Personal Protective Equipment Market Size, Share, Trends and Forecast by Equipment Type, End Use Industry, and Region, 2026-2034

Global Personal Protective Equipment (PPE) Market Size, Share, Trends & Forecast (2026-2034)

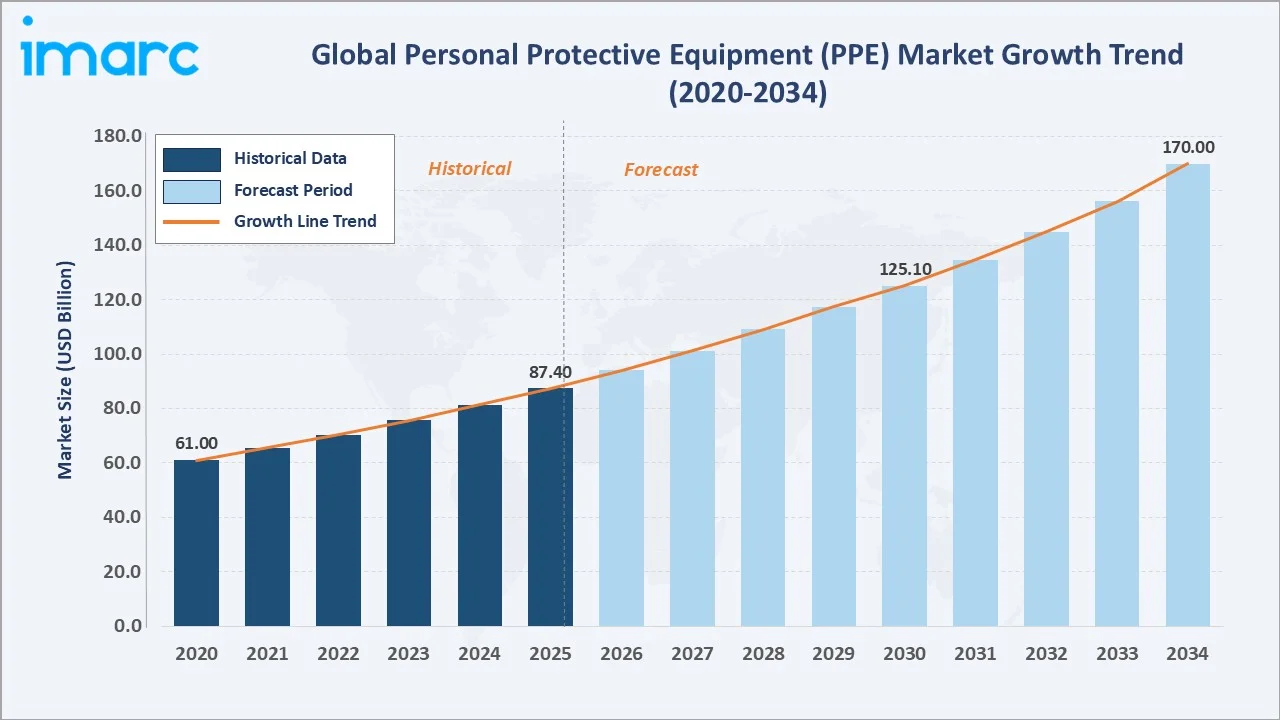

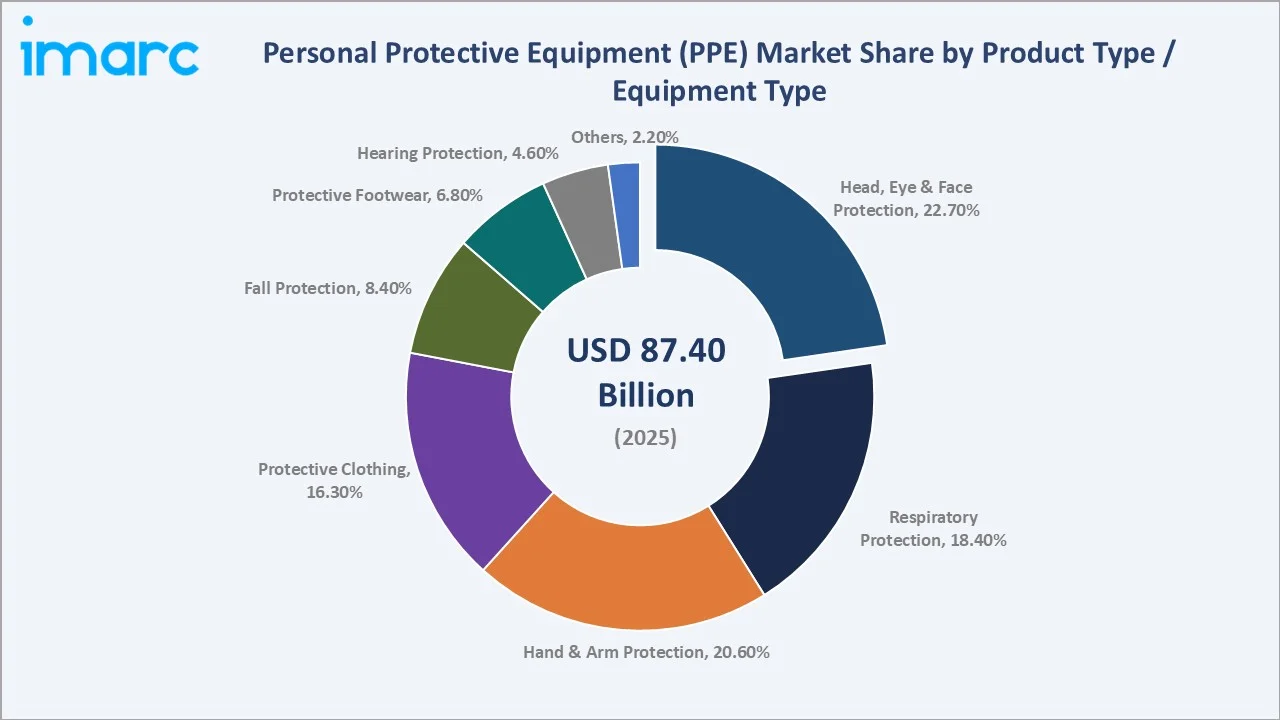

The global personal protective equipment (PPE) market was valued at USD 87.4 Billion in 2025. It is projected to reach USD 170.0 Billion by 2034, growing at a CAGR of 7.45%, driven by stringent safety regulations and global industrial expansion.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 87.4 Billion |

