Pneumococcal Vaccine Market Size, Share, Trends and Forecast by Vaccine Type, Product Type, Distribution Channel, End User, and Region, 2026-2034

Global Pneumococcal Vaccine Market Size, Share, Trends & Forecast (2026-2034)

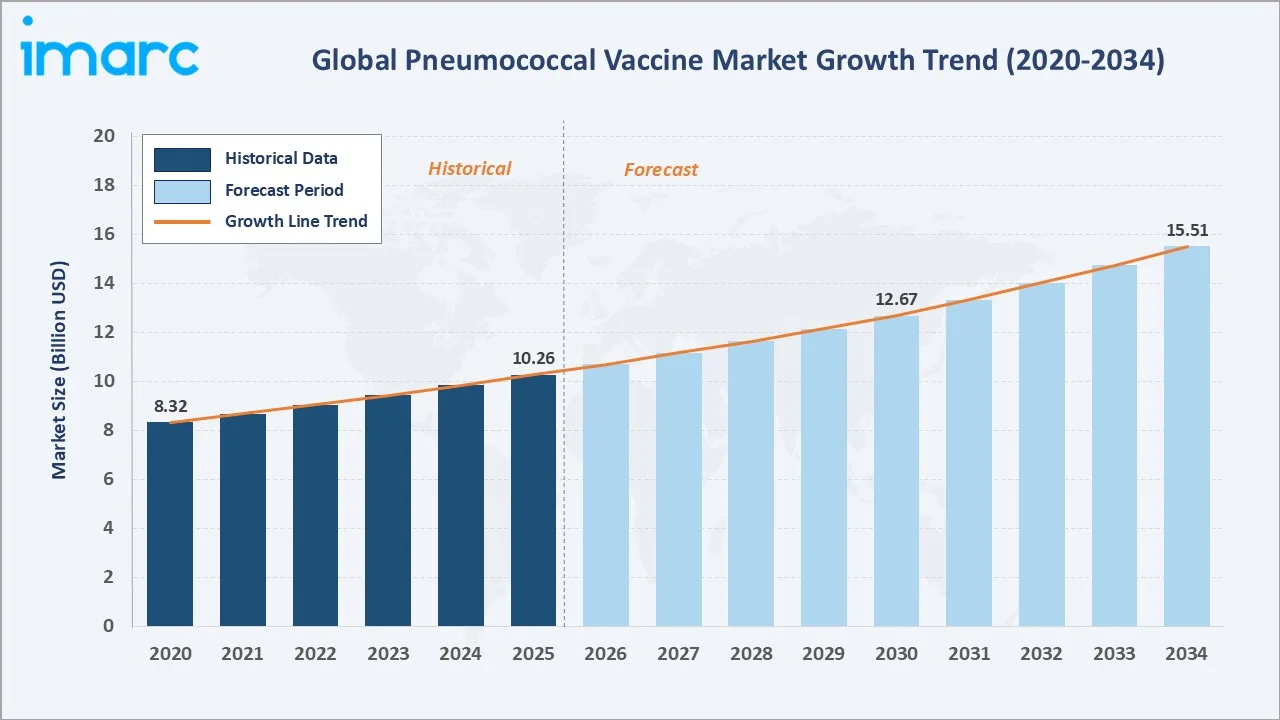

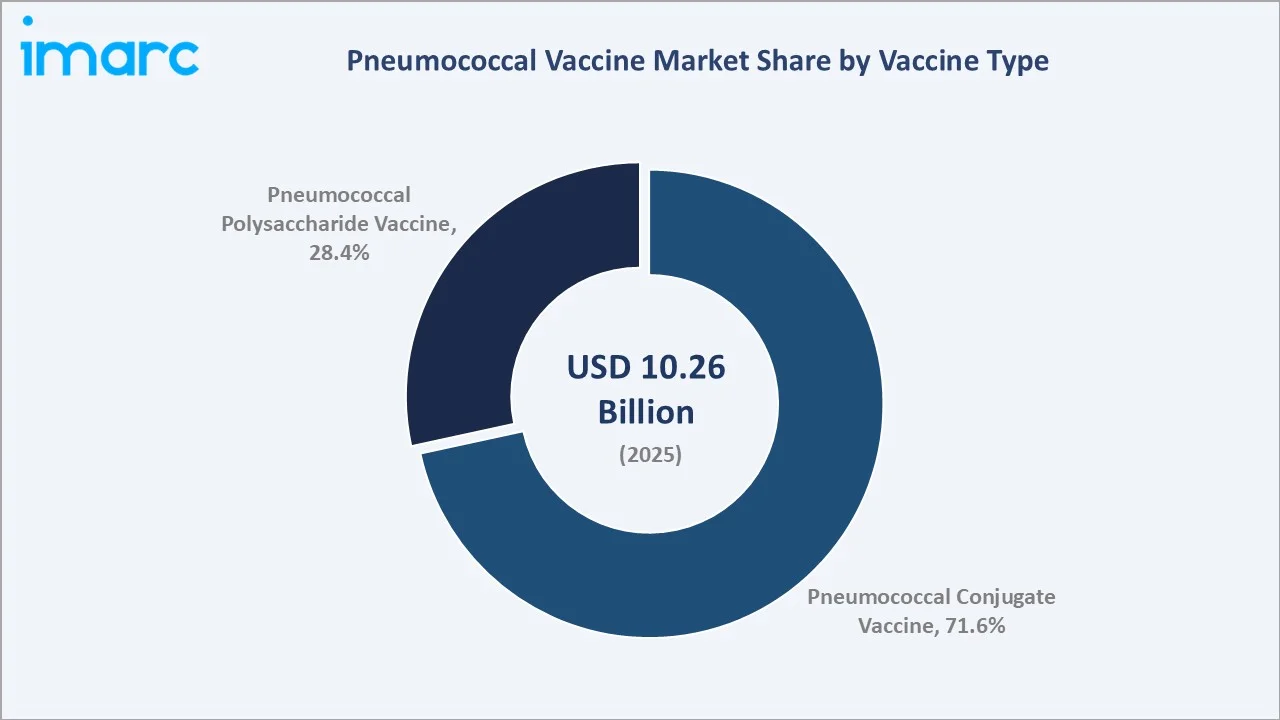

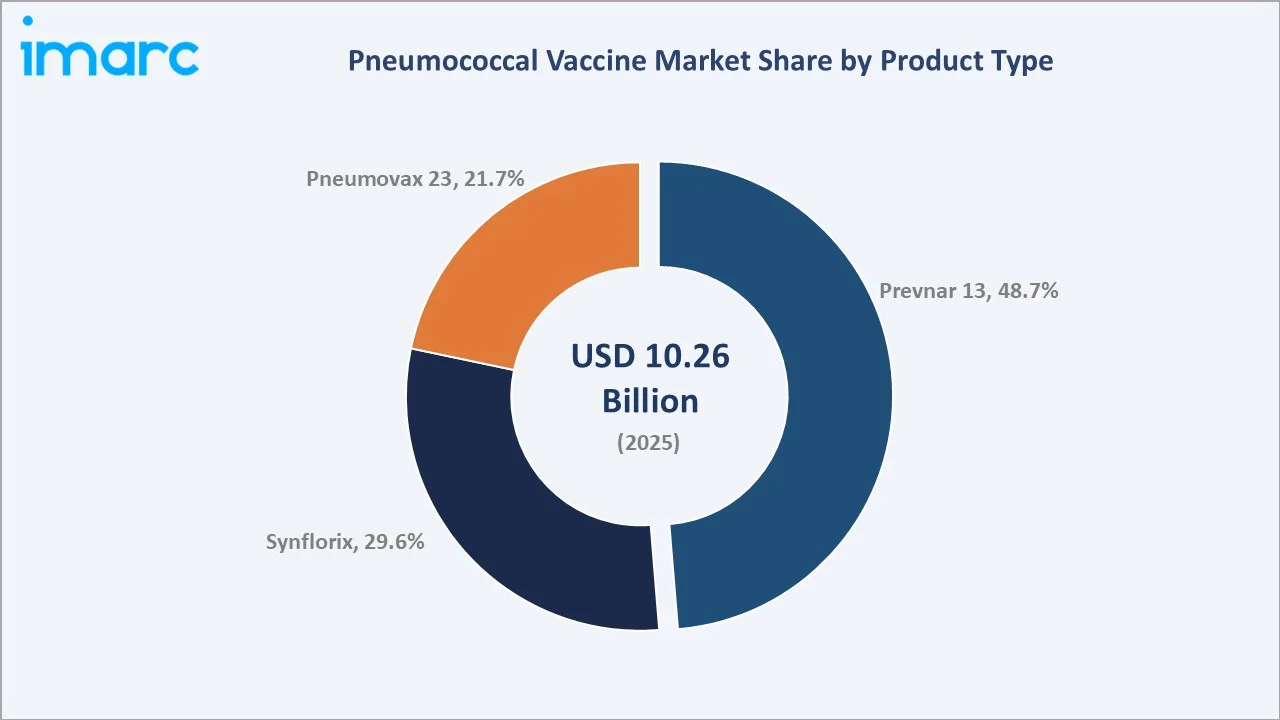

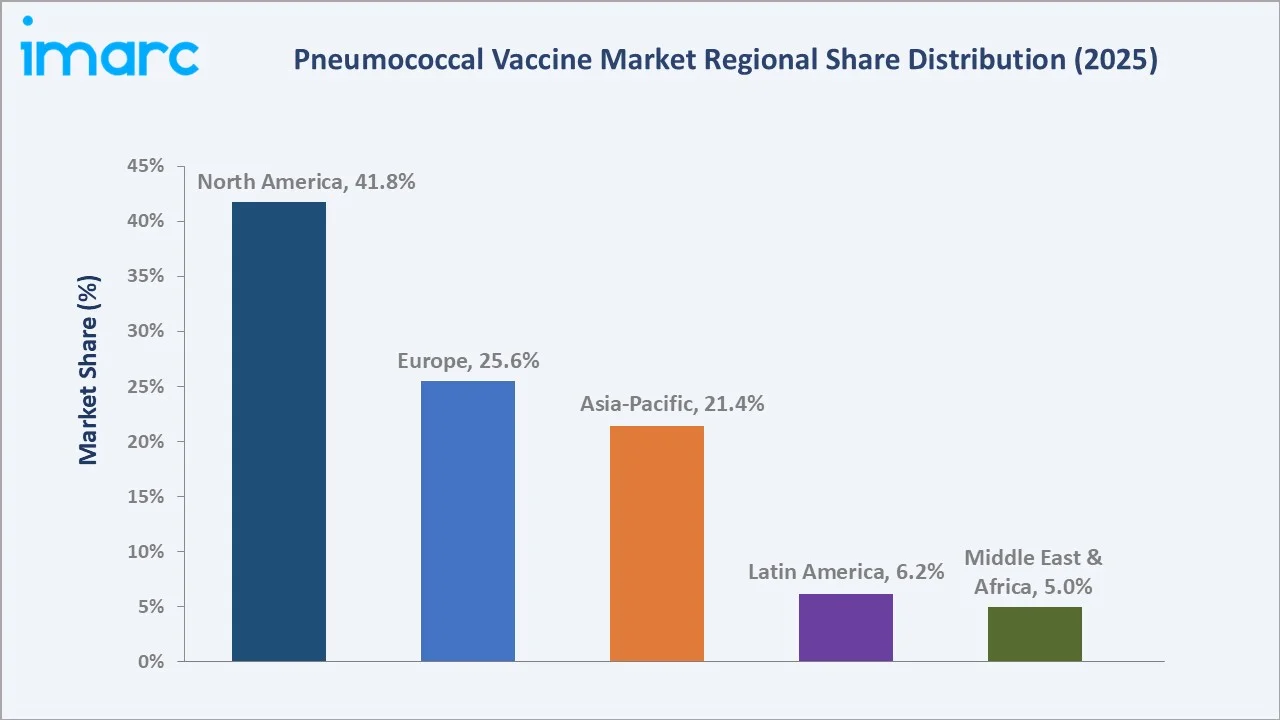

The global pneumococcal vaccine market size was valued at USD 10.26 Billion in 2025 and is projected to reach USD 15.51 Billion by 2034, exhibiting a CAGR of 4.30% during the forecast period 2026-2034. Rising geriatric populations, expanding government immunization programs, growing burden of pneumococcal disease, and steady progress in next-generation conjugate vaccine platforms are driving the pneumococcal vaccine market growth. Pneumococcal conjugate vaccines lead at 71.6% share in 2025, while Prevnar 13 alone accounts for 48.7% of global product demand. North America dominates with 41.8% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.26 Billion |

|

Forecast Market Size (2034) |

USD 15.51 Billion |

|

CAGR (2026-2034) |

4.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (41.8% share, 2025) |

|

Fastest Growing Region |

Middle East & Africa (~5.8% CAGR) |

|

Leading Vaccine Type |

Pneumococcal Conjugate Vaccine (71.6%, 2025) |

|

Leading Product Type |

Prevnar 13 (48.7%, 2025) |

The global pneumococcal vaccine market growth trajectory from 2020 through 2034 reflects sustained demand anchored by paediatric immunization uptake, adult catch-up programs, and rising adoption of higher-valency conjugate platforms across developed and emerging economies.

