Paper Packaging Market Size, Share, Trends and Forecast by Product Type, Grade, Packaging Level, End Use Industry, and Region, 2026-2034

Global Paper Packaging Market Size, Share, Trends & Forecast (2026-2034)

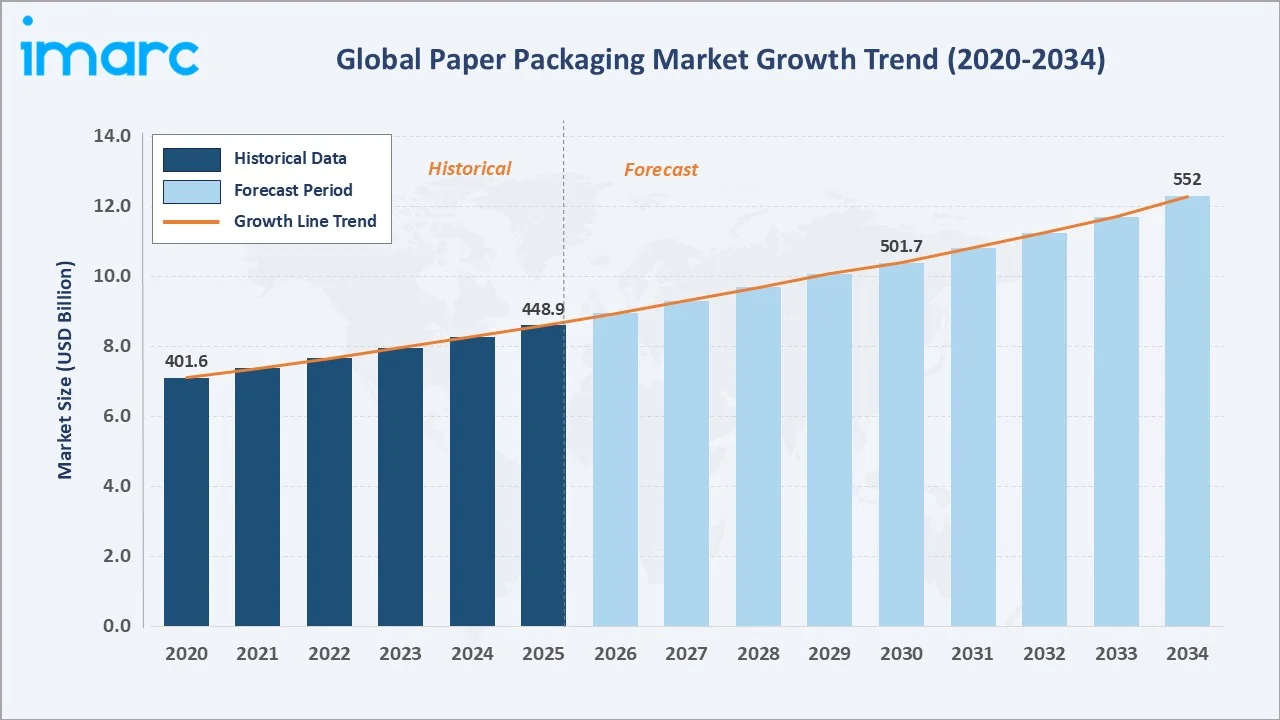

The global paper packaging market size was valued at USD 448.9 Billion in 2025 and is projected to reach USD 552.0 Billion by 2034, expanding at a CAGR of 2.25% during the forecast period 2026-2034. Market expansion is driven by growing environmental awareness, sweeping plastic ban legislation, the global e-commerce surge, and rising demand from food, beverage, and pharmaceutical end-use industries.

