Paper Straw Market Report by Material (Virgin Paper, Recycled Paper), Product Type (Non-printed, Printed), Straw Length (<5.75 Inches, 5.75-7.75 Inches, 7.75-8.5 Inches, 8.5-10.5 Inches, >10.5 Inches), Diameter (<0.15 Inches, 0.15 - 0.196 Inches, 0.196 - 0.25 Inches, 0.25 - 0.4 Inches, >0.4 Inches), Sales Channel (B2B, B2C), End Use (Foodservice, Institutional, Household, Food Processing Industry), and Region 2026-2034

Market Overview:

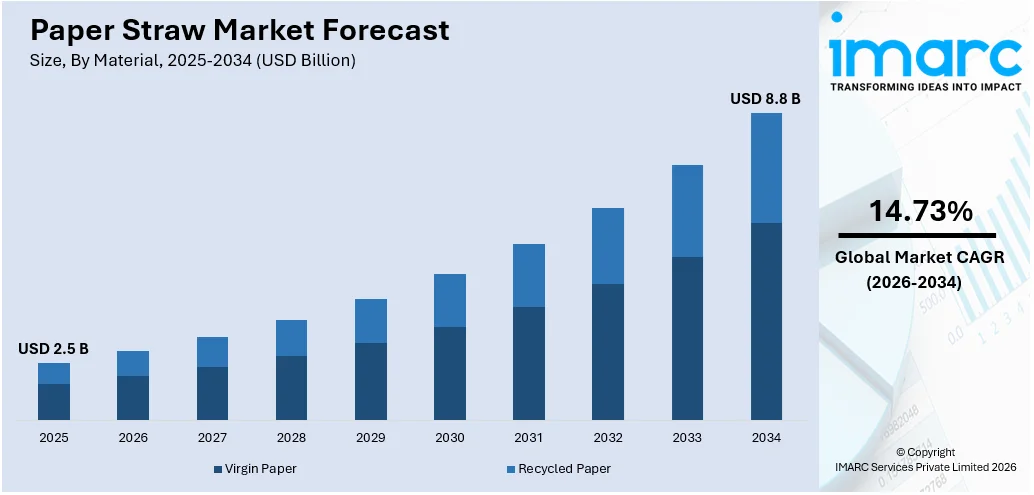

The global paper straw market size reached USD 2.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 8.8 Billion by 2034, exhibiting a growth rate (CAGR) of 14.73% during 2026-2034. The market is experiencing robust growth, driven by stringent environmental regulations, shifting consumer preferences toward sustainability, technological advancements in production, and increased corporate emphasis on eco-friendly practices across the food and beverage industry.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2034 | USD 8.8 Billion |

| Market Growth Rate (2026-2034) | 14.73% |

Paper straws are an eco-friendly alternative to their plastic counterparts, designed to reduce environmental impact. Comprising biodegradable materials, primarily paper and sometimes coated with a thin layer of beeswax or a plant-based substance, they represent a shift toward sustainable consumption. Their manufacturing process involves cutting and winding paper into a cylindrical shape, ensuring they are sturdy enough for single use. The rise in their popularity is largely attributed to growing environmental awareness and the global movement to reduce plastic waste, particularly in oceans and other natural habitats. Paper straws, while not as durable as plastic straws, offer a practical solution for consumers and businesses seeking to minimize their ecological footprint. They are widely used in various settings, including restaurants, cafes, and personal households.

To get more information on this market Request Sample

The global paper straw industry is being driven by technological advancements in manufacturing processes. Innovations in production technology have made the production of paper straws more cost-effective and efficient, reducing the price gap between plastic and paper straws. This economic viability is encouraging more businesses to transition to paper straws. Furthermore, the development of higher quality paper straws that are more durable and less prone to becoming soggy is enhancing consumer experience, thereby increasing their acceptance. Another significant driver is the growing trend of sustainability in the packaging industry. As companies aim to reduce their overall environmental impact, the focus is growing on the product and how it is packaged and disposed of. Paper straws, often made from recycled materials, fit well into this sustainable packaging trend. Additionally, the rise of online retail platforms has made it easier for consumers and businesses to access eco-friendly products, including paper straws, contributing to market growth. Besides this, the increase in outdoor events and fast-food consumption, where disposable utensils are in high demand, is also facilitating the market growth.

Paper Straw Market Trends/Drivers:

Environmental regulations and policies

A significant driver of the global paper straw industry is the increasing implementation of environmental regulations and policies by governments worldwide. These policies include bans or restrictions on single-use plastics, including plastic straws, to mitigate their negative impact on ecosystems, particularly marine environments. The European Union, for instance, has implemented directives to reduce plastic waste, propelling the demand for alternatives like paper straws. This regulatory landscape is encouraging manufacturers to innovate and produce eco-friendlier products as well as heightening consumer awareness and responsibility toward the environment. Consequently, industries such as food and beverage are rapidly adopting paper straws, aligning their practices with these regulatory demands and consumer expectations, thereby fueling the market growth for paper straws.

Consumer awareness and preferences

The shift in consumer preferences toward sustainable and eco-friendly products is another crucial factor driving the market. Heightened awareness about the detrimental effects of plastic pollution, particularly in oceans, has led to a growing demand for green alternatives. This change is reflected in consumer behavior and choices, with a significant portion of the population opting for products that have a lesser environmental impact. Paper straws, being biodegradable and compostable, align well with this eco-conscious ethos. Many consumers, especially millennials and Gen Z, are willing to pay a premium for sustainable options, influencing businesses across the hospitality and food service industries to replace plastic straws with paper alternatives. This consumer-driven demand is significantly propelling the growth of the industry, as businesses strive to meet these environmental and social expectations.

Corporate social responsibility (CSR) and brand image

Corporations are increasingly recognizing the importance of Corporate Social Responsibility (CSR) in shaping their brand image and building consumer trust. Adopting environmentally friendly practices, such as using paper straws, is a visible and tangible way for companies to demonstrate their commitment to sustainability. Major corporations, particularly in the food and beverage sector, have been transitioning to paper straws as part of their CSR initiatives. This shift is helping in reducing the environmental footprint of these companies and enhancing their brand image and appeal to environmentally conscious consumers. The move toward paper straws is often part of a broader strategy to achieve sustainability goals and project a responsible corporate image. This trend is particularly pronounced in the hospitality industry, where the use of eco-friendly products like paper straws is becoming a norm, thereby significantly driving the market growth for these products.

Paper Straw Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on material, product type, straw length, diameter, sales channel, and end use.

Breakup by Material:

- Virgin Paper

- Recycled Paper

Virgin paper accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the material. This includes virgin paper, and recycled paper. According to the report, virgin paper represented the largest segment.

Virgin paper is the leading material segment due to its superior quality and performance characteristics. Virgin paper, made from new pulp, exhibits higher strength and durability compared to recycled paper. This quality is crucial for paper straws, as it ensures they maintain their integrity and do not become soggy quickly when in contact with liquids. Additionally, virgin paper offers a smoother, more uniform surface, which is essential for printing and branding purposes, a key consideration for businesses in the hospitality and food service sectors. While recycled paper is more eco-friendly, the functional superiority of virgin paper makes it the preferred choice for manufacturers looking to balance sustainability with performance, driving its predominance in the market.

Breakup by Product Type:

- Non-printed

- Printed

Non-printed holds the largest share in the industry

A detailed breakup and analysis of the market based on the product types has also been provided in the report. This includes non-printed and printed. According to the report, non-printed accounted for the largest market share.

Non-printed straws currently lead the product type segment due to their simplicity, cost-effectiveness, and broader appeal. These straws, devoid of any printed designs or branding, are typically cheaper to produce as they bypass the additional processes and costs associated with printing. This cost efficiency makes them an attractive option for a wide range of businesses, especially those in the food and beverage industry operating with tight cost margins. Moreover, non-printed straws possess a universal aesthetic appeal, making them suitable for various settings and occasions, from casual dining to formal events. Their simplicity also aligns well with the minimalist and natural ethos often associated with sustainable products, further enhancing their popularity in a market increasingly driven by environmental consciousness.

Breakup by Straw Length:

- <5.75 Inches

- 5.75-7.75 Inches

- 7.75-8.5 Inches

- 8.5-10.5 Inches

- >10.5 Inches

7.75-8.5 inches represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the straw length. This includes <5.75 inches, 5.75-7.75 inches, 7.75-8.5 inches, 8.5-10.5 inches, and >10.5 inches. According to the report, 7.75-8.5 inches represented the largest segment.