To get more information on this market, Request Sample

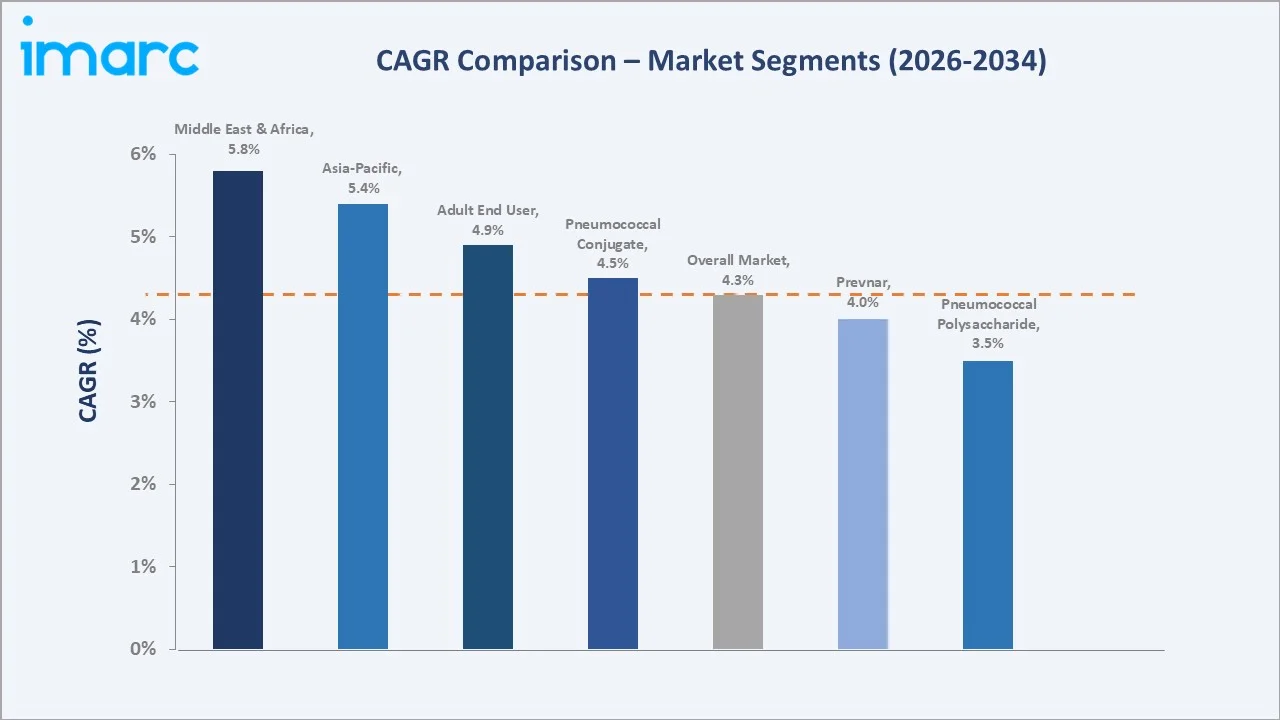

Segment-level CAGR comparisons highlight adult end users and emerging regions such as Middle East & Africa and Asia-Pacific as the fastest-accelerating sub-categories within the global pneumococcal vaccine market forecast through 2034.

Executive Summary

The global pneumococcal vaccine market is undergoing steady expansion. It is supported by rising disease awareness, aging populations, and sustained government-led immunization initiatives. Valued at USD 10.26 Billion in 2025, the market is forecast to reach USD 15.51 Billion by 2034 at a CAGR of 4.30%.

Pneumococcal conjugate vaccines command 71.6% share in 2025, anchored by broad paediatric adoption and expansion into higher-valency 15- and 20-serotype formulations. Prevnar 13 leads the product category with 48.7% of global demand, while Synflorix holds 29.6% and Pneumovax 23 accounts for 21.7%. Adult immunization is the fastest-growing end-user segment, advancing at an estimated CAGR of 4.9% through 2030.

North America leads with a 41.8% global revenue share in 2025, supported by CDC-backed immunization schedules and private payer coverage. Europe holds 25.6% and Asia-Pacific 21.4%. The pneumococcal vaccine market outlook remains constructive as serotype coverage widens, adult indications expand, and emerging economies scale up domestic manufacturing.

Key Market Insights

|

Insight |

Data |

|

Largest Vaccine Type |

Pneumococcal Conjugate - 71.6% share (2025) |

|

Leading Product |

Prevnar 13 - 48.7% share (2025) |

|

Second Product |

Synflorix - 29.6% share (2025) |

|

Leading Region |

North America - 41.8% revenue share (2025) |

|

Fastest Growing Region |

Middle East & Africa (~5.8% CAGR) |

|

Top Companies |

Pfizer Inc., Merck & Co. Inc., GSK Plc., Sanofi, Cyrus Poonawalla Group |

|

Global Doses (2025) |

180 million doses (conjugate + polysaccharide) |

Key Analytical Observations Supporting the Above Data:

- Pneumococcal conjugate vaccines' 71.6% dominance in 2025 reflects their superior immunogenicity in infants and the continued rollout of PCV13, PCV15, and PCV20 in routine childhood schedules across more than 150 countries.

- Prevnar 13's 48.7% product leadership is sustained by Pfizer's broad paediatric and adult indications, with Prevnar 20 progressively capturing adult volume in the U.S. and Europe following 2023-2024 expanded approvals.

- Synflorix's 29.6% share is anchored by Gavi-supported pediatric programs in low- and middle-income countries, where GSK supplies more than 40 eligible nations under long-term supply agreements.

- North America's 41.8% global dominance is underpinned by ACIP-recommended routine infant dosing and 2024 CDC guidance broadening adult PCV20 and PCV21 eligibility above age 50.

- Emerging market momentum, notably Asia-Pacific at 21.4% share, is being reinforced by domestic PCV13-equivalent launches from Serum Institute (Pneumosil) and Walvax (PCV13-TT) targeting cost-sensitive public procurement.

- Adult immunization expansion is structurally lifting demand. The U.S. ACIP’s shared clinical decision-making recommendations for adult vaccines expand access to certain populations, enabling individualized vaccination decisions for adults aged 50+, rather than broad population-wide eligibility

Global Pneumococcal Vaccine Market Overview

Pneumococcal vaccines are biological preparations designed to protect against Streptococcus pneumoniae, a bacterium responsible for pneumonia, meningitis, bacteraemia, and otitis media. The market includes two principal product families: pneumococcal conjugate vaccines (PCVs) such as Prevnar 13, Prevnar 20, and Synflorix, and polysaccharide vaccines such as Pneumovax 23. These formulations serve distinct age groups and risk profiles across paediatric, adult, and immuno-compromised populations.

The industry sits at the intersection of public health policy, pharmaceutical innovation, and global immunization financing. Growth is anchored by macroeconomic drivers including expanding healthcare budgets in middle-income economies, aging demographics in OECD markets, and multilateral funding from Gavi, the Vaccine Alliance. Technological evolution toward higher-valency PCVs and recombinant platforms is reshaping the competitive landscape and extending the product lifecycle across developed and emerging markets.

