Philippines Cement Market Size, Share, Trends and Forecast by Type, End-Use, and Region, 2026-2034

Philippines Cement Market Summary:

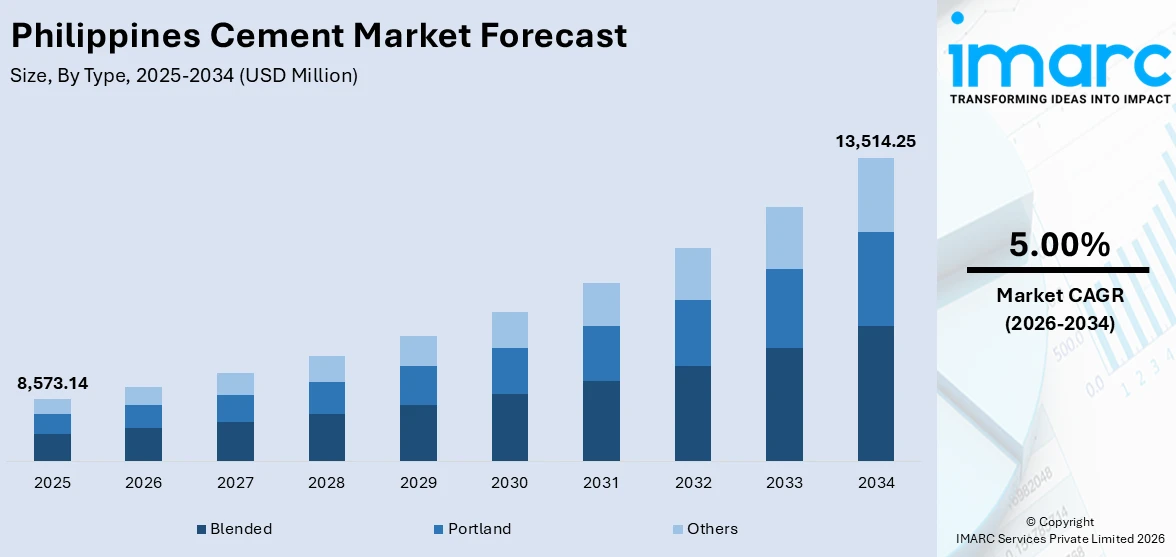

The Philippines cement market size was valued at USD 8,573.14 Million in 2025 and is projected to reach USD 13,514.25 Million by 2034, growing at a compound annual growth rate of 5.00% from 2026-2034.

The Philippines cement market is expanding steadily, driven by sustained government infrastructure investments, accelerating urbanization, and growing residential construction demand. The ongoing modernization of transportation networks, rising public-private partnerships, and expansion of industrial zones across the archipelago are strengthening cement consumption. Additionally, the increasing adoption of sustainable and blended cement solutions is reshaping product strategies, while regional development initiatives continue to diversify demand across Luzon, Visayas, and Mindanao.

Key Takeaways and Insights:

- By Type: Blended dominates the market with a share of 56.8% in 2025, owing to its cost-effectiveness, lower carbon footprint, and improved durability characteristics that align with evolving environmental regulations and green building standards across the Philippines.

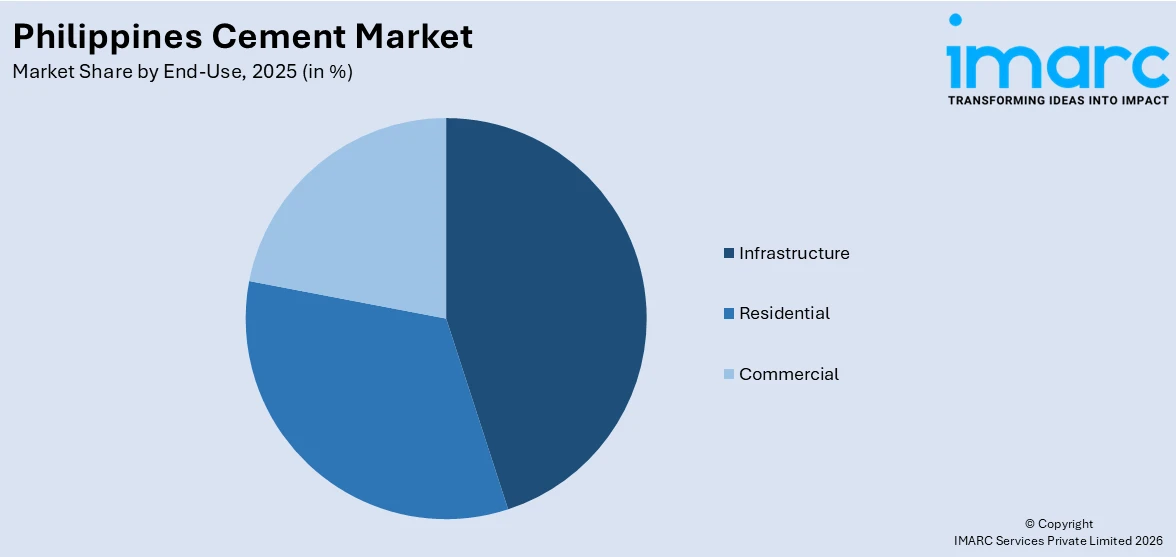

- By End-Use: Infrastructure leads the market with a share of 42.5% in 2025, driven by the government's sustained infrastructure spending under the Build Better More program, encompassing roads, railways, bridges, ports, and flood control systems across the archipelago.

- By Region: Luzon represents the largest region with 65.5% share in 2025, reflecting the concentration of major infrastructure projects, population density, commercial real estate development, and industrial activity in Metro Manila and surrounding provinces.

- Key Players: Key players drive the Philippines cement market by expanding production capacities, investing in energy-efficient technologies, strengthening distribution networks, and introducing sustainable product lines. Their focus on localized clinker production, digital operations, and strategic partnerships supports consistent supply and competitive positioning.

To get more information on this market Request Sample

The cement industry in the Philippines is acquiring increasing pace as the country speeds up its infrastructure development and modernization projects. The government’s Build Better More program, which covers a wide range of flagship projects in the areas of transport infrastructure, water resources, energy, and digital connectivity, is driving the demand for construction materials in the country. The increasing rate of urbanization, as more Filipinos continue to move to urban areas, is fueling the construction of residential and commercial buildings. The growth of industrial estates and special economic zones is also widening the demand for cement in the country. Moreover, the country’s move to finally solve its long-standing housing backlog is pouring in significant investments for socialized and affordable housing projects, especially in the country’s growth areas outside Metro Manila. The cement industry in the Philippines is adapting to the changing demands of the country’s infrastructure development needs by increasing production capacity, using energy-efficient kiln technology, and developing sustainable blended cement products that will comply with the country’s stringent environmental regulations.

Philippines Cement Market Trends:

Accelerating Adoption of Blended and Green Cement Products

The Philippine cement industry is witnessing a decisive shift toward blended and environmentally sustainable cement solutions as builders and developers increasingly prioritize lower-carbon construction materials. Regulatory pressure from the Philippine Green Building Code, combined with growing contractor preference for products with enhanced durability and workability, is driving manufacturers to expand their blended cement portfolios. In June 2023, Holcim Philippines introduced Holcim Optima, a blended Portland limestone cement that emits approximately ten percent less carbon dioxide than standard ordinary Portland cement. This shift is strengthening the Philippines cement market growth.

Digital Integration and Plant Modernization

Cement manufacturers in the Philippines are increasingly deploying digital technologies and AI-driven energy management systems to optimize production efficiency, reduce kiln downtime, and streamline supply chain operations. Plant modernization investments are prioritizing advanced clinker production technologies that improve output quality while lowering energy consumption and carbon emissions. In July 2024, Taiheiyo Cement Philippines inaugurated a PHP 12.8 Billion production line in San Fernando, Cebu, featuring state-of-the-art cement kiln renewal technology that boosted facility capacity to three Million tons annually and is expected to reduce carbon dioxide emissions by over ten percent.

Expansion of Waste Co-Processing and Alternative Fuel Utilization

Philippine cement producers are scaling the use of alternative fuels and waste co-processing programs to mitigate rising thermal energy costs and align with environmental mandates. This trend reflects a broader industry transition toward circular economy practices within cement manufacturing, where industrial waste, biomass, and refuse-derived fuels substitute traditional coal inputs. Manufacturers are investing in platforms that enable the co-processing of plastics, biomass, and industrial byproducts across their production facilities, reducing dependence on conventional fossil fuels. These initiatives are gaining traction particularly in regions with high kiln concentrations, as producers seek to improve energy efficiency, lower operational expenses, and comply with national waste reduction and emissions requirements.

