Plywood Market Size, Share, Trends and Forecast by Residential and Commercial Application, New Construction and Replacement Sector, and Region 2026-2034

Global Plywood Market Size, Share, Trends & Forecast (2026-2034)

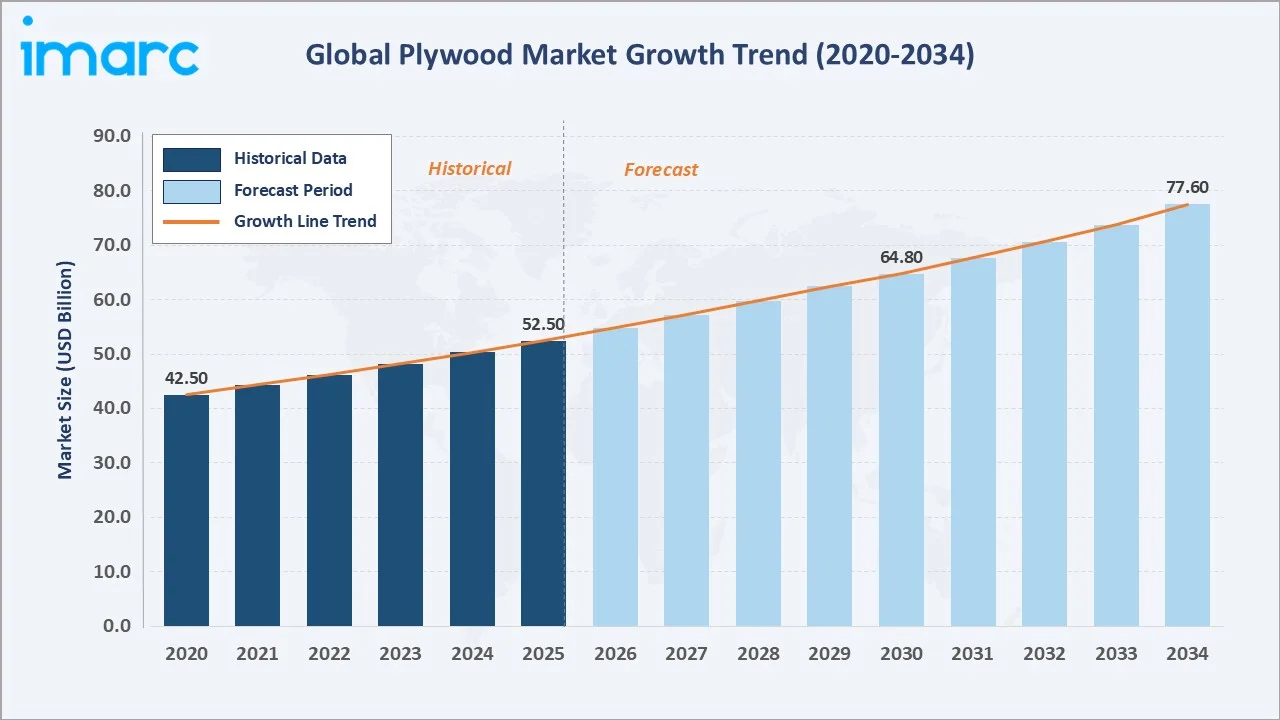

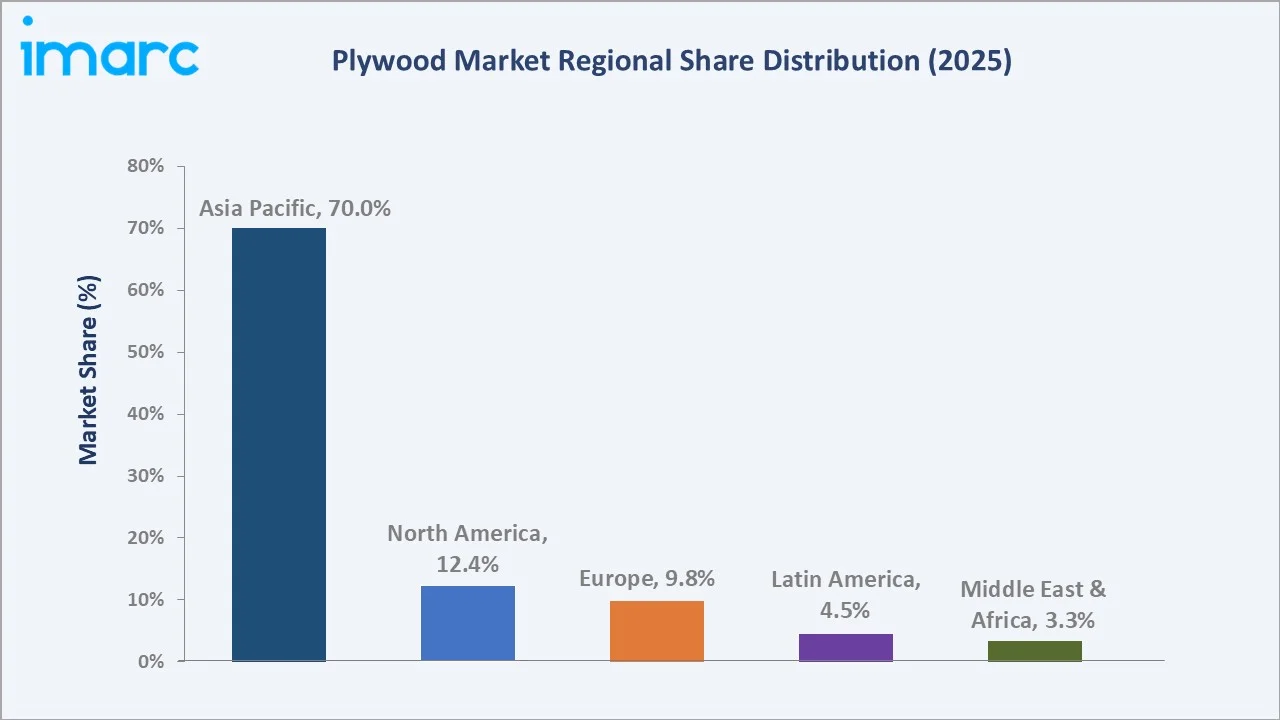

The global plywood market was valued at USD 52.5 Billion in 2025 and is projected to reach USD 77.6 Billion by 2034, exhibiting a CAGR of 4.31% during 2026-2034. Asia Pacific currently dominates the market, holding over 70.0% of the global share in 2025. The steady growth of the plywood market growth trajectory is underpinned by accelerating urbanization, escalating residential and commercial construction, surging government expenditure on affordable housing, and growing consumer preference for engineered wood products with superior durability and sustainability credentials.