Market Dynamics

To evaluate market opportunities, Request Sample

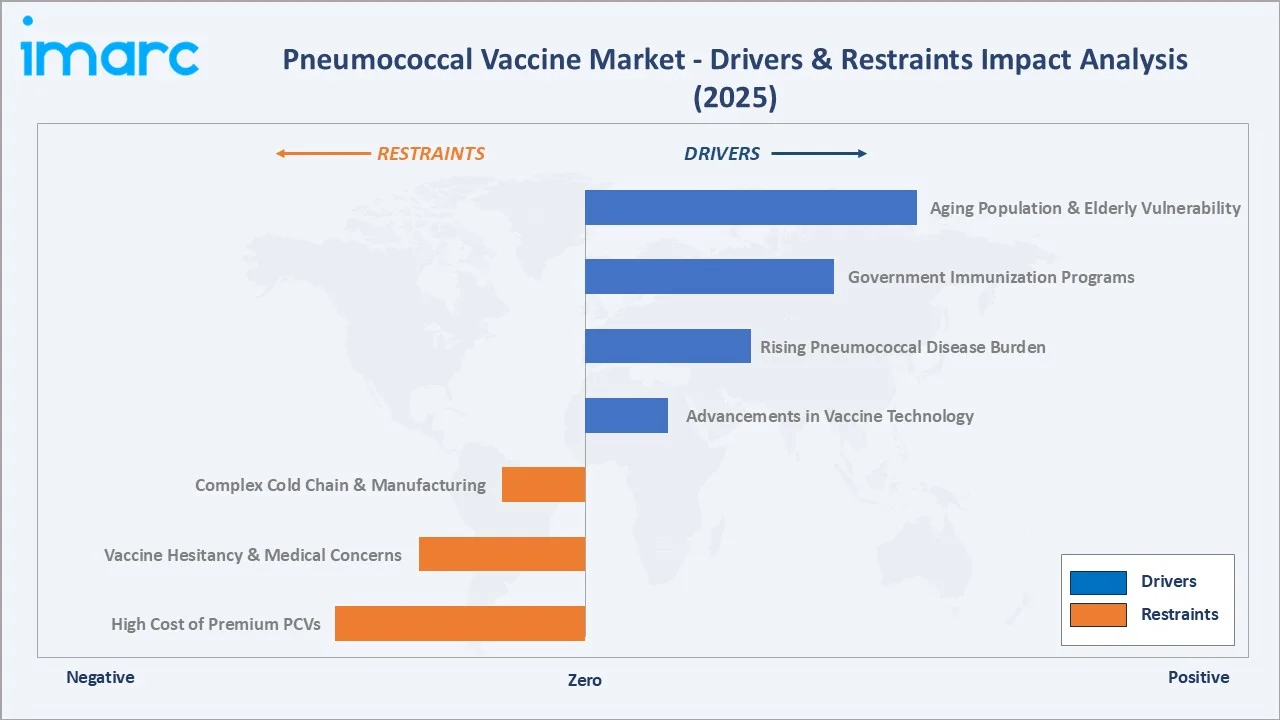

Market Drivers

- Aging Population and Elderly Vulnerability: The WHO projects the population aged 60+ to reach 2.1 billion by 2050. Older adults face markedly higher risk of invasive pneumococcal disease, driving sustained demand for adult-indicated PCV20 and PCV21 formulations in North America, Europe, and Japan.

- Government Immunization Programs: More than 150 countries have integrated PCVs into routine infant schedules. Gavi-supported pediatric coverage reached an estimated 82% in eligible low-income nations in 2024, creating structured multi-year procurement for Synflorix and Pneumosil.

- Rising Pneumococcal Disease Burden: Streptococcus pneumoniae remains a leading cause of community-acquired pneumonia and a major pathogen in pediatric sepsis. The WHO attributes nearly 20 million of global sepsis cases to children under 5, reinforcing the public-health case for expanded PCV coverage.

- Advancements in Vaccine Technology: Next-generation platforms such as Pfizer's PCV20 (Prevnar 20), Merck's Capvaxive (PCV21) approved by the U.S. FDA in June 2024, and Vaxcyte's V116 clinical-stage candidates are widening serotype coverage and lifting average selling prices across the adult segment.

Market Restraints

- High Cost of Premium PCVs: Private-market prices for Prevnar 20 and Capvaxive can exceed USD 250 per dose in developed markets, limiting affordability in self-pay settings and constraining uptake in middle-income procurement.

- Vaccine Hesitancy and Medical Concerns: Residual hesitancy following COVID-era misinformation is dampening adult catch-up campaigns. Safety-related concerns remain a persistent headwind, particularly in parts of Europe and Latin America.

- Complex Cold Chain and Manufacturing: PCVs require strict 2-8°C cold chain logistics and involve intricate conjugation chemistry, which limits the number of credible manufacturers and pressures margins for smaller entrants.

Market Opportunities

- Higher-Valency and Adult-Focused Vaccines: Expanded approvals for PCV20 and PCV21 open a sizeable adult immunization market. The U.S. ACIP’s 2024 expansion of routine pneumococcal vaccination to adults aged ≥50 significantly increases the addressable population, adding the previously uncovered 50–64 age cohort.

- Emerging-Market Domestic Manufacturing: Serum Institute's Pneumosil and Walvax's PCV13-TT are reshaping procurement economics in Africa and Asia. Gavi’s market-shaping strategy emphasizes supplier diversification to foster competition and reduce vaccine prices, supporting affordable and sustainable access to vaccines in lower-income countries

Market Challenges

- Serotype Replacement: Widespread PCV13 coverage has driven replacement disease from non-vaccine serotypes, compelling continuous reformulation. This dynamic inflates R&D cycles and creates obsolescence risk for lower-valency formulations over time.

- Regulatory Complexity: Divergent FDA, EMA, and WHO prequalification pathways add 18-24 months to global rollout timelines. Post-marketing surveillance requirements further raise the cost of maintaining a multi-region portfolio.

