Polyols Market Size, Share, Trends and Forecast by Type, Application, Industry, and Region, 2026-2034

Global Polyols Market Size, Share, Trends & Forecast (2026-2034)

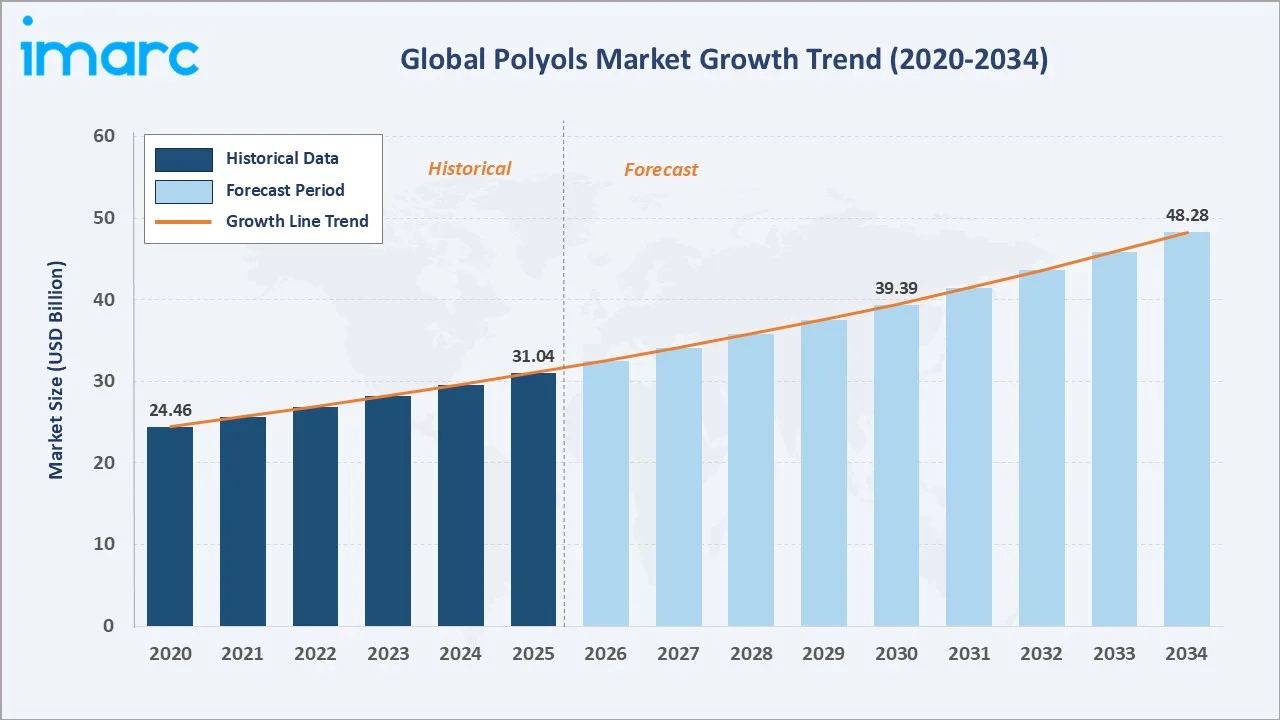

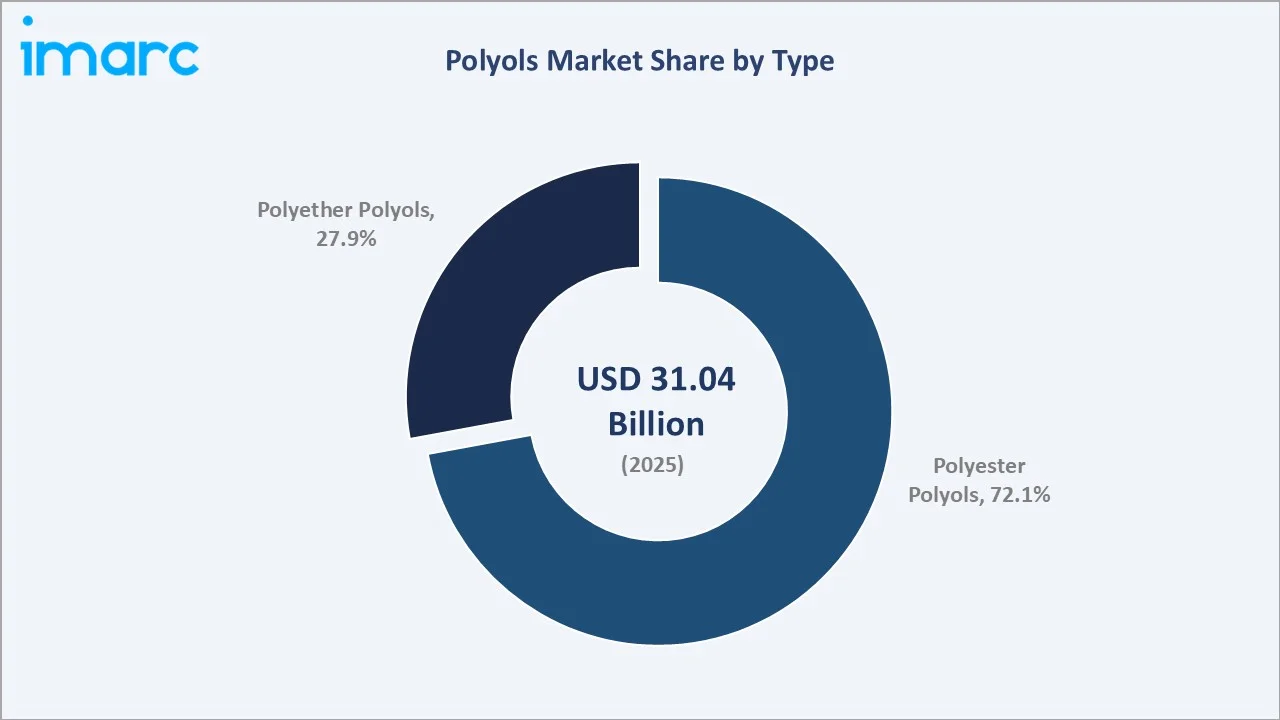

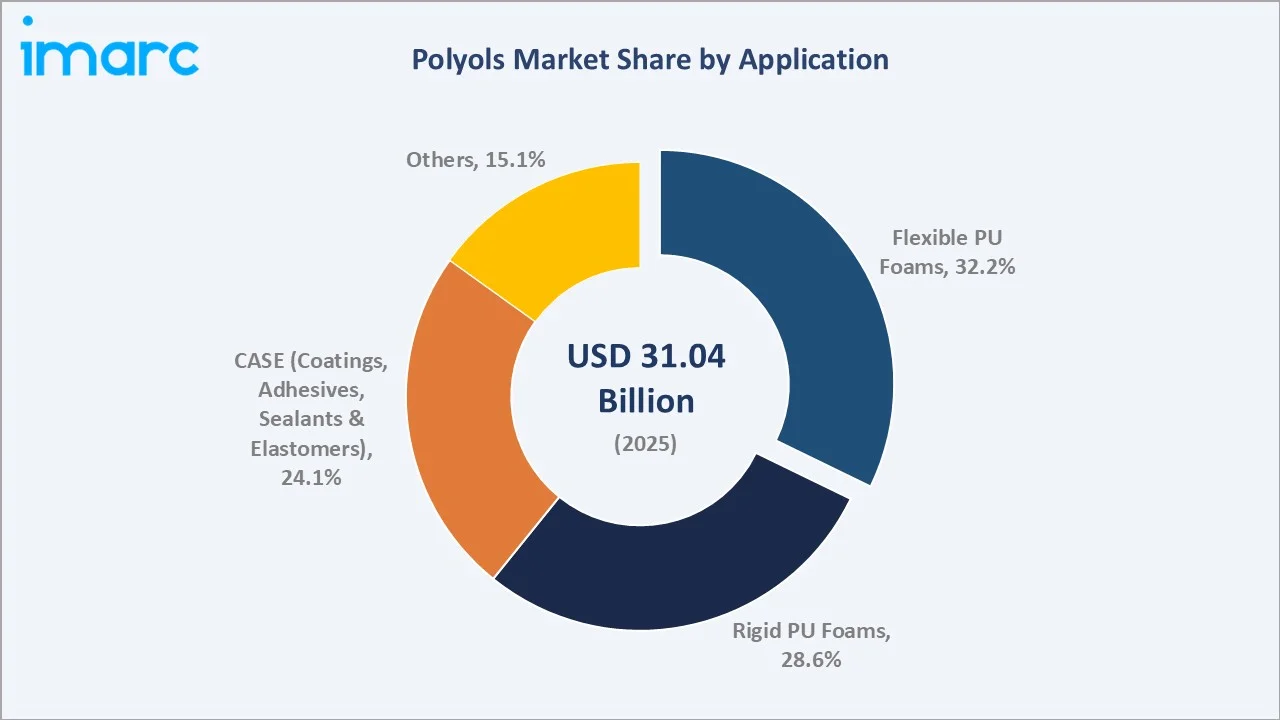

The global polyols market size was valued at USD 31.04 Billion in 2025 and is projected to reach USD 48.28 Billion by 2034, exhibiting a CAGR of 4.88% during the forecast period 2026-2034. Rising polyurethane demand across construction insulation, furniture and bedding, automotive interiors, and CASE (coatings, adhesives, sealants & elastomers) applications, alongside the IEA reporting buildings accounted for 30% of global final energy use in 2024, is driving polyols market growth. Flexible polyurethane foams lead at 32.2% in 2025, while polyester polyols dominate the type segment at 72.1%. Asia Pacific accounts for 44.3% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 31.04 Billion |

|

Forecast Market Size (2034) |

USD 48.28 Billion |

|

CAGR (2026-2034) |

4.88% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (44.3% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~5.8%) |

|

Leading Application |

Flexible Polyurethane Foams (32.2%, 2025) |

|

Leading Type |

Polyester Polyols (72.1%, 2025) |

The global polyols market growth trajectory from 2020 through 2034 contrasts a consistent historical expansion base against a sustained forecast curve powered by construction insulation mandates, circular polyol commercialization, and steady polyurethane demand across furniture, automotive, and appliance end-markets.

