Process Analyzer Market Size, Share, Trends and Forecast by Product Type, End Use Industry, and Region, 2026-2034

Process Analyzer Market Size, Share, Trends & Forecast (2026-2034)

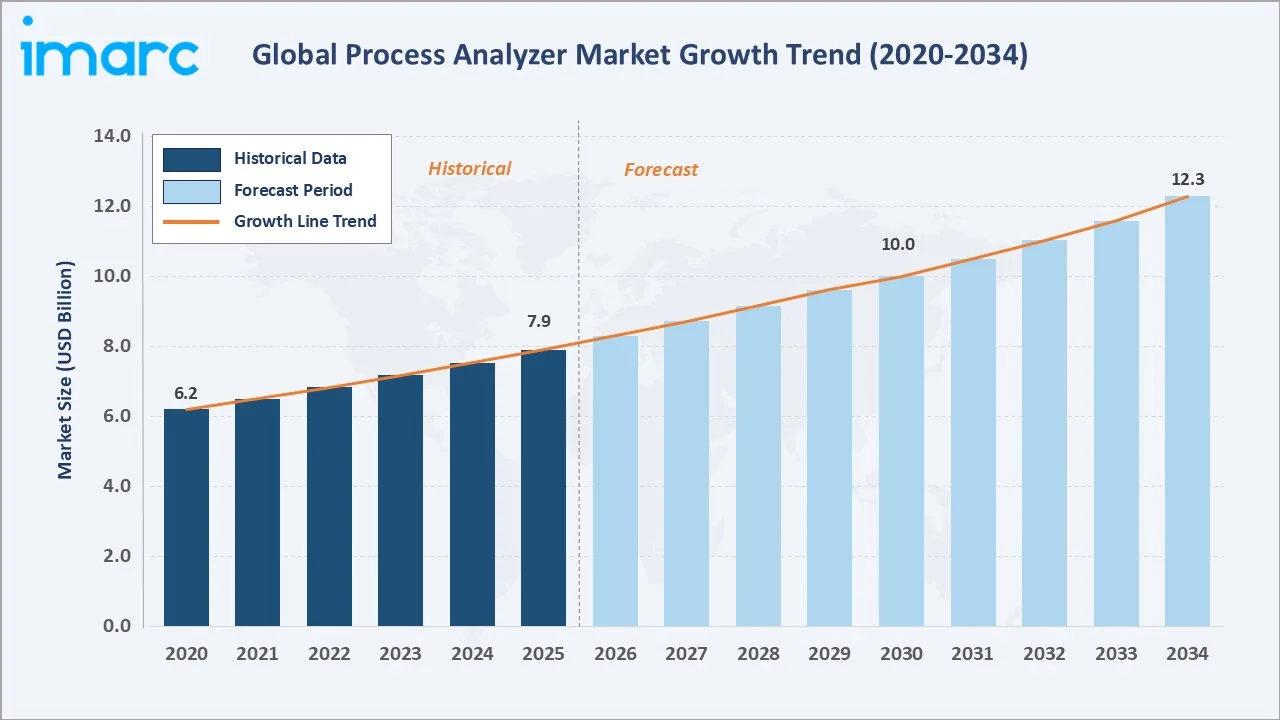

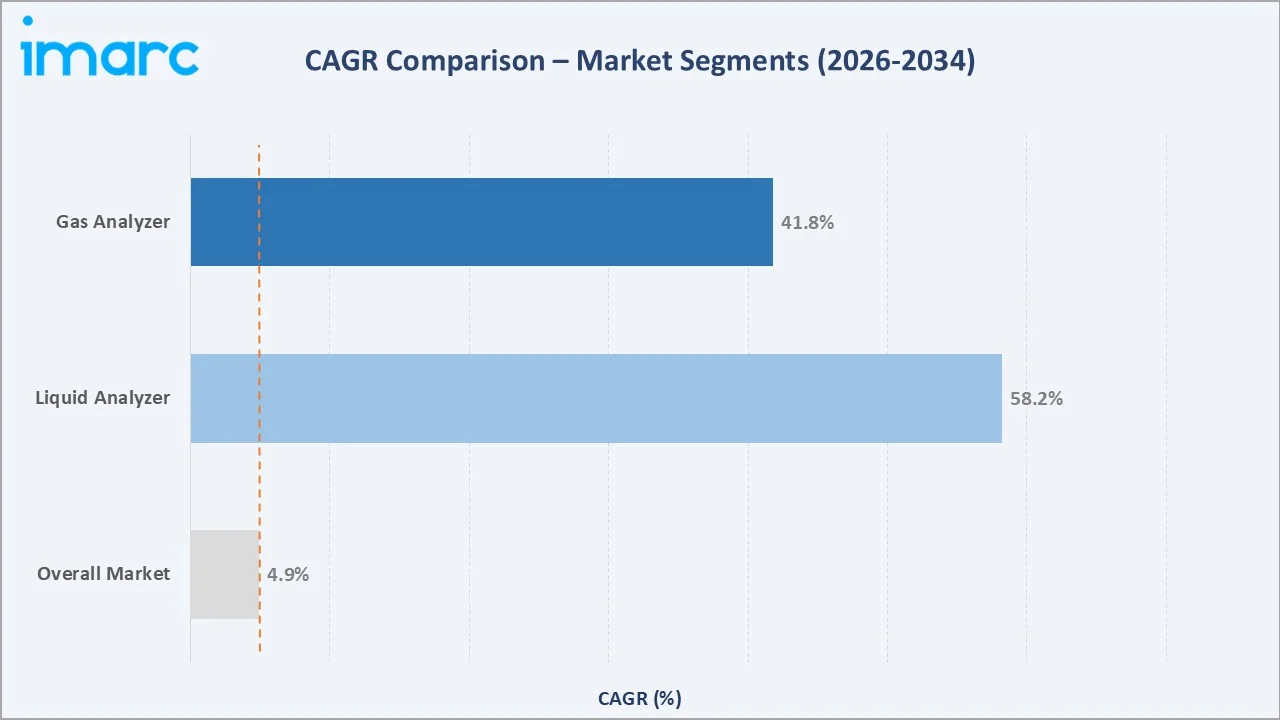

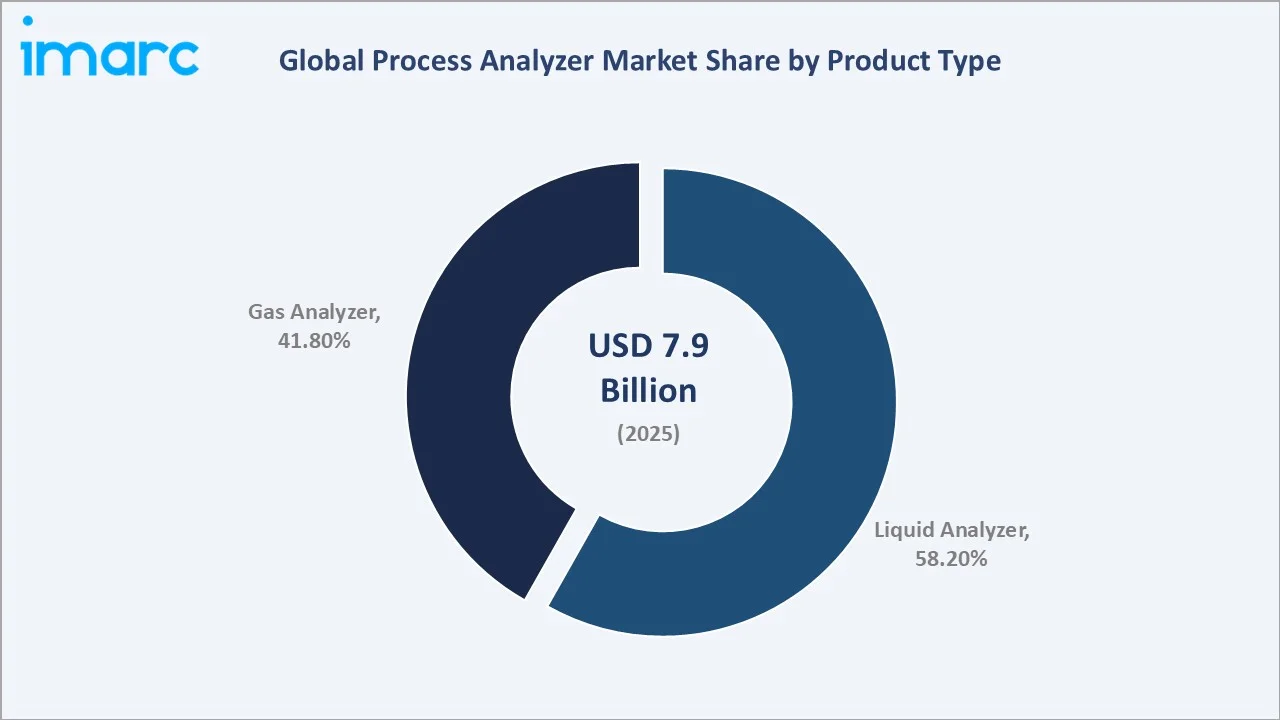

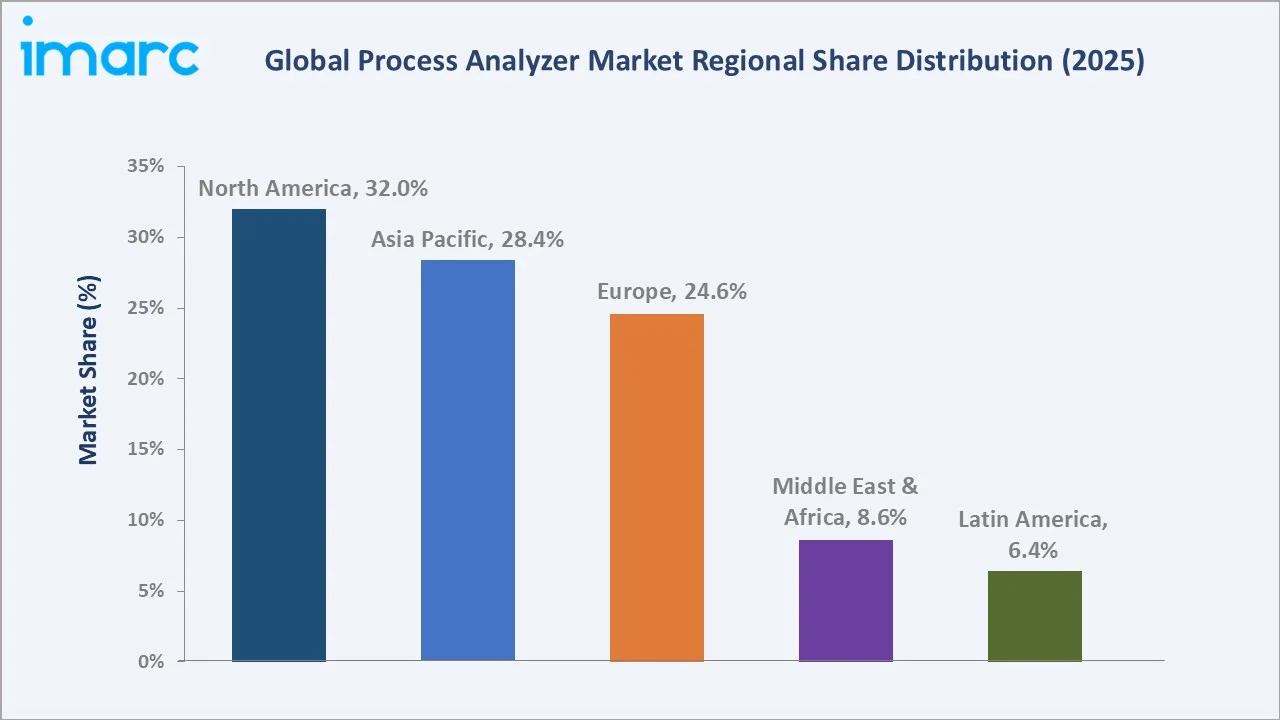

The global process analyzer market was valued at USD 7.9 Billion in 2025 and is projected to reach USD 12.3 Billion by 2034, registering a CAGR of 4.9% during the forecast period 2026-2034. Growing demand for real-time process monitoring across power generation, chemical processing, oil and gas, and water treatment industries is the primary engine of this expansion. Liquid analyzers held the dominant 58.2% share in 2025, while North America led regional demand at 32.0%. Rising regulatory compliance requirements and the accelerating adoption of Industry 4.0 technologies are expected to sustain robust market momentum through 2034.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.9 Billion |

