Philippines Buy Now Pay Later Market Size, Share, Trends and Forecast by Channel, Enterprise Size, End Use, and Region, 2026-2034

Philippines Buy Now Pay Later Market Size and Share:

The Philippines buy now pay later market size was valued at USD 2.5 Billion in 2025. Looking forward, the market is expected to reach USD 4.4 Billion by 2034, exhibiting a CAGR of 6.32% from 2026-2034. The market is influenced by growing e-commerce adoption, increasing financial inclusion for underbanked populations, rising demand for flexible payment options across industries, and affordability concerns for healthcare, education, and high-value purchases. Partnerships with retailers and digital platforms further accelerate BNPL integration and consumer adoption.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2034 | USD 4.4 Billion |

| Market Growth Rate (2026-2034) | 6.32% |

The Buy Now, Pay Later (BNPL) market in the Philippines is fueled by several key factors that align with the evolving needs of consumers and businesses in the country. The rapid growth of e-commerce is a significant driver for Philippines buy now pay later market growth. According to the International Trade Administration, with 73 million active internet users, the Philippines' eCommerce business generated $17 billion in sales in 2021. By 2025, this is projected to expand by 17% to $24 billion. With increased smartphone penetration, improved internet connectivity, and a growing number of digital platforms, online shopping has become more accessible. According to industry reports, at the beginning of 2024, when internet penetration was 73.6 percent, there were 86.98 million internet users in the Philippines. BNPL integrates seamlessly with e-commerce platforms, offering consumers flexible payment options for high-value and everyday purchases. This affordability encourages more spending, particularly among younger, tech-savvy demographics.

To get more information on this market Request Sample

The Philippines has a large underbanked population with limited access to traditional credit systems. BNPL provides an alternative to credit cards, allowing consumers to make purchases and pay in installments without lengthy approval processes or high interest rates. This inclusivity opens new opportunities for consumers and businesses, addressing financial barriers and expanding credit access, representing one of the key Philippines buy now pay later market trends. The rising inflation and limited disposable incomes have increased consumer demand for affordable and flexible payment options. According to industry reports, overall inflation, or headline inflation, in the Philippines rose from 2.5 percent in November 2024 to 2.9 percent in December 2024. BNPL allows users to manage their budgets better by spreading costs over time. Industries like healthcare, education, consumer electronics, and fashion benefit significantly, as BNPL solutions make essential and lifestyle purchases more manageable.

Key Trends of Philippines Buy Now Pay Later Market:

Growing E-Commerce Adoption

E-commerce expansion throughout the Philippines leads consumers toward BNPL adoption because they demand flexible payment methods for their digital purchases. Cost-conscious consumers are drawn to the ease of deferred payments, particularly for expensive goods like fashion and gadgets. Better internet connections and growing smartphone adoption have created simple online purchasing possibilities, while BNPL provider and e-commerce platform alliances boost user comfort. The expansion of digital wallets combined with online marketplaces facilitated the Philippines buy now pay later market demand because this payment solution appeals to both tech-literate buyers and customers watching their budgets. For instance, in August 2024, PayMongo, a payment processing platform, introduced the PayMongo Wallet, its newest product, intended to help small and medium-sized businesses (SMEs) in the Philippines with their digital transactions. The goal of the PayMongo Wallet, according to PayMongo CEO Jojo Malolos, is to revolutionize financial transactions for SMEs by offering a simple, safe, and inclusive solution.

Increasing Financial Inclusion

BNPL addresses financial inclusion challenges in the Philippines by offering credit access to underbanked and unbanked populations. With limited access to traditional credit cards, many Filipinos use BNPL as an alternative for flexible, interest-free installment payments. This solution empowers consumers to afford essential goods and services without the need for lengthy credit approval processes. BNPL providers capitalize on this opportunity by creating user-friendly platforms and targeting untapped market segments, driving widespread adoption across various demographics. For instance, in November 2024, Thunes, the Smart Superhighway for international money transfers, launched a new partnership with GCash, the top digital wallet in the Philippines. Through this innovative effort, users of GCash may spend money from their European and U.K. bank accounts to top up their wallet balances right within the app. Because of this partnership, cross-border top-ups are now more affordable and real-time, giving GCash users across Europe greater financial control and convenience.