To get more information on this market, Request Sample

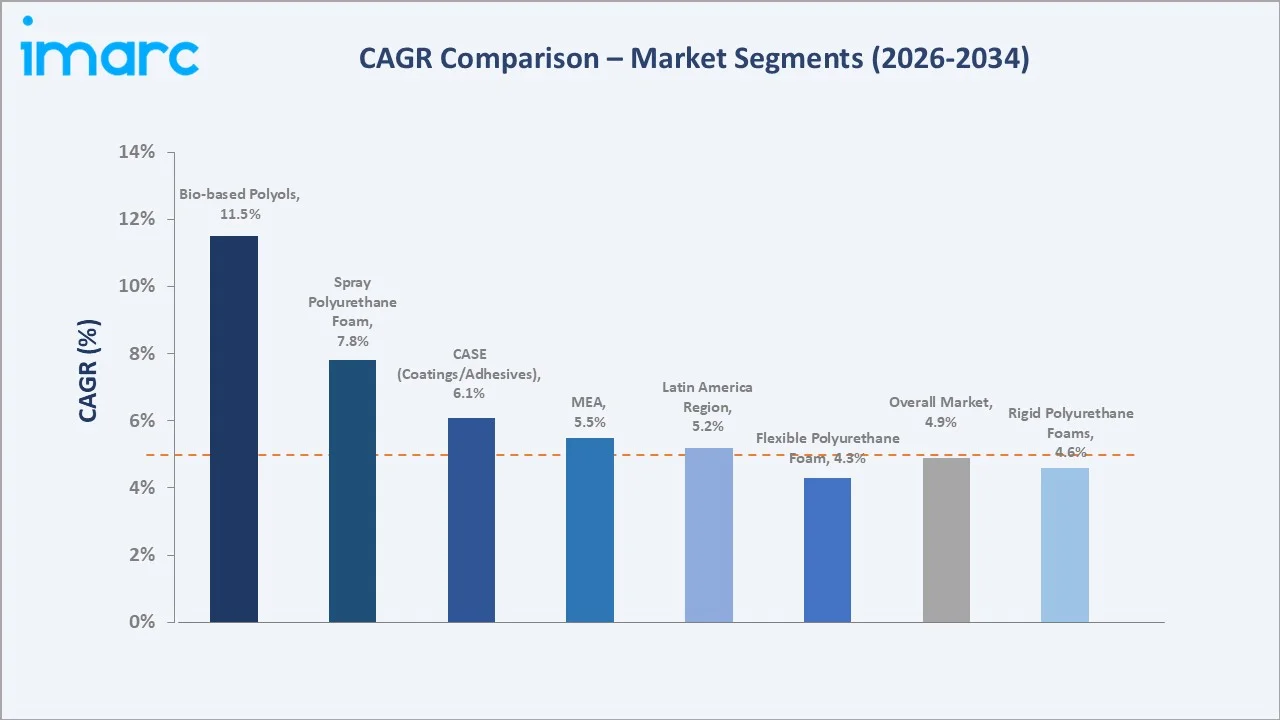

Segment-level CAGR comparisons highlight bio-based polyols and spray polyurethane foam as the two fastest-growing sub-categories within the global polyols industry analysis through 2034, sharply outpacing the overall market trajectory.

Executive Summary

The global polyols market is entering a structured expansion phase driven by polyurethane demand across construction, furniture, automotive, and CASE (coatings, adhesives, sealants & elastomers) applications. Valued at USD 31.04 Billion in 2025, the market is forecast to reach USD 48.28 Billion by 2034 at a CAGR of 4.88%. The International Energy Agency reported that buildings accounted for 32% of global final energy use in 2024, intensifying rigid polyurethane foam insulation demand across Europe and North America. Alongside this, the mattress industry exceeded USD 40 billion in 2024, sustaining flexible polyol volumes.

Flexible polyurethane foams command the dominant application share at 32.2% in 2025, driven by bedding, upholstered furniture, and automotive seating. Rigid polyurethane foams at 28.6% are the second-largest application, fuelled by insulation board, spray foam, and cold chain appliances. CASE (coatings, adhesives, sealants & elastomers) applications hold 24.1% share in 2025, supported by automotive refinish coatings, wind blade adhesives, and industrial flooring.

Asia Pacific dominates with a 44.3% global revenue share in 2025, led by China's polyurethane manufacturing scale, with the country accounting for more than 40% of global polyurethane consumption in 2024, alongside India's growing construction pipeline and Vietnam's footwear exports. Europe holds 23.6% and North America 18.9% in 2025, both shaped by building insulation regulations and bio-based polyol commercialization by Covestro, BASF, and Dow.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Flexible Polyurethane Foams - 32.2% share (2025) |

|

Leading Type |

Polyester Polyols - 72.1% share (2025) |

|

Leading Region |

Asia Pacific - 44.3% revenue share (2025) |

|

Second Region |

Europe - 23.6% revenue share (2025) |

|

Top Companies |

BASF, Covestro AG, Dow, Huntsman, Wanhua |

Key Analytical Observations Supporting the Above Data:

- Flexible polyurethane foam's 32.2% dominance in 2025 reflects sustained bedding, upholstered furniture, and automotive seating demand, underpinned by a global mattress market exceeding USD 40 billion in 2024.

- Polyester polyols lead the type segment at 72.1% in 2025, driven by CASE (coatings, adhesives, sealants & elastomers) end-uses, recycled PET-based polyester polyol capacity additions, and expanding use in high-performance coatings and adhesives across Europe and North America.

- Asia Pacific's 44.3% global dominance in 2025 reflects China's dual role as the world's largest polyurethane consumer and one of the largest producers, combined with India's furniture and construction-led growth.

Global Polyols Market Overview

Polyols are hydroxyl-functional compounds, primarily polyether and polyester types, that serve as the core reactive component in polyurethane chemistry. They react with isocyanates such as MDI and TDI to form flexible foams, rigid foams, coatings, adhesives, sealants, and elastomers (CASE) used across construction, automotive, furniture, footwear, appliances, and packaging.

Applications span mattress and upholstery foams, insulation panels, spray foam, automotive seating, footwear soles, wind blade adhesives, industrial flooring, and high-performance coatings.

Macroeconomic enablers include global construction spend and sustained bedding-furniture consumption from urbanization across the Asia Pacific. Circular chemistry, bio-based feedstocks, and CO2-derived polyols are reshaping sustainability economics.

