Polyethylene Terephthalate (PET) Fabric Market Size, Share, Trends and Forecast by Source, Fabric Type, Form, Application, and Region, 2026-2034

Polyethylene Terephthalate (PET) Fabric Market Size and Share:

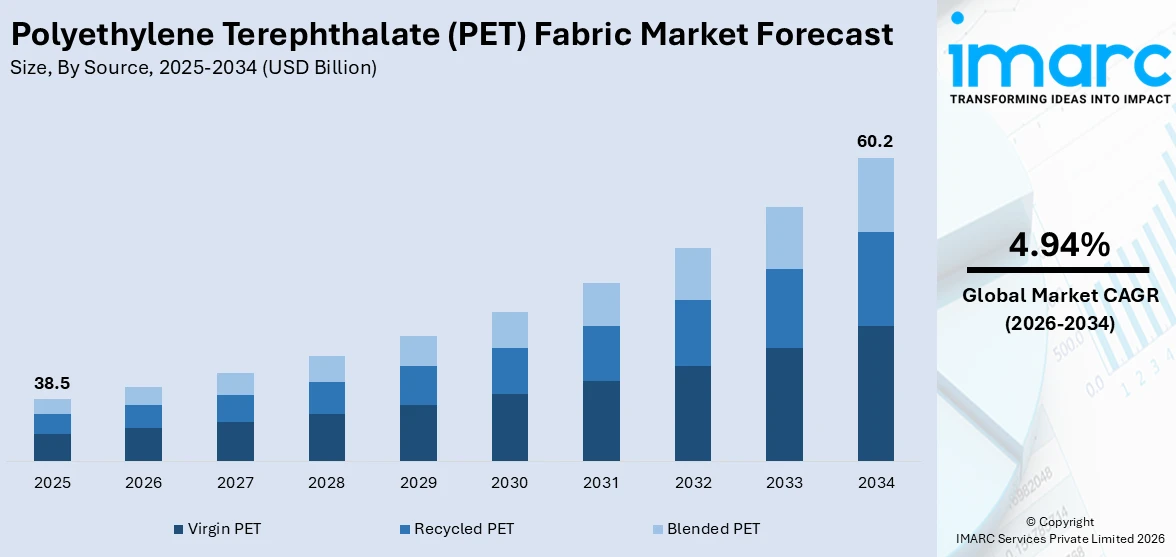

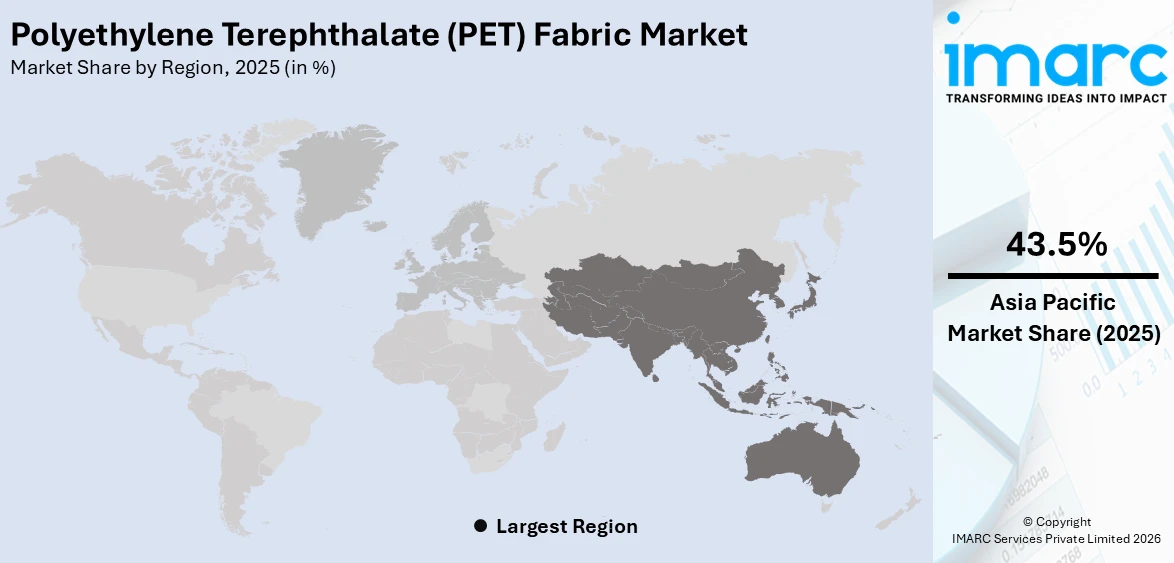

The global polyethylene terephthalate (PET) fabric market size was valued at USD 38.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 60.2 Billion by 2034, exhibiting a CAGR of 4.94% during 2026-2034. Asia-Pacific currently dominates the market, holding a significant market share of over 43.5% in 2025, due to its extensive textile manufacturing capacity, low production costs, and high domestic demand from industries like apparel, automotive, and home furnishings. The region also benefits from strong government support, expanding recycling initiatives, and a well-established supply chain.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 38.5 Billion |

|

Market Forecast in 2034

|

USD 60.2 Billion |

| Market Growth Rate 2026-2034 | 4.94% |

The global polyethylene terephthalate (PET) fabric industry is majorly impacted by heightening requirement for cost-efficient, durable, and lightweight textiles in several key sectors, mainly encompassing home furnishings, apparel, and automotive. Notable increase in customer preference for synthetic fibers because of their robustness, moisture resistance, and recyclability is further bolstering market expansion. Enhancements in PET recycling technologies and increasing sustainability initiatives are supporting the adoption of recycled PET fabrics. Additionally, expanding applications in technical textiles, such as industrial filtration and protective clothing, are driving demand. Rapid urbanization, evolving fashion trends, and growth in the sportswear and athleisure segments are further contributing to the polyethylene terephthalate (PET) fabric market growth.

To get more information on this market Request Sample

The United States plays a significant role in the global PET fabric market, driven by strong demand from the apparel, automotive, and home furnishing sectors. The growing preference for durable, lightweight, and moisture-resistant textiles is fueling market expansion. Increasing sustainability initiatives, including the adoption of recycled PET fabrics, are further supporting growth. The presence of major textile manufacturers, advancements in fabric innovation, and expanding applications in performance wear and technical textiles contribute to market development. In addition to this, government policies promoting