Plant-Based Meat Market Size, Share, Trends and Forecast by Product Type, Source, Meat Type, Distribution Channel, and Region, 2026-2034

Global Plant-Based Meat Market Size, Share, Trends & Forecast (2026-2034)

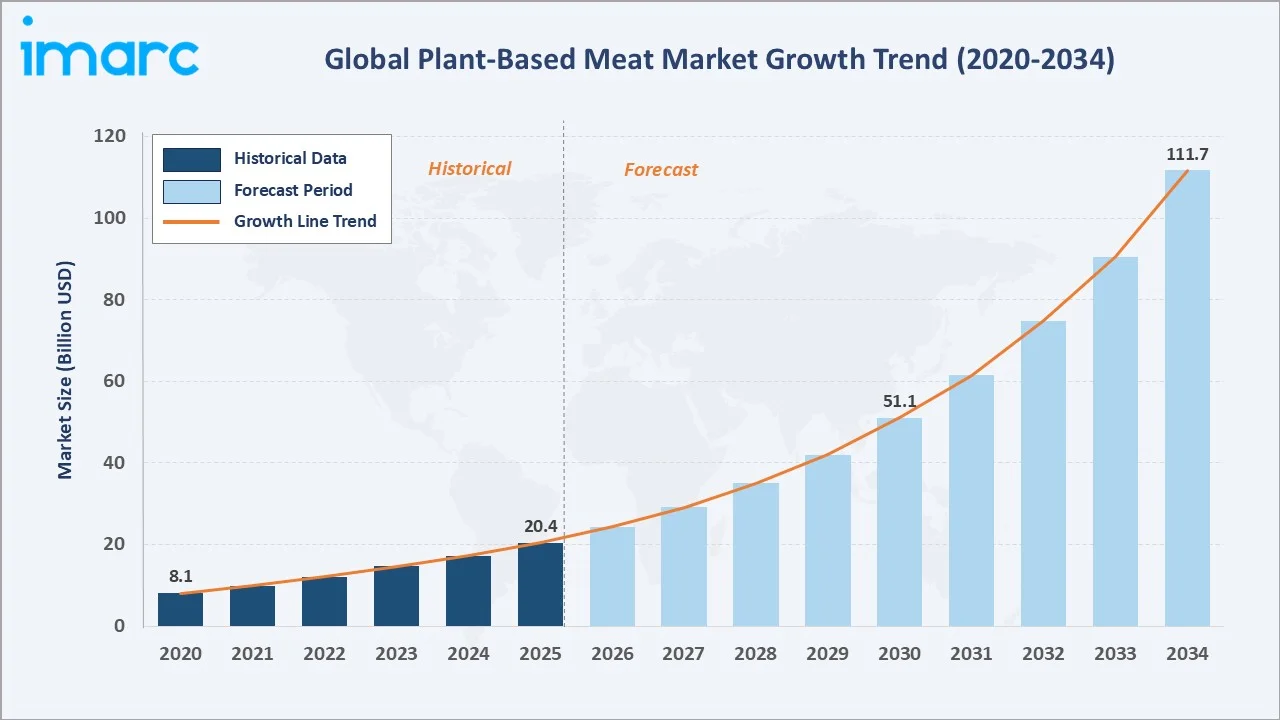

The global plant-based meat market size was valued at USD 20.4 Billion in 2025 and is projected to reach USD 111.7 Billion by 2034, exhibiting a CAGR of 20.20% during the forecast period 2026-2034. Surging consumer preference for sustainable protein, rising flexitarian adoption, growing environmental awareness, and rapid product innovation are primary drivers of plant-based meat market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size in 2025 |

USD 20.4 Billion |

|

Market Forecast in 2034 |

USD 111.7 Billion |

|

CAGR (2026-2034) |

20.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Source Segment |

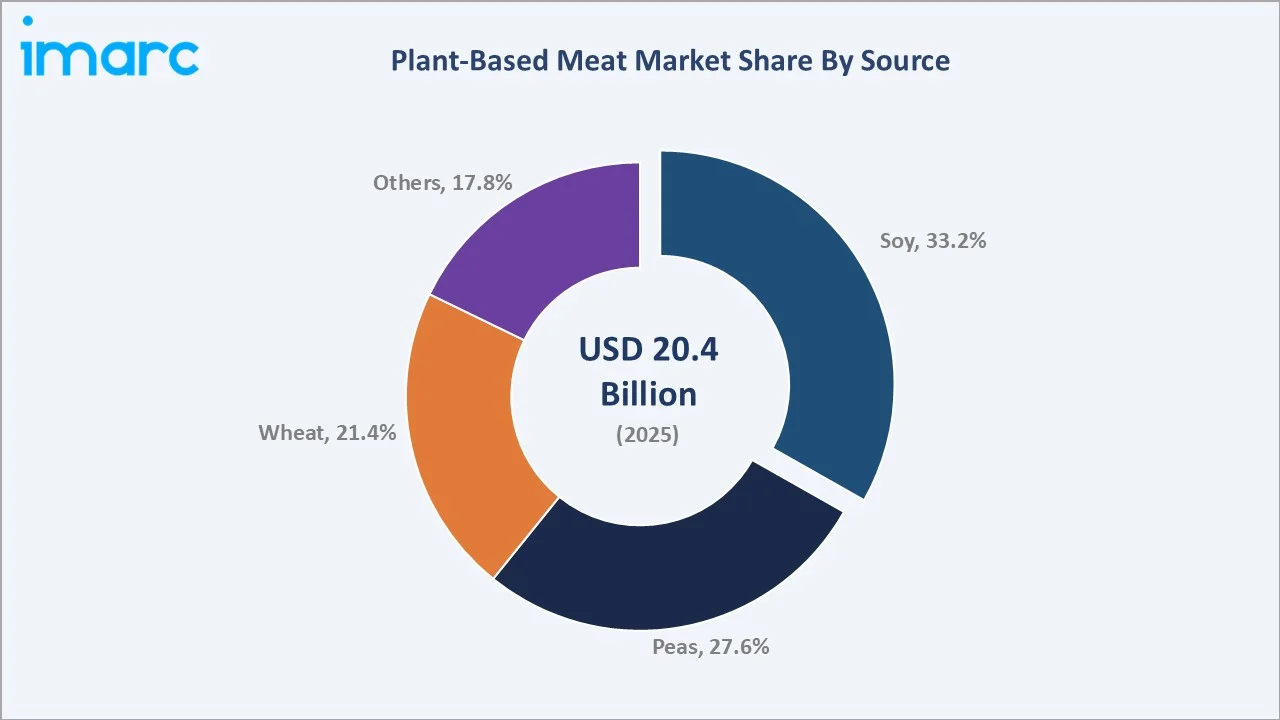

Soy Protein – 33.2% (2025) |

|

Largest Meat Type Segment |

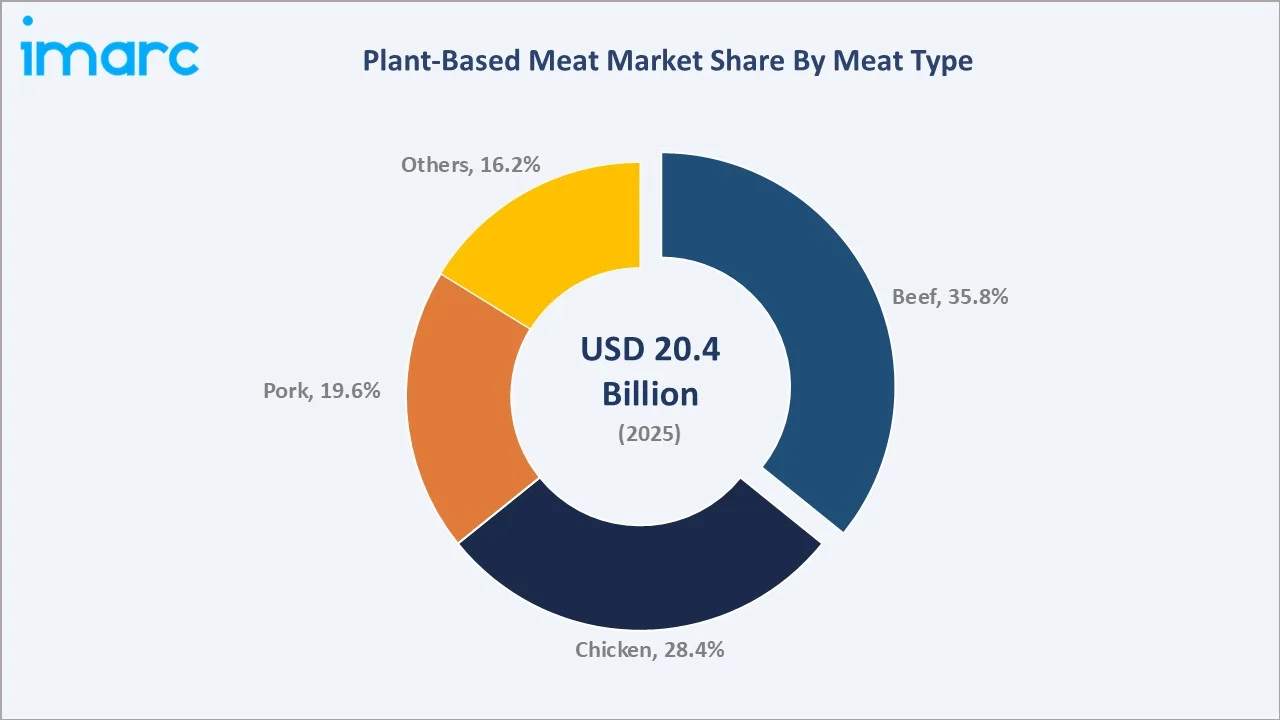

Beef – 35.8% (2025) |

|

Leading Region |

North America – 36.2% (2025) |

|

Fastest Growing Segment |

Peas Protein – est. CAGR ~18% (2026-2034) |

The market growth trajectory from 2020 through 2034 highlights historical momentum at 20.4 billion in 2025 against a strong forecast curve powered by environmental concerns, health consciousness, and expanding foodservice penetration globally.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight Asia Pacific and pea-protein sources as the fastest-growing sub-categories within the global plant-based meat market forecast through 2034.

Executive Summary

The global plant-based meat market is undergoing a profound structural transformation. It is driven by shifting dietary habits, rising environmental awareness, and accelerating consumer demand for sustainable protein alternatives. Valued at USD 20.4 Billion in 2025, the market is forecast to reach USD 111.7 Billion by 2034, representing a CAGR of 20.20% - one of the highest growth trajectories in the global food and beverage sector.

Soy-based sources dominate with a 33.2% revenue share in 2025, underpinned by mature supply chains and broad product compatibility. Beef lead the meat-type breakdown at 35.8%, fueled by widespread burger-patty formats and QSR partnerships. Retail and e-commerce penetration continues to expand access across emerging markets, with platforms such as Amazon Fresh and Plantaway (India) driving online adoption.

North America commands 36.2% global revenue, anchored by the United States' mature retail infrastructure and strong flexitarian population. Europe holds 27.4%, characterized by robust sustainability regulations and premium product demand. The plant-based meat market outlook remains highly positive as precision fermentation, improved texturization, and price-parity milestones reshape competitive dynamics through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Source Segment |

Soy - 33.2% share (2025) |

|

Second Source Segment |

Peas - 27.6% share (2025) |

|

Largest Meat Type |

Beef - 35.8% share (2025) |

|

Fastest Growing Meat Type |

Chicken - ~22.1% CAGR (2026-2034) |

|

Leading Region |

North America - 36.2% revenue share (2025) |

|

Top Companies |

Beyond Meat Inc., Impossible Foods Inc., Monde Nissin, Maple Leaf Foods, and Fazenda Futuro |

|

Market Opportunity |

Price parity is expected to be achieved in the coming years; India is emerging as the fastest-growing market |

Key Analytical Observations:

- Soy's 33.2% dominance in 2025 reflects its established protein isolation infrastructure, cost advantages, and compatibility with burger patties, sausages, and nugget formats globally.

- Peas are the fastest-growing source segment at an estimated ~22.8% CAGR through 2034, driven by cleaner labels, allergen-free positioning, and rising adoption in North American and European markets.

- Beef' 35.8% share is underpinned by mainstream burger-patty demand. Companies like Beyond Meat and Impossible Foods continue to drive significant retail traction in the U.S., reflecting sustained consumer adoption of plant-based protein products.

- North America's 36.2% revenue dominance, supported by a large base of flexitarian consumers in the United States, along with widespread grocery retail availability and expanding quick-service restaurant (QSR) menu offerings that continue to drive adoption.

- Asia Pacific is the fastest-growing region at ~23.5% CAGR, powered by India's growing vegetarian consumer base, government-backed protein diversification, and new entrants like Plantaway.

- Retail and e-commerce channels are reshaping access, with online plant-based meat sales projected to grow at ~25% CAGR through 2030, outpacing traditional supermarket channels.

Global Plant-Based Meat Market Overview

Plant-based meat refers to food products designed to replicate the taste, texture, and nutritional profile of conventional animal meat using proteins derived from plants such as soy, peas, wheat, and mycoprotein. The market encompasses burger patties, sausages, nuggets, strips, and whole-cut formats, serving retail, foodservice, and institutional end users globally.

The industry ecosystem spans protein ingredient suppliers, food technology innovators, OEM manufacturers, cold-chain logistics providers, and diverse distribution channels including supermarkets, QSRs, and e-commerce platforms. Macroeconomic influences including climate change policy, evolving food labeling regulations, and rising per-capita protein demand in developing economies are reshaping the industry's growth trajectory and investment landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

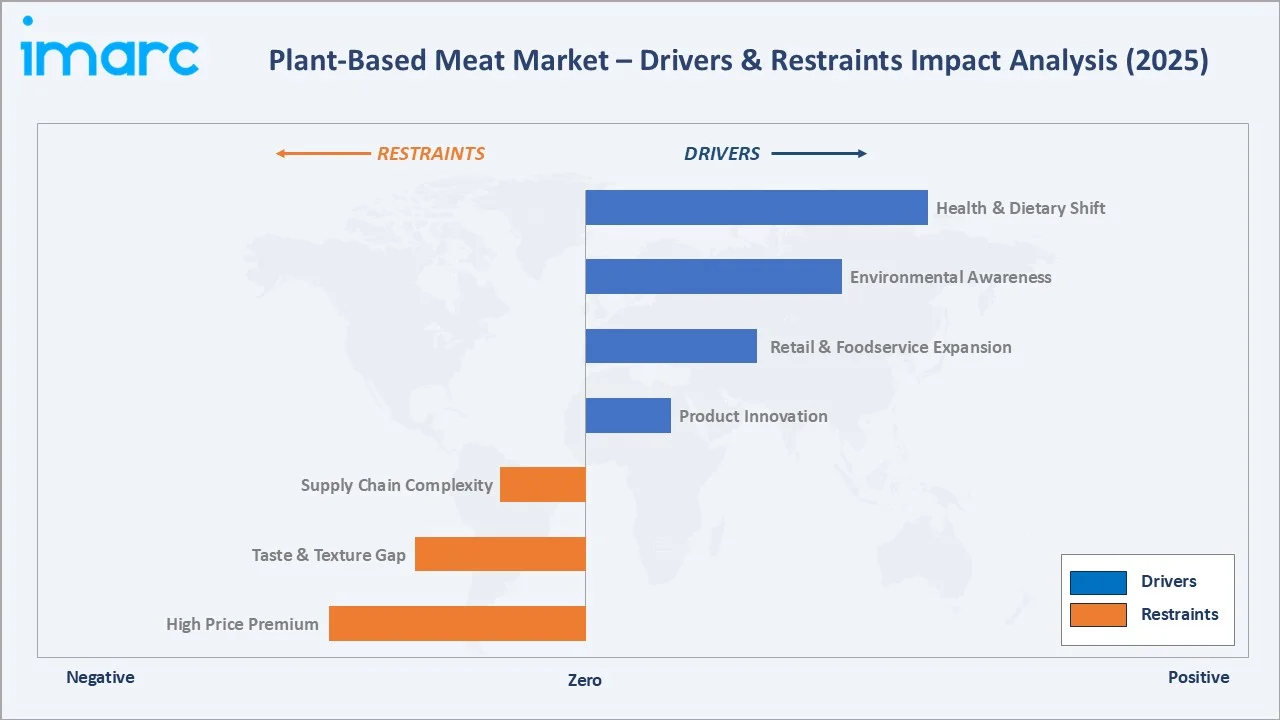

Market Drivers

- Health and Dietary Shift: The global flexitarian population is expanding rapidly. Approximately 22% of the world's population adheres to a vegetarian diet - are actively seeking meat-like texture alternatives. Rising prevalence of chronic diseases linked to red meat consumption is driving dietary substitution across developed and emerging markets.

- Rising Environmental Awareness: In a survey conducted in the United States, a majority of consumers expressed concern about climate change and recognized the environmental impact of food production. Life cycle assessment studies indicate that partially replacing ground beef with plant-based proteins can significantly reduce greenhouse gas emissions, water usage, and land requirements.

- Retail and Foodservice Expansion: Major QSR chains globally have introduced plant-based menu items, expanding consumer touchpoints. In June 2024, Tender Food secured USD 11 million in Series A funding and partnered with Clover Food Lab to feature its vegan meats.

- Product Innovation and Technology Advances: Improvements in texturization, flavoring, and nutritional fortification have narrowed the organoleptic gap with conventional meat. In July 2024, Plantaway launched India's first plant-based chicken fillet made from pea protein.

Market Restraints

- High Price Premium: Plant-based meat products continue to be priced at a noticeable premium compared to conventional meat, which remains a key barrier to widespread adoption, particularly among cost-sensitive consumers in emerging markets.

- Taste and Texture Gap: Despite rapid improvement, a subset of consumers - particularly older demographics - remain unconvinced by the sensory experience of plant-based products compared to animal meat.

- Supply Chain and Cold-Chain Complexity: Maintaining product freshness requires sophisticated cold-chain infrastructure, increasing logistics costs and limiting penetration in underdeveloped markets with inadequate refrigeration networks.

Market Opportunities

- Precision Fermentation and Cost Reduction: Advances in precision fermentation are enabling scalable production of key proteins and flavor compounds, significantly improving product quality and cost efficiency. This progress is expected to accelerate the pathway toward price parity with conventional meat, supporting broader adoption of plant-based alternatives.

- Emerging Markets - India and Southeast Asia: India's large vegetarian consumer base and the government's protein diversification initiatives create a structural demand foundation. Southeast Asia's expanding middle class and urbanization further present a high-growth opportunity for localized plant-based formats.

- Institutional and B2B Foodservice Procurement: Hospitals, corporate cafeterias, airlines, and school nutrition programs represent large-volume, specification-grade procurement channels with strong sustainability mandates.

Market Challenges

- Regulatory Labeling Complexity: Divergent regulations across markets regarding the use of terms such as "meat," "burger," and "sausage" for plant-based products create compliance challenges and restrict marketing strategies across jurisdictions.

- Consumer Perception and Ingredient Scrutiny: A segment of health-conscious consumers views highly processed plant-based products with skepticism, citing long ingredient lists and sodium levels. Manufacturers must balance taste achievement with "clean label" demands.

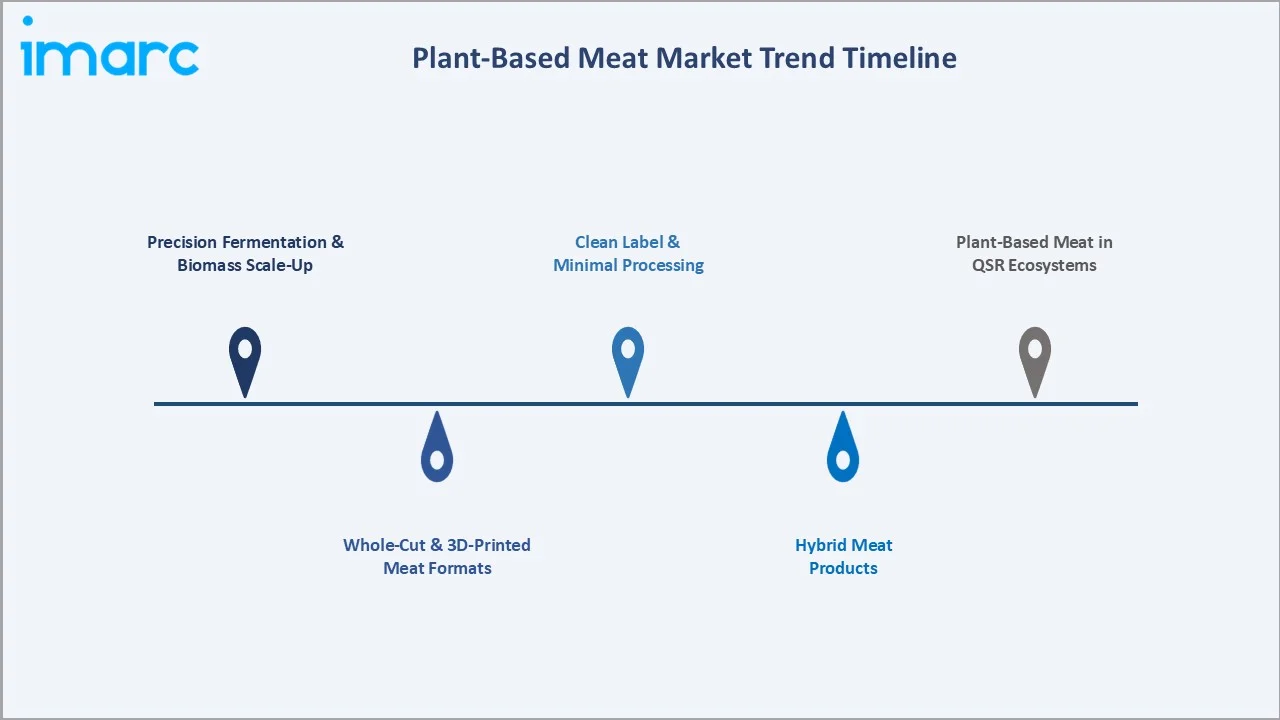

Emerging Market Trends

1. Precision Fermentation and Biomass Scale-Up

Precision fermentation is enabling the production of heme proteins, casein, and complex flavor compounds that mirror animal-derived ingredients. Companies are scaling bioreactor capacity to reduce production costs, targeting a cost crossover with soy protein by 2028-2030.

2. Whole-Cut and 3D-Printed Meat Formats

Consumer demand for steak, chicken breast, and whole-fish alternatives is driving investment in 3D food printing and extrusion technologies. NovaMeat and Redefine Meat are leading this space, targeting premium foodservice and fine-dining channels where texture fidelity is critical.

3. Hybrid Meat Products

Blended products combining small amounts of animal protein with plant-based extenders are gaining traction among flexitarians. Hybrid burgers and sausages offer improved taste at lower price points, acting as a transition gateway for mainstream consumers.

4. Clean Label and Minimal Processing

Brands are increasingly reformulating products to simplify ingredient lists, reduce sodium content, and eliminate artificial additives. Clean-label offerings with shorter ingredient lists are gaining traction in premium retail segments, particularly in regions such as North America and Northern Europe, where consumers are willing to pay a premium for perceived quality and transparency.

5. Plant-Based Meat in Quick Service Restaurants (QSR) Ecosystems

Global QSR chains such as McDonald's, Burger King, and KFC are continuing to expand plant-based menu offerings across international markets. These partnerships provide significant scale and visibility, reinforcing foodservice as a key growth channel for plant-based products, with strong consumer uptake validating long-term demand.

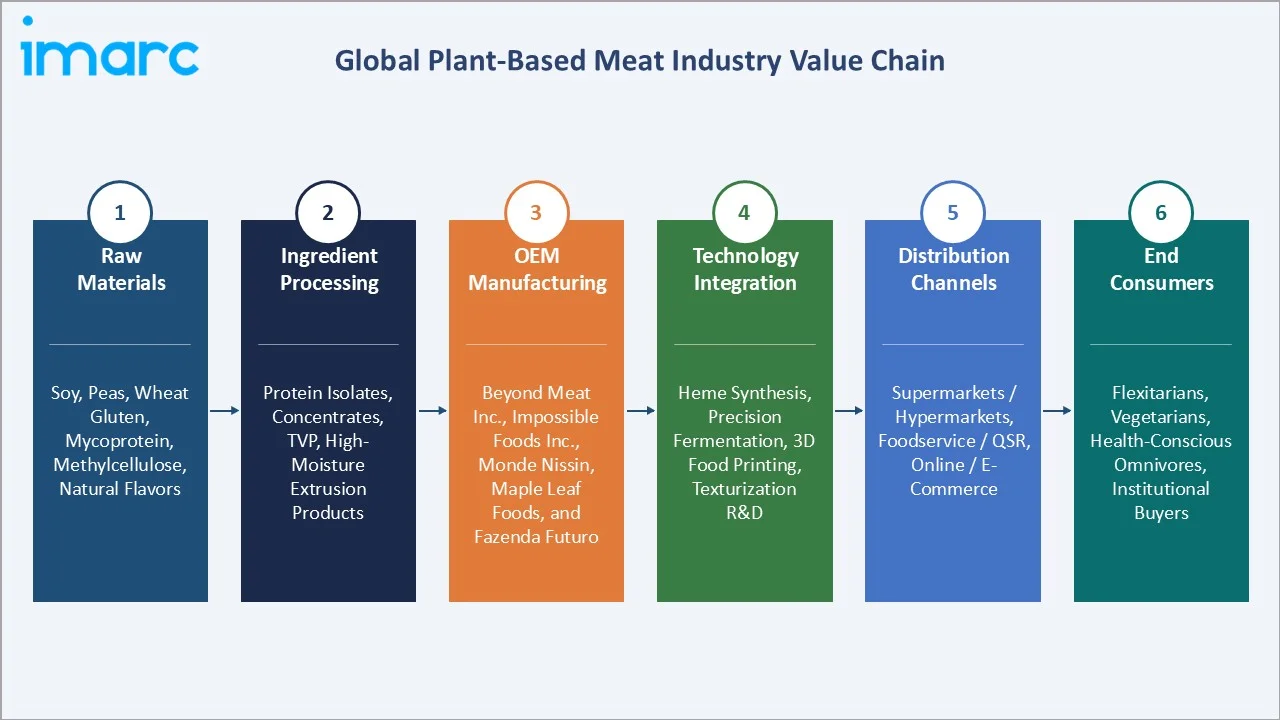

Industry Value Chain Analysis

The global plant-based meat industry value chain spans six integrated stages from raw material sourcing through consumer purchase. Each stage presents distinct competitive dynamics and margin profiles relevant to overall plant-based meat market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Soy, peas, wheat gluten, mycoprotein, methylcellulose, coconut oil, natural flavors - sourced from agri-commodity suppliers in the U.S., Canada, Netherlands, and China |

|

Ingredient Processing |

Protein isolates and concentrates, texturized vegetable protein (TVP), high-moisture extrusion products |

|

OEM Manufacturing |

Beyond Meat Inc., Impossible Foods Inc., Monde Nissin, Maple Leaf Foods, Fazenda Futuro- full product assembly, flavoring, shaping, and cold-chain packaging |

|

Technology Integration |

Heme/leghemoglobin synthesis, precision fermentation platforms, 3D food printing systems, texturization R&D - led by Impossible Foods, NovaMeat, and Redefine Meat |

|

Distribution Channels |

Supermarkets and hypermarkets, foodservice/QSR, online/e-commerce |

|

End Users |

Flexitarian and vegetarian consumers, health-conscious omnivores, institutional buyers (hospitals, schools, airlines), and corporate catering segments |

OEMs hold the highest strategic value by integrating protein science, product design, and brand equity. Meanwhile, e-commerce and direct-to-consumer channels are reshaping distribution and allowing manufacturers to capture higher margins while building direct consumer relationships.

Technology Landscape in the Plant-Based Meat Industry

High-Moisture Extrusion (HME) Technology

HME is the dominant manufacturing process for plant-based whole-cut formats, using controlled heat and moisture to create fibrous, meat-like textures from pea and soy protein concentrates. Advances in screw geometry and die design are enabling production of chicken-breast and pulled-pork analogs with improved fiber alignment at commercial scale.

Precision Fermentation and Synthetic Biology

Precision fermentation uses engineered microorganisms to produce targeted proteins—such as soy leghemoglobin (heme) that are central to the flavor differentiation strategy of Impossible Foods. As production scales and technology advances, costs for fermentation-derived proteins are declining rapidly, supporting broader application across multiple product categories and accelerating mainstream adoption.

3D Food Printing and Structured Protein Assembly

Companies including NovaMeat and Redefine Meat are deploying multi-nozzle 3D printing systems capable of producing complex protein structures mimicking whole-cut steak and lamb at premium foodservice scales. Production costs remain high, but continued scale-up.

Sustainable Ingredient Innovation

Mycoprotein (derived from Fusarium venenatum fungus) is gaining traction as a high-fiber, complete-protein alternative - the core of Quorn's product portfolio. Duckweed, algae, and insect-derived proteins are also under development as next-generation feedstocks with significantly lower land and water footprints than soy or peas.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Burger Patties |

31.8% |

2025 |

|

Source Type |

Soy |

33.2% |

2025 |

|

Meat Type |

Beef |

35.8% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

36.9% |

2025 |

|

Region |

North America |

36.2% |

2025 |

By Source

To access detailed market analysis, Request Sample

Soy dominates the global plant-based meat market by source with a 33.2% share in 2025. Soy protein's versatility, established processing infrastructure, and competitive cost position make it the backbone of the industry.

By Meat Type

Beef dominates the global plant-based meat market by type, accounting for a leading share of approximately 35.8%. Its strong position is driven by widespread consumer familiarity with burger and ground meat formats, along with extensive foodservice integration and product innovation, making it the cornerstone of the plant-based meat category.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.2% |

Flexitarian population, QSR adoption |

|

Europe |

27.4% |

EU Green Deal, sustainability mandates |

|

Asia Pacific |

21.6% |

India vegetarian base, China plant-forward trend, Plantaway India launch |

|

Latin America |

8.1% |

Brazil urban middle class, Fazenda Futuro growth, growing retail access |

|

Middle East & Africa |

6.7% |

Halal-certified PBM demand, UAE foodservice innovation, health awareness |

North America commands 36.2% global revenue share in 2025. The United States is the world's largest plant-based meat market, with approximately 18 million self-identified flexitarians and a robust retail infrastructure supporting products from Beyond Meat, Impossible Foods, and Lightlife Foods. The U.S. plant-based meat retail market surpassed USD 1.5 billion in 2024. Canada's Maple Leaf Foods - operating the largest plant-based protein facility in North America - is a key regional contributor. North America is also the leading market for QSR plant-based menu integration.

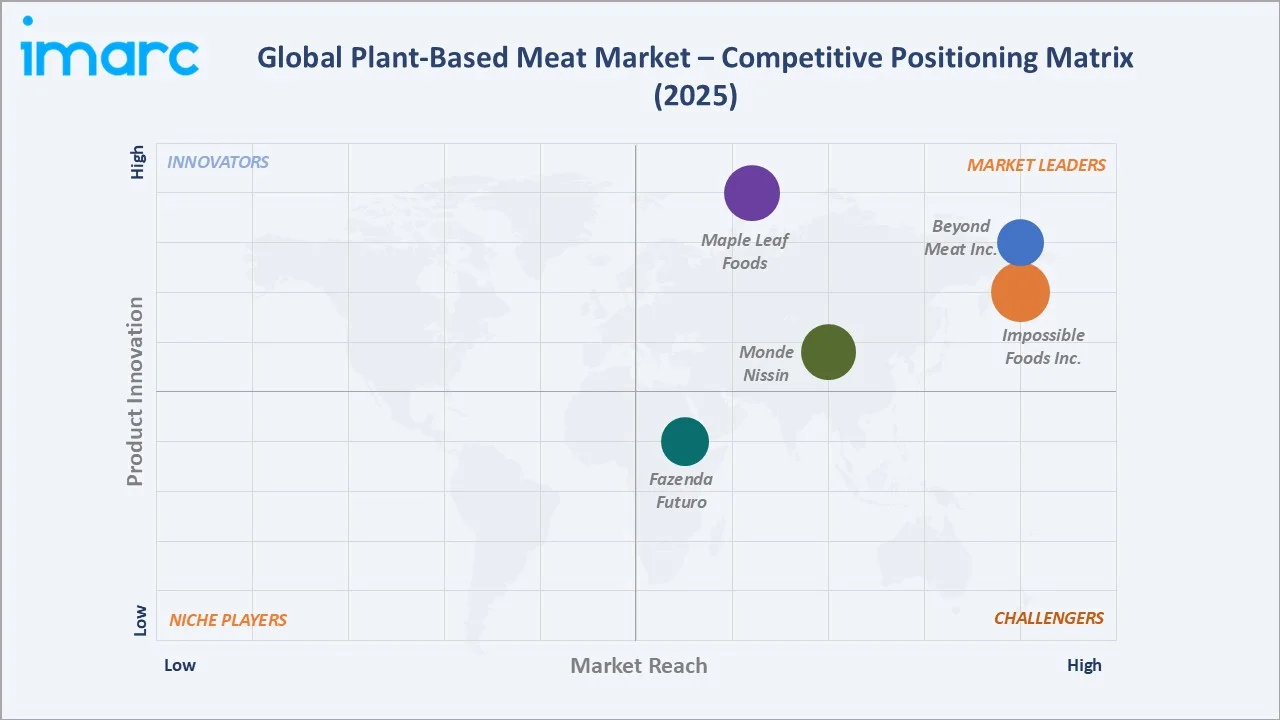

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Beyond Meat Inc. |

Beyond Burger, Beyond Beef |

Leader |

Retail scale, QSR partnerships, pea protein IP |

|

Impossible Foods Inc. |

Impossible Burger |

Leader |

Heme technology, flavor differentiation, foodservice |

|

Monde Nissin |

Quorn Foods |

Leader |

Mycoprotein IP, European market depth, low-calorie positioning |

|

Maple Leaf Foods |

Lightlife, Field Roast |

Challenger |

Largest North America plant-based production facility |

|

Fazenda Futuro |

Fazenda Futuro |

Challenger |

Latin American market leadership, hybrid product portfolio |

The global plant-based meat competitive landscape is moderately concentrated at the top tier, with strong fragmentation in mid- and emerging-player segments.

Key Company Profiles

Beyond Meat Inc.

Beyond Meat, Inc. is a U.S.-based food technology company specializing in plant-based meat alternatives designed to replicate the taste, texture, and cooking experience of animal protein using ingredients derived from plants.

- Product Portfolio: Beyond Meat's product portfolio includes the Beyond Burger, Beyond Sausage, Beyond Meatballs, Beyond Chicken Tenders, and the new Beyond Sun Sausage line. Products are based on pea protein isolate with added coconut oil, rice protein, and natural flavors.

- Recent Developments: In 2024, Beyond Meat Inc. announced the expansion of its Beyond IV product line with the launch of a new, fourth generation Beyond Sausage across U.S. retail channels. The updated product features improved taste, texture, and nutritional profile, reinforcing the company’s focus on advancing plant-based meat offerings. This move highlights continued innovation in the plant-based meat category, as brands work to enhance product quality and drive broader consumer adoption.

- Strategic Focus: Beyond Meat’s strategy centers on achieving price parity with conventional beef, expanding international QSR partnerships, and leveraging manufacturing scale to reduce cost per kilogram. The company is investing in next-generation protein isolate technology to improve margins.

Impossible Foods Inc.

Impossible Foods Inc. is food technology company focused on developing plant-based substitutes for animal meat and dairy products, using bioengineered ingredients to replicate the taste, texture, and cooking behavior of conventional meat. Company headquartered in Redwood City, California, United States.

- Product Portfolio: Impossible Foods Inc. offers the Impossible Burger, Impossible Sausage (Original and Spicy), Impossible Pork, Impossible Chicken Nuggets, and Impossible Beef Lite. Products target both retail grocery and foodservice channels, with presence in 30,000+ foodservice locations globally.

- Recent Developments: In early 2023, Impossible Foods Inc. announced the launch of its leanest and most protein-packed plant-based beef product, designed to compete directly with lean ground animal meat. The new offering delivers high protein content with significantly lower saturated fat and zero cholesterol, while maintaining taste and cooking performance similar to conventional beef.

- Strategic Focus: Impossible Foods Inc. is focused on FDA-approved heme protein scaling, expanding its patent portfolio in flavor chemistry, and entering new protein categories including fish and dairy alternatives. International expansion in Asia Pacific and Europe are key medium-term priorities.

Monde Nissin

Monde Nissin is a leading Philippine food and beverage company with a diversified portfolio spanning instant noodles, biscuits, packaged foods, and plant-based protein products. Quorn Foods, a subsidiary of Monde Nissin. It is the world's leading mycoprotein-based food company.

- Product Portfolio: Quorn's portfolio encompasses over 100 products including nuggets, mince, fillets, sausages, and ready meals. All core products are mycoprotein-based, offering a complete protein with high fiber content at significantly lower caloric density than conventional meat.

- Recent Developments: In 2025, Monde Nissin is renewing its strategic focus on the plant-based meat segment, aiming to drive growth in its alternative protein portfolio amid evolving market dynamics. The company is emphasizing brand repositioning, product reformulation, and targeted marketing initiatives for its Quorn business to enhance consumer appeal and improve performance.

- Strategic Focus: Monde Nissin’s strategy focuses on mycoprotein brand leadership, sustainability differentiation (including carbon footprint labeling), and expansion into high-growth markets in North America and Asia Pacific through both retail and foodservice distribution.

Market Concentration Analysis

The global plant-based meat market exhibits moderate concentration at the premium branded tier. The top five players - Beyond Meat Inc., Impossible Foods Inc., Monde Nissin, Maple Leaf Foods, Fazenda Futuro- collectively account for an estimated 38-45% of global branded retail revenue in 2025.

The market features a bifurcated structure. At the premium OEM tier, consolidation is occurring around brand equity, proprietary protein technology IP, and QSR partnership exclusivity. Simultaneously, a large ecosystem of regional and emerging players is generating competitive diversity across sub-premium and localized product categories.

The overall market fragmentation index remains high due to low entry barriers in basic extrusion-based product manufacturing. However, barriers to competing at scale - driven by supply chain complexity, cold-chain requirements, technology IP, and marketing investment - are creating structural differentiation between leaders and followers. Consolidation through M&A activity is expected to accelerate through 2028-2030 as the market matures.

Investment & Growth Opportunities

Fastest-Growing Segments

Pea-based source alternatives represent the fastest-growing ingredient segment, driven by strong adoption across next-generation plant protein formulations. E-commerce and direct-to-consumer plant-based meat sales are emerging as the most rapidly expanding distribution channel, supported by shifting online purchasing behavior. Chicken-type alternatives are the fastest-growing meat-type segment, fueled by global demand for nugget and tender formats popularized across quick-service restaurant menus.

Emerging Market Expansion

India represents the highest-potential emerging market - around 33% of the Indian population is vegetarian and a growing urban middle class increasingly receptive to processed protein products. In July 2024, Plantaway's pea-protein chicken fillet launch validated the commercial opportunity. Southeast Asia's foodservice expansion, ASEAN urbanization, and China's protein security policy collectively represent the next major investment frontier for global and regional plant-based meat brands.

Venture and Strategic Investment Trends

Venture and corporate investment in the plant-based meat sector remained significant globally, with funding directed toward next-generation innovation platforms, including fermentation-based technologies, texture enhancement solutions, and expansion-focused ventures in the Asia Pacific region. Key strategic investment themes include improving the cost efficiency of precision fermentation, advancing clean-label reformulation, developing halal-certified product offerings, and integrating procurement platforms tailored for B2B foodservice channels.

Future Market Outlook (2026-2034)

The global plant-based meat market forecast projects sustained high-growth value expansion from USD 20.4 Billion in 2025 to USD 111.7 Billion by 2034, at a CAGR of 20.20%. This trajectory is underpinned by five structural tailwinds: environmental policy alignment, demographic dietary transition, technology cost reduction, expanding retail access, and QSR institutionalization of plant-based menu items.

Asia Pacific will transition from the third-largest region in 2025 to the second largest by 2030, surpassing Europe on volume growth alone. North America will retain value leadership through premium segment expansion. Price parity between plant-based Beef and conventional ground beef is projected by approximately 2028-2030 in the U.S. market, which is expected to unlock mainstream omnivore adoption at scale.

Precision fermentation and 3D food printing represent the two most disruptive technological forces through 2034. Fermentation-derived heme and flavor proteins will reduce sensory gaps with animal meat, while 3D printing will enable premium whole-cut formats at competitive margins. Companies investing early in these platforms are positioned to capture disproportionate market share as technology costs decline through the forecast period.

Research Methodology

Primary Research

Primary research includes in-depth interviews with senior executives across the plant-based meat value chain - including ingredient suppliers, OEM manufacturers, retail buyers, foodservice operators, and industry analysts. IMARC Group conducted over 150 primary interviews globally, supplemented by consumer surveys across North America, Europe, and Asia Pacific targeting flexitarian and vegetarian demographics.

Secondary Research

Secondary research encompasses analysis of company annual reports, SEC filings, investor presentations, trade association publications (Good Food Institute, ProVeg International), regulatory filings (FDA, EFSA, FSSAI), and industry trade publications. Macroeconomic and demographic data are sourced from the World Bank, FAO, and national statistical agencies.

Forecasting Models

Market forecasts are generated using a combination of top-down and bottom-up modeling approaches. Bottom-up estimation builds the market from country-level protein consumption data, demographic trends, and per-capita plant-based adoption rates. Top-down validation uses total addressable market sizing derived from the global alternative protein sector. CAGR projections are validated against historical actuals and cross-referenced with primary research findings.

Plant-Based Meat Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Burger Patties, Sausages, Nuggets and Strips, Ground, Meat, Meatballs, Others |

| Sources Covered | Soy, Wheat, Peas, Others |

| Meat Types Covered | Chicken, Beef, Pork, Others |

| Distribution Channels Covered | Restaurants and Catering Industry, Supermarkets and Hypermarkets, Convenience and Specialty Stores, Online Retail |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, United Kingdom, Germany, Italy, France, Netherlands, Sweden, China, Australia, South Korea, Brazil, Mexico, Turkey, Saudi Arabia, UAE |

| Companies Covered | Beyond Meat Inc., Impossible Foods Inc., Monde Nissin, Maple Leaf Foods, Fazenda Futuro, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the plant-based meat market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global plant-based meat market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the plant-based meat industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Plant-Based Meat Market Report

The global plant-based meat market was valued at USD 20.4 Billion in 2025. It is expected to reach USD 111.7 Billion by 2034, growing at a CAGR of 20.20%.

Key drivers include rising flexitarian adoption, environmental awareness, product innovation in texture and flavor, expanding QSR partnerships, and increasing retail distribution globally.

North America leads with a 36.2% revenue share in 2025, driven by the U.S.' mature retail infrastructure, large flexitarian population, and QSR market integration.

Soy holds the largest source segment share at 33.2% in 2025, supported by mature supply chains, cost efficiency, and wide product application versatility.

Asia Pacific is the fastest-growing region at approximately 23.5% CAGR through 2034, powered by India's vegetarian consumer base, China's protein policy, and Southeast Asia's urbanization.

Leading players include Beyond Meat Inc., Impossible Foods Inc., Monde Nissin, Maple Leaf Foods, and Fazenda Futuro.

Key technologies include high-moisture extrusion, precision fermentation for heme proteins, 3D food printing for whole-cut formats, and sustainable novel protein development from mycoprotein and duckweed.

The global plant-based meat market is estimated to reach approximately USD 51.1 Billion by 2030, representing strong mid-period growth at a sustained 20%+ CAGR from the 2025 base.

QSR integration is emerging as a major growth channel. The McPlant burger has achieved large-scale global sales, reinforcing foodservice as a key mainstream channel for consumer trial and broader adoption of plant-based offerings.

Key challenges include high price premiums vs. conventional meat, persistent taste-texture gaps for certain consumer segments, regulatory labeling complexity, and cold-chain infrastructure requirements in emerging markets.

The global plant-based meat market is projected to grow at a CAGR of 20.20% during the forecast period 2026-2034, making it one of the fastest-growing segments in food and beverages.

Beef lead at 35.8% share in 2025, followed by chicken at 28.4%, pork alternatives at 19.6%, and other meat types at 16.2%, per IMARC Group 2025 analysis.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)