Prostate Cancer Treatment Market Size, Share, Trends and Forecast by Drug Type, Distribution Channel, and Region, 2026-2034

Prostate Cancer Treatment Market Size, Share, Trends & Forecast (2026-2034)

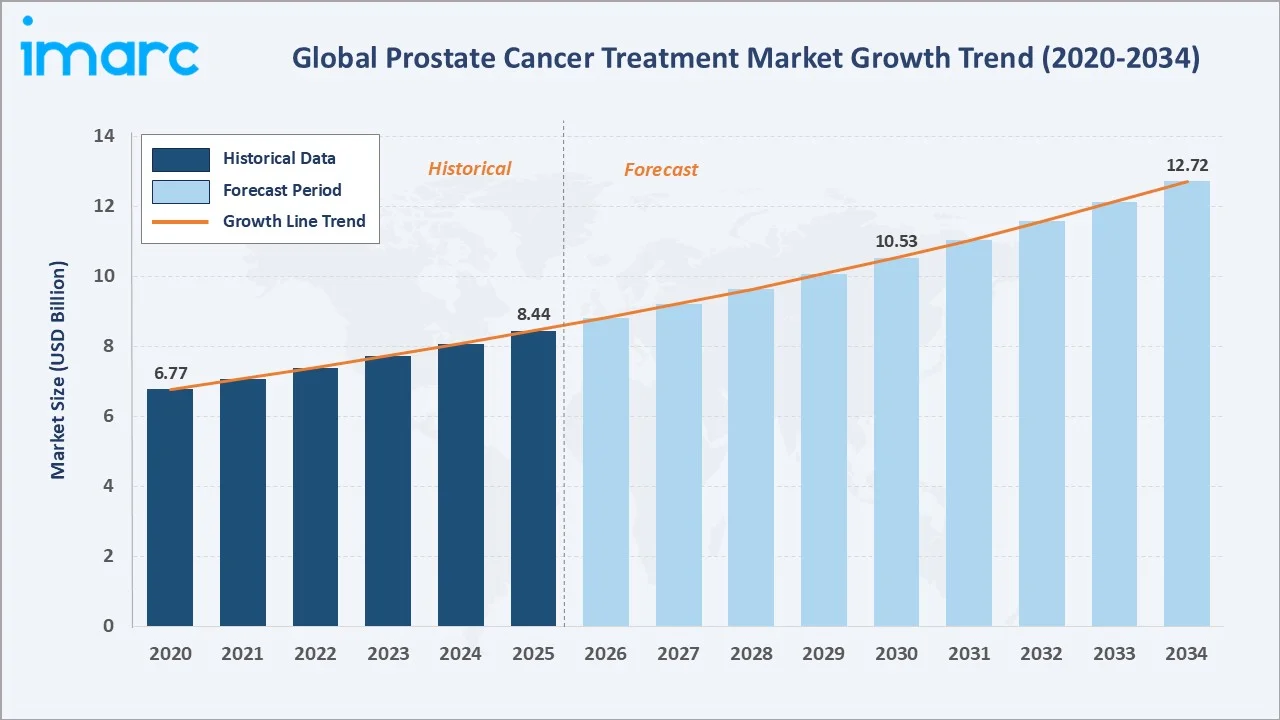

The prostate cancer treatment market was valued at USD 8.44 Billion in 2025 and is projected to reach USD 12.72 Billion by 2034, exhibiting a CAGR of 4.52% during 2026-2034. Market growth is being driven by the rising prevalence of prostate cancer, surging adoption of targeted and hormonal therapies, expanding geriatric population, advancements in diagnostic technologies, and increasing healthcare expenditure across major economies.

