Predictive Maintenance Market Size, Share, Trends and Forecast by Component, Technique, Deployment Type, Organization Size, Industry Vertical, and Region, 2026-2034

Global Predictive Maintenance Market Size, Share, Trends & Forecast (2026-2034)

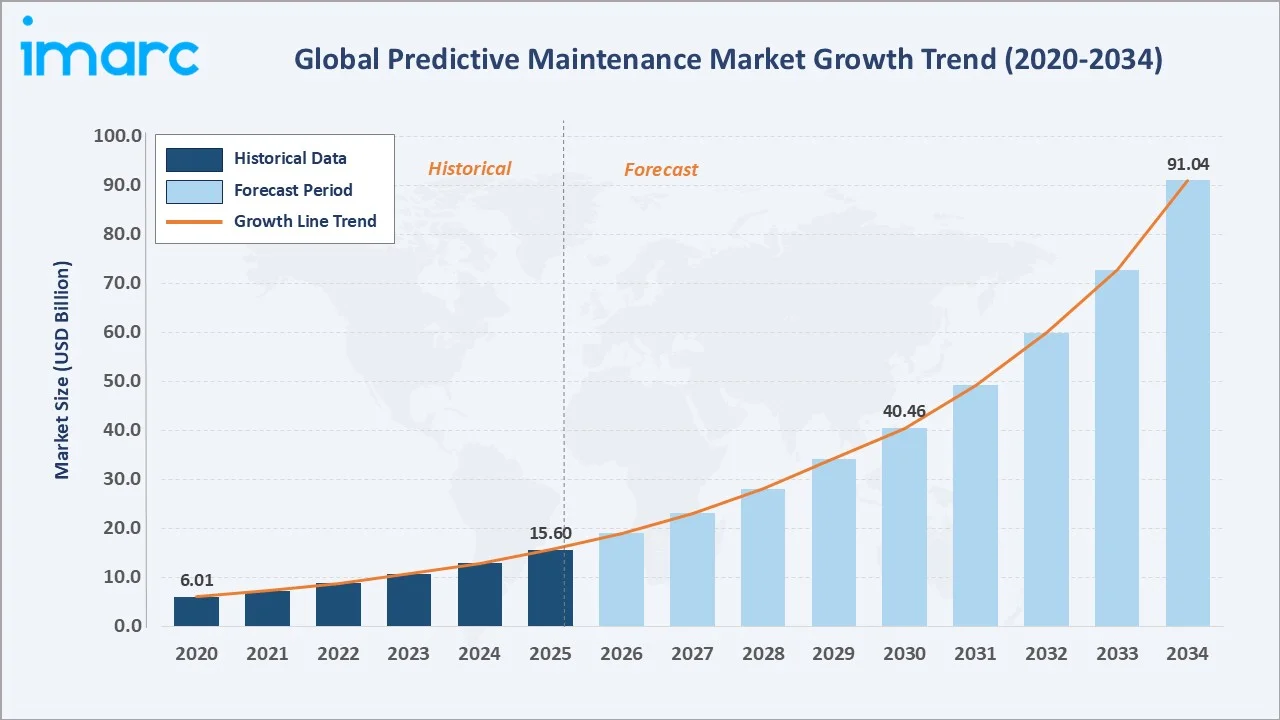

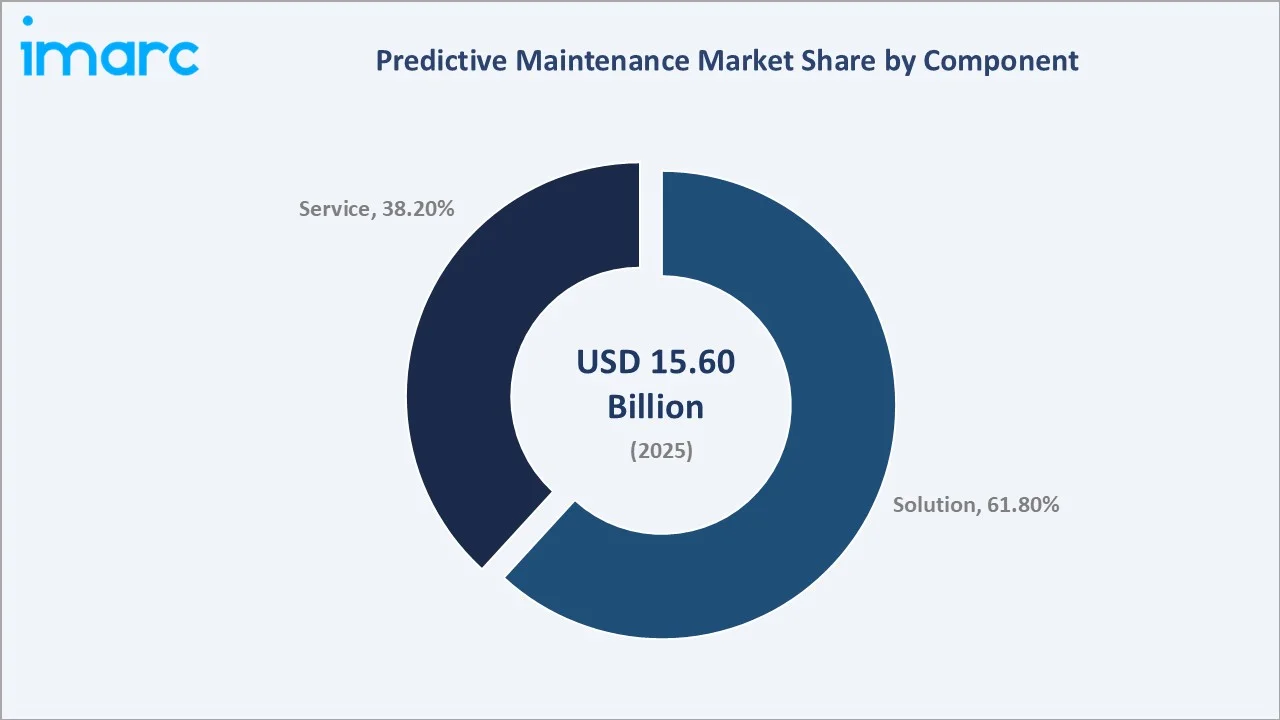

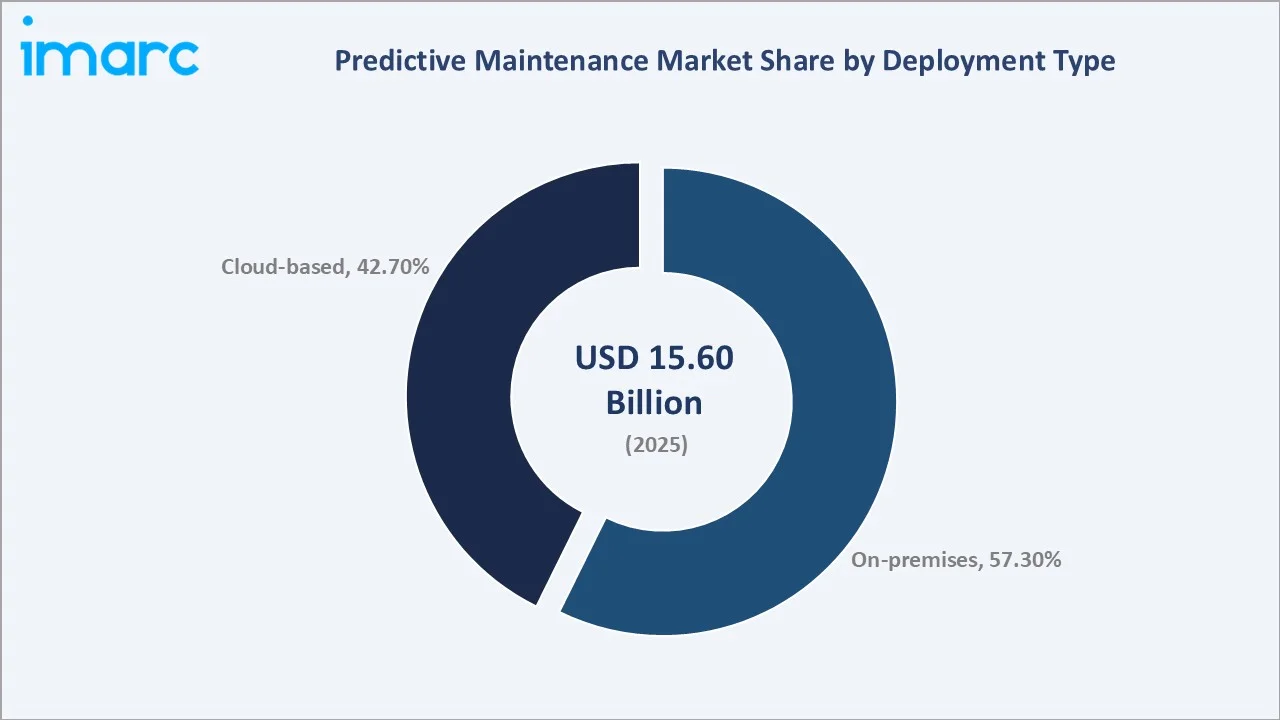

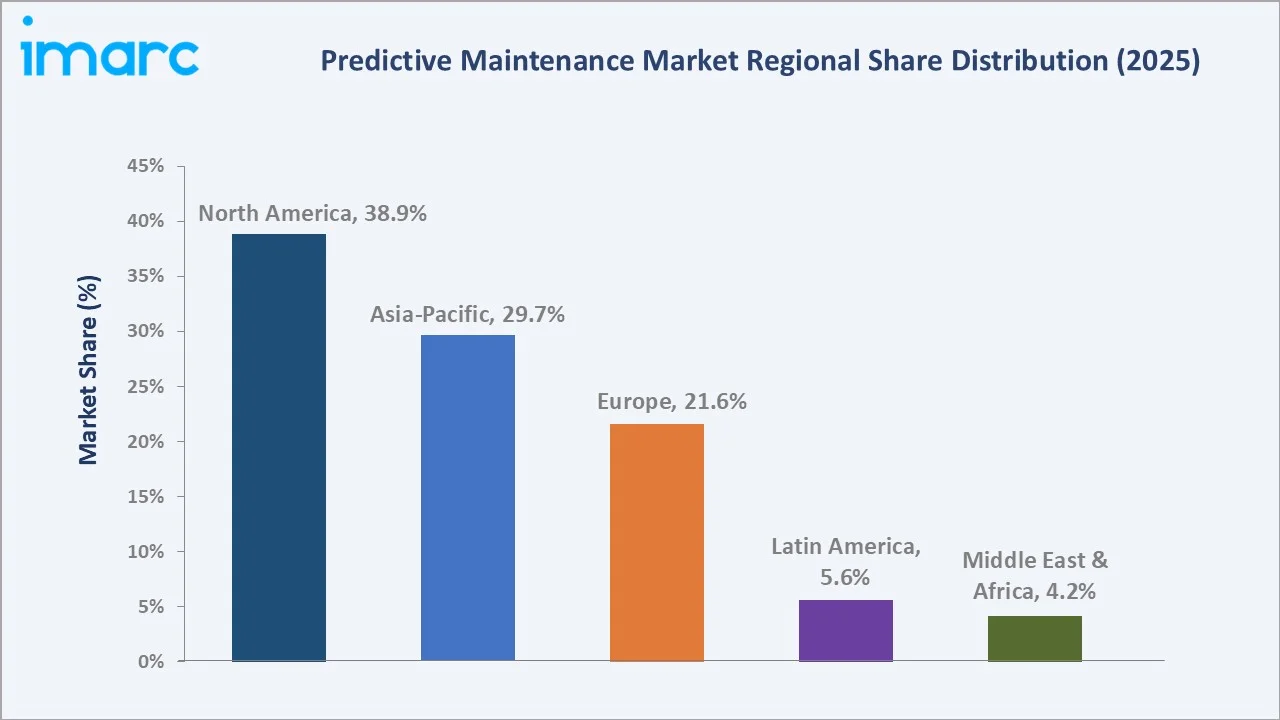

The global predictive maintenance market was valued at USD 15.60 Billion in 2025 and is projected to reach USD 91.04 Billion by 2034, expanding at a CAGR of 21.01% during the forecast period (2026-2034). Explosive growth is driven by accelerating IIoT and Industry 4.0 adoption (Over a decade after its inception, Industry 4.0 appears to be thriving, with public search interest increasing by 140 times since its creation), AI/ML-powered anomaly detection reducing unplanned downtime costs, and the rapid scale-up of cloud-based PdM platforms across manufacturing, energy, aerospace, and transportation sectors. Solution components dominate at 61.8% market share (2025), while on-premises deployment leads at 57.3%. North America holds the largest regional share at 38.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.60 Billion |

|

Forecast Market Size (2034) |

USD 91.04 Billion |

|

CAGR (2026-2034) |

21.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.9%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~24.5%, 2026-2034) |