|

Market Size (2030) |

USD 10.0 Billion |

|

Forecast Market Size (2034) |

USD 12.3 Billion |

|

CAGR (2026-2034) |

4.9% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Product Segment |

Liquid Analyzer (58.2%, 2025) |

|

Largest End-Use (Liquid) |

Power (20.0%, 2025) |

|

Largest Region |

North America (32.0%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

To get more information on this market, Request Sample

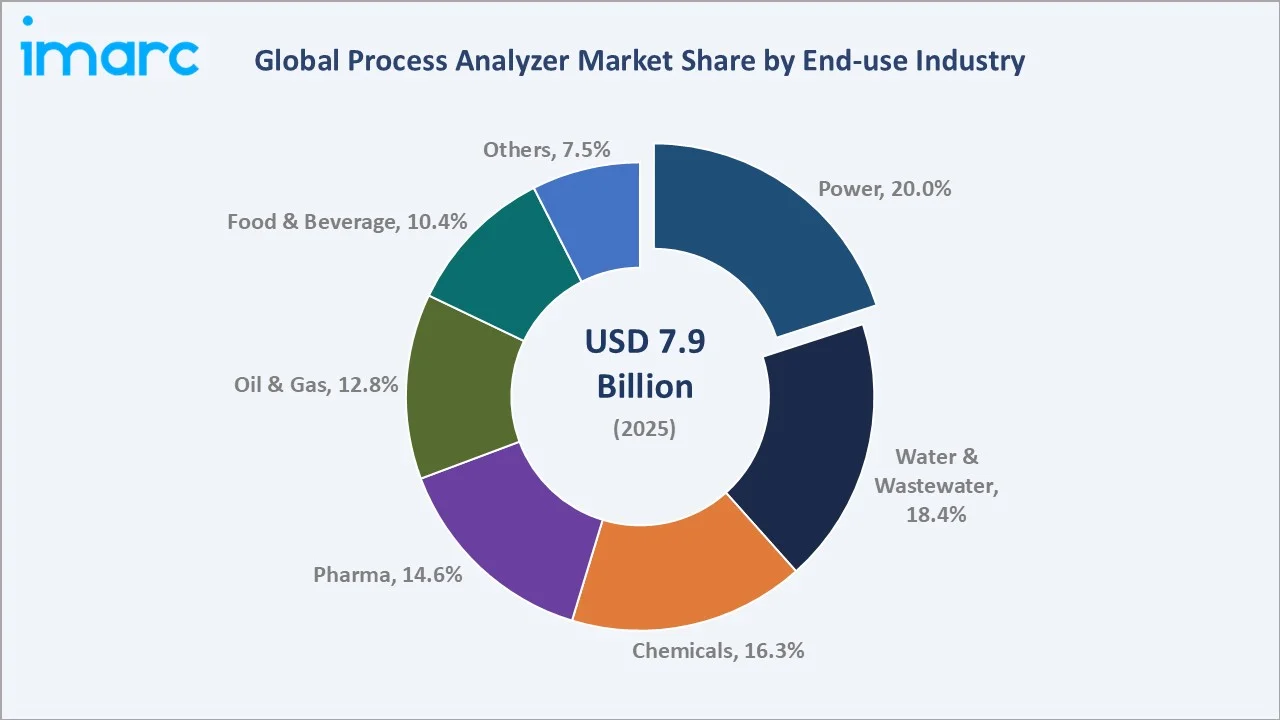

The analyzer market is evolving with increasing demand for real-time monitoring and process optimization across industries, led by liquid analyzers holding a 58.2% share. Within this segment, the power sector dominates with 20.0%, supported by the need for efficient water and emission management systems.

Executive Summary

The global process analyzer market recorded a value of USD 6.2 billion in 2020 and advanced to USD 7.9 billion by 2025, reflecting steady compound annual growth. The market is set to accelerate further, reaching USD 12.3 billion by 2034, driven by rising industrialization, stringent environmental norms, and the widespread integration of automation in process industries.

North America dominated the market in 2025 with a 32.0% share, underpinned by mature refining infrastructure, and robust regulatory frameworks. Key investment corridors include water and wastewater treatment, power generation, and pharmaceutical quality assurance.

Technology evolution - particularly tunable diode laser (TDL) spectroscopy, wireless connectivity, and cloud-based analytics - is reshaping the competitive landscape. The market outlook for 2026-2034 remains favorable, with increased capex in industrial decarbonization and smart plant initiatives creating incremental demand across all end-use segments.

Key Market Insights

|

Insight |

Data |

|

Market Size (2025) |

USD 7.9 Billion |

|

Largest Product Segment |

Liquid Analyzer – 58.2% share (2025) |

|

Largest End-Use (Liquid Analyzer) |

Power – 20.0% share (2025) |

|

Leading Region |

North America – 32.0% share (2025) |

|

Fastest Growing Region |

Asia Pacific (28.4% share, 2025) |

|

CAGR (Forecast Period) |

4.9% (2026-2034) |

|

Top Companies |

ABB Group, Honeywell International Inc, Siemens AG, Emerson Electric Co., Endress+Hauser AG |

|

Key Market Opportunity |

Smart manufacturing & IIoT-enabled inline analytics |

Key Highlights from the Process Analyzer Market Intelligence Study:

- Liquid Analyzer Dominance (58.2%, 2025): Liquid analyzers hold the majority revenue share due to their critical role in water quality monitoring, pharmaceutical batch control, and chemical process optimization. pH analyzers, conductivity meters, and dissolved oxygen sensors are the highest-volume sub-types.

- Power Sector Leads Liquid Analyzer End-Use (20.0%, 2025): The power generation sector's reliance on water chemistry control to protect boiler and turbine systems drives the highest demand for liquid analyzers. Strict water treatment standards in thermal and nuclear plants sustain steady procurement cycles.

- North America at USD ~2.5 billion (2025): The U.S. and Canada together represent approximately USD 2.5 billion of the global market, supported by heavy industrial investment, EPA compliance mandates, and a high density of oil and gas refining infrastructure.