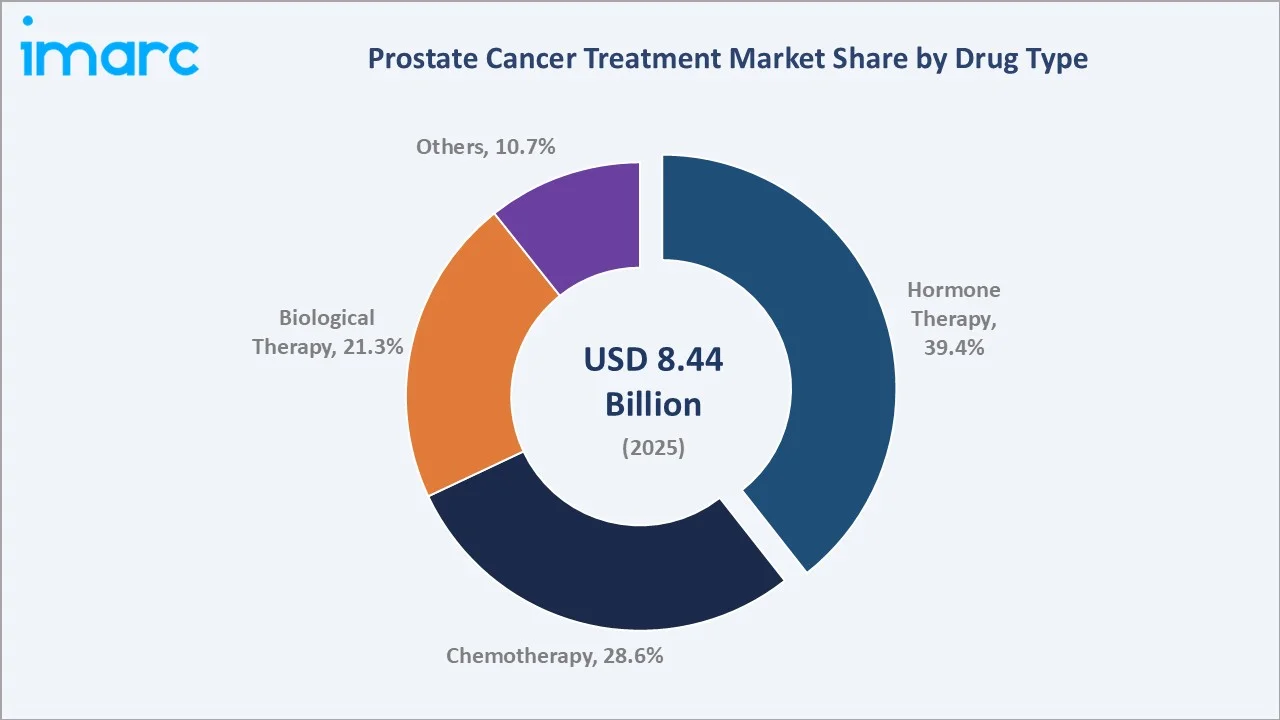

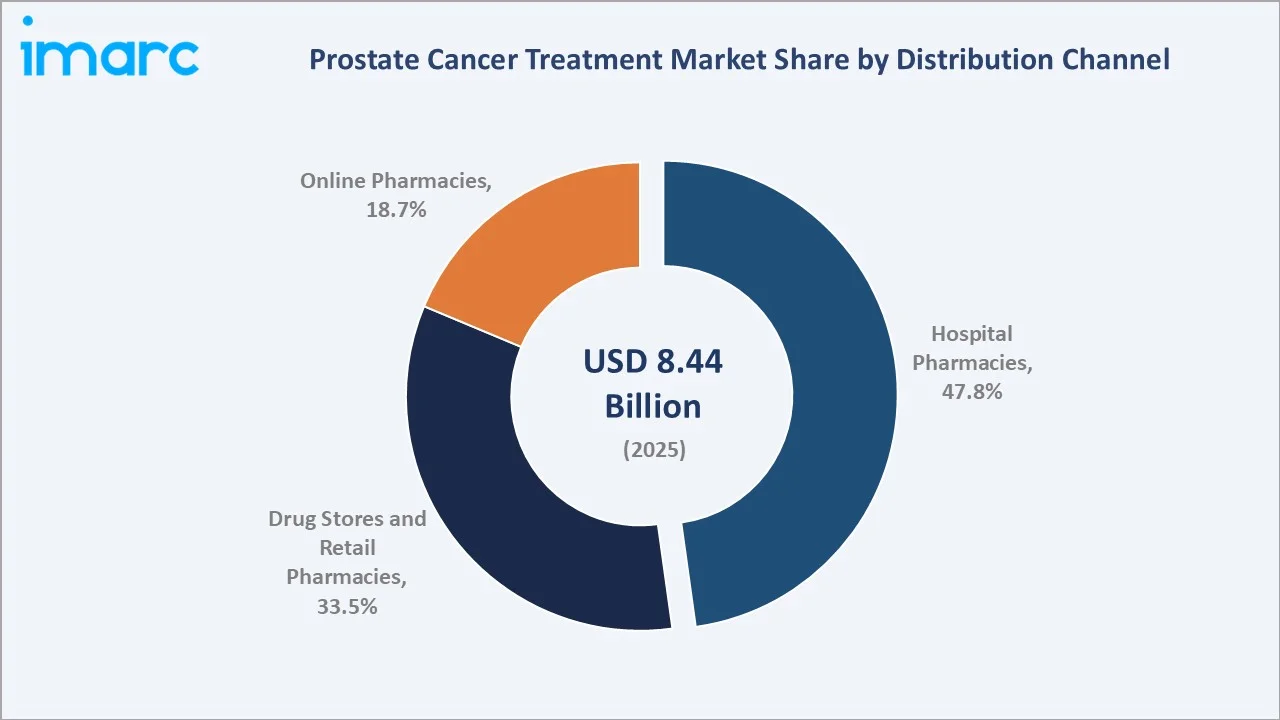

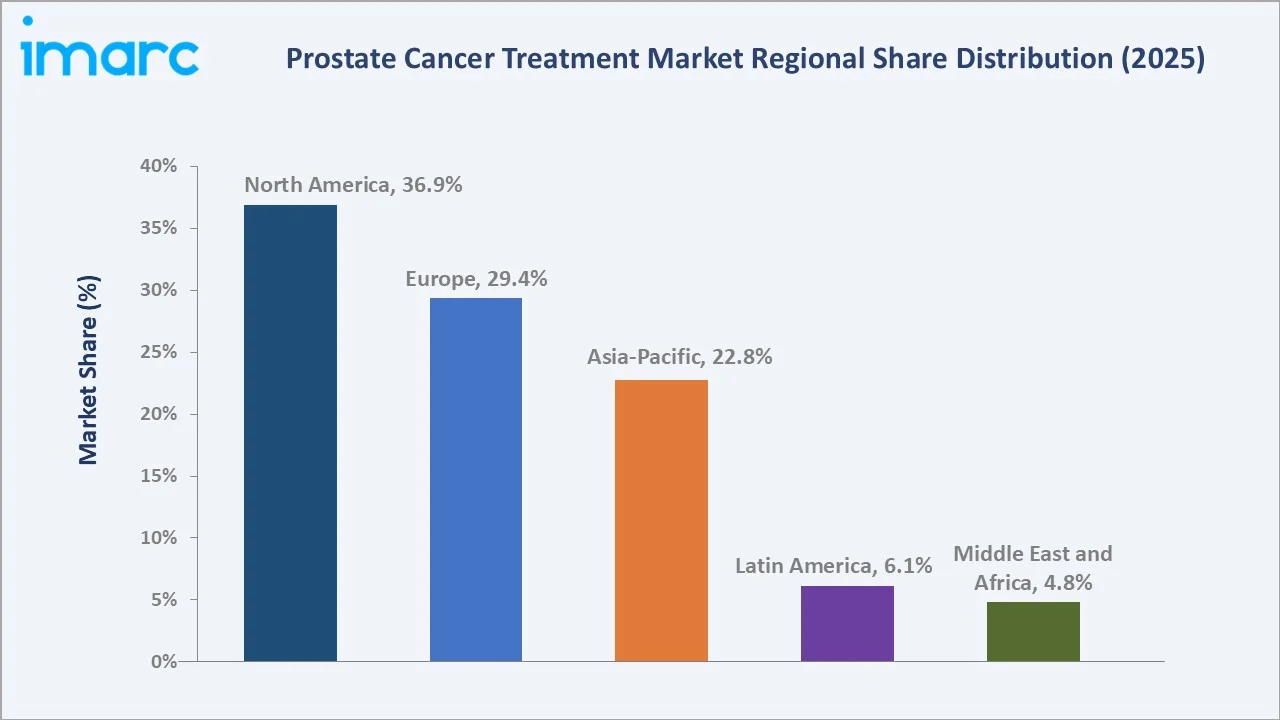

Hormone therapy leads the drug type segment at 39.4%, hospital pharmacies dominate the distribution channel at 47.8%, and North America commands 36.9% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.44 Billion |

|

Forecast Market Size (2034) |

USD 12.72 Billion |

|

CAGR (2026-2034) |

4.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.9%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (22.8%, 2025) |

|

Leading Drug Type |

Hormone Therapy (39.4%, 2025) |

|

Leading Distribution Channel |

Hospital Pharmacies (47.8%, 2025) |

The prostate cancer treatment market expanded from USD 6.77 Billion in 2020 to USD 8.44 Billion in 2025, driven by rising cancer prevalence, increasing treatment awareness, and expanding access to targeted therapies. Anchored at USD 10.53 Billion in 2030, the market is forecast to reach USD 12.72 Billion by 2034, supported by therapeutic advancements and rising healthcare investments.