Market Outlook 2026-2034:

The cement industry in the Philippines is expected to continue its growth trajectory over the forecast period, driven by the government's plan to allocate funds for infrastructure development every year until 2028. The country's transportation infrastructure, flood control systems, and connectivity projects are expected to drive demand for various types of cement. The urbanization shifts in the country, the ongoing efforts to address the housing backlog, and the development of industrial and special economic zones are also expected to diversify cement demand. The imposition of safeguard tariffs on imported cement is also expected to rationalize cement production in the country. The market generated a revenue of USD 8,573.14 Million in 2025 and is projected to reach a revenue of USD 13,514.25 Million by 2034, growing at a compound annual growth rate of 5.00% from 2026-2034.

Philippines Cement Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Type | Blended | 56.8% |

| End-Use | Infrastructure | 42.5% |

| Region | Luzon | 65.5% |

Type Insights:

- Blended

- Portland

- Others

Blended dominates with a market share of 56.8% of the total Philippines cement market in 2025.

Blended cement has established itself as the predominant product type in the Philippines, driven by its superior durability, enhanced workability, and lower carbon emissions compared to ordinary Portland cement. The incorporation of supplementary cementitious materials such as fly ash, slag, and volcanic ash reduces clinker dependency while improving long-term structural performance. Growing contractor preference for sustainable construction materials, combined with manufacturer investments in dedicated blended cement distribution terminals and logistics networks across major consumption regions, is reinforcing the shift toward environmentally responsible building solutions that align with the country's green building standards and decarbonization objectives.

The growing regulatory emphasis on environmental sustainability and the Philippine Green Building Code have further accelerated blended cement adoption across residential, commercial, and infrastructure projects. Manufacturers are actively expanding blended cement production lines and optimizing logistics to ensure consistent supply to major construction corridors. The Climate Change Service of the Department of Environment and Natural Resources has acknowledged that substituting clinker with supplementary cementitious materials is a key mitigation measure for reducing greenhouse gas emissions in the cement industry, with blended cement offering approximately 30 percent lower carbon footprint compared to standard ordinary Portland cement.

End-Use Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Infrastructure

Infrastructure leads with a share of 42.5% of the total Philippines cement market in 2025.

The infrastructure segment commands the largest share of cement consumption in the Philippines, propelled by the government's sustained commitment to large-scale public works programs. The Build Better More initiative, encompassing numerous flagship projects spanning transportation, water systems, and regional connectivity, has channeled massive construction demand into roads, railways, bridges, ports, airports, and flood control systems. Continued prioritization of infrastructure spending as a significant share of gross domestic product ensures a stable pipeline of cement-intensive projects across the nation.

Key transportation projects including commuter railway systems, subway developments, and multiple expressway expansions are generating sustained bulk cement orders across Luzon and other regions. Public-private partnerships continue to expand the scope and scale of infrastructure investments, with official development assistance and foreign investments supplementing national budget allocations. The continued upward trajectory in public construction spending directly supports cement demand across diverse project categories spanning urban transit, maritime connectivity, and rural road networks throughout the archipelago.

Regional Insights:

- Luzon

- Visayas

- Mindanao

Luzon exhibits a clear dominance with a 65.5% share of the total Philippines cement market in 2025.

Luzon accounts for the highest concentration of construction activity in the Philippines, driven by the economic primacy of Metro Manila, Central Luzon, and Calabarzon, which collectively represent the largest share of national economic output. The region hosts the majority of ongoing transportation megaprojects, including commuter railway systems, subway developments, and extensive expressway expansions, alongside urban flood control systems and port modernization initiatives that sustain robust and consistent cement demand throughout the year across both public and private construction segments.

The concentration of residential development, commercial real estate expansion, and industrial zone growth in Luzon further solidifies the region's dominant position in cement consumption. The region accounts for the majority of national cement demand, prompting manufacturers to establish dedicated distribution terminals and logistics networks to ensure timely supply to major construction corridors. This strategic positioning enables producers to efficiently serve the growing requirements of both government infrastructure contractors and private sector developers operating across the island.

Market Dynamics:

Growth Drivers:

Why is the Philippines Cement Market Growing?

Government-Led Infrastructure Investments Under the Build Better More Program

The main driving force behind the growth of the cement market in the Philippines is the continued focus of the Philippine government on large-scale infrastructure development. The Build Better More program, which replaced the Build, Build, Build program, involves a wide range of flagship projects covering transportation infrastructure, water infrastructure, digital infrastructure, and energy infrastructure. This wide-ranging investment program ensures a steady and increasing demand for cement products in every sector of the construction industry. The focus of the Build Better More program on regional connectivity projects, such as railways, highways, and port improvements, is creating a steady stream of bulk cement orders from both government and private construction contractors. Annual infrastructure spending remains a major component of the country's gross domestic product, with the Department of Public Works and Highways allocated a major share of the budget to support regional development and flagship projects.

Rapid Urbanization and Rising Residential Construction Demand

The Philippines is undergoing a rapidly urbanizing process, which is creating a substantial demand for building materials used in the construction of residential and commercial buildings. The increasing middle-class sector, urbanization, and housing backlog of the Philippines are contributing to the sustained demand for cement used in various types of buildings. The increasing urban population is driving the demand for both high-rise residential buildings in urban areas and horizontal residential developments in new suburban areas. Housing programs initiated by the Department of Human Settlements and Urban Development have created a demand for cement in growth areas outside of Metro Manila, including Davao, Iloilo, and Baguio, while the increasing disposable income and availability of housing financing from Pag-IBIG Fund are widening the scope of residential construction.

Expansion of Industrial Zones and Foreign Direct Investment Inflows

The Philippines' rising appeal as an investment destination is fueling the emergence of new industrial estates, economic zones, and manufacturing plants that require large volumes of cement. The ease of doing business and other government initiatives are encouraging foreign investments in manufacturing, logistics, and technology industries, which are all cement-demand drivers in the construction sector. The construction of new manufacturing plants, warehouses, and commercial buildings in economic zones is also fueling new consumption patterns in the cement industry. The trend is a result of rising private sector investments in megaprojects, logistics facilities, and tourism-related projects that require consistent cement supplies

Market Restraints:

What Challenges the Philippines Cement Market is Facing?

High Energy Costs and Production Expense Pressures

Cement manufacturing in the Philippines remains heavily dependent on coal and imported fuel, exposing producers to volatile energy markets and rising electricity tariffs. High thermal and electrical energy costs are compressing profit margins and limiting the ability of manufacturers to invest in modernization and capacity expansion. Grid tariff increases and bunker fuel price volatility continue to drive margin compression across the industry, with plants shifting production schedules and investing in captive solar installations to mitigate peak-hour pricing impacts.

Import Competition and Market Share Erosion

Despite provisional safeguard measures, the Philippines cement industry continues to face intense competition from imported cement, primarily from Vietnam and Indonesia. The domestic industry's market share declined as low-priced imports entered the market. Capacity utilization among local producers has fallen, weakening financial positions, reducing employment, and curtailing investment in sustainability initiatives and plant modernization.

Regulatory Complexity and Raw Material Access Constraints

Environmental regulations have made quarry permitting increasingly complex across the Philippines, particularly in Central Luzon and parts of Mindanao. Varying environmental approval procedures across local government units are delaying raw material extraction permits and new kiln investments. Several cement firms have experienced delayed project rollouts due to permitting inconsistencies and insufficient coordination between national and local regulatory frameworks, limiting expansion timelines and overall market growth potential.

Competitive Landscape:

The Philippines cement industry has a competitive environment that is dominated by local players as well as foreign-invested cement producers expanding their presence. The players are concentrating on boosting their clinker capacity, setting up new distribution terminals, and developing new cement lines that are blended and low carbon. The competition is also being fueled by investments in digitalization, predictive maintenance solutions, and alternative fuel solutions that improve cost effectiveness. Partnerships with infrastructure contractors and government procurement initiatives are helping the players win large-scale contracts. The application of safeguard duties on imported cement is giving local players a fairer competitive platform, and this is encouraging investments in modernization and optimizing capacities. The players are now working on strategies to improve market positioning and meet sustainability challenges.

Philippines Cement Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Blended, Portland, Others |

| End-Uses Covered | Residential, Commercial, Infrastructure |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Philippines Cement Market Report

The Philippines cement market size was valued at USD 8,573.14 Million in 2025.

The Philippines cement market is expected to grow at a compound annual growth rate of 5.00% from 2026-2034 to reach USD 13,514.25 Million by 2034.

Blended dominated the market with a share of 56.8%, driven by its lower carbon footprint, improved durability characteristics, regulatory preference under the Philippine Green Building Code, and growing contractor demand for sustainable construction materials.

Key factors driving the Philippines cement market include government-backed infrastructure programs, rapid urbanization, expanding residential and commercial construction, industrial zone developments, foreign investment inflows, and rising adoption of sustainable cement products.

Major challenges include high energy and production costs, intense import competition from low-priced cement, declining capacity utilization rates, complex environmental permitting requirements, raw material access constraints, and supply chain vulnerabilities linked to freight disruptions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)