|

Forecast Market Size (2034) |

USD 170.0 Billion |

|

CAGR (2026-2034) |

7.45% |

|

Largest Region (2025) |

Europe (30.3%) |

|

Fastest Growing Region |

Middle East & Africa |

|

Leading Equipment Type (2025) |

Head, Eye & Face Protection (22.7%) |

|

Leading End Use Industry (2025) |

Oil and Gas (16.7%) |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

To get more information on this market, Request Sample

Executive Summary

The global PPE market reached USD 87.4 Billion in 2025, propelled by stringent workplace safety regulations, expanding heavy industries, and rising occupational hazard awareness. It is forecast to reach USD 170.0 Billion by 2034 at a CAGR of 7.45%.

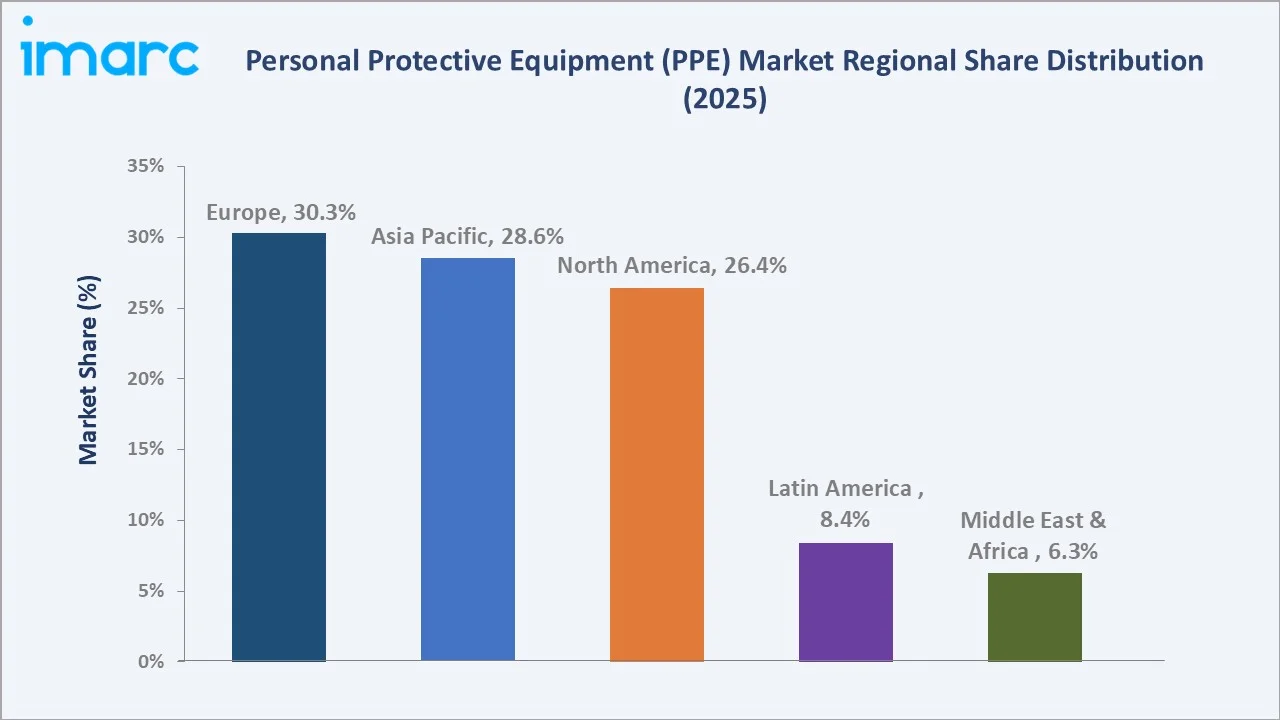

Europe commands a 30.3% revenue share in 2025, anchored by Regulation (EU) 2016/425 and strong industrial demand across construction, manufacturing, oil and gas, and healthcare sectors across member states.

Head, Eye and Face Protection leads the equipment type segment at 22.7% share. Oil and Gas dominates end use at 16.7%, driven by high-risk operational environments requiring comprehensive safety compliance programs globally.

Key market consolidation events include PIP's USD 1.325 billion acquisition of Honeywell's PPE business (May 2025) and Ansell's USD 640 million takeover of Kimberly-Clark's PPE unit (July 2024), reshaping the competitive hierarchy.

Technology leadership is defined by smart PPE integration, nano-enhanced materials, and sustainable product design. 3M, DuPont, MSA Safety, and Ansell remain the dominant innovation drivers across all major equipment categories globally.

Key Market Insights

|

Insight |

Data |

|

Largest Equipment Type |

Head, Eye & Face Protection – 22.7% (2025) |

|

Largest End Use Industry |

Oil and Gas – 16.7% (2025) |

|

Leading Region |

Europe – 30.3% (2025) |

|

Fastest Growing Region |

Middle East & Africa |

|

Top Companies |

3M, DuPont, Ansell, MSA Safety, PIP Inc. |

Key Analytical Observations:

- Head, Eye & Face Protection's 22.7% share reflects its status as the universal safety baseline mandated across virtually every high-risk industry and country-level regulatory framework globally.

- Oil and Gas dominates end use at 16.7% due to complex upstream and downstream hazard profiles requiring comprehensive head-to-toe PPE programs under stringent international safety standards.

- Europe's 30.3% leadership stems from the world's most rigorous occupational health regulations, a diverse industrial base, and mandated compliance across all PPE categories under EU law.

- Market consolidation via PIP-Honeywell and Ansell-Kimberly-Clark transactions signals strategic scaling among top players, with innovation and sustainability now central to premium market positioning globally.

Market Overview

Personal protective equipment encompasses certified devices and apparel designed to protect workers from physical, chemical, biological, and thermal workplace hazards. Core categories include head protection, respiratory equipment, gloves, protective clothing, safety footwear, fall protection systems, and hearing devices.

Global PPE demand is anchored by mandatory compliance across construction, oil and gas, manufacturing, healthcare, and mining. Regulatory bodies including OSHA and the European Agency for Safety and Health at Work establish and enforce minimum PPE usage standards across high-hazard industries worldwide.

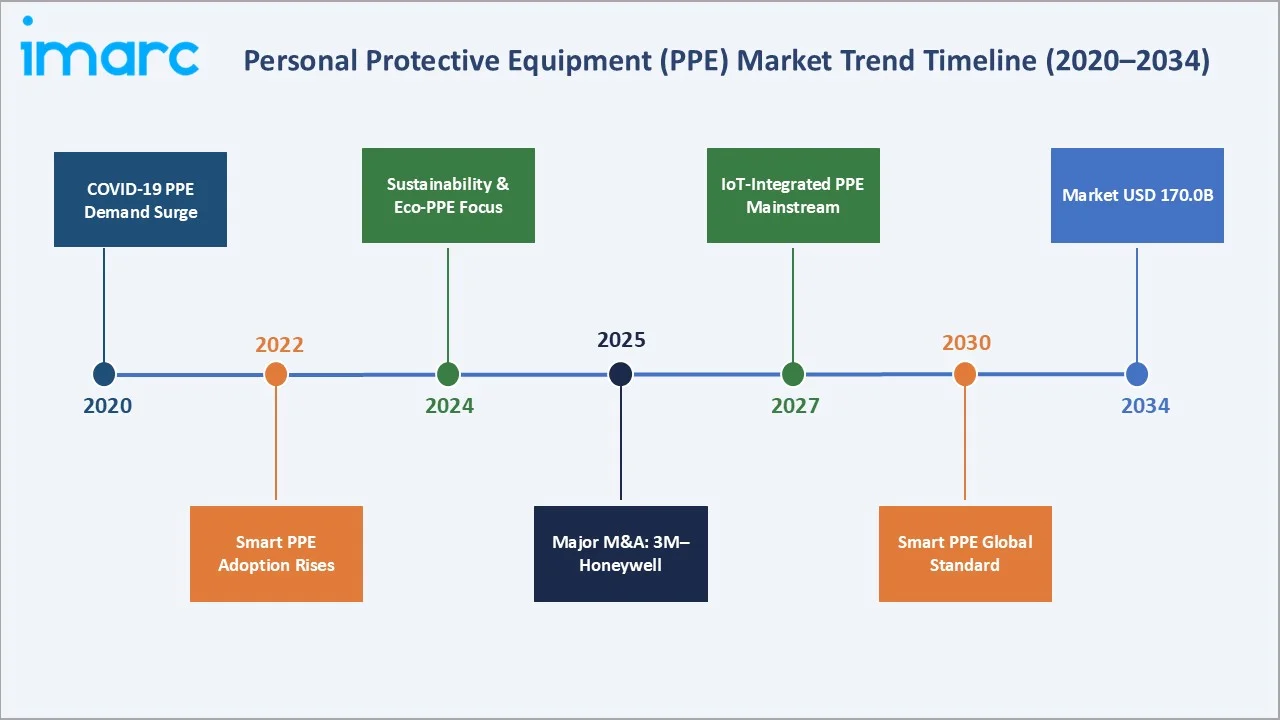

The COVID-19 pandemic dramatically amplified PPE awareness, expanding demand beyond traditional industrial users into healthcare and logistics sectors. Post-pandemic, the market consolidated around industrial and institutional demand, supported by permanently elevated safety culture and compliance consciousness globally.

Market Dynamics

To evaluate market opportunities, Request Sample

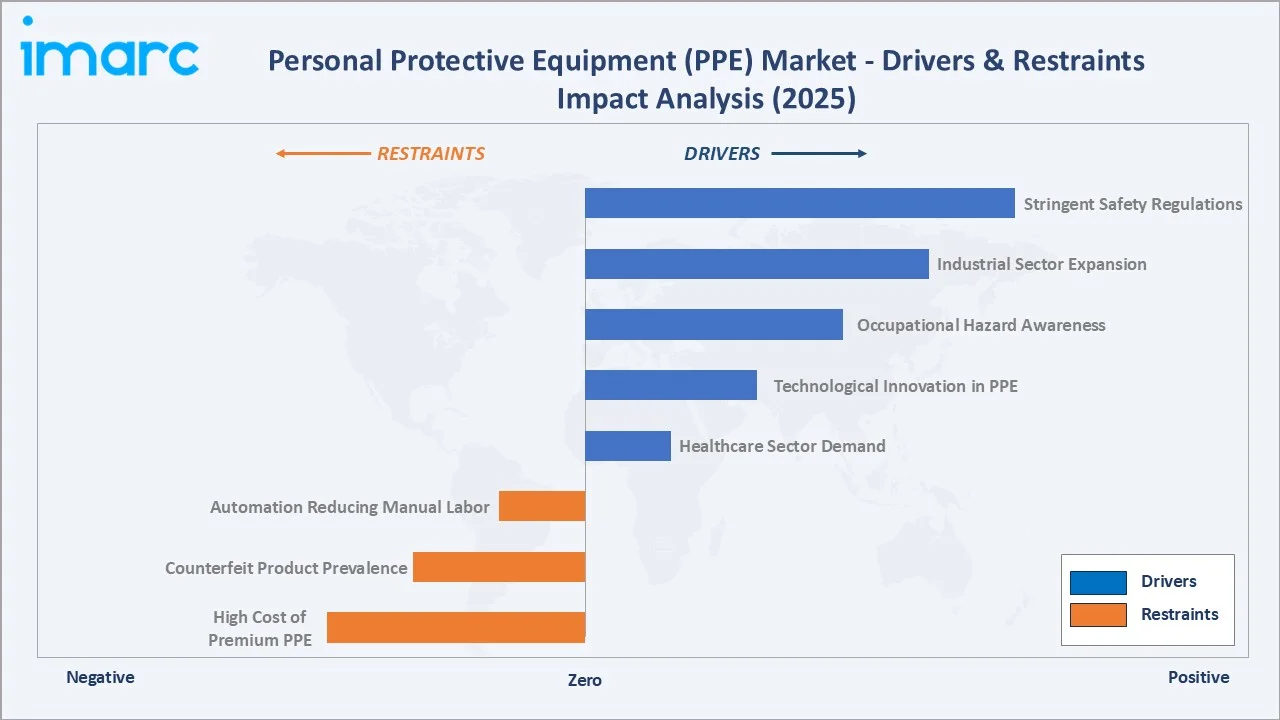

Market Drivers

- Stringent Regulatory Frameworks: OSHA, EU Regulation 2016/425, and equivalent global bodies mandate certified PPE usage across construction, oil and gas, manufacturing, and healthcare. OSHA's proposed civil penalty increases of up to 3% in 2025 are accelerating institutional procurement cycles.

- Industrial Sector Expansion: Global expansion in manufacturing, construction, and energy industries is generating millions of new workers requiring PPE programs. In May 2022, Honeywell finalized the sale of its Personal Protective Equipment (PPE) business to Protective Industrial Products for $1.325 billion in an all-cash deal. The divestment is part of Honeywell’s strategy to streamline its portfolio and concentrate on core growth areas, while enabling the PPE unit to expand under new ownership. This transaction also marks Honeywell’s complete exit from the PPE sector.

- Occupational Hazard Awareness: Rising awareness of long-term health risks from chemical, thermal, and physical workplace exposure is driving proactive PPE investment. The ILO reports approximately 2.3 million work-related fatalities annually, maintaining strong institutional demand.

- Technological Innovation: Integration of IoT sensors, nano-enhanced materials, and smart monitoring capabilities into PPE products is expanding the value proposition. Smart PPE is transitioning from a niche premium feature to an expected standard across major industries.

Market Restraints

- High Cost of Advanced PPE: Premium smart and nano-enhanced PPE products carry significantly higher price points than traditional alternatives. Cost sensitivity in emerging markets and among small-to-medium enterprises limits adoption of high-performance protective equipment beyond minimum compliance requirements.

- Counterfeit Product Prevalence: The proliferation of substandard and counterfeit PPE undermines market integrity and end-user safety. DuPont filed an ITC complaint against Chinese firms in October 2024 over alleged Tyvek infringement, highlighting persistent challenges with counterfeit protective apparel in global supply chains.

- Automation Reducing Manual Labor: Industry 4.0 and increasing automation in manufacturing and logistics are reducing the number of workers in traditional high-PPE-consumption roles. Long-term demand growth in automated industrial settings is expected to be tempered by declining manual workforce requirements.

Market Opportunities

- Smart & Connected PPE: Growth in the smart PPE segment is being driven by the integration of IoT technologies and real-time worker monitoring capabilities. Increasing investment by organizations in connected safety platforms is creating a base of high-value customers, offering strong potential for recurring revenue for manufacturers. Rising emphasis on workplace safety regulations and compliance requirements is further accelerating adoption across industries. Advancements in wearable technology and data analytics are also enabling more proactive risk management and operational efficiency.

- Emerging Market Penetration: India, Southeast Asia, Africa, and GCC nations present vast underserved opportunity. Rapid industrialization, improving regulatory frameworks, and growing safety awareness are expanding the addressable PPE market significantly in these high-growth geographies through 2034.

- Sustainable PPE Development: Demand for biodegradable, recyclable, and eco-friendly protective products is growing strongly. Companies pioneering sustainable PPE, aligned with the EU Green Deal and ESG procurement mandates, can access premium pricing and institutional contracts prioritizing environmental responsibility.

Market Challenges

- Supply Chain Vulnerability: Global emergencies can cause severe PPE shortages, logistical disruptions, and price volatility, as demonstrated during COVID-19. Building supply chain resilience through regional manufacturing and strategic stockpiling remains a core operational challenge for major PPE suppliers worldwide.

- Comfort vs. Protection Trade-off: Designing PPE that provides maximum protection without compromising user comfort is a persistent engineering challenge. Discomfort often leads to improper use or non-compliance, rendering equipment ineffective, driving ongoing investment in ergonomic design and lightweight advanced materials.

- Regulatory Compliance Complexity: Multinational PPE manufacturers must comply with varying standards across OSHA, EN, ISO, and regional equivalents. Navigating divergent certification requirements across 50+ regulatory jurisdictions adds significant cost and complexity to product development and global market entry strategies.

Emerging Market Trends

The global PPE market is being reshaped by converging trends redefining product innovation, distribution, and competitive dynamics through 2034.

1. Regulatory Enforcement and Mandatory Compliance

Stricter global safety regulations—OSHA civil penalty increases of up to 3% in 2025 and EU Regulation 2016/425—are compelling industrial organizations to invest proactively in certified PPE. Regulatory audits are accelerating institutional procurement cycles across manufacturing, construction, and energy sectors.

2. Smart PPE and IoT Integration

Wearable sensors, real-time biometric monitoring, and AI-powered safety platforms are transforming PPE from passive protection into active safety management systems. Smart PPE is projected to grow at a 13.2% CAGR through 2030, driven by construction, oil and gas, and manufacturing sector adoption.

3. Sustainability and Eco-Friendly Materials

Manufacturers are adopting biodegradable materials, recyclable components, and energy-efficient production processes aligned with the EU Green Deal and ESG procurement mandates. DuPont's next-generation Tyvek apparel, launched in 2024, exemplifies lifecycle extension through enhanced durability and breathability improvement.

4. Women-Specific and Inclusive PPE Design

Growing female participation in industrial workforces is driving demand for ergonomically designed size-diverse PPE solutions. Regulatory pressure and corporate inclusion commitments are pushing manufacturers to develop gender-inclusive product lines spanning head protection, gloves, protective clothing, and safety footwear.

5. Post-Pandemic Healthcare PPE Institutionalization

Healthcare systems globally have institutionalized elevated PPE standards post-COVID-19. Sterile glove and gown consumption in biopharma manufacturing grew 18% in 2023, per the European Federation of Pharmaceutical Industries, reflecting permanently elevated demand within healthcare and pharmaceutical end-use segments.

Industry Value Chain Analysis

Raw Materials

The PPE value chain begins with specialized raw materials including polycarbonates, high-performance polymers, aramid fibers (Kevlar/Nomex), nitrile compounds, and technical textiles. Material suppliers play a critical role, as input quality directly determines protective performance and certification compliance outcomes.

Component Manufacturing & PPE Production

Component manufacturers produce specialized sub-assemblies including lenses, filters, harnesses, and shells. OEMs integrate components into certified PPE products at dedicated manufacturing facilities. Automated production lines and precision molding are enabling higher throughput and consistent certification-grade quality standards.

Quality Testing & Certification

All PPE must undergo rigorous performance testing against ANSI, EN, ISO, or equivalent national standards before market entry. Notified bodies in Europe and certified testing laboratories globally validate protection levels, durability, and compliance, serving as a critical quality gateway for market access.

Logistics, Distribution & End Users

Distributors, industrial safety dealers, and direct B2B channels deliver PPE to end users across construction, oil and gas, manufacturing, healthcare, and mining sectors. E-commerce platforms are gaining share in SME procurement, complementing established direct sales and distributor channels globally.

Technology Landscape in the Personal Protective Equipment Industry

Smart PPE and IoT-Enabled Worker Monitoring

Wearable sensor technology embedded into helmets, vests, gloves, and boots is transforming personal protective equipment from passive barriers into active safety management systems. Real-time biometric monitoring platforms track worker fatigue, heat stress, impact exposure, and hazardous gas levels, transmitting alerts to supervisors through centralized safety dashboards.

Advanced Materials, Nanotechnology, and Sustainable Innovation

The relentless advancement in materials science is enabling a new generation of PPE that delivers superior protection without compromising wearer comfort, mobility, or sustainability. Nano-composite coatings applied to gloves and protective apparel are delivering enhanced chemical resistance, cut protection, and thermal barrier performance at significantly reduced product weights compared to traditional alternatives.

Digital Safety Management, Compliance Platforms, and AI Integration

Enterprise safety management software, digital compliance tracking systems, and AI-powered risk assessment platforms are becoming central to how large organizations procure, deploy, and monitor PPE programs at scale. Honeywell, prior to its PPE divestiture, integrated sensors into helmets and vests for real-time worker monitoring compliant with GDPR frameworks across European industrial facilities. AI-powered analytics engines are analyzing workforce injury patterns, equipment usage data, and compliance audit records to predict high-risk exposure scenarios and automate PPE procurement cycles.

Automated Manufacturing and Quality Testing Technology

Precision automated production systems controlling material composition, seam integrity, filter porosity, and protection-grade consistency are standardizing PPE quality across high-volume global manufacturing operations.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global personal protective equipment market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, technology, price range, distribution channel, and end user.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Equipment Type |

Head, Eye and Face Protection |

22.7% |

2025 |

|

End Use Industry |

Oil and Gas |

16.7% |

2025 |

|

Region |

Europe |

30.3% |

2025 |

By Product Type

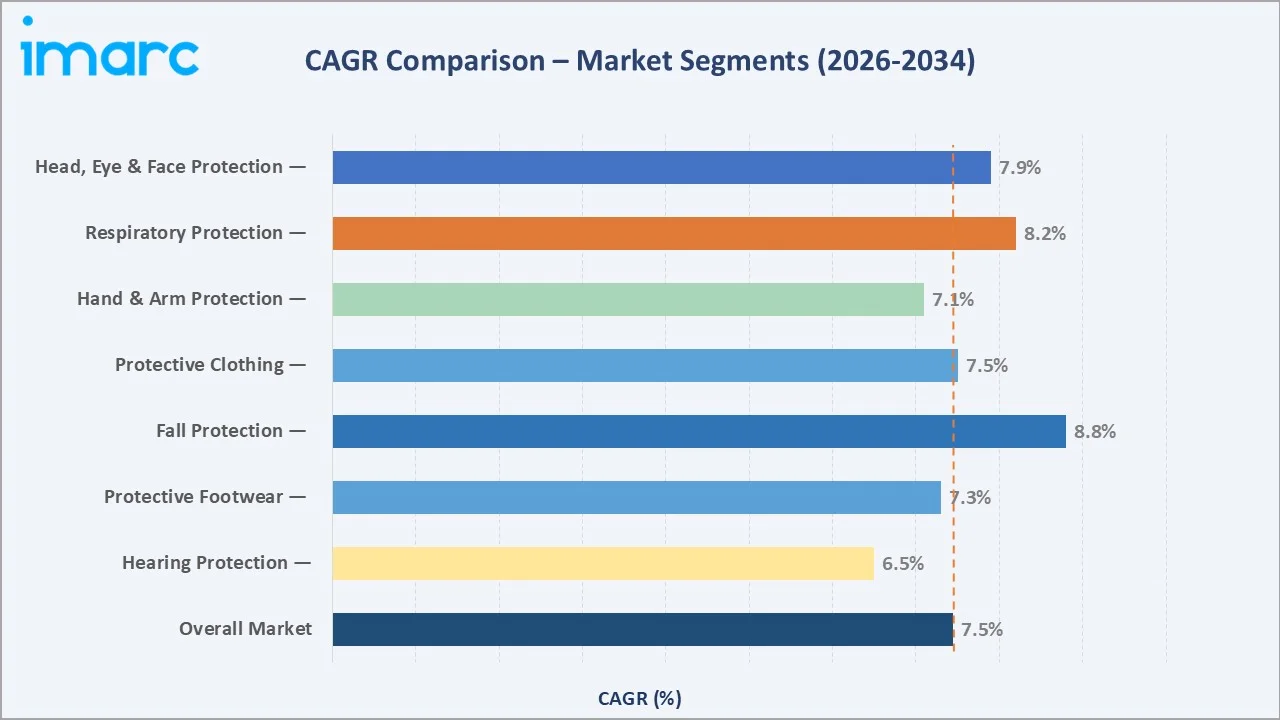

Head, Eye and Face Protection accounts for the largest equipment type share at 22.7% in 2025. Its dominance reflects universal mandates across construction, manufacturing, oil and gas, and healthcare, covering safety helmets, goggles, face shields, and welding masks for diverse hazard protection.

MSA Safety's V-Gard H2 Helmet, launched July 2024 with integrated Mips brain protection technology, exemplifies product premiumization driving higher replacement cycles. Demand is amplified by construction booms across Asia Pacific and the Middle East, where millions of new workers enter high-hazard worksites annually.

Respiratory Protection is the second-fastest growing sub-segment, supported by OSHA identifying respiratory lapses as the fourth-most frequent workplace violation in 2024. NIOSH-certified N95 respirators and advanced SCBA systems continue to see strong demand from oil and gas, healthcare, and construction end users.

To access detailed market analysis, Request Sample

By End User

Oil and Gas is the leading end user segment at 16.7% of the global PPE market in 2025. High-risk upstream, midstream, and downstream operations mandate comprehensive head-to-toe protection programs certified to IOGP, OSHA, and EN standards for all personnel categories worldwide.

North Sea reactivation, hydrogen infrastructure development, and Saudi Vision 2030 are collectively expanding the oil and gas workforce, sustaining strong demand for specialized respiratory systems, fall protection, flame-resistant apparel, and chemical-resistant gloves across upstream and downstream operations. In November 2025, DuPont introduced Tyvek® APX™, a next-generation disposable chemical protective fabric designed to enhance worker safety by combining high breathability with strong protection and durability. The innovation addresses the long-standing challenge of improving comfort without compromising performance, enabling better heat dissipation and overall wearer well-being in demanding work environments.

Construction is the largest individual volume contributor in absolute terms, driven by global infrastructure investment across Asia Pacific, the Middle East, and Europe.

Regional Market Insights

The global PPE market exhibits distinct regional dynamics across revenue share, regulatory maturity, growth trajectory, and end-use concentration. Europe leads with 30.3% market share in 2025, while the Middle East and Africa represent the fastest-growing regional opportunity through 2034.

Europe holds the largest PPE market share at 30.3% in 2025, anchored by Regulation (EU) 2016/425 mandating conformity assessment across all PPE categories. Over 2.8 million occupational injury cases were recorded across the EU in 2023, reinforcing sustained institutional PPE investment.

Asia Pacific is the fastest-growing major region, driven by China's manufacturing expansion under 'Made in China 2025,' India's construction boom, and rapid industrialization across Southeast Asia. Foreign direct investment in Vietnam, Indonesia, and Thailand is generating millions of new workers requiring PPE programs.

Competitive Landscape

The global PPE market is moderately concentrated, with top 5 players, 3M, DuPont, Ansell, MSA Safety, and PIP Inc., accounting for approximately 30–35% of global revenue. The remainder is served by thousands of regional suppliers and specialty manufacturers across diverse product categories.

Market leadership is determined by portfolio breadth, global manufacturing footprint, regulatory certification depth, brand equity in key industries, and investment in smart PPE capabilities. PIP's USD 1.325B acquisition of Honeywell's PPE business in May 2025 significantly reshaped the competitive hierarchy.

|

Company |

Key Product Focus |

Market Position |

Primary Strategy |

|

3M Company |

Respiratory, Eye & Face, Hearing |

Global Leader |

IoT-connected PPE, innovation, global distribution |

|

DuPont de Nemours Inc. |

Protective Clothing, Chemical PPE |

Global Leader – Chemical |

Tyvek/Nomex/Kevlar/ Tychem, IP enforcement |

|

Ansell Limited |

Gloves, Protective Clothing |

Leader – Hand & Body |

Acquisitions, healthcare expansion, sustainability |

|

MSA Safety Inc. |

Head, Fall, Gas Detection |

Leader – Head & Fall |

Smart PPE, premium helmets, gas detection |

|

Protective Industrial Products, Inc. (PIP) |

Head-to-Toe Portfolio |

Major Player – Post-Acq. |

Portfolio integration, brand consolidation |

|

Delta Plus Group |

Full-range PPE |

European Leader |

European distribution strength |

|

Lakeland Industries |

Protective Clothing |

Global Established |

Chemical/fire-resistant apparel |

|

Drägerwerk AG & Co. KGaA |

Respiratory, Gas Detection |

Leader – Respiratory |

Safety tech integration, European heritage |

|

Sioen Industries NV |

Protective Clothing, Textiles |

European Established |

Technical textile innovation |

|

Alpha Pro Tech Ltd. |

Disposable Apparel, Masks |

Niche – Disposable PPE |

Healthcare PPE, capacity expansion |

The report provides a comprehensive analysis of the competitive landscape in the personal protective equipment market with detailed profiles of all major companies, include 3M Company, Ansell Limited, DuPont de Nemours Inc., Lakeland Industries Inc., MSA Safety Incorporated, Protective Industrial Products Inc. (PIP), Alpha Pro Tech Ltd., Delta Plus Group, Sioen Industries NV, Drägerwerk AG & Co. KGaA, and Others.

Key Company Profiles

3M Company

3M is a global diversified technology and manufacturing leader with a dominant position in safety and industrial PPE. Its safety division generates substantial annual revenues through a broad portfolio spanning respiratory protection, eye and face safety, hearing protection, and connected worker solutions.

- Product Portfolio: N95 and P100 respirators, safety goggles, protective eyewear, earmuffs, welding helmets, disposable protective apparel, and IoT-integrated safety monitoring systems across industrial, healthcare, and construction markets.

- Recent Developments: The company completed USD 67 million manufacturing facility expansion in Nebraska in 2024.

- Strategic Focus: Smart PPE innovation, domestic manufacturing expansion, sustainability in product design, and global distribution network optimization across key industrial and healthcare end-use markets worldwide.

DuPont de Nemours Inc.

DuPont is the global leader in chemical and biological protective apparel, renowned for Tyvek, Kevlar, and Nomex—industry-standard materials for contamination control, ballistic protection, and flame resistance.

- Product Portfolio: Tyvek disposable coveralls, Nomex fire-resistant apparel, Kevlar-reinforced gloves and garments, and chemical-resistant suits for hazmat, pharma, oil and gas, and military applications worldwide.

- Recent Developments: Launched next-generation Tyvek protective apparel in 2025 with enhanced breathability and extended durability.

- Strategic Focus: IP protection of premium branded materials, sustainability-driven product lifecycle extension, pharmaceutical and industrial sector expansion, and partnership programs to enhance market-specific PPE program implementation.

Ansell Limited

Ansell is Australia's leading global PPE manufacturer, specializing in hand protection, protective clothing, and chemical-resistant solutions for industrial and healthcare markets. Its 2023 annual revenue of USD 1.6 billion reflects strong market positions across industrial gloves and healthcare protective apparel categories.

- Product Portfolio: Chemical-resistant gloves, cut-resistant gloves, disposable nitrile and latex gloves, protective suits, chemical splash apparel, and specialized hand protection for oil and gas, manufacturing, and healthcare applications.

- Recent Developments: Completed USD 640 million acquisition of Kimberly-Clark's PPE unit in July 2024. Committed to 100% recyclable packaging by 2025. Pursuing smart PPE solutions for real-time worker monitoring.

- Strategic Focus: Strategic acquisitions expanding healthcare and industrial channels, sustainability leadership through recyclable materials, global distribution network strengthening, and digital innovation in worker safety monitoring.

MSA Safety Incorporated

MSA Safety is a specialized global PPE manufacturer with over 5,000 employees operating across 140+ countries. Its V-Gard helmet series is the world's most popular industrial head protection product. MSA's focus on smart PPE and gas detection technology defines its premium market positioning globally.

- Product Portfolio: V-Gard helmets, self-contained breathing apparatus, fall protection systems, gas detection equipment, firefighter turnout gear, and IoT-connected worker safety monitoring platforms for high-risk industrial environments.

- Recent Developments: Introduced V-Gard H2 Safety Helmet with Mips brain protection technology in July 2024.

- Strategic Focus: Premium head protection innovation, smart and connected safety technology integration, gas detection expansion into emerging energy sectors, and sustainable materials adoption across its global product portfolio.

Protective Industrial Products Inc. (PIP)

PIP is a global supplier and manufacturer of PPE with over 40 years of experience. Its May 2025 USD 1.325 billion acquisition of Honeywell's PPE business created a world-class head-to-toe protection platform spanning brands including Fendall, Fibre-Metal, Howard Leight, North, Miller, and Salisbury.

- Product Portfolio: Full head-to-toe protection including hearing protection, hard hats, eye and face protection, respiratory equipment, fall protection, safety footwear, electrical safety, first aid, and first responder equipment across major industrial markets.

- Recent Developments: Completed USD 1.325B Honeywell PPE acquisition in May 2025. Partnered with Quin in October 2025 to integrate intelligent safety technology into Traverse Safety Helmets, debuting AI-powered impact analytics for industrial head protection.

- Strategic Focus: Portfolio integration and brand consolidation post-acquisition, smart PPE innovation through technology partnerships, head-to-toe product expansion, and customer-service-driven market share growth across global industrial safety markets.

Market Concentration Analysis

The global PPE market is structurally fragmented at the product level, with the top 5 players—3M, DuPont, Ansell, MSA Safety, and PIP Inc.—accounting for approximately 30–35% of global revenue. The remaining 65–70% is served by thousands of regional manufacturers and specialty suppliers.

In mature markets—North America and Europe—branded franchise tier concentration is higher, with global manufacturers representing 40–50% of revenue in urban premium segments. In emerging markets including India, Eastern Europe, and Sub-Saharan Africa, regional suppliers dominate, presenting white space for premium brand entry.

The smart and connected PPE sub-segment is more concentrated, with 3M, MSA Safety, and emerging tech-enabled players controlling most of the innovation investment. Technology differentiation is becoming the primary competitive battleground separating premium market leaders from commoditized mid-market suppliers.

Investment & Growth Opportunities

Fastest Growing Segments

- Smart / Connected PPE: This segment is driven by IoT integration and real-time worker monitoring adoption across construction, oil and gas, and manufacturing industries globally.

- Fall Protection: It is supported by rising construction activity, offshore platform operations, and tightening fall-protection mandates under OSHA and EN standards.

- Sustainable PPE: ESG-aligned procurement mandates from multinational corporations and EU Green Deal compliance requirements are creating strong premium pricing opportunities for biodegradable and recyclable protective equipment manufacturers.

Emerging Market Expansion

- Middle East & Africa: The fastest-growing PPE region globally, UAE industrial zone expansion, and growing mining activity. International brands are entering through regional distribution partnerships targeting construction and energy sector demand.

- India: Rapid infrastructure investment, smart city programs, and expanding manufacturing under 'Make in India' are generating strong structural demand for PPE across construction, chemical, and healthcare sectors through 2034.

- Southeast Asia: Vietnam, Indonesia, and Thailand are experiencing FDI-driven manufacturing booms, creating large new workforce cohorts requiring PPE programs aligned with multinational customer safety standards and local regulatory requirements.

Technology and Innovation Investment Trends

- Smart PPE manufacturers and IoT safety platform providers are attracting significant venture and PE investment, with AI-powered worker monitoring, predictive injury prevention, and compliance automation representing high-value software layers above traditional hardware.

- Nano-material and advanced textile R&D investment is growing, enabling next-generation protective fabrics with superior barrier properties and lightweight comfort. DuPont's USD 2 billion annual R&D investment exemplifies the scale of innovation commitment among global PPE leaders.

- Sustainability-focused PPE recycling and take-back programs—such as Earth Safe PPE's textile recycling initiative—represent emerging business model innovation, recognized with healthcare and pharmaceutical industry awards in 2025.

Future Market Outlook (2026-2034)

The global PPE market is poised for sustained growth through 2034, anchored by demographic demand expansion, franchise network penetration into underdeveloped markets, and product category evolution toward smart and sustainable protective solutions. The market is expected to reach USD 170.0 Billion by 2034.

Smart PPE integration will be the primary competitive battleground. Brands that successfully combine IoT-enabled safety intelligence with durable, certified protection will command premium pricing and institutional loyalty, particularly from multinationals standardizing global safety protocols across all operational geographies.

Sustainability will transition from a differentiator to a baseline expectation. EU Green Deal compliance requirements and corporate ESG mandates will make recyclable, bio-based PPE a procurement standard, rewarding manufacturers with established sustainable product lines and supply chain transparency frameworks.

Regional growth dynamics will increasingly favor Asia Pacific, the Middle East, and Africa as industrial expansion drives new worker cohorts into high-hazard jobs requiring PPE. These regions will contribute a growing proportion of global PPE volume growth through 2034, reshaping the market's geographic revenue distribution.

Consolidation among top-tier branded manufacturers will continue, with private equity-backed platforms seeking scale through strategic acquisitions. Smaller regional manufacturers will face increasing pressure to either partner with global brands or invest heavily in product certification and differentiation capabilities.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 150 industry participants in 2024–2025, comprising PPE manufacturers, industrial safety distributors, end-user procurement managers, regulatory compliance specialists, and occupational health professionals across key markets globally.

Secondary Research

Secondary research encompassed a comprehensive review of company press releases, regulatory filings, trade publications (Occupational Health & Safety Magazine, EHS Today, Safety+Health), industry association reports (IOGP, ISEA, EASA), government safety agency databases, and publicly available market intelligence from credible sources.

Forecasting Models

Market size estimations and growth projections were derived using bottom-up end-user demand modeling by industry and geography, combined with top-down spending analysis incorporating occupational workforce data, regulatory mandate timelines, and PPE compliance cost modeling across all major regional markets.

Personal Protective Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered |

|

| End Use Industries Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3M Company, DuPont de Nemours Inc., Ansell Limited, MSA Safety Inc., Protective Industrial Products, Inc. (PIP), Delta Plus Group, Lakeland Industries, Drägerwerk AG & Co. KGaA, Sioen Industries NV, Alpha Pro Tech Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the personal protective equipment market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global personal protective equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the personal protective equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Personal Protective Equipment Market Report

The global PPE market was valued at USD 87.4 Billion in 2025, growing from USD 61.0 Billion in 2020, reflecting robust compound growth driven by intensifying regulatory mandates and industrial expansion worldwide.

The market is projected to exhibit a CAGR of 7.45% during 2026-2034, reaching USD 170.0 Billion by 2034. Growth is anchored by regulatory enforcement, smart PPE adoption, and accelerating industrial activity in emerging economies.

Europe leads with a 30.3% market share in 2025, driven by Regulation (EU) 2016/425, stringent occupational health enforcement, and deep industrial demand from manufacturing, construction, healthcare, and oil and gas sectors across member states.

Head, Eye and Face Protection lead with a 22.7% share in 2025. Its universal mandates across construction, manufacturing, oil and gas, and healthcare, covering helmets, goggles, and face shields, make it the largest and most broadly adopted PPE category globally.

Oil and Gas commands 16.7% of global PPE demand in 2025. High-risk upstream and downstream operations mandate comprehensive head-to-toe protection programs certified to IOGP, OSHA, and EN standards for all personnel categories worldwide.

Key drivers include stringent government safety regulations (OSHA, EU 2016/425), global industrial expansion, growing occupational hazard awareness, smart PPE technology adoption, post-pandemic healthcare institutionalization, and rising ESG-driven procurement standards across multinational corporations.

Leading companies include 3M Company, Ansell Limited, DuPont de Nemours Inc., Lakeland Industries Inc., MSA Safety Incorporated, Protective Industrial Products Inc. (PIP), Alpha Pro Tech Ltd., Delta Plus Group, Sioen Industries NV, Drägerwerk AG & Co. KGaA, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)