To get more information on this market, Request Sample

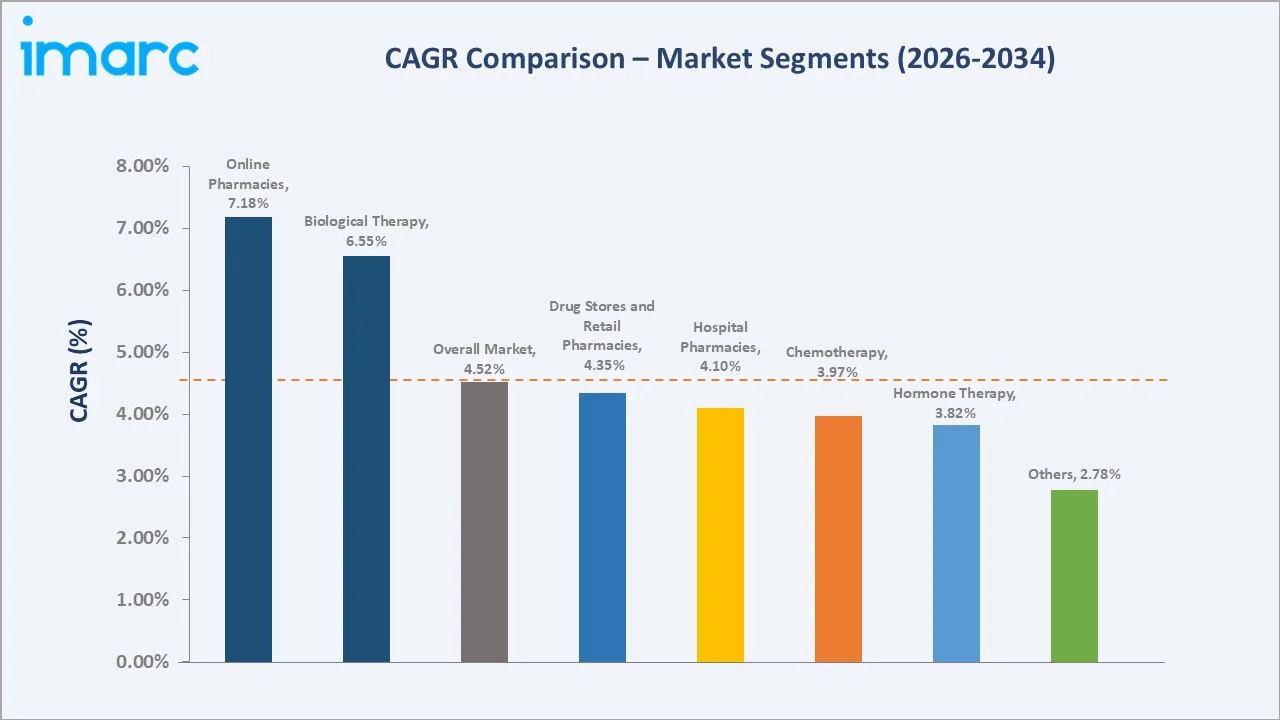

CAGR trajectories across drug type and distribution channel sub-segments show biological therapy and online pharmacies expanding faster than the overall 4.52% market CAGR, driven by innovation in precision oncology and the digital transformation of pharmaceutical distribution.

Executive Summary

The prostate cancer treatment market is on a steady growth trajectory, expanding from USD 6.77 Billion in 2020 to a projected USD 12.72 Billion by 2034. Rising global cancer incidence, aging male demographics, advances in targeted drug development, and expanding treatment access across healthcare systems are the primary drivers. The increasing adoption of combination therapy regimens is further supporting sustained revenue growth.

Hormone therapy holds the largest share at 39.4% in 2025, reflecting its established clinical role as the cornerstone of prostate cancer management. Hospital pharmacies lead distribution at 47.8%, underpinned by the complexity of cancer drug administration. North America commands 36.9% of the global market in 2025, supported by the United States' advanced oncology ecosystem, strong reimbursement frameworks, and high prostate cancer incidence and screening rates. The ACS 2024 Cancer Facts and Figures report estimated that there would be 299,010 new prostate cancer cases diagnosed in the United States in 2024.

Key Market Insights

|

Insight |

Data |

|

Leading Drug Type |

Hormone Therapy – 39.4% share (2025) |

|

Second Drug Type |

Chemotherapy – 28.6% share (2025) |

|

Leading Distribution Channel |

Hospital Pharmacies – 47.8% share (2025) |

|

Second Distribution Channel |

Drug Stores and Retail Pharmacies – 33.5% share (2025) |

|

Leading Region |

North America – 36.9% share (2025) |

|

Fastest Growing Region |

Asia-Pacific – 22.8% share (2025) |

|

Top Companies |

Johnson & Johnson, AstraZeneca, Astellas Pharma Inc., Bayer AG, Pfizer Inc., Sanofi, Novartis AG |

Key Analytical Observations Expanding on the Data Above:

- Hormone therapy dominance at 39.4% reflects its foundational role as first-line treatment across castration-sensitive and castration-resistant prostate cancer settings, supported by widespread use of androgen deprivation therapy and next-generation oral hormonal agents.

- Chemotherapy at 28.6% is sustained by the established clinical utility of docetaxel in metastatic disease and cabazitaxel in the second-line castration-resistant setting, supporting consistent revenue contribution from this segment.

- Hospital pharmacies at 47.8% reflect the centralization of cancer drug dispensing in specialist hospital settings, driven by complex infusion requirements, specialist supervision, and high-cost drug management protocols of oncology treatment.

- Drug stores and retail pharmacies at 33.5% serve the dispensing of oral targeted therapies, including next-generation androgen receptor inhibitors and PARP inhibitors, to ambulatory patients, benefiting from broad network coverage and accessible prescription fulfillment.