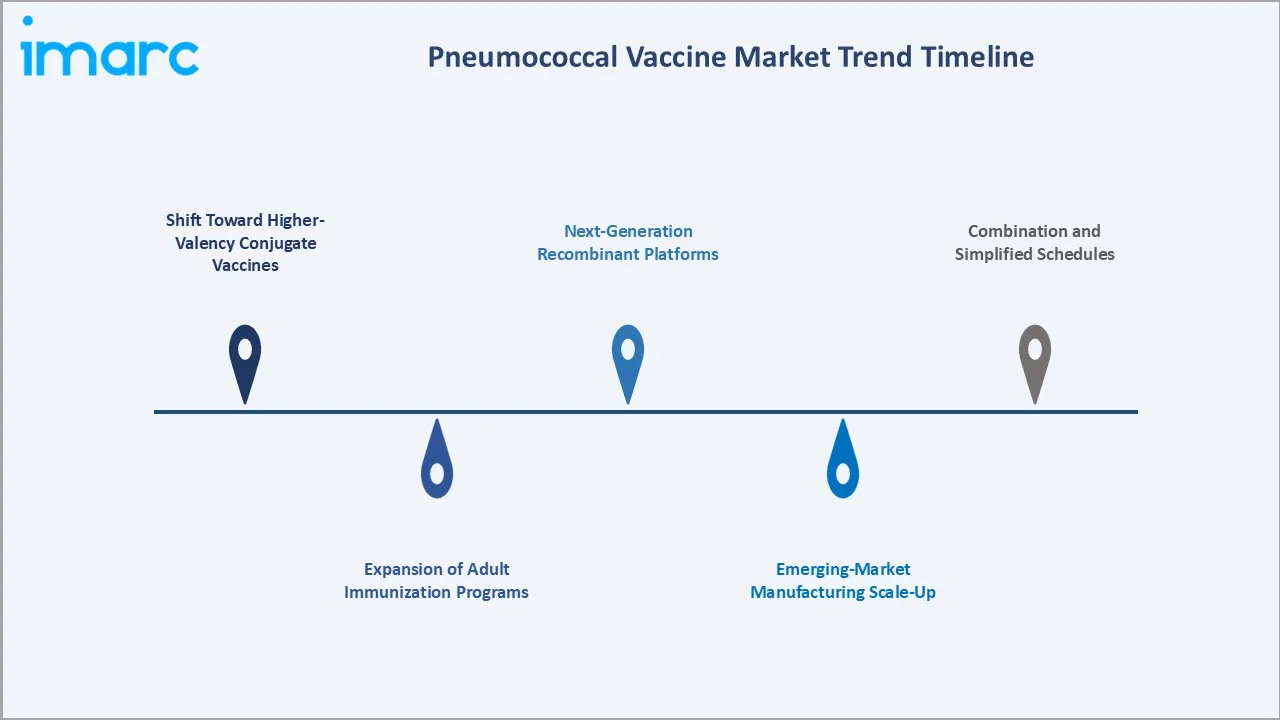

Emerging Market Trends

1. Shift Toward Higher-Valency Conjugate Vaccines

PCV20 and PCV21 are displacing PCV13 in adult immunization schedules across the U.S., EU, and Japan. Higher-valency platforms deliver broader serotype coverage and command premium pricing, supporting an estimated 3-4% annual uplift in average revenue per dose through 2030.

2. Expansion of Adult Immunization Programs

The adult pneumococcal market is the fastest-growing segment. ACIP's 2024 shared clinical decision-making recommendation for adults 50+ and parallel EMA guidance updates are driving pharmacy-led catch-up vaccination, particularly in the U.S. retail channel.

3. Emerging-Market Manufacturing Scale-Up

Serum Institute (Pneumosil) and Walvax (PCV13-TT) have reshaped global procurement economics. Pneumosil received WHO prequalification in December 2019 and has since expanded across multiple LMIC markets, supported by a long-term supply agreement of up to 100 million doses through Gavi-backed procurement mechanisms.

4. Next-Generation Recombinant Platforms

Vaxcyte's V116 and V117 candidates, built on cell-free protein synthesis technology, promise 24- and 30-valent coverage and are in late-stage clinical development. Positive Phase 3 readouts expected through 2026-2027 could redefine competitive benchmarks for adult immunization.

5. Combination and Simplified Schedules

Research into combination PCV-meningococcal and reduced-dose (2+1 vs 3+1) infant schedules is gaining traction. Simplified regimens could ease cold-chain burden in low-income markets while preserving clinical efficacy, expanding the addressable base across Sub-Saharan Africa and South Asia.

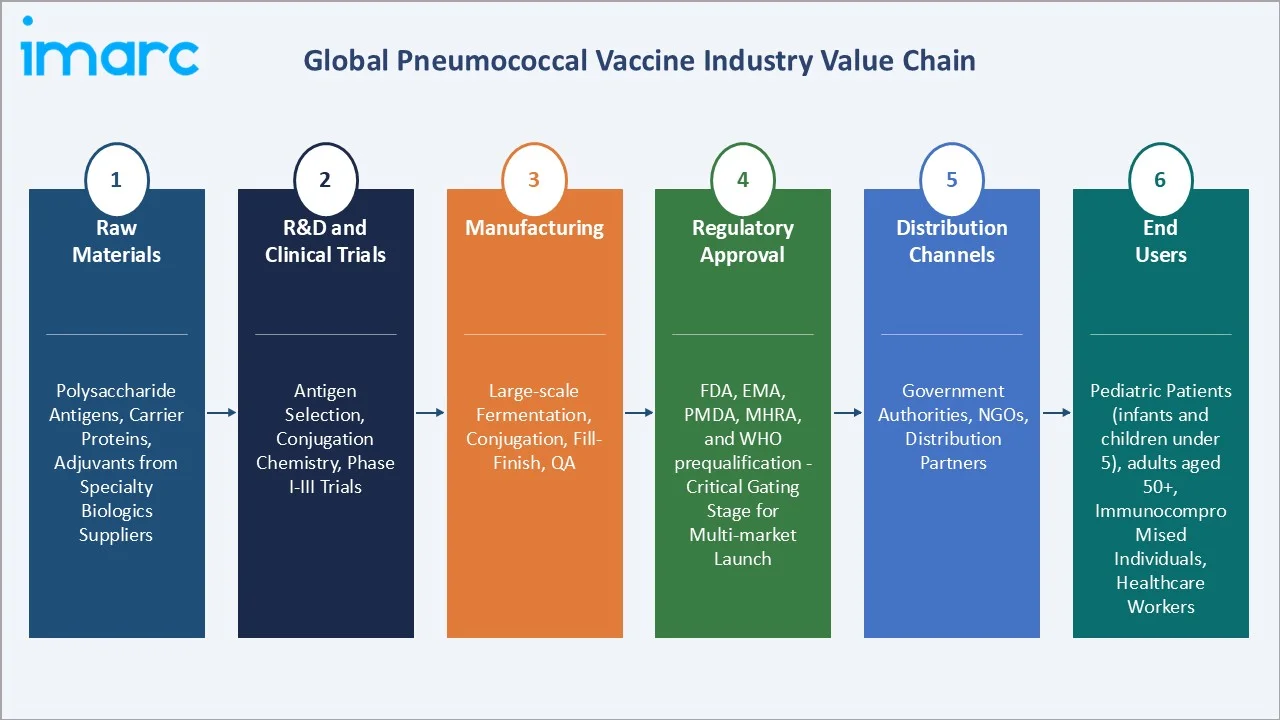

Industry Value Chain Analysis

The global pneumococcal vaccine value chain spans six integrated stages from antigen production through end-recipient immunization. Each stage features distinct competitive dynamics, margin structures, and technological investment requirements relevant to the overall pneumococcal vaccine market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Polysaccharide antigens, carrier proteins (CRM197, tetanus toxoid), adjuvants, lipid excipients sourced from specialty biologics suppliers |

|

R&D and Clinical Trials |

Antigen selection, conjugation chemistry, and Phase I-III trials - led by Pfizer, Merck, GSK, Sanofi, Vaxcyte, and Serum Institute of India |

|

Manufacturing |

Large-scale fermentation, conjugation, fill-finish, QA release - Pfizer (McPherson, Ireland), Merck (Durham), GSK (Belgium), Serum (Pune) |

|

Regulatory Approval |

FDA, EMA, PMDA, MHRA, and WHO prequalification - critical gating stage for multi-market launch |

|

Distribution Channels |

Government authorities, NGOs (Gavi, UNICEF), distribution partner companies serving ~65% of global paediatric volume |

|

End Users |

Paediatric patients (infants and children under 5), adults aged 50+, immunocompromised individuals, healthcare workers |

