Parking Management Market Size, Share, Trends and Forecast by Offering Type, Deployment Mode, Parking Site, and Region, 2026-2034

Parking Management Market Size, Share, Trends & Forecast (2026-2034)

The global parking management market reached USD 5.53 Billion in 2025 and is projected to reach USD 10.43 Billion by 2034, growing at a CAGR of 7.07% during 2026-2034. Rapid urbanization driving parking scarcity, smart city investments deploying connected parking infrastructure, rising vehicle ownership creating demand for efficient space utilization, and the integration of electric vehicle charging with parking systems are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.53 Billion |

|

Forecast Market Size (2034) |

USD 10.43 Billion |

|

CAGR (2026-2034) |

7.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

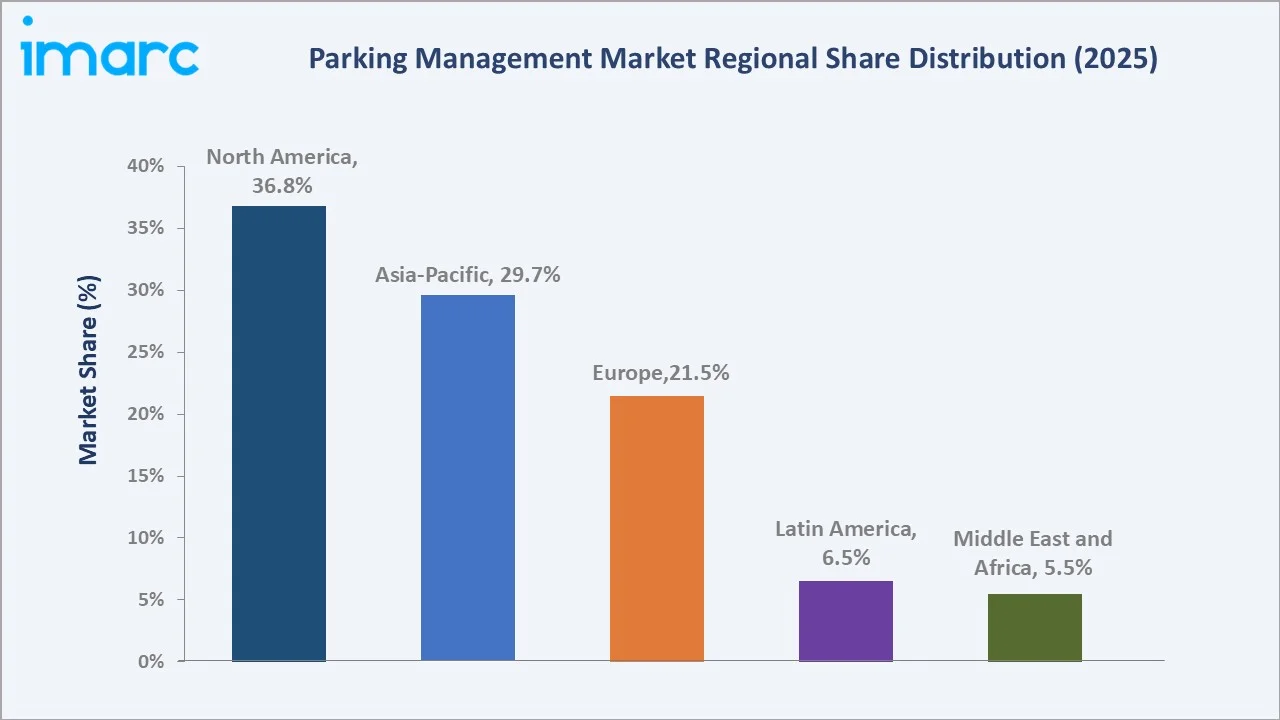

North America leads regionally with a 36.8% market share in 2025, driven by the highest concentration of smart city investment, mature parking technology infrastructure, high vehicle ownership rates, and the early adoption of AI-powered and cloud-native parking management platforms. Solution offerings command the dominant 67.8% share, reflecting the market’s primary revenue driver in parking access and revenue control systems (PARCS), guidance platforms, and reservation management solutions deployed across airports, municipalities, commercial real estate, and healthcare facilities.

To get more information on this market, Request Sample

The parking management market is underpinned by three structural demand forces: the physical scarcity of urban parking driven by population growth and vehicle density that makes intelligent space management a city operational necessity; the smart city technology adoption wave deploying IoT sensors, AI analytics, and mobile payment infrastructure that transforms parking from infrastructure to a data-driven service; and the EV transition creating new requirements for integrated charging management within parking assets.

Executive Summary

The global parking management market is experiencing sustained growth, driven by the convergence of worsening urban parking scarcity, large-scale smart city infrastructure programs deploying connected parking technology, and the progressive digitalization of parking operations from manual cash collection to AI-powered dynamic systems. The market was valued at USD 5.53 Billion in 2025 and is forecast to reach USD 10.43 Billion by 2034, growing at a CAGR of 7.07%.

