Pharmaceutical Contract Packaging Market Size, Share, Trends and Forecast by Industry, Type, Packaging, and Region, 2026-2034

Pharmaceutical Contract Packaging Market Size, Share, Trends & Forecast (2026-2034)

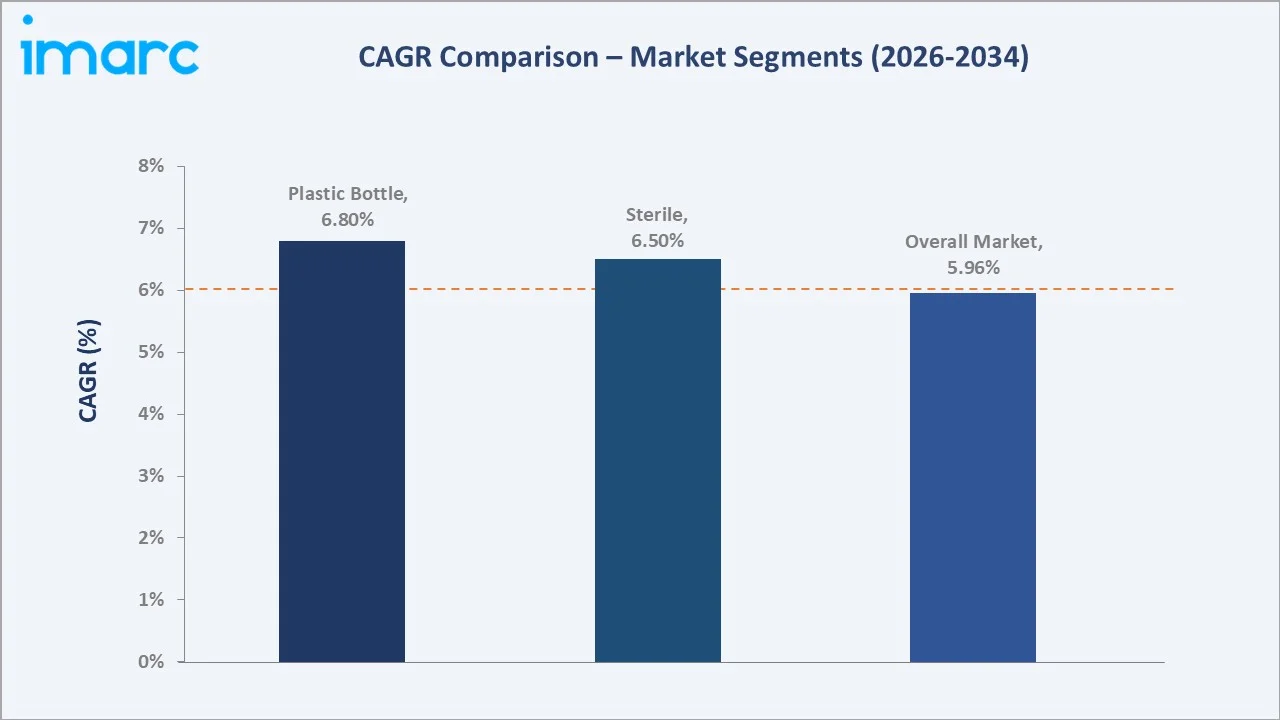

The global pharmaceutical contract packaging market reached USD 24.66 Billion in 2025 and is projected to reach USD 42.18 Billion by 2034, growing at a CAGR of 5.96% during 2026-2034. Rising demand for specialized sterile and primary packaging solutions, accelerating pharmaceutical outsourcing trends, and stringent global serialization mandates are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.66 Billion |