Manufacturers hold the highest strategic value by integrating proprietary conjugation chemistry, sterile fill-finish capacity, and complex regulatory dossiers. Meanwhile, multilateral procurement through Gavi and PAHO Revolving Fund continues to reshape pricing dynamics in emerging markets, offering high-volume access in exchange for structured multi-year tenders.

Technology Landscape in the Pneumococcal Vaccine Industry

Conjugation Chemistry

Conjugation of capsular polysaccharides to carrier proteins such as CRM197 and tetanus toxoid remains the cornerstone PCV technology. Advances in site-specific conjugation are improving immunogenicity and enabling 20- and 21-valent formulations without proportional antigen interference, a critical factor for Prevnar 20 and Capvaxive.

Recombinant and Cell-Free Platforms

Vaxcyte’s XpressCF platform enables high-valency conjugate vaccines (24-valent and beyond 30 serotypes) by bypassing constraints of traditional fermentation-based manufacturing and supporting more efficient, scalable vaccine design, with the potential to accelerate development timelines (Source: Vaxcyte).

Adjuvant and Formulation Innovation

Novel adjuvant systems including aluminum-based and saponin-based adjuvants are being evaluated to enhance immunogenicity in elderly populations, where immunosenescence typically blunts vaccine response. These innovations are particularly relevant for adult-indicated formulations targeting the 65+ demographic.

Cold Chain and Digital Quality Assurance

Investment in passive cold-chain containers, real-time temperature monitoring, and blockchain-enabled batch tracking is reducing wastage. Gavi-supported programs are leveraging digital cold chain solutions to improve vaccine management and reduce wastage, with some country deployments reporting substantial reductions in stock losses, even as global wastage rates remain significant.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Vaccine Type | Pneumococcal Conjugate Vaccine | 71.6% |

2025 |

| Product Type | Prevnar 13 |

48.7% |

2025 |

| Distribution Channel | Non-Governmental Organizations (NGO) |

🔒 |

2025 |

| End User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

41.8% |

2025 |

IMARC Group provides a detailed analysis of the key trends in each segment of the global pneumococcal vaccine market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on vaccine type and product type.

By Vaccine Type

Pneumococcal conjugate vaccines lead the global market with a 71.6% share in 2025. Demand is driven by broad paediatric adoption and progressive expansion into adult indications. PCV20 and PCV21 are accelerating average selling prices in the U.S. and EU, while PCV13 continues to dominate infant schedules in emerging markets. Sensor-based cold-chain monitoring and co-administration approvals with influenza and RSV vaccines are strengthening commercial positioning.

To access detailed market analysis, Request Sample

Pneumococcal polysaccharide vaccines account for 28.4% of the global market, led by Pneumovax 23. Although volume is smaller than conjugate formulations, the segment retains relevance for adults with specific risk profiles due to its broad 23-serotype coverage. ACIP guidance continues to position PPSV23 as complementary to PCVs in adult sequential schedules, sustaining steady demand through 2034.

By Product Type

Prevnar 13 is the dominant product globally, commanding 48.7% of pneumococcal vaccine revenue in 2025. Pfizer's flagship PCV13 remains the cornerstone of paediatric immunization schedules in more than 100 countries and has progressively transitioned adult demand toward Prevnar 20 following 2021 FDA approval. Commercial continuity is supported by broad private-payer coverage in the U.S. and government procurement in Europe and Japan.

Synflorix, developed by GSK, holds 29.6% of global product share. The 10-valent conjugate vaccine is a key supply asset in Gavi-supported pediatric programs, serving more than 40 eligible countries under multi-year agreements. Pneumovax 23, Merck's 23-valent polysaccharide vaccine, accounts for 21.7%, primarily serving adult populations in developed markets through sequential PCV-PPSV23 schedules and risk-based indications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

41.8% |

CDC/ACIP immunization schedules, Medicare coverage, private payer reimbursement, PCV20/PCV21 adult uptake |

|

Europe |

25.6% |

EMA harmonized approvals, national immunization programs, aging population, Prevnar 20 rollout |

|

Asia-Pacific |

21.4% |

China NIP inclusion, India UIP scale-up, Japan adult PCV coverage, domestic manufacturing (Serum, Walvax) |

|

Latin America |

6.2% |

PAHO Revolving Fund procurement, Brazil PNI program, Mexico universal pediatric coverage |

|

Middle East & Africa |

5.0% |

Gavi-supported PCV introductions, GCC national programs, domestic fill-finish expansion |

North America commands 41.8% global revenue share in 2025. The United States anchors regional dominance with a robust CDC/ACIP framework supporting both pediatric 2+1 dosing and adult sequential PCV20-PPSV23 schedules. Medicare Part B reimbursement for adult PCVs and broad private-insurance coverage underpin sustained demand. Canada contributes through NACI-aligned provincial programs, while both markets continue transitioning adult volume to PCV20 and PCV21 following 2023-2024 expanded approvals.

Europe holds 25.6% of global revenue, supported by centralized EMA approvals and national immunization programs in Germany, France, UK, Italy, and Spain. In June 2025, the European Centre for Disease Prevention and Control (ECDC) reinforced adult vaccination guidance emphasizing PCV uptake among individuals aged 65+. Asia-Pacific accounts for 21.4%, led by China's progressive NIP inclusion, India's Universal Immunization Programme, and Japan's adult PCV coverage. Latin America represents 6.2%, supported by PAHO procurement, while Middle East & Africa contributes 5.0% with strong Gavi-supported introductions across Sub-Saharan Africa.