The 7.75-8.5 inches length range is optimally suited for the majority of beverage containers used in the food and beverage industry. Straws within this length are versatile, comfortably fitting into a wide array of glasses, cups, and bottles, making them a practical choice for various settings, from quick-service restaurants to high-end bars. This size is particularly ideal for standard soft drink and water glasses, as well as most takeaway beverage cups. The universal applicability of this length range simplifies inventory management for businesses and reduces the need for multiple straw sizes, thereby enhancing the operational efficiency and consumer convenience, which in turn drives its leading position in the market.

Breakup by Diameter:

- <0.15 Inches

- 0.15 - 0.196 Inches

- 0.196 - 0.25 Inches

- 0.25 - 0.4 Inches

- >0.4 Inches

0.196 - 0.25 inches exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the diameter has also been provided in the report. This includes <0.15 inches, 0.15 - 0.196 inches, 0.196 - 0.25 inches, 0.25 - 0.4 inches, and >0.4 inches. According to the report, 0.196 - 0.25 inches accounted for the largest market share.

The diameter range of 0.196 - 0.25 inches diameter is sufficiently wide to accommodate a variety of beverages, from soft drinks to thicker drinks like smoothies, without compromising the ease of drinking. It is particularly effective for the most commonly consumed beverages in cafes and restaurants. Moreover, this size is compatible with standard straw dispensers and lids, making it highly convenient for food service operators. The versatility of this diameter range, catering to a broad spectrum of drinking needs while ensuring a comfortable sipping experience, has established it as the preferred choice.

Breakup by Sales Channel:

Access the comprehensive market breakdown Request Sample

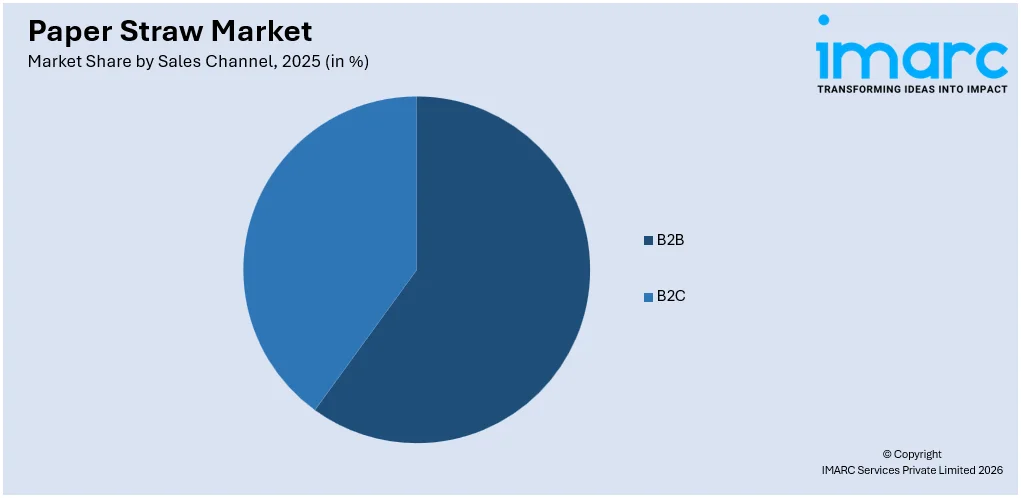

- B2B

- B2C

B2B dominates the market

The report has provided a detailed breakup and analysis of the market based on the sales channel. This includes B2B and B2C. According to the report, B2B represented the largest segment.

The Business-to-Business (B2B) segment holds the leading position in the market primarily due to the substantial demand from the food service and hospitality industries. Establishments such as restaurants, cafes, bars, and hotels are significant consumers of paper straws, requiring them in large quantities to serve their customers. B2B channels facilitate bulk purchases, often at discounted rates, which is economically advantageous for these businesses. Additionally, B2B transactions ensure a steady, reliable supply of paper straws, which is essential for operational continuity in these sectors. The high volume of usage in such commercial settings, coupled with the need for consistent quality and supply, makes the B2B channel the predominant sales route in the market.