- Asia Pacific – High-Growth Corridor: With industrial output expanding rapidly across China (the world's largest chemical producer) and India (doubling refining capacity), Asia Pacific is projected to record the highest incremental demand through 2034.

- Pharmaceuticals & Food Safety Driving New Demand: Rising global health standards and food safety regulations are accelerating liquid analyzer adoption for continuous quality monitoring in pharmaceutical manufacturing and food and beverage processing.

- Digital Transformation as a Catalyst: Integration of AI-driven anomaly detection, remote diagnostics, and SCADA-linked process analyzers is shortening maintenance cycles and increasing overall equipment utilization – a core growth catalyst expected through 2034.

Global Process Analyzer Market Overview

The global process analyzer market was valued at USD 7.9 billion in 2025 and is projected to reach USD 12.3 billion by 2034, registering a CAGR of 4.9% during the forecast period 2026-2034.

Process analyzers are precision instruments deployed inline, online, or at-line within industrial operations. The product ecosystem spans liquid analyzers - including pH, conductivity, turbidity, and dissolved oxygen sensors - and gas analyzers leveraging technologies such as electrochemical cells, infrared spectroscopy, tunable diode lasers, and paramagnetic sensors.

Industries across chemicals (The 50 companies in the ranking combined for $1.014 trillion in chemical sales in 2024, oil and gas, power generation, and pharmaceutical manufacturing rely on continuous analytical data to optimize yields, reduce waste, and ensure regulatory compliance. Together, these dynamics position process analyzers as essential infrastructure in modern industrial ecosystems.

Industry Ecosystem Map

|

Ecosystem Stage |

Key Players / Actors |

Primary Role |

|

Instrument Manufacturers |

ABB, Honeywell, Siemens, Yokogawa |

Core hardware/software R&D |

|

Technology Suppliers |

Sensor & detection component makers |

Electrochemical, optical, laser modules |

|

System Integrators |

Process automation specialists |

DCS/SCADA integration, calibration services |

|

Distributors & VARs |

Regional industrial distributors |

Last-mile delivery, field support |

|

End-Use Industries |

Power, Oil & Gas, Pharma, Chemicals, Water |

Process control and regulatory compliance |

Market Dynamics

To evaluate market opportunities, Request Sample

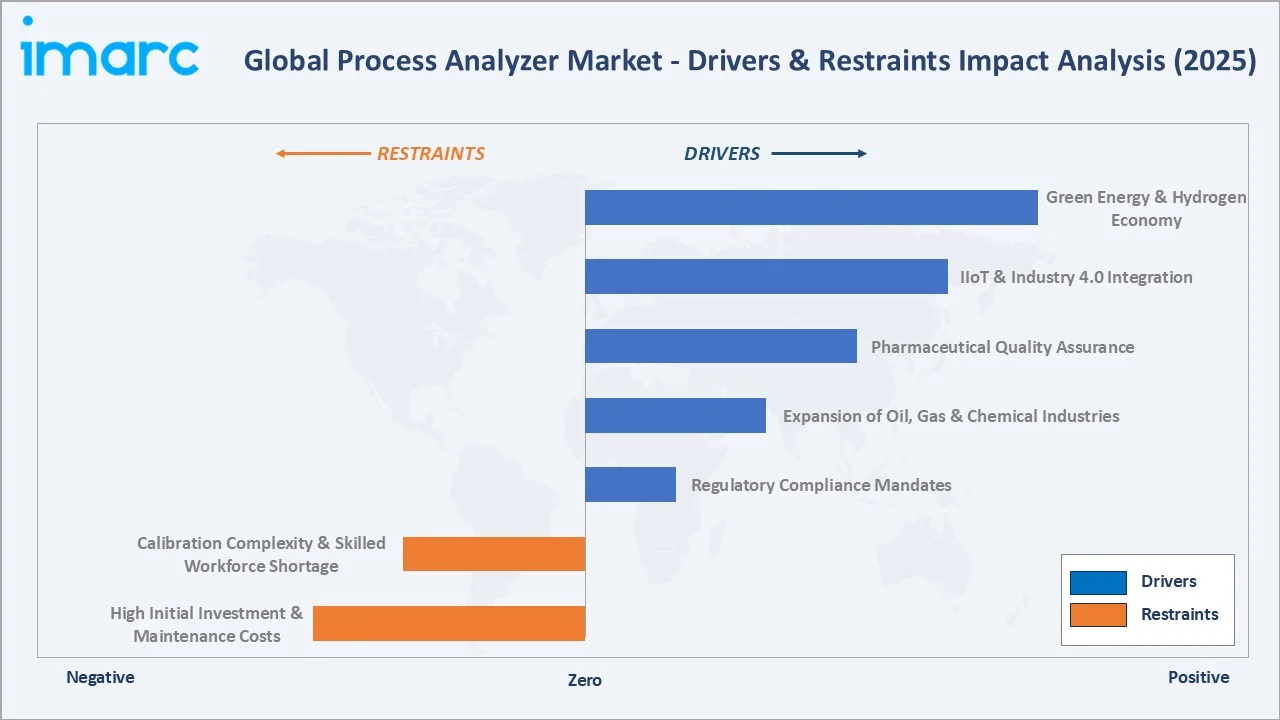

Market Drivers

- Regulatory Compliance Mandates: Stricter EPA (U.S.), EU IED, and national environmental norms compel industries to deploy certified process analyzers for continuous emissions monitoring (CEMS) and effluent discharge tracking.

- Expansion of Oil, Gas & Chemical Industries: Global refining capacity is projected to increase by an average of 620,000 barrels per day (BBL/d) between 2025 and 2027. This expansion is expected to drive proportional growth in demand for on-stream gas analyzers, particularly for measuring H₂S, O₂, and hydrocarbons.

- Pharmaceutical Quality Assurance: The rise of continuous manufacturing in biopharma, combined with FDA Process Analytical Technology (PAT) guidelines, is accelerating online liquid analyzer adoption for real-time batch release. The global pharmaceutical market currently stands at about $1.6 trillion.

Market Restraints

- High Initial Investment & Maintenance Costs: Advanced process analyzers, particularly laser-based gas analyzers, involve significant upfront and ongoing maintenance costs, limiting adoption among small and mid-sized manufacturers.

