Phenol Market Report by End-Use (Bisphenol A, Phenolic Resins, Caprolactam, Alkyl Phenyls, and Others), and Region 2026-2034

Phenol Market Overview:

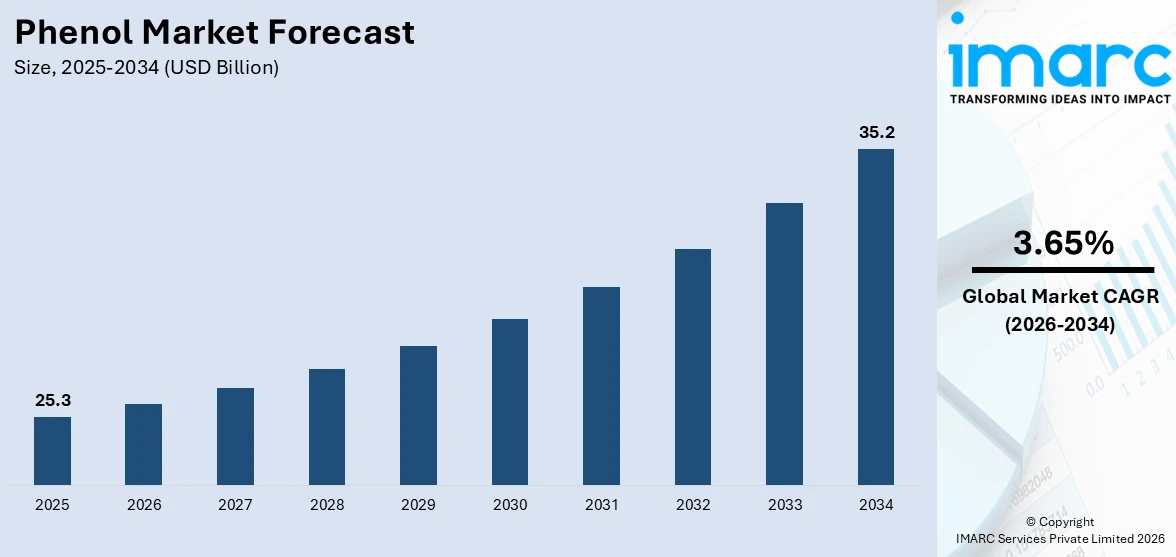

The global phenol market size reached USD 25.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 35.2 Billion by 2034, exhibiting a growth rate (CAGR) of 3.65% during 2026-2034. The growing demand for various cleaning and sanitizing products, increasing utilization as bio preservatives, and rising incorporation in paints, adhesives, and coatings represent some of the key factors driving the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 25.3 Billion |

|

Market Forecast in 2034

|

USD 35.2 Billion |

| Market Growth Rate 2026-2034 | 3.65% |

Phenol Market Analysis:

- Major Market Drivers: Growing demand from the construction, automotive, and personal care sectors is driving phenol consumption. Its affordability, versatility, and increasing application in resins, plastics, and antiseptics are major drivers propelling its mass industrial and consumer usage worldwide.

- Key Market Trends: Increasing the use of phenol in skincare, cleaning agents, and bio-preservatives is driving the expansion of the market. The growth of phenolic resin application in the electronics and automotive sectors, and a shift to high-performance plastics, is also underpinning positive trends.

- Competitive Landscape: The phenol industry is somewhat fragmented with multinational players as well as regional ones. Price, access to raw materials, scale of production, and technology efficiency drive competition. Low product differentiation and zero switching costs contribute to rivalry intensity.

- Challenges and Opportunities: Environmental regulations relating to phenol handling and production create challenges for compliance. But opportunities arise through the application of biobased phenol alternatives, expanding applications in healthcare, and increased demand for phenol-derived polycarbonates and epoxy resins within sustainable construction and electric vehicle components.

To get more information on this market Request Sample

Rising Demand for Phenol in Various End-Use Industries Augmenting Market Growth

The diversified industrial applications of phenol due to its versatile nature and affordable pricing is propelling the growth of the market. The economic reform resulting in the increasing disposable incomes and changing lifestyle patterns of individuals across the globe has significantly catalyzed the demand for phenol in various end-use industries. The rising construction of various residential apartments and roads, and highways around the world is propelling the demand for phenol.

Expanding Utilization in Personal Care Products

Phenol is also utilized as a solvent and cleaning agent in households and various commercial setups to prevent the spread of diseases. It is employed as a cleaner for various electronic devices and industrial machinery, as it possesses enhanced penetrating power into organic matter. Moreover, the increasing demand for phenol in the manufacturing of various personal care products to maintain hygiene and prevent the formation of mouth and body odors is impelling the growth of the market. Phenol is also used as an essential raw material in the plastic industry to manufacture plastics and various explosives, such as picric acid, which is an essential component for making matchsticks and electric batteries. The growing utilization of phenol as a raw material in the manufacturing of drugs and antioxidants is offering a favorable market outlook. Furthermore, the increasing adoption of phenol as a primary component in wood preservatives, such as creosote, is bolstering the growth of the market.

Insights into Market Rivalry

The phenol market is fragmented in nature, with several small and large players operating in the industry. The volume of new entrants is moderate in the phenol industry due to the presence of high capital investments, the requirement of manufacturers to gain economies of scale, and easy access to distribution networks. Furthermore, the market is characterized by low product differentiation rates and switching costs.

Competitive analysis such as market structure, market share by key players, player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

What is Phenol?

Phenol is an aromatic compound that occurs in a white crystalline form at room temperature. It comprises strong hydrogen bonds, which makes it more soluble in water than alcohol and possesses higher boiling points as compared to other hydrocarbons with similar molecular weight. It is mildly acidic and caustic in nature and occurs either as a colorless liquid or white solid. It darkens slowly on exposure to light and possesses a characteristically sweet odor. Phenol was initially manufactured through a synthetic process involving the sulfonation and chlorination of benzene. It is currently manufactured from benzene and propylene by converting them into cumene, then oxidizing it into cumene hyperoxide, and hydrolyzing it to form phenol.

Major Applications of Phenol

Phenol is commercially available as n-hexylresorcinol, which is often incorporated in cough drops and syrups, and other antiseptic applications. It is also used in the synthesis of butylated hydroxytoluene (BHT), which is non-toxic and a common antioxidant in various food products. It is incorporated into mouthwashes and household cleaners to restrict the growth of various disease-causing microorganisms. It is often utilized as a slimicide which is a broad-spectrum antimicrobial pesticide used to kill slime-producing microorganisms, such as algae, bacteria, and fungi. Phenol is employed in the manufacturing of a wide variety of arts and crafts supplies, body paints, glitters, and other play cosmetics. It is also employed in the pharmaceutical industry as a preservative in vaccines to retain their efficiency. It is also utilized in manufacturing oral analgesics, throat and nasal sprays, and surgeries for ingrown toenails. It is utilized as a gentle preservative for a wide variety of personal care products, such as soaps, deodorants, antiperspirants, shampoos, toothpaste, and toners. It is also injected into muscles to prevent the occurrence of muscle spasticity, which hampers the ability to walk. Furthermore, as it is easily available, cost-effective, and can be purchased in bulk quantities, the demand for phenol is increasing across the globe.

Leading Trends Fostering the Phenol Market Growth:

At present, the rising demand for various cleaning and sanitizing products due to growing health consciousness among the masses represents one of the primary factors influencing the market positively. Besides this, the increasing utilization of phenolic resins for producing thermosetting plastics is propelling the growth of the market. Additionally, there is a reduction in the price of raw materials required for the manufacturing of phenol around the world. This, coupled with the limited availability of substitutes for phenol, is contributing to the growth of the market. Apart from this, the growing demand for phenol in the manufacturing of various skincare products, such as chemical peels to remove dead skin cells and smoothen the skin texture, is offering a favorable market outlook. In addition, the increasing utilization of phenolic compounds as bio preservatives for enhancing the antioxidant and antimicrobial capacity of fresh fruits and vegetables is supporting the growth of the market. Moreover, the rising incorporation of phenol in paints, adhesives, and coatings is impelling the growth of the market. Furthermore, the increasing demand for preservatives in the food and beverage (F&B) industry to retain the taste and quality of various consumable and perishable products is bolstering the growth of the market.

Key Market Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the global phenol market report, along with forecasts at the global and regional level from 2026-2034. Our report has categorized the market based on end-use.

End-Use Insights:

Access the comprehensive market breakdown Request Sample

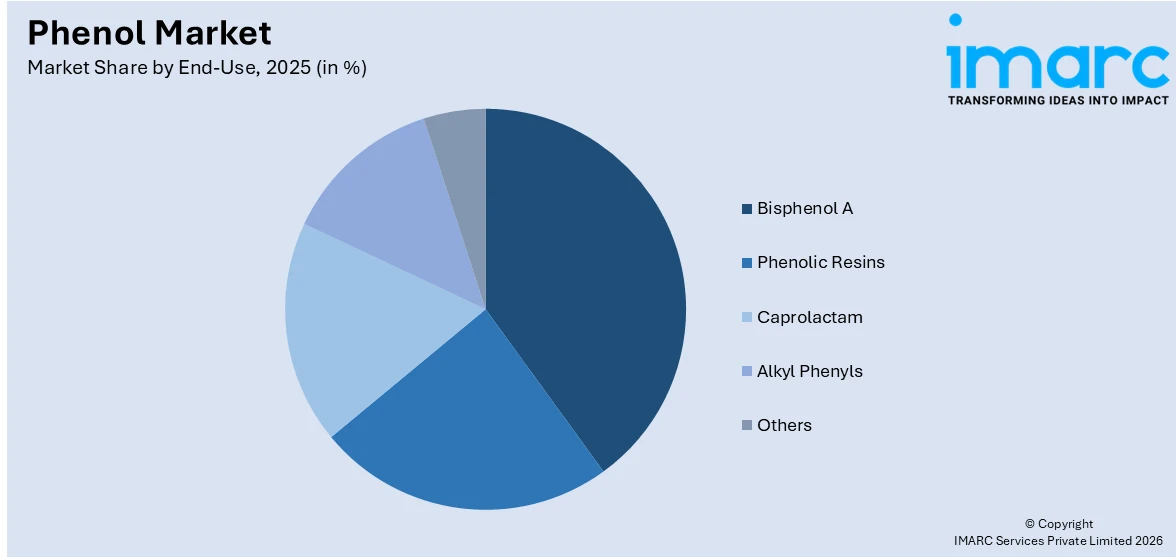

- Bisphenol A

- Phenolic Resins

- Caprolactam

- Alkyl Phenyls

- Others

Bisphenol A Holds Strong Market Presence Due to Epoxy Resins and Polycarbonate Demand

The report has provided a detailed breakup and analysis of the phenol market based on the end-use. This includes bisphenol A, phenolic resins, caprolactam, alkyl phenyls, and others. According to the report, bisphenol A represented the largest segment as it finds vast applications in the production of epoxy resins and polycarbonates which are used for manufacturing plastic lenses in eyewear, protective gears, cover for greenhouses, and exterior lighting fixatures. Besides this, the rising utilization of bisphenol A in the manufacturing of food and beverage containers, electronic equipment, medical devices, household appliances, telephones, and automotive parts is propelling the growth of the respective segment.

Regional Insights:

- Asia Pacific

- Europe

- North America

- Middle East and Africa

- Latin America

Asia Pacific Takes the Lead with Strong Investments in the Chemical Industry

The report has also provided a comprehensive analysis of all the major regional markets, which include Asia Pacific, Europe, North America, the Middle East and Africa, and Latin America. According to the report, Asia Pacific was the largest market for phenol. Some of the factors driving the Asia Pacific phenol market included the growing investment in the chemical industry, rising installation of advanced machinery to boost the production rate and increasing demand for various personal care products to maintain self-hygiene and prevent body odors. In addition, the increasing construction of various residential and commercial buildings, coupled with the rising demand for renovation and remodeling of public infrastructures is catalyzing the demand for phenol across the region.

Key Regional Takeaways:

Asia Pacific Phenol Market Analysis

Asia Pacific controls the world phenol market due to the region's solid chemical manufacturing sector, good industrial infrastructure, and growing demand from industries like construction, automotive, and electronics. Growth in the consumption of plastics, coatings, adhesives, and sanitizing agents is driving phenol use. Urbanization, especially in developing economies, is generating steady demand for materials based on phenol that are used in residential and commercial construction projects. Also, large investment in healthcare and hygiene industries has resulted in increased production of antiseptics, disinfectants, and personal care products where phenol is a major input. Government initiatives for manufacturing expansion and domestic self-reliance are also benefiting domestic production of phenol. Phenol synthesis and resin processing technology advancements are also helping in terms of increased output and supply chain efficiencies. With a growing middle-class consumer population and a growing base of consumers, the region will continue to lead in phenol consumption and remain a key growth driver in the global market.

Europe Phenol Market Analysis

The European phenol market is driven by established industrial markets and the increasing demand for high-performance materials in automotive, electronics, and construction applications. Phenol is used more and more in the production of thermosetting plastics, resins, and specialty chemicals, which are all vital to the continent's high-tech manufacturing sector. Firm demand from polycarbonate and epoxy resin markets for automotive interiors, electrical components, and structural parts is underpinning steady consumption. Growth in development of personal care and pharmaceutical products has also driven up the use of phenol-based materials, especially in hygiene products and medicines. The market is supported by strong research capacity, which enables continual innovation in phenol derivatives as well as better formulations in polymers and coatings. Moreover, emphasis on next-generation packaging materials and bio-based phenolic materials is fueling market growth. Through continued investment in industrial innovation and value-added applications, Europe remains a leading force in the international phenol market scenario.

North America Phenol Market Analysis

North America accounts for a substantial proportion of the phenol industry, driven by sophisticated industrial activity and increasing demand in major industries like construction, consumer products, and automotive production. The high priority given to infrastructure expansion and reconstruction in the region leads to consistent demand for phenol-based adhesives, insulating materials, and engineered wood products. In the medical and personal care sector, phenol is widely employed in disinfectants, antiseptics, and dental hygiene preparations, propelling consumption. Heavy investment in polymer and resin technology has raised the demand for products derived from phenol like bisphenol A and phenolic resins. In addition, the availability of technologically advanced manufacturing plants allows for effective manufacturing and promotes exports. Expansion in thermoplastics for auto parts and electronic appliances is also propelling the regional market further. With a robust distribution network in place and a strong emphasis on specialty chemicals and advanced performance materials, North America continues to be a prime driver of the overall phenol value chain globally.

Latin America Phenol Market Analysis

Latin American phenol market is experiencing steady growth, led by increasing industrialization and increasing demand from the construction, pharmaceutical, and consumer goods industries. Rising infrastructure activities in urban areas are driving the demand for phenol-based resins, adhesives, and paints. The personal care segment is growing gradually, mainly in Brazil and Mexico, leading to higher phenol consumption for producing hygiene products and cosmetic preparations. The emerging healthcare industry in the region is also driving phenol demand, particularly for antiseptics, oral pharmaceuticals, and disinfectants. Increased use of plastics and packaging materials, in which phenol serves as a principal input, is also driving market growth. Regional initiatives to upgrade manufacturing capacity and increase local production are also contributing to import substitution and supply chain resilience. With changing consumer lifestyles and population growth in urban areas, the market for phenol-based products is likely to increase consistently, further positioning the region as a major player in the global phenol market.

Middle East and Africa Phenol Market Analysis

Middle East and Africa phenol market is growing with increasing investments in industrialization, escalating construction operations, and growing demand for consumer and hygiene products. Urban development in the Gulf and African countries has hastened the application of phenol in paints, coatings, and engineered wood. Phenol use in plastics and resins production is in line with the region's packaging and infrastructure needs, which is supporting increased demand. Increased demand is also being driven in the personal care segment, buoyed by increasing awareness of hygiene and well-being, driving consumption of phenol in soap, shampoo, and disinfectants. Drug production is also picking up in a number of countries, propelling demand for phenol antiseptics and formulations. The area is augmented by enhancing industrial policies and investment in chemical processing facilities, allowing for greater domestic production. With growing consumer demand coupled with continued industrial diversification, the Middle East and Africa will play an increasingly prominent position in the world phenol supply and application chain.

Competitive Landscape:

The report has also provided a comprehensive analysis of the competitive landscape in the global phenol market. Some of the companies covered in the report include:

- INEOS Phenol Gmbh

- CEPSA Química S.A. (Compañía Española de Petróleos S.A.U.)

- Mitsui Chemicals Inc.

- Formosa Chemicals & Fibre Corporation

- Kumho P & B Chemicals Inc. (Kumho Petrochemical Co. Ltd.)

- Shell Chemicals (Shell plc)

Please note that this only represents a partial list of companies and the complete list has been provided in the report.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Segment Coverage | End-Use, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | INEOS Phenol Gmbh, CEPSA Química S.A. (Compañía Española de Petróleos S.A.U.), Mitsui Chemicals Inc., Formosa Chemicals & Fibre Corporation, Kumho P & B Chemicals Inc. (Kumho Petrochemical Co. Ltd.) and Shell Chemicals (Shell plc) |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the phenol market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global phenol market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the phenol industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The phenol market is massively growing on a global scale. As per the IMARC Group, the global phenol market size was USD 25.3 Billion in 2025. The growing demand for phenol as an industrial cleaner for machinery and electronic devices is primarily driving the global market. Moreover, the increasing utilization of phenol in the preparation of mouthwash, liquid detergents, dyes and inks, floor cleaners, disinfectants, etc., is also propelling the market growth. Additionally, the rising application of phenol in the pharmaceutical sector to produce antioxidant drugs is further augmenting the global market.

As per the IMARC Group, the global phenol market size is anticipated to be USD 35.2 Billion by 2034. The emerging popularity of Ready-to-Eat (RTE) food products, coupled with the increasing demand for preservatives in the F&B industry to retain the taste and quality of perishable goods, will continue to augment the market growth. Moreover, a significant reduction in the price of raw materials required for the manufacturing of phenol is further expected to propel the global market. Additionally, the growing consumer health consciousness and escalating prevalence of various communicable diseases are driving the demand for phenol-based disinfectant products, thereby creating a positive outlook for the market growth.

The introduction of new catalysts and improved production technologies to enhance yield, ensure safety, and optimize overall costs represents one of the major trends in the market.

The market is currently experiencing a negative impact on account of the rapid spread of the coronavirus disease (COVID-19) and consequent lockdowns imposed by governments of several countries, which has resulted in a labor shortage, supply chain disruptions and limited availability of raw materials.

Based on the end-use, the market has been classified into bisphenol A (BPA), phenolic resins, caprolactam, alkyl phenyls and others.

On the geographical front, the market has been segmented into Asia Pacific, Europe, North America, Latin America, and Middle East and Africa.

Some of the largest manufacturers of phenol are INEOS Phenol Gmbh, CEPSA Química S.A. (Compañía Española de Petróleos S.A.U.), Mitsui Chemicals Inc., Formosa Chemicals & Fibre Corporation, Kumho P & B Chemicals Inc. (Kumho Petrochemical Co. Ltd.) and Shell Chemicals (Shell plc), amongst others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)