recycling and sustainable materials are accelerating the adoption of PET-based fabrics across various industries. For instance, as per industry reports, around 25% of PET obtained from packaging is recycled across the United States, with the nation actively striving to increase this by developing a new recycling plant in Alabama that will capture approximately 1.3 million new pounds of PET annually.

Polyethylene Terephthalate (PET) Fabric Market Trends:

Growing Demand for PET Fabrics in the Textile Industry

The rising demand for PET fabrics is largely driven by their increasing utilization in the textile sector, as manufacturers seek alternatives to natural fibers such as cotton and wool. PET fabrics offer numerous advantages, including durability, resistance to wrinkles, heat, and stretching, making them highly suitable for fashion, sportswear, and industrial textiles. Additionally, government initiatives supporting textile research and development are further fueling industry growth. According to the India Brand Equity Foundation, in June 2023, the Indian government approved R&D projects worth USD 7.4 million in the textile sector. These investments are expected to drive innovation and expand the application of PET fabrics in various industries. The shift toward synthetic fibers is also influenced by fluctuating raw material costs and the need for sustainable textile solutions, further strengthening the PET fabric market’s growth.

Increasing Adoption of Recycled PET Fabrics for Sustainability

Environmental concerns over plastic waste and carbon emissions is one of the major polyethylene terephthalate (PET) fabric market trends significantly shaping the industry dynamics. For instance, the world produced around 400 million tons of plastic waste per year. As a result, industries are increasingly adopting recycled PET fibers to minimize pollution and promote circular economy practices. Fabrics made from recycled PET bottles help reduce landfill waste and lower the environmental impact without compromising quality. This has led to the widespread adoption of recycled PET in applications such as fiber filling for insulated clothing, disposable medical garments, and eco-friendly fashion. The anti-bacterial and anti-fungal properties of PET fibers further enhance their appeal in the healthcare and protective clothing sectors. As sustainability becomes a priority for consumers and businesses, the market for recycled PET fabrics continues to expand, supported by advancements in recycling technologies and increasing regulatory emphasis on sustainable material usage.