- Calibration Complexity & Skilled Workforce Shortage: Multi-parameter analyzers require periodic calibration and subject-matter expertise for maintenance, creating operational bottlenecks in regions with limited trained instrumentation engineers.

Market Opportunities

- IIoT & Industry 4.0 Integration: The convergence of process analyzers with Industrial Internet of Things (IIoT) platforms unlocks predictive maintenance, remote monitoring, and data-driven process optimization.

- Green Energy & Hydrogen Economy: IRENA envisages that two-thirds of green hydrogen production in 2050. Process analyzers - particularly for purity measurement and trace contaminant detection in hydrogen streams - represent a high-value emerging application segment.

- Emerging Markets Modernization: India, Southeast Asia, Africa, and Latin America are upgrading aging industrial infrastructure. Government-led water privatization and power sector reforms in these regions are expected to drive incremental demand for analyzers by 2034.

Market Challenges

- Intense Price Competition: Low-cost Asian manufacturers are aggressively pricing entry-level analyzers, compressing margins for premium-brand vendors and commoditizing basic liquid analyzer segments.

- Cybersecurity Risks in Connected Systems: As analyzers integrate with SCADA and cloud platforms, cybersecurity becomes a critical concern, particularly in critical infrastructure such as power plants and water utilities.

- Long Replacement Cycles: Process analyzers in stable industrial environments often operate for extended periods before replacement. This long equipment lifecycle slows the pace of technology refresh and limits near-term upgrade revenue potential.

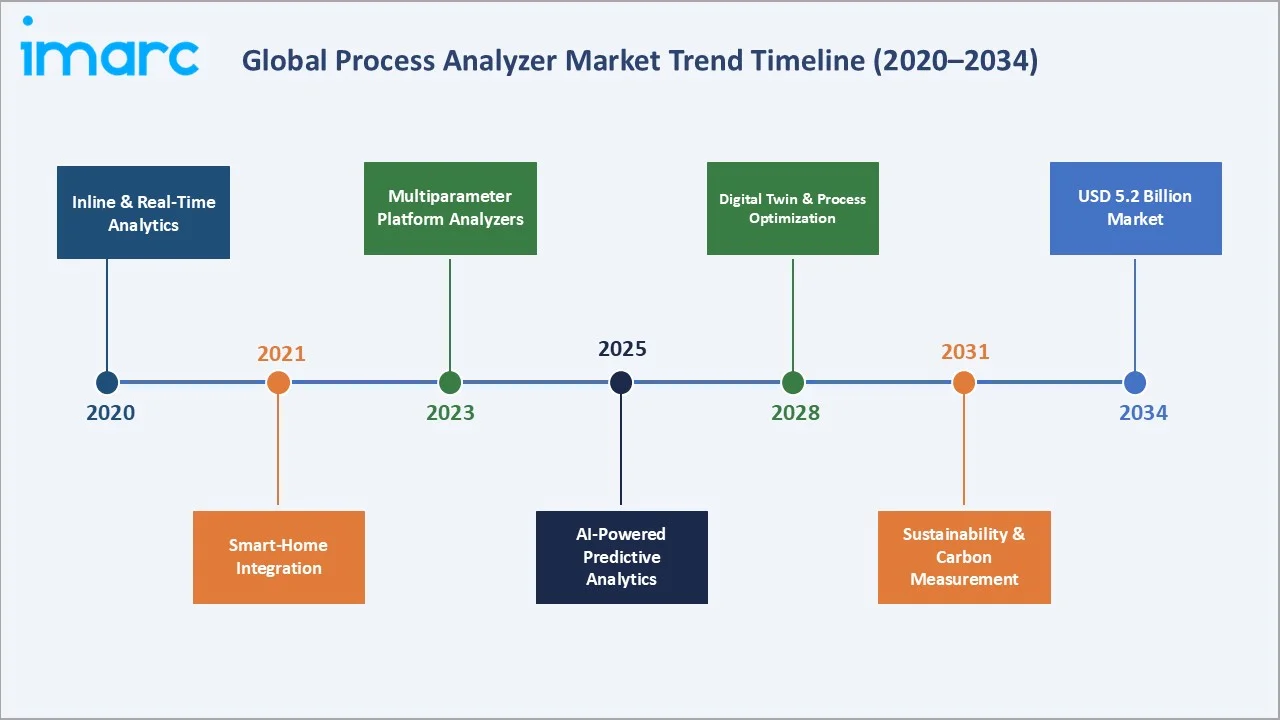

Emerging Market Trends

1: Inline & Real-Time Analytics Replacing Laboratory Testing

Industrial operators are increasingly replacing offline laboratory batch analysis with inline continuous measurement. Real-time data reduces product non-conformance and enables immediate process adjustments.

2: Multiparameter Platform Analyzers

Manufacturers are launching integrated platforms that measure five or more parameters simultaneously - pH, conductivity, dissolved oxygen, turbidity, and oxidation-reduction potential - from a single analyzer housing. This trend reduces installation footprint and total cost of ownership.

3: AI-Powered Predictive Analytics & Digital Twins

Leading vendors are embedding machine learning algorithms into analyzer firmware to detect drift, predict sensor fouling, and recommend calibration intervals. Digital twin technology - creating virtual replicas of process streams - enables simulation-based optimization.

5: Sustainability & Carbon Measurement Applications

Industrial decarbonization initiatives are generating new demand for CO2, NOx, and methane process analyzers to support Scope 1 emissions tracking and carbon credit certification. Process analyzer vendors are co-marketing with ESG reporting software providers, creating bundled solutions for continuous emissions monitoring.

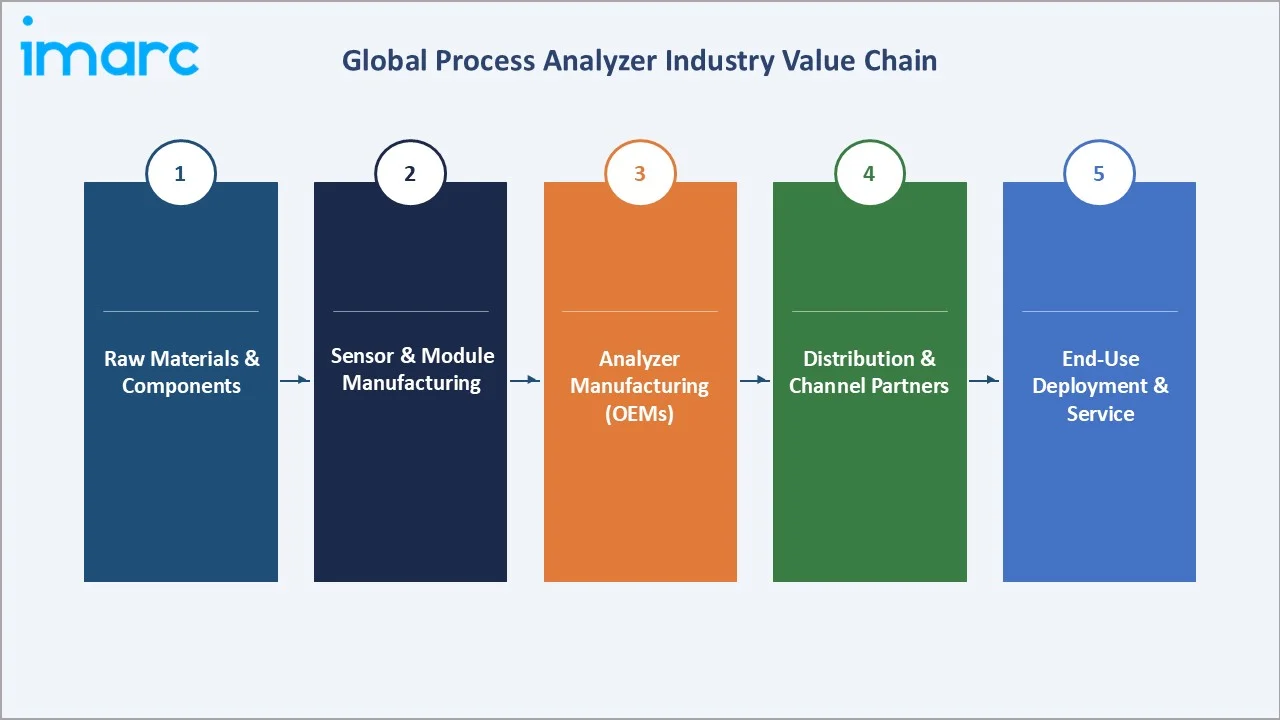

Industry Value Chain Analysis

The process analyzer industry value chain spans raw material extraction through end-user deployment and post-sales support. Each stage contributes specialized value and involves distinct stakeholders.

|

Value Chain Stage |

Description |

Key Players / Examples |

|

Raw Materials & Components |

Glass, metals, semiconductors, optical elements; specialty chemicals for reference solutions |

Schott AG (optics), Hamamatsu (detectors), specialty gas suppliers |

|

Sensor & Module Manufacturing |

Electrochemical cells, infrared sources, laser modules, membranes |

Membrapure, Aculon, OEM sensor manufacturers |

|

Analyzer Manufacturing (OEMs) |

Final assembly, calibration, software development, QA/testing |

ABB, Honeywell, Siemens, Emerson, HORIBA, Yokogawa |

|

Distribution & Channel Partners |

Authorized distributors, value-added resellers, system integrators |

Regional industrial distributors, local service firms |

|

End-Use Deployment & Service |

Installation, commissioning, calibration services, maintenance contracts |

Power plants, refineries, pharma, water utilities, food processors |

The process analyzer value chain spans raw materials, sensor manufacturing, OEM assembly, distribution networks, and end-use deployment with installation, calibration, and maintenance services.

Technology Landscape

The process analyzer technology landscape is bifurcated into liquid measurement technologies and gas analysis platforms, each underpinned by distinct detection physics. Liquid analyzers predominantly rely on electrochemical detection (for pH, dissolved oxygen, and conductivity) and optical scattering (for turbidity). The gas analyzer segment is more technologically diverse, with the following major platforms:

- Electrochemical Analyzers: Based on amperometric or potentiometric cells, these are cost-effective and widely used for O2, CO, H2S, and toxic gas monitoring. Market-mature but steadily upgraded with longer-life electrode materials.

- Infrared (IR) Spectroscopy: Non-dispersive infrared (NDIR) and Fourier transform infrared (FTIR) analyzers dominate hydrocarbon and CO2 measurement in petrochemical and cement industries. FTIR multi-component analysis is gaining share in pharmaceutical exhaust monitoring.

- Tunable Diode Laser (TDL) Spectroscopy: TDL analyzers offer high sensitivity, fast response time, and zero drift - ideal for H2O, NH3, HF, and O2 measurement in extreme temperature/pressure conditions such as cement kilns and blast furnaces. The TDL technology segment is projected to grow at approximately 7% CAGR through 2034.

- Catalytic Combustion Sensors: Used for flammable gas detection in hazardous area classified zones. Increasingly supplemented by photoionization detection (PID) for low-level volatile organic compound (VOC) monitoring.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Liquid Analyzer |

58.2% |

2025 |

|

End-Use Industry |

|

|

2025 |

|

Region |

North America |

32.0% |

2025 |

By Product Type

The process analyzer market is segmented by product type into liquid analyzers and gas analyzers

To access detailed market analysis, Request Sample

Liquid analyzers represent the single largest product segment, encompassing pH sensors, conductivity meters, dissolved oxygen analyzers, turbidity meters, and online total organic carbon (TOC) analyzers. Their pervasive deployment in water treatment facilities is the foundational demand driver. The pharmaceutical segment adds high-value demand, with FDA and EMA regulations mandating continuous critical quality attribute (CQA) monitoring during drug manufacturing..

By End-Use Industry (Liquid Analyzer)

The end-use breakdown for liquid analyzers in 2025 reveals a diversified demand profile spanning seven industries.

The power sector's dominance reflects the critical nature of water chemistry in boiler feed water and condensate management. A 0.1 pH deviation in boiler water chemistry can accelerate corrosion rates by orders of magnitude, creating strong incentives for continuous real-time monitoring.