- North America at 36.9% leads globally owing to advanced oncology infrastructure, comprehensive insurance coverage, and a robust FDA-driven drug approval pathway. In May 2026, Schoolcraft Memorial Hospital introduced an innovative Nuclear Medicine service line, providing advanced prostate cancer treatment to Michigan's Upper Peninsula for the first time. The hospital provided Pluvicto (lutetium Lu-177 vipivotide tetraxetan), an FDA-approved targeted treatment for individuals with advanced metastatic prostate cancer.

Prostate Cancer Treatment Market Overview

Prostate cancer treatment encompasses a broad spectrum of pharmaceutical and clinical interventions designed to manage androgen-sensitive and castration-resistant disease across localized, locally advanced, and metastatic stages.

The global ecosystem integrates pharmaceutical manufacturers developing hormone therapies, chemotherapeutic agents, and biological drugs, alongside oncology hospitals, specialty clinics, retail and online pharmacies, regulatory bodies, and patient advocacy organizations. Macroeconomic factors, including healthcare expenditure growth, aging male populations, improved diagnostic infrastructure, and expanding oncology reimbursement frameworks, influence adoption trends across the prostate cancer treatment market.

Market Dynamics

To evaluate market opportunities, Request Sample

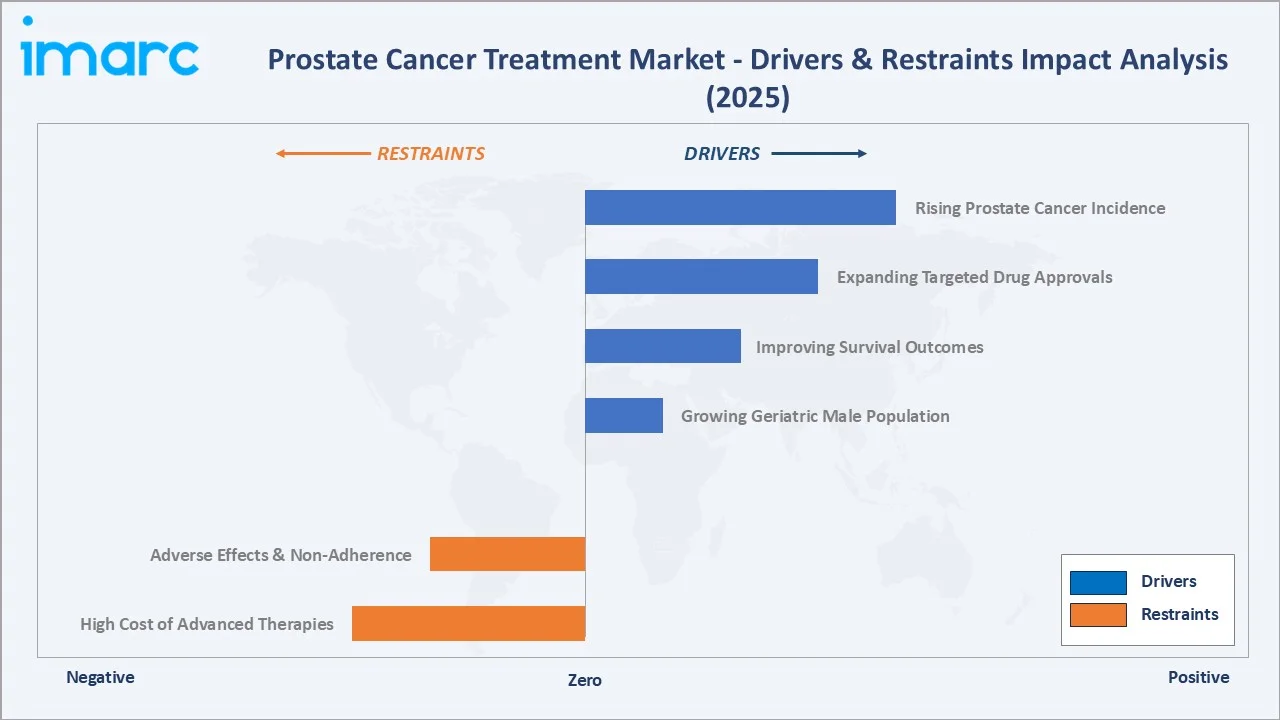

Market Drivers

- Rising Prostate Cancer Incidence: The growing burden of prostate cancer, driven by aging male populations and increased screening uptake, is generating consistent demand for pharmacological treatment solutions across all disease stages and geographies globally. As per Canadian Cancer Statistics 2025, it was estimated that there would be 30,400 new prostate cancer cases and 5,200 anticipated deaths. 1 in 9 men or 12% was expected to receive a prostate cancer diagnosis in their lifetime, while 1 in 34 men or 3% was projected to die from prostate cancer.

- Expanding Approvals for Targeted Therapies: The broadening regulatory approval landscape for next-generation androgen receptor inhibitors, PARP inhibitors, and radioligand therapies is creating new treatment lines, extending the addressable patient population, and supporting market revenue growth.

- Improving Survival Outcomes and Treatment Adoption: Advances in hormonal and targeted therapy regimens have significantly improved patient survival. These developments are encouraging earlier treatment initiation, expanding therapy adoption rates, and supporting sustained demand for advanced prostate cancer therapeutics.

- Growing Geriatric Male Population: The global demographic shift toward an older male population is structurally expanding the pool of men at elevated risk for prostate cancer, directly supporting long-term demand for treatment products across all segments.

Market Restraints

- High Cost of Advanced Therapeutics: The elevated price of newer androgen receptor signaling inhibitors, PARP inhibitors, and radioligand therapies creates significant affordability barriers. Limited reimbursement coverage in several regions further restricts patient access to advanced treatments.

- Adverse Effects and Patient Non-Adherence: Hormone therapy and chemotherapy regimens are associated with significant side effects, including fatigue, sexual dysfunction, bone loss, and cardiovascular risks, contributing to treatment discontinuation and suboptimal outcomes in a meaningful proportion of patients.

Market Opportunities

- Emerging Market Expansion: Increasing cancer awareness, improving diagnostic infrastructure, and healthcare spending growth across Asia-Pacific, Latin America, and the Middle East present significant volume growth opportunities for established and emerging prostate cancer treatment modalities.

- Precision Oncology and Biomarker-Driven Therapy: The expanding role of genomic profiling and companion diagnostics is enabling more targeted treatment selection, opening new commercial pathways for PARP inhibitors, checkpoint inhibitors, and radioligand therapies in genomically defined patient populations.