Expanding Use of PET Fabrics in Performance and Technical Textiles

The demand for PET fabrics is rising in performance and technical textiles due to their superior strength, durability, and resistance to environmental factors. Industries such as automotive, aerospace, and industrial manufacturing are increasingly incorporating PET fabrics into high-performance applications, including seat covers, airbags, filtration systems, and protective gear. For instance, in August 2024, Škoda Elroq launched its sustainable design for automotive interior by utilizing materials like Technofi and Recytitan. Recytitan is primarily leveraged by the company for the production of dashboard, door panels, armrest, seat covers, and knee pads, and it is made of 78% recycled for of PET, with leftover material composed of 16% new PET. Moreover, the growing focus on lightweight and high-strength materials in automotive interiors and industrial fabrics is further driving demand. Additionally, advancements in fabric engineering have enabled the development of PET textiles with enhanced breathability, UV resistance, and moisture-wicking properties, making them ideal for sportswear and outdoor apparel. As manufacturers innovate to meet evolving industry standards and sustainability goals, it shapes a positive polyethylene terephthalate (PET) fabric market outlook.

Polyethylene Terephthalate (PET) Fabric Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global polyethylene terephthalate (PET) fabric market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on source, fabric type, form, and application.

Analysis by Source:

- Virgin PET

- Recycled PET

- Blended PET

Virgin PET stand as the largest source segment in 2025, holding around 78.6% of the market, due to its widespread use in high-quality textile applications. It offers superior strength, durability, and resistance to wear and moisture, making it the preferred choice for apparel, home furnishings, and industrial textiles. The availability of cost-effective raw materials and advanced polymerization technologies supports its large-scale production. While sustainability concerns are driving the growth of recycled PET, virgin PET remains dominant due to its consistent performance, purity, and ability to meet stringent quality standards. Manufacturers continue to invest in process enhancements to improve efficiency and reduce environmental impact. Additionally, growing demand from sectors such as sportswear, outdoor gear, and high-performance fabrics reinforces its market position. Despite increasing regulatory pressure to promote circular economy practices, virgin PET continues to lead, particularly in applications requiring premium material properties and long-term durability.

Analysis by Fabric Type:

- Woven

- Non-Woven

- Knitted

Woven polyethylene terephthalate (PET) fabric is crucial due to its high durability, tensile strength, and versatility across various industries. It is widely used in apparel, upholstery, industrial textiles, and automotive applications, offering excellent dimensional stability and resistance to wear. The structured interlacing of fibers enhances fabric longevity, making it ideal for high-performance and heavy-duty applications. Increasing demand for strong, lightweight textiles further supports its market growth.

Non-woven PET fabric is gaining traction due to its cost-effectiveness, lightweight nature, and diverse applications in hygiene products, filtration, and geotextiles. Its seamless structure offers breathability, moisture resistance, and enhanced functionality in medical and industrial use. Advancements in spunbond and meltblown technologies are driving product innovation, while rising demand for sustainable and disposable textiles is further accelerating the growth of this segment.

Knitted PET fabric holds a significant market share, particularly in sportswear, athleisure, and technical textiles. Its elasticity, softness, and breathability make it highly desirable for stretchable and form-fitting applications. The fabric’s ability to provide comfort while maintaining durability is driving its adoption in fashion and activewear. Continuous advancements in knitting technology, along with the demand for moisture-wicking and performance textiles, are contributing to its expansion.

Analysis by Form:

- Staple

- Filament

- Fiberfill

- Tow

Staple fiber holds a significant share in the global PET fabric market due to its widespread use in apparel, home textiles, and nonwoven applications. It offers excellent durability, moisture resistance, and affordability, making it a preferred choice for blended fabrics and insulation materials. Growing demand for sustainable textiles has also led to increased production of recycled PET staple fiber, further strengthening its market presence.

