Pan Masala Market in India Size, Share, Trends and Forecast by Type, Price, Packaging, and State, 2026-2034

Pan Masala Market in India Size, Share, Trends & Forecast (2026-2034)

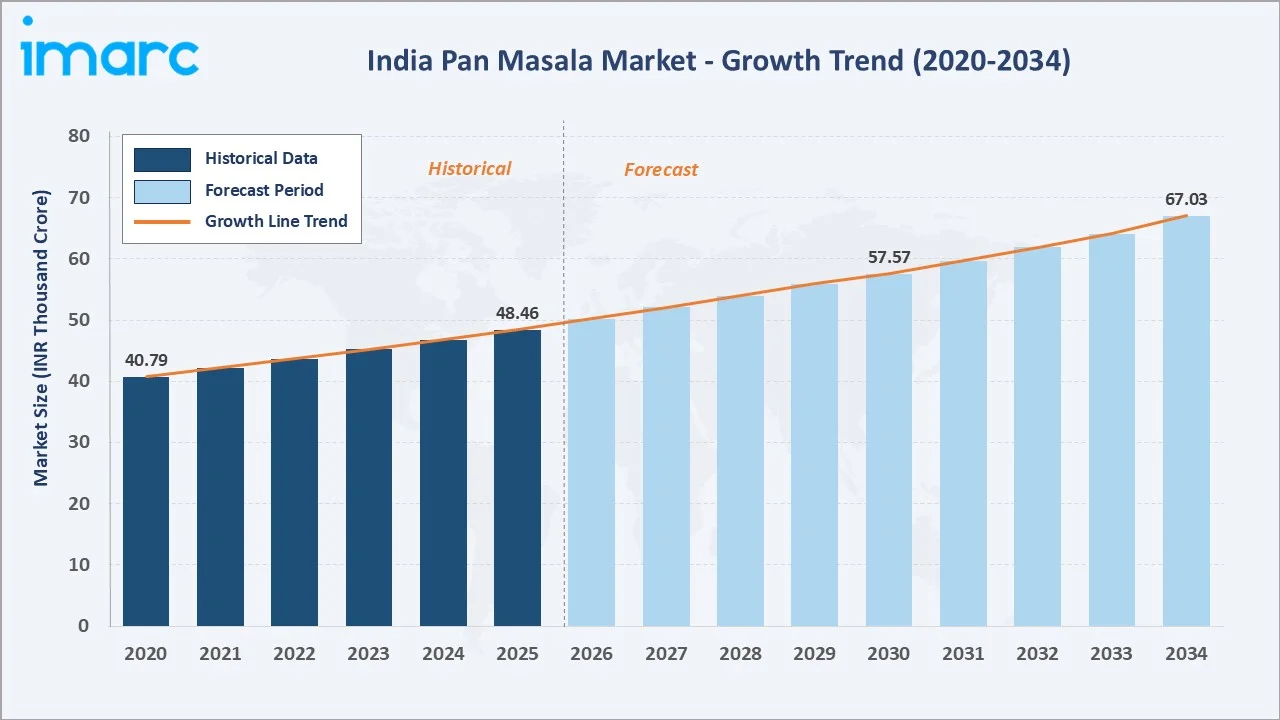

The pan masala market in India size reached INR 48.46 Thousand Crore in 2025 and is projected to reach INR 67.03 Thousand Crore by 2034, exhibiting a CAGR of 3.51% during 2026-2034. Rising consumer disposable incomes, expansion of retail and e-commerce networks, and growing demand for innovative flavoured variants are the primary growth drivers.