To get more information on this market, Request Sample

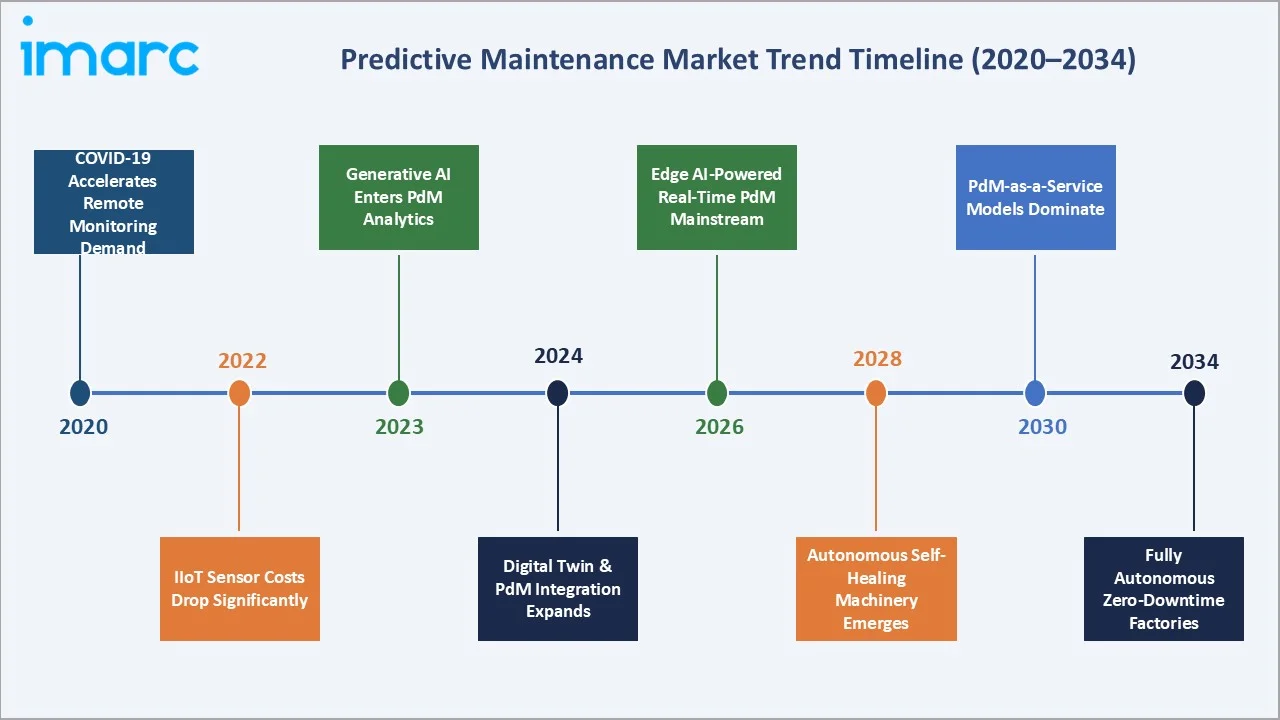

The global predictive maintenance market from 2020 through 2034, expanded from USD 6.01 Billion in 2020 to USD 15.60 Billion in 2025, driven by COVID-19-accelerated remote monitoring adoption, falling IIoT sensor costs, and enterprise digital transformation investment. The market is forecast to cross USD 40.46 Billion in 2030 before reaching USD 91.04 Billion by 2034.