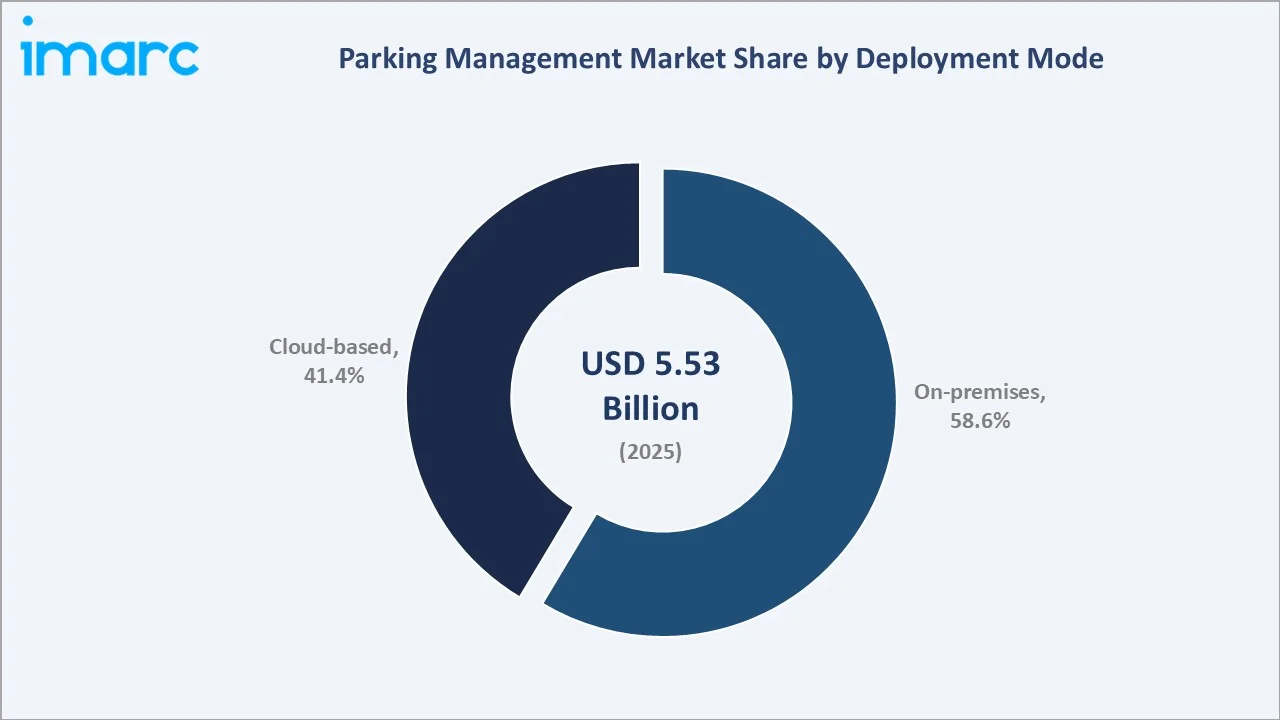

Solution accounts for 67.8% of the market in 2025, reflecting the primacy of software-centric parking access control, revenue management, guidance, and reservation platforms as the primary revenue category across all end-user segments. On-premises deployment at 58.6% reflects the installed base of legacy PARCS infrastructure at airports, hospitals, and municipalities that were deployed under on-premises architecture and are being progressively migrated to cloud or hybrid deployments.

North America leads regionally at 36.8%, driven by mature smart city investment, the highest density of technology-enabled parking operators, and the largest EV fleet requiring integrated charging management. Key players collectively define the competitive landscape through platform capability, system integration expertise, and long-term operator relationships.

Key Market Insights

|

Insight |

Data |

|

Largest Offering Type |

Solution – 67.8% share (2025) |

|

Fastest Growing Offering Type |

Solution – ~7.8% CAGR (2026-2034) |

|

Largest Deployment Mode |

On-premises – 58.6% share (2025) |

|

Fastest Growing Deployment Mode |

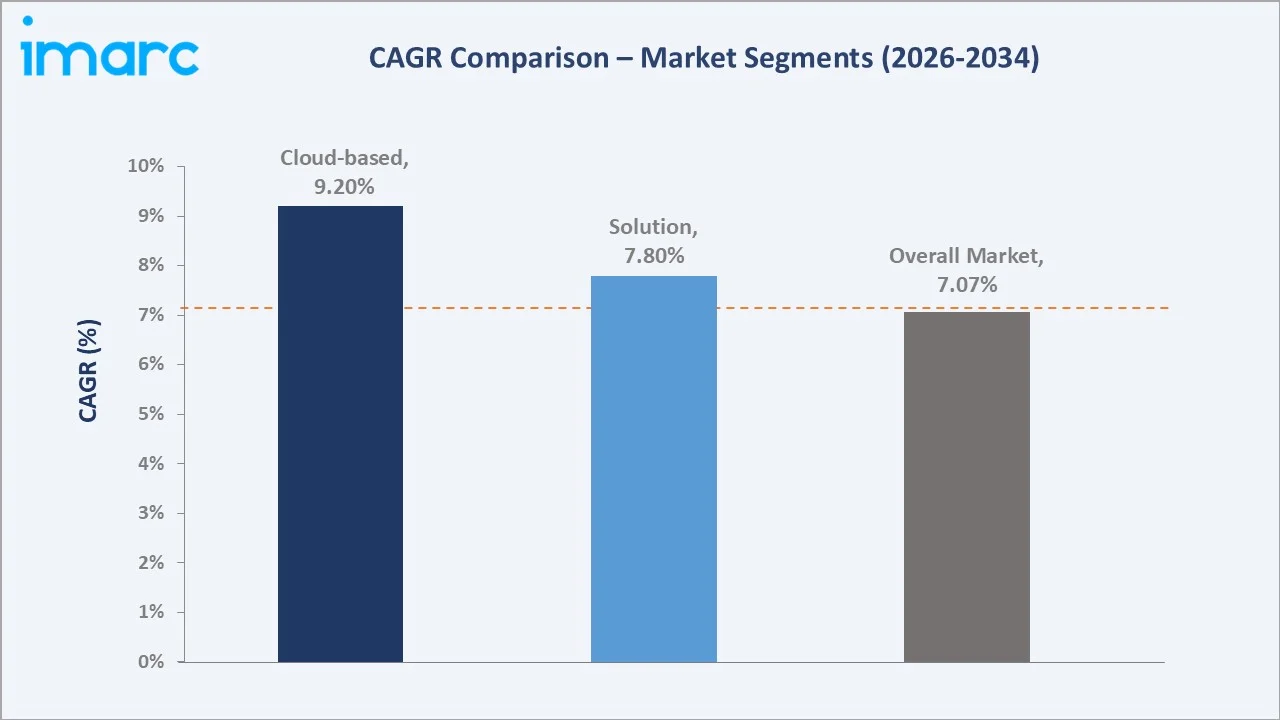

Cloud-based – ~9.2% CAGR (2026-2034) |

|

Leading Region |

North America – 36.8% share (2025) |

|

Top Companies |

Siemens AG, IBM Corporation, Robert Bosch GmbH, SAP SE, Amano Corporation |

Key Analytical Observations Supporting The Above Data:

- Solution at 67.8% (2025) leads as parking management software, encompassing PARCS, parking guidance systems (PGS), reservation platforms, permit management, and enforcement systems, represents the primary revenue category. These solutions generate recurring software license, SaaS subscription, and analytics revenue that exceeds hardware revenue in technology-mature markets.

- On-premises at 58.6% (2025) reflects the large installed base of existing on-premises PARCS infrastructure at airports, hospitals, and municipalities that were originally deployed under capital expenditure models. Many of these systems are being upgraded rather than replaced, sustaining on-premises revenue while cloud adoption accelerates in greenfield deployments.

- Cloud-based deployment accounts for 41.4% (2025), driven by new installations’ preference for SaaS parking management that offers lower upfront cost, real-time multi-site visibility, OTA updates, and integration with mobile payment and navigation platforms through open APIs.

- North America’s 36.8% share (2025) reflects the region’s combination of the highest vehicle ownership rates among major regions, the most mature smart parking technology ecosystem, and the largest concentration of airports, commercial real estate portfolios, and university campuses representing the highest-value parking management end-user segments.

Parking Management Market Overview

Parking management encompasses the technologies, systems, and services used to optimize parking space utilization, automate parking access and revenue collection, guide drivers to available spaces, enable digital payment and reservation, and provide operational analytics for parking operators. The global market spans hardware (sensors, cameras, barrier gates, payment terminals, LPR systems), software (PARCS, PGS, reservation management, enforcement, and analytics platforms), and professional services (system integration, consulting, maintenance, and managed services).

Macroeconomic drivers include the UN projecting 68% of the global population living in urban areas by 2050, creating sustained pressure on urban parking infrastructure; global smart city investment projected to exceed USD 2.5 trillion through 2030; and India's target of achieving a 30% EV share in total vehicle sales by 2030 (NITI Aayog). These macro forces ensure that the addressable market for parking management solutions continues to expand independently of economic cycles.