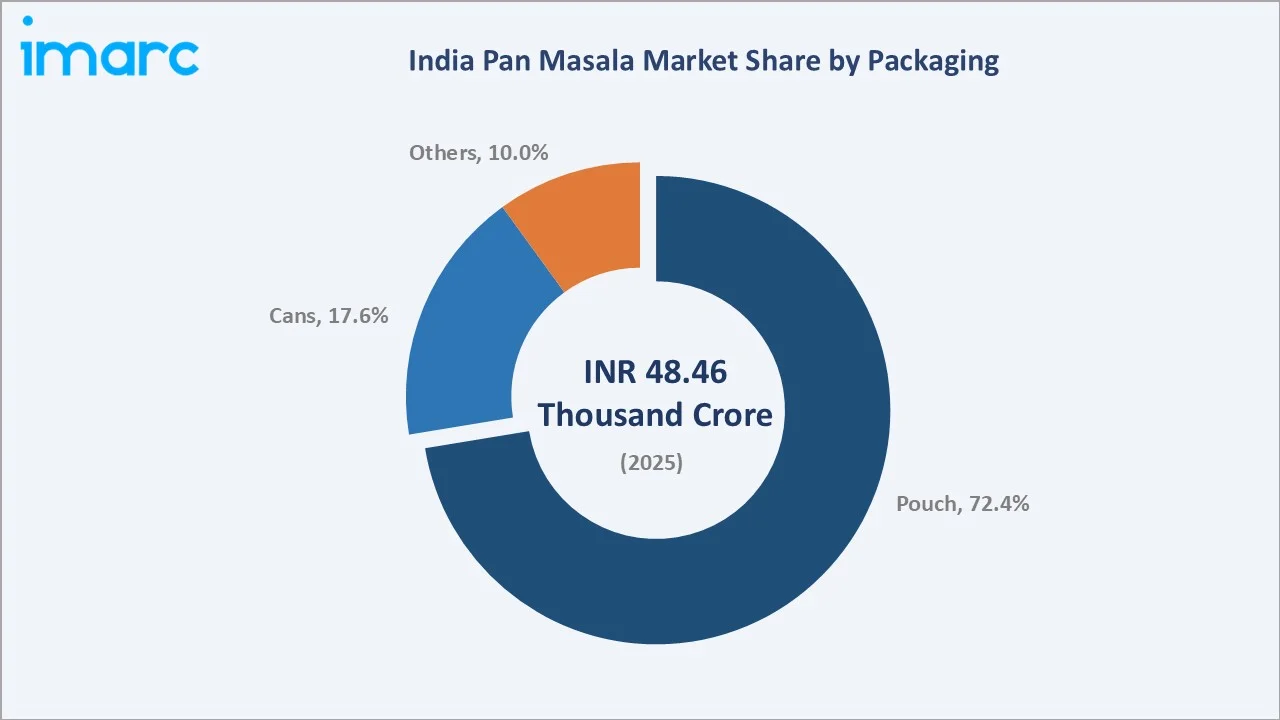

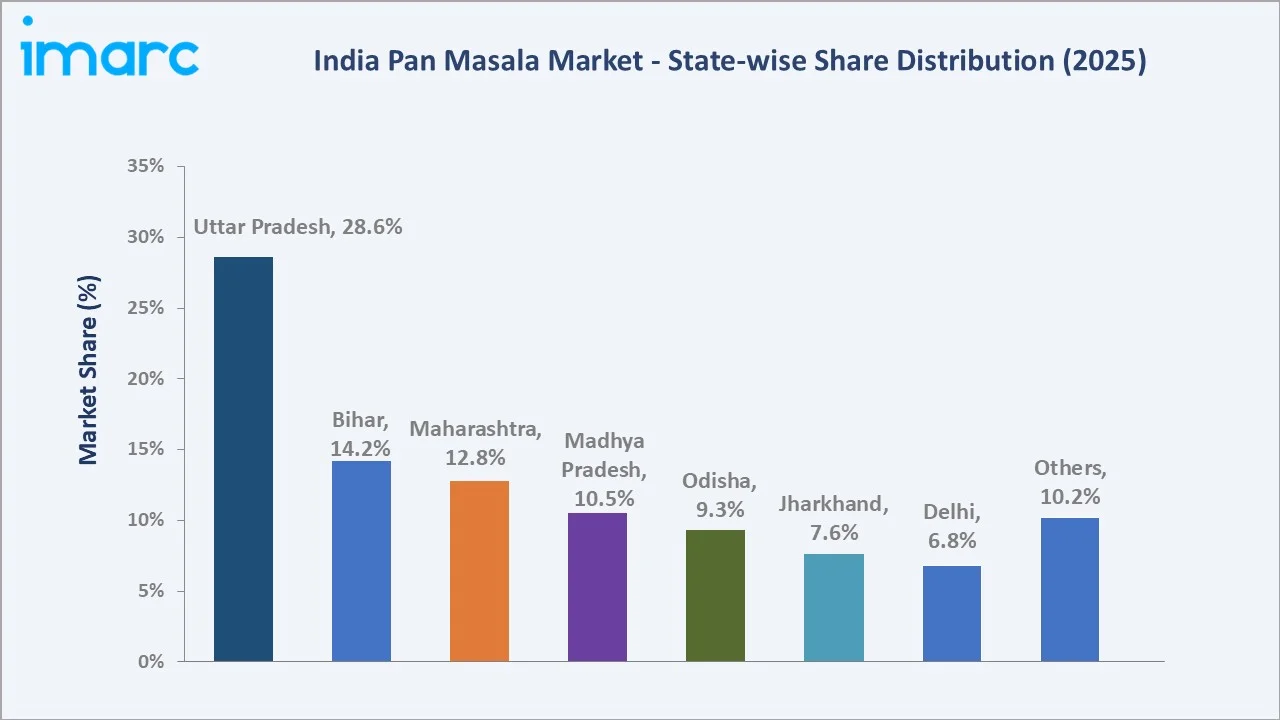

Pouch packaging dominates at 72.4% and Uttar Pradesh commands 28.6% state-level share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 48.46 Thousand Crore |

|

Forecast Market Size (2034) |

INR 67.03 Thousand Crore |

|

CAGR (2026-2034) |

3.51% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Uttar Pradesh (28.6% share, 2025) |

|

Leading Packaging |

Pouch (72.4%, 2025) |

|

Leading Price Segment |

Non-Premium (68.9%, 2025) |

The pan masala market in India growth trajectory from 2020 through 2034, with historical expansion to INR 48.46 Thousand Crore in 2025, reflects consistent demand driven by cultural relevance and distribution expansion, while the forecast to INR 67.03 Thousand Crore captures accelerating premiumisation, flavour innovation, and rural market penetration.