Filament PET fibers are prominent in the market due to their superior strength, smooth texture, and versatility in textile manufacturing. These continuous fibers are widely used in high-performance fabrics, sportswear, and technical textiles requiring durability and flexibility. Their application in industrial textiles, such as conveyor belts and automotive interiors, further drives demand. Advancements in filament yarn processing continue to enhance product quality and expand market opportunities.

Fiberfill PET fibers hold a strong market position due to their extensive use in insulation, bedding, and upholstery applications. Their lightweight structure, thermal efficiency, and resilience make them ideal for comfort-based products. Increasing demand for eco-friendly and hypoallergenic fiberfill materials has further fueled growth, with manufacturers focusing on sustainable production practices and recycled PET-based fiberfill solutions to meet consumer and regulatory requirements.

Tow PET fibers contribute significantly to the market, primarily serving filtration, industrial, and specialty textile applications. These large bundles of continuous fibers are essential in producing high-strength fabrics and technical materials. Their application in cigarette filters, upholstery, and reinforcement textiles highlights their importance. Increasing investments in advanced manufacturing processes and rising demand for high-performance synthetic fibers are driving growth in the PET tow segment.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Apparel

- Household

- Industrial

- Carpet and Rugs

- Others

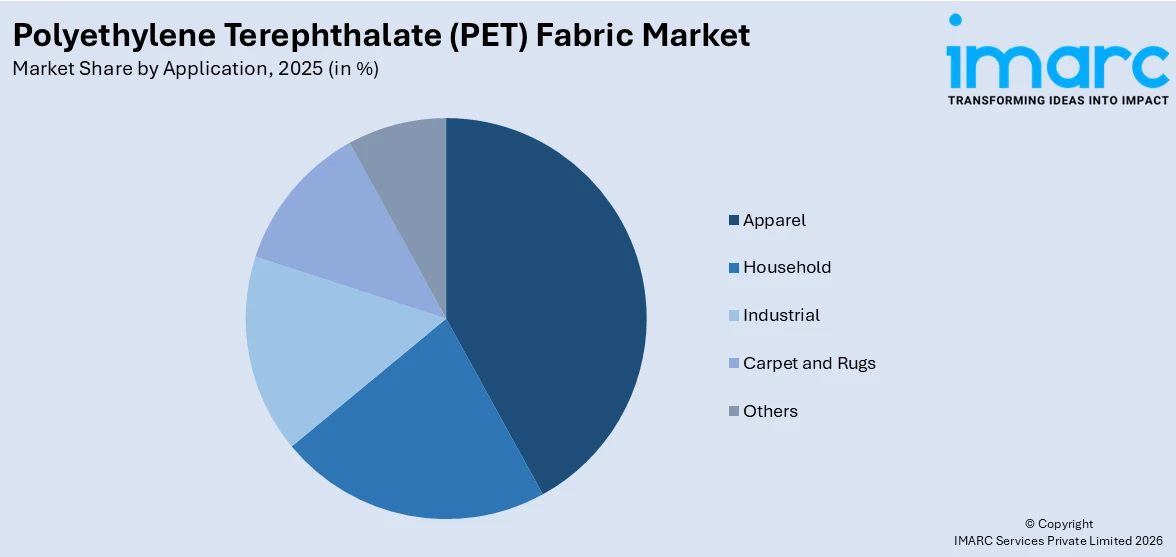

Apparel accounts for the majority of the polyethylene terephthalate (PET) fabric market share, driven by rising demand for durable, lightweight, and moisture-resistant textiles. PET fabrics are widely used in sportswear, athleisure, and fast fashion due to their strength, wrinkle resistance, and affordability. The growth of e-commerce and shifting consumer preferences toward functional and sustainable clothing further support market expansion. Additionally, PET fabrics offer versatility in blending with natural fibers, enhancing their appeal for diverse fashion applications. Manufacturers are increasingly focusing on developing high-performance PET-based textiles with advanced features such as UV resistance, breathability, and antimicrobial properties. Sustainability initiatives are also influencing the segment, with brands incorporating recycled PET fabrics to reduce environmental impact. The expanding influence of global fashion trends, rapid urbanization, and increased spending on affordable yet high-quality clothing reinforce the apparel segment’s dominant position in the PET fabric market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- Italy

- Spain

- Poland

- United Kingdom

- Others

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Others

- Middle East and Africa

- Turkey

- Saudi Arabia

- United Arab Emirates

- Israel

- Others

- Latin America

- Brazil

- Mexico

- Others

In 2025, Asia-Pacific accounted for the largest market share of over 43.5%. The growing PET fabric market demand is influenced by the increasing plastic waste, driving a shift towards sustainable textile alternatives. According to reports, India is home to population surpassing 1.4 billion and yields 26,000 tons of plastic waste on a daily basis. The demand for eco-friendly solutions is rising as industries focus on minimizing environmental impact. The accumulation of plastic waste has led to a surge in interest in recyclable materials, with PET fabric emerging as a viable option. The push for circular economy initiatives is increasing, encouraging the use of synthetic fibers derived from post-consumer plastics. The growing awareness of environmental sustainability is prompting manufacturers to invest in textile solutions that reduce landfill waste. The demand for versatile and lightweight fabrics made from recycled materials is expanding across multiple applications, supporting the shift towards resource-efficient alternatives. The increased focus on waste management strategies is fueling the production of PET fabric, aligning with efforts to address plastic pollution concerns. The rising integration of sustainable practices in the textile industry is promoting the adoption of synthetic fabrics that contribute to waste reduction while meeting performance requirements.

Key Regional Takeaways:

United States Polyethylene Terephthalate (PET) Fabric Market Analysis

In 2025, the United States accounted for 89.50% of the market share in North America. The growing PET fabric adoption is driven by the increasing demand for anti-bacterial and anti-fungal properties due to growing skin problems. For instance, 31.6 million individuals, i.e., 10.1%, across the US have some kind of eczema. Rising consumer awareness about hygiene and health is influencing fabric choices, leading to a preference for materials with anti-microbial properties. The demand for durable and moisture-resistant textiles is increasing, particularly in activewear and medical applications, as consumers seek long-lasting and hygienic solutions. With the growing emphasis on personal care and wellness, the preference for fabrics that prevent bacterial and fungal growth is expanding. The rising cases of skin sensitivities and allergies have further fueled the shift towards synthetic materials that provide enhanced protection. Additionally, the demand for functional textiles that offer both comfort and health benefits is shaping the market. The emphasis on sustainable production and technological advancements in fabric treatment is increasing, further supporting the adoption of polyethylene terephthalate (PET) fabric. As the demand for innovative materials that combine hygiene with durability continues to rise, manufacturers are developing solutions that integrate anti-bacterial and anti-fungal attributes, ensuring market expansion.

North America Polyethylene Terephthalate (PET) Fabric Market Analysis

North America is a key market for PET fabric, driven by strong demand from the apparel, automotive, and home furnishing industries. The region's growing emphasis on sustainability has accelerated the adoption of recycled PET fabrics, supported by government regulations and corporate sustainability initiatives. Innovations in textile technology, encompassing the designing of high-performance and moisture-resistant fabrics, are further fueling market growth. The expanding sportswear, athleisure, and technical textile segments contribute to increasing PET fabric consumption. For instance, as per IMARC Group, sportswear market segment across the US is anticipated to exhibits a growth rate of 5.80% during the time period 2024 to 2032. In addition to this, the presence of major textile manufacturers, strong supply chain infrastructure, and rising consumer preference for lightweight, durable, and cost-effective materials are key factors supporting market expansion in North America.

Europe Polyethylene Terephthalate (PET) Fabric Market Analysis

The growing PET fabric adoption is driven by the demand for fabric composed of recycled PET bottles, which aids in minimizing pollution levels by lowering waste disposal. For instance, the EU has a set an aim for 2030 of a net reduction by 55 % in greenhouse gas emissions. The increasing awareness of environmental sustainability is promoting the use of synthetic materials that support circular economy initiatives. The demand for textiles derived from post-consumer plastics is growing as industries seek to reduce environmental impact. The focus on greenhouse gases reduction is encouraging the adoption of resource-efficient alternatives that align with emission control strategies. The emphasis on responsible consumption is driving investments in sustainable textile solutions, leading to higher adoption rates of PET fabric. The preference for innovative materials that contribute to waste minimization is increasing, influencing market dynamics. The rising demand for functional textiles that integrate eco-friendly attributes is reinforcing the growth of PET fabric in multiple applications. The shift towards reducing plastic waste and greenhouse gas emissions is accelerating industry-wide transitions to synthetic fibers made from recycled sources, enhancing long-term sustainability efforts.

Latin America Polyethylene Terephthalate (PET) Fabric Market Analysis

The growing PET fabric adoption is influenced by the increasing demand in household applications due to growing disposable income. According to reports, Latin America's total disposable income is expected to grow by nearly 60% from 2021 to 2040. The rising affordability of synthetic textiles is leading to higher consumption across domestic sectors. The preference for durable and cost-effective materials is increasing as consumers seek practical and long-lasting fabric options. The demand for versatile textiles that offer comfort and affordability is supporting the expansion of PET fabric in household applications. The rising focus on home furnishings and interior textiles is fueling the market for synthetic fibers. The shift towards functional and low-maintenance materials is encouraging the adoption of PET fabric across various household uses.

Middle East and Africa Polyethylene Terephthalate (PET) Fabric Market Analysis

The growing PET fabric adoption is driven by the increasing demand in the textile industry sector. According to reports, in 2022, the UAE textile market was valued at more than USD10 Billion and is now expected to expand by more than 5% a year over the medium term. The expanding manufacturing base is fueling the need for cost-effective and high-performance synthetic fibers. The demand for durable and lightweight textiles is increasing as industries seek reliable alternatives for various applications. The rising focus on industrial textiles and performance-driven fabric solutions is supporting the adoption of PET fabric. The growth in fashion and apparel production is further driving the preference for versatile and resource-efficient synthetic fibers. The emphasis on fabric innovations is promoting the use of PET-based materials across multiple textile industry segments.

Competitive Landscape:

The market is intensely competitive, with key players focusing on innovation, sustainability, and capacity expansion to strengthen their market presence. Leading manufacturers invest in advanced recycling technologies to enhance the production of recycled PET fabrics, meeting the rising demand for eco-friendly textiles. Various firms are also augmenting their product lines to address the varying applications, involving apparel, automotive interiors, and industrial textiles. Besides this, strategic partnerships, mergers, and acquisitions are common strategies to gain a competitive edge. For instance, as per industry reports, in May 2024, Loop Industries, Inc. entered into a joint venture with Ester Industries Ltd. to develop a production plant in India. The 50/50 joint venture combines Loop’s advanced recycled PET and polyester fiber technology with Ester’s acumen in polymer production, utilizing both companies' strengths for enhanced manufacturing capabilities. In addition to this, Asia Pacific-based manufacturers dominate the market due to cost-effective production, while North American and European players emphasize high-performance and sustainable PET fabric solutions.

The report provides a comprehensive analysis of the competitive landscape in the polyethylene terephthalate (PET) fabric market with detailed profiles of all major companies, including:

- Alpek S.A.B.

- Toray Industries, Inc.

- Eastman Chemical Company

- William Barnet & Son, LLC.

- Reliance Industries Limited

- Indorama Ventures Public Company Limited

- Märkische Faser GmbH

- Sun Fiber LLC.

- Zhejiang Hengyi Group Co., Ltd.

Latest News and Developments:

- February 2025: IFC and Ghana’s Mohinani Group are partnering to establish PET recycling plants in Ghana and Nigeria, producing 15,000 tons of recycled PET annually. The initiative will create over 4,000 jobs and save USD 21 Million in imports per country. IFC is providing a USD 37 Million loan and advisory services to enhance recycling efficiency. The project aims to reduce plastic waste, emissions, and reliance on virgin PET.

- November 2024: Kvadrat has launched Ame, its first recycled polyester textile made from waste fabric instead of PET bottles. Designed with Teruhiro Yanagihara, Ame represents a shift toward "textile-to-textile" recycling. Unlike traditional downcycling, which degrades material quality, this approach helps close the textile lifecycle loop. Kvadrat aims to redefine polyester recycling beyond PET-based methods.

- November 2024: Revalyu Resources has launched its second PET recycling plant in Nashik, India, boosting its capacity to recycle over 20 million PET bottles daily into 160 tons of high-quality PET chips. The company’s glycolysis-based technology reduces water use by 75% and energy consumption by 91% compared to conventional methods. A third plant, set to be completed by Q3 2025, will add 120 tons of daily capacity. This expansion aligns with growing sustainability demands across industries like packaging, textiles, and automotive.

- June 2024: Arkema has introduced eco-friendly powder coating resins with up to 40% post-consumer recycled PET, reducing Product Carbon Footprint by 20%. This innovation supports circular, high-performance solutions and sustainable lifestyles. The solvent-free, low-waste technology replaces fossil-based raw materials with recycled PET from end-of-life packaging. Arkema, a specialty materials leader, achieved approximately USD 10 Billion in 2023 sales across 55 countries.

- July 2024: BASF unveiled Haptex® 4.0, a revolutionizing polyurethane solution for producing 100% recyclable synthetic leather with PET fabric. This breakthrough eliminates the need for layer separation, enabling seamless recycling through a new formulation and technical pathway. Addressing industry challenges, Haptex 4.0 enhances fabric sustainability while ensuring a waste-free manufacturing process. BASF aims to drive green transformation by promoting high-performance, recyclable fabric materials.

Polyethylene Terephthalate (PET) Fabric Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Virgin PET, Recycled PET, Blended PET |

| Fabric Types Covered | Woven, Non-Woven, Knitted |

| Forms Covered | Staple, Filament, Fiberfill, Tow |

| Applications Covered | Apparel, Household, Industrial, Carpet and Rugs, and Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, Italy, Spain, Poland, United Kingdom, China, Japan, India, South Korea, Australia, Turkey, Saudi Arabia, United Arab Emirates, Israel, Brazil, Mexico |

| Companies Covered | Alpek S.A.B., Toray Industries, Inc., Eastman Chemical Company, William Barnet & Son, LLC., Reliance Industries Limited, Indorama Ventures Public Company Limited, Märkische Faser GmbH, Sun Fiber LLC., Zhejiang Hengyi Group Co., Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the polyethylene terephthalate (PET) fabric market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global polyethylene terephthalate (PET) fabric market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the polyethylene terephthalate (PET) fabric industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Polyethylene Terephthalate Fabric Market Report

The polyethylene terephthalate (PET) fabric market was valued at USD 38.5 Billion in 2025.

IMARC estimates the polyethylene terephthalate (PET) fabric market to reach USD 60.2 Billion by 2034, exhibiting a CAGR of 4.94% during 2026-2034.

The market is driven by rising demand for durable, lightweight, and moisture-resistant textiles across apparel, automotive, and home furnishing industries. Advancements in recycling technologies, increasing sustainability initiatives, expanding technical textile applications, rapid urbanization, and evolving fashion trends further contribute to market growth.

Asia Pacific currently dominates the polyethylene terephthalate (PET) fabric market, accounting for a share exceeding 43.5%. This dominance is fueled by its large textile manufacturing base, high demand from apparel and automotive sectors, cost-effective production, and strong presence of key industry players.

Some of the major players in the polyethylene terephthalate (PET) fabric market include Alpek S.A.B., Toray Industries, Inc., Eastman Chemical Company, William Barnet & Son, LLC., Reliance Industries Limited, Indorama Ventures Public Company Limited, Märkische Faser GmbH, Sun Fiber LLC., Zhejiang Hengyi Group Co., Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)