Market Challenges

- Complex Regulatory and Reimbursement Environment: Navigating diverse regulatory approval pathways and heterogeneous reimbursement policies across global markets adds time, cost, and complexity to product launches and market access strategies for prostate cancer treatment developers.

- Emergence of Drug Resistance in Advanced Disease: Acquired resistance to androgen deprivation therapy and second-generation hormonal agents in castration-resistant prostate cancer remains a significant clinical and commercial challenge, driving the need for continued investment in novel therapy development.

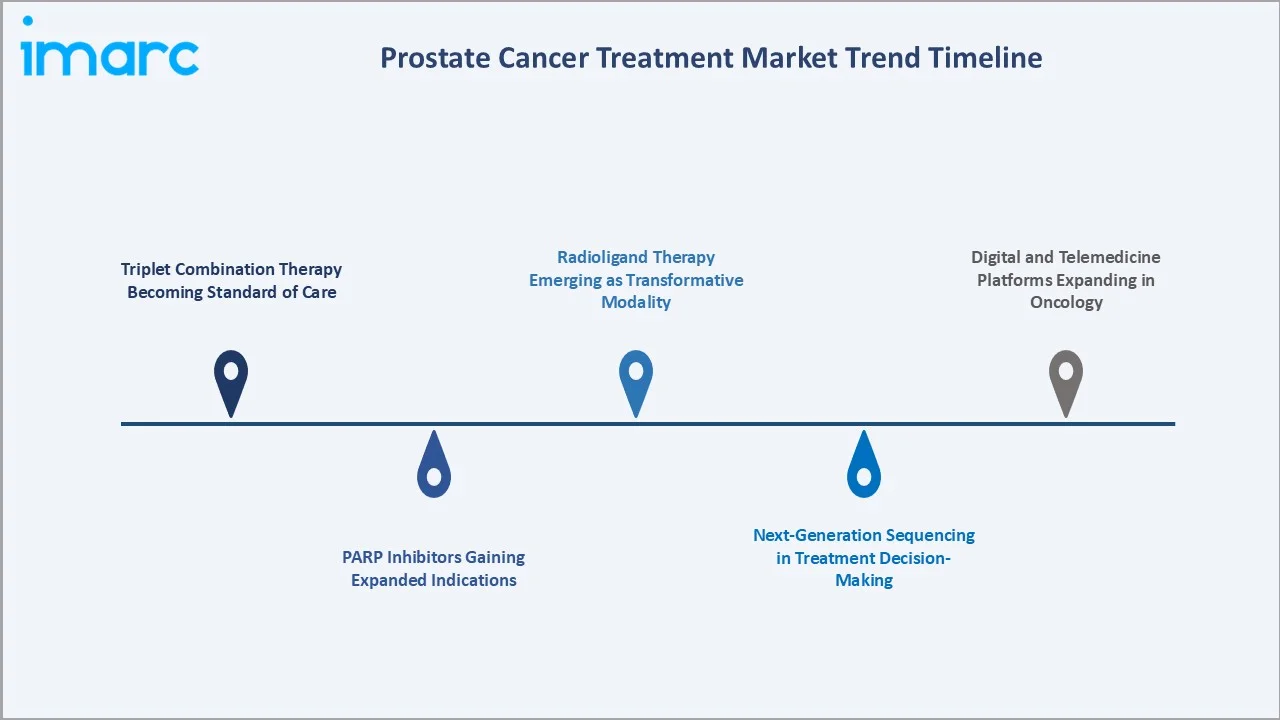

Emerging Market Trends

1. Triplet Combination Therapy Becoming Standard of Care for Metastatic Disease

The shift from androgen deprivation therapy monotherapy to doublet and triplet combination regimens incorporating second-generation hormonal agents, such as enzalutamide, apalutamide, and darolutamide alongside docetaxel, is reshaping treatment protocols. This evolution is expanding product utilization per patient and supporting revenue growth across the hormone therapy and chemotherapy segments.

2. PARP Inhibitors Gaining Expanded Indications in Prostate Cancer

PARP inhibitors, initially approved for BRCA-mutated metastatic castration-resistant prostate cancer, are gaining expanded clinical acceptance. Ongoing clinical trials and combination therapy approaches are supporting their broader use across advanced prostate cancer treatment settings.

3. Radioligand Therapy Emerging as a Transformative Treatment Modality

Radioligand therapy is emerging as a breakthrough approach for the treatment of advanced and metastatic prostate cancer, offering targeted delivery mechanisms with improved therapeutic outcomes. Growing clinical success and increasing investment in targeted radiopharmaceutical development are accelerating innovation across the biological therapy landscape and reshaping competitive dynamics within the market.

4. Integration of Next-Generation Sequencing in Treatment Decision-Making

The adoption of comprehensive genomic profiling as a standard diagnostic step before initiating systemic therapy is enabling more precise patient stratification and treatment selection. Companion diagnostic development is accelerating alongside targeted drug approvals, creating a tightly integrated diagnostic-treatment ecosystem within the prostate cancer treatment market.

5. Expanding Role of Digital and Telemedicine Platforms in Oncology Care

Digital health platforms, remote monitoring tools, and telemedicine consultations are expanding patient access to specialist oncology care, particularly in geographically underserved markets. As per IMARC Group, the global digital health market size was valued at USD 573.3 Billion in 2025. This trend supports consistent medication adherence, earlier treatment initiation, and enhanced patient-physician communication, indirectly benefiting pharmaceutical treatment utilization rates.