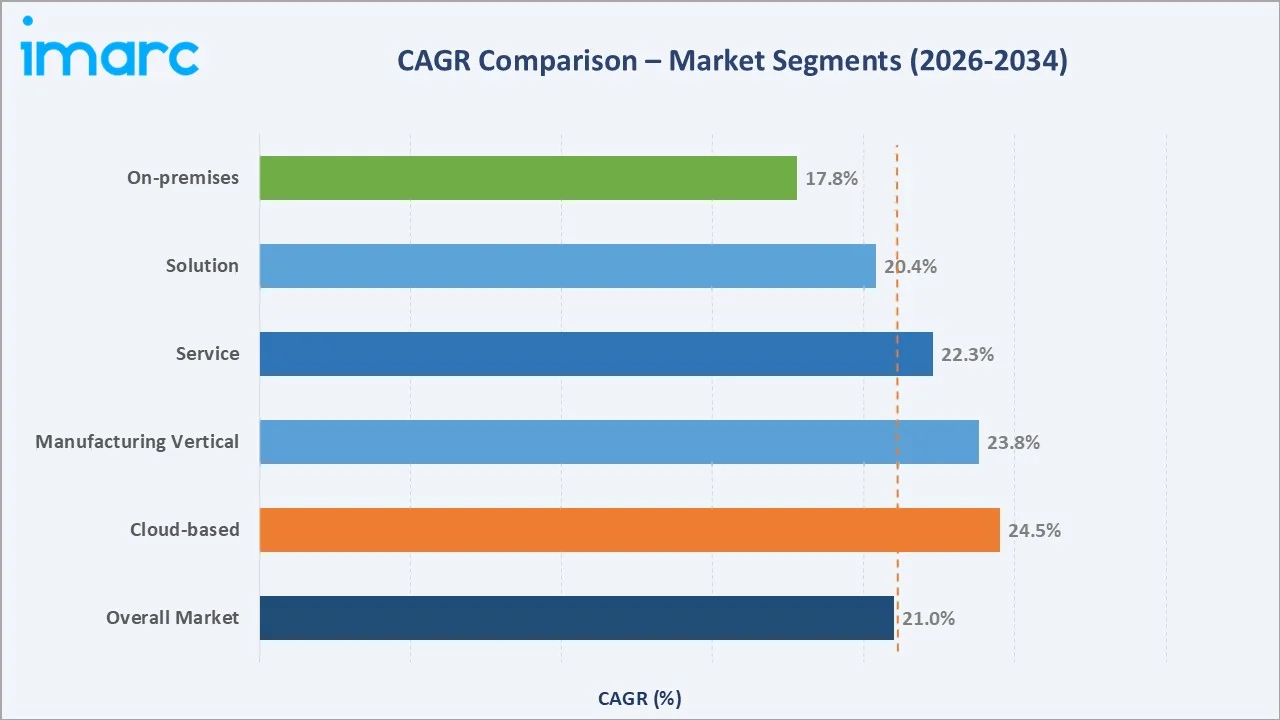

Cloud-based deployment leads at ~24.5% CAGR, reflecting rapid enterprise migration to scalable subscription-based PdM platforms. The manufacturing vertical at ~23.8% CAGR is the fastest-growing end-use industry, as factory operators deploy sensor-driven AI analytics to protect high-value production assets from unscheduled stoppages through 2034.

Executive Summary

The global predictive maintenance market is experiencing one of the highest CAGRs among all industrial software categories. From USD 6.01 Billion in 2020, the market surged to USD 15.60 Billion in 2025, representing a 2.6× increase driven by accelerating IIoT sensor deployments, cloud computing cost democratization, and the maturation of machine learning models capable of predicting equipment failure with accuracy across diverse industrial equipment types. The forecast trajectory to USD 91.04 Billion by 2034 reflects five compounding structural drivers: over USD 1 trillion annual cost of unplanned industrial downtime globally, Industry 4.0 mandates from governments, the energy transition creating new asset monitoring requirements, post-COVID supply chain resilience investment, and the generative AI revolution enabling non-technical users to deploy predictive models.

Solution components dominate with 61.8% market share (2025), encompassing software platforms, AI/ML analytics engines, and digital twin applications that form the intelligence layer of every PdM deployment. The service component at 38.2% is the faster-growing segment at ~22.3% CAGR through 2034, as enterprises increasingly outsource PdM model development, sensor calibration, and managed monitoring services to specialized vendors.

On-premises deployment at 57.3% (2025) remains dominant in data-sensitive industries including aerospace, defence, and critical infrastructure. Cloud-based at 42.7% is growing fastest at ~24.5% CAGR, as SMEs and mid-market manufacturers adopt subscription PdM platforms without upfront infrastructure investment. North America’s 38.9% leadership reflects the U.S.’s position as the world’s largest industrial technology spender. Asia-Pacific at 29.7% is the fastest-growing region, driven by China’s Made in China 2025 smart manufacturing mandate and Japan’s Society 5.0 industrial AI initiatives.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Solution - 61.8% revenue share (2025) |

|

Dominant Deployment Type |

On-premises - 57.3% revenue share (2025) |

|

Leading Region |

North America - 38.9% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~24.5%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Solution dominates at 61.8% (2025): Solutions encompasses comprehensive software platforms combining condition monitoring, failure mode prediction, remaining useful life (RUL) estimation, and maintenance work order generation.

- On-premises at 57.3% but cloud accelerating: On-premises PdM dominance reflects legacy IT security policies in aerospace, defence, and critical infrastructure that require air-gapped or private network deployment.

- North America leads at 38.9% (2025): The U.S. Department of Defense introduced its Predictive Maintenance and Condition-Based Maintenance Plus (CBM+) initiative two decades ago, but significant progress occurred after 2018 with the launch of the Army's Project Convergence and the Navy's Project Overmatch.

- Asia-Pacific fastest growing at ~24.5% CAGR: China’s Made in China 2025 program is raising the domestic content of core components and materials to 70% by 2025, creating the world’s largest national PdM adoption mandate.

Global Predictive Maintenance Market Overview

Predictive maintenance (PdM) encompasses the technologies, software platforms, and services that monitor industrial equipment condition in real time, apply AI and machine learning algorithms to historical and live sensor data, and predict equipment failure before it occurs, enabling maintenance to be performed at precisely the right time to prevent unplanned downtime while minimising unnecessary scheduled maintenance costs. The PdM ecosystem integrates hardware sensors, IIoT connectivity platforms, edge and cloud computing infrastructure, and AI analytics software into unified asset health monitoring systems.

Applications span manufacturing, energy, aerospace, transportation, and healthcare. The global cost of industrial downtime, estimated at USD 1 trillion annually, represents the total addressable cost problem that predictive maintenance addresses. Macroeconomic influences include global capital expenditure cycles in heavy industry, IIoT sensor cost deflation, and cloud computing economics, enabling small operations to access enterprise-grade analytics.