Market Snapshot

|

Report Attribute |

Key Statistics |

|

Market Size in 2025 |

USD 448.9 Billion |

|

Market Forecast in 2034 |

USD 552.0 Billion |

|

Market Growth Rate (2026-2034) |

2.25% |

|

Base Year |

2025 |

|

Forecast Years |

2026-2034 |

|

Largest Region (2025) |

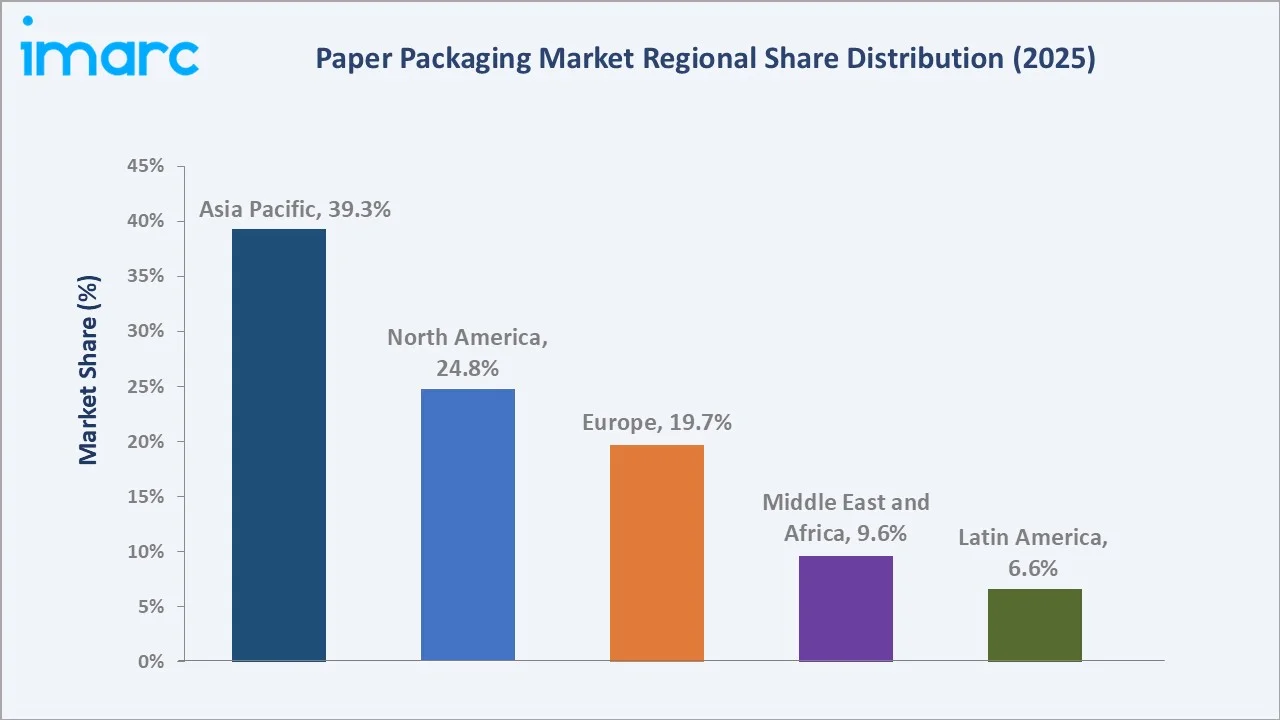

Asia Pacific - 39.3% |

|

Fastest Growing Segment |

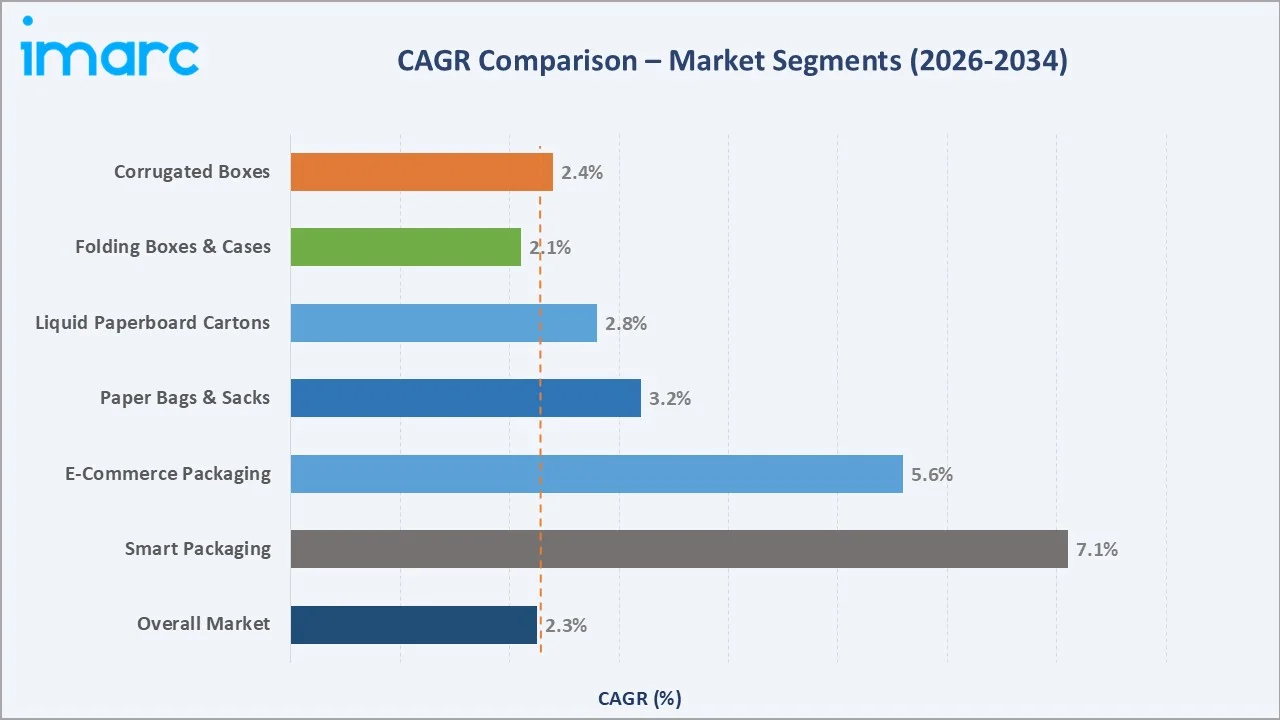

Smart & Active Packaging (CAGR ~7.1%) |

Asia Pacific dominates the market, accounting for 39.3% of global revenue in 2025, underpinned by its manufacturing base, rapid urbanization, and e-commerce ecosystem growth. Among product type, folding boxes and cases hold the leading share at 45.2%, while smart packaging and fiber-based flexible packaging are the fastest-growing categories through 2034.

To get more information on this market, Request Sample

The paper packaging market is expanding rapidly as industries shift toward biodegradable and recyclable packaging solutions amid growing environmental concerns. Rising e-commerce activity, food delivery services, and regulatory pressure on single-use plastics are further accelerating market expansion.

Executive Summary

The global paper packaging market continues to demonstrate resilient growth, underpinned by the global sustainability transition, accelerating plastic substitution, and the exponential expansion of e-commerce and packaged food industries. Valued at USD 448.9 Billion in 2025, the market is forecasted to exceed USD 552.0 Billion by 2034, growing at a CAGR of 2.25%.

Among the key growth drivers, the e-commerce sector’s exponential demand for corrugated and paper-based protective packaging remains a primary catalyst. The folding boxes and cases product type accounted for 45.2% share in 2025, with paper-based cartons, trays, and wraps becoming the preferred alternative to plastic containers.

Asia Pacific retains its market leadership with a 39.3% share in 2025, supported by China’s dominant paper manufacturing base, India’s rapidly expanding FMCG and e-commerce sectors, and Japan’s strong recycling culture. Europe is the most regulation-driven market, with the EU Packaging and Packaging Waste Regulation (PPWR) compelling rapid adoption of recyclable and renewable packaging materials.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Folding Boxes and Cases - 45.2% share (2025) |

|

Largest Segment (Grade) |

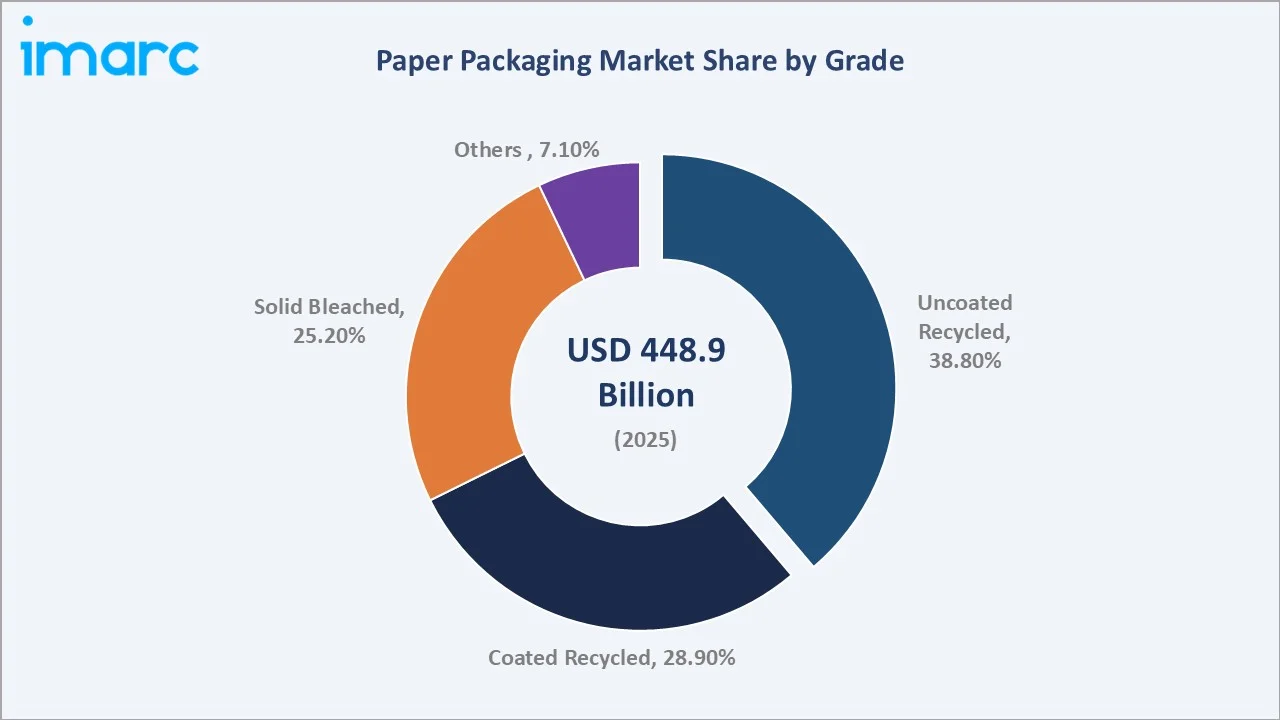

Uncoated Recycled - 38.8% share (2025) |

|

Leading Region |

Asia Pacific - 39.3% revenue share (2025) |

|

Fastest Growing Distribution Channel |

E-commerce Packaging - CAGR ~5.6% (2026-2034) |

|

Top Companies |

International Paper, Smurfit Kappa, WestRock, Mondi, DS Smith |

|

Key Market Opportunity |

Plastic-to-paper conversion: USD 50+ Billion addressable by 2034 |

Key Analytical Observations Supporting the Above Data:

- Folding boxes and cases lead with a 45.2% product type share (2025), driven by strong demand for retail-ready secondary packaging across food, personal care, electronics, and pharmaceutical segments, alongside the rapid shift from plastic to paper-based packaging formats.

- Uncoated recycled grade represents the largest grade segment at 38.8% (2025), reflecting strong demand for cost-effective, sustainable, and recycled-content board across a broad range of packaging applications, including corrugated boxes, industrial packaging, and retail-ready formats.

- Asia Pacific accounts for 39.3% of global revenues (2025), anchored by China’s role as the world’s largest paper packaging producer and consumer, complemented by India's 22-25% annual packaging market growth trajectory.

- Smart and active packaging represents the fastest-growing innovation segment, with RFID-embedded paper packaging, QR-coded boxes, and moisture-indicator cartons growing at a fast pace, more than three times the overall market rate.

Global Paper Packaging Market Overview

The paper packaging industry constitutes one of the oldest, largest, and most strategically important segments within the global packaging and materials ecosystem. Paper-based packaging encompasses a vast spectrum of products, from industrial corrugated shipping boxes and retail folding cartons to liquid paperboard milk cartons, paper bags, kraft sacks, and emerging fiber-based flexible formats that collectively serve virtually every consumer-facing and industrial sector on the planet.

Paper packaging's key competitive advantage lies in its sustainability credentials: it is biodegradable, compostable, recyclable, and renewable. Data from the European Paper Recycling Council indicates that the recycling rate for all paper products, including graphic paper, packaging, and tissue, reached 75.1% in 2024. The growing consumer preference for packaging that is visually aligned with sustainability values has accelerated brand migration from plastic to paper across food, retail, personal care, and pharmaceutical categories.