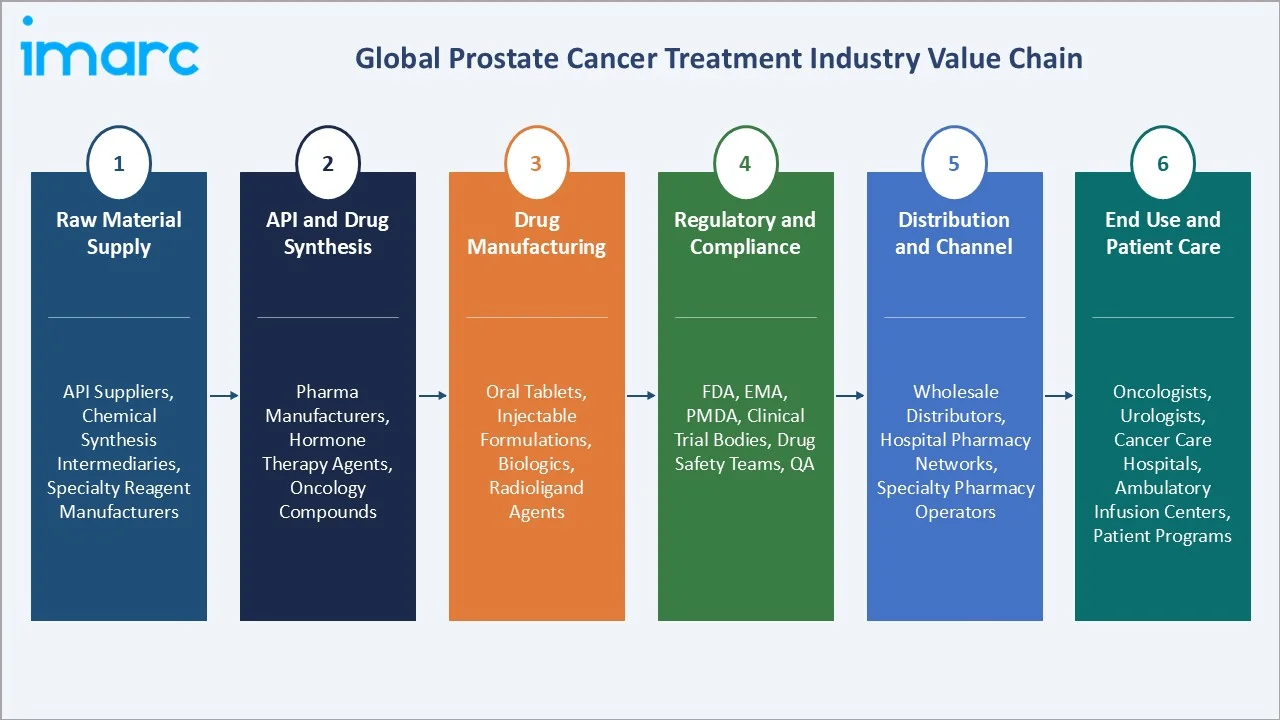

Industry Value Chain Analysis

The prostate cancer treatment value chain spans six stages from raw material supply through end-use patient care. Drug formulation and manufacturing capture the highest value-add, while specialist distribution relationships and reimbursement program enrollment generate downstream competitive advantages.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Active pharmaceutical ingredient suppliers, chemical synthesis intermediaries, and specialty reagent manufacturers supporting oncology drug production |

|

API and Drug Synthesis |

Pharmaceutical manufacturers specializing in hormone therapy agents, chemotherapeutic molecules, and targeted oncology compounds |

|

Drug Manufacturing |

Manufacturers producing oral tablets, injectable formulations, radiopharmaceuticals, and biologic agents for oncological treatment |

|

Regulatory and Compliance |

Standards organizations, clinical trial bodies, pharmacovigilance teams, and quality assurance functions supporting global market access |

|

Distribution and Channel Management |

Oncology-focused wholesale distributors, hospital pharmacy networks, specialty pharmacy operators, and e-commerce pharmaceutical platforms |

|

End Use and Patient Care |

Oncologists, urologists, radiation oncologists, cancer care hospitals, ambulatory infusion centers, and patient support programs |

Vertically integrated manufacturers, which operate across drug discovery, clinical development, manufacturing, and global distribution, maintain structural advantages over smaller players reliant on contract manufacturing or third-party API sourcing.

Technology Landscape in the Prostate Cancer Treatment Industry

Androgen Receptor Pathway Inhibition

Next-generation androgen receptor pathway inhibitors represent the most commercially significant technology platform in the market. These agents target multiple nodes of the androgen signaling cascade including androgen synthesis, receptor binding, and nuclear translocation. Ongoing research focuses on overcoming androgen receptor splice variants that confer resistance to existing agents, with several novel compounds in late-stage clinical development.

PARP Inhibitor Technology

PARP inhibitors exploit DNA repair deficiencies in tumors harboring homologous recombination repair gene mutations, particularly BRCA1, BRCA2, and ATM alterations. The mechanistic selectivity of PARP inhibitors is driving companion diagnostic integration into clinical decision-making and expanding precision oncology platforms in prostate cancer.

Diagnostic and Companion Diagnostic Integration

Advanced PSMA-targeted PET imaging tracers and comprehensive genomic profiling platforms are enabling more precise staging and patient selection. These diagnostic tools create tightly coupled treatment-diagnostic ecosystems that accelerate drug adoption and support premium pricing for targeted therapeutic regimens.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Drug Type | Hormone Therapy | 39.4% | 2025 |

| Distribution Channel | Hospital Pharmacies | 47.8% | 2025 |

| Region | North America | 36.9% | 2025 |

By Drug Type

Hormone therapy commands a 39.4% majority share in 2025, reflecting its foundational role as the standard first-line treatment for locally advanced and metastatic prostate cancer. Androgen deprivation therapy and next-generation agents, including enzalutamide, apalutamide, and abiraterone acetate, are widely adopted across disease settings from adjuvant and neoadjuvant use to metastatic castration-sensitive and castration-resistant disease.

To access detailed market analysis, Request Sample

Chemotherapy holds a 28.6% share in 2025, driven by the continued use of docetaxel as a backbone of first-line treatment for metastatic disease and cabazitaxel as a second-line option in castration-resistant prostate cancer.

By Distribution Channel

Hospital pharmacies dominate the distribution channel with a 47.8% share in 2025, reflecting the complexity of oncology drug dispensing, infusion center infrastructure, and the specialist-supervised nature of prostate cancer treatment protocols. The centralization of cancer care in hospital settings supports the continued primacy of this channel.

Drug stores and retail pharmacies hold 33.5% of the distribution channel segment in 2025, supporting the dispensing of oral targeted therapies and post-treatment supportive medications to ambulatory patients.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.9% |

Advanced oncology infrastructure, strong drug reimbursement, high prostate cancer screening rates, and a robust drug approval pipeline |

|

Europe |

29.4% |

Comprehensive cancer care networks, established treatment guidelines, aging male population, and supportive healthcare funding frameworks |

|

Asia-Pacific |

22.8% |

Growing cancer incidence, expanding healthcare access, rising diagnostic awareness, and increasing pharmaceutical market investments |

|

Latin America |

6.1% |

Improving cancer treatment infrastructure, rising awareness, expanding insurance coverage, and growing access to branded and generic oncology therapies |

|

Middle East and Africa |

4.8% |

Healthcare modernization initiatives, increasing cancer registry development, expanding hospital oncology capacity, and growing adoption of international treatment protocols |

North America at 36.9% in 2025 leads the global market, underpinned by the United States' advanced oncology ecosystem, strong FDA approval track record for novel therapies, comprehensive insurance coverage, and high prostate cancer screening rates among men over 50.

