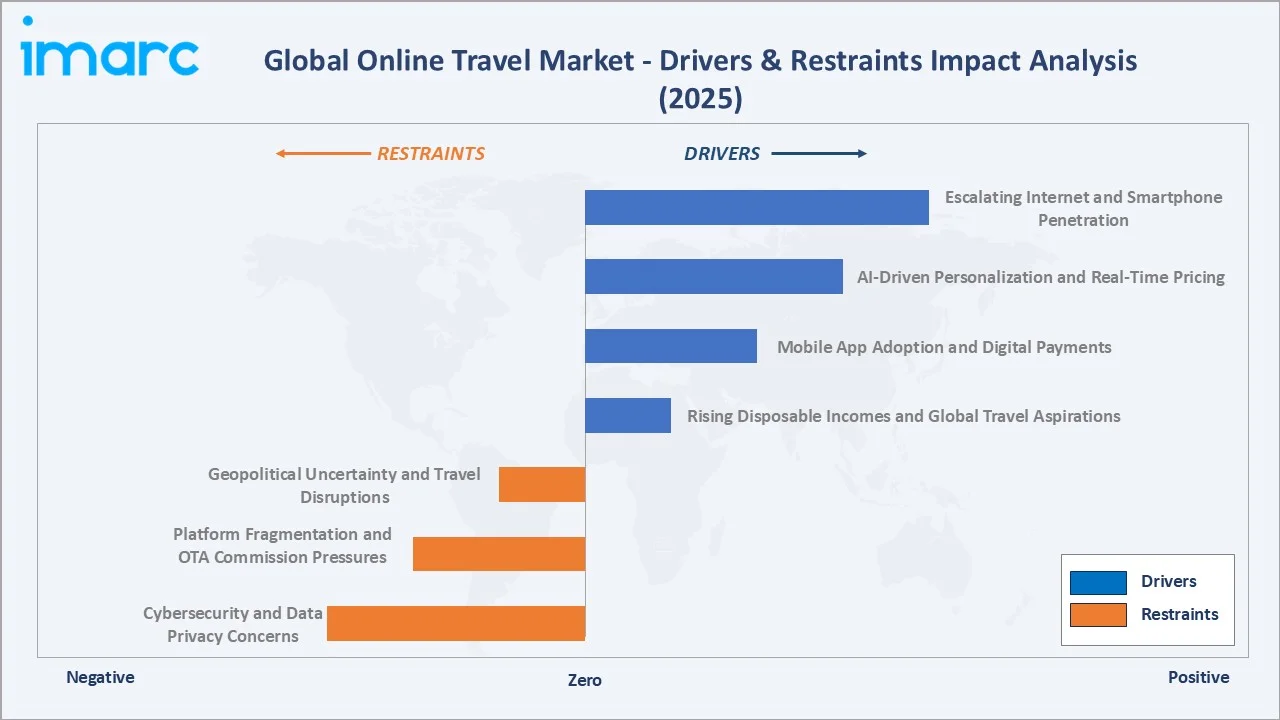

Market Drivers

- Escalating Internet and Smartphone Penetration: As of 2024, 5.5 billion people globally use the internet, representing 68% of the world population. This expanding connectivity is the foundational enabler of online travel booking growth, particularly in Asia-Pacific and Latin America, where first-time digital users are rapidly converting to online travel consumers.

- AI-Driven Personalization and Real-Time Pricing: Generative AI tools, machine learning-based recommendation engines, and intelligent chatbots are enabling platforms to deliver hyper-personalized itineraries, dynamic pricing, and real-time availability—dramatically improving conversion rates and average booking values.

- Mobile App Adoption and Digital Payments: Mobile bookings accounted for 63% of all online reservations in 2025. The integration of digital wallets, UPI systems, and buy-now-pay-later options has lowered booking friction significantly, particularly in markets with historically low credit card penetration.

- Rising Disposable Incomes and Global Travel Aspirations: Growing middle-class populations across China, India, Brazil, and Southeast Asia are driving first-time international travel demand, with platforms responding through localized language support, regional payment options, and culturally tailored recommendations.

Market Restraints

- Cybersecurity and Data Privacy Concerns: 41% of consumers express hesitation about booking travel online due to data security concerns, particularly regarding payment data and personal identification information managed by OTA platforms.

- Platform Fragmentation and OTA Commission Pressures: Independent hotels and smaller travel operators face unsustainable OTA commission rates of 15-25%, creating friction in the ecosystem and driving investment in direct booking alternatives that may reduce OTA growth over the long term.

- Geopolitical Uncertainty and Travel Disruptions: Visa policy changes, geopolitical tensions, and macroeconomic headwinds can rapidly suppress travel demand and booking volumes, creating revenue volatility for online travel platforms.

Market Opportunities

- Agentic AI and Autonomous Travel Booking: A quarter to a third of global travelers in 2025 expressed interest in allowing AI agents to book travel on their behalf. OTAs that develop robust autonomous booking capabilities stand to capture significant incremental revenue from time-constrained professional travelers.

- Emerging Market Expansion in LATAM, MEA: Latin America's 74% online booking penetration among travelers and the growing Online Travel Market in Latin America, along with MEA's rapidly expanding digital infrastructure, represent structurally underpenetrated markets with high growth ceilings for OTA expansion and mobile-first platform investments.

- Sustainable and Experiential Travel Products: 70% of travelers in 2025 expressed willingness to pay a premium for sustainable travel experiences, creating opportunities for platforms to differentiate through eco-certified inventories, carbon offset tools, and curated local experience offerings.

Market Challenges

- Intensifying Competition from Tech Giants: Google Travel, Meta, and emerging AI-native travel platforms represent existential competitive threats to traditional OTAs by controlling the top of the search and discovery funnel, potentially disintermediating established players.

- Consumer Loyalty Fragmentation: With 45% of travelers wanting to book entire trips on a single platform, OTAs face the challenge of building genuinely unified travel management ecosystems across flights, hotels, experiences, and ground transport—a technically complex and capital-intensive undertaking.

Emerging Market Trends

1. Agentic AI Transforming the Booking Paradigm

AI platforms are evolving from recommendation tools to autonomous travel agents capable of end-to-end trip planning, negotiation, and booking. By the second half of 2025, generative AI platforms surged from 6% to 15% of travel research tool usage, while traditional search engines declined from 51% to 36% as the primary research channel. OTAs are racing to embed agentic capabilities before tech giants establish dominance in AI-powered travel.

2. Sustainable Travel as a Core Booking Criterion

Sustainability has shifted from a niche preference to a mainstream booking criterion. Over half of global travelers now actively consider environmental impact when booking, and 46% of corporate travel managers had sustainability budget strategies in place by 2024. Rail.

3. Mobile-First and Super-App Ecosystem Integration

Mobile booking platforms are evolving beyond simple flight and hotel search into comprehensive travel management super-apps integrating payments, loyalty, visa assistance, travel insurance, and in-destination services.

4. Experiential and Event-Driven Travel Surge

Travelers are increasingly booking around experiences and events rather than destinations. In 2026, 57% of all travelers plan to book around sporting events, with 65% of top-searched travel dates aligning with global events such as the FIFA World Cup and cultural festivals. Platforms are responding through partnerships with event organizers and real-time inventory integration.

5. Social Media-Influenced Destination Discovery

Over 80% of travelers in 2025 used social media platforms to research destinations and share experiences, with social network usage for trip research rising from 16% in 2023 to 19% in 2025 in the United States. Influencer-driven destination discovery is compressing booking windows and driving demand for platform-native social discovery features.

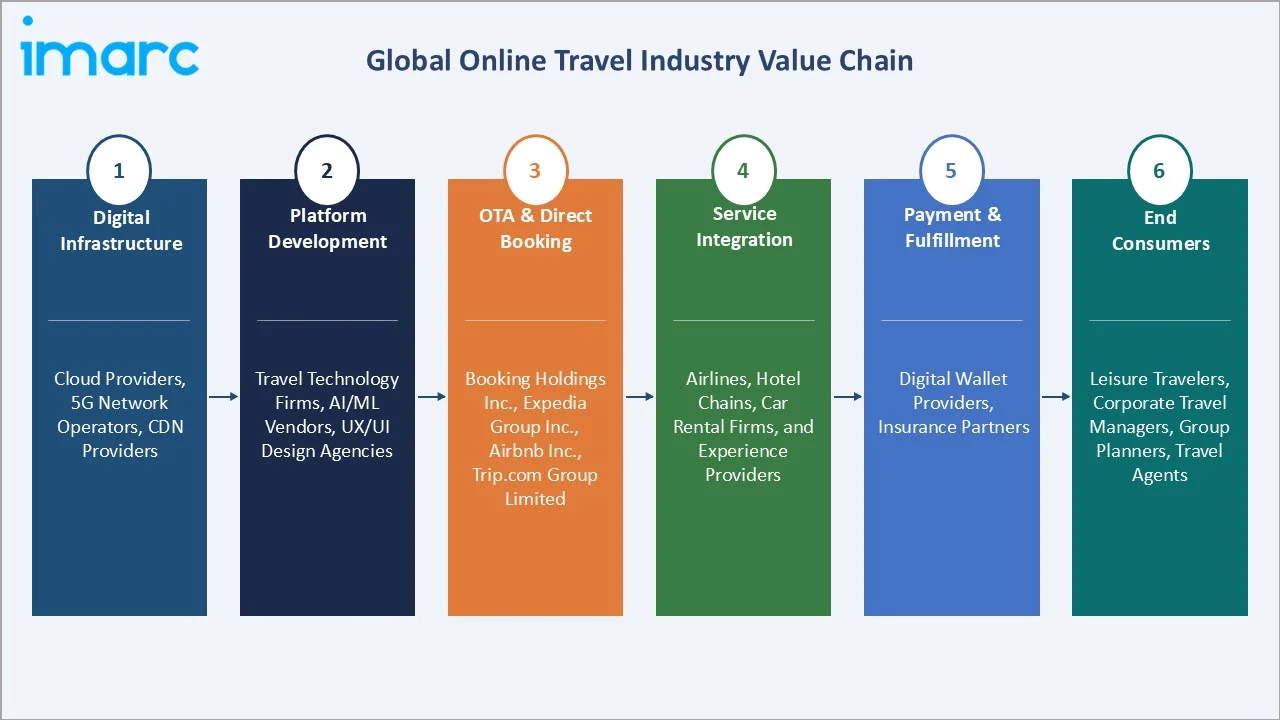

Industry Value Chain Analysis

The online travel value chain spans six integrated stages from digital infrastructure through end-consumer experience delivery, each presenting distinct competitive dynamics and innovation opportunities.

|

Stage |

Key Players / Examples |

|

Digital Infrastructure |

Cloud providers, 5G network operators, CDN providers |

|

Platform Development |

Travel technology firms, AI/ML vendors, UX/UI design agencies |

|

OTA & Direct Booking |

Booking Holdings Inc., Expedia Group Inc., Airbnb Inc., Trip.com Group Limited |

|

Service Integration |

Airlines, hotel chains, car rental firms, and experience providers |

|

Payment & Fulfillment |

Digital wallet providers, insurance partners |

|

End Consumers |

Leisure travelers, corporate travel managers, group planners, travel agents |

OTA platforms occupy the highest strategic value position in the online travel value chain, aggregating multi-supplier inventory into unified, AI-curated consumer experiences. However, direct supplier portals are steadily growing their share by offering loyalty-linked pricing, exclusive packages, and superior personalization, challenging OTA intermediaries' revenue model.

Technology Landscape in the Online Travel Industry

Artificial Intelligence and Machine Learning

AI and machine learning are now embedded across the entire online booking journey. Predictive pricing algorithms dynamically adjust fares and rates based on demand signals, browsing behavior, and competitive data. Natural language processing powers conversational chatbots and virtual travel assistants capable of handling complex multi-stop itinerary construction. Generative AI platforms are advancing toward agentic booking capabilities where AI autonomously searches, compares, and completes bookings on behalf of users, a paradigm that could fundamentally disrupt the traditional OTA search-and-click model.

Mobile Technology and Digital Payments

The integration of digital wallets (PayPal, Alipay, Google Pay, UPI), buy-now-pay-later options, and biometric authentication within travel apps has dramatically reduced booking friction, particularly in markets with low credit card penetration. App-exclusive pricing and in-app loyalty integration are further concentrating booking activity within platform ecosystems.

Data Analytics and Personalization Platforms

First-party data strategies are becoming critical competitive assets as privacy regulations tighten and third-party cookie tracking phases out. Platforms investing in proprietary behavioral data collection, CRM integration, and real-time personalization engines are demonstrating measurably higher repeat booking rates and customer lifetime values.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Service Type | Transportation | 41.4% | 2025 |

| Platform | Desktop | 67.3% | 2025 |

| Mode of Booking | Direct Travel Suppliers | 53.7% | 2025 |

| Age Group | 32–43 Years | 35.1% | 2025 |

| Region | Asia Pacific | 31.8% | 2025 |

By Age Group

The 32-43 years age group commands 35.1% of market revenue in 2025—the dominant segment, reflecting the high disposable income, strong digital literacy, and active travel engagement of this cohort. These consumers frequently blend business and leisure travel and drive disproportionately high average booking values through premium bookings and multi-destination packages.

To access detailed market analysis, Request Sample

The 22-31 years segment at 28.6% is the fastest-growing age cohort, driven by mobile-first booking habits, strong social media influence on destination choices, and rising interest in experiential and adventure travel. The 44-56 years group (22.8%) contributes strongly to premium vacation packages and luxury travel bookings, while the Above 56 years segment (13.5%) shows steady growth in wellness tourism, cruise bookings, and guided tour packages facilitated through digital platforms.

By Platform

Desktop platforms lead with 67.3% of market revenue in 2025, driven by the preference for larger screens when managing complex, high-value bookings such as multi-destination itineraries, group travel arrangements, and corporate travel management. The comprehensive interface, side-by-side comparison capabilities, and more detailed checkout flows make desktop the preferred platform for high-consideration bookings.

The Mobile platform segment at 32.7% is growing at approximately 13.5% CAGR through 2034—the highest growth rate across all segments. Mobile bookings accounted for 63% of all online reservations in 2025, underscoring that while Desktop leads in revenue value, Mobile leads in booking volume, particularly for last-minute hotel reservations, domestic flights, and activity bookings. Asia-Pacific and Latin America are the key drivers of mobile booking growth, with platforms in these regions designing mobile-native experiences that bypass desktop channels entirely.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

31.8% |

China outbound rebound, India digital expansion, mobile-first platforms, ASEAN growth |

|

North America |

28.4% |

High digital maturity, OTA innovation, US corporate travel recovery, loyalty ecosystems |

|

Europe |

24.6% |

Sustainable travel demand, rail preference, OTA diversification, and premium tourism |

|

Latin America |

8.8% |

Mobile-first adoption, rising disposables, Brazil tourism earnings record, and digital payments |

|

Middle East & Africa |

6.4% |

Intra-regional travel surge, Gulf Cooperation Council investment, and smartphone penetration |

Asia-Pacific commands a 31.8% global revenue share in 2025, the largest regional position, driven by China's post-reopening outbound travel surge with an 80% increase in outbound travel in 2024-2025, alongside India's 650+ million smartphone users and Japan's technology-dense Tier-1 travel ecosystem.

North America, with 28.4% in 2025, is anchored by the US market, where the United States accounted for 86.30% of North American online travel revenue. Europe, at 24.6%, is being reshaped by sustainable travel mandates and rail travel's 12.7% CAGR growth through 2029. Latin America at 8.8% and MEA at 6.4% sees regional travelers planning intra-regional trips in 2025.

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Booking Holdings Inc. |

Booking.com, Priceline |

Leader |

Global OTA scale, connected trip, loyalty innovation |

|

Expedia Group Inc. |

Expedia, Hotels.com, Vrbo |

Leader |

B2B partnerships, One Key loyalty, AI Comet browser |

|

Airbnb Inc. |

Airbnb |

Leader |

Short-term rentals, experiences, and platform diversification |

|

Trip.com Group Limited |

Trip.com, Skyscanner |

Leader |

Asia-Pacific dominance, AI recommendations, global expansion |

|

MakeMyTrip Pvt. Ltd. |

MakeMyTrip, GoIbibo |

Challenger |

India market leader, 200,000+ global tours and experiences |

|

TripAdvisor |

TripAdvisor, Viator |

Challenger |

Reviews ecosystem, experience bookings, OTA diversification |

|

Hostelworld Group plc |

Hostelworld |

Emerging |

Budget & social travel, youth traveler niche, mobile bookings |

The global online travel competitive landscape is dominated by a small number of platform giants commanding enormous scale, proprietary data assets, and deeply integrated loyalty ecosystems. Competition is intensifying on three key fronts: agentic AI booking capabilities, connected trip offering completeness, and mobile ecosystem depth.

Key Company Profiles

Booking Holdings Inc.

- Company Overview: Booking Holdings is the world's largest online travel agency by market capitalization, operating Booking.com, Priceline, Kayak, OpenTable, and Agoda across 40+ languages and 220+ countries.

- Product Portfolio: Hotel bookings, flights, car rentals, attractions, restaurant reservations, and the "Connected Trip" integrated platform designed to manage entire journeys across a single ecosystem.

- Recent Developments: In October 2025, Booking.com announced the launch of its first customer-facing agentic AI innovations: Smart Messenger and Auto-Reply, designed to make partner-to-guest communication faster, streamlined, and more intuitive.

- Strategic Focus: Platform ecosystem integration, AI-first personalization, loyalty program deepening, and B2B partner network expansion across hotels and airlines globally.

Expedia Group Inc.

- Company Overview: Expedia Group is the world's second-largest OTA by bookings (USD 14.37 billion revenue, 2025), operating Expedia, Hotels.com, Vrbo, and the Trivago metasearch brand across global markets.

- Product Portfolio: Hotels, flights, vacation rentals, cruises, car rentals, activities, and the "One Key" unified loyalty program linking rewards across all Expedia Group brands.

- Recent Developments: In October 2025, Expedia launched Comet, an AI-powered travel browser offering personalized itinerary suggestions and dynamic pricing insights.

- Strategic Focus: AI-native booking experiences, B2B partner distribution growth, One Key loyalty ecosystem deepening, and premium accommodation segment expansion via Vrbo.

Airbnb Inc.

- Company Overview: Airbnb is the global leader in short-term rental and experience bookings, with USD 23.06 Billion in global total assets as of 2025, operating in 220+ countries across 7+ million listings.

- Product Portfolio: Short-term home rentals, Airbnb Experiences, curated local activities, Airbnb Services, and newly launched hotel inventory partnerships in 2026.

- Recent Developments: In May 2025, Airbnb launched a redesigned app to showcase the company’s push to let travelers book services, like catering and personal training, at their home rentals.

- Strategic Focus: Platform diversification beyond stays, hotel inventory expansion, loyalty program introduction in 2026, and deepening experiential travel offerings with local host partners.

Market Concentration Analysis

The global online travel market exhibits moderate-to-high concentration at the platform level, with Booking Holdings and Expedia Group together holding approximately 65% of the global OTA market share in 2025. This concentration is reinforced by powerful network effects: larger platforms attract more suppliers and travelers, enabling superior pricing algorithms, richer personalization, and stronger brand trust.

The market is experiencing a bifurcated structural dynamic. At the premium platform tier, consolidation is occurring as AI infrastructure investment, loyalty ecosystem development, and global supplier network management require massive capital commitments that only the largest OTAs can sustain. Simultaneously, regional specialists are gaining share in high-growth markets—India (MakeMyTrip), Southeast Asia (Trip.com), and Latin America (Despegar)—by offering hyperlocalized features and pricing that incumbent global platforms struggle to replicate. This continued shift from offline to online channels structurally benefits entrenched digital platforms while creating a limited runway for offline travel agency recovery.

Investment & Growth Opportunities

Fastest-Growing Segments

Mobile platform is the highest-growth segment at approximately 13.5% CAGR through 2034, driven by smartphone proliferation across emerging markets and app-native booking experiences. The 22-31 years age group is the fastest-growing age segment, fueled by experiential travel preferences and mobile-first digital behaviors.

Emerging Market Expansion

Latin America presents the highest-potential underserved opportunity, with digital travel adoption accelerating rapidly. The growth of the Online Travel Market in Brazil is driven by rising tourism revenues, along with the country’s expanding middle class and improving mobile payment infrastructure, which continue to create favorable conditions for OTA penetration. Middle East & Africa, underpinned by Gulf Cooperation Council infrastructure investment and Saudi Vision 2030 smart mobility initiatives, represents an emerging premium travel market where digital booking adoption is accelerating.

Venture & Private Investment Trends

Institutional investor sentiment toward online travel platforms strengthened materially in 2025, with Expedia Group shares recording gains of approximately 27.2% over three months following B2B segment momentum and margin expansion. The travel technology market is expected to expand, attracting significant venture capital into AI travel agents, sustainable travel infrastructure, and mobile payment integration startups across Asia-Pacific and Latin America.

Future Market Outlook (2026-2034)

The global online travel market forecast projects steady value expansion from USD 622.6 Billion in 2025 to USD 1,438.4 Billion by 2034 at a CAGR of 9.75%—a near-tripling of market value underpinned by digital adoption deepening across emerging markets, AI-driven platform evolution, and sustained growth in global travel aspirations, particularly among younger demographics in Asia-Pacific and Latin America.

Three shifts will reshape the market through 2034: agentic AI will automate trip planning and bookings, disrupting traditional OTAs; mobile super-apps will dominate travel transactions across emerging markets; and sustainability will become a baseline requirement. By 2034, the industry will evolve into AI-driven travel lifestyle platforms, where leaders differentiate through integrated supply, personalization, loyalty ecosystems, and sustainable offerings.

Research Methodology

Primary Research

Primary research included structured interviews (2024–2025) with OTA product leaders, corporate travel managers, digital payments experts, tourism board representatives, and travel tech investors, validating market sizing, segmentation, technology adoption timelines, and competitive positioning.

Secondary Research

Secondary sources include Phocuswright Travel Forward Report (December 2025), U.S. Travel Association travel spending forecasts, Euromonitor World Market for Travel (2025), Mastercard Economics Institute Travel Trends Report (May 2025), TravelPerk online booking statistics, Grand View Research OTA market reports, company annual reports, and trade publications including Skift, Travel Weekly, and PhocusWire.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, internet penetration indices, smartphone adoption data, consumer expenditure patterns, and historical online travel market evolution. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic and geopolitical uncertainty.

Online Travel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Service Types Covered | Transportation, Travel Accommodation, Vacation Packages |

| Platforms Covered | Mobile, Desktop |

| Modes of Bookings Covered | Online Travel Agencies (OTAs), Direct Travel Suppliers |

| Age Groups Covered | 22-31 Years, 32-43 Years, 44-56 Years, Above 56 Years |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Booking Holdings Inc., Expedia Group Inc., Airbnb Inc., Trip.com Group Limited, MakeMyTrip Pvt. Ltd., TripAdvisor, Hostelworld Group plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the online travel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global online travel market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the online travel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Online Travel Market Report

The global online travel market was valued at USD 622.6 Billion in 2025.

The market is projected to reach USD 1,438.4 Billion by 2034.

The 32-43 years age group leads with 35.1% market share in 2025.

Desktop platforms lead with 67.3% revenue share in 2025.

Asia-Pacific dominates with 31.8% share in 2025.

Key drivers include escalating internet penetration, AI-driven personalization, mobile booking adoption, rising disposable incomes in emerging markets, growing experiential and luxury travel demand, and the influence of social media on destination discovery.

Leading companies include Booking Holdings Inc., Expedia Group Inc., Airbnb Inc., Trip.com Group Limited, MakeMyTrip Pvt. Ltd., TripAdvisor, Hostelworld Group plc, among others.

The mobile travel booking segment is growing at approximately 13.5% CAGR through 2034. The mobile booking market was valued at USD 228.4 Billion in 2024 and is projected to exceed USD 526.4 Billion by 2032, reflecting explosive smartphone-driven adoption.

Asia-Pacific growth is driven by China's 80% outbound travel surge in 2024-2025, India's 650+ million smartphone users, expanding 5G connectivity, digital payment infrastructure, and the proliferation of mobile-first super-app ecosystems across China, India, and Southeast Asia.

High-growth investment opportunities include agentic AI booking platforms, mobile-first OTAs in Asia-Pacific and Latin America, sustainable travel infrastructure, AI-driven personalization technology, and experience-layer travel products targeting the rapidly expanding 22-31 years traveler segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade