Peptic Ulcer Drugs Market by Product Type (Proton Pump Inhibitors, Potassium-Competitive Acid Blocker (P-CAB), Antacids, H2-Antagonists, Antibiotics, Ulcer protective), Ulcer Type (Gastric Ulcer, Duodenal Ulcer, and Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Region 2026-2034

Global Peptic Ulcer Drugs Market:

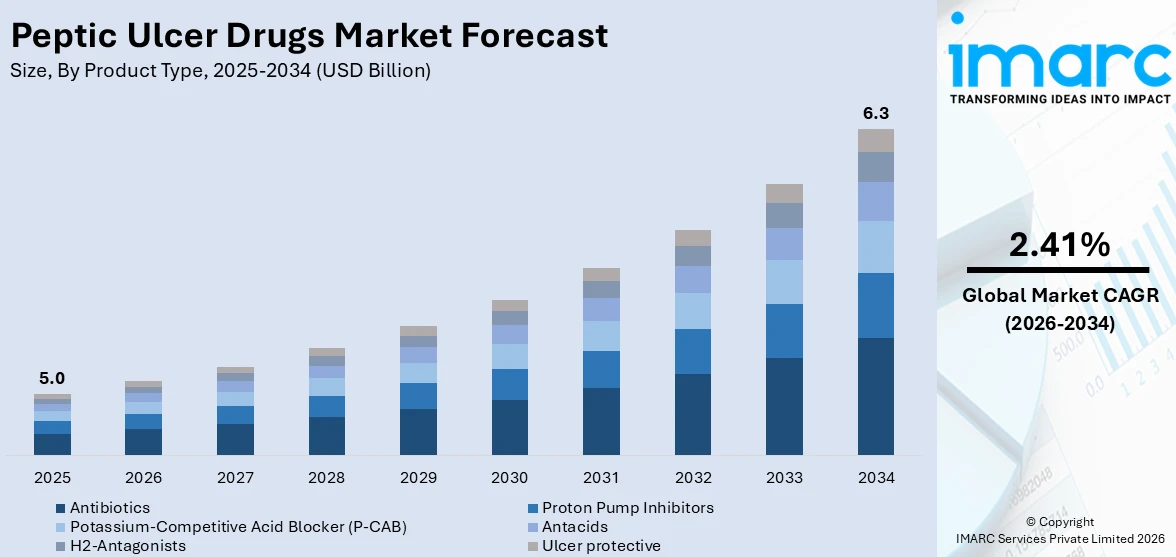

The global peptic ulcer drugs market size reached USD 5.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 6.3 Billion by 2034, exhibiting a growth rate (CAGR) of 2.41% during 2026-2034. The increasing prevalence of peptic ulcers, especially amongst the geriatric population and shifting consumer inclination toward various medications over invasive surgeries represent some of the key factors driving the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 5.0 Billion |

| Market Forecast in 2034 | USD 6.3 Billion |

| Market Growth Rate 2026-2034 | 2.41% |

Peptic Ulcer Drugs Market Analysis:

- Major Market Drivers: The increasing prevalence of peptic ulcers, especially amongst the geriatric population, represents one of the key factors driving the market growth. Moreover, unhealthy lifestyle habits and rising instances of stomach cancer are resulting in a growing number of individuals suffering from peptic ulcers. This, along with the shifting consumer inclination towards various peptic ulcer-curing drugs over invasive surgeries, in turn, is contributing to the peptic ulcer drugs market share.

- Key Market Trends: The ongoing approvals of peptic ulcer drugs and several government investments in pharmaceutical companies for the formulation of medications are supporting the market growth. Additionally, extensive research and development (R&D) activities to enhance product efficacy and the increasing investments in the development of the over-the-counter (OTC) medications for treating peptic ulcers, are positively impacting the peptic ulcer drugs market growth.

- Competitive Landscape: Some of the prominent peptic ulcer drugs market companies include Abbott Laboratories, AstraZeneca plc, Boehringer Ingelheim International GmbH, Novitium Pharma LLC, Pfizer Inc., PharmaKing Co. Ltd., RedHill Biopharma Ltd, Viatris Inc., Yuhan Corporation, and Zydus Lifesciences Limited, among many others.

- Geographical Trends: According to the peptic ulcer drugs market dynamics, North America dominates the overall market. Peptic ulcer disease (PUD) has become increasingly prevalent in North America due to lifestyle factors such as poor dietary habits, stress, smoking, and alcohol consumption. The growing number of people affected by PUD is driving demand for treatments, including proton pump inhibitors (PPIs), antacids, and antibiotics.

- Challenges and Opportunities: The high competition among key players and the rising concerns over long-term PPI use are hampering the market's growth. However, there is increasing consumer demand for OTC treatments to manage the symptoms of peptic ulcers and gastroesophageal reflux disease (GERD), such as antacids, H2-receptor blockers, and PPIs.

To get more information on this market Request Sample

Peptic Ulcer Drugs Market Trends:

Aging Population

There has been a significant increase in the geriatric population. For instance, according to the World Health Organization (WHO), by 2030, one in every six persons in the world will be 60 or older. At this time, the proportion of the population aged 60 and up will rise from 1 billion in 2020 to 1.4 billion. By 2050, the global population of persons aged 60 and up will double (2.1 billion). The number of people aged 80 and older is anticipated to treble between 2020 and 2050, reaching 426 million. The global aging population is more susceptible to peptic ulcers, especially due to the increased use of NSAIDs and the weakening of the gastrointestinal lining in elderly individuals. This demographic shift is expected to drive demand for medications that treat or manage peptic ulcers. These factors further positively influence the peptic ulcer drugs market share.

Rising Incidence of Peptic Ulcers

The rising incidence of peptic ulcers, largely due to factors such as infection with Helicobacter pylori and the widespread use of nonsteroidal anti-inflammatory drugs (NSAIDs), is a major driver for the demand for peptic ulcer drugs. For instance, according to an article published by the National Library of Medicine, peptic ulcer disease (PUD) affects four million individuals worldwide each year, with a lifetime prevalence of 5- 10% in the general population. These factors are expected to propel the peptic ulcer drugs market share in the coming years.

Technological Advancements in Drug Development

Advances in pharmaceutical research have led to the development of more effective peptic ulcer medications, including next-generation PPIs, combination therapies, and antibiotics with fewer side effects. For instance, in September 2024, Jeil Pharmaceutical released Jaqbo (zastaprazan citrate), a novel potassium-competitive acid blocker (P-CAB) that will enter Korea's peptic ulcer medicine market, thereby boosting the peptic ulcer drugs market growth.

Global Peptic Ulcer Drugs Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global peptic ulcer drugs market, along with forecasts at the global, regional, and country levels from 2026-2034. Our report has categorized the market based on product type, ulcer type, and distribution channel.

Breakup by Product Type:

- Proton Pump Inhibitors

- Potassium-Competitive Acid Blocker (P-CAB)

- Antacids

- H2-Antagonists

- Antibiotics

- Ulcer protective

Antibiotics represented the largest segment

The report has also provided a detailed breakup and analysis of the peptic ulcer drugs market based on the product type. This includes proton pump inhibitors, potassium-competitive acid blocker (P-CAB), antacids, H2-antagonists, antibiotics, and ulcer protective. According to the report, antibiotics represented the largest segment.

According to the peptic ulcer drugs market outlook, h. pylori infection is the primary cause of peptic ulcers, responsible for the majority of cases globally. Antibiotics are a critical component of combination therapy used to eradicate infection and prevent the recurrence of ulcers.

Breakup by Ulcer Type:

- Gastric Ulcer

- Duodenal Ulcer

- Others

Duodenal ulcer accounted for the largest market share

A detailed breakup and analysis of the peptic ulcer drugs market based on the ulcer type has also been provided in the report. This includes gastric ulcer, duodenal ulcer, and others. According to the report, duodenal ulcer accounted for the largest market share.

According to the peptic ulcer drugs market overview, diets high in spicy foods, alcohol, and caffeine are risk factors for developing duodenal ulcers. As fast-food consumption and alcohol use rise globally, the incidence of duodenal ulcers and demand for related treatments grow. Moreover, as public awareness of gastrointestinal health issues improves and access to healthcare grows, more individuals seek diagnosis and treatment for ulcers, driving up the demand for medical services and drugs.

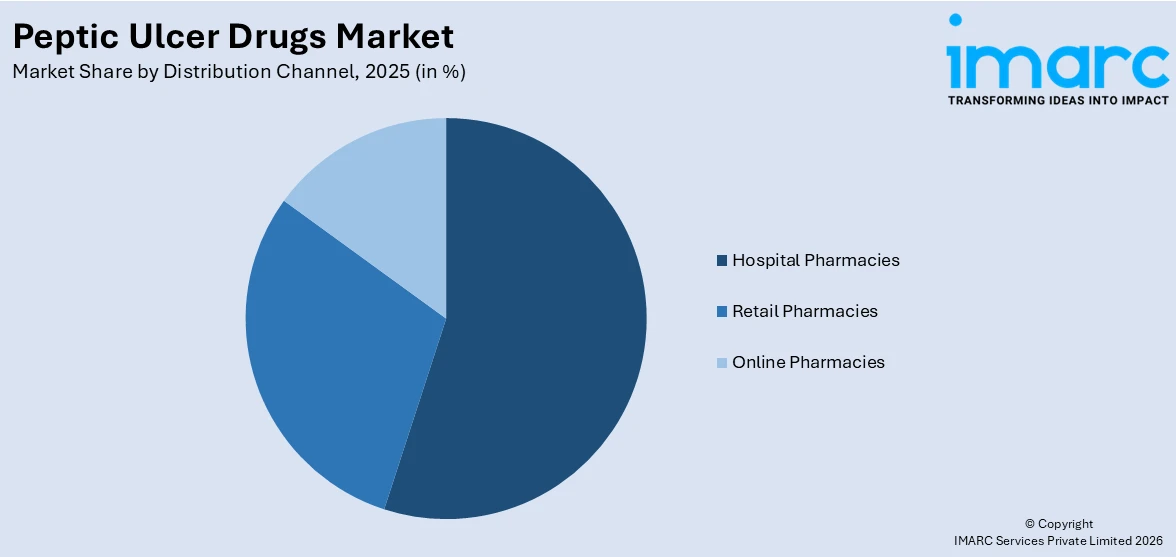

Breakup by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Hospital pharmacies represented the largest segment

The report has also provided a detailed breakup and analysis of the peptic ulcer drugs market based on the distribution channel. This includes hospital, retail, and online pharmacies. According to the report, hospital pharmacies represented the largest segment.

The aging population is more prone to gastrointestinal disorders, including peptic ulcers, due to weakened gastric mucosa, higher use of NSAIDs, and comorbid conditions. This increases hospital admissions for ulcer-related complications and subsequently drives demand for ulcer drugs in hospital pharmacies. Moreover, hospitals often administer peptic ulcer drugs prophylactically to patients at risk for stress-related mucosal disease, such as those in intensive care units (ICUs), patients undergoing surgery, or those with mechanical ventilation. This drives demand for intravenous formulations of ulcer medications.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America was the largest market for peptic ulcer drugs

The report has also provided a comprehensive analysis of all the major regional markets that include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and Middle East and Africa. According to the report, North America was the largest market for peptic ulcer drugs.

According to the peptic ulcer drugs market statistics, some of the factors driving the North America peptic ulcer drugs market included the increasing prevalence of peptic ulcers, especially amongst the geriatric population, and shifting consumer inclination toward various peptic ulcer curing drugs over invasive surgeries and the fueling need for over the counter (OTC) medications in the healthcare sector. There has been a significant increase in peptic ulcers. For instance, peptic ulcer disease (PUD) is a widespread ailment that affects more than six million people in the United States annually. These factors are further propelling the peptic ulcer drugs market size.

Competitive Landscape:

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major market companies have also been provided. Some of the key players in the market include:

- Abbott Laboratories

- AstraZeneca plc

- Boehringer Ingelheim International GmbH

- Novitium Pharma LLC

- Pfizer Inc.

- PharmaKing Co. Ltd.

- RedHill Biopharma Ltd

- Viatris Inc.

- Yuhan Corporation

- Zydus Lifesciences Limited

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Peptic Ulcer Drugs Market Recent Developments:

- September 2024: HK inno.N announced that its new drug for gastroesophageal reflux disease and peptic ulcer, "K-CAB" received approval in six Latin American countries.

- September 2024: Jeil Pharmaceutical released Jaqbo (zastaprazan citrate), a novel potassium-competitive acid blocker (P-CAB) that will enter Korea's peptic ulcer medicine market.

- June 2024: Mankind Pharma and Takeda Pharmaceutical Company Limited signed a non-exclusive patent license agreement to commercialize 'Vonoprazan' in the Indian market. The deal permits Mankind Pharma to market a unique medicine for treating Gastroesophageal Reflux Disease (GERD) under its trademark. The medication is beneficial in treating duodenal and peptic ulcers.

Peptic Ulcer Drugs Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Proton Pump Inhibitors, Potassium-Competitive Acid Blocker (P-CAB), Antacids, H2-Antagonists, Antibiotics, Ulcer protective |

| Ulcer Types Covered | Gastric Ulcer, Duodenal Ulcer, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, AstraZeneca plc, Boehringer Ingelheim International GmbH, Novitium Pharma LLC, Pfizer Inc., PharmaKing Co. Ltd., RedHill Biopharma Ltd, Viatris Inc., Yuhan Corporation, Zydus Lifesciences Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the peptic ulcer drugs market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global peptic ulcer drugs market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the peptic ulcer drugs industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Peptic Ulcer Drugs Market Report

The peptic ulcer drugs market was valued at USD 5.0 Billion in 2025.

The peptic ulcer drugs market is projected to exhibit a CAGR of 2.41% during 2026-2034.

The peptic ulcer drugs market is driven by increasing prevalence of gastrointestinal disorders, aging populations, and rising stress levels. Additionally, the growing awareness about treatment options, advancements in drug formulations, and the demand for effective therapies to manage ulcer-related symptoms are propelling market growth.

North America currently dominates the market driven by the increasing prevalence of peptic ulcers, especially amongst the geriatric population, and shifting consumer inclination toward various peptic ulcer curing drugs over invasive surgeries and the fueling need for over the counter (OTC) medications in the healthcare sector.

Some of the major players in the peptic ulcer drugs market include Abbott Laboratories, AstraZeneca plc, Boehringer Ingelheim International GmbH, Novitium Pharma LLC, Pfizer Inc., PharmaKing Co. Ltd., RedHill Biopharma Ltd, Viatris Inc., Yuhan Corporation, Zydus Lifesciences Limited, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)