Regional Market Insights

The process analyzer market exhibits distinct regional demand profiles shaped by industrial composition, regulatory frameworks, and infrastructure investment cycles.

|

Region |

2025 Share |

Key Demand Drivers |

|

North America |

32.0% |

Mature industrial base; EPA/OSHA compliance driving CEMS demand; strong oil and gas and pharma sectors |

|

Asia Pacific |

28.4% |

Fastest growing; rapid industrialization in China, India; environmental regulation tightening |

|

Europe |

24.6% |

Stringent EU IED/BAT standards; chemical and pharma manufacturing hubs; strong sustainability focus |

|

Middle East & Africa |

8.6% |

Oil and gas expansion; GCC water scarcity programs; Saudi Vision 2030 industrial diversification |

|

Latin America |

6.4% |

Mining, oil and gas, and food processing growth in Brazil, Mexico, Colombia, and Chile |

North America represents the largest regional market. Continuous emissions monitoring system (CEMS) mandates from the EPA and the Clean Air Act underpin a large installed base of stack-mounted gas analyzers across power, cement, and chemical plants.

Asia Pacific is the highest-growth regional market, driven by China's status as the world's largest chemical producer. Moreover, Indian refining capacity has increased from 256.8 Million Metric Tonne Per Annum (MMTPA) in FY24 to 258.1 MMTPA as of FY25.

Competitive Landscape

The global process analyzer market is moderately consolidated, with the top five players estimated to collectively hold approximately 55-60% of global revenues in 2025. ABB Group, Honeywell International Inc, Siemens AG, Emerson Electric Co., Endress+Hauser AG lead the market.

|

Company Name |

Brand / Division |

Market Position & Strength |

|

ABB Group |

ABB Measurement & Analytics |

Market Leader – broad portfolio across gas and liquid analyzers; strong IIoT integration |

|

Honeywell International Inc |

Honeywell Process Solutions |

Market Leader – CEMS leadership; Forge digital analytics platform; strong in oil and gas |

|

Siemens AG |

Siemens Process Analytics |

Market Leader – comprehensive range; deep DCS integration; leading TDL technology |

|

Emerson Electric Co. |

Rosemount Analytical |

Challenger – strong in refining; #1 in zirconia O2 analyzers; extensive field service network |

|

Endress+Hauser AG |

Liquiline / Endress+Hauser Optical Analysis |

Challenger – dominant in water/wastewater liquid analyzers; multiparameter platform leader |

|

HORIBA Group |

HORIBA Process & Environment |

Challenger – leading in automotive emissions, semiconductor gases, and pharma water quality |

|

Yokogawa Electric Corp. |

FLXA / TDLS Analyzer Series |

Challenger – strong in TDL spectroscopy; process gas chromatography; Asia Pacific leader |

|

Mettler Toledo SA |

Ingold / Thornton (Process Analytics) |

Emerging – pharma water quality specialist; strong FDA PAT compliance portfolio |

|

Schneider Electric SE |

AVEVA |

Emerging – software-defined analytics; digital twin integration; targeting smart plant upgrades |

|

Ametek Inc. |

Process Instruments Division |

Emerging – strong in industrial gas; tunable diode laser portfolio; North America focus |

|

Teledyne Technologies |

Teledyne Analytical Instruments |

Niche Leader – specialty gas measurement; trace O2/CO; defense and aerospace applications |

|

Thermo Fisher Scientific |

Thermo Scientific Analyzers |

Emerging – pharma/lab-grade inline analyzers; spectroscopy integration; pharma PAT segment |

Key Company Profiles

ABB Group

ABB Group is a Swiss Swedish multinational engineering and technology corporation headquartered in Zurich, Switzerland. Its Measurement & Analytics division is one of the world's leading providers of process analyzers, flow meters, and instrumentation for industrial process control.

- Product Portfolio: ACX Series gas analyzers, AW400 Series online liquid analyzers, Aztec pH/conductivity transmitters, and the EL3020 CEMS platform.

- Recent Developments: In 2026, ABB announced the launch of its first fully integrated gas analyser package for Carbon Capture, Utilisation and Storage applications, combining three proven ABB technologies into a single, streamlined solution. In 2025, ABB launched Sensi+ NG, the latest evolution of its innovative multi-gas contaminant analyzer for the biogas and natural gas industries.

- Strategic Focus: ABB is focused on IIoT-enabled remote monitoring, digital service contracts, and expanding its hydrogen economy analyzer portfolio.

Honeywell International Inc.

Honeywell International is a U.S.-based diversified technology and manufacturing conglomerate. Its Process Solutions division provides integrated automation, process analyzers, and safety systems to industrial end-users worldwide.

- Product Portfolio: MultiRAE multi-gas monitors, Midas gas detection system, Optima series CEMS, and the Sensepoint XCL fixed gas detectors.

- Recent Developments: In 2026, Honeywell introduced a new gas sensor that uses optical non-dispersive infrared (NDIR) technology to detect flammable gases, such as methane, propane and butane, in industrial settings.

- Strategic Focus: Honeywell's strategic focus centers on digital transformation services, carbon monitoring solutions, and expansion of software-enabled analyzer service contracts, targeting recurring revenue growth in the industrial analytics segment.

Siemens AG

Siemens AG is a German multinational conglomerate with global leadership in industrial automation, digitalization, and electrification. Its Process Analytics division develops and manufactures advanced gas and liquid process analyzers integrated with its broader automation ecosystem.

- Product Portfolio: ULTRAMAT/OXYMAT series infrared/paramagnetic gas analyzers, MAXUM II process gas chromatograph, SIPAN liquid analyzer platform, and LDS 6 tunable diode laser analyzer.

- Recent Developments: In 2026, Siemens introduced Drivetrain Analyzer Onsite (DTA Onsite), an on-premises analytics solution for industrial drive systems. The software allows users to evaluate drive data within their own infrastructure to address data-sovereignty requirements. In 2025, Atellica DT 250 Drug Testing Analyzer, a new benchtop analyzer from Siemens Healthineers is making quality drug testing easier to perform.

- Strategic Focus: Siemens is focused on digitally native analyzer platforms, seamless integration with MindSphere and Siemens Industrial AI tools, and co-selling analyzer hardware with broader automation contracts across chemicals and energy.

Market Concentration Analysis

The global process analyzer market exhibits moderate concentration. The top five companies - ABB Group, Honeywell International Inc, Siemens AG, Emerson Electric Co., Endress+Hauser AG - collectively account for an estimated 55-60% of total market revenues in 2025.