Market Snapshot

|

Report Attribute |

Key Statistics |

|

Base Year |

2025 |

|

Forecast Years |

2026-2034 |

|

Historical Years |

2020-2025 |

|

Market Size in 2025 |

USD 52.5 Billion |

|

Market Forecast in 2034 |

USD 77.6 Billion |

|

Market Growth Rate (2026-2034) |

4.31% CAGR |

The global plywood market has exhibited consistent expansion, reflecting strong underlying demand across construction and furniture sectors even through pandemic disruptions. The rapid rise of urban populations across Asia, the Middle East, and Latin America has intensified the need for residential infrastructure, positioning plywood as the material of choice for flooring, wall sheathing, roofing, and interior paneling due to its cost efficiency, dimensional stability, and ease of fabrication.

Government programs targeting affordable housing and infrastructure renewal, particularly India’s PMAY scheme targeting millions of urban households, along with rising disposable income levels in emerging economies are structurally reinforcing plywood consumption at scale. This broad demand base translates into resilient plywood market outlook through the forecast horizon. By 2030, almost 60 percent of 8.3 billion people will live in cities, according to UN estimates. Almost 1400 of the world’s cities will have half a million or more inhabitants.

To get more information on this market, Request Sample

The United States has emerged as a major region in the plywood market owing to many factors. The residential construction sector accounts for approximately 87.9% of total plywood consumption in the US, supported by robust housing starts data from the US Census Bureau reporting over 1.4 million new housing units authorized in 2023. Federal programs including the Department of Energy’s Building Technologies Office continue to promote energy-efficient engineered wood applications, while US Forest Service initiatives in sustainable forestry and laminated veneer lumber adoption further support premium plywood demand.

Executive Summary

The global plywood market stood at USD 52.5 Billion in 2025, propelled by accelerating urbanization across emerging economies, robust residential and commercial construction activity, and sustained demand from the furniture and interior design industries worldwide. The market is projected to reach USD 77.6 Billion by 2034 at a CAGR of 4.31%. Asia Pacific commands a dominant 70.0% revenue share (2025), anchored by China's expansive construction and furniture manufacturing ecosystem, India's government-backed housing missions, and Vietnam's rapidly growing wood products export industry.