Breakup by End Use:

- Foodservice

- Institutional

- Household

- Food Processing Industry

Food processing industry is the predominant market segment

A detailed breakup and analysis of the market based on the end use has also been provided in the report. This includes foodservice, institutional, household, and food processing industry. According to the report, food processing industry accounted for the largest market share.

The food processing industry emerges as the leading end-use segment due to the extensive use of straws in packaged beverages. This industry, encompassing a wide range of drinkable products like juices, dairy drinks, and ready-to-drink teas and coffees, often requires straws for consumer convenience. Paper straws are increasingly preferred in this sector for their eco-friendly attributes, aligning with the growing trend towards sustainable packaging. As consumers become more environmentally conscious, the demand for sustainable options in packaging, including straws, has surged. This shift is particularly noticeable in the food processing industry, where companies are keen to project an environmentally responsible image, making paper straws an essential component of their packaging strategy.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest paper straw market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America(the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America paper straw market is driven by stringent environmental regulations, heightened consumer awareness about sustainability, and proactive corporate responsibility initiatives. In this region, particularly in the United States and Canada, there has been a significant push towards reducing plastic waste, with numerous states and municipalities implementing bans or restrictions on single-use plastics, including plastic straws. This regulatory environment, combined with a growing consumer preference for eco-friendly products, is propelling the demand for paper straws. Furthermore, North American companies, especially in the food and beverage sector, are increasingly adopting sustainable practices, including the use of paper straws, to enhance their brand image and comply with consumer expectations.

Competitive Landscape:

The key players in the industry are actively engaging in strategies such as product innovation, mergers and acquisitions (M&A), and expanding their distribution networks to strengthen their market position. They are focused on developing more durable and functional paper straws, often incorporating advanced, eco-friendly materials to enhance the user experience and extend the lifespan of the product. Additionally, companies are collaborating with or acquiring smaller, specialized manufacturers to broaden their product range and market reach. To capitalize on the growing demand, these market leaders are also enhancing their production capabilities and exploring new markets, particularly in regions with stringent plastic ban regulations. This proactive approach is driving competition within the market and accelerating the overall growth and diversification of the industry.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- BioPak

- Footprint

- Hoffmaster Group, Inc

- Huhtamaki Group

- Jinhua Suyang Plastic Production Co., Ltd.

- Matrix pack

- Novolex

- Tetra Laval Group

- Transcend Packaging

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Paper Straw Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Virgin Paper, Recycled Paper |

| Product Types Covered | Non-printed, Printed |

| Straw Lengths Covered | <5.75 Inches, 5.75-7.75 Inches, 7.75-8.5 Inches, 8.5-10.5 Inches, >10.5 Inches |

| Diameters Covered | <0.15 Inches, 0.15 - 0.196 Inches, 0.196 - 0.25 Inches, 0.25 - 0.4 Inches, >0.4 Inches |

| Sales Channels Covered | B2B, B2C |

| End Uses Covered | Foodservice, Institutional, Household, Food Processing Industry |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BioPak, Footprint, Hoffmaster Group, Inc, Huhtamaki Group, Jinhua Suyang Plastic Production Co., Ltd., Matrix Pack, Novolex, Tetra Laval Group, Transcend Packaging, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the paper straw market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global paper straw market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the paper straw industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Paper Straw Market Report

The paper straw market was valued at USD 2.5 Billion in 2025.

The paper straw market is projected to exhibit a CAGR of 14.73% during 2026-2034, reaching a value of USD 8.8 Billion by 2034.

The paper straw market is driven by growing bans on plastic straws, rising consumer demand for eco-friendly alternatives, increasing awareness of environmental pollution, and government regulations promoting sustainable packaging. Support from foodservice and beverage industries also contributes to the market's steady expansion.

In 2025, North America dominated the paper straw market driven by strict environmental regulations, early adoption of plastic alternatives, and strong demand from the foodservice sector. Government initiatives promoting single-use plastic bans have accelerated regional growth, making Europe a key market for paper straw manufacturers.

Some of the major players in the global paper straw market include BioPak, Footprint, Hoffmaster Group, Inc, Huhtamaki Group, Jinhua Suyang Plastic Production Co., Ltd., Matrix Pack, Novolex, Tetra Laval Group, Transcend Packaging, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)