To get more information on this market, Request Sample

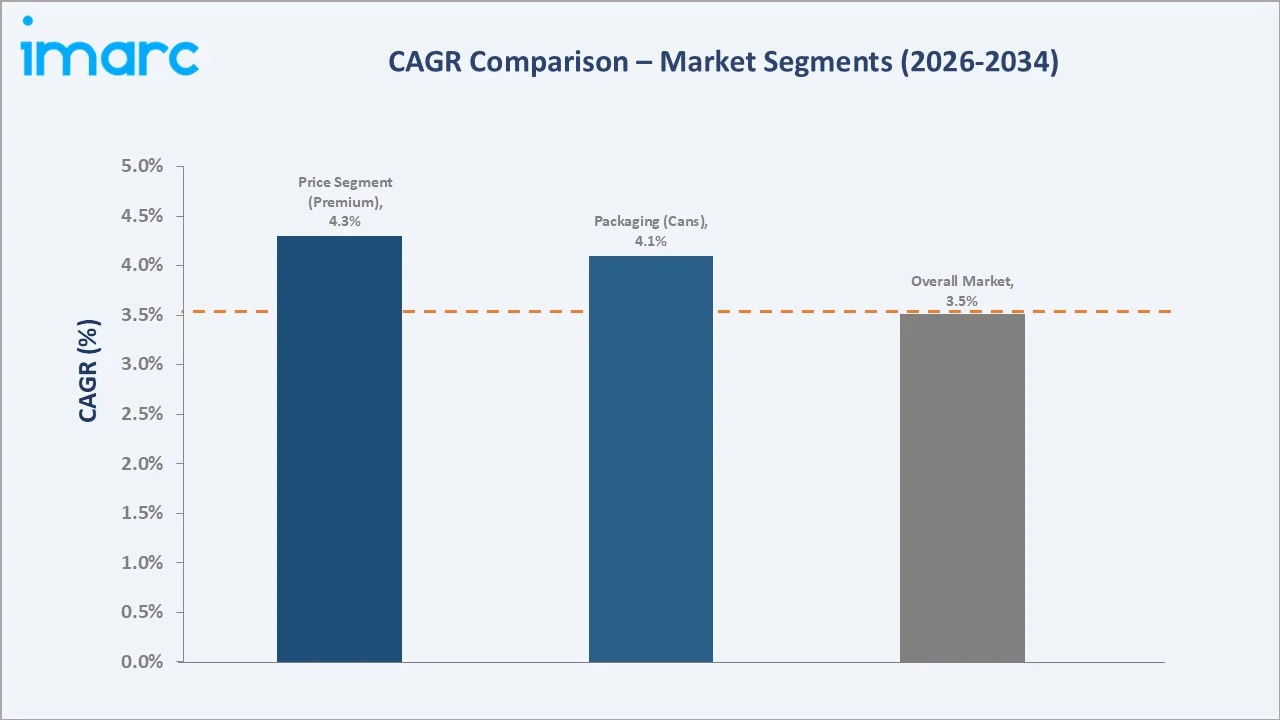

The CAGR trajectories across key packaging, price, and regional sub-segments, with Premium segment at ~4.3% CAGR and Cans packaging at ~4.1% CAGR, are the fastest-growing categories within the India pan masala industry analysis through 2034.

Executive Summary

The pan masala market in India is on a sustained growth trajectory from INR 48.46 Thousand Crore in 2025 to INR 67.03 Thousand Crore by 2034. Pan masala, a ready-made chewing alternative for traditional paan served as a mouth freshener, benefits from deep cultural significance and broad demographic appeal across India.

Pouch packaging dominates at 72.4% in 2025, owing to its convenience, affordability, and suitability for impulse purchases at kirana stores and paan shops. Cans (17.6%) command premium positioning in gifting and social occasion segments.

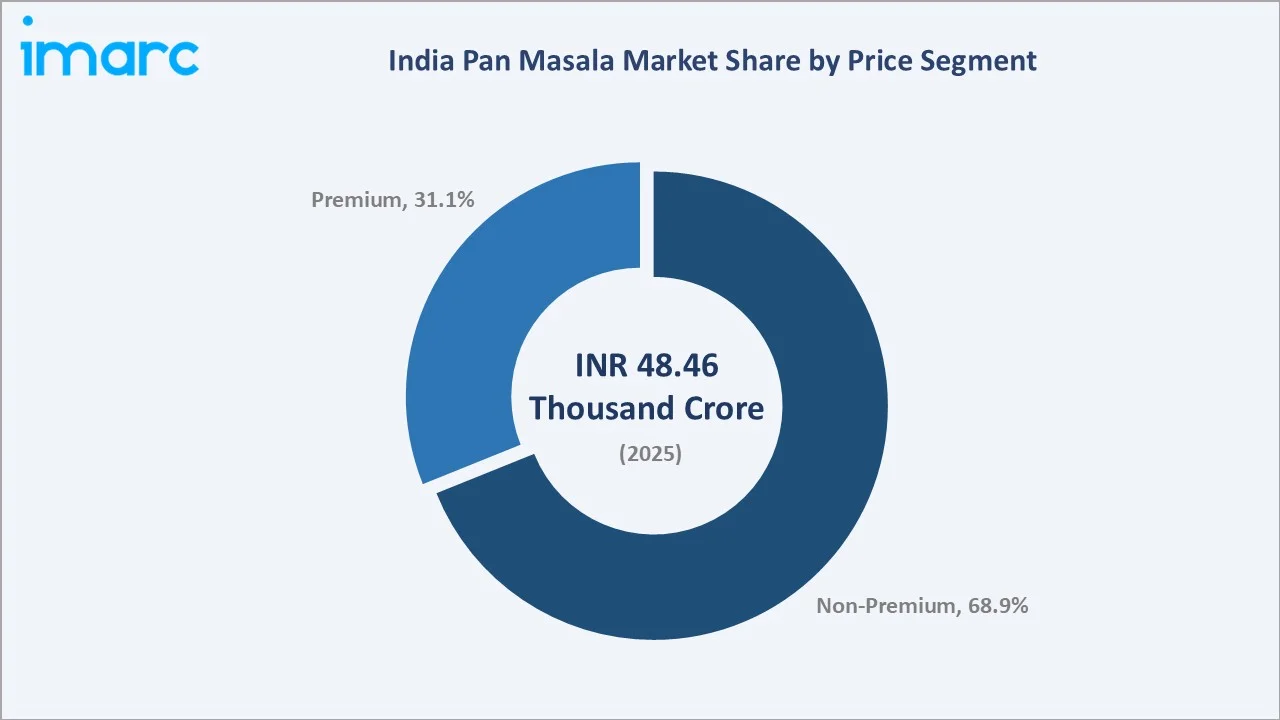

Non-Premium leads at 68.9% reflecting pan masala's mass-market appeal, while Premium (31.1%) grows faster driven by product innovation.