Market Dynamics

To evaluate market opportunities, Request Sample

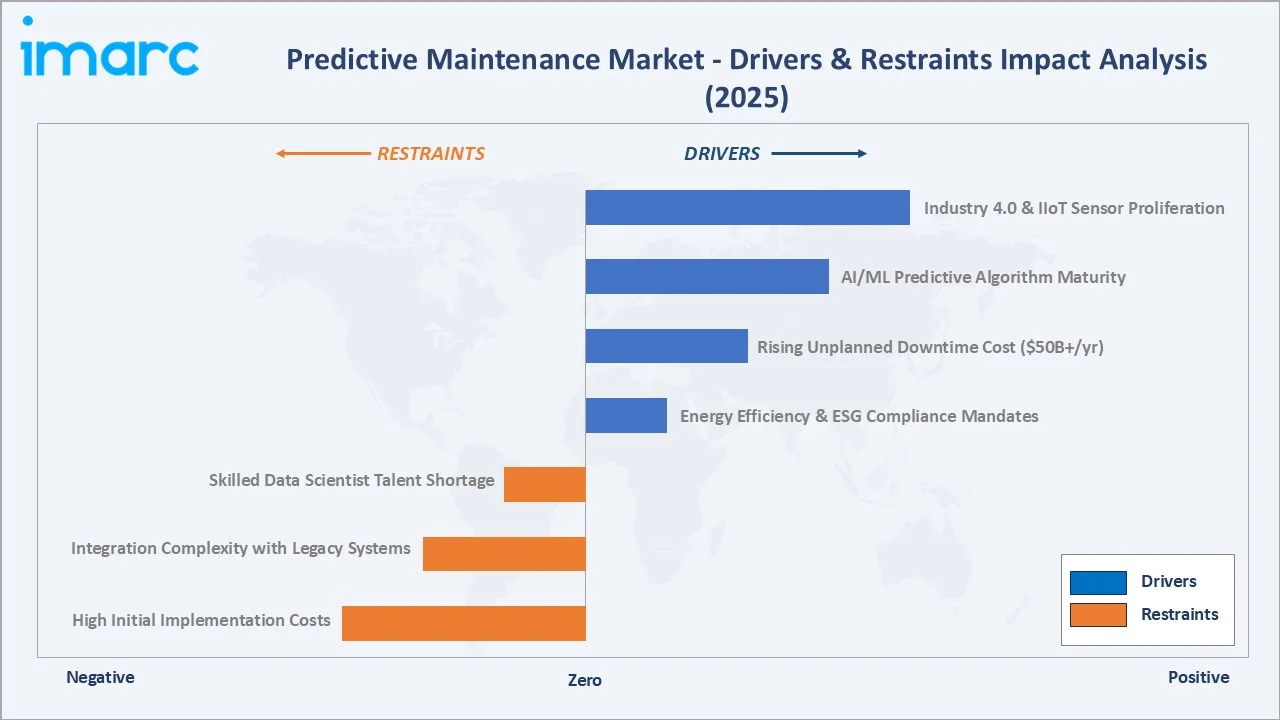

Market Drivers

- IIoT and Industry 4.0 Adoption Acceleration: The global IIoT market growth, with connected industrial devices generating the sensor data that predictive maintenance algorithms require. IIoT sensor shipments growth, with accelerometer, vibration, and thermal sensor costs falling below USD 5 per unit at volume, making pervasive equipment monitoring economically viable for the first time in manufacturing history.

- AI/ML Dramatically Reducing Unplanned Downtime Costs: Industrial unplanned downtime costs USD 260,000 per hour for large automotive plants and USD 2.5 million per hour for energy sector shutdowns. AI-powered PdM predicts bearing failures 3–6 weeks in advance, compressor fouling 1–2 weeks ahead, and electrical insulation degradation months before catastrophic failure.

- Energy Sector Digital Asset Management Expansion: The global renewable energy transition is creating new predictive maintenance demand at an extraordinary scale. Global wind turbine installed 117 GW of new capacity globally in 2024, with each turbine requiring maintenance spending.

Market Restraints

- High Initial Implementation and Integration Costs: A comprehensive PdM deployment for a 500-asset manufacturing plant requires premium investment encompassing sensors, IIoT gateways, software licensing, system integration, and change management. This capital barrier limits adoption among small manufacturers and emerging market industrial operators.

- Data Security and OT/IT Convergence Risk: Industrial control systems (ICS) and SCADA environments present critical cybersecurity attack surfaces when connected to PdM cloud platforms.

Market Opportunities

- Generative AI Enabling No-Code PdM for Non-Technical Users: Microsoft Copilot integrated with Azure IoT and IBM’s watsonx.ai are enabling maintenance engineers to build, deploy, and interpret predictive models through natural language interfaces without data science expertise.

- Digital Twin Integration Creating New Analytics Revenue: The convergence of predictive maintenance with digital twin technology, virtual replicas of physical assets that simulate equipment behavior under varying operating conditions, creates a new market category. Ansys Twin Builder, and GE Predix Digital Twin enable physics-based failure prediction that improves PdM accuracy for complex equipment including turbines, compressors, and CNC machines.

Market Challenges

- Model Accuracy Degradation and Concept Drift: PdM machine learning models trained on historical failure data degrade in accuracy over time as equipment ages, operating conditions change, and sensor wear affects data quality.

- Interoperability of Heterogeneous Industrial Systems: The average manufacturing plant operates equipment from 10–20 different OEMs using 5–10 different industrial communication protocols. Integrating these disparate data sources into a unified PdM analytics layer requires substantial middleware engineering and ongoing maintenance as firmware updates and equipment changes alter data schemas.

Emerging Market Trends

1. Generative AI Transforms PdM Accessibility and Insight Depth

Large language models integrated with industrial time-series data are enabling maintenance engineers to interrogate equipment health through conversational interfaces for the first time. By 2026, Gartner predicts 40% of enterprise apps will feature task-specific AI agents, reducing time-to-first-insight.

2. Digital Twin + PdM Convergence Creating Physics-Based Prediction

The fusion of physics-based simulation (digital twins) with data-driven machine learning is achieving prediction accuracy above 95% for complex rotating equipment. Siemens Xcelerator and Ansys Twin Builder generate synthetic failure data that trains ML models even for rare failure modes with limited historical examples.

3. Sustainability-Driven PdM as an ESG Metric

Predictive maintenance is increasingly recognized as an energy efficiency and sustainability tool, not merely a downtime reduction tool. Achieving 99.99% uptime through AI-driven predictive maintenance in manufacturing leads to a 15-20% decrease in energy consumption, as the most reliable machines are also the most energy-efficient.

5. PdM-as-a-Service (PdMaaS) Eliminating Upfront Barriers

Outcome-based pricing models, where PdM vendors charge per-downtime-hour-prevented rather than per software license, are emerging as the most disruptive commercial innovation in the market.

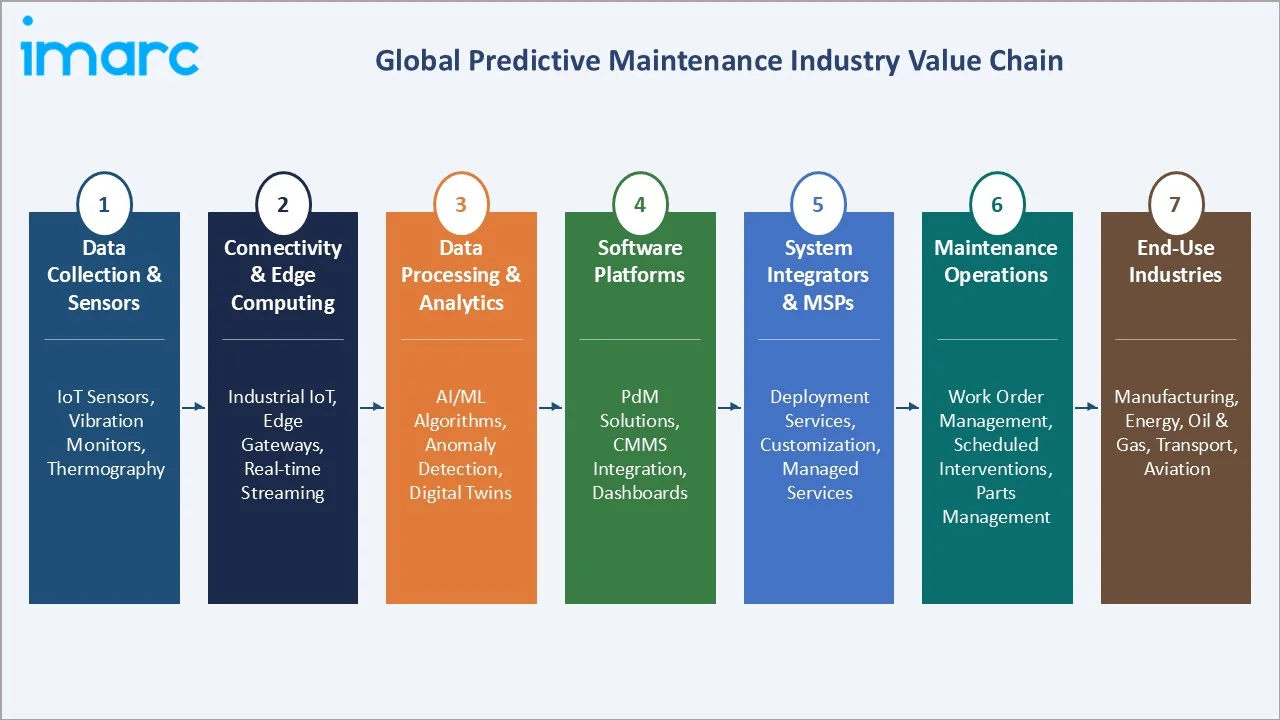

Industry Value Chain Analysis

The predictive maintenance value chain spans physical sensor hardware through cloud/edge compute infrastructure, AI analytics software, system integration services, and final enterprise deployment across industrial end-use verticals.

|

Stage |

Key Players & Examples |

|

Sensor & Data Collection |

MEMS sensors, vibration sensors, wireless sensor networks, precision vibration/pressure sensors |

|

Connectivity & Edge Layer |

Industrial networking, IIoT gateways, edge AI modules |

|

System Integration & Deployment |

Accenture (Industry X), Deloitte Digital, Capgemini Engineering, local industrial system integrators |

|

End-Use Industries |

Manufacturing, Energy & Utilities, Transportation, Healthcare, Aerospace & Defense |

The AI analytics and software layer captures the highest margins in the PdM value chain. Hardware providers achieve 35–55% gross margins on sensors. System integrators typically operate at 15–25% gross margins but drive the highest deal values.

Technology Landscape in the Predictive Maintenance Industry

Machine Learning and Deep Learning Algorithms

Modern PdM platforms deploy an ensemble of ML models for maximum accuracy. Long Short-Term Memory (LSTM) neural networks excel at time-series anomaly detection for continuous vibration and current data. Random Forests and Gradient Boosting (XGBoost) provide interpretable failure probability scores that maintenance teams can trust.

Digital Twin and Physics-Based Simulation Integration

Physics-informed neural networks (PINNs) embed thermodynamic, mechanical, and electrical physics equations as constraints within ML training, enabling accurate failure prediction even for equipment with limited historical failure data. Siemens’ Simcenter Digital Twin and ANSYS Twin Builder generate millions of simulated failure scenarios that augment real sensor data, solving the “data scarcity problem” for rare failure modes.

Generative AI and Large Language Model Integration

OpenAI GPT-4 integrated with Microsoft Azure IoT Timeseries Insights enables plain-language equipment health queries. AI can generate root cause analysis narratives from multivariate sensor anomaly patterns, translating complex ML model outputs into actionable maintenance work orders.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Solution | 61.8% | 2025 |

| Technique | Vibration Monitoring | 🔒 | 2025 |

| Deployment Type | On-premises | 57.3% | 2025 |

| Organization Size | Large Enterprises | 🔒 | 2025 |

| Industry Vertical | Manufacturing | 🔒 | 2025 |

| Region | North America | 38.9% | 2025 |

By Component

Solution dominates with 61.8% market share (2025). This encompasses software platforms, AI/ML analytics engines, digital twin applications, and dashboards/visualization tools. Cloud-native SaaS solutions are growing fastest within this segment, with annual subscription revenue growing at 28–32% versus 15–18% for perpetual license software.

Service at 38.2% encompasses system integration, consulting, training, and managed monitoring services, which are growing at ~22.3% CAGR through 2034, as enterprises outside core IIoT competency industries prefer outcome-based monitoring contracts over building internal PdM operations teams.

By Deployment Type

On-premises leads at 57.3% market share (2025). This reflects the installed base of large industrial enterprises, particularly in aerospace, defence, oil & gas, and utilities, that deployed PdM on private infrastructure under strict data sovereignty and cybersecurity policies.

Cloud-based at 42.7% is the fastest-growing deployment mode at ~24.5% CAGR through 2034. Microsoft Azure IoT, AWS Industrial IoT, and Google Cloud for Industrial each process hundreds of thousands of industrial equipment connections, providing elastic scalability that on-premises infrastructure cannot match. The shift to cloud accelerated dramatically when COVID-19 demonstrated the operational fragility of on-premises-only monitoring systems when IT staff could not physically access facilities.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.9% |

U.S. IIoT adoption in manufacturing, oil & gas industry unplanned downtime cost savings, hyperscaler AI infrastructure |

|

Asia-Pacific |

29.7% |

China Made in China 2025 smart factory program, Japan Society 5.0 industrial digitization, India PLI manufacturing scheme |

|

Europe |

21.6% |

Germany Industrie 4.0 factory digitization, EU machinery regulation requiring predictive safety systems |

|

Latin America |

5.6% |

Brazil oil & gas PdM for Petrobras assets, Mexico maquiladora factory automation, nearshoring manufacturing investment, driving plant digital upgrades |

|

Middle East and Africa |

4.2% |

Saudi Vision 2030 smart industrial city programs, UAE AI Strategy 2031 industrial applications, South Africa mining equipment PdM, GCC petrochemical plant maintenance |

North America’s 38.9% market dominance (2025) reflects the co-location of world-leading PdM software vendors, the world’s largest industrial capital expenditure market, and a regulatory environment that mandates predictive maintenance in aviation (FAA), defence (DoD CBM+), and nuclear power (NRC). The U.S. Bipartisan Infrastructure deal includes more than $62 Billion for the U.S. Department of Energy (DOE), specify digital asset management as a qualifying technology, creating government-funded demand at unprecedented scale.

Asia-Pacific’s 29.7% share (2025) and fastest growth trajectory through 2034 reflect Asia’s emergence as the world’s manufacturing heartland and an aggressive government-directed digital transformation agenda. Japan’s Society 5.0 and India’s PLI manufacturing scheme collectively create the regulatory and incentive conditions for the world’s largest near-term PdM market expansion.

Competitive Landscape

The global predictive maintenance market exhibits moderate concentration at the platform tier, with Microsoft, IBM, and GE collectively accounting for approximately 35-40% of total market revenue.

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Microsoft Corporation |

Microsoft Azure |

Market Leader |

World’s leading industrial IoT cloud platform, Azure Digital Twins for predictive asset modelling |

|

IBM Corporation |

IBM Maximo Application Suite |

Market Leader |

IBM Maximo Application Suite is the world’s #1 enterprise asset management platform |

|

GE Vernova |

SmartSignal |

Strong Challenger |

Proficy is a process analytics suite; GE Vernova wind turbine predictive maintenance |

|

|

Vertex AI |

Strong Challenger |

Vertex AI AutoML for PdM model development; Google Cloud for industrial |

|

PTC |

ServiceMax AI |

Established |

ThingWorx is a top-3 IIoT platform by revenue, strong aerospace and automotive vertical presence |

|

C3.ai Inc. |

C3 AI Asset Performance Suite |

Growth Challenger |

Purpose-built enterprise AI application for PdM, fastest time-to-value proposition |

The broader competitive landscape is highly fragmented below the top tier, with specialist vendors competing across industry verticals, equipment types, and deployment models. Competition is driven by AI model accuracy, deployment speed, platform integration breadth, vertical domain expertise, and total cost of ownership.

Key Company Profiles

Microsoft Corporation

Microsoft is one of the global leaders in cloud-based predictive maintenance infrastructure through its Azure platform for industrial applications.

- Product Portfolio: Microsoft Azure

- Recent Developments: Launched Azure IoT Operations, unified cloud-edge PdM architecture.

- Strategic Focus: Copilot-powered natural language PdM interface democratization; Azure IoT Operations as unified OT/IT convergence platform; partner ecosystem (Siemens, Litmus, Rockwell Automation) for global deployment scale; sustainability-linked PdM as energy efficiency metrics for enterprise ESG reporting.

IBM Corporation

IBM is one of the world’s largest enterprise asset management and predictive maintenance software vendors, with IBM Maximo Application Suite.

- Product Portfolio: IBM Maximo Application Suite.

- Recent Developments: Launched Maximo Application Suite 9.0 with generative AI work order generation.

- Strategic Focus: Maximo + watsonx.ai convergence as generative AI PdM platform; U.S. and European defence/aerospace maintenance modernization; sustainability-linked maintenance analytics for Scope 1 reduction; hybrid cloud PdM bridging on-premises legacy and cloud-native architectures.

GE Vernova

GE Vernova (energy technology) operates the world’s most domain-specialized predictive maintenance platforms for power generation.

- Product Portfolio: Proficy CSense, SmartSignal.

- Recent Developments: In March 2024, GE Vernova announced that it will supply its advanced predictive analytics software to National Industrialization Company (TASNEE). GE Vernova will integrate its SmartSignal software into TASNEE's existing Asset Performance Management (APM) system, helping to reduce downtime and enhance operational efficiency.

- Strategic Focus: Renewable energy PdM as primary growth driver under energy transition; AI-powered performance optimization beyond failure prevention; energy efficiency and emissions monitoring as PdM service extension.

C3.ai Inc.

C3.ai is a pure-play enterprise AI company with predictive maintenance as its flagship application, positioning itself as the technology-neutral AI layer that connects to any existing industrial data infrastructure.

- Product Portfolio: C3 AI Asset Performance Suite.

- Recent Developments: In October 2024, C3 AI announced the newly re-branded C3 AI Asset Performance Suite, which includes C3 AI Reliability, C3 AI Process Optimization, and C3 AI Energy Management.

- Strategic Focus: Generative AI as primary differentiation versus IBM and Microsoft; outcome-based pricing model for risk-averse enterprise customers; U.S. federal government (DoD, DOE) as strategic revenue anchor; ecosystem partnerships with AWS, Microsoft, and Google for go-to-market leverage against self-build competition.

Market Concentration Analysis

The global predictive maintenance market exhibits moderate-to-high concentration at the platform tier and high fragmentation in the broader ecosystem. Microsoft, IBM, and GE collectively generate an estimated USD 6–7 Billion in annual PdM-related revenue, representing approximately 40–45% of the 2025 total market. The top six companies’ combined share of 55–65% is moderately concentrated by industrial software standards.