Market Dynamics

To evaluate market opportunities, Request Sample

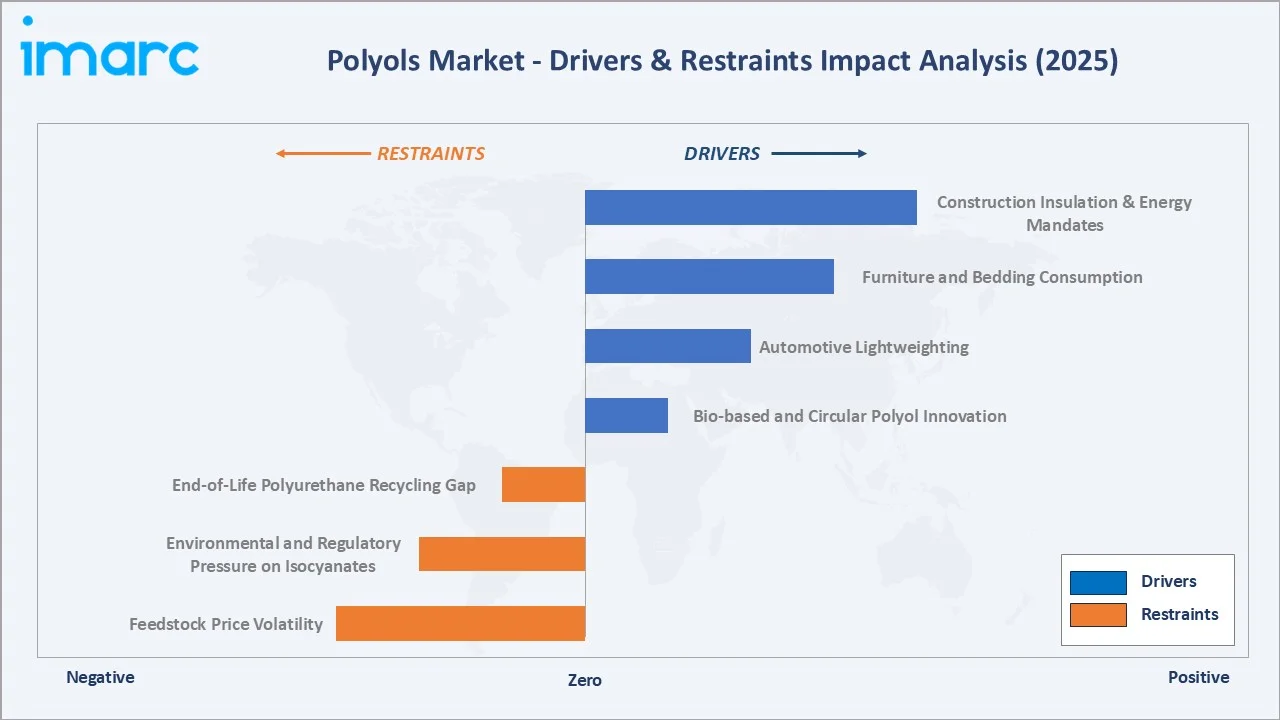

Market Drivers

- Construction Insulation and Energy Efficiency Mandates: Rigid polyurethane foams are central to building insulation upgrades. The International Energy Agency reported that buildings account for 30% of global energy demand in 2024, intensifying retrofit activity across the EU, UK, and North America, supported by the EU EPBD revision enacted in 2024.

- Furniture and Bedding Consumption: Flexible polyurethane foams underpin mattress and upholstery production. The global mattress industry is expanding, with e-commerce mattress brands scaling demand for high-resilience and viscoelastic foam polyols.

- Automotive Lightweighting and Interior Comfort: Polyurethane foams and CASE systems support lightweight seating, headliners, acoustic insulation, and NVH parts. With over 92 million vehicles produced globally in 2024, automotive OEMs remain a structural volume driver.

- Bio-based and Circular Polyol Innovation: Covestro's cardyon CO2-based polyols, Dow's RENUVA chemical recycling platform, and BASF's ChemCycling are expanding the sustainable polyol pool. Recycled PET-based polyester polyols are scaling rapidly across CASE applications in Europe.

Market Restraints

- Feedstock Price Volatility: Propylene oxide and adipic acid prices track crude oil and natural gas swings, creating margin pressure. Propylene oxide prices fluctuated by more than 28% across 2023-2024 per ICIS benchmarks, directly impacting polyol producer margins.

- Environmental and Regulatory Pressure on Isocyanates: REACH, TSCA, and OSHA restrictions on TDI and MDI exposure raise compliance costs for downstream polyurethane manufacturers, indirectly capping polyol demand growth in sensitive applications.

- End-of-Life Polyurethane Recycling Gap: Less than 30% of post-consumer polyurethane foam is currently recycled, creating brand reputation risk for downstream OEMs and regulatory exposure for polyol producers through 2034.

Market Opportunities

- CO2-based Polyol Commercialization: Covestro's cardyon polyols use up to 20% CO2 as a raw material, offering measurable carbon footprint reduction. The platform is scaling through partnerships with bedding and automotive customers through 2028.

- Bio-based Polyester Polyols from Recycled PET: Post-consumer PET is being converted into polyester polyols for CASE applications, supporting circular economy commitments from adhesive and coating customers across Europe and North America.

- Spray Polyurethane Foam Insulation Expansion: Spray polyurethane foam for commercial and residential insulation is growing at roughly 7-8% CAGR globally, offering a premium rigid polyol channel through 2034.

Market Challenges

- Scope 3 Emissions Accountability: Automotive, construction, and bedding customers are tightening supplier sustainability reporting, requiring polyol producers to document feedstock origin, carbon intensity, and renewable content at the SKU level.

- Overcapacity Risk in Polyether Polyols: Chinese propylene oxide and polyether polyol capacity additions, with Wanhua and Sanjiang ramping up through 2025-2026, risk regional oversupply that pressures global pricing benchmarks.

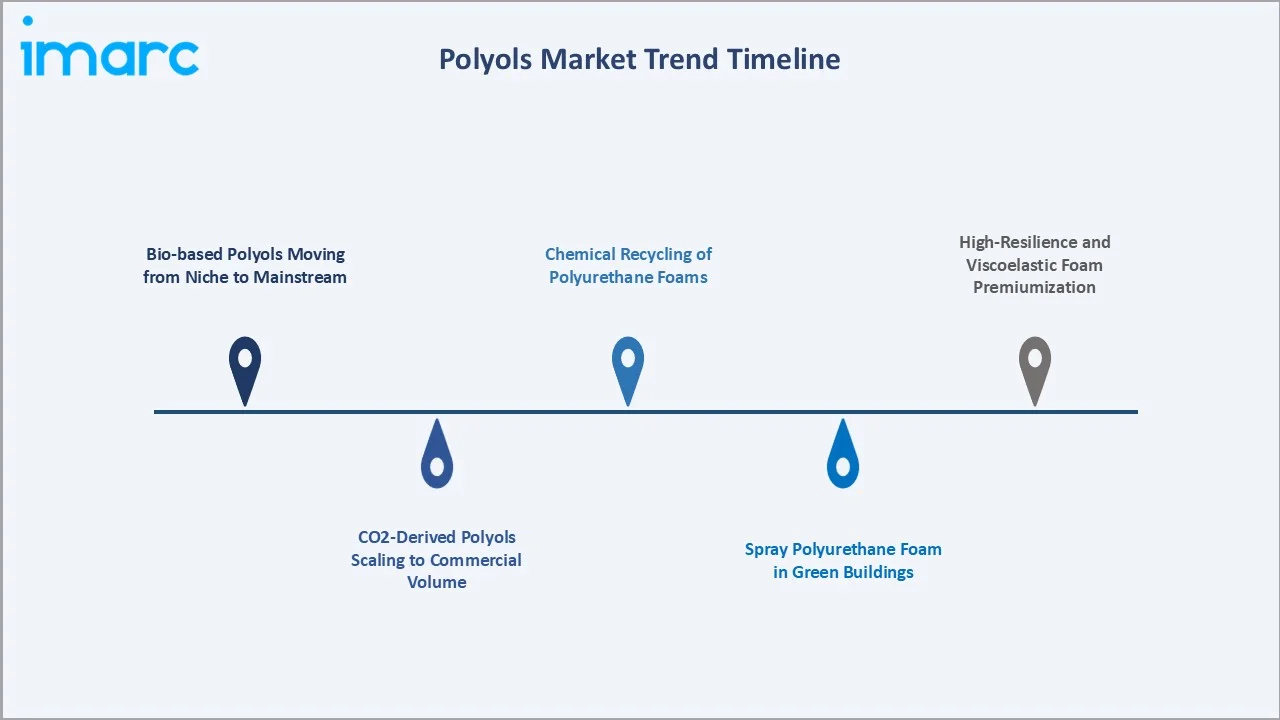

Emerging Market Trends

1. Bio-based Polyols Moving from Niche to Mainstream

Natural oil polyols derived from soybean, castor, and palm oils are gaining traction in flexible foam and CASE applications. Cargill's BiOH polyols and Emery Oleochemicals' EMEROX platforms are now integrated into major bedding and automotive OEM supply chains, with capacity expansions exceeding 500 kilotons announced through 2028.

2. CO2-Derived Polyols Scaling to Commercial Volume

Covestro's cardyon platform and Econic Technologies' licensed catalysts are commercializing CO2-containing polyether polyols. Carbon-embedded chemistry is expected to address Scope 3 reduction requirements from construction, bedding, and automotive buyers through 2030.

3. Chemical Recycling of Polyurethane Foams

BASF's ChemCycling, Dow's RENUVA program, and H&S Anlagentechnik's glycolysis units are converting post-consumer polyurethane mattresses and construction foam into recycled polyols, targeting over 300 kilotons of recycled polyol capacity by 2028.

4. Spray Polyurethane Foam in Green Buildings

The demand for LEED and BREEAM building certification is lifting spray polyurethane foam insulation. US spray foam demand grew by nearly 8% in 2024, supporting premium rigid polyol volumes with higher functionality and closed-cell performance.

5. High-Resilience and Viscoelastic Foam Premiumization

Bedding and seating are shifting toward high-resilience and memory foam formulations, supporting polyether polyols with narrow molecular weight distribution and higher hydroxyl numbers for improved comfort engineering and premium consumer positioning.

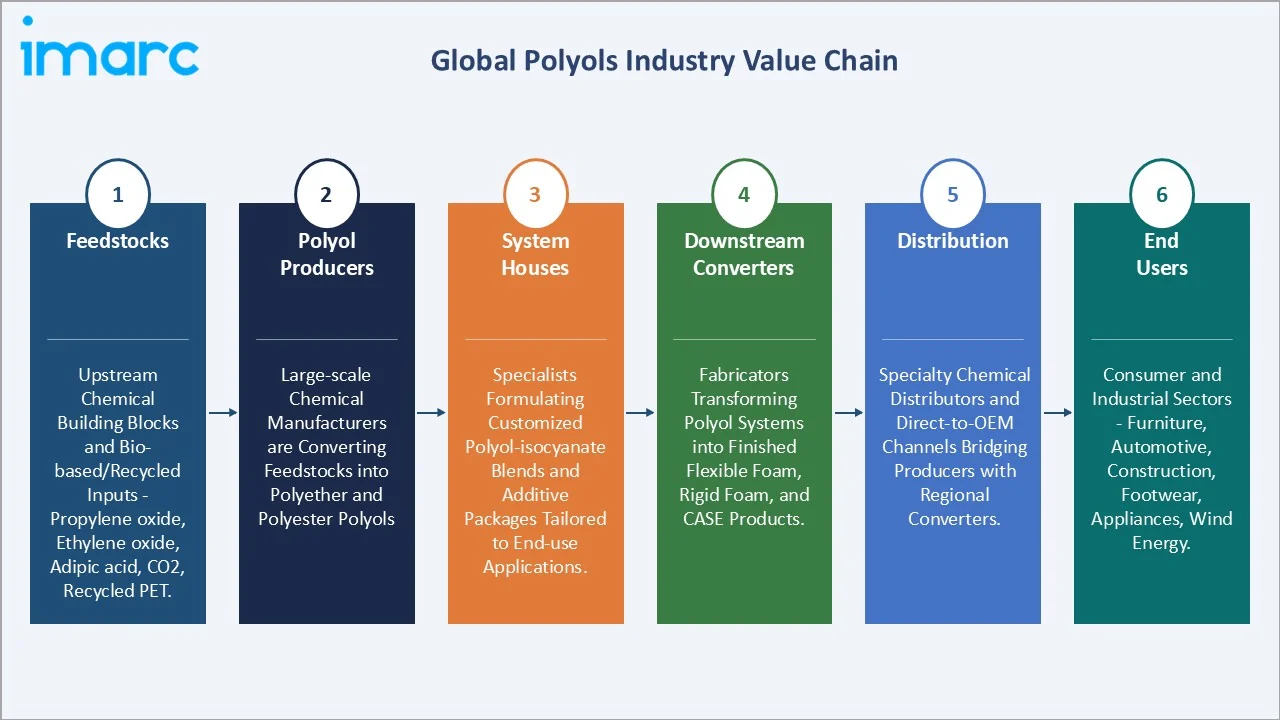

Industry Value Chain Analysis

The polyols value chain spans six integrated stages from petrochemical feedstock through end-consumer polyurethane product delivery. Each stage presents distinct competitive dynamics, margin profiles, and sustainability-investment requirements.

|

Stage |

Key Players / Examples |

|

Feedstocks |

Upstream chemical building blocks and bio-based/recycled inputs that form the raw foundation for polyol synthesis. |

|

Polyol Producers |

Large-scale chemical manufacturers that convert feedstocks into polyether and polyester polyols through proprietary catalytic processes. |

|

System Houses |

Specialists who formulate customized polyol–isocyanate blends and additive packages tailored to specific application requirements. |

|

Downstream Converters |

Fabricators that transform polyol systems into finished flexible foam, rigid foam, and CASE (coatings, adhesives, sealants, elastomers) products. |

|

Distribution |

Specialty chemical distributors and direct-to-OEM channels that bridge producers with fragmented regional and mid-volume end-market demand. |

|

End Users |

Consumer and industrial sectors that embed polyol-derived components into finished goods across mobility, comfort, construction, and packaging applications. |

Polyol producers occupy the highest strategic value position in the polyols value chain, integrating feedstock assets, proprietary catalyst technology, and scale economics. System houses capture formulation-IP margin, while converters operate at tighter spreads aligned with end-market cyclicality. Sustainability leadership is shifting value upstream toward producers with circular platforms.

Technology Landscape in the Polyols Industry

Bio-based and Recycled Feedstock Platforms

Bio-based polyols from soy, castor, palm, and recycled PET are transitioning from sampling to commercial SKUs. Covestro launched its mass-balanced MDI and polyol range in 2024 with ISCC PLUS certification across European assets, enabling drop-in circular polyols for automotive and bedding customers.

CO2 Utilization in Polyether Polyols

CO2-based polyether polyols embed captured carbon into the polymer backbone. Covestro's Dormagen facility produces cardyon with up to 20% CO2 content, commercialized across mattresses, sports flooring, and shoe soles through 2025-2028.

Chemical Recycling via Glycolysis and Acidolysis

Glycolysis of flexible polyurethane scrap regenerates polyols that can be blended up to 30% into new formulations. H&S Anlagentechnik and Dow's RENUVA have commissioned industrial units supplying recycled polyols to mattress OEMs across Europe.

Automation and Digital Process Control

Advanced process control, real-time hydroxyl number measurement, and inline viscosity monitoring are reducing batch variability. Digital twins at BASF and Covestro polyether units are lifting asset utilization above 92% in 2024-2025, improving feedstock yields.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Polyether Polyols | 27.9% | 2025 |

| Application | Flexible Polyurethane Foams | 32.2% | 2025 |

| Industry | Packaging | 🔒 | 2025 |

| Region | Asia Pacific | 44.3% | 2025 |

By Type

Polyester polyols command a 72.1% majority share in 2025, supported by wide use in CASE (coatings, adhesives, sealants & elastomers) applications, elastomers, and high-performance coatings. Bio-based polyester polyol capacity from recycled PET and succinic acid routes is expanding rapidly across North America and Europe, led by Resinate Materials Group and Stepan Company.

To evaluate market opportunities, Request Sample

Polyether polyols hold 27.9% in 2025, anchored in flexible foam for bedding, furniture, and automotive seating, together with rigid foam insulation for construction and appliances. Chinese polyether polyol capacity expansions by Wanhua, Sanjiang, and Sadara through 2026 are reshaping regional supply balances.

By Application

Flexible polyurethane foams dominate application share at 32.2% in 2025, powered by bedding, upholstered furniture, and automotive seating demand. The flexible foam segment benefits from the rise in premium mattresses and high-resilience foam formulations, alongside commercial vehicle seating volumes across the Asia Pacific.

Rigid polyurethane foams at 28.6% in 2025 are driven by insulation board, spray foam, and cold chain appliance segments across North America, Europe, and the Asia Pacific, supported by the EU Energy Performance of Buildings Directive (EPBD) revision and the US Greener Homes programs. CASE (coatings, adhesives, sealants & elastomers) applications account for 24.1% in 2025, while other applications (binders, dispersions, specialty elastomers) account for 15.1%.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

44.3% |

China PU scale, India construction pipeline, Vietnam footwear, ASEAN appliance demand |

|

Europe |

23.6% |

EPBD insulation mandates, bio-based polyol leadership, and CASE wind blade demand |

|

North America |

18.9% |

Spray foam insulation, mattress e-commerce, RENUVA recycling, Greener Homes program. |

|

Middle East & Africa |

6.8% |

GCC construction pipelines, cold chain build-out, Saudi NEOM housing |

|

Latin America |

6.4% |

Brazil and Mexico's auto production, furniture exports, and appliance manufacturing |

Asia Pacific commands a 44.3% global revenue share in 2025, the most dominant regional position of any global polyols market. China is the single most important national market, accounting for more than 40% of global polyurethane consumption in 2024, backed by its furniture export base of over USD 70 Billion and rapid cold-chain appliance growth. India is emerging as a high-growth sub-region, with the Ministry of Housing and Urban Affairs targeting three crore new dwellings under PMAY through 2029.

Europe holds 23.6% in 2025, anchored by the EU EPBD revision, CASE demand from wind energy, and leadership in bio-based and CO2-based polyol commercialization by Covestro and BASF. North America's 18.9% share in 2025 is supported by spray polyurethane foam growth, mattress e-commerce expansion, and Canadian insulation retrofit incentives under the Greener Homes program.

Middle East & Africa holds 6.8% in 2025, supported by GCC construction pipelines and Saudi Vision 2030 smart city development. Latin America holds 6.4%, anchored by Brazilian and Mexican automotive production and furniture export growth.

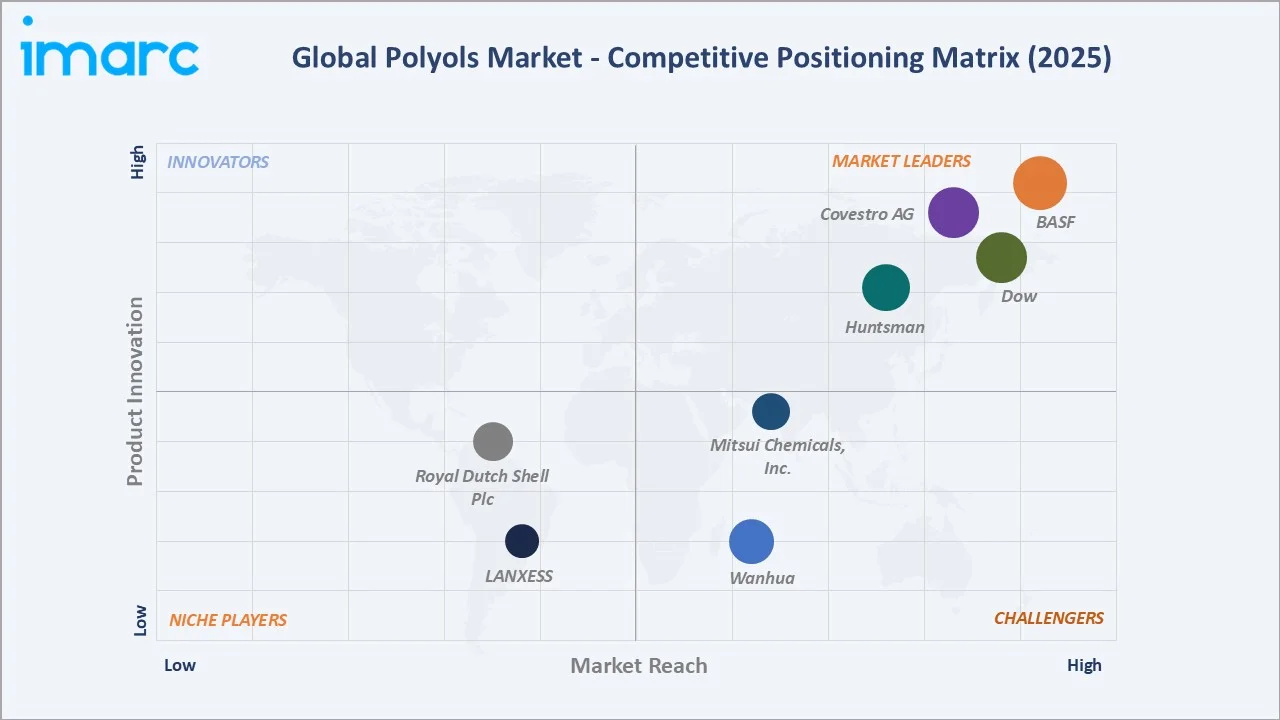

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

BASF |

Pluracol, Lupraphen |

Leader |

Integrated PO, Verbund, bio-based polyols, global scale |

|

Covestro AG |

Desmophen |

Leader |

CO2-based polyols, bio-based portfolio, MDI integration |

|

Dow |

VORANOL |

Leader |

Flexible foam polyols, chemical recycling leadership |

|

Huntsman |

JEFFOL |

Leader |

Rigid foam, CASE, spray polyurethane foam systems |

|

Wanhua |

Wanol |

Challenger |

Integrated MDI-PO, Chinese cost leadership |

|

Royal Dutch Shell Plc |

CARADOL |

Emerging |

Polyether polyols, global feedstock base |

|

Mitsui Chemicals, Inc. |

ACTCOL |

Challenger |

Japanese premium PU, elastomers, R&D depth |

|

LANXESS |

Adiprene |

Emerging |

High-performance elastomers, niche polyester |

The global polyols competitive landscape is characterized by a small number of global chemical majors commanding scale, feedstock integration, and deep OEM relationships, alongside regional Chinese challengers scaling capacity aggressively, and specialty emerging players differentiating on bio-based and circular chemistry.

Key Company Profiles

BASF

BASF is a chemical company and a global polyols producer, with integrated propylene oxide, polyether, and polyester polyol capacity across Germany, the US, China, and Malaysia.

- Product & Platform Portfolio: Lupranol polyether polyols, Lupraphen polyester polyols, Lupranate isocyanates, Elastopan shoe soling systems, Elastollan TPU.

- Recent Developments: In February 2025, BASF is offering biomass-balanced (BMB)[1] and Ccycled grades of its plasticizer portfolio from production sites in Pasadena, Texas, and Cornwall, Ontario, to customers. The sites and mass-balanced products have been certified according to the International Sustainability and Carbon Certification (ISCC) PLUS scheme.

- Strategic Focus: BASF's polyols strategy centers on integrated Verbund economics, circular-economy polyol solutions, and localized capacity in China and Southeast Asia to capture polyurethane demand growth across automotive, construction, and furniture end-markets.

Covestro AG

Covestro AG is a leader in high-performance polymers and one of the world's top polyether polyol suppliers, with flagship cardyon CO2-based polyols commercialized from its Dormagen facility and strong MDI-polyol integration.

- Product & Platform Portfolio: Desmophen polyester and polyether polyols, cardyon CO2-based polyols, Baydur composites, Baytec elastomer systems.

- Recent Developments: In May 2025, Covestro secured the ISCC (International Sustainability and Carbon Certification) PLUS certification for its site in South Charleston, West Virginia, USA.

- Strategic Focus: Covestro prioritizes circular economy leadership through cardyon, bio-attributed feedstocks, and chemical recycling, alongside continued MDI-polyol integration advantages and premium flexible foam growth in the Asia Pacific.

Dow

Dow is a global polyether polyols producer with integrated propylene oxide assets and the RENUVA chemical recycling platform addressing end-of-life flexible polyurethane foam.

- Product & Platform Portfolio: VORANOL polyether polyols, VORASURF silicone surfactants, SPECFLEX specialty polyols, RENUVA recycled polyols.

- Recent Developments: In July 2020, Dow recruited another partner to its Renuva mattress recycling programme. The company announced that it will collaborate with Eco-mobilier, the French mattress and furniture EPR (Extended Producer Responsibility) organisation, on the collection and supply of post-consumer polyurethane foam for the programme.

- Strategic Focus: Dow's strategy targets circular polyurethane leadership via RENUVA, premium flexible foam differentiation through SPECFLEX, and North American construction insulation growth via spray foam and rigid polyol volumes.

Market Concentration Analysis

The global polyols industry exhibits moderate-to-high concentration, with the top five players (BASF, Covestro, Dow, Huntsman, and Wanhua) collectively accounting for approximately 45-52% of global polyol revenue in 2025. The remaining share is distributed across Shell, Mitsui, LANXESS, Repsol, Stepan, and a fragmented tier of regional producers.

The polyols market is experiencing a bifurcated structural dynamic. In polyether polyols, consolidation is pronounced, as integrated propylene oxide access and scale economics define competitive position. Polyester polyols are more fragmented, with specialty and regional players competing on CASE formulation depth and bio-based credentials.

Chinese capacity additions by Wanhua, Sanjiang, and Hongbaoli are gradually shifting the supply curve, exerting pricing pressure on global polyether polyol benchmarks through 2026-2028 while expanding regional self-sufficiency and creating competitive pressure on international producers.

Investment & Growth Opportunities

Fastest-Growing Segments

Bio-based and CO2-based polyols are the fastest-growing sub-segments, expanding at double-digit CAGR through 2034. Spray polyurethane foam is the fastest-growing rigid foam channel at approximately 7-8% CAGR, driven by North American and European insulation retrofit programs. CASE applications in wind energy adhesives and industrial flooring are expanding at a 6-7% CAGR through 2034.

Emerging Market Expansion

India, Vietnam, and Indonesia are the highest-potential polyol growth markets. India's polyurethane consumption is growing at over 8% annually, supported by furniture, cold-chain, and construction demand. Vietnam is becoming a regional footwear polyurethane hub, while Indonesia is expanding PU appliance and construction applications.

Venture & Strategic Investment Trends

Strategic investment is concentrated in circular chemistry. Covestro, Dow, and BASF have each committed over USD 100 million toward chemical recycling and CO2-based polyol capacity through 2028. Private capital is targeting recycled PET-based polyester polyol producers such as Resinate Materials Group and bio-based innovators, including Cargill-led ventures.

Future Market Outlook (2026-2034)

The global polyols market forecast projects steady value expansion from USD 31.04 Billion in 2025 to USD 48.28 Billion by 2034 at a CAGR of 4.88%, underpinned by construction insulation demand, polyurethane furniture and bedding volumes, automotive interior growth, and the structural shift toward circular and bio-based polyol chemistry across premium end-markets through the forecast period.

Three transitions are most likely to reshape the polyols market through 2034. Circular polyols (recycled and CO2-based) are expected to account for 10-15% of global polyol demand by 2034, driven by Scope 3 commitments from automotive, bedding, and appliance OEMs. Chinese capacity growth will continue to rebalance global supply-demand and compress polyether polyol spreads. Bio-based polyester polyols will scale from niche into mainstream CASE adoption.

By 2034, the global polyols industry is forecast to have transitioned from a volume-led petrochemical market to a differentiated chemistry market where sustainability credentials, recycled content, and regulatory compliance define premium pricing. Leadership will reward producers combining feedstock flexibility, circular platforms, and regional scale.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024-2025 with senior stakeholders across the polyols value chain, including polyol plant managers, system house formulators, polyurethane converter procurement leads, automotive and bedding OEM sustainability managers, and industry association technical committees. Primary insights validated market sizing, regional splits, and segment share estimates.

Secondary Research

Secondary sources include company annual reports from BASF, Covestro, Dow, Huntsman, Wanhua, Shell, and Mitsui; IEA buildings reports; ICIS and Platts price benchmarks; ISOPA publications; Polyurethane Manufacturers Association outlooks; and trade coverage across Urethanes Technology International and Chemical Week.

Forecasting Models

Market size and growth projections were derived using top-down and bottom-up forecasting models, incorporating GDP growth, construction expenditure, and historical evolution. Scenario analysis (base, optimistic, conservative) accounts for feedstock volatility, construction cycles, and bio-based adoption pace.

Polyols Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Polyether Polyols, Polyester Polyols |

| Applications Covered | Flexible Polyurethane Foams, Rigid Polyurethane Foams, CASE (Coatings, Adhesives, Sealants & Elastomers), Others |

| Industries Covered | Carpet Backing, Packaging, Furniture, Automotive, Building & Construction, Electronics, Footwear, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | BASF, Covestro AG, Dow, Huntsman, Wanhua, Royal Dutch Shell Plc, Mitsui Chemicals, Inc., LANXESS, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the polyols market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global polyols market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the polyols industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Polyols Market Report

The global polyols market was valued at USD 31.04 Billion in 2025, driven by polyurethane foam demand across furniture, bedding, construction insulation, and automotive interiors.

The polyols market is projected to reach USD 48.28 Billion by 2034, growing at a CAGR of 4.88% during 2026 to 2034, supported by insulation and bio-based adoption.

Flexible polyurethane foams lead with a 32.2% share in 2025, driven by bedding, upholstered furniture, and automotive seating demand across North America, Europe, and the Asia Pacific.

Polyester polyols lead with a 72.1% share in 2025, supported by CASE (coatings, adhesives, sealants & elastomers) applications, high-performance coatings, and expanding bio-based and recycled PET feedstock availability.

Asia Pacific leads with a 44.3% share in 2025, driven by China's polyurethane scale, India's construction expansion, and Vietnam's footwear polyol consumption growth.

Key drivers include construction insulation mandates, mattress and furniture demand, automotive interior volumes, spray foam adoption, and scaling bio-based and CO2-derived polyol platforms.

Bio-based and CO2-based polyols are the fastest-growing sub-segments, expanding at double-digit CAGR through 2034 as OEMs pursue Scope 3 emissions reductions.

Leading companies include BASF, Covestro AG, Dow, Huntsman, Wanhua, Royal Dutch Shell Plc, Mitsui Chemicals, Inc., and LANXESS.

Bio-based polyols are produced from renewable feedstocks, including soybean, castor, palm oil, glycerine, and recycled PET, offering a reduced carbon footprint versus conventional polyether polyols.

Chemical recycling via glycolysis and acidolysis, led by Dow RENUVA and BASF ChemCycling, is reintroducing recycled polyols into flexible foam, supporting circular economy goals.

CO2 is embedded into polyether polyol backbones via Covestro cardyon, reducing fossil feedstock content by up to 20%, commercialized across mattresses, sports flooring, and shoe soles.

Rigid polyurethane foam insulation, spray foam, and CASE (coatings, adhesives, sealants & elastomers) coatings serve construction. Building energy mandates across the EU, the US, and China are lifting rigid polyol demand through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)