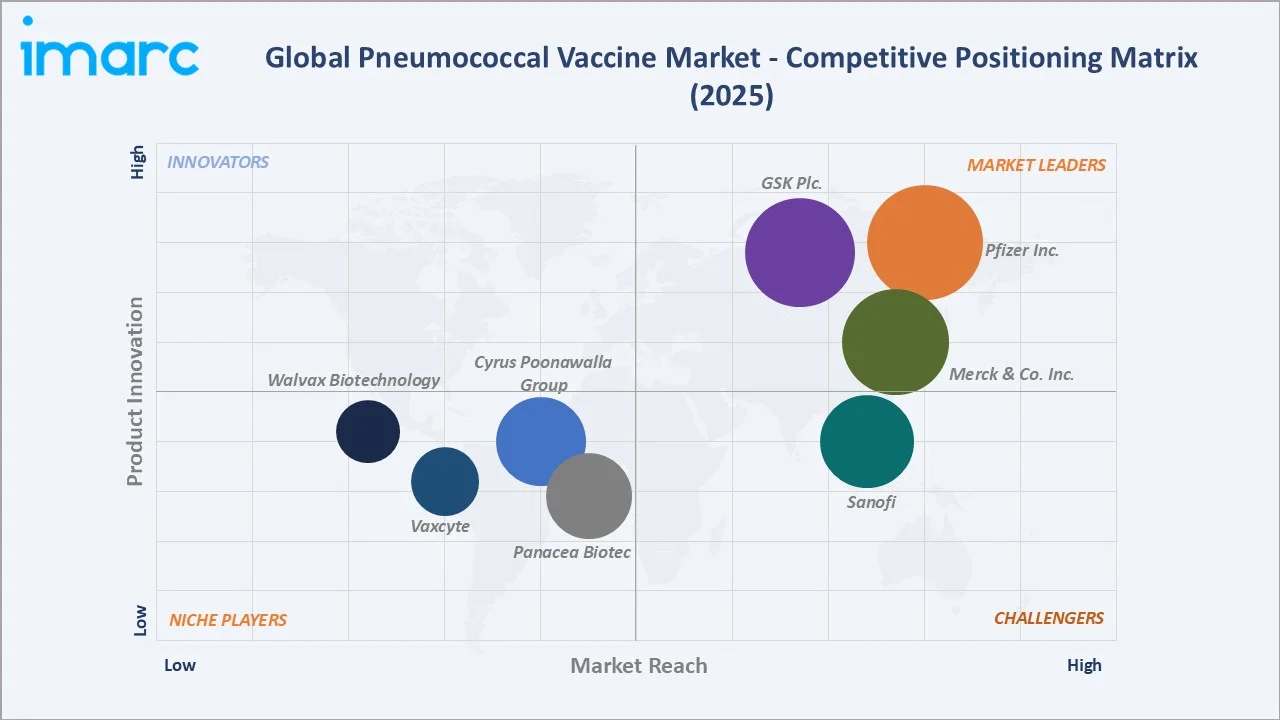

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

| Pfizer Inc. | Prevnar 13, Prevnar 20 | Leader | Adult and pediatric franchise dominance, global scale |

| Merck & Co. Inc. | CAPVAXIVE™ | Leader | Adult PCV21 innovation, 21-serotype breadth |

| GSK Plc. | Synflorix | Leader | Gavi pediatric procurement, emerging markets |

| Sanofi | PCV21 | Challenger | R&D collaborations, combination vaccine platforms |

| Cyrus Poonawalla Group | Serum Institute of India (Pneumosil) | Emerging | Low-cost manufacturing, WHO prequalification, Africa scale |

| Walvax Biotechnology Co. Ltd | Meningococcal Polysaccharide Vaccine, Pneumococcal Polysaccharide Conjugate Vaccine | Emerging | China domestic leadership, Asia-Pacific reach |

| Panacea Biotec | NuVac-23, NuCoVac-11 | Emerging | India UIP supply, combination product portfolio |

| Vaxcyte | Vax-31, Vax-24 | Emerging | Cell-free protein synthesis, higher-valency candidates |

The global pneumococcal vaccine market's competitive landscape is moderately concentrated at the top, with Pfizer, Merck, and GSK commanding a dominant share. Leading players compete on serotype coverage, adult indications, clinical trial outcomes, and Gavi procurement positioning. Strategic acquisitions remain an important tool. In November 2023, Vaxcyte signed a commercial-scale manufacturing agreement with Lonza to support its V116 launch preparations, highlighting the capital-intensity of late-stage PCV development.

Key Company Profiles

Pfizer Inc.

Pfizer Inc. is a global biopharmaceutical leader headquartered in New York, USA. Founded in 1849, the company operates across vaccines, oncology, internal medicine, and rare disease therapeutics in more than 125 countries.

- Product & Platform Portfolio: Pfizer's pneumococcal franchise is anchored by Prevnar 13 and Prevnar 20 (PCV20), with broad approvals spanning pediatric and adult indications across the U.S., EU, and Japan.

- Recent Developments: In January 2024, Pfizer received marketing authorization from the EMA's CHMP for its 20-valent pneumococcal conjugate vaccine (20vPnC) for pediatric use, extending Prevnar 20 into infant and child immunization schedules.

- Strategic Focus: Pfizer's strategy centres on defending Prevnar leadership through serotype expansion, driving adult immunization through Prevnar 20, and leveraging global manufacturing scale to compete in tiered-pricing procurement.

Merck & Co. Inc.

Merck & Co. Inc. (known as MSD outside the U.S. and Canada) is a leading global pharmaceutical company headquartered in Rahway, New Jersey. Founded in 1891, Merck operates across human health, animal health, and vaccines segments in more than 140 countries.

- Product & Platform Portfolio: Merck's pneumococcal portfolio includes Pneumovax 23 (PPSV23) and Capvaxive (PCV21), which received U.S. FDA approval in June 2024 as the first 21-valent pneumococcal conjugate vaccine specifically designed for adults.

- Recent Developments: In June 2024, Merck secured FDA approval for Capvaxive (PCV21) for adults aged 18+, providing coverage for serotypes responsible for approximately 85% of invasive pneumococcal disease cases in U.S. adults aged 50+.

- Strategic Focus: Merck's strategy focuses on establishing Capvaxive as the adult immunization standard, sustaining Pneumovax 23 in sequential schedules, and expanding international approvals through EMA and other regulatory pathways.

GSK Plc.

GSK Plc. is a global biopharmaceutical company headquartered in Brentford, United Kingdom. Founded in 2000 through the merger of Glaxo Wellcome and SmithKline Beecham, GSK serves specialty medicines, vaccines, and general medicines across more than 150 countries.

- Product & Platform Portfolio: GSK's pneumococcal portfolio centres on Synflorix, a 10-valent PCV designed for pediatric use, with strong positioning in Gavi-eligible low- and middle-income countries supported by long-term supply agreements.

- Recent Developments: GSK continues to advance its next-generation PCV pipeline and has strengthened emerging-market supply commitments through multi-year Gavi procurement contracts, supporting over 40 eligible countries with Synflorix doses.