Uttar Pradesh dominates at 28.6% in 2025, reflecting the state's position as both the largest consumer market and a major manufacturing hub. Bihar (14.2%) and Maharashtra (12.8%) follow as key regional markets with strong cultural and demographic drivers.

Key Market Insights

|

Insight |

Data |

|

Largest Packaging Segment |

Pouch — 72.4% share (2025) |

|

Second Packaging Segment |

Cans — 17.6% share (2025) |

|

Leading Price Segment |

Non-Premium — 68.9% share (2025) |

|

Premium Segment |

Premium — 31.1% share (2025) |

|

Leading Region |

Uttar Pradesh — 28.6% share (2025) |

|

Second Largest Region |

Bihar — 14.2% share (2025) |

|

Top Companies |

Dinesh Pouches Private Ltd, DS Group, Manikchand Group, Red Rose Group of Companies, Shikhar Group |

Key Analytical Observations Expanding On The Above Data:

- Pouch packaging, with 72.4% in 2025, dominates because of its low unit price points enabling impulse purchases, ideal product freshness preservation, and compatibility with mass-market distribution through kirana stores, paan shops, and roadside vendors across all geographies.

- Non-Premium segment, with 68.9% in 2025, leads because of pan masala's traditionally mass-market positioning and broad rural consumption base across lower-income demographics in North and Central Indian states.

- Uttar Pradesh's 28.6% dominance in 2025 reflects multiple structural forces: largest state population in India, deep-rooted cultural tradition of pan masala consumption, well-established manufacturing clusters, and extensive distribution networks.

- Bihar, with 14.2% in 2025, benefits from rising disposable incomes, expanding retail infrastructure, and strong cultural affinity for pan masala across both urban and rural demographics.

Pan Masala Market in India Overview

Pan masala is a traditional Indian chewable product consisting of areca nut, slaked lime, catechu, cardamom, mint, saffron, rose petals, and various flavouring and perfuming agents. It is widely consumed as a mouth freshener after meals and during social gatherings, holding deep cultural significance across North, Central, and Eastern India.

The Indian ecosystem integrates raw material suppliers, pan masala manufacturers, packaging material providers, national and regional distributors, organised retail chains, kirana stores, and diverse end-use consumer segments spanning urban, semi-urban, and rural demographics.

Market Dynamics

To evaluate market opportunities, Request Sample

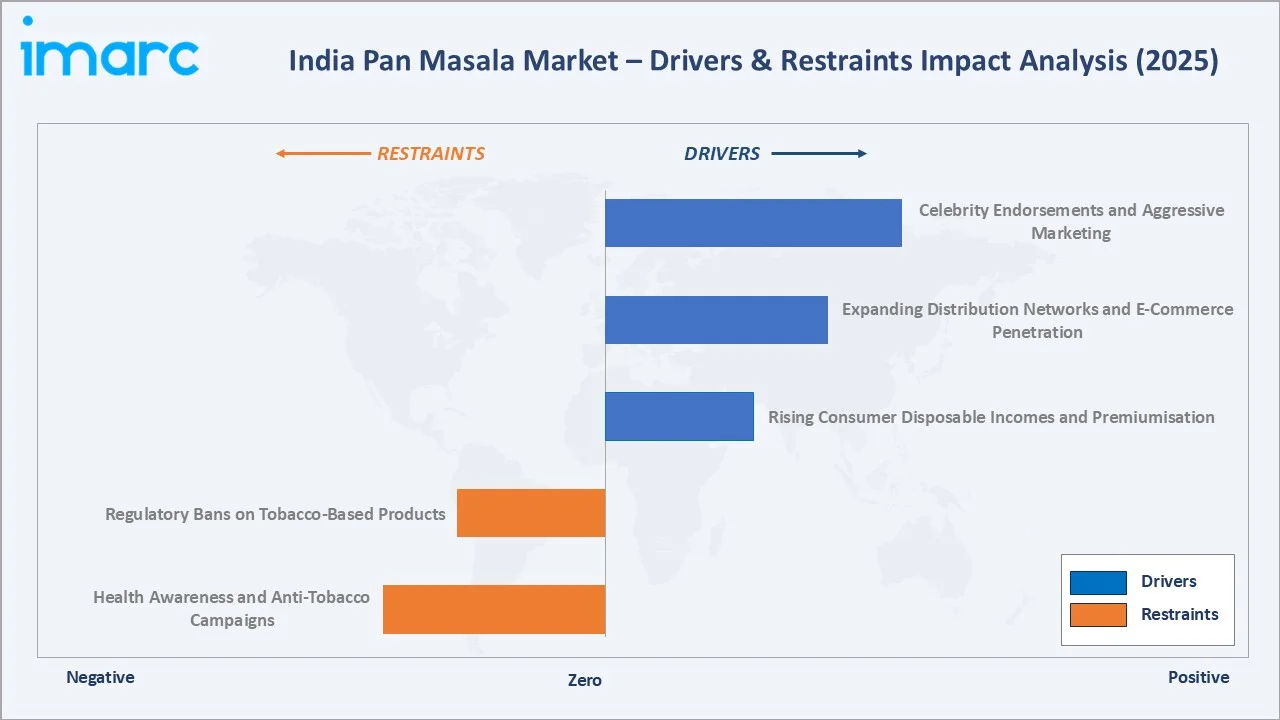

Market Drivers

- Rising Consumer Disposable Incomes and Premiumisation: India's GDP per capita growth and expanding middle class are enabling broader consumption of premium pan masala variants. Premium product launches targeting aspirational urban consumers have demonstrated strong initial sales uptake across organised retail channels.

- Expanding Distribution Networks and E-Commerce Penetration: Rapid multiplication of kirana stores, convenience outlets, and e-commerce platforms has significantly improved product accessibility across Tier-2, Tier-3 cities and rural markets, driving strong volume growth for established national brands.

- Celebrity Endorsements and Aggressive Marketing: High-profile endorsements by Bollywood and cricket celebrities have created aspirational brand appeal for pan masala brands, particularly among younger consumers in semi-urban markets seeking aspirational lifestyle associations.

Market Restraints

- Regulatory Bans on Tobacco-Based Products: Multiple state-level bans on gutkha and tobacco-containing pan masala under the Food Safety and Standards Act have forced manufacturers to pivot toward plain and flavoured non-tobacco variants, disrupting existing revenue streams and distribution networks.

- Health Awareness and Anti-Tobacco Campaigns: Growing consumer awareness about health risks associated with areca nut and tobacco consumption, driven by government campaigns and NGO activities, is moderating growth in traditional pan masala categories across urban and educated demographics.

Market Opportunities

- Herbal and Tobacco-Free Variants Innovation: Regulatory pressure toward non-tobacco products is creating a large innovation opportunity in herbal, vitamin-enriched, and functional mouth freshener categories, with manufacturers launching cardamom, saffron, and gulkand-based products for health-conscious consumers.

- Export Market Expansion to Indian Diaspora: An estimated 35 million Indian diaspora across Gulf countries, United Kingdom, United States, Canada, Southeast Asia, and other countries represents a large, culturally aligned export opportunity for established pan masala brands with strong heritage recognition.

Market Challenges

- Raw Material Price Volatility: Areca nut prices are subject to seasonal fluctuations and supply disruptions, with production variability in Karnataka and Assam directly impacting manufacturing cost structures across all pan masala producers throughout the year.

- Unorganised Sector Competition: A substantial proportion of the Indian pan masala market is served by unorganised regional manufacturers operating outside formal regulatory frameworks, creating significant and persistent pricing pressure on organised branded players.

Emerging Market Trends

1. Tobacco-Free and Herbal Variant Innovation

The regulatory crackdown on tobacco-based pan masala is accelerating innovation in herbal, vitamin C enriched, and functional mouth freshener categories. Manufacturers are incorporating cardamom, saffron, gulkand, rose, and silver-coated betel nut formulations to offer health-conscious alternatives that retain cultural appeal.

2. Premium Packaging and Gifting Segment Growth

Premium packaging formats including tin boxes, decorative jars, and gift-wrap pouches are gaining traction in urban markets and diaspora gifting. Premium silver-coated and saffron-enriched variants are capturing high-value consumers willing to pay significant premiums for differentiated pan masala products.

3. E-Commerce and Quick Commerce Distribution

Pan masala brands are increasingly leveraging quick commerce platforms to reach urban consumers seeking convenient home delivery. E-commerce penetration is enabling brands to bypass traditional distributor margins and directly engage with premium segment customers in metropolitan areas.

4. Flavour Innovation Targeting Youth Consumers

Chocolate, pineapple, blueberry, and exotic fruit-infused pan masala variants are being introduced to attract younger demographics. These innovations expand pan masala's consumer base beyond traditional adult male consumers to younger urban populations seeking novel sensory experiences.

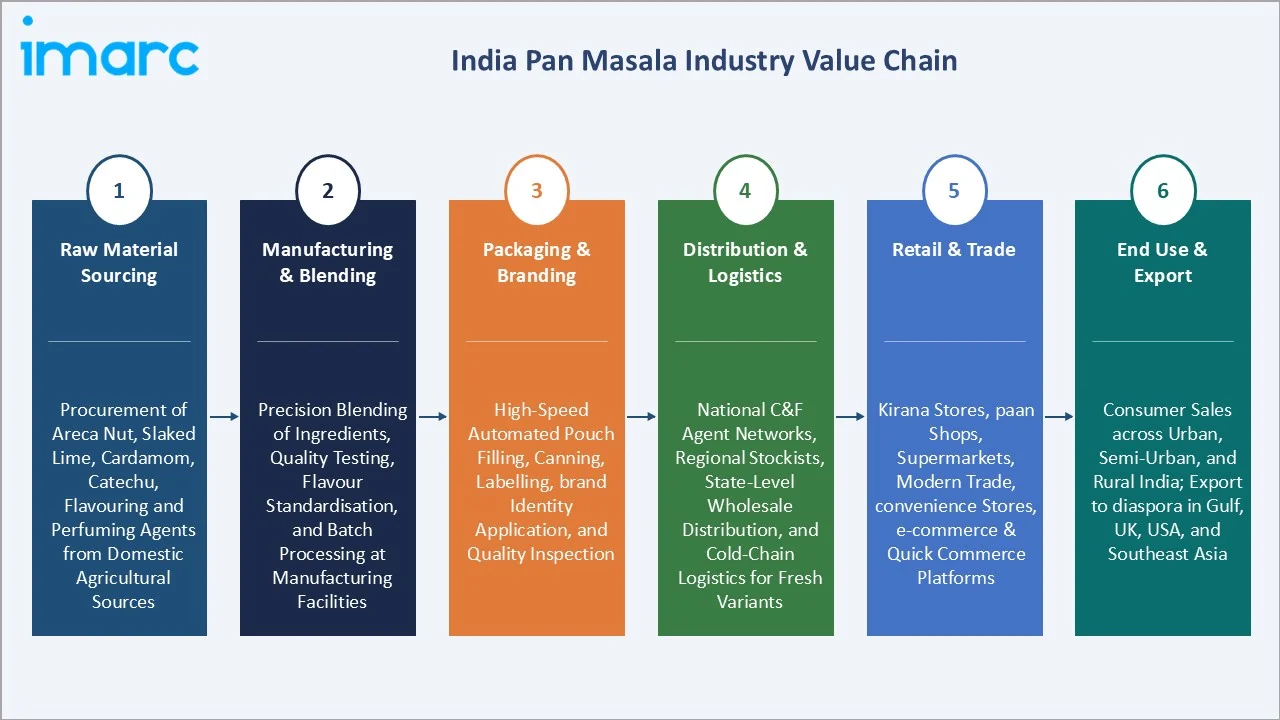

Industry Value Chain Analysis

The pan masala value chain spans six stages from raw material procurement through end-use consumption. Manufacturing and branding capture the highest value-add margins, while distribution logistics and last-mile penetration generate significant competitive differentiation among well-established market players.