Market Dynamics

To evaluate market opportunities, Request Sample

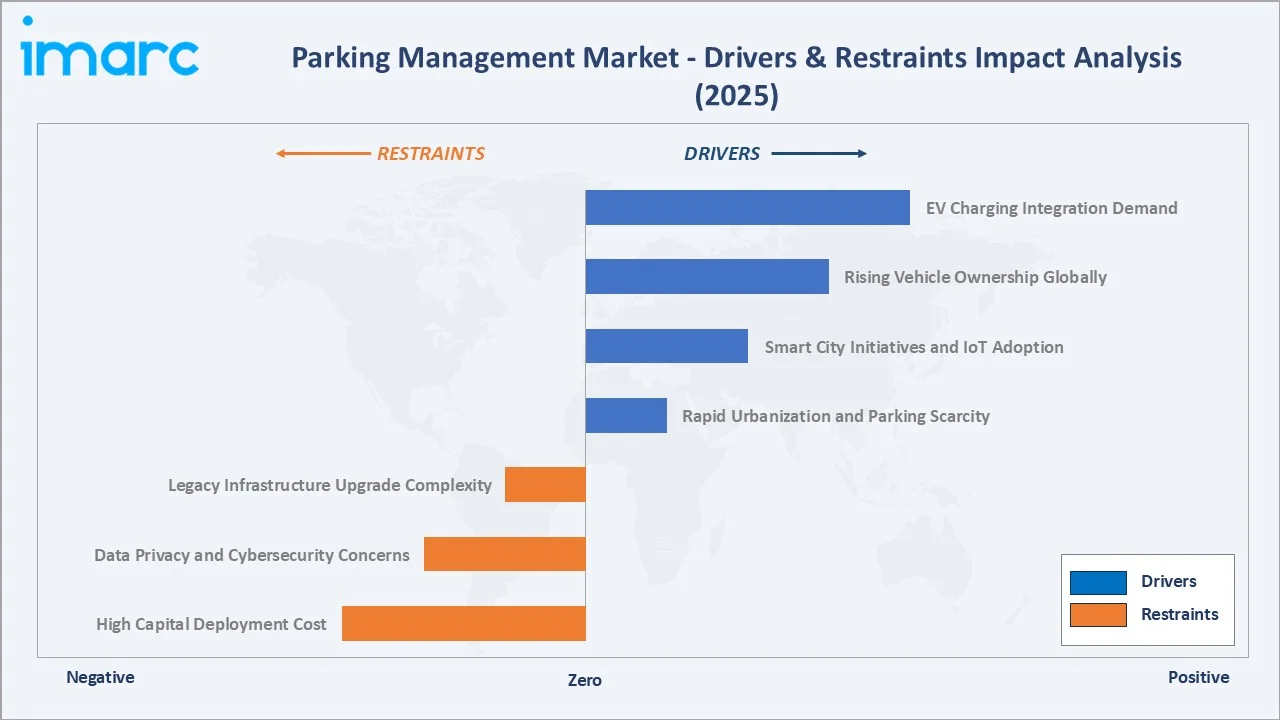

Market Drivers

- Rapid Urbanization and Parking Scarcity: The global population living in urban areas is projected to rise to 68% by 2050, increasing pressure on the finite urban parking supply. Intelligent parking management systems directly address this scarcity by optimizing space utilization, reducing search time by 30–70%, and enabling dynamic pricing that balances demand across available supply.

- Smart City Initiatives and IoT Adoption: Smart city programs in North America, Europe, and Asia-Pacific are deploying IoT-connected parking sensors, smart meters, variable messaging signs, and mobile parking applications as foundational urban intelligence infrastructure. These programs create large-scale government procurement for connected parking management systems.

- Rising Vehicle Ownership Globally: Worldwide registrations in 2025 increased by 3.5% to 77.6 million units, supported by a 5.5% rise in China, where rising middle-class incomes are driving first-time vehicle purchases. This growth in vehicle population directly expands the demand for both physical parking infrastructure and the management systems required to operate it efficiently, creating sustained greenfield market demand in emerging urban centers.

- EV Charging Integration Demand: The global EV transition is compelling parking operators to integrate EV charging management with parking payment and reservation systems, creating new technology upgrade demand across airports, commercial real estate, and municipal parking facilities. integrated EV and parking management platforms that combine parking payment, session management, and charging billing into a unified operator console represent the highest-growth product category within the solutions segment.

Market Restraints

- High Capital Deployment Cost: Comprehensive smart parking system deployments require substantial capital investment that creates adoption barriers for smaller municipal operators and private parking operators without access to technology financing or PPP funding structures. The payback period for full smart parking deployments can range from 3–7 years, extending procurement decision cycles.

- Data Privacy and Cybersecurity Concerns: Parking management systems increasingly collect sensitive personal data, including license plate numbers, payment information, location data, and movement patterns. GDPR in Europe, CCPA in California, and emerging data protection frameworks globally impose significant compliance obligations that increase system complexity and create liability risk for operators, particularly for LPR-based enforcement and mobile-integrated payment systems.

- Legacy Infrastructure Upgrade Complexity: Large parking facilities, including airports, hospitals, and municipal garages, operate legacy PARCS infrastructure with 10–20+ year lifespans that is expensive and disruptive to replace. System migration from legacy on-premises to cloud or hybrid architectures requires careful change management, downtime minimization, and staff retraining, constraining the speed of technology transition in established high-volume parking operations.

Market Opportunities

- Cloud-Native SaaS Parking Management: The transition from on-premises capital expenditure models to cloud-native SaaS parking management subscriptions is creating a structural revenue model shift that expands the addressable market. SaaS delivery reduces the upfront cost barrier for smaller operators, enables multi-site management from a single platform, and provides operators with continuous feature updates and AI analytics.

- Autonomous Vehicle Valet Parking: The anticipated commercialization of autonomous vehicle valet parking by 2027–2030 represents a transformative new application for parking management technology. AV valet systems require real-time communication between vehicle guidance software, space allocation algorithms, and facility management systems, creating a new high-value technology category within the parking management market.

Market Challenges

- Fragmented Technology Standards and Interoperability: The parking management market lacks universal interoperability standards, resulting in proprietary system ecosystems that create vendor lock-in, limit third-party integration, and complicate multi-vendor site upgrades. Proprietary ecosystems from SKIDATA and Amano create switching barriers that slow competitive disruption and increase the total cost of ownership for operators managing multi-vendor facility portfolios.

- Balancing Revenue Maximization and Public Access: Municipal parking operators face competing pressures: maximizing parking revenue through dynamic pricing versus ensuring affordable public access to city centers. Political resistance to algorithmic surge pricing in public parking facilities limits the adoption of revenue-optimizing dynamic pricing models.

Emerging Market Trends

1. AI-Powered Dynamic Pricing and Demand Prediction

AI-powered parking management platforms are enabling real-time dynamic pricing that adjusts parking rates based on real-time occupancy, time of day, local event calendars, and weather conditions. Operators deploying AI dynamic pricing report 15–25% revenue uplift and 10–20% improvements in space utilization versus fixed-rate pricing. Machine learning demand prediction models are enabling parking operators to pre-position staffing, lighting, and access systems ahead of predicted demand peaks, reducing operational cost while improving user experience.

2. License Plate Recognition as the Primary Access Credential

LPR-based frictionless entry and exit is replacing traditional ticket-based PARCS as the primary access control paradigm across high-volume airports, commercial real estate, and hospital parking facilities. LPR eliminates the ticket issuance hardware and transaction latency of barrier systems, enabling 4–8 vehicles per minute throughput versus 2–4 for traditional systems. The combination of LPR access with mobile payment pre-authorization is enabling fully contactless parking experiences that reduce transaction friction and operational cash handling costs.

3. EV Charging Management Integration

Parking operators are deploying integrated EV parking and charging management platforms that combine session management, payment, and load balancing for EV charging infrastructure within parking facilities. Integrated platforms enable dynamic allocation of EV-ready spaces, real-time charging status visibility for drivers, and utility load management compliance.

4. Cloud Migration and SaaS Subscription Transition

The parking management market is experiencing a structural transition from on-premises capital expenditure to cloud-native SaaS subscription models. New facility deployments are overwhelmingly opting for cloud-native platforms that offer real-time multi-site dashboards, mobile operator interfaces, OTA updates, and open API integrations with navigation platforms, payment processors, and smart city data exchanges. In January 2025, EasyPark Group (now Arrive) completed its acquisition of Flowbird Group, creating a global SaaS parking platform.

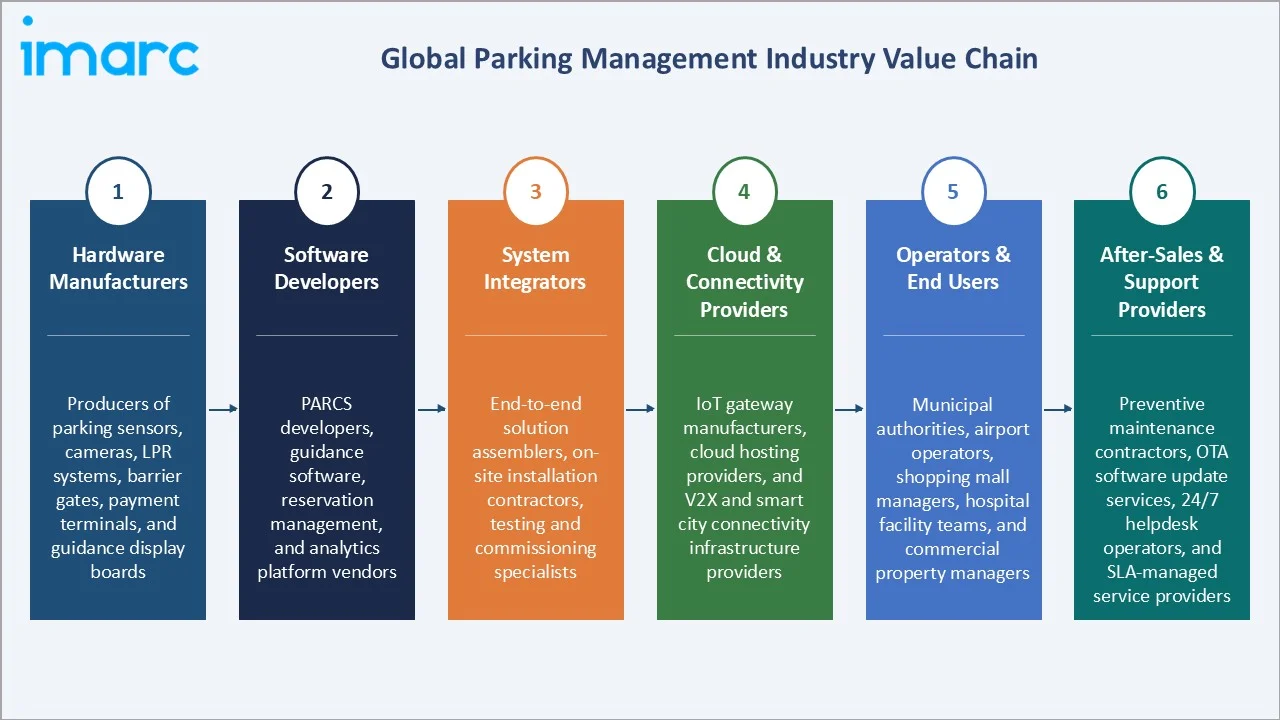

Industry Value Chain Analysis

The parking management value chain spans from hardware component manufacturing through software platform development, system integration, cloud hosting, and end-user operations across municipal, commercial, and institutional parking facilities. System integrators play a central value-add role by assembling multi-vendor hardware, proprietary software, and third-party applications into operational parking management systems tailored to specific facility types and regulatory environments.

|

Stage |

Key Players / Examples |

|

Hardware Manufacturers |

Producers of parking sensors, cameras, LPR systems, barrier gates, payment terminals, and guidance display boards |

|

Software Developers |

PARCS developers, guidance software, reservation management, and analytics platform vendors |

|

System Integrators |

End-to-end solution assemblers, on-site installation contractors, testing and commissioning specialists |

|

Cloud & Connectivity Providers |

IoT gateway manufacturers, cloud hosting providers, and V2X and smart city connectivity infrastructure providers |

|

Operators & End Users |

Municipal authorities, airport operators, shopping mall managers, hospital facility teams, and commercial property managers |

|

After-Sales & Support Providers |

Preventive maintenance contractors, OTA software update services, 24/7 helpdesk operators, and SLA-managed service providers |

Technology Landscape in the Parking Management Industry

Parking Access and Revenue Control Systems (PARCS)

PARCS remains the core technology platform for managed parking facilities, encompassing barrier gates, ticket dispensers, payment terminals, cashier workstations, and revenue management software. Modern PARCS platforms have evolved from standalone on-premises systems to cloud-connected platforms with real-time occupancy dashboards, dynamic pricing engines, mobile payment integration, and LPR-based ticketless operation.

IoT Sensor Networks and Parking Guidance Systems

Ultrasonic, magnetometer, and computer vision-based parking sensors are deployed to detect individual space occupancy in real time, feeding data to parking guidance systems that direct drivers to available spaces through variable message signage and mobile applications. IoT sensor networks for parking are evolving from single-site installations to city-wide sensor meshes that aggregate parking availability data across public and private facilities into unified real-time parking availability maps accessible through navigation apps and smart city platforms.

AI Analytics and Predictive Management Platforms

AI-powered analytics platforms are transforming parking management from reactive operations to predictive management. Machine learning models trained on historical occupancy, payment, event, and environmental data enable demand prediction, dynamic pricing, fraud detection in payment transactions, and predictive maintenance alerts for physical parking infrastructure.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Offering Type |

Solution |

67.8% |

2025 |

|

Deployment Mode |

On-premises |

58.6% |

2025 |

|

Parking Site |

Off-street |

🔒 |

2025 |

|

Region |

North America |

36.8% |

2025 |

By Offering Type

Solution leads with a 67.8% share of the global parking management market in 2025. It reflects the market’s primary revenue driver in software-centric parking management platforms, encompassing PARCS software, parking guidance systems, mobile payment platforms, permit management systems, violation enforcement platforms, and operational analytics dashboards.

To access detailed market analysis, Request Sample

Service at 32.2% of the market encompasses professional services, including system integration, implementation, customization, training, and managed services, including 24/7 helpdesk support, preventive maintenance contracts, and SLA-managed operations outsourcing. The services segment is growing steadily as operators increasingly outsource parking system operations to managed service providers rather than maintaining in-house technical teams.

By Deployment Mode

On-premises deployment leads with a 58.6% share in 2025, reflecting the large installed base of legacy PARCS infrastructure deployed over the past two decades at airports, hospitals, universities, and municipal facilities. These systems represent substantial sunk costs and operational continuity requirements that make immediate migration to cloud deployment economically and operationally impractical, sustaining on-premises revenue from maintenance, upgrade, and managed services contracts.

Cloud-based deployment accounted for 41.4% (2025) and is projected to grow at approximately 9.2% CAGR through 2034. New parking facility deployments across greenfield commercial real estate, new airport terminals, and municipal smart city programs are overwhelmingly selecting cloud-native SaaS platforms that offer lower upfront cost, real-time multi-site management, rapid feature deployment, and open API integration with mobile and smart city platforms.

Regional Market Insights

North America’s dominant position (36.8%, 2025) reflects the region’s combination of the highest vehicle ownership rates, the most mature smart city and technology-enabled parking ecosystem, the largest concentration of airports and commercial real estate parking operations, and early adoption of cloud-native parking management platforms.

Asia-Pacific at 29.7% is the fastest-growing region, driven by China’s massive smart city program deploying connected parking infrastructure across 500+ pilot smart cities, India’s Smart Cities Mission funding urban parking technology, and Japan and South Korea’s advanced automated multi-story parking system markets.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.8% |

Strong smart city investment, high vehicle ownership, mature parking technology ecosystem, leading EV charging integration, and established municipal digital transformation programs |

|

Asia-Pacific |

29.7% |

Rapid urbanization, rising vehicle ownership, large-scale smart city deployments, growing middle-class consumer mobility demand, and government-led urban infrastructure modernization |

|

Europe |

21.5% |

Stringent urban mobility regulations, strong sustainability policy frameworks, growing demand for contactless and mobile parking solutions, and established multi-modal urban transport integration |

|

Latin America |

6.5% |

Rapid urban population growth, increasing vehicle penetration, growing private parking infrastructure investment, and rising mobile payment adoption, enabling digital parking management |

|

Middle East and Africa |

5.5% |

Smart city flagship projects, high-income urban mobility demand, growing real estate and commercial parking infrastructure investment, and government digital transformation initiatives |

Europe’s 21.5% share (2025) benefits from strong regulatory drivers, including urban access restriction zones (ULEZ, LEZ), creating demand for integrated parking and access management. Latin America at 6.5% and the Middle East and Africa at 5.5% are growing markets driven by rapid urbanization and smart city investment in Dubai, Riyadh, and NEOM.

Competitive Landscape

The global parking management market exhibits moderate concentration at the enterprise platform tier, with large technology companies competing alongside specialist parking technology providers.

|

Company Name |

Products/Solutions |

Market Position |

Core Strength |

|

Siemens AG |

Desigo CC |

Market Leader |

Smart city ecosystem integration, large-scale municipal deployments, and end-to-end urban mobility platform capability |

|

IBM Corporation |

IBM Intelligent Operations Center, Enterprise Hybrid Cloud Platform |

Market Leader |

AI analytics, cloud-native architecture, and deep enterprise and government sector relationships |

|

Robert Bosch GmbH |

Connected Mobility |

Strong Challenger |

Hardware-software integration capability, large IoT sensor portfolio, and automotive ecosystem connectivity |

|

SAP SE |

SAP Real Estate and Facilities Management Solution |

Strong Challenger |

Enterprise ERP integration, a large commercial real estate customer base, and a data analytics platform depth |

|

Amano Corporation |

Ticketless LPR, Parking System, Parking Facility Data Center Services, Bicycle Parking System, Security Gate Systems, Toll road systems, Commissioned Management Service, Amano ONE |

Challenger |

Comprehensive PARCS hardware-software portfolio, strong operator relationships, and multi-venue deployment experience |

The combined revenue of the top players accounts for approximately 40–50% of global market revenues in 2025, with a fragmented mid-market of regional and specialist providers serving the remainder. The competitive landscape is evolving as cloud-native SaaS parking platforms challenge incumbent on-premises PARCS vendors.

Key Company Profiles

Siemens AG

Siemens AG is one of the world's leading global technology conglomerates and one of the leading providers of integrated parking management solutions as part of its broader smart infrastructure and urban traffic management portfolio.

- Product Portfolio: Desigo CC (building management platform with third-party parking integration capability), and smart city mobility integration platforms.

- Strategic Focus: Smart city platform integration for unified urban mobility management; EV charging management integration with parking systems; public-private partnership model for municipal smart parking deployment.

IBM Corporation

IBM Corporation’s parking management offering is distinguished by its AI-powered analytics, predictive maintenance, and enterprise integration capabilities that serve large-scale operators requiring enterprise-grade data management and intelligent decision support.

- Product Portfolio: IBM Watsonx, IBM Maximo Application Suite, and IBM Intelligent Operations Center (IOC).

- Strategic Focus: AI-native parking analytics for predictive management; hybrid cloud deployment for enterprise and municipal operators; integration with broader smart city and transit data ecosystems.

Amano Corporation

Amano Corporation is one of the world’s leading parking system manufacturers, providing comprehensive PARCS hardware and software solutions that serve airports, commercial real estate, transit hubs, and municipal operators across global markets through its international subsidiaries.

- Product Portfolio: Ticketless LPR, Parking System, Parking Facility Data Center Services, Bicycle Parking System, Security Gate Systems, Toll road systems, Commissioned Management Service, and Amano ONE.

- Recent Developments: In June 2024, Amano McGann, Inc. integrated Amano ONE with ParkChirp, enabling users to reserve, pre-pay, and sign up for monthly parking through the ParkChirp app. Parkers can enter Amano ONE-equipped garages by scanning a QR code, improving convenience and parking management efficiency.

- Strategic Focus: Cloud connectivity for legacy PARCS installed base; LPR-based frictionless parking experience; EV charging management integration for multi-level parking facilities.