- Strategic Focus: GSK's strategy prioritizes Synflorix leadership in Gavi markets, investment in next-generation PCV and combination vaccine candidates, and expansion of its adult vaccines franchise across its global infectious disease portfolio.

Market Concentration Analysis

The global pneumococcal vaccine market is highly concentrated at the top. The leading three players - Pfizer, Merck, and GSK - collectively account for approximately 80-85% of global market revenue in 2025. Pfizer alone holds an estimated 55-60% share through Prevnar 13 and Prevnar 20 combined. The remaining market is distributed across Sanofi, Serum Institute, Walvax, Panacea Biotec, and clinical-stage challengers such as Vaxcyte.

The market is experiencing a bifurcated dynamic. At the premium tier, consolidation is intensifying around higher-valency conjugate platforms, adult immunization indications, and next-generation recombinant candidates. Meanwhile, domestic manufacturers in India and China are reshaping low- and middle-income procurement by supplying cost-optimized PCV10 and PCV13-equivalent products, supported by Gavi and regional public procurement agencies through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Adult immunization represents the highest-growth end-user segment at an estimated 4.9% CAGR through 2030, propelled by ACIP-expanded eligibility and PCV20/PCV21 uptake. Middle East & Africa is the fastest-accelerating region at approximately 5.8% CAGR, driven by Gavi-supported introductions. Higher-valency conjugate platforms - PCV20, PCV21, and pipeline candidates V116/V117 - represent the premium growth opportunity, with Capvaxive generating more than USD 200 million in initial U.S. revenue within six months of launch.

Emerging Market Expansion

China and India represent the highest-potential emerging markets, supported by domestic manufacturing (Walvax, Serum, Panacea) and progressive inclusion of PCVs in national immunization programs. Sub-Saharan Africa's Gavi-supported pediatric coverage and Southeast Asia's adult immunization expansion collectively represent USD 1.5-2.0 billion in medium-term incremental revenue opportunity through 2030.

Venture and Strategic Investment Trends

Strategic partnerships are reshaping the innovation landscape. In November 2023, Vaxcyte signed a commercial manufacturing agreement with Lonza to scale V116 production. Investment in cell-free protein synthesis platforms, higher-valency serotype coverage, and adjuvant innovation for elderly immunization are the primary focus areas for venture and corporate capital in the pneumococcal vaccine industry through 2034.

Future Market Outlook (2026-2034)

The global pneumococcal vaccine market forecast projects steady value expansion from USD 10.26 Billion in 2025 to USD 15.51 Billion by 2034 at a CAGR of 4.30%. North America will retain regional leadership while emerging markets accelerate structurally. Europe and Japan will sustain premium value growth through adult immunization expansion and higher-valency product transitions.

Three key shifts will reshape the pneumococcal vaccine market through 2034. First, higher-valency PCVs (20-, 21-, and 24-valent platforms) will progressively replace PCV13 in both pediatric and adult schedules, lifting average revenue per dose by an estimated 3-4% annually in developed markets. Second, adult immunization will transition from a supplementary segment to a core demand pillar, particularly in the U.S. and EU. Third, domestic manufacturers in India and China are expected to achieve comparable serotype coverage and quality benchmarks, intensifying competition in Gavi and middle-income tenders across Asia-Pacific, Africa, and Latin America.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with pneumococcal vaccine industry stakeholders, including medical directors at multinational vaccine manufacturers, procurement specialists at multilateral agencies (Gavi, UNICEF, PAHO), public-health officials at national immunization programmes, hospital pharmacy leads, and biotech investors. Primary insights validated market sizing, segmentation estimates, and adoption timelines.

Secondary Research

Secondary sources include WHO publications, U.S. CDC and ACIP guidance, EMA and FDA approval records, Gavi and UNICEF procurement dashboards, company annual reports and SEC filings, peer-reviewed journals including The Lancet and Vaccine, trade publications, and regional public-health association databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating demographic trends, immunization coverage rates, per-dose pricing, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for regulatory and public-health uncertainty.

Pneumococcal Vaccine Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Pneumococcal Vaccine Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vaccine Types Covered | Pneumococcal Conjugate Vaccine, Pneumococcal Polysaccharide Vaccine |

| Product Types Covered | Prevnar 13, Synflorix, Pneumovax 23 |

| Distribution Channels Covered | Distribution Partner Companies, Non-Governmental Organizations (NGO), Government Authorities |

| End Users Covered | Pediatrics, Adults |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Pfizer Inc., Merck & Co. Inc., GSK Plc., Sanofi, Cyrus Poonawalla Group, Walvax Biotechnology Co. Ltd, Panacea Biotec, Vaxcyte, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pneumococcal vaccine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global pneumococcal vaccine market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pneumococcal vaccine industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Pneumococcal Vaccine Market Report

The global pneumococcal vaccine market was valued at USD 10.26 Billion in 2025, driven by aging populations, expanding government immunization programs, and rising adult immunization uptake.

The market is projected to reach USD 15.51 Billion by 2034, growing at a CAGR of 4.30% during 2026-2034, supported by higher-valency conjugate vaccines and adult immunization expansion.

Pneumococcal conjugate vaccines lead with a 71.6% share in 2025, driven by broad pediatric adoption, expanded adult indications, and higher-valency platforms such as PCV20 and PCV21.

Prevnar 13 holds the largest share at 48.7% in 2025, supported by routine pediatric use in over 100 countries and Pfizer's established global distribution and reimbursement footprint.

North America dominates with a 41.8% share in 2025, anchored by CDC/ACIP immunization schedules, strong Medicare and private-payer reimbursement, and rapid Prevnar 20 adoption.

Key drivers include aging populations, government immunization programs, rising pneumococcal disease burden, expanded adult indications, and advancements in higher-valency conjugate vaccine technology.

Major players include Pfizer Inc., Merck & Co. Inc., GSK Plc., Sanofi, Cyrus Poonawalla Group, Walvax Biotechnology Co. Ltd, Panacea Biotec, Vaxcyte, with Pfizer holding the leading global share.

Adult immunization is the fastest-growing end-user segment at approximately 4.9% CAGR through 2030, driven by ACIP eligibility expansion and uptake of Prevnar 20 and Capvaxive.

Key opportunities include higher-valency PCVs, adult immunization platforms, emerging-market domestic manufacturing, cell-free recombinant technologies, and adjuvants optimized for elderly populations.

COVID-19 boosted awareness of respiratory vaccines and accelerated adult immunization discussions, supporting sustained demand for PCVs as complementary protection against secondary bacterial pneumonia.

Capvaxive (PCV21) is Merck's 21-valent conjugate vaccine approved by the FDA in June 2024 for adults, covering serotypes responsible for roughly 85% of invasive pneumococcal disease in U.S. adults.

Gavi's multi-year procurement of Synflorix and Pneumosil has driven pediatric coverage above 85% in eligible countries, while recent multi-supplier sourcing is reshaping global pricing dynamics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)