Rising Healthcare and Education Costs

The escalating costs of healthcare and education in the Philippines make BNPL an attractive solution for managing essential expenses. According to industry reports, healthcare costs in the Philippines are expected to climb by 18.3% in 2025, continuing the nation's record of double-digit rises in medical costs. According to a survey, out-of-pocket expenses accounted for 44.7% of health expenditures in the Philippines in 2022, or USD 9 Billion. By 2028, this amount is predicted to increase to US$13 billion, highlighting the burden on homeowners. Families leverage BNPL to spread out payments for medical treatments, consultations, and tuition fees, easing financial strain. Healthcare providers and educational institutions partner with BNPL companies to offer installment plans, ensuring access to quality services without immediate financial burden. This demand for affordability in critical sectors significantly contributes to BNPL adoption in the country.

Growth Drivers of Philippines Buy Now Pay Later Market:

Emerging Mobile Commerce and Digital Payments Infrastructure

Rapid growth of mobile commerce coupled with capable digital payments infrastructure is one of the largest drivers of BNPL expansion in the Philippines. Filipinos are among the most prolific global users of both smartphone‑based shopping and mobile internet, and many merchants today construct e‑commerce businesses that expect users to pay by phone or app. This has been made possible due to widening network coverage, higher penetration of smartphones outside Metro Manila to rural provinces, and powerful digital wallet platforms. Domestic fintech companies and payment service providers are becoming integrated with retailers, both digitally and offline, with in-app checkout or point-of-sale BNPL options. Since most Filipinos are underbanked by conventional credit card infrastructure, BNPL serves a purpose by permitting access to installment‑based payment terms without the entire upfront expense. Since most transactions are done through mobile phones, and since networks of logistics (such as delivery and collection) are getting better in previously difficult‑to‑reach places, BNPL becomes more practical and appealing as a method of payment.

Demographics, Consumer Behavior & Affordability Pressure

Another integral driver of growth is the population profile and spending habits in the Philippines, especially among millennial and Gen Z consumers. Millennials and Gen Z are digitally literate, accustomed to using the internet and other digital channels for purchases, and apt to experiment with newer financial products. They tend not to have well‑documented credit histories, or access to standard credit cards, yet eagerly purchase items (gadgets, fashion, lifestyle) that BNPL facilitates. Affordability issues, motivated by cost of living, inflation, or irregular incomes, pressure consumers to make payments over time instead of upfront. Furthermore, the consumerist ambitions in urban areas (Manila, Cebu, Davao etc.) witness individuals desire greater access to consumption and lifestyle products yet are unable to make full payment. BNPL smooths that gap, enabling consumers to utilize sales, promotions, or new product launches without being restricted by their short-term cash flow.

Merchant Adoption, Competition & Product Innovation

Another key driver in the Philippines is the rising merchant adoption of BNPL, coupled with competitive forces and product innovation among providers. Retailers, large chains and smaller SMEs alike, view BNPL to bring in shoppers, grow basket size, enhance conversion rates, and decrease cart abandonment, particularly within online checkout processes. Providers are fighting back by providing flexible plan types like installment periods, low or zero interest, and easier application or payback procedures. Some are embedding BNPL within both web shops and in-store checkouts. With each new fintech entrant, there is likewise innovation in risk assessment, fraud protection, and integrating BNPL with other offerings such as loyalty or digital wallet functionality. Regulation and supervision are likewise improving gradually, making consumers comfortable and providers legitimate. Moreover, as supply chains, last-mile delivery, and logistics expand in the archipelagic landscape, merchants are inclined to sell costly products with a BNPL option since fulfillment obstacles are reduced.

Opportunity of Philippines Buy Now Pay Later Market:

Deepening Penetration into Under-Banked Areas and Informal Economy

Extending services to the Philippines' numerous provinces, islands, and informal economy sectors that remain under-banked by formal credit is among the largest opportunities for BNPL. Most Filipinos in the more rural or distant regions lack access to credit cards or conventional finance yet increasingly rely on smartphone and mobile internet. With increasingly efficient logistics networks and internet penetration outside major metropolitan hubs such as Metro Manila, Cebu, and Davao, BNPL players can collaborate with local merchants like sari‑sari stores, markets, small shops, so that individuals in these regions are able to avail installment payment for consumer items as well as daily essentials. This also provides an opportunity to create BNPL plans that can be tailored to local cash flow cycles, where incomes could be erratic or seasonal, providing smaller-value purchases and flexible repayment terms. Moreover, providers can establish trust by employing localized onboarding, ID verification appropriate to local documents, and collaboration with neighborhood financial service agents. Since most Filipinos already have confidence in domestic remittance services, cooperatives, or quasi‑formal financial centers, BNPL providers who are integrating or partnering with such networks can tap underlying demand. Expanding beyond the urban middle class into lower‑income, rural, or informal segments is a significant growth opportunity.

Integration with Mobile Wallets, E‑Commerce Platforms, and Everyday Services

Deep integration into the already big and expanding ecosystem of mobile wallets, e‑commerce sites, and point‑of‑sale systems in the Philippines is another good chance. Filipino consumers are highly familiar with using e‑wallets and digital payment apps both for small and substantial transactions, whether for bills, food delivery, transport, or online shopping. BNPL solutions integrated into these platforms (in‑app checkout, pay later buy now at offline POS, or through partner merchants) will be more convenient and compelling. Additionally, through collaborations with large e‑commerce marketplaces, social commerce vendors, and even ride‑hailing or delivery businesses, BNPL businesses can make their offerings ubiquitous—providing installments for different kinds of goods or services other than gadgets or fashion items—like appliances, education, healthcare, or even utility payments. Since most Filipinos use digital services on a daily basis, plugging BNPL into such habitual touchpoints reduces friction and turns BNPL into more of a standard feature than a premium add-on. Moreover, this can permit cross-promotions, loyalty offers, or bundling with wallet or app-based credit lines, enhancing retention and deepening usage beyond initial trials.

Innovation in Risk Management, Alternative Credit Scoring, and Regulatory Support

Another area of opportunity in the Philippines is credit assessment, risk management innovation, and regulatory collaboration. Since most potential BNPL consumers lack formal credit history, leveraging alternative data such as mobile phone behavior, bill payment history, utility bills, or digital wallet transaction history can enable providers to underwrite safely customers who are typically shut out of traditional credit. Fintechs that develop robust risk models tailored to local cultural and behavioral trends can differentiate themselves. Additionally, regulatory systems are slowly catching up, and BNPL providers can collaborate with regulators to provide consumer protection—honesty in terms, equitable repayment systems, and means to prevent over‑extension of debt. Providers who engage cooperatively with government agencies and central bank regulation can acquire legitimacy and trust from consumers. Apart from this, there is opportunity in creating education and awareness campaigns to improve financial literacy about BNPL, so that users understand obligations, fees, and repayment schedules, thus reducing default risk. Altogether, these innovations in underwriting, coupled with favorable regulation, can unlock much wider adoption without excessive risk.