Market Concentration Analysis

The global parking management market exhibits moderate concentration, with enterprise technology companies and specialist parking technology providers collectively representing approximately 40–50% of global market revenues. The remaining market is distributed across regional specialists, municipal systems integrators, and a growing tier of cloud-native SaaS parking platforms that are collectively disrupting the incumbent hardware-centric market structure.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud-based parking management (~9.2% CAGR), EV-integrated parking and charging platforms (~12% annual growth), and AI-powered dynamic pricing and analytics modules represent the highest-growth investment vectors within the parking management market through 2034. Mobile-first parking platforms combining guidance, reservation, payment, and enforcement in unified consumer applications are growing at above-market rates as digital mobility consumer expectations migrate from hardware-centric to app-centric parking experiences.

Emerging Market Expansion

India, Indonesia, Vietnam, and Sub-Saharan African cities represent significant greenfield smart parking market opportunities as rapid urban vehicle population growth outpaces parking supply expansion. Entry strategies for parking management providers in these markets include SaaS-based cloud parking platforms requiring minimal upfront hardware investment, mobile payment integration with dominant local fintech platforms, and public-private partnership structures with municipal authorities seeking parking revenue optimization.

Technology Investment Trends

- AI-powered demand prediction and dynamic pricing platform investment is attracting both incumbent parking technology company R&D and venture-backed startup competition, with AI pricing engine providers reporting 15–25% revenue uplift for operators adopting algorithmic versus fixed-rate pricing structures.

- Autonomous vehicle valet parking technology development represents a longer-term structural investment theme, with major parking operators and automotive OEMs co-investing in AV-ready parking facility design and management system integration for 2028–2034 commercial deployment.

Future Market Outlook (2026-2034)

The global parking management market is positioned for sustained growth through 2034. From USD 5.53 Billion in 2025, the market is projected to reach USD 10.43 Billion by 2034, representing total incremental value creation of USD 4.90 Billion at a CAGR of 7.07%.

This growth is underpinned by urbanization-driven parking scarcity that is a long-term demographic certainty, the smart city investment cycle sustaining IoT and connected infrastructure deployment, and the EV transition creating new technology upgrade requirements across all parking asset categories.

The market’s revenue composition will shift progressively toward software and services and away from hardware, as SaaS parking management subscriptions replace capital equipment purchases as the primary commercial model. Cloud-based deployment is projected to approach or exceed the on-premises share by 2034, and the recurring revenue characteristics of cloud SaaS parking management will attract premium valuation multiples that sustain continued private equity and strategic investor interest in parking management platform consolidation.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including parking management software vendors, system integrators, municipal parking authority executives, airport parking operations managers, commercial real estate parking directors, and smart city technology advisors. Expert input validated market sizing, segment growth rates, and regional penetration estimates.

Secondary Research

Secondary research encompassed parking management company annual reports and investor presentations, Smart Cities World and Intelligent Transportation Society publications, International Parking and Mobility Institute (IPMI) industry statistics, US Department of Transportation ITS deployment data, European Commission urban mobility policy publications, and industry media, including Parking Today, Parknews, and Smart City Dive.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating global managed parking facility count data, average system revenue per facility benchmarks by facility type and geography, deployment mode transition rate modelling, and end-user segment capex and opex budget trend analysis. The base-case CAGR of 7.07% reflects consensus estimates validated against operator procurement budget disclosures and smart city program investment schedules for 2026–2034.

Parking Management Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Parking Management Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Offering Types Covered |

|

| Deployment Modes Covered | On-Premises, Cloud-Based |

| Parking Sites Covered | Off-Street, On-Street |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Siemens AG, IBM Corporation, Robert Bosch GmbH, SAP SE, Amano Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, parking management market forecasts, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global parking management market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the parking management industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides parking management market insights into the current positions of key players in the market.

Frequently Asked Questions About the Parking Management Market Report

The global parking management market reached USD 5.53 Billion in 2025 and is projected to reach USD 10.43 Billion by 2034.

The market is expected to grow at a CAGR of 7.07% during 2026-2034, driven by urbanization-driven parking scarcity, smart city IoT investment, EV charging integration, and cloud-native SaaS platform adoption.

North America leads with a 36.8% share in 2025, driven by high vehicle ownership, mature smart parking technology infrastructure, large commercial real estate and airport parking sectors, and early adoption of cloud and AI-powered parking management platforms.

Solution leads with a 67.8% share in 2025, encompassing PARCS software, parking guidance systems, mobile payment platforms, permit management, enforcement systems, and operational analytics dashboards as the primary revenue category.

On-premises holds a 58.6% share in 2025, reflecting the large installed base of legacy PARCS infrastructure at airports, hospitals, and municipalities deployed under capital expenditure models over the past two decades.

Some of the key players include Siemens AG, IBM Corporation, Robert Bosch GmbH, SAP SE, and Amano Corporation.

Key drivers include rapid urbanization creating parking scarcity, smart city IoT infrastructure investment, rising global vehicle ownership, and the transition to cloud-native SaaS parking management, reducing operational barriers.

Key opportunities include cloud-native SaaS parking management platforms, EV charging integrated parking systems, AI-powered dynamic pricing engines, and MaaS platform integration enabling unified urban mobility journey management.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)