Asia-Pacific at 22.8% in 2025 is the fastest-growing region through 2034. Rising prostate cancer awareness, expanding genomic testing adoption, and increasing investment in oncology drug access programs across China, Japan, South Korea, and India are driving accelerated regional market growth.

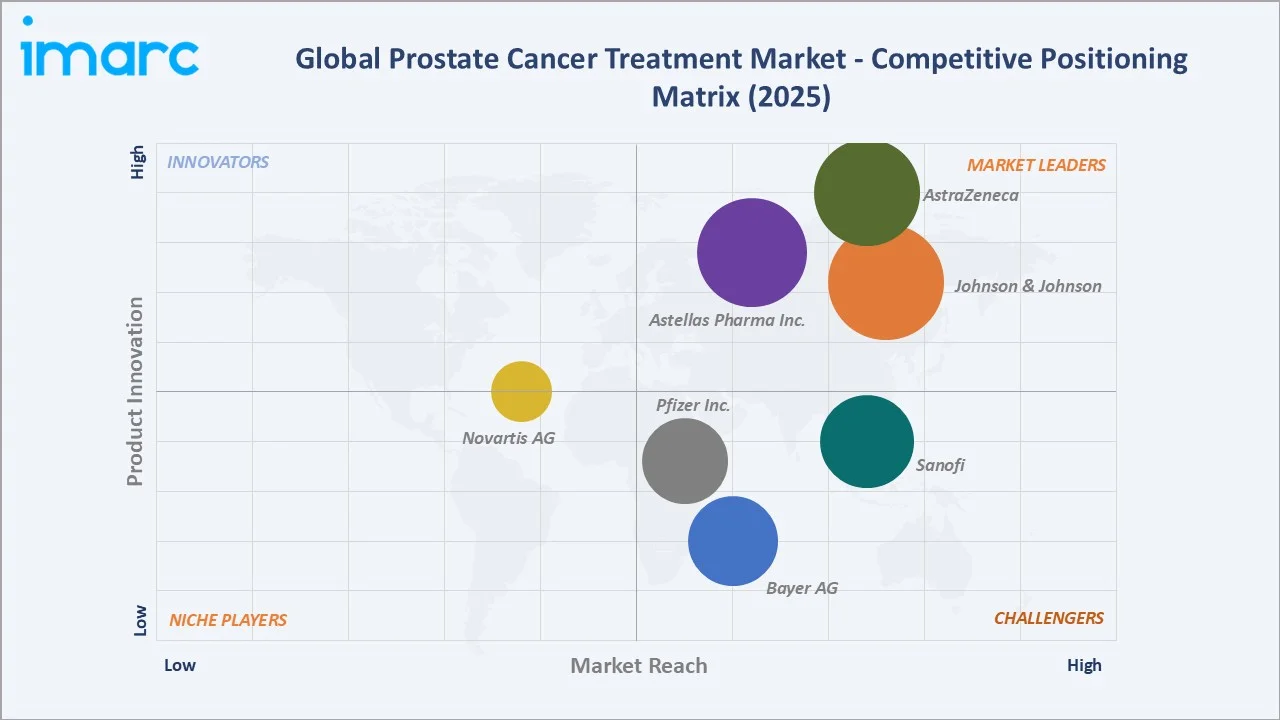

Competitive Landscape

The prostate cancer treatment market is moderately concentrated, with large multinational pharmaceutical corporations dominating across hormone therapy, chemotherapy, and biological therapy segments. Market leaders leverage extensive clinical development pipelines, global regulatory capabilities, established oncology sales forces, and deep reimbursement relationships to maintain competitive positions across multiple treatment lines.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Johnson & Johnson |

Erleada, Akeega |

Leader |

Broad oncology portfolio across multiple disease stages and treatment lines |

|

AstraZeneca |

Lynparza (Co-developed) |

Leader |

Precision oncology and companion diagnostic-driven treatment development |

|

Astellas Pharma Inc. |

Xtandi (Co-developed) |

Leader |

Hormonal therapy lifecycle management and global market penetration |

|

Bayer AG |

Nubeqa (Co-developed), Xofigo |

Challenger |

Targeted radiotherapy and hormonal therapy with broad urology channel reach |

|

Pfizer Inc. |

Talzenna |

Challenger |

PARP inhibitor and oncology portfolio expansion with global commercial infrastructure |

|

Sanofi |

Jevtana |

Challenger |

Chemotherapy lifecycle management and specialty oncology distribution |

|

Novartis AG |

Pluvicto |

Emerging |

Radioligand therapy platform leadership and PSMA-targeted innovation |

Key players include Johnson & Johnson, AstraZeneca, Astellas Pharma Inc., Bayer AG, Pfizer Inc., Sanofi, and Novartis AG, among others.

Key Company Profiles

Johnson & Johnson

Johnson & Johnson operates a leading oncology division focused on advanced prostate cancer therapeutics across hormone-sensitive, castration-resistant, and genetically targeted treatment settings. The company continues to strengthen its market position through ongoing innovation in targeted therapies, combination treatment approaches, and global commercialization strategies for prostate cancer care.

- Product Portfolio: Erleada (apalutamide) for non-metastatic and metastatic castration-sensitive prostate cancer.

- Recent Developments: Johnson & Johnson secured a second FDA approval for Akeega in December 2025, expanding its indication to BRCA2-mutated metastatic castration-sensitive prostate cancer, significantly broadening the addressable patient population for this precision oncology combination.

- Strategic Focus: Comprehensive prostate cancer franchise spanning multiple disease stages, with strategic focus on PARP inhibitor combinations.

AstraZeneca

AstraZeneca is a global biopharmaceutical company focused on precision oncology and advanced prostate cancer therapeutics. The company maintains a strong presence in targeted cancer treatment through continued investment in PARP inhibitor research, biomarker-driven therapies, and an expanding oncology pipeline addressing advanced and genetically defined prostate cancer settings.

- Product Portfolio: Lynparza (olaparib), co-developed with Merck & Co., Inc., targeting homologous recombination repair-deficient metastatic castration-resistant prostate cancer; pipeline assets spanning additional targeted oncology mechanisms.

- Recent Developments: The company continues to strengthen its oncology portfolio through ongoing clinical research, expanded targeted therapy development programs, and strategic collaborations focused on improving treatment outcomes across advanced prostate cancer settings.

- Strategic Focus: Precision oncology leadership anchored on companion diagnostic-driven patient selection, multi-indication portfolio expansion, and global regulatory market access capabilities.

Sanofi

Sanofi participates in the prostate cancer treatment market through its oncology portfolio, focusing on therapies for advanced and treatment-resistant prostate cancer settings. The company continues to support oncology innovation through investments in cancer research, therapeutic development, and global commercialization strategies aimed at improving patient outcomes.

- Product Portfolio: Jevtana for metastatic castration-resistant prostate cancer in the post-docetaxel setting; supportive oncology products across the treatment continuum.

- Recent Developments: Sanofi has pursued combination chemotherapy strategies and specialty oncology positioning while undertaking portfolio transformation through internal pipeline and external partnership investments.

- Strategic Focus: Chemotherapy lifecycle management, specialty oncology channel optimization, and portfolio transformation toward precision oncology through internal and external development activities.

Market Concentration Analysis

The prostate cancer treatment market is moderately concentrated, with the top seven players (Johnson & Johnson, AstraZeneca, Astellas Pharma Inc., Bayer AG, Pfizer Inc., Sanofi, and Novartis AG) estimated to collectively hold approximately 60–70% of global market revenue share in 2025.

Barriers to entry include substantial clinical development investment requirements, complex oncology regulatory pathways, companion diagnostic integration needs, and established physician prescription relationships.

Consolidation is progressing through pipeline acquisitions, licensing agreements, and combination therapy co-development partnerships among established pharmaceutical players and emerging biotechnology companies.

Investment & Growth Opportunities

Fastest-Growing Segments

Biological therapy at 21.3% is the fastest-growing drug type, driven by accelerating PARP inhibitor adoption, expanding radioligand therapy indications, and growing clinical investigation of immune checkpoint inhibitors in select prostate cancer settings. Online pharmacies at 18.7% are the fastest-growing distribution channel as digital health platforms scale and specialty drug home delivery programs expand globally.

Emerging Markets

Asia-Pacific at 22.8% is the highest-growth region through 2034. China, Japan, India, and South Korea represent significant volume opportunities, driven by rising prostate cancer incidence, improving PSA screening rates, expanding treatment guidelines, and growing reimbursement depth for specialty oncology drugs. Latin America and the Middle East and Africa also present meaningful medium-term expansion opportunities.

Venture & Investment Trends

Investment activity is concentrated in next-generation radioligand therapy, PSMA-targeted combination approaches, androgen receptor-directed novel mechanisms, and AI-enabled diagnostics for prostate cancer treatment selection. Biotech-to-pharma acquisition activity remains elevated as large pharmaceutical companies seek to replenish prostate cancer pipeline assets and access novel therapeutic platforms.

Future Market Outlook (2026-2034)

The prostate cancer treatment market is forecast to expand from USD 8.44 Billion in 2025 to USD 12.72 Billion by 2034 at a CAGR of 4.52%, representing approximately USD 4.28 Billion in incremental annual market value over the forecast period.

Four forces will define the market trajectory: continued expansion of next-generation hormonal therapy indications into earlier disease settings; rapid scaling of radioligand therapy manufacturing and clinical access infrastructure; growing adoption of PARP inhibitors in genomically selected patient populations; and increased market penetration in Asia-Pacific and other high-growth emerging markets.

By 2034, biological therapy is expected to represent a meaningfully larger share of overall treatment revenue, as precision oncology approaches continue to gain clinical and regulatory validation.

Research Methodology

Primary Research

Primary research included interviews with senior oncologists, urologists, pharmaceutical medical affairs leaders, healthcare payers, hospital pharmacists, and prostate cancer patient advocacy representatives. These interactions validated market sizing assumptions, segment growth estimates, regional demand dynamics, and competitive positioning assessments.

Secondary Research

Secondary sources included published oncology clinical trial data, cancer registry reports from the International Agency for Research on Cancer and national cancer institutes, regulatory filings from the FDA, EMA, and PMDA, corporate annual reports and investor presentations, and published peer-reviewed oncology literature.

Forecasting Models

Market forecasts were developed using top-down and bottom-up modeling incorporating prostate cancer incidence projections, drug approval pipeline timing, pricing and reimbursement data, patient share assumptions by treatment line, and macroeconomic healthcare expenditure growth rates. Scenario analysis addressed variations in clinical trial outcomes, competitive launch timing, and pricing policy changes across key markets.

Prostate Cancer Treatment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Types Covered | Chemotherapy, Biological Therapy, Hormone Therapy, Others |

| Distribution Channels Covered | Hospital Pharmacies, Drug Stores and Retail Pharmacies, Online Pharmacies |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Johnson & Johnson, AstraZeneca, Astellas Pharma Inc., Bayer AG, Pfizer Inc., Sanofi, Novartis AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the prostate cancer treatment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global prostate cancer treatment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the prostate cancer treatment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Prostate Cancer Treatment Market Report

The market was valued at USD 8.44 Billion in 2025, driven by rising cancer incidence, expanding drug approvals, and growing treatment adoption globally across all disease stages.

The market is projected to grow at a CAGR of 4.52% from 2026 to 2034, reaching USD 12.72 Billion, supported by novel drug launches and emerging market expansion.

Hormone therapy leads with 39.4% share in 2025, reflecting its foundational clinical role across castration-sensitive and castration-resistant prostate cancer treatment lines.

Hospital pharmacies dominate at 47.8% in 2025, fueled by specialist supervision requirements and the availability of infusion center infrastructure for complex prostate cancer drug administration.

North America leads with 36.9% share in 2025, driven by advanced oncology infrastructure, comprehensive reimbursement, and high screening and diagnosis rates for prostate cancer.

Leading players include Johnson & Johnson, AstraZeneca, Astellas Pharma Inc., Bayer AG, Pfizer Inc., Sanofi, and Novartis AG.

PARP inhibitor approvals, radioligand therapy commercialization, and expanding clinical acceptance of targeted agents in genomically defined populations are fueling biological therapy growth.

Precision oncology is enabling targeted treatment selection based on genomic profiling, expanding PARP inhibitor and radioligand therapy utility, and supporting premium pricing for biomarker-driven regimens.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade