Power Quality Equipment Market Size, Share, Trends and Forecast by Equipment, Phase, End User, and Region, 2026-2034

Power Quality Equipment Market Size, Share, Trends & Forecast (2026-2034)

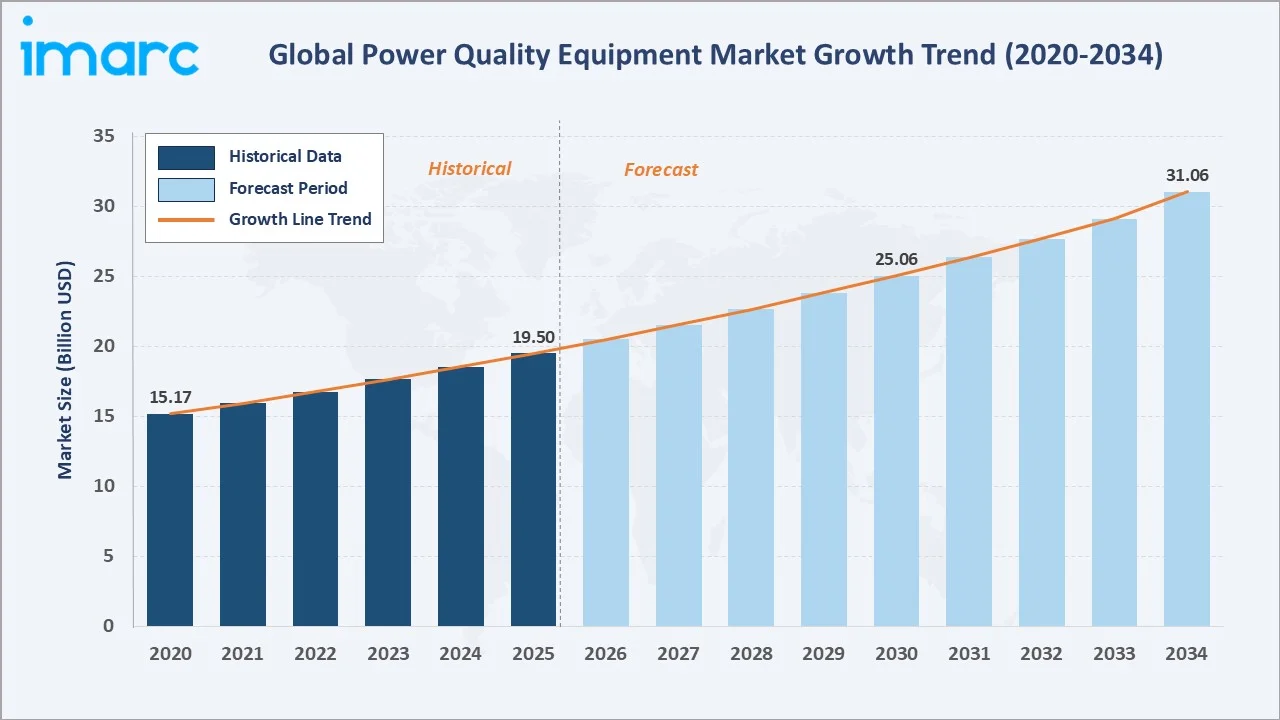

The global power quality equipment market reached USD 19.50 Billion in 2025 and is projected to reach USD 31.06 Billion by 2034, growing at a CAGR of 5.15% during 2026-2034. The market is driven by rising industrial automation, renewable energy integration, expanding data center infrastructure, and increasing demand for uninterrupted power supply.

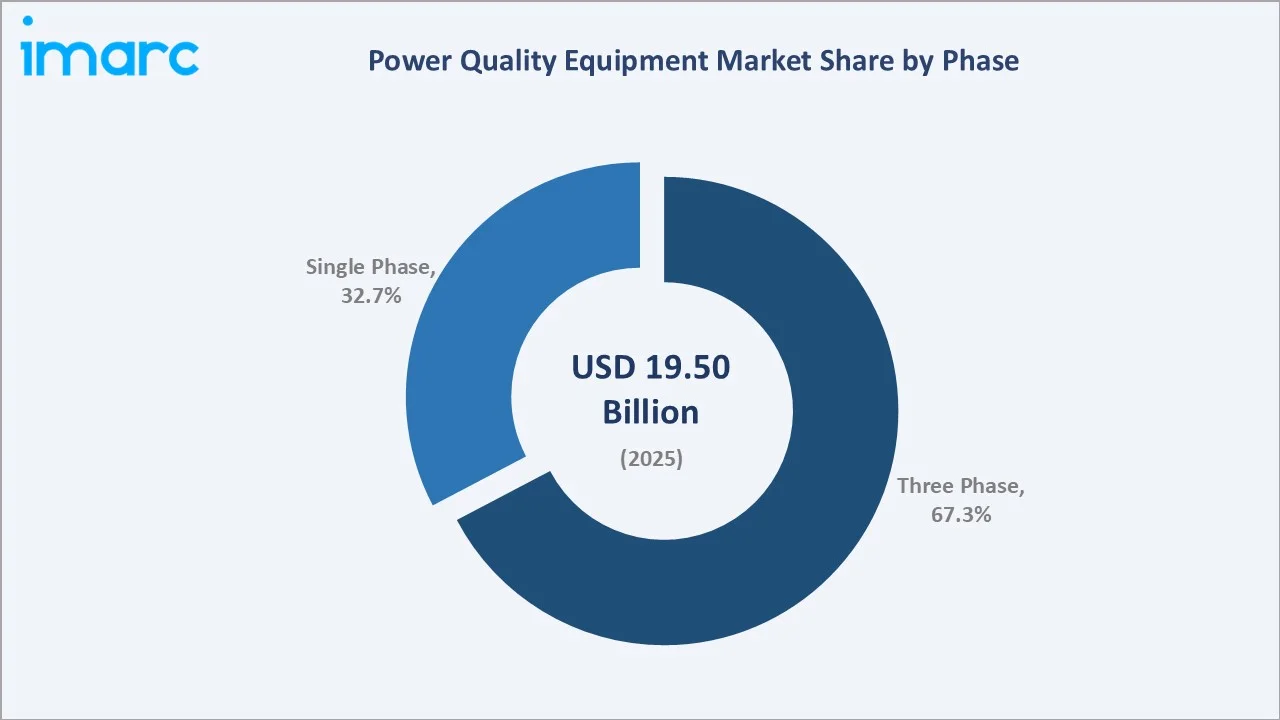

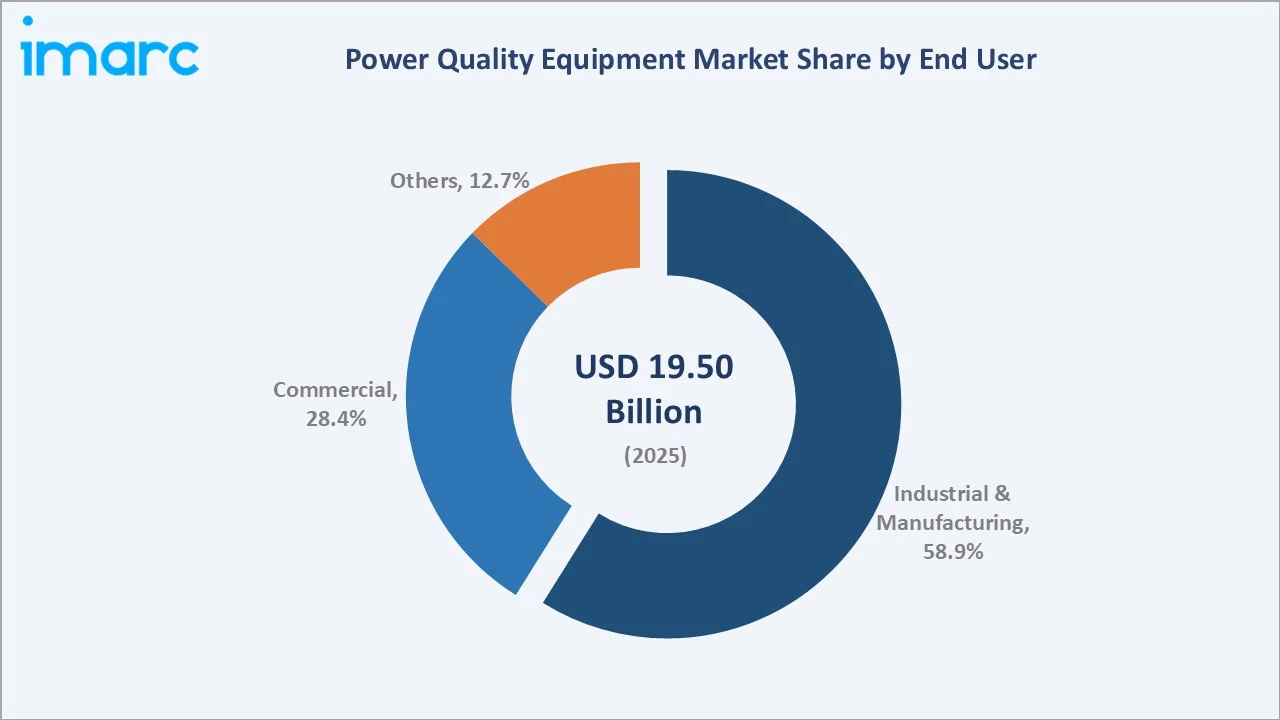

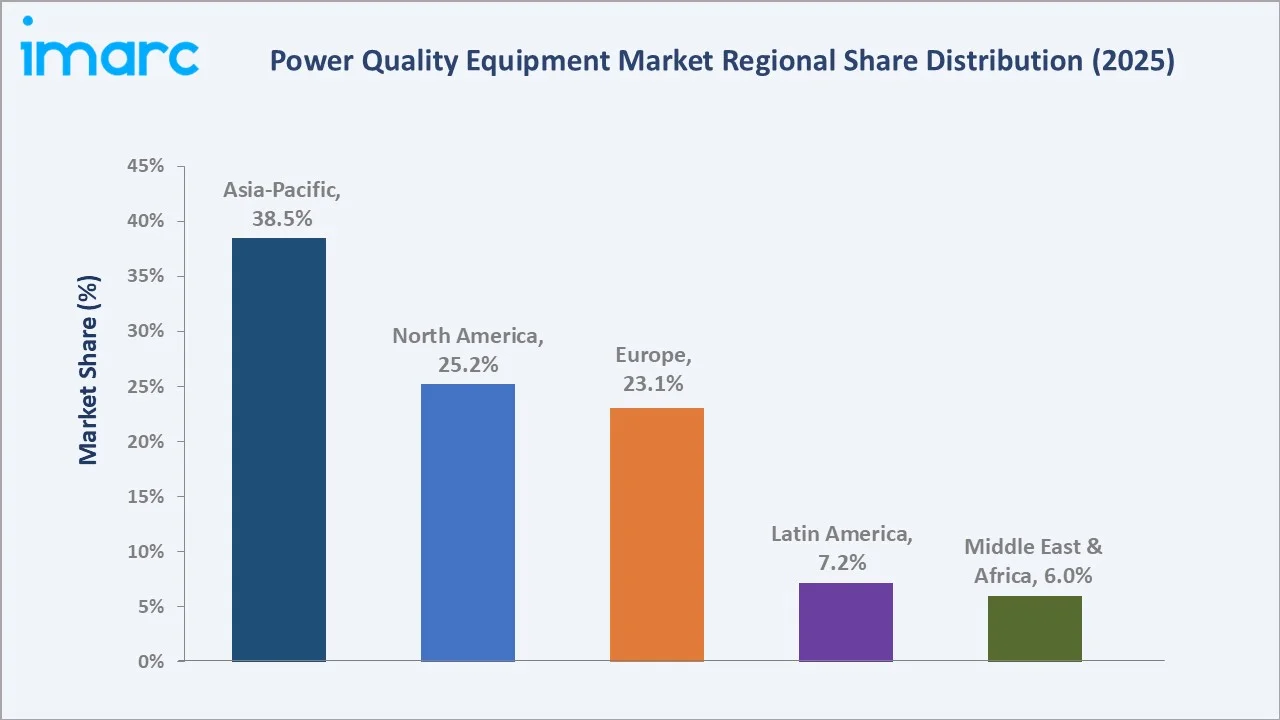

Three Phase leads at 67.3%. Industrial and Manufacturing dominate end use at 58.9%. Asia-Pacific commands 38.5% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 19.50 Billion |

|

Forecast Market Size (2034) |

USD 31.06 Billion |

|

CAGR (2026-2034) |

5.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Phase |

Three Phase (67.3%, 2025) |

|

Dominant End User |

Industrial and Manufacturing (58.9%, 2025) |

|

Leading Region |

Asia-Pacific (38.5%, 2025) |

The market expanded from USD 15.17 Billion in 2020 to USD 19.50 Billion in 2025, anchored at USD 25.06 Billion in 2030 and forecast to reach USD 31.06 Billion by 2034. Sustained growth reflects structural demand from industrial automation expansion, renewable energy grid integration, and data center construction globally.

To get more information on this market, Request Sample

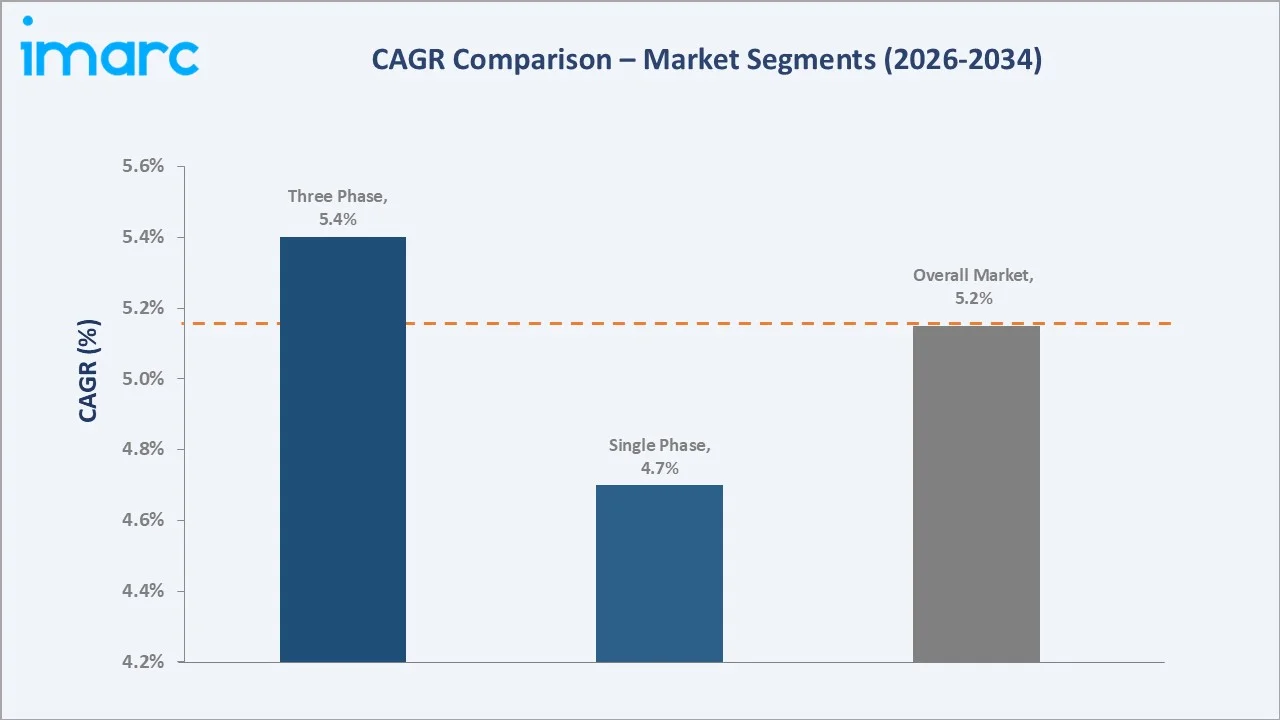

Three Phase segment grows at ~5.4% CAGR, maintaining dominance through industrial and utility-scale power quality applications requiring balanced three-phase systems. Single Phase accelerates at ~4.7% CAGR as commercial and SME power protection awareness rises. Industrial and Manufacturing end user leads at 5.6% CAGR through automation expansion.

Executive Summary

The global power quality equipment market reached USD 19.50 Billion in 2025, driven by industrial automation expansion, renewable energy integration, and increasing data center infrastructure investment. The market is projected to reach USD 31.06 Billion by 2034 at a 5.15% CAGR through sustained demand across all end-use segments globally.

Three Phase at 67.3% dominates through industrial and utility-scale power protection requirements. Industrial and Manufacturing at 58.9% leads through the highest sensitivity to power disruptions and associated financial losses. Asia-Pacific at 38.5% commands global leadership through rapid industrialization, urbanization, and expanding manufacturing and data center output.

Key Market Insights

|

Insight |

Data |

|

Dominant Phase |

Three Phase - 67.3% market share (2025) |

|

Dominant End User |

Industrial and Manufacturing - 58.9% market share (2025) |

|

Leading Region |

Asia-Pacific - 38.5% market share (2025) |

|

Market Opportunity |

Smart grid integration; IoT-enabled PQE monitoring; renewable energy stabilization; data center UPS |

Key Analytical Observations Supporting The Above Data:

- Three Phase at 67.3%: Three Phase equipment dominates as industrial processes, commercial facilities, and utility installations require high-power, balanced three-phase systems for motors, HVAC, and large electrical loads. Higher voltage stability requirements in industrial environments sustain strong three-phase UPS and harmonic filter procurement globally.

- Industrial and Manufacturing at 58.9%: Industrial and manufacturing operations are the most sensitive to power quality disturbances, as voltage sags, harmonic distortion, and power interruptions directly cause production stoppages and financial losses. Rising factory automation further increases the critical importance of comprehensive power quality protection equipment.

- Asia-Pacific at 38.5%: Asia-Pacific leads through rapid industrialization across major economies, combined with expanding manufacturing output, large-scale data center construction, and growing electricity consumption driving sustained demand for uninterruptible power supply and power conditioning equipment.

Power Quality Equipment Market Overview

The global power quality equipment market encompasses the design, manufacture, and supply of equipment used to monitor, detect, and correct electrical power supply disturbances. Key product categories include uninterruptible power supplies, harmonic filters, static VAR compensators, voltage regulators, surge protection devices, and power quality meters.

The ecosystem integrates raw material and component suppliers, PQE manufacturers, system integrators, distributors, end-user industries, and regulatory bodies establishing power quality standards. Key macroeconomic drivers include rising electricity demand, industrial automation expansion, renewable energy growth, and increasing data center construction globally.

Market Dynamics

To evaluate market opportunities, Request Sample

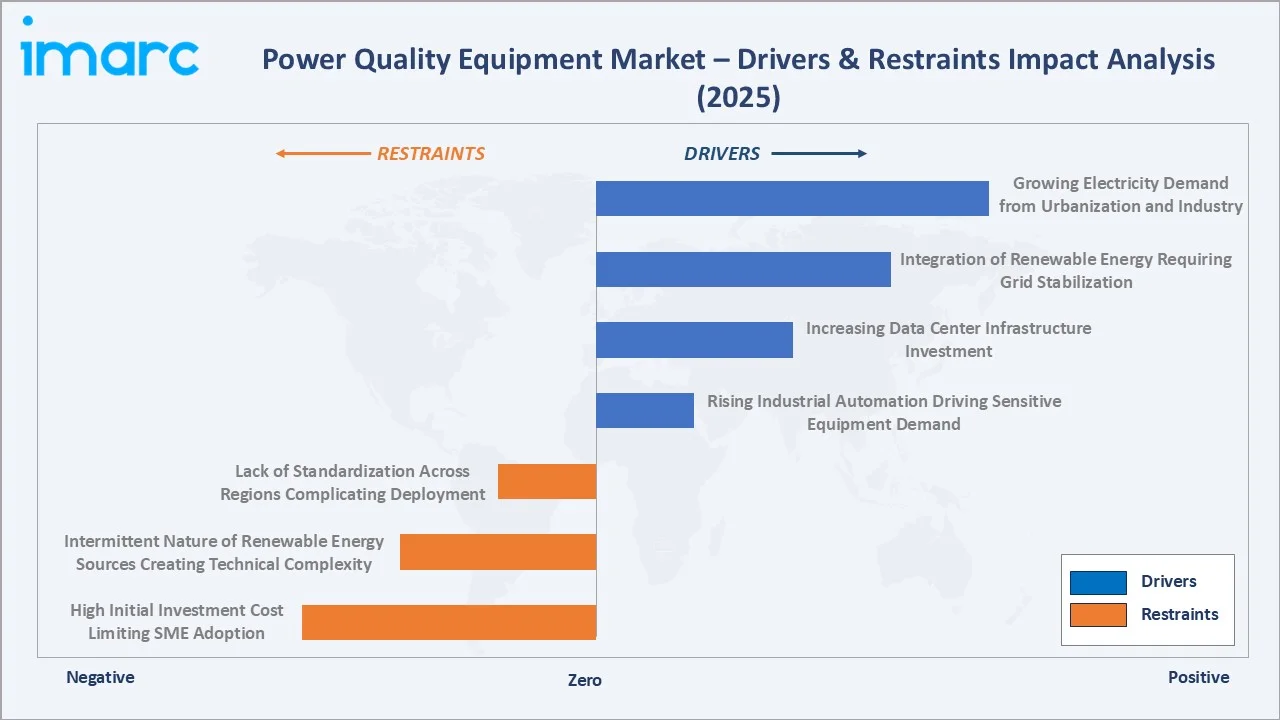

Market Drivers

- Growing Electricity Demand from Urbanization and Industry: Rapid urbanization and industrial expansion globally are driving electricity consumption to record levels. Increased power demand creates greater strain on grid infrastructure, amplifying the frequency of voltage sags, surges, and power quality disturbances. This directly increases demand for PQE to protect sensitive industrial and commercial electrical loads from disruption and associated financial losses.

- Increasing Data Center Infrastructure Investment: Global data center construction is accelerating as cloud computing, AI, and digital transformation drive exponential growth in compute demand. Data centers require highest-tier power quality protection, including online double-conversion UPS systems, harmonic filters, and power conditioning equipment, creating a high-value and growing procurement segment for PQE manufacturers.

- Integration of Renewable Energy Requiring Grid Stabilization: The large-scale integration of solar and wind energy into national grids introduces voltage instability, frequency variations, and harmonic distortion. Static VAR compensators, harmonic filters, and advanced power conditioning equipment are deployed to maintain grid stability, creating structural demand growth for power quality solutions across utility markets.

- Rising Industrial Automation Driving Sensitive Equipment Demand: The deployment of programmable logic controllers, robotics, CNC machines, and variable frequency drives in manufacturing creates an expanding base of power-sensitive equipment vulnerable to voltage disturbances. Manufacturers invest in three-phase UPS systems and harmonic filters to protect automated production lines from costly downtime and equipment failures.

Market Restraints

- High Initial Investment Cost Limiting SME Adoption: The procurement and installation of comprehensive power quality equipment systems — particularly three-phase UPS systems and static VAR compensators — requires significant capital investment. Small and medium-sized enterprises often lack the budget to deploy full power quality solutions, limiting total addressable market penetration in cost-sensitive customer segments.

- Intermittent Nature of Renewable Energy Sources Creating Technical Complexity: While renewable energy integration drives demand for PQE, the technical complexity of stabilizing variable solar and wind generation creates design and engineering challenges. Power quality solutions must address rapidly fluctuating voltage and frequency profiles, increasing product development complexity and total system costs for end users.

- Lack of Standardization Across Regions Complicating Deployment: Varying national grid standards, voltage levels, frequency specifications, and power quality regulatory frameworks across geographies complicate the design and deployment of globally standardized PQE solutions. Manufacturers must develop region-specific product variants, increase portfolio complexity and reducing economies of scale in manufacturing operations.

Market Opportunities

- Smart Grid Integration Enabling IoT-Based Power Quality Monitoring: The global smart grid deployment creates an opportunity for IoT-enabled power quality monitoring systems that provide real-time disturbance detection, predictive maintenance alerts, and remote diagnostics. Smart PQE systems delivering actionable intelligence can command premium pricing and service contract revenue alongside hardware sales globally.

- Emerging Market Infrastructure Development Generating New Demand Pools: Rapid infrastructure development across Southeast Asia, Latin America, Africa, and the Middle East is creating new demand pools for power quality equipment as industrial facilities, commercial buildings, and utilities are established. Lower grid reliability in these regions creates particularly strong demand for UPS systems and voltage regulators.

Market Challenges

- Commodity Price Volatility Affecting Manufacturing Costs: Power quality equipment relies on copper, electrical steel, capacitors, and semiconductor components whose commodity prices are subject to global supply chain volatility. Input cost inflation directly compresses PQE manufacturer margins, particularly in competitive commodity-grade product segments such as entry-level UPS and surge protection devices.

- Rapid Technological Change Requiring Continuous R&D Investment: The power quality equipment industry is experiencing rapid technology evolution driven by wide-bandgap semiconductor adoption, digital monitoring integration, and smart grid compatibility requirements. Manufacturers must continuously invest in R&D to maintain product relevance, creating financial pressure on mid-tier players with limited development budgets.

Emerging Market Trends

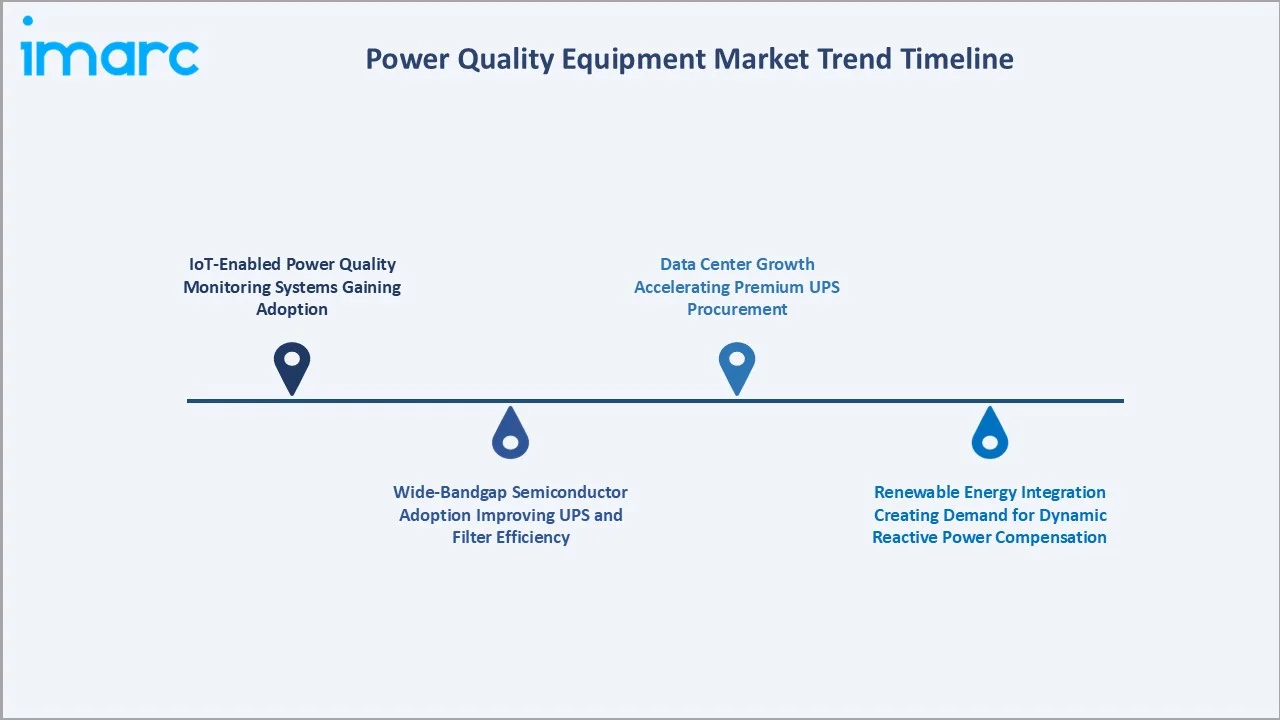

1. IoT-Enabled Power Quality Monitoring Systems Gaining Adoption

Advanced PQE systems are integrating IoT sensors, cloud connectivity, and real-time analytics for continuous power quality monitoring and predictive maintenance. These systems allow facility managers to identify disturbance patterns, schedule preventive maintenance, and reduce unplanned downtime, transitioning PQE from passive protection devices to active operational intelligence platforms.

2. Wide-Bandgap Semiconductor Adoption Improving UPS and Filter Efficiency

Silicon carbide (SiC) and gallium nitride (GaN) semiconductors are being adopted in UPS inverters and active harmonic filters, delivering significant improvements in switching efficiency, thermal performance, and power density. This enables more compact and energy-efficient PQE products, particularly relevant for high-density data center and industrial automation applications.

3. Renewable Energy Integration Creating Demand for Dynamic Reactive Power Compensation

The large-scale grid integration of solar and wind power is driving deployment of dynamic reactive power compensation systems including static VAR compensators and STATCOM systems. These advanced PQE solutions respond in milliseconds to voltage fluctuations caused by intermittent renewables, maintaining grid stability across high-renewable penetration networks globally.

4. Data Center Growth Accelerating Premium UPS Procurement

AI-driven data center expansion is creating strong demand for premium double-conversion online UPS systems, modular UPS architectures, and advanced power conditioning products. The criticality of data center uptime and the high density of AI server power loads drive procurement of high-specification three-phase PQE solutions with comprehensive digital monitoring capabilities.

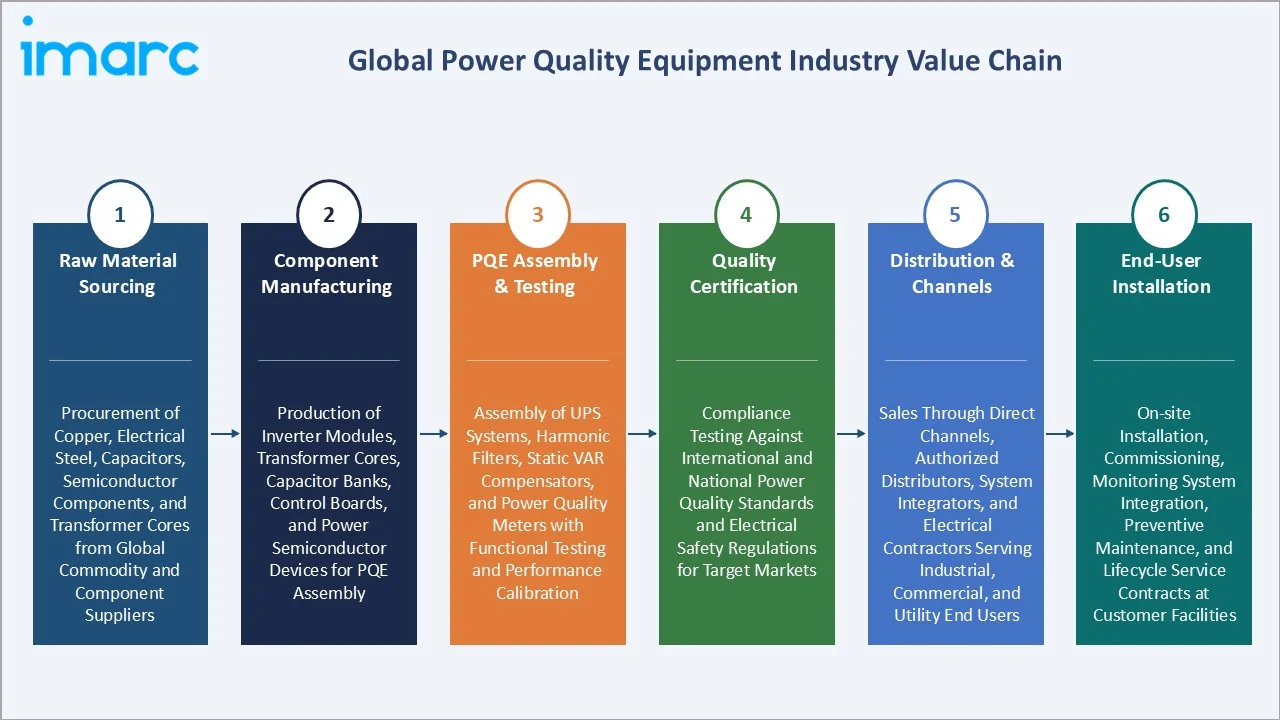

Industry Value Chain Analysis

The power quality equipment value chain integrates raw material and component sourcing, equipment manufacturing and assembly, quality certification, distribution through channels, and end-user installation and maintenance. The chain is globally distributed, with component manufacturing concentrated in Asia and final assembly spanning global markets with regional service support.

|

Stage |

Key Activities |

|

Raw Material Sourcing |

Procurement of copper, electrical steel, capacitors, semiconductor components, and transformer cores from global commodity and component suppliers |

|

Component Manufacturing |

Production of inverter modules, transformer cores, capacitor banks, control boards, and power semiconductor devices for PQE assembly |

|

PQE Assembly & Testing |

Assembly of UPS systems, harmonic filters, static VAR compensators, and power quality meters with functional testing and performance calibration |

|

Quality Certification |

Compliance testing against applicable international and national power quality standards and electrical safety regulations for target markets |

|

Distribution & Channels |

Sales through direct channels, authorized distributors, system integrators, and electrical contractors serving industrial, commercial, and utility end users |

|

End-User Installation |

On-site installation, commissioning, monitoring system integration, preventive maintenance, and lifecycle service contracts at customer facilities |

The raw material sourcing stage faces the most significant commodity price volatility through copper and semiconductor market cycles. The quality certification stage represents the key regulatory barrier to market entry, with international compliance testing requirements forming a meaningful cost and timeline barrier for new product introductions globally.

Technology Landscape in the Power Quality Equipment Industry

Uninterruptible Power Supply (UPS) Technology

UPS technology has evolved from offline and line-interactive configurations toward double-conversion online systems offering near-zero transfer time. Modular UPS architectures enable scalable power protection for data center and industrial applications, while lithium-ion battery integration is replacing traditional lead-acid batteries for improved energy density, cycle life, and monitoring capability.

Active Harmonic Filter Technology

Active harmonic filters dynamically detect and inject compensating currents to cancel harmonic distortion generated by non-linear loads such as variable frequency drives and switching power supplies. Wide-bandgap semiconductor adoption in active filter inverters is improving switching frequency, reducing residual harmonics, and enabling more compact filter designs for industrial installations.

Static VAR Compensator and STATCOM Technology

Static VAR compensators and STATCOM systems provide dynamic reactive power compensation to stabilize voltage profiles on transmission and distribution networks. Voltage source converter-based STATCOM systems offer superior dynamic response versus traditional thyristor-controlled SVCs and are increasingly deployed at renewable energy grid connection points for voltage stability management.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Equipment |

🔒 |

🔒 |

2025 |

|

Phase |

Three Phase |

67.3% |

2025 |

|

End User |

Industrial and Manufacturing |

58.9% |

2025 |

|

Region |

Asia-Pacific |

38.5% |

2025 |

By Phase

Three Phase leads at 67.3% in 2025, reflecting the dominant role of industrial, commercial, and utility-scale power quality applications that require balanced three-phase power protection. Three-phase UPS systems, harmonic filters, and static VAR compensators serve the highest-value equipment categories in the power quality equipment market.

To access detailed market analysis, Request Sample

Single Phase at 32.7% serves commercial buildings, SME facilities, healthcare, and residential applications where single-phase power distribution is standard. Growing commercial construction and expanding IT infrastructure in emerging markets are sustaining Single Phase segment growth throughout the forecast period to 2034.

By End User

Industrial and Manufacturing leads at 58.9% in 2025, driven by the highest sensitivity to power quality disturbances and the greatest financial exposure to power interruptions across automated production environments. Manufacturing facilities procure the full range of PQE equipment including UPS systems, harmonic filters, and voltage regulators.

Commercial at 28.4% includes data centers, office buildings, retail, hospitality, and healthcare facilities requiring reliable power protection for IT infrastructure and critical operations. Others at 12.7% covers utilities, transportation, and government facilities deploying PQE for grid and infrastructure protection applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Power Quality Equipment Market Drivers & Characteristics |

|

Asia-Pacific |

38.5% |

Driven by rapid industrialization, expanding manufacturing output, large-scale data center construction, and rising electricity consumption across major regional economies |

|

North America |

25.2% |

Supported by mature industrial base, high data center density, ongoing grid modernization investment, and stringent power quality standards across key industries |

|

Europe |

23.1% |

Driven by renewable energy integration requirements, industrial energy efficiency mandates, grid stability investments, and compliance with stringent power quality regulations |

|

Latin America |

7.2% |

Driven by industrial expansion, grid reliability challenges, increasing data center investment, and growing awareness of power quality protection requirements |

|

Middle East & Africa |

6.0% |

Emerging demand driven by infrastructure development, industrial projects, renewable energy integration, and increasing commercial construction activity across the region |

Asia-Pacific, at 38.5%, leads through rapid industrialization and expanding data center construction. North America, at 25.2%, reflects the world's highest data center density and mature industrial power quality standards. Europe, at 23.1%, is driven by renewable energy integration mandates and stringent power quality compliance requirements.

Latin America, at 7.2%, and Middle East and Africa, at 6.0%, represent growing adoption markets driven by infrastructure development and industrialization. Both regions show above-average growth potential as grid reliability challenges and rising industrial investment create strong structural demand for UPS systems and voltage regulators.

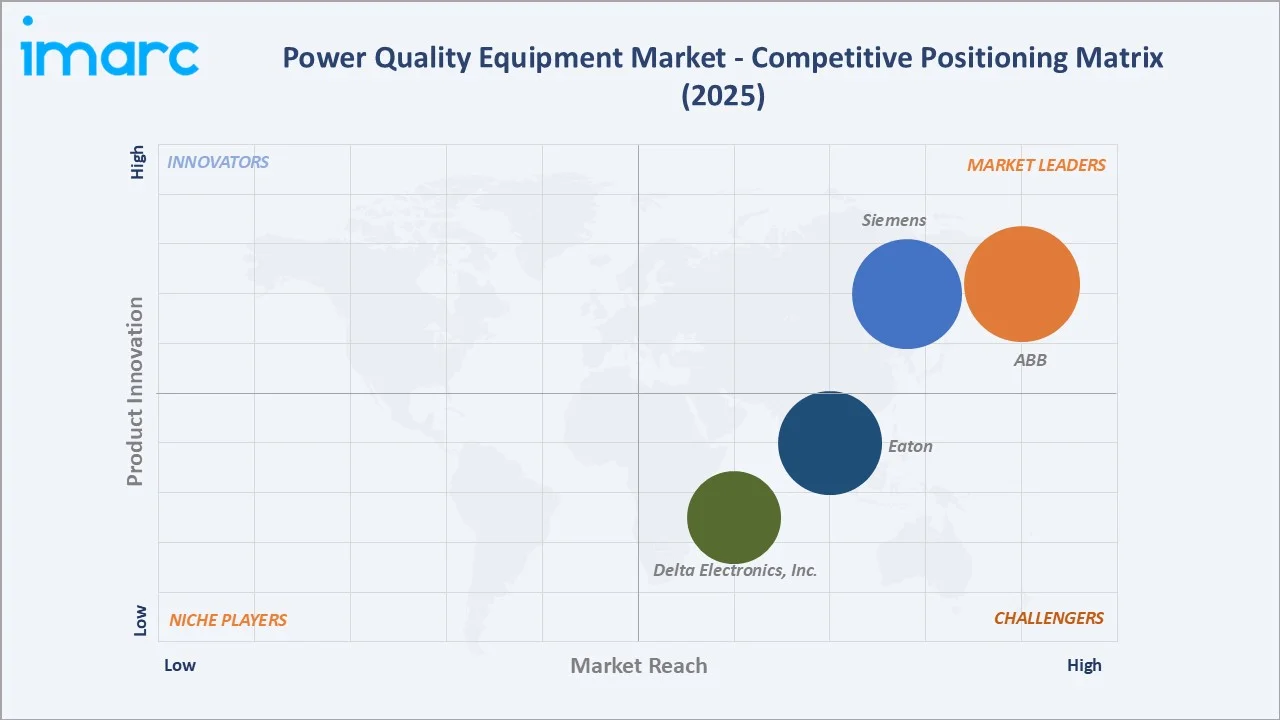

Competitive Landscape

The global power quality equipment market is moderately concentrated, with global diversified electrical equipment manufacturers dominating the upper tier. Leading players compete on product breadth, technology leadership, service network scale, and the ability to integrate PQE within broader electrical and digital infrastructure platforms.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

ABB |

Power Quality monitoring, Transient Surge Protection, Reactive Power Compensation, Voltage and Frequency Protection, Power Cuts and Outage Protection |

Market Leader |

Global leader in electrification and automation; broadest PQE portfolio spanning grid-scale to facility-level power quality solutions |

|

Siemens |

Power Quality Meters & Accessories, SICAM Q100 |

Market Leader |

Global industrial technology leader with integrated power quality solutions across smart grid, industrial, and building infrastructure applications |

|

Eaton |

9PX UPS, 5P UPS |

Strong Challenger |

Specialized power management solutions provider; strong UPS and power distribution portfolio for industrial and data center markets globally |

|

Delta Electronics, Inc. |

Active Harmonic (Power) Filter, Static Var Generator (SVG) |

Strong Challenger |

Power electronics specialist with competitive UPS and active harmonic filter portfolio for industrial and commercial IT markets globally |

Key players include ABB, Siemens, Eaton, Delta Electronics, Inc., and others.

Key Company Profiles

ABB

ABB is a Switzerland-based global leader in electrification and automation technologies, with a comprehensive power quality equipment portfolio spanning UPS systems, harmonic filters, static VAR compensators, and STATCOM solutions for industrial, commercial, and utility applications worldwide.

- Key Products: Power Quality monitoring, Transient Surge Protection, Reactive Power Compensation, Voltage and Frequency Protection, Power Cuts and Outage Protection.

- Strategic Focus: Expanding integrated power quality and electrification solutions for renewable energy, industrial automation, and smart grid applications, with emphasis on digital monitoring and IoT-connected PQE products delivering real-time operational intelligence to end users.

Siemens

Siemens is a Germany-based global industrial technology company with a comprehensive power quality equipment portfolio addressing industrial, commercial, and grid-scale applications through its integrated digital infrastructure and energy management platforms.

- Key Products: Power Quality Meters & Accessories, SICAM Q100.

- Strategic Focus: Integrating power quality solutions within Siemens' digital industries and smart infrastructure platforms, targeting industrial facilities, data centers, and smart buildings requiring seamless integration of power quality protection and comprehensive operational intelligence systems.

Market Concentration Analysis

The power quality equipment market is moderately concentrated, with leading global electrical equipment manufacturers collectively accounting for a significant portion of global PQE revenue across industrial and utility segments. The UPS sub-segment is more fragmented, with specialized players competing alongside diversified electrical equipment manufacturers globally.

Market concentration varies significantly by product category and geography. Grid-scale SVCs and STATCOM systems are concentrated among a small number of high-engineering-capability suppliers, while standard UPS and surge protection products are served by a broader competitive field including regional specialists and cost-competitive manufacturers.

Investment & Growth Opportunities

Highest Growth Segments

Industrial and Manufacturing end user (~5.6% CAGR), Three Phase equipment (~5.4% CAGR), data center-grade UPS systems (~7-8% CAGR from growing base), Asia-Pacific regional expansion (~6%+ CAGR), and IoT-connected power quality monitoring services represent the highest-return investment vectors through 2034.

Emerging Investment Opportunities

The global data center construction boom driven by AI infrastructure investment represents the largest near-term growth opportunity for premium three-phase UPS and power conditioning equipment. Hyperscale and edge data center operators require highest-specification double-conversion UPS systems at scale, generating substantial procurement volumes for market leaders.

Investment Themes

- Renewable energy grid integration PQE: Static VAR compensators, STATCOM, and harmonic filtering solutions are structurally positioned for above-market growth as solar and wind generation penetration increases globally, creating essential reactive power management requirements at renewable energy grid connection points.

- IoT-enabled power quality monitoring services: Transitioning from hardware-only to hardware-plus-recurring-service business models through connected PQE platforms delivering real-time power quality analytics, predictive maintenance, and remote diagnostics creates higher lifetime customer value and more stable revenue streams.

- Emerging market UPS and voltage regulator expansion: Distributing cost-competitive single-phase and three-phase UPS systems and automatic voltage regulators into Southeast Asia, Latin America, and Africa captures growing demand pools driven by infrastructure development and persistent grid reliability challenges.

Future Market Outlook (2026-2034)

The global power quality equipment market is projected to grow from USD 19.50 Billion in 2025 to USD 31.06 Billion by 2034, delivering a 5.15% CAGR. The market anchor of USD 25.06 Billion in 2030 reflects the midpoint of sustained expansion driven by industrial automation, renewable energy integration, and data center construction globally.

Industrial and Manufacturing will continue to dominate through expanding factory automation globally, while the Commercial segment accelerates through data center growth. Asia-Pacific will consolidate its leadership as major regional economies continue industrial and infrastructure investment programs. Technology evolution toward IoT-connected, digitally monitored PQE systems will define the competitive landscape through 2034.

Three structural forces sustain market growth: industrial automation expansion creating ongoing power quality protection demand, renewable energy integration requiring dynamic reactive power compensation, and data center construction driving premium UPS procurement. Manufacturers integrating hardware, monitoring software, and service contracts will achieve structural competitive advantages through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including PQE product engineers, industrial procurement managers, data center facility operators, utility grid engineers, renewable energy integration specialists, and electrical system consultants across key global markets.

Secondary Research

Secondary research encompassed company annual reports, IEC and IEEE power quality standards documentation, national grid authority reports, IEA electricity demand projections, data center construction databases, industrial automation market data, and renewable energy integration studies. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a demand-side bottom-up model: (i) end-user segment electricity consumption and sensitive equipment base; (ii) PQE penetration rate by end user and region; (iii) average equipment spend per MW of protected load; (iv) technology mix adjustment for premium IoT-connected versus standard PQE products.

Power Quality Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipments Covered | Uninterruptable Power Supply (UPS), Harmonic Filters, Static VAR Compensator, Power Quality Meters, Others |

| Phases Covered | Single Phase, Three Phase |

| End Users Covered | Industrial and Manufacturing, Commercial, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB, Siemens, Eaton, Delta Electronics Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the power quality equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global power quality equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the power quality equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Power Quality Equipment Market Report

The global power quality equipment market reached USD 19.50 Billion in 2025, growing from USD 15.17 Billion in 2020, driven by Three Phase dominance at 67.3%, Industrial and Manufacturing leading end use at 58.9%, and Asia-Pacific commanding 38.5% of global market share.

The power quality equipment market grows at 5.15% CAGR during 2026-2034, reaching USD 31.06 Billion by 2034, driven by industrial automation expansion, renewable energy integration, data center growth, and emerging market infrastructure development.

Three Phase leads at 67.3%, reflecting the dominance of industrial, commercial, and utility-scale power quality applications requiring balanced three-phase power protection including UPS systems, harmonic filters, and static VAR compensators across global markets.

Industrial and Manufacturing leads at 58.9% through the highest sensitivity to power quality disturbances, greatest financial exposure to power interruptions, and expanding factory automation creating a growing base of power-sensitive equipment requiring comprehensive protection.

Asia-Pacific leads at 38.5% through rapid industrialization, expanding data center construction, and growing electricity consumption across major regional economies driving demand for comprehensive power quality protection equipment.

Leading companies include ABB, Siemens, Eaton, Delta Electronics, Inc., and others.

The market is projected to reach USD 31.06 Billion by 2034, anchored at USD 25.06 Billion in 2030, with Industrial and Manufacturing maintaining dominance, Three Phase consolidating its leading share, and Asia-Pacific strengthening its regional leadership position.

Three priority investment opportunities: renewable energy grid integration SVCs and harmonic filters; IoT-enabled power quality monitoring and services platforms; and premium data center three-phase UPS systems capturing the AI infrastructure construction-driven demand surge through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)