Below the top tier, the market is highly fragmented with specialist vendors serving specific verticals, specific geographies, or specific technical niches. This fragmentation creates ongoing M&A opportunities as large platforms seek to acquire domain expertise or vertical-specific customer bases. Consolidation will accelerate significantly between 2026 and 2030 as generalist AI platforms extend native PdM capabilities, pressuring specialist pure-play vendors to either achieve sufficient scale or exit through acquisition.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud-based deployment (CAGR ~24.5%), Service component (CAGR ~22.3%), and SME-targeted subscription platforms (CAGR ~28–32%) represent the three highest-growth investment vectors. Generative AI-powered PdM, the emerging intersection of LLMs and industrial sensor data, is growing from a 2024 base, representing the most asymmetric investment opportunity in the market.

Emerging Markets

India’s smart manufacturing under PLI schemes, Southeast Asia’s industrial FDI surge, and Middle East energy asset digitization under Vision 2030 collectively represent an incremental PdM opportunity through 2030 that current market leaders are underserving. Local language AI capabilities, sovereign cloud deployment options, and affordable SME-oriented pricing are the three critical enablers for capturing these emerging market opportunities.

Venture Investment Trends

PdM and industrial AI attracted venture investment globally, with edge AI, industrial digital twins, and outcome-based PdM platforms leading subsegment allocation.

- Key investment themes: Edge AI inference chips, digital twin PdM platforms, outcome-based service models, vertical-specialist PdM for energy transition assets (EV batteries, wind turbines), and generative AI maintenance interfaces.

- Government-directed investment: U.S. Department of Energy Advanced Manufacturing Office, EU Horizon Europe, and Japan NEDO allocated investments for industrial AI and PdM research, creating a pipeline of pre-commercial technologies that will drive the next generation of market offerings.

Future Market Outlook (2026-2034)

The global predictive maintenance market is positioned for transformational growth through 2034. From USD 15.60 Billion in 2025, the market is forecast to reach USD 91.04 Billion by 2034, an absolute value addition of USD 75.4 Billion at a 21.01% CAGR. This trajectory represents one of the most powerful secular growth stories in all of industrial technology, compelled by three irreversible drivers: over USD 1 trillion global unplanned downtime cost problem that PdM directly addresses; the AI revolution making expert-level failure prediction accessible to non-specialist users for the first time.

Between 2026 and 2030, the defining transformation will be the generative AI integration across all major PdM platforms. The 2030-2034 period will be defined by autonomous self-healing industrial systems where PdM transitions from “predict and alert” to “predict and act.” AI-integrated maintenance execution systems will automatically generate work orders, reserve spare parts, schedule maintenance windows, and in some cases trigger automated robotic maintenance procedures, all without human intervention.

Research Methodology

Primary Research

Primary research encompassed structured interviews with 150+ industry stakeholders in 2025, including PdM software product executives, industrial IoT technology managers, maintenance engineering directors, operations technology (OT) cybersecurity specialists, and industrial AI investors. Geographies covered included North America, Europe, Japan, China, India, and the Middle East. Primary insights validated platform market share estimates, deployment model preferences, and emerging technology adoption timelines.

Secondary Research

Secondary research encompassed company annual reports and earnings call transcripts, IDC and Gartner industrial IoT and AI market data, McKinsey Manufacturing Analytics research, Deloitte industrial downtime cost studies, patent filing databases, and government industrial policy documents (U.S. CHIPS Act, EU Machinery Regulation, China Made in China 2025, India PLI). Over 310 secondary sources were reviewed and synthesized.

Forecasting Models

Market size forecasts were developed using a bottom-up demand aggregation validated against top-down methodology. Key inputs include global industrial capex forecasts, IIoT sensor shipment data, cloud computing price curves, AI adoption S-curves by industry vertical, and government industrial digitization program timelines.

Predictive Maintenance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Solution, Service |

| Techniques Covered | Vibration Monitoring, Electrical Testing, Oil Analysis, Ultrasonic Leak Detectors, Shock Pulse, Infrared, Others |

| Deployment Types Covered | Cloud-based, On-premises |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Industry Verticals Covered | Manufacturing, Energy and Utilities, Aerospace and Defense, Transportation and Logistics, Government, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Microsoft Corporation, IBM Corporation, GE Vernova, Google, PTC, C3.ai Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the predictive maintenance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global predictive maintenance market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the predictive maintenance industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Predictive Maintenance Market Report

The global predictive maintenance market was valued at USD 15.60 Billion in 2025 and is projected to reach USD 91.04 Billion by 2034, growing at a CAGR of 21.01%.

North America leads with 38.9% revenue share (2025), anchored by U.S. tech vendors, DoD CBM+ mandate, and the world’s largest industrial capex market.

Solution dominates with 61.8% share (2025), encompassing AI/ML software platforms, digital twin applications, and analytics dashboards generating high-margin recurring subscription revenue.

Cloud-based deployment is fastest growing at ~24.5% CAGR, as SMEs and mid-market manufacturers adopt subscription PdM without upfront infrastructure investment through Azure, AWS, and Google Cloud.

Key market players include Microsoft Corporation, IBM Corporation, GE Vernova, Google, PTC, and C3.ai Inc.

Key drivers include IIoT sensor democratization, AI reducing 30-50% of unplanned downtime, cloud PdM-as-a-service for SMEs, energy transition asset monitoring needs, and generative AI making PdM accessible to non-technical users.

PdM reduces unplanned downtime by 30–50%, extends equipment life by 20–40%, and cuts overall maintenance costs by 10–25% versus time-based maintenance, delivering 12–24 month ROI payback.

Key trends include generative AI natural language interfaces, edge AI for offline operation, digital twin physics-based prediction, ESG-linked energy efficiency monitoring, and outcome-based PdMaaS pricing models.

Key challenges include high initial integration costs, OT cybersecurity risk when connecting to cloud, ML model accuracy degradation (concept drift), and shortage of engineers combining data science with industrial physics knowledge.

Asia-Pacific holds 29.7% market share (2025) and is the fastest growing region at ~24.5% CAGR, driven by China Made in China 2025, Japan Society 5.0, and India PLI manufacturing digitization mandates.

Top opportunities include edge AI PdM chips, digital twin platforms, generative AI maintenance interfaces, SME subscription platforms, energy transition asset monitoring, and outcome-based PdM service contracts.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)