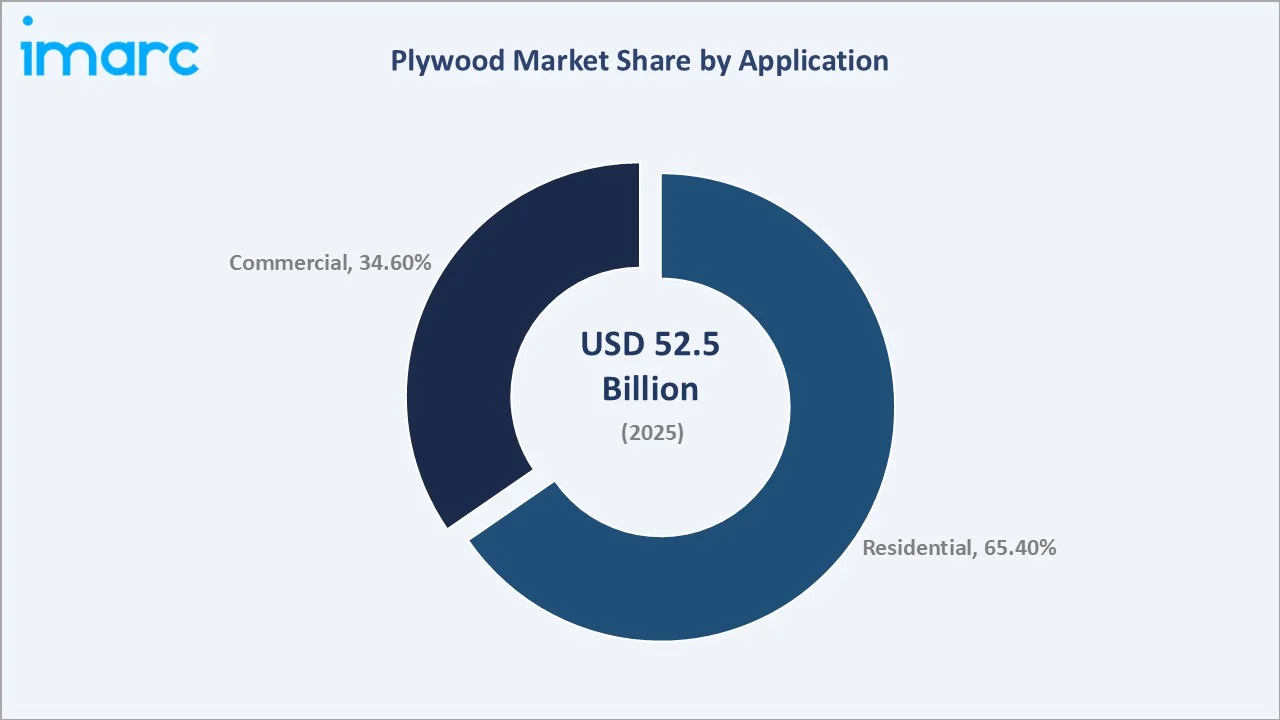

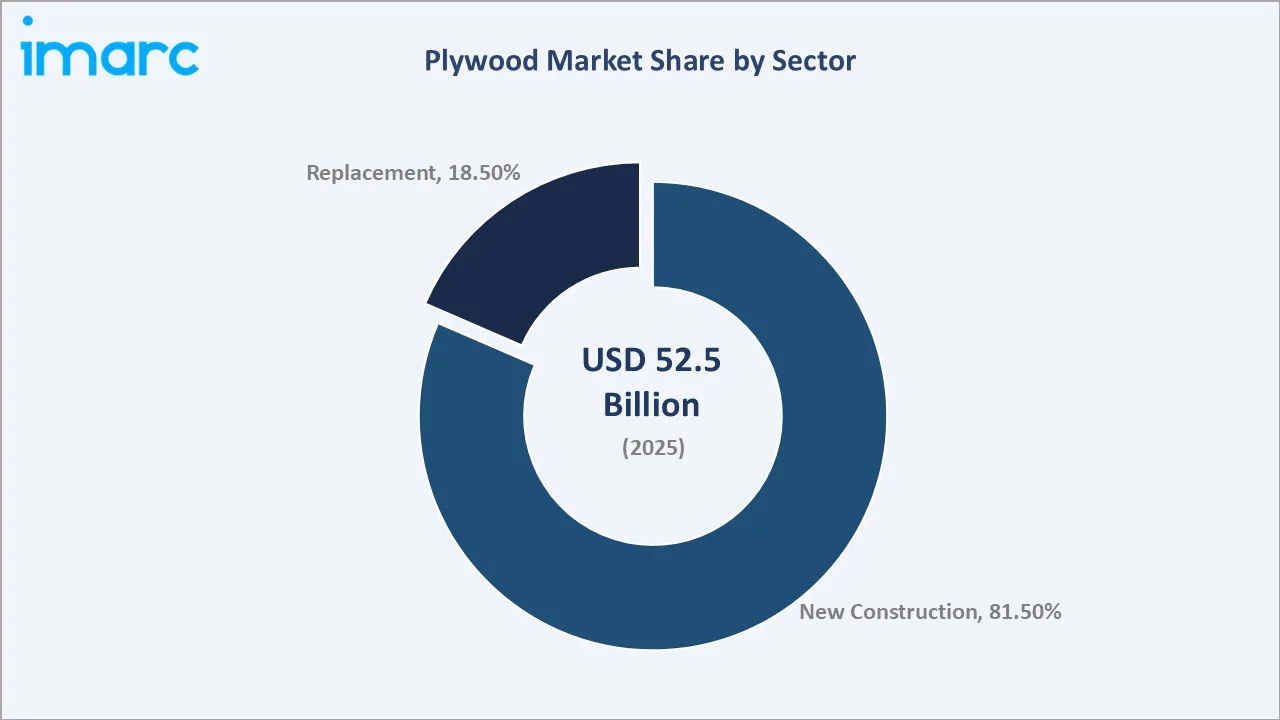

By sector, new construction leads at 81.5% (2025), driven by large-scale residential and infrastructure development across Asia, the Middle East, and Latin America. By application, residential dominates at 65.4% (2025), fueled by rising urbanization, affordable housing demand, and growing preference for plywood in flooring, wall sheathing, and roofing across developing economies.

North America (12.4%), Europe (9.8%), Latin America (4.5%), and the Middle East and Africa (3.3%) complete the regional landscape. Key growth trends include the rising adoption of sustainable and FSC-certified plywood aligned with green building standards, growing demand for fire-resistant and moisture-resistant engineered wood variants, and increasing penetration of plywood in prefabricated and modular construction.

Key Market Insights

|

Insight |

Data |

|

Largest Base Ingredient |

New Construction – 81.5% (2025) |

|

Largest Flavor Segment |

Residential – 65.4% (2025) |

|

Leading Region |

Asia Pacific – 70.0% (2025) |

|

Fastest Growing Region |

Middle East & Africa (~5.6% CAGR) |

|

Top Companies |

Weyerhaeuser, Georgia-Pacific, Greenply Industries, UPM, Boise Cascade, SVEZA |

|

Key Opportunity |

Sustainable & engineered plywood for green building certification — USD 10B+ addressable by 2034 |

Key Analytical Observations Supporting the Above Data:

- New construction's 81.5% share (2025) reflects plywood's indispensable role in structural sheathing, concrete formwork, roofing, and wall cladding across large-scale residential and infrastructure projects. Rapid urbanization in China, India, Indonesia, and Vietnam continues to generate unprecedented volume demand, with plywood favored for its structural integrity, cost-efficiency, and installation versatility.

- Residential application's 65.4% dominance (2025) is driven by surging affordable housing demand across developing economies, rising home renovation spending in mature markets, and the growing DIY culture. India's Smart Cities Mission and government-backed housing programs are generating sustained, high-volume plywood procurement across Tier-1 and Tier-2 urban centers.

- Asia Pacific's 70.0% share reflects the region's dual position as both the world's largest plywood producer and consumer. China's expansive real estate and furniture manufacturing base, India's infrastructure investment pipeline, and Vietnam and Indonesia's export-oriented wood processing industries collectively anchor this dominant regional market concentration through 2034.

Global Plywood Market Overview

Market Trends

To evaluate market opportunities, Request Sample

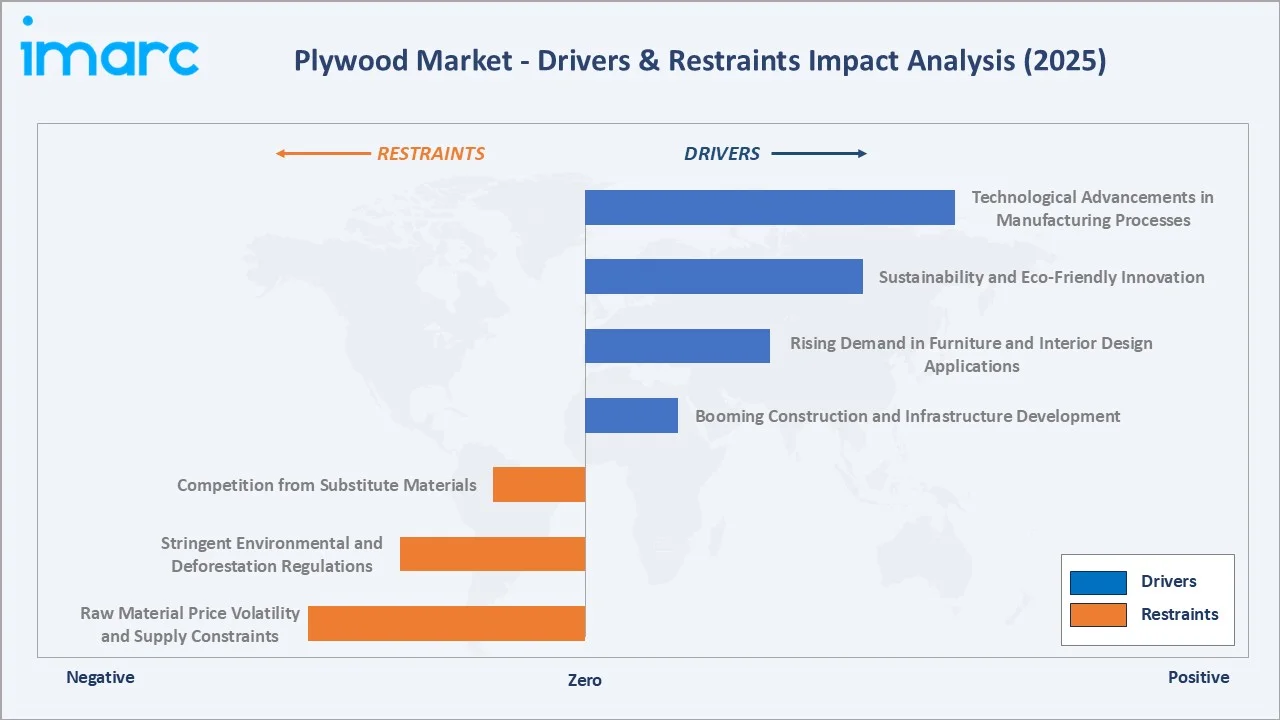

- Technological Advancements in Manufacturing Processes: Technological innovation is fundamentally reshaping plywood production efficiency and product quality across leading manufacturing economies. Modern plywood mills integrating automation, digital precision cutting, and real-time quality monitoring systems have demonstrated the ability to reduce variable production costs by approximately 14% while increasing output capacity by 13% to 28% without physical capacity expansion, representing a significant competitive advantage for technology-adopters. The integration of smart logistics and inventory management platforms further enables manufacturers to respond with greater agility to volatile demand signals.

- Sustainability and Eco-Friendly Innovation: Environmental sustainability has transitioned from a market preference to an industry imperative, reshaping procurement standards and product development priorities across global plywood markets. According to Trade Promotion Council of India (TPCI), the global furniture industry is expected to increase at a CAGR of 6% between 2021 and 2030, reaching US$ 872.5 billion by 2030, signaling robust structural demand for low-emission, certified plywood panels.

- Rising Demand in Furniture and Interior Design Applications: The global furniture manufacturing and interior design sector represents one of the most dynamic demand drivers for plywood, propelled by urbanization, rising disposable incomes, and evolving design preferences favoring modular, minimalist, and space-efficient living solutions. Plywood’s unique combination of workability, structural strength, smooth surface finishing compatibility, and aesthetic appeal makes it the preferred substrate for modern furniture cabinetry, bespoke wall paneling, and commercial interior fit outs. The total annual construction expenditure in the United States reached USD 2.2 Trillion in 2024, with significant volumes channeled into interior renovation and commercial fit-out projects that extensively specify plywood for partitions, ceilings, and furniture installations.

Market Restraints

- Raw Material Price Volatility and Supply Constraints: Plywood production depends heavily on timber logs and petrochemical-based adhesives like formaldehyde resins. Prices of these inputs are highly volatile due to weather conditions, logging restrictions, and crude oil fluctuations. According to the Trade and Export Promotion Centre 2026 report, Nepal exported plywood worth Rs 2.69 billion in the review period, compared to Rs 5 billion in the same period of the previous fiscal year. The move was also aimed at preventing Chinese products from entering the Indian market through neighbouring countries. This instability directly impacts production costs and profit margins.

- Stringent Environmental and Deforestation Regulations: Governments worldwide are tightening rules on deforestation, carbon emissions, and sustainable sourcing of wood. Compliance with certifications like FSC and PEFC increases operational costs and complexity, especially for small manufacturers. Increasing environmental scrutiny is slowing down raw material availability and limiting expansion, particularly in export-driven markets like Europe and North America.

- Competition from Substitute Materials (MDF, OSB, Particleboard): The plywood market faces intense competition from engineered wood products such as MDF and OSB, which are often cheaper and offer uniform quality. These substitutes are gaining popularity in furniture and construction due to ease of machining and lower cost. This shift is gradually reducing plywood’s share in price-sensitive segments and increasing market fragmentation.

Market Opportunities

- Booming Construction and Infrastructure Development: Rapid urbanization and population growth are driving strong demand for residential and commercial construction globally. Plywood is widely used in flooring, roofing, wall sheathing, and structural applications. By 2040, the world is projected to invest $106 trillion in infrastructure projects across all sectors. Asia is expected to account for two-thirds of total investment, or roughly $70 trillion.

- Growth of Furniture and Interior Design Industry: Rising disposable incomes and changing lifestyles are increasing demand for modular furniture, home décor, and interior applications. Plywood is preferred for its durability, strength, and flexibility in design. The global furniture market expansion is directly boosting plywood consumption, especially in premium and customized interior segments.

- Rising Demand for Sustainable and Value-Added Products: There is a growing shift toward eco-friendly plywood with low formaldehyde emissions and certified sustainable sourcing. Manufacturers are innovating with fire-resistant, waterproof, and marine-grade plywood to cater to specialized applications. This trend is creating premium product segments and export opportunities, particularly in environmentally regulated markets like the EU and US.

Market Challenges

- Raw Material Availability and Price Volatility: The plywood industry is highly dependent on timber and petrochemical-based adhesives, making it vulnerable to fluctuations in raw material supply and pricing. Factors such as deforestation regulations, logging restrictions, and volatility in resin costs linked to crude oil prices create supply uncertainty and margin pressure for manufacturers operating across global markets.

- Quality Standardization vs. Regional Variability: While plywood is widely used across construction and furniture applications, maintaining consistent product quality across different regions remains a challenge. Variations in raw material quality, manufacturing processes, and lack of standardized grading systems in emerging markets lead to inconsistent product performance, impacting brand reliability and export competitiveness.

- Environmental Regulations and Compliance Costs: Increasing global focus on sustainability and deforestation control is leading to stricter regulations on wood sourcing, emissions, and chemical usage. Compliance with certifications such as FSC and low-formaldehyde emission standards requires significant investment in sustainable sourcing and production technologies, raising operational costs and creating barriers for smaller manufacturers.

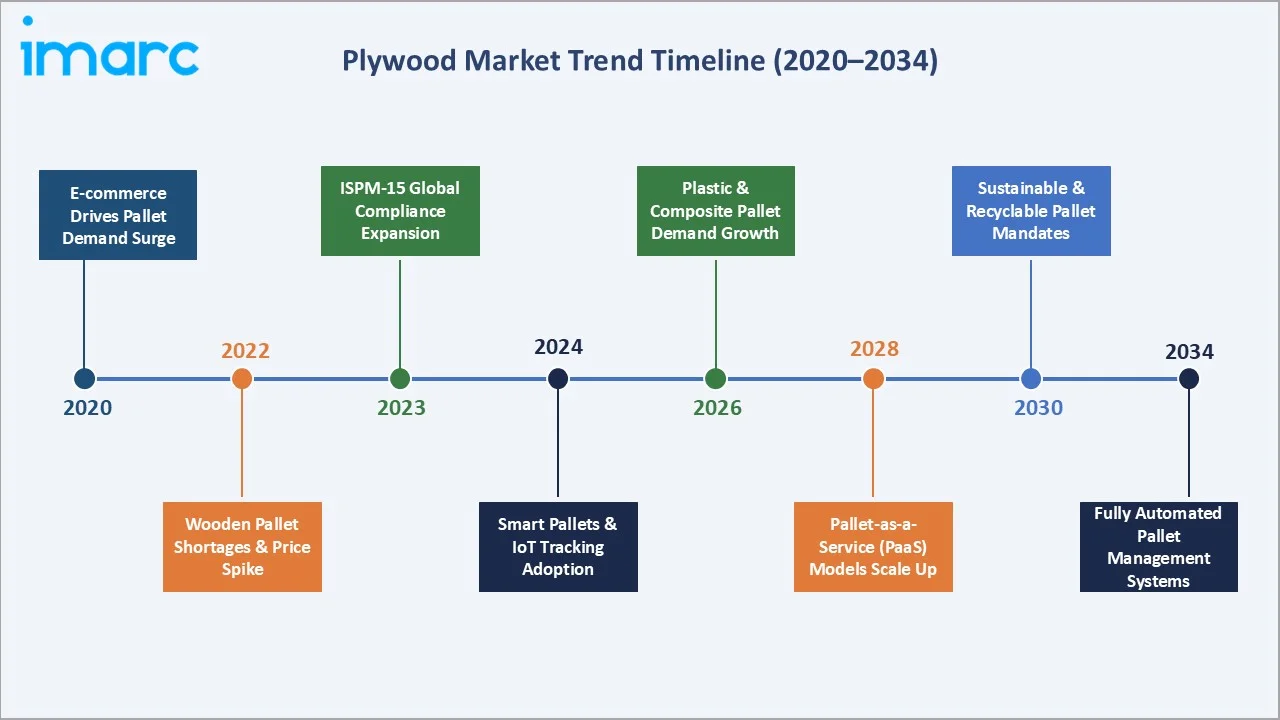

Emerging Market Trends

The global plywood market is being reshaped by five converging trends redefining product innovation, sustainability standards, and competitive dynamics across all geographies through 2034.

1. Sustainability, Green Certification, and Deforestation Regulation Compliance

Rising green building mandates and tightening environmental regulations are fundamentally reshaping plywood procurement globally. The EU Deforestation Regulation and FSC certification requirements are compelling manufacturers to adopt responsibly sourced timber and low-emission adhesives, directly influencing supplier selection across North America, Europe, and export-oriented Asian manufacturing hubs.

2. Engineered and Performance-Grade Plywood Innovation

Demand for fire-resistant, moisture-resistant, and formaldehyde-free plywood variants is reshaping product development priorities. Builders and specifiers increasingly require performance-grade engineered wood meeting stringent building codes for high-rise, commercial, and infrastructure projects, moving procurement decisively beyond commodity-grade panels toward technically differentiated, application-specific engineered wood products.

In June 2023, Duroply launched Techply — India's first ready-to-use customizable plywood with a veneer-like finish — exemplifying the market's accelerating shift toward premium, application-specific engineered plywood formulations.

3. Modular Construction and Prefabricated Housing Expansion

The global rise of prefabricated and modular construction is generating sustained high-volume plywood demand. Plywood's structural integrity, dimensional consistency, and fabrication ease make it the preferred panel material for factory-built modular units — particularly across Southeast Asia, Australia, and North America where rising construction labor costs favor off-site manufacturing.

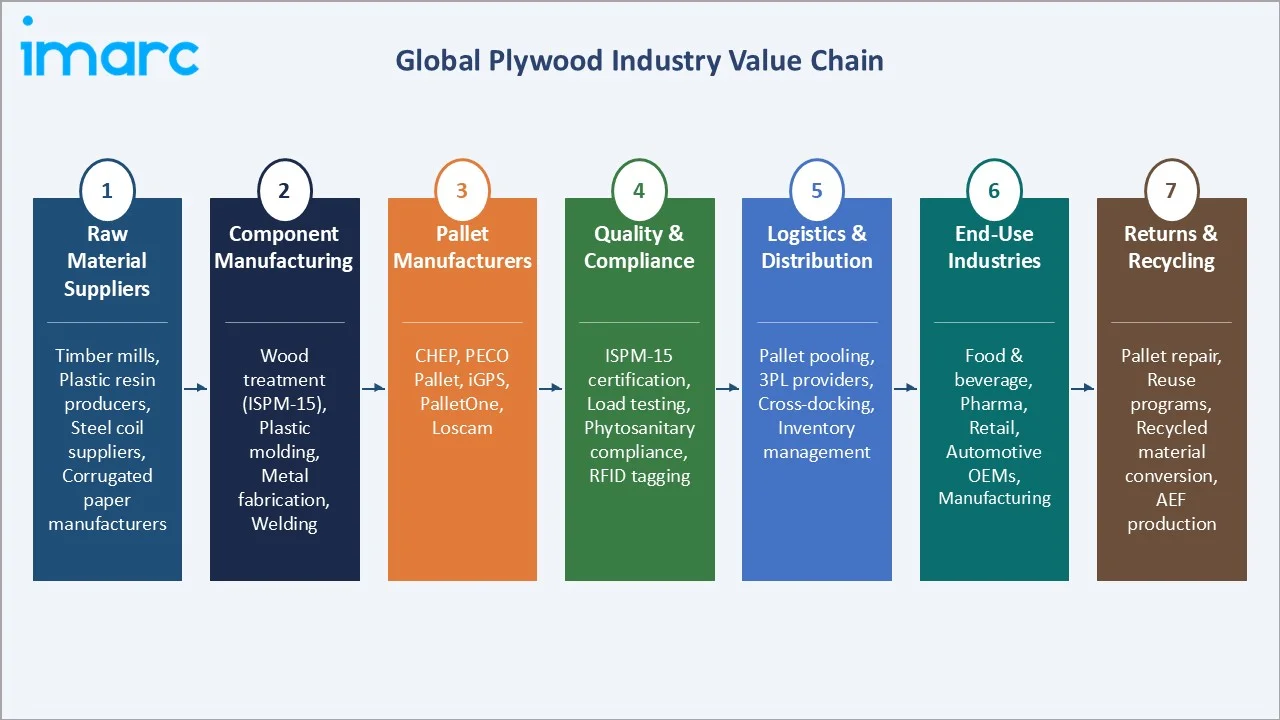

Industry Value Chain Analysis

The plywood industry value chain encompasses seven interconnected stages from raw timber sourcing through to end-application installation. Each stage requires specialized forestry management, precision manufacturing, and rigorous quality certification to meet the structural, aesthetic, and environmental performance standards demanded by construction, furniture, and interior design end-users globally.

|

Stage |

Key Activities |

Representative Players |

|

Timber Sourcing & Forestry |

Sustainable timber harvesting, FSC/PEFC certification, log procurement, veneer peeling |

Weyerhaeuser, Jaya Tiasa Holdings, Indonesian and Malaysian forestry operators |

|

Veneer Processing & Manufacturing |

Log peeling, veneer drying, adhesive application, hot-press lamination, panel fabrication |

Greenply Industries, SVEZA, Boise Cascade, Georgia-Pacific, Koskisen |

|

Performance Treatment & Finishing |

Fire-resistant treatment, moisture-resistant coating, formaldehyde-free adhesive application, sanding |

Duroply, Century Plyboards, specialist treatment facilities |

|

Quality Testing & Certification |

Grade classification (MR/BWR/BWP), structural load testing, emission compliance, export certification |

Bureau Veritas, SGS, national standards bodies (BIS, EN, CARB) |

|

Distribution & Wholesale |

Bulk logistics, port handling, bonded warehousing, regional wholesale distribution |

Regional timber merchants, B2B wholesale distributors across Asia, Europe, and the Americas |

|

Retail & Project Supply |

Builder's merchants, DIY retail chains, e-commerce platforms, project-specific direct supply |

Home Depot, Lowe's, Bunnings, Amazon, regional builder's merchants globally |

|

End-Application Installation |

Residential construction, commercial fit-out, furniture manufacturing, industrial formwork |

Construction contractors, furniture OEMs, interior fit-out specialists, industrial packaging operators |

The veneer processing and manufacturing stage is the primary value creation point — where proprietary adhesive formulations, press technology, and panel engineering determine structural performance and certification eligibility. Leading manufacturers including Greenply, SVEZA, and Georgia-Pacific invest heavily in precision hot-press systems and low-emission adhesive technology to command premium pricing over commodity producers.

Technology Landscape in the Plywood Industry

Automated Manufacturing and Precision Processing Technology

Computer-controlled hot-press systems, automated veneer grading lines, and CNC panel-cutting machines are standardizing plywood quality across large-scale facilities. Automated machine vision defect detection reduces waste and improves grading accuracy, enabling consistent panel dimensions and superior surface quality that support premium market positioning across construction and furniture end-user segments.

Sustainable Adhesive and Emission-Reduction Technology

Formaldehyde-free and low-emission adhesive technologies are becoming critical product differentiators as regulatory frameworks tighten globally. Soy-based, bio-resin, and MDI adhesive systems are replacing conventional urea-formaldehyde binders in premium-grade production, directly addressing CARB Phase 2, EU REACH, and LEED material health compliance requirements across key export markets.

Digital Supply Chain and E-Commerce Distribution Technology

Digital procurement platforms, real-time inventory management systems, and B2B e-commerce portals are transforming plywood distribution efficiency. Large contractors and furniture manufacturers are sourcing directly through digital platforms, compressing traditional wholesale margins. Blockchain-based timber traceability systems are emerging tools for verifying FSC certification compliance across complex multi-country supply chains.

Global Plywood Industry Segmentation

IMARC Group provides an analysis of the key trends in each segment of the global plywood market, along with forecast at the global, regional, and country levels from 2026–2034. The market has been categorized based on residential and commercial application and new construction and replacement sector.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Residential and Commercial Application |

Residential |

65.4% |

2025 |

|

New Construction and Replacement Sector |

New Construction |

81.5% |

2025 |

|

Region |

Asia Pacific |

70.0% |

2025 |

Analysis by Application:

The residential segment dominates the global plywood market with a 65.4% share in 2025, propelled by accelerating urbanization, population growth, and rising disposable incomes that are collectively generating unprecedented demand for new housing, particularly across Asia Pacific and Latin America. Plywood’s unique combination of cost-effectiveness, dimensional stability, load-bearing performance, and versatility for flooring, roofing, and wall sheathing applications makes it the structural material of choice for residential construction across all income segments.

To access detailed market analysis, Request Sample

Analysis by New Construction and Replacement Sector:

The new construction sector commands an 81.5% share of the global plywood market in 2025, reflecting the decisive role of large-scale building activity in driving structural plywood demand globally. As governments across emerging economies accelerate infrastructure investment programs, the demand for plywood in concrete formwork, structural sheathing, floor underlayment, and temporary site structures is growing commensurately. Construction spending during December 2024 was estimated at a seasonally adjusted annual rate of $2,192.2 billion, 0.5 percent above the revised November estimate of $2,180.3 billion, representing a significant base of new construction activity that extensively specifies plywood for both structural and interior applications.

Key Regional Takeaways

Asia Pacific commands 70.0% of the global plywood market in 2025, reflecting the region’s unrivaled combination of manufacturing scale, raw material availability, vast domestic construction markets, and rapidly growing middle-class consumption of furniture and interior products. China remains the world’s largest plywood producer and consumer, supported by ongoing urban housing development programs and enormous export volumes to global markets. According to China's 2020 statistical yearbook, the average floor area per person reached 41.76 square meters, which is not small but is still an issue.

North America accounts for 12.4% of the global plywood market in 2025, anchored primarily by the United States which represents the world’s largest single-country demand market for construction-grade plywood. US imports of hardwood plywood increased by 19% in 2025, reaching more than 3.28 million cubic metres, according to data from the US Department, reflecting robust underlying construction demand even amid elevated mortgage rates.

Competitive Landscape

The global plywood market is moderately consolidated, with leading international manufacturers competing alongside a large base of regional and local producers, particularly across Asia. The top global manufacturers collectively represent approximately 30–40% of organized sector revenues, while the remainder is distributed among regional players and unorganized mills primarily operating in high-growth Asian markets. Major established players have pursued strategies including capacity modernization investments, sustainability certifications, strategic acquisitions, and geographic diversification to strengthen competitive positioning.

|

Company |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Georgia-Pacific LLC |

DryPly, Plytanium, Sturd-I-Floor |

Leader – North America |

Strong distribution network, construction-grade plywood focus, vertical integration in timber sourcing |

|

PotlatchDeltic Corporation |

PotlatchDeltic Wood Products |

Domestic Leader- USA |

Timberland ownership advantage, cost-efficient production, focus on structural panels |

|

Weyerhaeuser Company |

Weyerhaeuser Plywood |

Global Leader – Timber & Wood |

Vertical integration (forest → product), sustainable forestry, large-scale production efficiency |

|

Boise Cascade Company |

Boise Cascade |

Leader – North America |

Strong dealer network, focus on engineered wood + plywood mix, construction sector dominance |

|

UPM-Kymmene Oyj |

WISA |

Leader – Europe |

Sustainability leadership, high-performance birch plywood, innovation in bio-based materials |

|

Sveza Group |

SVEZA |

Leader – Birch Plywood (Global) |

Premium Russian birch plywood, export-oriented strategy, specialty industrial applications |

|

Metsä Wood (Metsäliitto Cooperative) |

Metsä Wood |

Leader – Europe Premium |

Kerto LVL + plywood synergy, sustainability focus, industrial construction solutions |

|

Latvijas Finieris AS |

Riga Wood |

Leader – Global Birch Plywood |

Birch plywood specialization, niche industrial segments, strong EU presence |

|

Austral Plywoods Pty Ltd. |

Austral Plywoods |

Established – Australia |

Hoop Pine plywood specialist — appearance, marine, structural, and architectural grades; 100% Australian plantation-grown timber |

The companies covered in the report includes Georgia-Pacific LLC, PotlatchDeltic Corporation, Weyerhaeuser Company, Boise Cascade Company, UPM-Kymmene Oyj, SVEZA Group, Metsä Wood (Metsäliitto Cooperative), Latvijas Finieris AS, Austral Plywoods Pty Ltd., and others.

Key Company Profiles

Georgia-Pacific LLC

Georgia-Pacific LLC is one of the world's largest manufacturers and distributors of plywood and engineered wood products, operating as a wholly owned subsidiary of Koch Industries. With manufacturing facilities across the United States and a distribution network spanning North America and international markets, the company holds a dominant position in the structural and industrial plywood segments.

- Product Portfolio: Primary plywood brand Plytanium, the most commercially recognized plywood brand.

- Recent Developments: Expanded investment in its Southern U.S. manufacturing network through capacity upgrades at key mills; advanced its building products digital commerce platform to streamline contractor and distributor procurement in 2024.

- Strategic Focus: North American market leadership, manufacturing operational efficiency, sustainable forestry sourcing, digital distribution channel development, and construction-sector demand capture.

Weyerhaeuser Company

Weyerhaeuser Company is one of the largest private owners of timberlands in the United States, managing approximately 10.5 million acres of productive forestland. Operating as a Real Estate Investment Trust (REIT), the company integrates timberland ownership with wood products manufacturing, giving it a structurally differentiated competitive position in the global plywood market.

- Product Portfolio: Structural plywood panels, OSB, engineered lumber, I-joists, laminated veneer lumber (LVL), and framing lumber for residential and commercial construction markets.

- Recent Developments: Announced strategic capital investment in its Wood Products segment to modernise manufacturing facilities; continued expansion of its distribution partnership network across U.S. homebuilder channels amid housing market recovery signals.

- Strategic Focus: Timberland asset optimisation, housing construction demand alignment, manufacturing cost efficiency, ESG-led sustainable forestry certification, and long-term REIT shareholder value generation.

UPM-Kymmene Oyj

UPM-Kymmene Oyj, operating through its UPM Plywood business unit, is Europe's leading plywood manufacturer and a significant global player. Headquartered in Helsinki, Finland, UPM brings a strong emphasis on product innovation, sustainability credentials, and high-value specialty plywood solutions that command premium pricing in international markets.

- Product Portfolio: WISA® spruce and birch plywood, WISA-Form concrete shuttering panels, WISA-Trans and WISA-Floor vehicle flooring solutions, moisture-resistant plywood, and specialty coated panels for construction, transportation, and industrial end-uses.

- Strategic Focus: Premium specialty plywood segment leadership, decarbonisation of manufacturing operations, transportation and construction sector diversification, and circular bioeconomy value chain development.

SVEZA Group

SVEZA group is Russia's largest birch plywood producer and one of the top birch plywood manufacturers globally, with an annual production capacity exceeding 1.4 million cubic metres across seven integrated manufacturing facilities. The company has historically served European, Asian, and North American export markets, leveraging abundant Russian birch timber resources to compete on quality and scale.

- Product Portfolio: Birch plywood, laminated plywood, moisture-resistant (WBP) plywood, formaldehyde-free panels, concrete shuttering plywood, and custom-dimension specialty panels for construction, furniture, and industrial sectors.

- Strategic Focus: Asian export market development, value-added laminated product portfolio expansion, sustainable birch sourcing certification, operational resilience under evolving trade conditions, and domestic Russian construction demand capture.

Market Concentration Analysis

The global plywood market is moderately fragmented at the manufacturing level, with a large number of regional and local producers operating alongside a limited set of large integrated forestry and wood product companies. A significant portion of plywood production is controlled by small and mid-sized mills, particularly in Asia-Pacific and Latin America, where unorganized and semi-organized players contribute substantially to total output.

In mature markets including North America and Europe, market concentration is higher, with vertically integrated companies such as Weyerhaeuser, Georgia-Pacific, and UPM controlling a significant share of industrial-grade and structural plywood demand. These players benefit from timberland ownership, advanced processing capabilities, and established distribution networks. In contrast, emerging markets such as India, Southeast Asia, and Africa remain highly fragmented, with independent manufacturers dominating price-sensitive segments and limited brand differentiation.

Consolidation at the industry level is expected to accelerate through 2034, driven by increasing environmental regulations, certification requirements (FSC/PEFC), and the need for scale efficiencies. Larger players are expected to pursue acquisitions of regional mills and enter into strategic partnerships to secure raw material supply and expand geographic reach. The market is likely to witness steady merger and acquisition activity, particularly in export-oriented and high-value plywood segments.

Investment & Growth Opportunities

Fastest Growing Segments

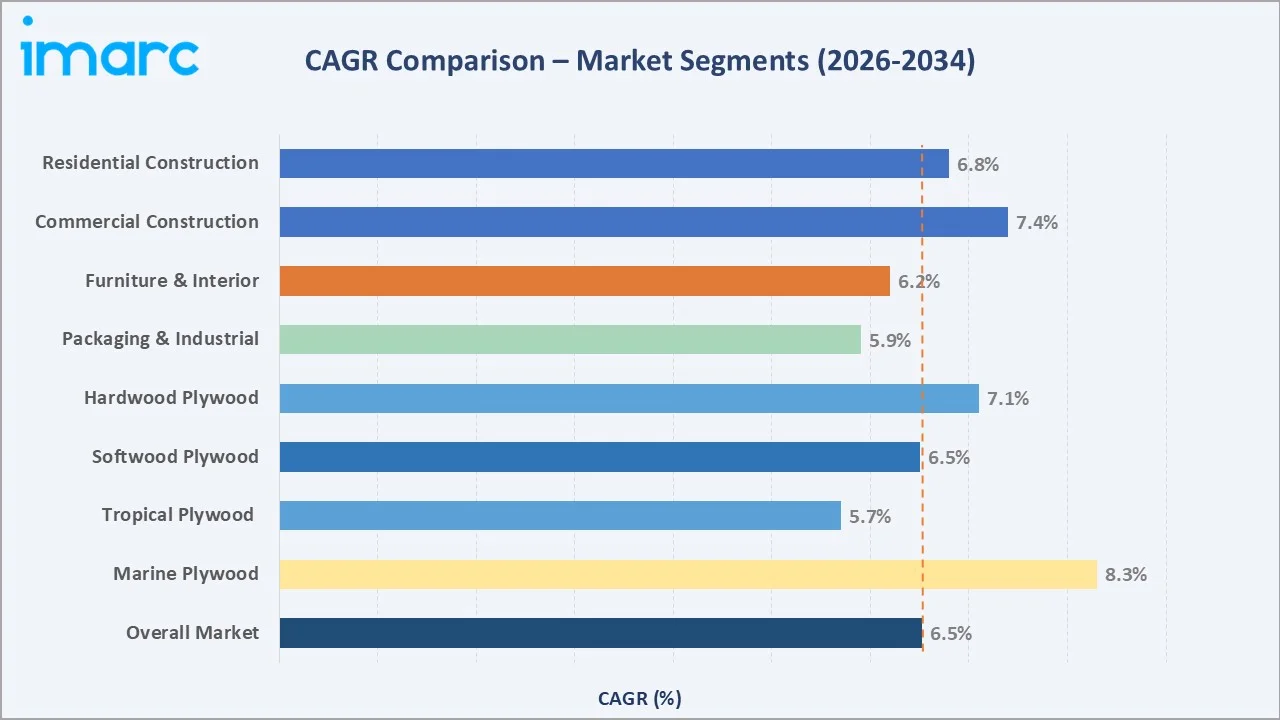

Engineered plywood, marine-grade plywood, fire-resistant plywood, and eco-certified (low-formaldehyde) plywood represent the fastest-growing segments through 2034. These segments cater to premium applications in construction, infrastructure, and interiors, addressing a growing demand for durability, safety, and sustainability. Collectively, these value-added categories are expected to account for a significant share of incremental market growth, supported by stricter building codes and rising consumer awareness.

Emerging Market Expansion

Asia-Pacific, the Middle East, and Africa represent the highest growth regions for plywood demand. Rapid urbanization, infrastructure development, and housing demand are driving strong consumption in countries such as India, Vietnam, Indonesia, Saudi Arabia, and the UAE. India, in particular, is witnessing consistent growth driven by real estate expansion and increasing adoption of branded plywood in Tier-1 and Tier-2 cities. The Middle East is benefiting from large-scale construction and commercial projects, creating strong import demand for high-quality plywood.

Technology and Innovation Investment Trends

- Manufacturers are investing in advanced veneer processing, automated pressing systems, and digital quality control technologies to improve efficiency, reduce waste, and enhance product consistency.

- Development of low-emission adhesives and bio-based resins is gaining traction, driven by environmental regulations and demand for green building materials.

- Supply chain digitization and traceability solutions are becoming critical, enabling companies to ensure sustainable sourcing and comply with international certification standards.

Future Market Outlook (2026-2034)

The global plywood market is expected to witness steady, infrastructure-driven growth through 2034, supported by rising construction activity, urbanization, and increasing demand for engineered wood products. Growth will be particularly strong in emerging economies, where housing demand and industrial development continue to expand.

Product innovation and sustainability will define the competitive landscape. Companies that successfully integrate eco-friendly materials, low-emission technologies, and high-performance product features will gain a competitive advantage in both domestic and export markets. The shift toward certified sustainable plywood and value-added variants will drive margin expansion across the industry.

By 2034, the plywood market is expected to become more consolidated, with large integrated players increasing their market share through acquisitions, capacity expansions, and global distribution strategies. Premium and engineered plywood segments will account for a larger proportion of total demand, positioning the industry for long-term, stable growth.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 150 industry participants in 2024–2025, comprising bubble tea franchise operators, ingredient and equipment suppliers, retail buyers, food service distributors, and end consumers across Asia Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company press releases, franchise disclosure documents, trade publications (QSR Magazine, Food Business News, Nation's Restaurant News), industry databases (Euromonitor, Mintel), and publicly available market data including government trade statistics and tea industry association reports. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up outlet count and average revenue per outlet modeling, combined with top-down consumer expenditure analysis incorporating tea consumption data, café culture penetration rates, and social media trend analytics.

Plywood Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Cubic Metres, Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Residential and Commercial Applications Covered | Residential, Commercial |

| New Construction and Replacement Sectors Covered | New Construction, Replacement |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Georgia-Pacific LLC, PotlatchDeltic Corporation, Weyerhaeuser Company, Boise Cascade Company, UPM-Kymmene Oyj, SVEZA Group, Metsä Wood (Metsäliitto Cooperative), Latvijas Finieris AS, Austral Plywoods Pty Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the plywood market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global plywood market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the plywood industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Plywood Market Report

The plywood market was valued at USD 52.5 Billion in 2025.

The plywood market is projected to exhibit a CAGR of 4.31% during 2026-2034, reaching a value of USD 77.6 Billion by 2034.

Key growth drivers include rapid urbanization and residential construction activity in emerging economies, rising government expenditure on affordable housing and infrastructure, growing demand in the furniture and interior design sectors, and increasing adoption of eco-certified and technologically advanced plywood products aligned with green building standards globally.

Asia Pacific currently dominates the plywood market, accounting for a share of 70.0% in 2025, underpinned by China’s massive production base, India’s accelerating construction sector, and strong domestic demand across Southeast Asian economies.

Some of the major players in the plywood market include Georgia-Pacific LLC, PotlatchDeltic Corporation, Weyerhaeuser Company, Boise Cascade Company, UPM-Kymmene Oyj, SVEZA Group, Metsä Wood (Metsäliitto Cooperative), Latvijas Finieris AS, Austral Plywoods Pty Ltd., and others.

The plywood market faces challenges such as fluctuating raw material prices, stringent environmental regulations related to deforestation and emissions, and increasing competition from alternative engineered wood products like MDF and particleboard, which can limit market share in cost-sensitive applications.

Emerging opportunities include growing demand for eco-certified and sustainable plywood, rising adoption of value-added products such as fire-resistant and marine-grade plywood, and increasing use in modular furniture and prefabricated construction, particularly in rapidly urbanizing regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)