|

Forecast Market Size (2034) |

USD 42.18 Billion |

|

CAGR (2026-2034) |

5.96% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (Type) |

Sterile – 57.9% share (2025) |

|

Largest Segment (Packaging) |

Plastic Bottles – 28.4% share (2025) |

|

Largest Region |

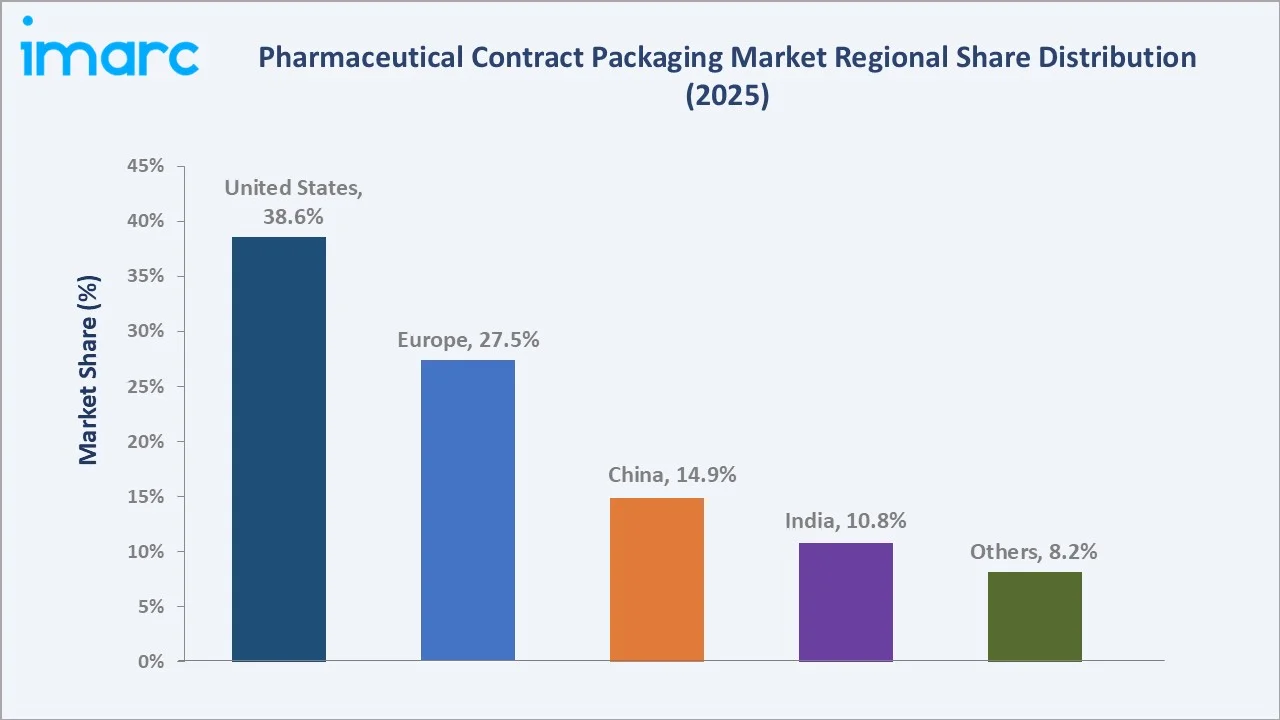

United States – 38.6% share (2025) |

The United States dominates, holding a 38.6% market share in 2025, while the sterile segment leads type demand at 57.9%. Plastic bottles remain the dominant packaging format with a 28.4% share. Pharmaceutical contract packaging enables manufacturers to outsource complex packaging operations—including primary containment, secondary labelling, serialization, and cold-chain logistics, allowing a sharper focus on core drug development and commercialization.

To get more information on this market, Request Sample

With applications spanning small molecule drugs, biologics, and vaccines, the market is expected to continue expanding, supported by innovations in sterile packaging technology and growing regulatory enforcement of serialization across North America, Europe, and Asia.

Executive Summary

The global pharmaceutical contract packaging market is on a sustained growth path, underpinned by increasing pharmaceutical outsourcing, rising demand for sterile primary packaging, and the widespread shift toward specialized contract packaging organizations (CPOs) for regulatory compliance and supply chain efficiency. The market reached USD 24.66 Billion in 2025 and is forecast to surpass USD 42.18 Billion by 2034. This trajectory reflects a healthy CAGR of 5.96% over the forecast period.

The United States leads globally with a 38.6% revenue share in 2025, driven by a robust biopharmaceutical sector, full enforcement of the Drug Supply Chain Security Act (DSCSA), and strong outsourcing rates among both large pharmaceutical companies and emerging biotech firms. Europe, at 27.5%, represents the second-largest market, supported by EU Falsified Medicines Directive (FMD) serialization mandates and a large pharmaceutical manufacturing base across Germany, Switzerland, France, and the United Kingdom.

The sterile packaging segment dominates the 2025 market at 57.9%, reflecting the exponential growth of biologics, vaccines, and injectable therapies. Plastic bottles command the largest share of packaging at 28.4%, followed by blister packs (21.7%) and caps and closures (16.3%). Leading players, including West Pharmaceutical Services, Inc., PCI Pharma Services, Gerresheimer AG, Sharp Services, LLC, CCL Industries, and NIPRO, continue to invest in sterile fill-finish, serialization infrastructure, and sustainable packaging solutions to align with tightening environmental and regulatory standards.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Sterile – 57.9% share (2025) |

|

Largest Segment (Packaging) |

Plastic Bottles – 28.4% share (2025) |

|

Leading Region |

United States – 38.6% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (India 9.1% CAGR; China 8.7% CAGR) |

|

Top Companies |

West Pharmaceutical Services, Inc., PCI Pharma Services, Gerresheimer AG, Sharp Services, LLC, CCL Industries, and NIPRO |

|

Market Opportunity |

Prefilled syringes advancing at 11.43% CAGR; sterile packaging surge through 2034 |

Key Analytical Observations Supporting the Above Data:

- The sterile segment accounts for 57.9% of the pharmaceutical contract packaging market in 2025, driven by the exponential growth of biologics, vaccines, and injectable formulations requiring aseptic processing and contamination-proof primary containment.

- Plastic bottles are the dominant packaging format at 28.4% (2025), valued for cost efficiency, versatility across oral solid and liquid dosage forms, and compatibility with high-speed automated packaging lines.

- The United States holds 38.6% of the global market in 2025, underpinned by full DSCSA serialization enforcement (November 2024), a mature biopharmaceutical ecosystem, and high CPO outsourcing rates across large pharma and emerging biotech companies alike.

- Asia Pacific is emerging as the fastest-growing region, driven by India's expanding FDA-approved sterile packaging facility base and China's rapid biosimilar production scale-up targeting export markets.

- Sustainability mandates are gaining regulatory momentum, with the EU's Packaging and Packaging Waste Regulation (PPWR) 2025/40 requiring full packaging recyclability by 2030, reshaping procurement standards for contract packaging organizations globally.

Global Pharmaceutical Contract Packaging Market Overview

Pharmaceutical contract packaging is a specialized outsourced service where third-party contract packaging organizations (CPOs) handle the primary, secondary, and tertiary packaging of pharmaceutical products on behalf of drug manufacturers. Originally adopted to reduce capital expenditure on packaging infrastructure, the service has expanded to encompass complex sterile fill-finish operations, serialization and track-and-trace compliance, cold-chain logistics packaging, and patient-centric packaging design.

Macroeconomic factors, including rising pharmaceutical R&D expenditure, the growing biologics and biosimilar pipeline, and tightening global regulatory frameworks for drug traceability and safety, are primary growth catalysts. Pharmaceutical contract packaging enables manufacturers to avoid heavy capital investments in packaging lines and serialization infrastructure while achieving full regulatory compliance and operational scalability across multiple markets.

Market Dynamics

To evaluate market opportunities, Request Sample

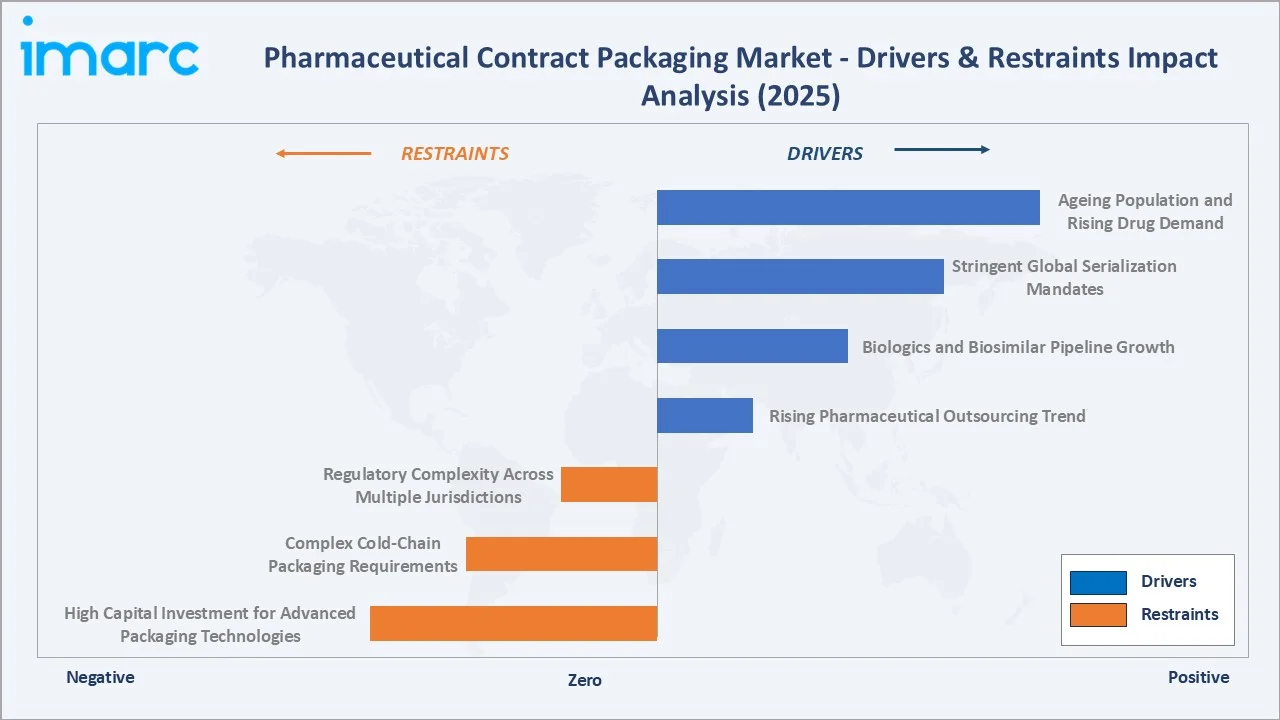

Market Drivers

- Rising Pharmaceutical Outsourcing Trend: Approximately 65% of pharmaceutical brands now rely on contract packagers for blister sealing, bottling, and labelling. This model delivers operational flexibility, faster regulatory compliance, and reduced in-house infrastructure costs, reinforcing the structural shift toward CPO partnerships across large and emerging pharma companies alike.

- Biologics and Biosimilar Pipeline Growth: Worldwide sterile medicinal product output is climbing at a 15% CAGR to 2027. Biologic license applications registered consistent growth, with the FDA’s Center for Drug Evaluation and Research (CDER) approving 55 novel drugs in the U.S. , driving sustained demand for specialized sterile primary packaging, including pre-filled syringes, vials, and ampoules.

- Stringent Global Serialization Mandates: Full DSCSA enforcement in November 2024 requires unique serial numbers, barcodes, and aggregation data at every packaging level, compelling pharmaceutical manufacturers to engage CPOs with validated track-and-trace platforms. Similar mandates across the EU (FMD), Gulf states, and Canada further drive outsourcing demand.

- Ageing Population and Rising Drug Demand: According to the World Health Organization, the proportion of the global population aged over 60 will nearly double from 12% to 22% between 2015 and 2050, fueling pharmaceutical manufacturing volumes and demand for diverse packaging formats across oral solids, injectables, and specialty formulations.

These drivers reinforce a self-sustaining growth cycle, regulatory compliance requirements drive institutional outsourcing, which accelerates CPO investment in advanced sterile and serialization capabilities, which in turn lowers barriers for smaller biotech firms to access world-class packaging infrastructure.

Market Restraints

- High Capital Investment for Advanced Packaging Technologies: Fill lines, isolator suites, cold rooms, and track-and-trace systems require substantial initial capital, particularly for small-to-medium CPOs. The average cost of establishing a sterile fill-finish line ranges from USD 30–100 million, creating significant barriers to entry and capacity expansion.

- Complex Cold-Chain Packaging Requirements: The rapid growth of temperature-sensitive biologics, mRNA vaccines, and GLP-1 agonists demands highly specialized cold-chain packaging infrastructure with continuous temperature monitoring, adding significant operational complexity and cost across global distribution networks.

- Regulatory Complexity Across Multiple Jurisdictions: Diverging serialization, labelling, and packaging standards across the US (FDA/DSCSA), EU (EMA/FMD), and Asia-Pacific markets create multi-jurisdiction compliance burdens that increase per-product certification costs and extend time-to-market for global pharmaceutical launches.

Market Opportunities

- Sustainable and Recyclable Packaging Innovation: The EU's PPWR 2025/40, requiring full recyclability by 2030, is accelerating investment in mono-material packaging designs and post-consumer recycled (PCR) materials.

- Emerging Market Expansion: India and China collectively represent the fastest-growing CPO markets globally, advancing at 9.1% and 8.7% CAGR through 2035, respectively. Expanding FDA-approved facility bases, cost advantages, and growing domestic pharmaceutical manufacturing create substantial opportunities for both local and multinational CPOs.

- AI-Driven Packaging Automation: AI-enabled changeover systems, machine vision inspection, and robotic packaging lines are trimming validation cycles and boosting line productivity. In February 2025, Systech introduced UniSecure artAI, an AI-powered cloud-based authentication system designed to guarantee packaging quality and protect brands using machine vision technology.

Market Challenges

- Serialization Infrastructure Transition Costs: Error-rate spikes of 30% in early DSCSA roll-outs underscored the need for next-generation serialization platforms with open architectures. Legacy CPOs face substantial retrofit investment to achieve compliance with evolving global track-and-trace requirements across multiple jurisdictions simultaneously.

- Supply Chain Disruption Risk: The pharmaceutical packaging supply chain remains vulnerable to raw material shortages, geopolitical disruptions, and single-source supplier dependencies, particularly for specialized glass vials, polymer resins, and aluminum foil, creating resilience challenges for both CPOs and their pharmaceutical clients.

Emerging Market Trends

1. Sterile Packaging Infrastructure Surge Driven by Biologics Pipeline

Pre-filled syringes and auto-injector formats are advancing at an 11.43% CAGR, reflecting the shift toward self-administered biologics for GLP-1 agonists, diabetes, and rheumatoid arthritis therapies. In January 2026, Sharp committed over EUR 20 million to enhance its injectable packaging, assembly, and cold-chain storage capabilities across its Belgium and Netherlands facilities, as part of a broader USD 100 million investment program announced in November 2025.

2. Serialization 2.0 and Digital Packaging Infrastructure Investment

GlobFull DSCSA enforcement from November 2024 has compelled CPOs to transform legacy packaging lines into data-rich operations capable of managing millions of serial numbers daily. Error-rate spikes of 30% in early roll-outs created urgent demand for next-generation serialization platforms with open architectures and real-time EPCIS data exchange. In January 2026, AUSTAR Group presented its latest one-stop pharmaceutical packaging, inspection, and serialization technologies at Pharmapack Paris, engineered for full international regulatory compliance.

3. Patient-Centric Design and Sustainability Transformation

As treatments for chronic conditions increasingly shift from clinical settings to home-based self-administration, packaging must enable ease of use, safety, and medication adherence without compromising product integrity. Simultaneously, the EU Packaging and Packaging Waste Regulation (PPWR) 2025/40 is compelling CPOs to invest in mono-material designs and post-consumer recycled glass and plastic packaging.

4. Hybrid CDMO-CPO Platform Integration Reshapes Competitive Landscape

The USD 16.5 Billion acquisition of Catalent by Novo Holdings in 2024, followed by Novo Nordisk's USD 11 Billion site commitment, fundamentally reshaped the sector's competitive landscape. Private equity interest remains elevated, targeting mid-tier CPOs with certified sterile capabilities, proven serialization systems, and diversified client exposure across oncology, immunology, and metabolic disease therapeutic areas.

Industry Value Chain Analysis

The pharmaceutical contract packaging value chain spans raw material procurement through end-user drug consumption, with each stage populated by specialized operators whose performance directly influences product quality, regulatory compliance, and supply chain efficiency. CPOs occupy the central and highest-value node of this chain, integrating inputs from upstream component manufacturers with downstream pharmaceutical distribution and logistics networks.

|

Stage |

Key Players / Examples |

|

Raw Material Procurement |

BASF SE, Dow Inc. (polymers); SCHOTT Pharma AG & Co. KGaA, Nipro (glass tubing); Constantia Flexibles (aluminium foil) |

|

Packaging Component Manufacturing |

West Pharmaceutical Services (closures, syringes); Gerresheimer AG (vials, ampoules); AptarGroup (dispensing systems) |

|

Contract Packaging Operations |

PCI Pharma Services; Sharp Services LLC; Tjoapack |

|

Serialization and Track-and-Trace |

Systech (UniSecure artAI); Zebra Technologies, TraceLink |

|

Distribution and Cold-Chain Logistics |

UPS Healthcare; DHL Supply Chain; Cencora (AmerisourceBergen); McKesson Corporation |

|

End Users |

Large pharmaceutical manufacturers, biotech firms, generic drug companies, vaccine manufacturers, and hospital systems |

Technology Landscape in the Pharmaceutical Contract Packaging Industry

Advanced Packaging Materials and Barrier Technology

Borosilicate glass remains the dominant primary container material for injectables, but cyclic olefin copolymer (COC) and cyclic olefin polymer (COP) vials and syringes are gaining rapid adoption for biologics and mRNA therapies due to their superior break resistance, low protein adsorption, and compatibility with automated aseptic filling lines.

Intelligent and Connected Packaging Systems

NFC-enabled and RFID-tagged secondary packaging is supporting patient engagement through smartphone connectivity, providing dosing reminders, instructional content, and adverse event reporting pathways. In February 2025, Systech, a division of Markem-Imaje, launched UniSecure artAI, a fully cloud-based AI authentication system that uses machine vision and machine learning applied to existing packaging artwork to deliver real-time quality assurance and anti-counterfeiting verification across pharmaceutical packaging lines globally.

Sustainable Packaging Technology

Post-consumer recycled (PCR) glass content in pharmaceutical vials and bottles is advancing, with bio-based polymer resins derived from renewable feedstocks being evaluated for non-sterile oral solid packaging applications, and lightweight packaging redesigns are reducing material intensity per unit dose across high-volume generic drug packaging operations.

Serialization and Track-and-Trace Technology

In January 2026, AUSTAR Group showcased its one-stop pharmaceutical packaging, inspection, and serialization platform at Pharmapack Paris, engineered for full international regulatory compliance across DSCSA, EU FMD, and GCC serialization frameworks. CPOs with harmonized global serialization systems are capturing an increasing outsourcing share from multinational pharmaceutical manufacturers pursuing multi-market simultaneous product launches.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Industry | Small Molecule | 🔒 | 2025 |

| Type | Sterile | 57.9% | 2025 |

| Packaging | Plastic Bottles | 28.4% | 2025 |

| Region | United States | 38.6% | 2025 |

By Type

The sterile segment accounts for the largest share, representing 57.9% of the global pharmaceutical contract packaging market in 2025. Its dominance is directly linked to the exponential growth of biologics, biosimilars, vaccines, and parenteral formulations, all of which require aseptic processing environments and contamination-proof primary packaging under stringent GMP Annex 1 and FDA cGMP standards.

To access detailed market analysis, Request Sample

Non-sterile packaging holds a 42.1% share and serves the large oral solid dosage market, including tablets, capsules, sachets, and powders. This segment remains a high-volume, cost-efficient category predominantly serving generic pharmaceutical manufacturers and over-the-counter (OTC) drug producers, benefiting from established plastic bottle, blister pack, and cap-and-closure supply chains with mature automation infrastructure.

By Packaging

Plastic bottles represent the largest packaging format at 28.4% in 2025 (approximately USD 7.00 Billion). Their dominance reflects cost efficiency, lightweight properties, design versatility across oral solid and liquid formulations, and compatibility with high-speed automated filling and capping lines serving both prescription and OTC pharmaceutical manufacturers globally.

Blister packs hold a 21.7% share (approx. USD 5.35 Billion), predominantly used for oral solid dose packaging for tablets and capsules, delivering excellent moisture and oxygen barrier protection alongside patient-friendly unit-dose dispensing. Caps and closures account for 16.3% of the market, driven by innovations in child-resistant, tamper-evident, and senior-friendly closure designs meeting global regulatory standards.

Regional Market Insights

The United States' market leadership (38.6%, 2025) reflects a highly advanced biopharmaceutical sector, the world's highest pharmaceutical outsourcing rates, and full DSCSA serialization enforcement from November 2024, which mandated embedded serial numbers, barcodes, and aggregation data at every packaging level.

|

Region |

Share (2025) |

Key Growth Drivers |

|

United States |

38.6% |

Biologics pipeline, DSCSA enforcement, and high outsourcing rates |

|

Europe |

27.5% |

FMD serialization, biosimilar growth, and sustainable packaging mandates |

|

China |

14.9% |

Generics boom, biosimilar scale-up, government healthcare investment |

|

India |

10.8% |

Generic drug exports, FDA-approved facility-based, cost advantage |

|

Others |

8.2% |

Emerging pharma markets, regional CDMO expansion, and healthcare access |

Europe is the second-largest market at 27.5%, underpinned by a large pharmaceutical manufacturing base and EU FMD serialization mandates that have driven sustained investment in compliant packaging infrastructure. The PPWR 2025/40 is reshaping European CPO investment toward sustainable mono-material packaging and recycled-content materials. China, at 14.9%, is rapidly scaling CPO capabilities, supported by NMPA regulatory reforms improving alignment with international GMP standards.

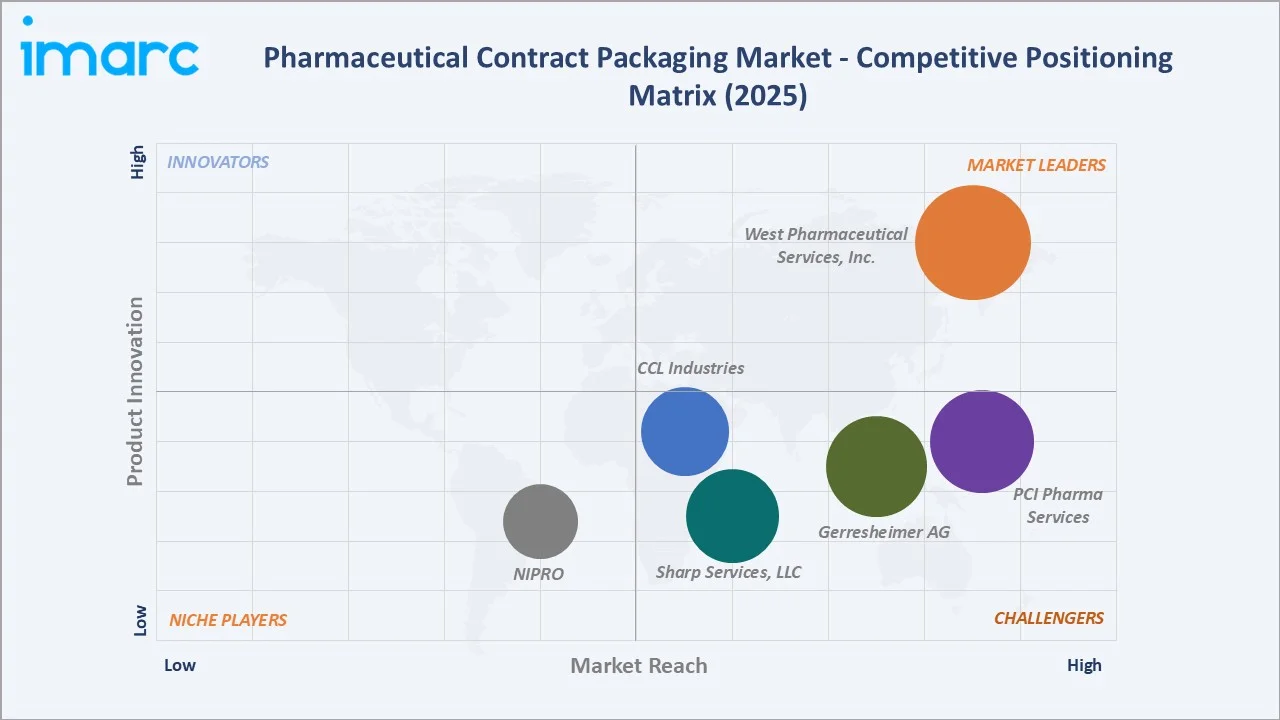

Competitive Landscape

The global pharmaceutical contract packaging market exhibits a moderately fragmented structure. The top five CPOs and integrated CDMOs, West Pharmaceutical Services, Inc., PCI Pharma Services, Gerresheimer AG, Sharp Services, LLC, CCL Industries, and NIPRO, collectively hold approximately 35–42% of global market revenue in 2025. Regional specialists, niche sterile packaging providers, and private-label packaging operators account for the balance, particularly across Asia Pacific and Latin America.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

West Pharmaceutical Services, Inc. |

Westar, FluroTec, SmartDose, Envision, West Synchrony |

Market Leader |

Primary containment; injectable delivery systems |

|

PCI Pharma Services |

PCI, clinicalSMART |

Strong Challenger |

Serialisation & clinical packaging expertise |

|

Gerresheimer AG |

Gx, Gx RTF, Gx Elite, Gx Advance, Gx Value, Gx Inbeneo, Gx RTF ClearJect, EZ-fill Smart |

Strong Challenger |

Glass & plastic primary packaging components |

|

Sharp Services, LLC |

Sharp, Sharp Clinical Services |

Challenger |

Clinical to commercial packaging scale-up |

|

CCL Industries |

CCL Healthcare, CCL Label, CCL Clinical, CCL Faubel |

Challenger |

Global label & packaging solutions network |

|

NIPRO

|

Nipro PharmaPackaging, D2F, Vialex |

Niche Player |

Glass & plastic primary packaging; Japan base |

Key Company Profiles

West Pharmaceutical Services, Inc.

West Pharmaceutical Services, headquartered in Exton, Pennsylvania, is a global leader in the design and manufacture of containment and delivery systems for injectable drugs and healthcare products.

- Product Portfolio: Elastomeric closures, FluroTec-coated components, NovaPure

- Recent Developments: In January 2026, West Pharmaceutical Services confirmed its participation at Pharmapack 2026 in Paris to showcase its expertise in drug packaging and delivery, including the global launch of its new West Synchrony S1 prefillable syringe system with multiple format options and barrier technologies.

- Strategic Focus: Sterile primary packaging for biologics; self-injection device innovation; sustainability through lightweight packaging component design.

PCI Pharma Services

PCI Pharma Services is a leading global CDMO with contract packaging expertise spanning clinical trials to commercial launch across North America, Europe, and Asia. Headquartered in Philadelphia, the company offers fully integrated clinical and commercial packaging services.

- Product Portfolio: Clinical and commercial packaging; serialization and aggregation; clinical labelling; controlled temperature storage and distribution.

- Recent Developments: In September 2024, PCI Pharma Services announced investment of over USD 365 million in expanding and building new facilities in the U.S. and Europe to support clinical‑ and commercial‑scale assembly and packaging of advanced drug delivery and drug‑device combination products, particularly for injectable therapies.

- Strategic Focus: End-to-end serialization and track-and-trace; clinical packaging speed-to-market; cold-chain pharmaceutical packaging leadership.

Gerresheimer AG

Gerresheimer, headquartered in Düsseldorf, Germany, is a global specialist in the development and production of high-quality drug delivery systems and packaging for the pharmaceutical and healthcare industry.

- Product Portfolio: Glass vials, ampoules, pre-fillable syringes, plastic drug delivery systems, insulin pens.

- Recent Developments: In September 2025, Gerresheimer began construction of a new €30 million production facility at its Wertheim, Germany site to manufacture ready‑to‑fill (RTF/RTU) vials using its next‑generation EZ‑fill Smart platform, with production expected to start by mid‑2027.

- Strategic Focus: Premium glass and polymer primary packaging for biologics; Asia Pacific sterile packaging capacity expansion; mRNA vaccine packaging innovation.

Market Concentration Analysis

The pharmaceutical contract packaging market exhibits moderate concentration at the manufacturing and service level, with the top five global CPOs and integrated CDMOs holding approximately 35–42% of total revenue in 2025. However, a long tail of 600+ regional packaging specialists and niche sterile service providers, particularly across China, India, and Latin America, ensures substantial market fragmentation below the top tier.

Consolidation activity is accelerating, driven by serialization compliance costs, GMP certification requirements, and the capital intensity of sterile packaging infrastructure, which collectively create barriers to entry for smaller operators. Between 2020 and 2025, several significant M&A transactions reshaped the competitive map, most notably Novo Holdings' USD 16.5 Billion acquisition of Catalent. Private equity interest remains elevated, targeting mid-tier CPOs with certified sterile capabilities.

Investment & Growth Opportunities

Fastest Growing Segments

Prefilled syringes and sterile primary containers (advancing at 11.43% CAGR), AI-driven serialization platforms (estimated 15% CAGR), and sustainable mono-material packaging systems (driven by PPWR 2025/40 mandates) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable market of approximately USD 8–10 Billion by 2030, underpinned by structural pharmaceutical pipeline shifts toward biologics, self-injection therapies, and environmentally compliant packaging formats.

Emerging Market Expansion

India and China collectively represent the most significant incremental CPO market opportunity through 2034, projected to advance at 9.1% and 8.7% CAGR, respectively. Entry via greenfield facility investment in India's FDA-approved sterile packaging corridor, partnerships with NMPA-compliant Chinese CDMOs, and alignment with regional government healthcare investment programs represent the preferred investment modalities. The Middle East, South Korea, and Brazil also offer meaningful secondary expansion opportunities as local pharmaceutical manufacturing scales.

Venture and Institutional Investment Trends

- Key investment themes include DSCSA-compliant serialization infrastructure, aseptic fill-finish capacity for GLP-1 agonists and biosimilars, AI-enabled packaging quality inspection systems, and cold-chain integrated primary packaging for mRNA and gene therapies.

- Private equity firms and strategic acquirers are increasingly targeting vertical integration plays — consolidating primary packaging component manufacturing, fill-finish operations, secondary packaging, and serialization capabilities into single integrated platform companies to capture the full packaging value chain margin.

Future Market Outlook (2026-2034)

The global pharmaceutical contract packaging market is positioned for sustained, broad-based growth through 2034. From a base of USD 24.66 Billion in 2025, the market is projected to reach USD 42.18 Billion by 2034, representing total incremental value creation of USD 17.52 Billion over the forecast decade at a CAGR of 5.96%.

Regulatory evolution, particularly DSCSA full enforcement, the EU's FMD and PPWR 2025/40 mandates, and Asia-Pacific GMP harmonization, will drive significant serialization infrastructure investment and sustainable packaging innovation across the CPO landscape. Contract packaging organizations that achieve validated serialization, sterile fill-finish, and sustainability-compliant product portfolios by 2026 are positioned to capture a disproportionate share of pharmaceutical outsourcing budgets as regulatory complexity continues to escalate.

Long-term, the market's trajectory is tied to three structural macro-themes: the biologics revolution (creating sustained demand for sterile primary packaging and cold-chain logistics), the serialization mandate wave (driving technology differentiation among CPOs globally), and the patient-centric care shift (transforming packaging from a commodity function to a strategic therapeutic enabler).

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2025–2026, including pharmaceutical contract packaging executives, CDMO operations managers, pharmaceutical procurement officers, regulatory compliance specialists, and end consumers across the United States, Europe, and Asia Pacific.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, regulatory filings, FDA and EMA technical documentation, industry databases (IQVIA, IBISWorld, Euromonitor), trade publications (Contract Pharma, Pharmaceutical Technology), and publicly available financial data. Over 250 secondary sources were reviewed and triangulated to validate market estimates and trend insights.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating pharmaceutical outsourcing expenditure trends, biologics pipeline data, serialization investment flows, and historical market evolution across key geographies. A base-case CAGR of 5.96% reflects consensus analyst estimates validated against reported CPO and CDMO revenue growth rates for 2023–2025.

Pharmaceutical Contract Packaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Industries Covered | Small Molecule, Biopharmaceutical, Vaccine |

| Types Covered | Sterile, Non-Sterile |

| Packagings Covered | Plastic Bottles, Caps and Closures, Blister Packs, Prefilled Syringes, Parenteral Vials and Ampoules, Others |

| Regions Covered | United States, Europe, China, India, Others |

| Companies Covered | West Pharmaceutical Services, Inc., PCI Pharma Services, Gerresheimer AG, Sharp Services, LLC, CCL Industries, NIPRO, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pharmaceutical contract packaging market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global pharmaceutical contract packaging market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pharmaceutical contract packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Pharmaceutical Contract Packaging Market Report

The global pharmaceutical contract packaging market reached USD 24.66 Billion in 2025. It is projected to reach USD 42.18 Billion by 2034.

The pharmaceutical contract packaging market is expected to grow at a CAGR of 5.96% during the forecast period from 2026 to 2034, supported by consistent demand from biologics packaging, pharmaceutical outsourcing, and serialization compliance sectors.

The United States leads the market with a 38.6% revenue share in 2025, driven by a mature biopharmaceutical sector, high CPO outsourcing rates, full DSCSA serialization enforcement (November 2024), and significant capital investment in sterile packaging infrastructure.

The sterile segment dominates with a 57.9% share in 2025. Its dominance is driven by the exponential growth of biologics, vaccines, and injectable formulations requiring aseptic fill-finish and contamination-proof primary containment.

Based on the type, the global pharmaceutical contract packaging market has been segregated into sterile and non-sterile. Currently, sterile pharmaceutical contract packaging exhibits a clear dominance in the market.

Key players include West Pharmaceutical Services, Inc., PCI Pharma Services, Gerresheimer AG, Sharp Services, LLC, CCL Industries, and NIPRO.

Serialization mandates such as the US DSCSA (fully enforced November 2024) and the EU Falsified Medicines Directive (FMD) are compelling pharmaceutical manufacturers to engage CPOs with validated track-and-trace platforms, transforming legacy packaging lines into data-rich compliance operations and creating strong demand for technologically advanced contract packaging services.

Key challenges include the high capital investment required for sterile packaging and serialization infrastructure, complex cold-chain packaging requirements for temperature-sensitive biologics, and regulatory complexity from diverging standards across the US, EU, and Asia-Pacific markets, increasing per-product certification costs.

Significant growth opportunities exist in India and China, advancing at 9.1% and 8.7% CAGR, respectively. Prefilled syringes and sterile primary packaging are the fastest-growing formats at 11.43% CAGR. CPOs offering AI-driven serialization, sustainable mono-material packaging, and integrated CDMO-CPO capabilities are best positioned to capture the highest-growth segments through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)