Macroeconomic influences, including urbanization, rising disposable incomes, growth of the organized retail sector, and food safety regulations, positively impact paper packaging demand across all regions. The industry's vertically integrated structure - from forest management through pulp and paper manufacturing to packaging conversion - creates significant barriers to entry while providing established players with cost and sustainability advantages.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

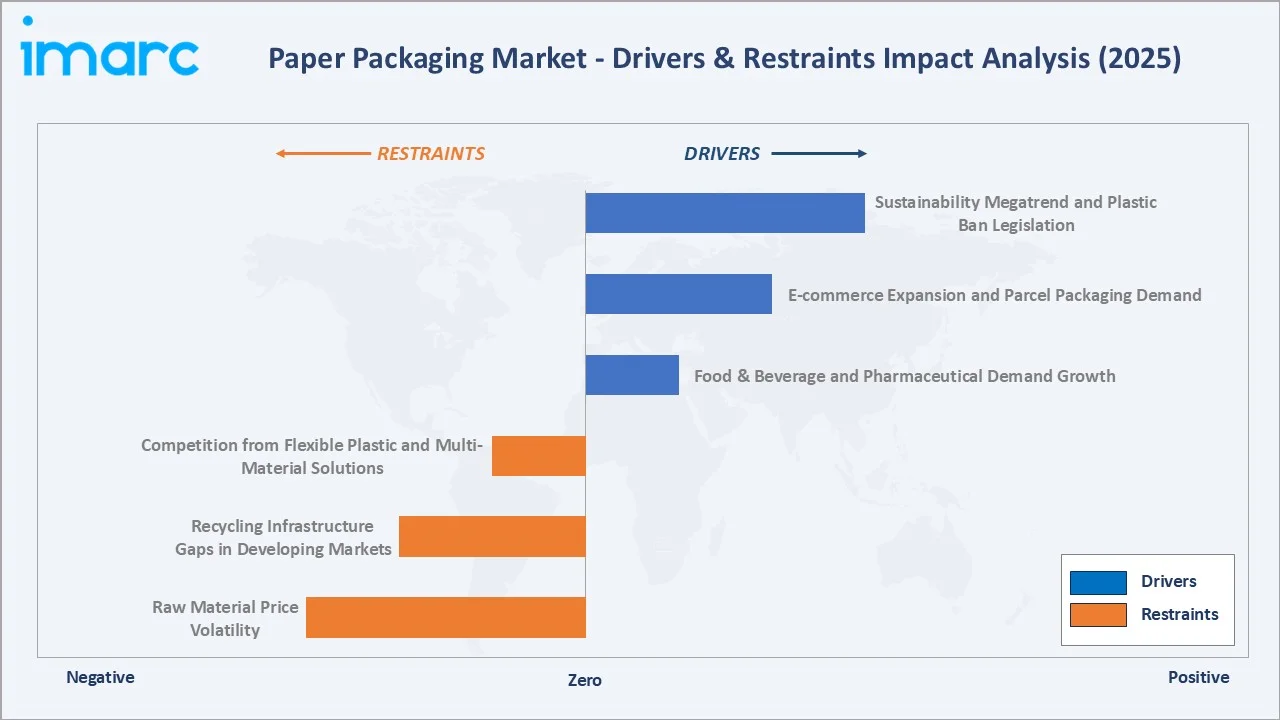

- Sustainability Megatrend and Plastic Ban Legislation: Over 100 countries have implemented some form of plastic restriction or ban as of 2025, with the EU's Single-Use Plastics Directive, UK Plastic Packaging Tax (GBP 217 per ton on packaging with less than 30% recycled content), and India's comprehensive single-use plastic ban directly redirecting packaging investment toward paper-based alternatives.

- E-commerce Expansion and Parcel Packaging Demand: Global B2C e-commerce revenue is projected to reach USD 5.5 trillion by 2027, growing at a steady compound annual growth rate (CAGR) of 14.4%, with parcel volumes demanding hundreds of billions of corrugated and paper-based protective packaging units annually.

- Food & Beverage and Pharmaceutical Demand Growth: Rising consumption of packaged food, ready-to-eat meals, beverages, and pharmaceutical products is fueling sustained demand for hygienic, food-safe paper packaging. Global packaged food revenues are projected to exceed USD 4.97 trillion by 2034, providing a robust volume base for paper packaging growth.

These drivers collectively reinforce a structural paper packaging market transition - sustainability mandates create regulatory demand, e-commerce creates volume demand, and technological innovation removes functional barriers that previously made plastic substitution difficult or commercially unviable.

Market Restraints

- Raw Material Price Volatility: As of December 2025, the average daily price of imported hardwood pulp in China reached RMB 4,627.63 per ton, reflecting an increase of RMB 385.26 per ton (9.08%) compared to September 30. This volatility compresses converter margins and creates planning complexity for brand owners’ negotiating annual packaging contracts.

- Recycling Infrastructure Gaps in Developing Markets: According to Singapore’s National Environment Agency, the paper recycling rate declined sharply from 52% to 32%. This drop is attributed to rising collection and freight costs, along with unfavorable commodity price trends.

- Competition from Flexible Plastic and Multi-Material Solutions: High-performance flexible plastics and multi-layer laminates continue to offer superior moisture, oxygen, and grease barrier properties at lower weight and cost compared to many paper alternatives, particularly in snack food, meat, and dairy packaging applications where paper's functional performance remains challenged.

Market Opportunities

- Plastic-to-Paper Conversion Pipeline: According to a new report released in March 2026 by the Ellen MacArthur Foundation, more than 40 leading organizations and experts are urging accelerated innovation in paper-based alternatives to address the growing challenge of flexible plastic packaging pollution.

- Smart and Active Packaging: The convergence of digital connectivity, IoT, and packaging is creating a rapidly growing smart paper packaging segment. RFID-embedded corrugated cases, QR-coded cartons, time-temperature indicator labels on pharmaceutical paper packaging, and augmented reality-enabled printing are expected to boost the market further.

- Emerging Market Organized Retail Expansion: Asia Pacific, Africa, and Latin America are experiencing rapid growth in organized retail and food processing sectors, creating significant incremental demand for branded paper packaging, retail-ready packaging, and food-grade cartons across previously underpenetrated geographic markets.

Market Challenges

- Achieving Cost Competitiveness with Plastic: Sustainable packaging typically carries a 10-25% unit cost premium over equivalent plastic packaging in many high-volume applications. As environmental regulation-driven plastic bans intensify, narrowing this cost gap through fiber efficiency, scale economics, and recycled content optimization remains a critical industry challenge.

- Food Contact Material Compliance Complexity: Increasingly stringent food contact material (FCM) regulations globally, including EFSA guidelines in Europe, FDA standards in the U.S., and national standards across Asia, are requiring significant reformulation investment for paper packaging manufacturers, particularly those using recycled fiber that may contain trace mineral oils.

- Supply Chain and Logistics Disruptions: Global paper packaging supply chains were significantly disrupted between 2021 and 2023 by port congestion, container shortages, and energy cost spikes at European mills. Building resilient, geographically diversified supply chains remains a priority for both manufacturers and large brand-owner customers.

Emerging Market Trends

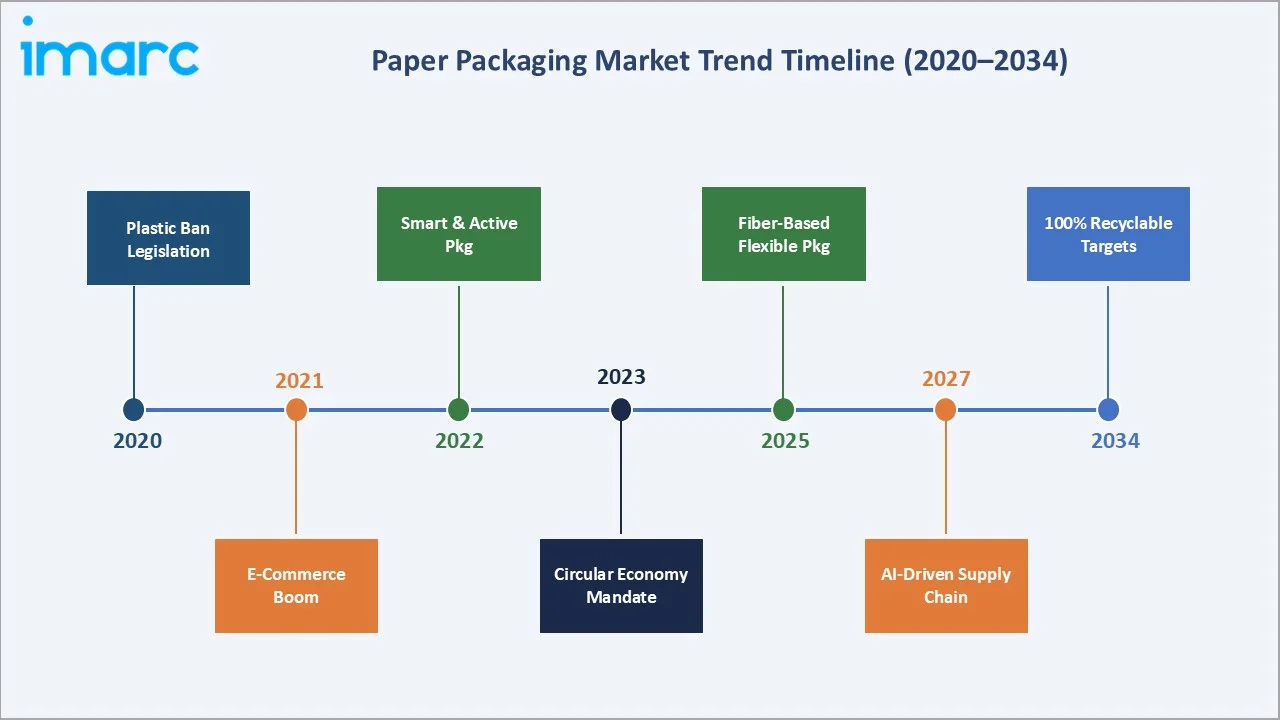

1. Plastic-to-Paper Substitution at Scale

The most transformative paper packaging market trend of the 2020s is the structural, policy-driven substitution of plastic packaging with paper-based alternatives across virtually every consumer product category. As part of its 2030 Ambition, Procter & Gamble aims to cut its use of virgin plastics by 50% by 2030, with paper-based materials as the primary beneficiary of this transition.

2. Smart and Digital Packaging Integration

Artificial intelligence, IoT connectivity, and digital printing technologies are converging to create a new generation of intelligent paper packaging. QR codes embedded on corrugated cases are enabling full supply chain traceability, with major FMCG corrugated packaging carrying machine-readable codes. RFID-enabled paper-based shipping cartons are accelerating in pharmaceutical logistics to meet serialization mandates.

3. E-commerce Packaging Innovation and Optimization

Amazon’s Frustration-Free Packaging (FFP) program focuses on reducing packaging and fulfillment costs by minimizing material use and labor. In the face of skilled labor shortages, automation can bridge the gap while reducing payroll costs by up to 40%.

4. Circular Economy and Recycled Fiber Innovation

The global paper packaging industry is increasingly engineering its products around circular economy principles, with recycled fiber content rising across all grade categories. Uncoated Recycled Board (URB), at 38.8% of market share in 2025, continues to grow as brands demand high recycled content, cost-effective packaging for industrial and secondary packaging applications. Chemical fiber-to-fiber recycling innovations, including enzymatic deinking and cellulose dissolution technologies, are improving the quality and applicability of recycled content paper, enabling use in food-contact applications previously limited to virgin fiber.

Industry Value Chain Analysis

The paper packaging value chain spans multiple interconnected stages from sustainable forest management and pulp production through paper and board manufacturing, packaging conversion, and final delivery to end-use industries.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Virgin wood pulp suppliers; recycled fiber collectors; Sappi, Stora Enso, forestry |

|

Pulp & Paper Mills |

International Paper, Nippon Paper, Holmen Group, Mondi, WestRock |

|

Packaging Converters |

Smurfit Kappa, DS Smith, Georgia-Pacific, Huhtamaki, Hood Packaging |

|

Printing & Finishing |

Flexographic and digital printers; coating and lamination specialists |

|

Distribution & Logistics |

Integrated supply chains; 3PLs; direct-to-manufacturer and retailer channels |

|

End-Use Industries |

Food & Beverage, E-commerce, Healthcare, Personal Care, Industrial |

Asia Pacific's dominant market position is anchored by its strength in the pulp, paper manufacturing, and high-volume conversion stages of the value chain. Europe's competitive advantage lies in sustainable forestry, premium board grades, and innovative converting capabilities for barrier and functional packaging.

Technology Landscape in the Paper Packaging Industry

Advanced Barrier and Coating Technologies

Barrier coating innovation is the single most strategically important technology frontier in paper packaging, enabling paper to replace plastics in applications requiring moisture, oxygen, grease, or aroma barrier performance. Water-based dispersion barrier coatings are achieving oxygen transmission rates (OTR) and water vapor transmission rates (WVTR) comparable to conventional plastic films in laboratory conditions.

Digital Printing and Customization

High-speed digital printing systems for corrugated and folding carton packaging are transforming the economics of short-run, customized, and versioned packaging. HP PageWide and Landa digital printing presses are enabling brand owners to implement personalized packaging programs, featuring regional, seasonal, and promotional variants, at near-offset economics and lead times measured in days rather than weeks.

Smart Packaging and Connectivity Technologies

RFID, NFC, and QR code integration into paper-based packaging is enabling brand owners to implement end-to-end supply chain traceability, anti-counterfeiting, and consumer engagement capabilities. Invisible inkjet-printed machine-readable codes on corrugated cases are being deployed at scale to replace traditional barcode labels, reducing waste and improving scan reliability across automated distribution environments.

Sustainable Manufacturing and Circular Technology

Closed-loop water systems, zero-liquid-discharge mill technologies, and lignin valorization programs are significantly improving the environmental footprint of paper and pulp manufacturing. Paper mills' on-site electricity generation, entirely powered by renewable biomass, is expected to double, increasing the facility’s energy self-sufficiency to over 80%.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Folding Boxes and Cases |

45.2% |

2025 |

|

Grade |

Uncoated Recycled |

38.8% |

2025 |

|

Packaging |

Primary Packaging |

48.3% |

2025 |

|

End Use Industry |

Food |

30.8% |

2025 |

|

Region |

Asia Pacific |

39.3% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Folding boxes and cases dominate the paper packaging market with a 45.2% share in 2025, driven by strong demand for retail-ready, visually appealing, and sustainable secondary packaging across food, personal care, electronics, and pharmaceutical industries. Corrugated boxes represent 28.1% of the market (2025), serving the e-commerce, food, and industrial shipping needs of brand owners globally.

By Grade

Uncoated recycled leads with a 38.8% market share (2025), reflecting strong demand for cost-effective, sustainable, and recycled-content board across industrial, corrugated, and secondary packaging applications. Coated recycled holds a 28.9% share in 2025, serving the consumer goods and retail packaging segments that require printable, bright-white coated surfaces for premium brand presentation.

Regional Market Insights

Asia Pacific’s market leadership (39.3% share in 2025) is anchored by China's position as the world's largest paper and paperboard producer, outputting approximately 130 million metric tons annually, and its massive manufacturing base for consumer goods that require paper packaging. In India, the installed capacity for paper and paperboard is approximately 5 million tons, with utilization levels exceeding 95%, indicating strong scale and operational efficiency.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Players |

|

Asia Pacific |

39.3% |

E-commerce boom, urbanization, food processing growth, rising middle class |

China GB standards; India BIS packaging norms |

Nippon Paper, Oji Holdings, ITC Ltd. |

|

North America |

24.8% |

Plastic ban legislation, e-commerce expansion, and sustainability mandates |

EPA guidelines; state-level plastic bans (CA, NY) |

International Paper, Georgia-Pacific, WestRock |

|

Europe |

19.7% |

EU Green Deal, circular economy targets, premium sustainable packaging |

EU Packaging & Packaging Waste Regulation (PPWR) |

Smurfit Kappa, DS Smith, Mondi, Stora Enso |

|

Middle East and Africa |

9.6% |

Growing retail & FMCG sector, urbanization, food exports |

GCC halal packaging compliance |

Napco National, local converters |

|

Latin America |

6.6% |

Food & beverage industry expansion, growing e-commerce adoption |

Brazil ABNT packaging standards |

Rigesa (WestRock), Klabin, Suzano |

North America (24.8% share, 2025) is being reshaped by aggressive plastic ban legislation at the state and city levels alongside e-commerce expansion. Legislation such as California's SB 343 and New York's Packaging Reduction and Recycling Infrastructure Act are accelerating brand owner migration to paper-based packaging solutions across consumer goods categories.

Competitive Landscape

The global paper packaging market exhibits a moderately consolidated competitive structure at the tier-1 level, with the top five players - International Paper, Smurfit Kappa, WestRock, Mondi, and DS Smith - collectively accounting for approximately 22-25% of global market revenues in 2025. The market's remaining revenues are distributed among hundreds of regional and national converters, specialty packaging producers, and mill-integrated players across Asia, Europe, and the Americas.

|

Company Name |

Key Brand / Division |

Market Position |

Core Strength |

|

International Paper Co. |

International Paper |

Market Leader |

Global corrugated & industrial packaging scale |

|

Smurfit WestRock |

Smurfit Kappa |

Market Leader |

Global corrugated packaging leader; integrated paper-based solutions; strong presence across Europe and North America |

|

Mondi Group Plc |

Mondi |

Strong Challenger |

Flexible paper & sustainable packaging innovation |

|

Amcor plc |

Amcor |

Specialty Leader |

Flexible & rigid packaging; global distribution network |

|

Stora Enso Oyj |

Stora Enso |

Sustainability Leader |

Renewable materials; fiber-based innovative solutions |

|

Huhtamaki Oyj |

Huhtamaki |

Food Service Leader |

Foodservice paper packaging: sustainability commitments |

The competitive landscape is evolving rapidly, characterized by consolidation among major players and increasing entry of regional converters targeting niche applications. Companies are differentiating through sustainability initiatives, lightweight packaging innovations, and e-commerce-ready designs to address changing regulatory and consumer demands.

Key Company Profiles

International Paper Company

International Paper (IP) is the world's prominent paper and packaging company by revenue, operating across 24 countries with approximately 37,000 employees and annual revenues exceeding USD 18.6 billion in 2024. IP's industrial packaging segment - producing corrugated boxes, linerboard, and medium - represents approximately 83% of total revenues, making it the dominant supplier to North American e-commerce, food, and industrial sectors.

- Product Portfolio: Corrugated containers, containerboard, kraftliner, coated paperboard, and fiber-based packaging solutions for industrial and consumer applications.

- Recent Developments: In January 2025, International Paper announced the completion of its USD 7.2 billion acquisition of DS Smith Plc, creating the world's largest corrugated packaging company with over USD 25 billion in combined revenues and a significantly strengthened European market position.

- Strategic Focus: Post-DS Smith integration synergy capture, North America corrugated volume growth, European market leadership, and sustainable packaging innovation, including 100% recycled and FSC-certified linerboard programs.

Mondi Group Plc

Mondi Group is a global leader in sustainable packaging and paper, with operations across 30+ countries and revenues of approximately EUR 7.4 billion in 2024. Mondi's unique strength lies in its dual capability in fiber-based flexible packaging and industrial corrugated solutions, positioning it as a leading beneficiary of the plastic-to-paper substitution trend across both rigid and flexible packaging formats.

- Product Portfolio: Kraft paper, industrial bags, fiber-based flexible packaging, corrugated, consumer packaging, and the innovative functional barrier paper range for plastic replacement applications.

- Recent Developments: In May 2024, Mondi launched TrayWrap, a fiber-based secondary paper packaging solution replacing plastic shrink-wrap in food service distribution. The company also expanded its EcoWicketBag product range in 2024, targeting the personal care and home care sectors as plastic bag replacement alternatives.

- Strategic Focus: Fiber-based plastic substitution portfolio growth, sustainable packaging design partnerships with FMCG brands, Eastern European manufacturing cost advantage leverage, and forest certification program deepening.

Smurfit WestRock

Smurfit WestRock is one of the world’s largest paper-based packaging companies, formed in 2024 through the merger of Smurfit Kappa and WestRock. The combined entity operates across 40 countries with a strong presence in Europe and North America, generating estimated combined revenues of over USD 30 billion. The company is a global leader in corrugated packaging, serving e-commerce, FMCG, and industrial sectors at scale.

- Product Portfolio: Corrugated containers, containerboard, paper-based packaging, bag-in-box solutions, point-of-sale displays, and sustainable fiber-based packaging solutions.

- Recent Developments: In July 2024, Smurfit Kappa and WestRock completed their merger to form Smurfit WestRock, creating a global packaging leader with enhanced geographic reach and operational scale. The company has since focused on integrating operations and optimizing its global mill and converting network.

- Strategic Focus: Post-merger integration and synergy realization, expansion of sustainable fiber-based packaging solutions, e-commerce packaging innovation, and strengthening leadership in circular packaging systems across key markets.

- Core Capabilities: Large-scale integrated operations, strong corrugated packaging expertise, sustainability leadership, and global supply chain efficiency.

Amcor plc

Amcor plc is a global leader in consumer and healthcare packaging, operating across 40 countries with approximately 41,000 employees and revenues of around USD 13–14 billion in 2024. While traditionally known for flexible plastic packaging, Amcor is increasingly expanding its portfolio into paper-based and recyclable packaging solutions in response to sustainability trends.

- Product Portfolio: Flexible packaging, rigid containers, paper-based packaging solutions, recyclable and high-barrier packaging for food, beverage, personal care, and healthcare applications.

- Recent Developments: Amcor has accelerated investments in recyclable and paper-based packaging innovations, including the development of high-performance paper packaging solutions aimed at replacing plastic in selected applications. The company has also expanded partnerships with FMCG brands to deliver sustainable packaging formats.

- Strategic Focus: Transition toward recyclable and sustainable packaging, material innovation (including paper-based alternatives), expansion in emerging markets, and strengthening partnerships with global consumer goods companies.

- Core Capabilities: Advanced material science, strong FMCG customer relationships, global manufacturing footprint, and leadership in flexible and sustainable packaging innovation.

Market Concentration Analysis

The global paper packaging market exhibits moderate concentration at the tier-1 level, with the Smurfit WestRock merger (completed 2024) creating a dominant global player with approximately USD 34 billion in annual revenues - significantly reshaping the competitive hierarchy. The combined entity, along with International Paper (post-DS Smith acquisition), now controls approximately 25-30% of global corrugated packaging capacity.

The folding carton and specialty paper packaging sub-segments remain more fragmented, with hundreds of regional converters and specialty printers serving brand-specific, short-run, and geographically proximate customer bases. In the Asia Pacific, local and national champions, including Nippon Paper, Rengo (Japan), ITC (India), and Nine Dragons Paper (China), dominate regional markets with limited Western multinational penetration.

M&A consolidation activity has accelerated dramatically since 2022, driven by the need for scale in fiber procurement, converting network coverage, and sustainability investment. The Smurfit WestRock and International Paper/DS Smith transactions signal the beginning of a global consolidation wave that is expected to continue through 2030, particularly targeting mid-sized European and Asian converters.

Investment & Growth Opportunities

Fastest Growing Segments

Smart packaging (CAGR ~7.1%), e-commerce packaging (CAGR ~5.6%), and paper bags & sacks (CAGR ~3.2%) represent the highest-growth investment vectors in the global paper packaging market through 2034. The plastic-to-paper substitution represents a large incremental investment opportunity, spanning barrier coatings, fiber-based flexible packaging, and molded fiber product development.

Emerging Market Expansion

India, Southeast Asia, Sub-Saharan Africa, and Brazil represent the most compelling geographic investment opportunities, with packaging consumption per capita in these markets running at 25-40% of mature market levels. India's paper packaging market is growing at 8-10% annually, driven by e-commerce, organized retail expansion, and food processing industry growth. Indonesia, Vietnam, and Thailand are experiencing 6-8% annual packaging demand growth on the back of manufacturing industrialization and FMCG market development.

Venture and Strategic Investment Trends

By 2025, more than 1,630 new businesses focused on clean packaging had emerged globally, experimenting with innovations such as plant-based starch materials and rock-derived paper alternatives.

- Key growth bets: By leveraging machine learning, companies in Egypt can forecast return trends based on historical data and consumer behavior. These accurate predictions support efficient inventory management by maintaining optimal stock levels and minimizing excess and waste.

- ESG-aligned institutional investors are targeting paper packaging companies with certified sustainable forestry programs, science-based emissions reduction targets, and demonstrated circular economy metrics as preferred investments, benefiting integrated players like Stora Enso, Mondi, and Smurfit WestRock.

- Strategic acquisition targets include specialty barrier paper manufacturers, molded fiber packaging innovators, and Asian regional converters with established relationships with electronics and e-commerce brand owners seeking paper packaging supply chain diversification away from China.

Future Market Outlook (2026-2034)

The global paper packaging market is positioned for sustained, broad-based growth through 2034, anchored by the structural plastic-to-paper transition, exponential e-commerce volume growth, and geographic expansion of organized retail in emerging economies. From a projected base of USD 448.9 Billion in 2025, the market is forecast to reach USD 552.0 Billion by 2034, representing absolute incremental value addition of approximately USD 103.1 Billion over the decade.

Technological disruptions, including AI-optimized packaging design, chemical fiber recycling breakthroughs, nano-barrier coating commercialization, and smart packaging platform proliferation, are expected to materially reshape both the cost structure and functional performance envelope of paper packaging through 2034.

The regulatory environment will intensify through 2034, with the EU PPWR implementation, extended producer responsibility (EPR) scheme expansions across Asia and the growing demand for sustainable alternatives across emerging economies, including the expanding Paper Packaging Market in Latin America, along with potential US federal plastic packaging legislation, is creating an increasingly favorable macro environment for paper packaging investment.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys with over 160 industry professionals in 2024-2025, comprising paper packaging executives, pulp and paper mill managers, brand owner packaging procurement directors, retail buyers, sustainability officers, and end consumers across Asia Pacific, North America, Europe, and emerging markets.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, sustainability reports, regulatory filings, trade publications (Packaging Digest, Packaging World, RISI Pulp & Paper Intelligence), industry association data (FEFCO, AF&PA, Confederation of European Paper Industries), and publicly available financial data from major industry participants.

Forecasting Models

Market size estimates and growth projections were derived through a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, packaging intensity ratios, plastic ban legislation timelines, e-commerce penetration projections, and historical paper packaging demand evolution patterns. Three-scenario analysis (base, optimistic, and conservative) was conducted to capture regulatory timing uncertainty and raw material price volatility.

Paper Packaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Corrugated Boxes, Folding Boxes and Cases, Liquid Paperboard Cartons, Paper Bags and Sacks, Others |

| Grades Covered | Solid Bleached, Coated Recycled, Uncoated Recycled, Others |

| Packaging Levels Covered | Primary Packaging, Secondary Packaging, Tertiary Packaging |

| End Use Industries Covered | Food, Beverage, Personal Care and Home Care, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | International Paper Co., Smurfit WestRock, Mondi Group Plc, Amcor plc, Stora Enso Oyj, Huhtamaki Oyj, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the paper packaging market from 2020-2034.

- The paper packaging market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the paper packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Paper Packaging Market Report

The global paper packaging market was valued at USD 448.9 Billion in 2025 and is projected to reach USD 552.0 Billion by 2034, growing at a CAGR of 2.25%.

The paper packaging market is expected to grow at a CAGR of 2.25% during the forecast period 2026-2034, driven by sustainability regulations and e-commerce packaging demand growth globally.

Folding boxes and cases lead with a 45.2% product-type share in 2025, driven by strong retail-ready packaging demand across food, personal care, electronics, and pharmaceutical sectors, alongside the accelerating plastic-to-paper substitution trend in secondary packaging.

Uncoated recycled leads with a 38.8% grade share in 2025, reflecting demand for cost-effective, sustainable, and high recycled-content board across industrial, corrugated, and secondary packaging applications globally.

Asia Pacific is the dominant region, holding a 39.3% market share in 2025, anchored by China’s manufacturing base, India’s FMCG and e-commerce growth, and Japan’s advanced recycling culture.

Key drivers include global plastic ban legislation, e-commerce expansion, food and pharmaceutical packaging demand, sustainability mandates from brands and retailers, and barrier coating innovations enabling plastic substitution.

Smart and active packaging (CAGR ~7.1%), e-commerce packaging optimization, plastic-to-paper substitution, circular economy fiber innovations, and sustainable barrier coating technologies are the fastest-growing trends through 2034.

Leading companies include Amcor plc, Huhtamäki Oyj, Smurfit WestRock, International Paper Group, Mondi Group Plc, Stora Enso Oyj, etc.

The EU Packaging and Packaging Waste Regulation mandates 100% recyclable packaging by 2030 and minimum recycled content targets through 2040, creating significant demand uplift for paper-based packaging as brands reformulate plastic-heavy portfolios.

High-growth opportunities include bio-based barrier coating innovations, smart packaging platform development, molded fiber product expansion, emerging market converter acquisitions, and plastic-to-paper substitution technology investment.

Key challenges include raw material price volatility, recycling infrastructure gaps in developing markets, achieving cost competitiveness with plastic in barrier-sensitive applications, and food contact material compliance complexity.

The Smurfit WestRock merger (2024) created the world's largest packaging company at USD 34 billion in revenues, significantly consolidating global corrugated capacity and reshaping competitive dynamics across North America and Europe.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)