|

Stage |

Key Activities / Examples |

|

Raw Material Sourcing |

Procurement of areca nut, slaked lime, cardamom, catechu, flavouring & perfuming agents from domestic agricultural sources |

|

Manufacturing & Blending |

Precision blending of ingredients, quality testing, flavour standardisation, and batch processing at manufacturing facilities |

|

Packaging & Branding |

High-speed automated pouch filling, canning operations, labelling, brand identity application, and quality inspection |

|

Distribution & Logistics |

National C&F agent networks, regional stockists, state-level wholesale distribution, and cold-chain logistics for fresh variants |

|

Retail & Trade |

Kirana stores, paan shops, supermarkets, modern trade outlets, convenience stores, and e-commerce & quick commerce platforms |

|

End Use & Export |

Direct consumer sales across urban, semi-urban, and rural India; export to Indian diaspora in Gulf, UK, USA, and Southeast Asia |

Vertically integrated manufacturers with captive raw material sourcing, in-house blending, quality control, and proprietary distribution networks achieve lower cost structures than manufacturers relying on external procurement. This vertical integration represents a meaningful competitive advantage in commodity market segments where price competition is intense.

Technology Landscape in the Pan Masala Industry

High-Speed Automated Sachet Packaging Technology

Advanced multi-lane vertical form-fill-seal (VFFS) machines capable of producing 1,500-2,000 pouches per minute are being adopted by leading manufacturers to reduce per-unit packaging costs. Automated weight-filling and nitrogen-flush sealing systems ensure consistent product quantity and extend shelf life across high-volume production runs.

Quality Control and Flavour Standardisation Technology

Gas chromatography-mass spectrometry (GC-MS) and near-infrared (NIR) spectroscopy are being deployed for real-time quality monitoring of raw material batches and finished product consistency. These analytical technologies ensure uniform flavour profiles across manufacturing batches and multiple production facilities nationwide.

Vacuum Sealing and Freshness Preservation Innovation

Nitrogen-flush packaging and advanced vacuum-sealing technologies are extending product shelf life from 6-9 months to 12-18 months, enabling pan masala manufacturers to expand confidently into export markets and modern organised retail channels that require extended shelf stability and superior freshness standards.

Digital Supply Chain and Traceability Systems

Leading pan masala manufacturers are adopting ERP-integrated digital supply chain platforms to improve raw material traceability, batch quality documentation, and distributor inventory management. RFID-enabled packaging and QR-code-based consumer authentication systems are being piloted to combat counterfeit products and build direct consumer engagement.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Pan Masala with Tobacco | 🔒 | 2025 |

| Price | Non-Premium | 68.9% | 2025 |

| Packaging | Pouch | 72.4% | 2025 |

| State | Uttar Pradesh | 28.6% | 2025 |

By Packaging

Pouch packaging commands a 72.4% majority share in 2025 owing to its fundamental cost-competitiveness and broad compatibility with impulse purchase behaviour at kirana stores, paan shops, and street-level retail. The low unit price of pouch SKUs drives very high transaction volumes across mass-market consumer segments in all geographies.

To access detailed market analysis, Request Sample

Cans packaging at 17.6% in 2025, growing fastest, represents the premium end of pan masala packaging, providing superior freshness preservation, extended shelf life, and perceived quality signals that justify premium pricing. Others (10.0%) serve gifting, institutional, and specialty retail applications where unique presentation is valued.

By Price Segment

Non-Premium pan masala commands a 68.9% majority share in 2025, reflecting the product category's historically mass-market positioning and broad rural and semi-urban consumption base. Non-Premium variants priced below INR 5-15 per sachet drive most transaction volumes across traditional trade channels.

Premium pan masala at 31.1% in 2025, growing at ~4.3% CAGR, is irreplaceable in gifting, social occasion, and urban modern retail segments where product quality, packaging aesthetics, and brand cachet are primary purchase drivers. Rising urban middle class and diaspora export demand are structural growth catalysts for the premium segment through 2034.

Regional Market Insights

|

State |

Share (2025) |

Key Growth Drivers |

|

Uttar Pradesh |

28.6% |

Largest consumer base; deep cultural tradition; established manufacturing clusters |

|

Bihar |

14.2% |

Rising disposable incomes; expanding retail penetration; strong demand growth |

|

Maharashtra |

12.8% |

Urban consumption; premium segment traction; organised retail expansion |

|

Madhya Pradesh |

10.5% |

Semi-urban demand growth; traditional consumption patterns; improving distribution |

|

Odisha |

9.3% |

Growing consumer awareness; improving logistics and supply chain networks |

|

Jharkhand |

7.6% |

Expanding industrial workforce; rising FMCG penetration in Tier-2 cities |

|

Delhi |

6.8% |

Premium and flavoured variant preference; high per-capita consumption |

|

Others |

10.2% |

Tamil Nadu, Gujarat, Rajasthan, West Bengal and other states with untapped potential |

Uttar Pradesh's 28.6% market dominance in 2025 is driven by the most structurally advantageous combination of population scale, cultural tradition, and manufacturing infrastructure in any Indian state. The state's dual role as a major consumer market and manufacturing hub creates integrated competitive advantages for locally established players.

Bihar, with 14.2% in 2025, is experiencing a pronounced growth trajectory fuelled by rising FMCG penetration, expanding retail infrastructure, and improving rural incomes. The state's large population base and strong cultural affinity for pan masala provide a structurally supportive demand environment for sustained volume expansion.

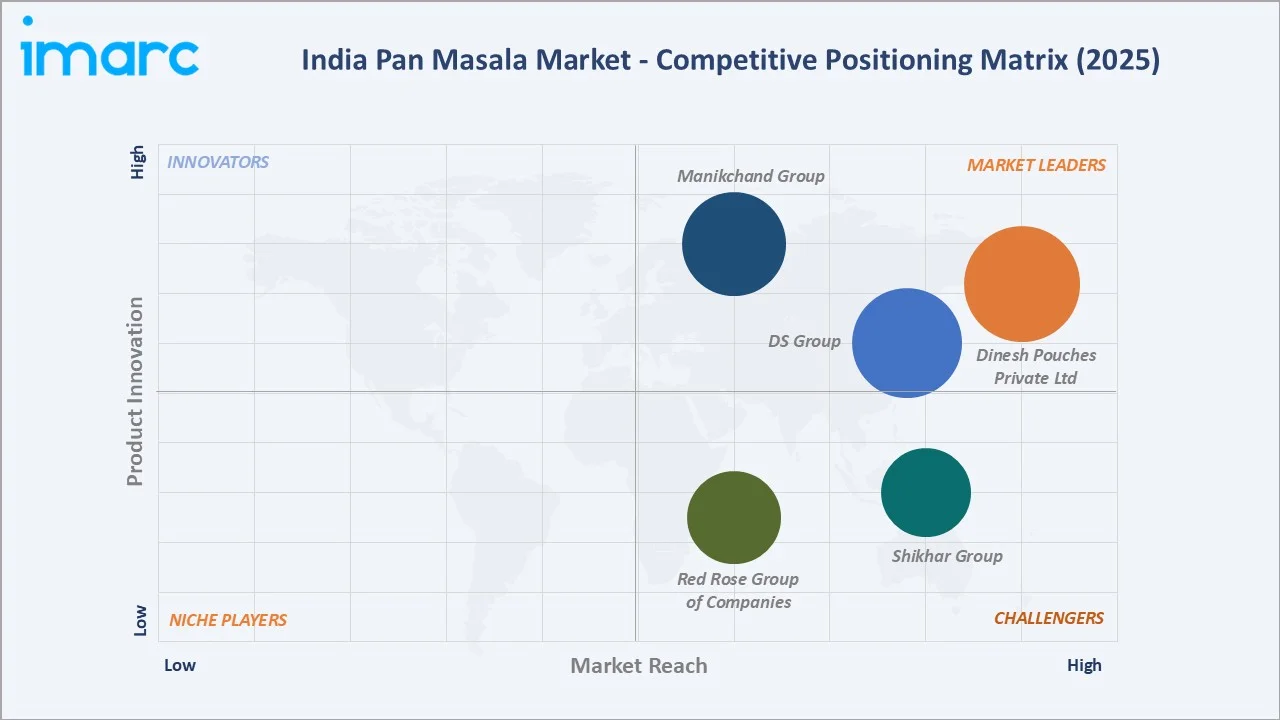

Competitive Landscape

The pan masala market in India is moderately fragmented at the national level, with regional leaders holding strong positions in home states while several large national brands compete across multiple geographies.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Dinesh Pouches Private Ltd |

2100, Royal King |

Leader |

West India dominance; Rajasthan & Gujarat stronghold; proprietary flavour blends |

|

DS Group |

Rajnigandha Pan Masala, Rajnigandha Saffron Pan Masala, Tansen Supreme, Mastaba |

Leader |

National pan-India leader; premium portfolio; celebrity-driven marketing |

|

Manikchand Group |

RMD - pan masala, Manikchand Pan Masala |

Leader |

Maharashtra & Central India dominance; mass-market positioning; wide distribution |

|

Red Rose Group of Companies |

24 Carat Pan Masala, Boss Zafrani Pan Masala, Boss Pan Masala, Pehla Nasha Pan Masala, RR 1000 Pan Masala, RR Gold Pan Masala and RR Premium Pan Masala |

Challenger |

South India stronghold; affordable pricing; rural market penetration |

|

Shikhar Group |

Shikhar Pan Masala |

Challenger |

Cost-competitive; gradually building premium variants |

Key players include Dinesh Pouches Private Ltd, DS Group, Manikchand Group, Red Rose Group of Companies, Shikhar Group, and others.

Key Company Profiles

DS Group

DS Group is a diversified Indian conglomerate headquartered in Noida, operating across tobacco, pan masala, confectionery, agro-forestry, and hospitality sectors. In pan masala, the company is the undisputed national leader through its flagship Rajnigandha brand.

- Product Portfolio: Rajnigandha Pan Masala, Rajnigandha Saffron Pan Masala, Tansen Supreme, Mastaba, and others.

- Recent Developments: In July 2025, DS Group launched a new TVC for its flagship brand Rajnigandha, centered around the theme ‘Yun hi nahin main Rajnigandha ban jaata hun,’ which emphasizes the effort and craftsmanship behind the product. The campaign highlights the meticulous process of sourcing high-quality ingredients and blending them to achieve a premium mouth freshener experience, reinforcing the brand’s legacy of excellence.

- Strategic Focus: DS Group's strategy leverages its vertically integrated supply chain and premium brand positioning to maintain national market leadership while expanding its non-tobacco and herbal portfolio to comply with evolving regulatory frameworks.

Manikchand Group

Manikchand Group is one of India's largest pan masala and tobacco manufacturers, headquartered in Pune, Maharashtra. The company is known for its RMD and Manikchand Pan Masala brands with particularly strong positioning in Maharashtra, Uttar Pradesh, and Central India.

- Product Portfolio: RMD Pan Masala and Manikchand Pan Masala

- Strategic Focus: Manikchand's strategy focuses on mass-market volume leadership through cost-competitive pricing, extensive kirana distribution, and consistent quality, while selectively investing in premium variants for urban upgrade consumers.

Dinesh Pouches Private Limited

Dinesh Pouches Private Limited is a Rajasthan-based pan masala manufacturer known for its flagship 2100 brand launched in 1993. The company holds a strong consumer franchise across Rajasthan, Gujarat, and Western India through its proprietary flavour blends.

- Product Portfolio: 2100, Royal King, and others

- Strategic Focus: Dinesh Pouches differentiates on unique proprietary flavour blends and premium ingredient sourcing with strong regional brand loyalty in Western India, while gradually building national distribution.

Market Concentration Analysis

The pan masala market in India is moderately fragmented at the national level, with no single company holding more than 15-18% of total market revenue. The organised sector competes alongside a significant unorganised segment of regional manufacturers operating across Tier-2 and Tier-3 cities.

Consolidation at the regional level is more advanced than national consolidation suggests. National brands with strong celebrity-driven recognition hold disproportionate value share in urban and premium markets. National consolidation through brand acquisitions and distribution partnerships is occurring among mid-tier regional players seeking scale.

Investment & Growth Opportunities

Fastest-Growing Segments

Premium pan masala at ~4.3% CAGR through 2034 is the highest-growth price segment, driven by urban middle-class premiumisation and gifting applications. Cans packaging growing at ~4.1% CAGR represents the fastest-growing format, driven by premium product association and superior freshness preservation performance.

Emerging Markets

Bihar and Jharkhand at ~3.6-3.8% CAGR are the fastest-growing state markets through 2034. Improving rural incomes, expanding retail infrastructure, and growing FMCG penetration are creating significant volume expansion opportunities for established national brands entering these underpenetrated markets.

Venture & Investment Trends

Private equity interest in consolidating fragmented regional pan masala markets is growing within India's broader consumer FMCG sector. Export market development targeting the 32-million Indian diaspora across Gulf countries and Southeast Asia represents a capital-efficient expansion opportunity for heritage brands with strong NRI community recognition.

Future Market Outlook (2026-2034)

The pan masala market in India is forecast to expand from INR 48.46 Thousand Crore in 2025 to INR 67.03 Thousand Crore by 2034 at a CAGR of 3.51%, adding approximately INR 18,578 Crore in incremental annual market value over the forecast period. This consistent growth reflects the market's culturally embedded, recurring demand characteristics.

Three structural forces will most significantly shape the landscape through 2034: the regulatory transition toward tobacco-free products redirecting innovation into herbal categories; premiumisation driven by urban middle-class income growth expanding the Premium segment share; and export market development to Indian diaspora communities creating new revenue streams for national brands.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024-2025 with pan masala industry stakeholders, including senior commercial managers at leading manufacturers, FMCG distribution professionals, retail channel experts, and consumer research specialists. Primary data validated market sizing, segment shares, and state-level demand estimates.

Secondary Research

Key secondary sources include FSSAI regulatory publications, Indian FMCG industry association data, state-level excise department publications, Consumer Affairs Ministry reports, Nielsen India FMCG panel data, and trade publications covering India's food and beverage sector.

Forecasting Models

Market size estimations were derived using a combination of top-down and bottom-up forecasting models incorporating GDP growth rates, per-capita consumption indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for regulatory uncertainty.

Pan Masala Market in India Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Thousand Crores |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Pan Masala with Tobacco, Plain Pan Masala, Flavored Pan Masala, Others |

| Prices Covered | Premium, Non-Premium |

| Packagings Covered | Pouch, Cans, Others |

| States Covered | Uttar Pradesh, Bihar, Maharashtra, Madhya Pradesh, Odisha, Jharkhand, Delhi, Others |

| Companies Covered | Dinesh Pouches Private Ltd, DS Group, Manikchand Group, Red Rose Group of Companies, Shikhar Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pan masala market in India from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the pan masala market in India.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pan masala industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Indian Pan Masala Market Report

The pan masala market in India reached INR 48.46 Thousand Crore in 2025, reflecting consistent demand from cultural relevance, rising disposable incomes, and expanding retail distribution networks across urban and rural India.

The market is projected to reach INR 67.03 Thousand Crore by 2034, growing at a CAGR of 3.51% during 2026-2034, driven by premiumisation, flavour innovation, regulatory-driven shift toward tobacco-free variants, and export market development.

Pouch packaging leads with a 72.4% market share in 2025, owing to low unit price points enabling impulse purchasing, superior freshness preservation, and broad compatibility with kirana store and paan shop distribution channels.

Non-Premium pan masala dominates with a 68.9% share in 2025, reflecting the category's historically mass-market positioning. The Premium segment at 31.1% is growing faster at ~4.3% CAGR, driven by urban middle-class premiumisation trends.

Uttar Pradesh is the largest state market, commanding a 28.6% share in 2025, supported by India's largest state population, deep-rooted cultural traditions of pan masala consumption, and established manufacturing and distribution infrastructure.

The key players in the pan masala market in India include Dinesh Pouches Private Ltd, DS Group, Manikchand Group, Red Rose Group of Companies, Shikhar Group, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)