The market's fragmentation level varies meaningfully by segment. Gas analyzers - particularly CEMS platforms and multi-stream gas chromatographs for refinery applications - are more concentrated. Liquid analyzers for standard water quality applications are more fragmented.

Investment & Growth Opportunities

Fastest Growing Segments

- TDL & Laser-Based Gas Analyzers (~7% CAGR): High-sensitivity, drift-free laser analyzers for hydrogen, ammonia, and trace contaminants in clean energy value chains represent the single highest-growth sub-segment through 2034.

- Pharmaceutical Liquid Analyzers (~6.5% CAGR): FDA PAT guidelines, biologics manufacturing growth, and emerging mRNA vaccine production requiring ultra-pure water quality monitoring drive premium demand in this segment.

- Water & Wastewater Analyzers (~5.5% CAGR): Global investment in water infrastructure, smart water networks, and industrial effluent monitoring underpins broad-based demand growth, particularly in Asia Pacific and the Middle East.

Emerging Markets

- India: India’s National Clean Air Programme, Jal Shakti Mission, and the expansion of pharmaceutical API manufacturing are driving improvements in environmental management and industrial capacity.

- Saudi Arabia & UAE: Vision 2030-aligned non-oil industrial projects and desalination infrastructure demand for analyzers are expected to drive Middle East revenues at ~6% CAGR through 2034.

- Southeast Asia: Vietnam, Indonesia, and Thailand - rapidly developing their chemical, food processing, and power generation sectors.

Venture & Strategic Investment Trends

Private equity investment in mid-market process analyzer companies has accelerated since 2021, with platforms such as Roper Technologies and AMETEK executing buy-and-build strategies. Strategic partnerships between analyzer OEMs and IIoT platform companies (e.g., Microsoft Azure IoT, Siemens MindSphere, AWS Industrial) are creating new software-enabled revenue streams. Green hydrogen project developers are actively signing long-term supply agreements with TDL and electrochemical analyzer vendors, creating predictable forward revenue visibility.

Future Market Outlook (2026-2034)

The global process analyzer market is projected to grow from USD 7.9 billion in 2025 to USD 12.3 billion by 2034, equivalent to a CAGR of 4.9% during the forecast period. Liquid analyzers will retain their dominant position, accounting for an estimated 57-59% of revenues through the forecast horizon.

Technological disruption will be the most significant determinant of competitive positioning through 2034. Vendors who successfully integrate AI-driven analytics, digital twin capabilities, and cloud-connected service platforms will command premium pricing and higher retention rates.

Regionally, Asia Pacific is forecast to close the gap with North America, potentially overtaking it as the largest regional market by total value by 2032-2033.

Research Methodology

IMARC Group employs a robust multi-stage research methodology to ensure accuracy, reliability, and analytical depth across all syndicated market research reports.

- Primary Research: Extensive interviews were conducted with C-suite executives, product managers, procurement officers, and operations specialists across key end-use industries globally.

- Secondary Research: A comprehensive review of annual reports, SEC filings, trade publications (Control Engineering, Chemical Engineering, Hydrocarbon Processing), industry association databases (NAMUR, ISA, WEF), patent filings, and government regulatory databases was conducted to establish market context and historical trends.

- Market Estimation – Bottom-Up Approach: Revenue was estimated by aggregating product-level and segment-level shipment data from primary respondents and cross-referencing with distributor sell-through data, import/export trade statistics, and company revenue disclosures.

- Market Estimation – Top-Down Approach: Cross-validation was performed using macro-level industry output data (chemical production indices, power generation capacity additions, pharmaceutical manufacturing indices) to validate bottom-up market size estimates.

- Forecasting Methodology: IMARC's proprietary forecasting model integrates historical growth rates, macroeconomic indicators (industrial production indices, capital expenditure cycles), regulatory pipeline analysis, and primary-sourced forward guidance from leading industry participants.

Process Analyzer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| End Use Industries Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, United States, Canada, Turkey, Saudi Arabia, Iran, United Arab Emirates, Brazil, Mexico, Argentina, Colombia, Chile, Peru |

| Companies Covered | ABB Group, Honeywell International Inc, Siemens AG, Emerson Electric Co., Endress+Hauser AG, HORIBA Group, Yokogawa Electric Corp., Mettler Toledo SA, Schneider Electric SE, Ametek Inc., Teledyne Technologies, Thermo Fisher Scientific, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the process analyzer market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global process analyzer market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the process analyzer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Process Analyzer Market Report

The global process analyzer market was valued at USD 7.9 billion in 2025 and is projected to reach USD 12.3 billion by 2034, at a CAGR of 4.9%.

The market is forecast to grow at a compound annual growth rate (CAGR) of 4.9% during the forecast period 2026-2034.

Liquid analyzers dominate with a 58.2% share in 2025, driven by strong demand from power generation, water treatment, and pharmaceutical manufacturing.

North America leads with a 32.0% share in 2025, supported by EPA regulatory compliance mandates and a mature oil, gas, and pharmaceutical manufacturing base.

Asia Pacific (28.4% share in 2025) is the fastest growing region, driven by rapid industrialization in China, India, and Southeast Asia through 2034.

Key drivers include environmental compliance regulations, Industry 4.0 adoption, expanding oil and gas infrastructure, water scarcity investments, and pharmaceutical quality mandates.

The power generation sector accounts for 20.0% of liquid analyzer demand in 2025, requiring steam and cooling water chemistry monitoring to protect plant equipment.

Leading companies include ABB Group, Honeywell International Inc, Siemens AG, Emerson Electric Co., Endress+Hauser AG, HORIBA Group, Yokogawa Electric Corp., Mettler Toledo SA, Schneider Electric SE, Ametek Inc., Teledyne Technologies, Thermo Fisher Scientific.

AI-based analytics, and cloud-connected platforms are enabling predictive maintenance and remote monitoring, adding significant value beyond hardware alone.

Key trends include multiparameter platform analyzers, tunable diode laser adoption, wireless connectivity, AI-driven drift compensation, and carbon measurement for industrial decarbonization.

The global process analyzer market is projected to reach USD 10.0 billion by 2030, reflecting the mid-point milestone of the 2026-2034 forecast trajectory.

Key challenges include high initial investment costs, complex calibration requirements, long equipment replacement cycles, price competition from Asian manufacturers, and cybersecurity risks in connected systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)