Challenges of Philippines Buy Now Pay Later Market:

Consumer Debt Risk and Lack of Credit Histories

One of the largest challenges for BNPL in the Philippines is the potential buildup of consumer debt, especially among individuals who do not have formal credit histories. Most Filipino consumers don't own credit cards or have existing bank relationships; they are "thin file" customers with minimal documented financial history. It becomes more challenging for BNPL providers to assess risk. Without robust mechanisms for assessing creditworthiness, providers risk exposure to elevated default rates. For shoppers, the allure to utilize several BNPL options at the same time or overcommit across multiple platforms heightens the risk of over‑indebtedness. Because BNPL can feel more readily available than traditional credit, some consumers might not fully understand the conditions that come with it, like late charges, interest, or fees for late payments, which can grow very quickly. For poorer or provincial consumers whose cash flow can be intermittent, this risk is exaggerated. The social and economic consequences of high delinquency, both for consumers and for the credibility of the BNPL industry, are an acute problem in a nation where money management competencies diverge, and large segments of the population are learning for the first time how digital funding operates in reality.

Regulatory Gaps, Legal Uncertainty, and Consumer Protection Concerns

Another significant challenge is the comparatively specific under‑development of the regulatory environment for BNPL in the Philippines. While there are general consumer protection, lending, and financial services laws, no specific detailed regulation exists exclusively to cover BNPL products. This uncertain legal environment makes it more difficult for providers to act with certainty, for consumers to know their rights, and for regulators to impose standards. For instance, terms and conditions like late charges, collection procedures, disclosures, are sometimes less standardized or more ambiguous than in more developed credit markets. Some customers complain that hidden fees, uncertain repayment terms, or punitive penalties are not adequately disclosed at the onset. Enforcement of fair debt collection practices continues to develop; harassment during collections or aggressive follow‑ups are concerns many customers find disconcerting. Secondly, disjointed jurisdiction among regulators like banking regulators, trade and consumer protection regulators, digital payments regulation, can impede the development of consistent rules. Local government units or municipalities in most provinces can have different capacities of enforcement, which will result in that rural or distant consumers' protection can fall behind consumers' protection in urban areas.

Infrastructure, Trust, and Adoption Barriers

The third group of challenges are structural: technology infrastructure, consumer-merchant trust, and uneven regional adoption. In the Philippines, an archipelago of numerous rural and remote islands, there is varying reliable internet connectivity, stable mobile data, and digital payment infrastructure. There are regions where there isn't significant network coverage or access to the devices required for BNPL use. Most small retailers in small towns or provinces remain unfamiliar or reluctant to incorporate BNPL systems into their point‑of‑sale sales; some still prefer old cash or cash‑on‑delivery sales. Further, there remains a deficit of trust among consumers regarding online payments: concerns regarding fraud, unauthorized transactions, privacy invasion, or non‑delivery of goods are common apprehensions. Even when BNPL is available, some users hold back due to fear that service quality, customer support, or dispute resolution will be poor or unavailable. Lastly, cultural or behavioral credit norms, where borrowing is sometimes demeaned or where individuals shun formal financing, can hinder adoption. Conquering these obstacles involves technical investment along with education, transparency, sound consumer protection, and salient positive experiences that give credibility, particularly in rural areas.

Philippines Buy Now Pay Later Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Philippines buy now pay later market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on channel, enterprise size, and end use.

Analysis by Channel:

- Online

- Point of Sale (POS)

The online segment is expected to hold a significant share of the Philippines' Buy Now, Pay Later (BNPL) market due to the rapid growth of e-commerce and the increasing adoption of digital payment methods. People who shop online value having postponed payment solutions since their income remains restricted. Popular online retailers work with BNPL platforms which helps these retailers by increasing visibility and boosting user activity. Online shopping access has risen because of improving network connections and growing smartphone user adoption. The COVID-19 pandemic further accelerated e-commerce adoption, making BNPL a preferred option for consumers looking for flexible payment plans in an evolving digital landscape.

Point-of-sale transactions dominate a large share of the Philippines' BNPL market because they give shoppers immediate purchasing opportunities with flexible payment methodologies. User-friendly POS BNPL solutions help people buy products immediately without needing upfront payment, thus boosting their spending on major items including appliances, electronics, and home furniture. Retail partnerships and integrated BNPL systems enhance accessibility, fostering adoption across malls and physical stores. The method appeals to a wide demographic, including those without credit cards, by offering seamless payment flexibility. With retail stores adapting to meet consumer demands for affordability, POS BNPL has become a crucial driver of in-store sales growth.

Analysis by Enterprise Size:

- Large Enterprises

- Small and Medium Enterprises

Large enterprises are expected to hold a significant share of the Philippines' Buy Now, Pay Later (BNPL) market due to their extensive customer base, established infrastructure, and financial resources. These companies leverage BNPL to attract and retain customers by offering flexible payment options, especially for high-value products like electronics, appliances, and luxury items. Their partnerships with BNPL providers enhance customer convenience and spending power. Additionally, large enterprises often integrate BNPL seamlessly into online and offline sales channels, driving higher adoption rates. With strong brand trust and the ability to implement advanced payment solutions, large enterprises are key players in expanding the BNPL ecosystem.

Small and medium enterprises (SMEs) are expected to hold significant Philippines buy now pay later market share because they can quickly adapt innovative payment solutions to improve customer engagement. BNPL helps SMEs compete in a competitive industry by providing alternative flexible payment solutions that promote higher sales and customer loyalty. Retail and e-commerce businesses face a lot of competition and a lot of opening to consumers who seek affordability and falling into the trap of shopping today and paying tomorrow, many SMEs partner with BNPL providers to attract cost-conscious consumers. SMEs’ approach to growing business without draining all their resources on the payment infrastructure is consistent with the accessibility of BNPL solutions. BNPL has become a must-have when small and medium enterprises embrace digital transformation to improve sales and market competitiveness.

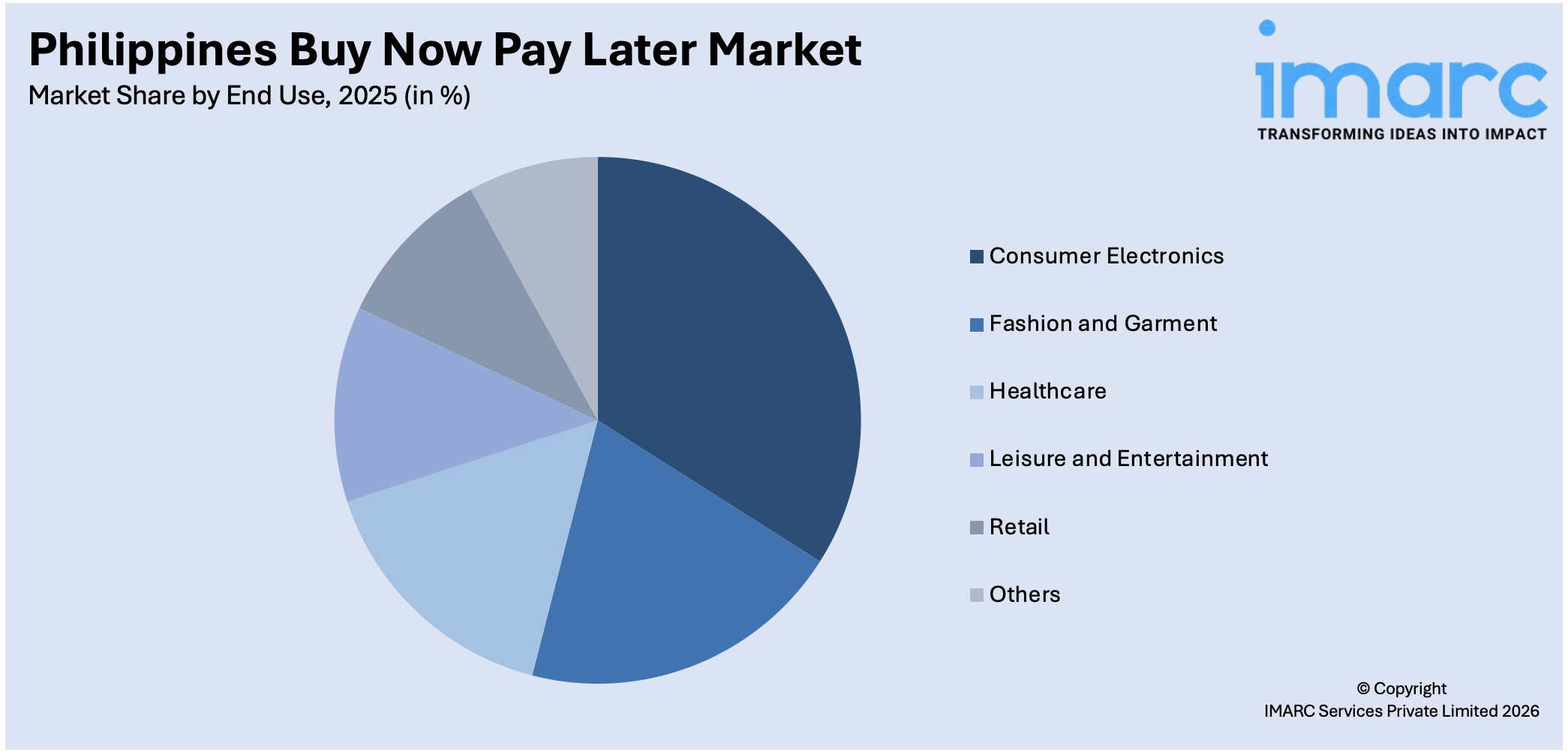

Analysis by End Use:

Access the comprehensive market breakdown Request Sample

- Consumer Electronics

- Fashion and Garment

- Healthcare

- Leisure and Entertainment

- Retail

- Others

The consumer electronics sector is expected to hold a large market share due to the high demand for expensive gadgets like smartphones, laptops, and appliances. BNPL enables consumers to access these products by spreading payments over time, making them more affordable for middle-income buyers. Retailers and e-commerce platforms offering BNPL options attract tech-savvy consumers seeking flexibility in managing their budgets. Additionally, the rapid pace of technological upgrades drives consumers to adopt BNPL solutions for purchasing the latest devices. With electronics being a priority expense, BNPL significantly supports sales growth in this sector.

Fashion and garments are key drivers of the Philippines buy now pay later market growth due to the sector’s focus on affordability and high consumer interest in clothing and accessories. BNPL aligns with consumer spending patterns, particularly for younger demographics seeking budget-friendly ways to purchase trending styles. BNPL enables online and offline retailers to attract cost-conscious shoppers to spend more without immediate financial burden. Seasonal sales and promotions increase BNPL adoption since consumers use flexible payments to maximize spending. BNPL has taken the lead for young Filipinos because of the ever-growing power of social media and e-commerce platforms.

Healthcare holds a substantial share of the Philippines' BNPL market as it addresses affordability concerns for medical expenses like consultations, procedures, and medications. BNPL enables patients to manage out-of-pocket costs by breaking them into manageable installments, ensuring access to essential services. Many healthcare providers, including clinics and pharmacies, partner with BNPL platforms to offer financial flexibility, especially for uninsured or underinsured individuals. The rising cost of healthcare and increased awareness of preventive care drive the adoption of BNPL solutions. With affordability being a critical factor in healthcare decision-making, BNPL helps bridge the gap between quality medical care and financial constraints.

Regional Analysis:

- Luzon

- Visayas

- Mindanao

Luzon drives the Philippines' Buy Now, Pay Later (BNPL) market due to its high urbanization, concentrated economic activity, and tech-savvy population. Metro Manila and nearby provinces host most large enterprises, retail outlets, and e-commerce hubs, facilitating BNPL adoption. The region's strong internet infrastructure supports digital payments, while partnerships between BNPL providers and retailers cater to diverse consumer needs. The demand for flexible financing options in consumer electronics, fashion, and healthcare further boosts BNPL usage. Additionally, Luzon’s growing middle class and younger demographics seeking budget-friendly payment solutions represent a major Philippines Buy Now Pay Later market trend in the region.

In Visayas, the BNPL market is fueled by expanding e-commerce penetration, improving digital connectivity, and rising retail activity. Cities like Cebu serve as economic and commercial hubs, where BNPL solutions cater to tech-savvy consumers and small to medium enterprises. The region’s tourism and hospitality sectors also leverage BNPL for travel-related services, appealing to locals and tourists alike. Increasing demand for affordable healthcare, gadgets, and fashion drives adoption further. With ongoing infrastructure development and digital transformation in the region, BNPL is becoming an attractive payment option for both urban and rural populations in Visayas.

The BNPL market in Mindanao is driven by rising awareness of digital payment solutions, expanding access to financial services, and increasing retail and e-commerce activity. Key cities like Davao and Cagayan de Oro act as growth centers, where BNPL caters to the needs of young, cost-conscious consumers. The region’s focus on improving digital infrastructure and financial inclusion boosts BNPL adoption, especially in underserved rural areas. Demand for affordable healthcare, electronics, and essential goods further drives the market. BNPL enables greater access to credit, empowering small businesses and consumers in Mindanao’s emerging economy to engage in more flexible spending.

Competitive Landscape:

The Philippines' Buy Now, Pay Later (BNPL) market is characterized by intense competition among local and international providers, driven by increasing consumer demand for flexible payment options. Key players include fintech companies, e-commerce platforms, and traditional financial institutions. Local firms focus on affordability and accessibility, targeting underserved segments, while global providers leverage advanced technology and strategic partnerships with major retailers. The market is shaped by collaborations with e-commerce platforms, healthcare providers, and brick-and-mortar stores. Differentiation is achieved through seamless integration, user experience, and innovative features like zero-interest plans. Rising adoption across industries intensifies competition, fostering innovation and expanding the BNPL ecosystem.

Latest News and Developments:

- In January 2024, Razer Merchant Services (RMS) and BillEase, a consumer financing app from the Philippines, announced partnership to integrate BillEase's payment solutions into RMS's merchant network to increase the availability of Buy Now, Pay Later (BNPL) services in the area.

- In December 2022, Pine Labs, a top merchant commerce omnichannel platform, and 2C2P, a global payments platform, teamed up to extend Buy Now Pay Later (BNPL) throughout Asia in six strategic markets: Singapore, Malaysia, Hong Kong, Indonesia, the Philippines, and Thailand. In contrast to other BNPL products, Pine Labs collaborates with participating banks to allow cardholders to make purchases with longer and various installment terms without needing to download any apps or sign up for extra e-wallet or payment services.

Philippines Buy Now Pay Later Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Channels Covered | Online, Point of Sale (POS) |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium Enterprises |

| End Uses Covered | Consumer Electronics, Fashion and Garment, Healthcare, Leisure and Entertainment, Retail, Others |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines buy now pay later market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Philippines buy now pay later market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines buy now pay later industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines Buy Now Pay Later Market Report

The buy now pay later market in the Philippines was valued at USD 2.5 Billion in 2025.

The growth of the market is driven by rising e-commerce adoption, increasing financial inclusion for underbanked populations, demand for flexible and affordable payment solutions, and growing partnerships with retailers and SMEs. Additionally, affordability needs in healthcare, education, and high-value purchases further propel BNPL adoption. The factors, collectively, are creating a positive Philippines buy now pay later market outlook.

The Philippines buy now pay later market is projected to exhibit a CAGR of 6.32% during 2026-2034, reaching a value of USD 4.4 Billion by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)