PVC Pipes Market Size, Share, Trends and Forecast by Application and Region, 2026-2034

Global PVC Pipes Market Size, Share, Trends & Forecast (2026-2034)

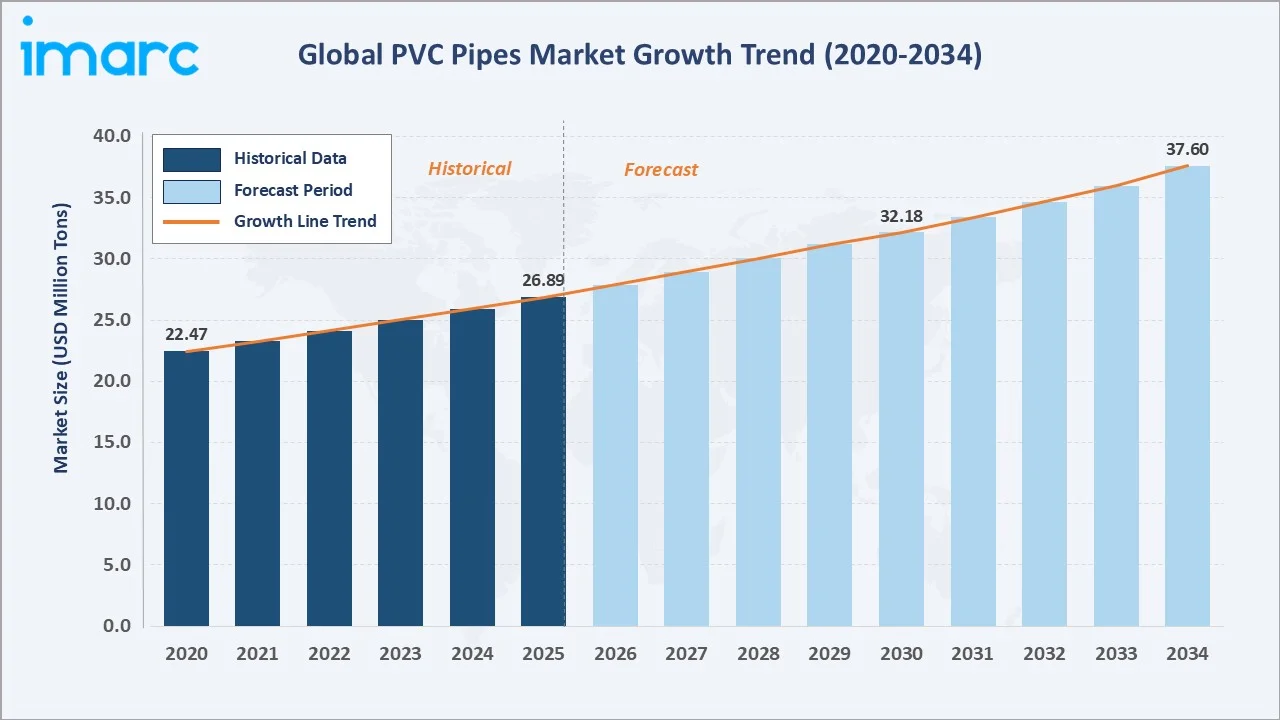

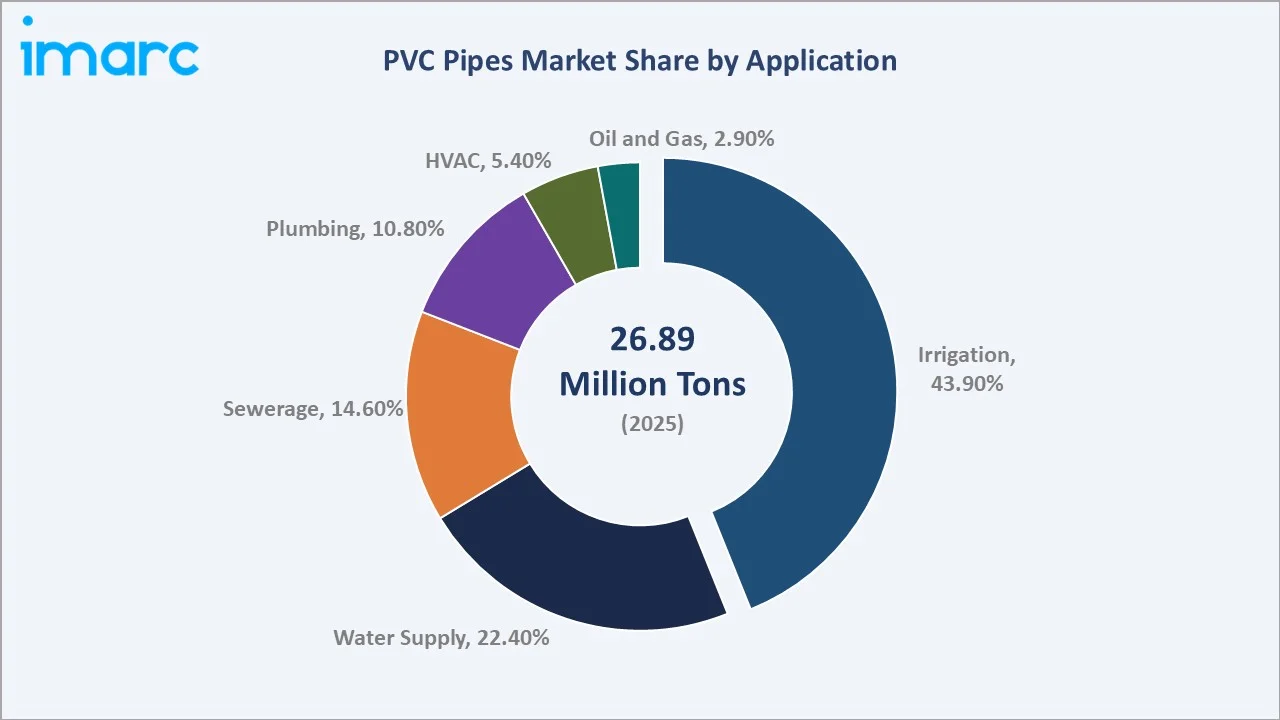

The global PVC pipes market was volumed at 26.89 Million Tons in 2025 and is projected to reach 37.60 Million Tons by 2034, expanding at a CAGR of 3.66% during 2026-2034. The market's consistent upward trajectory is driven by accelerating urbanization, government-led water infrastructure investments, agricultural modernization, and expanding construction activity globally.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

26.89 Million Tons |

|

Forecast Market Size (2034) |

37.60 Million Tons |

|

CAGR (2026-2034) |

3.66% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

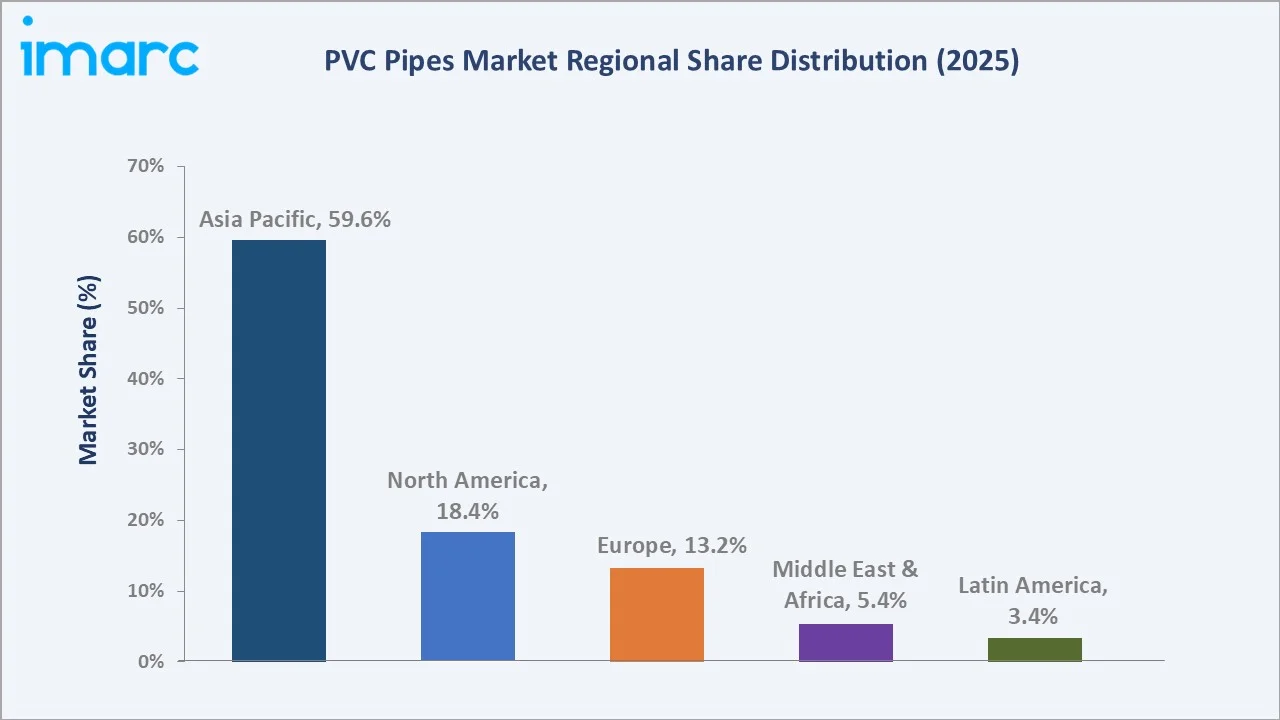

Asia Pacific (59.6% share, 2025) |

|

Largest Application |

Irrigation (43.9% share, 2025) |

Asia Pacific dominates with a commanding 59.6% market share in 2025, supported by large-scale public infrastructure projects across China, India, and Southeast Asia. The Irrigation application segment holds the largest share at 43.9%, reflecting the critical role of PVC pipes in modern agricultural water management worldwide.

To get more information on this market, Request Sample

The market is experiencing steady growth, fueled by urbanization, increasing infrastructure development, and the rising demand for sustainable and reliable piping solutions. Additionally, advancements in manufacturing technologies, along with a growing focus on eco-friendly materials, are further driving innovation and adoption of PVC pipes across both developed and emerging economies.

Executive Summary

The global PVC pipes market is experiencing steady expansion, underpinned by structural drivers including rapid urbanization, large-scale water infrastructure investments, and heightened agricultural modernization in developing economies. Volumed at 26.89 Million Tons in 2025, the market is forecast to reach 37.60 Million Tons by 2034, reflecting a CAGR of 3.66% over the forecast period.

Asia Pacific accounts for 59.6% of global demand, driven by China's infrastructure ambitions, India's Jal Jeevan Mission, and Southeast Asia's irrigation development programs. The irrigation segment leads with a 43.9% revenue share, reflecting PVC pipes' central role in modern drip and sprinkler systems.

Water supply follows at 22.4%, propelled by government programs to upgrade aging water distribution networks, particularly in the U.S., where the EPA has allocated USD 48 Billion through 2026 for water and wastewater infrastructure. Technological advancements in PVC formulation, including molecularly oriented PVC-O pipes with enhanced pressure resistance, are broadening application scope and supporting the PVC pipes market growth.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Application) |

Irrigation - 43.9% share (2025) |

|

Second Largest Application |

Water Supply - 22.4% share (2025) |

|

Leading Region |

Asia Pacific - 59.6% revenue share (2025) |

|

Fastest Growing Segment |

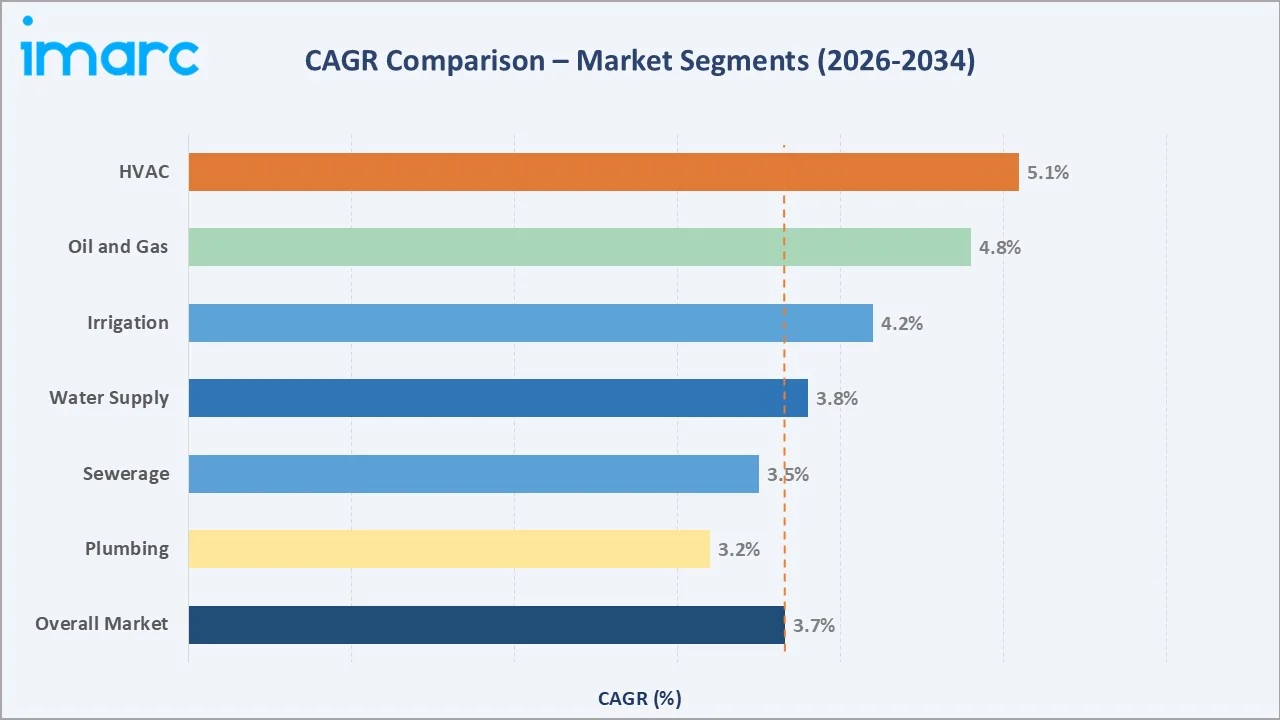

HVAC – estimated CAGR ~5.1% (2026-2034) |

|

Top Companies |

JM Eagle, China Lesso Group, Wavin (Orbia), Aliaxis Holdings, Finolex Industries, Georg Fischer, Sekisui Chemical, Westlake Corp. |

Key Analytical Observations Supporting the Above Data:

- Irrigation dominates with a 43.9% application share (2025), driven by global demand for drip and sprinkler irrigation systems serving over 307 million irrigated hectares worldwide, particularly in Asia, the Americas, and Africa.

- Water Supply represents 22.4% of market revenues (2025), supported by major government investments, including the U.S. EPA's USD 48 Billion water infrastructure commitment through 2026 and India's Jal Jeevan Mission targeting universal household tap water connections.

- Asia Pacific commands 59.6% of global market revenues (2025), driven by China's large-scale urban water projects, India's agricultural expansion, and Southeast Asia's rapid infrastructure investment cycle.

- HVAC is the fastest-growing application segment (estimated CAGR ~5.1%), driven by expanding commercial real estate, smart building adoption, and industrial cooling system deployments in emerging economies.

- PVC-O (molecularly oriented PVC) pipes represent a growing technology disruptor, offering low hydraulic resistance, ultra-high impact strength, excellent flexibility, high earthquake resilience, and superior water hammer resistance, making them ideal for demanding conditions and cost-effective installations.

- Over 2.1 billion people currently lack access to clean drinking water at home (WHO/UNICEF 2025), creating a sustained structural demand driver for PVC pipe networks in water distribution and sanitation infrastructure.

Global PVC Pipes Market Overview

PVC pipes constitute one of the most widely used thermoplastic piping materials across global construction, agriculture, water management, and industrial sectors. Derived from the polymerization of vinyl chloride monomer, PVC pipes offer a distinctive combination of durability, corrosion resistance, lightweight design, and cost-effectiveness that has enabled their adoption across virtually every geographic market and application vertical.

The global PVC pipes industry encompasses raw material suppliers, compounding and stabilizer manufacturers, pipe extrusion facilities, distributors, and end users spanning municipal utilities, contractors, agricultural operators, and industrial enterprises.

Macroeconomic drivers, including urbanization rates, government capital expenditure on water and sanitation infrastructure, agricultural modernization policies, and residential construction activity, directly influence PVC pipe demand. By 2050, with urban populations expected to represent nearly 68% of the global total, demand for reliable piping systems for water supply, sewerage, and building plumbing will continue to scale, anchoring the PVC pipes market forecast at sustained positive growth.

Market Dynamics

To evaluate market opportunities, Request Sample

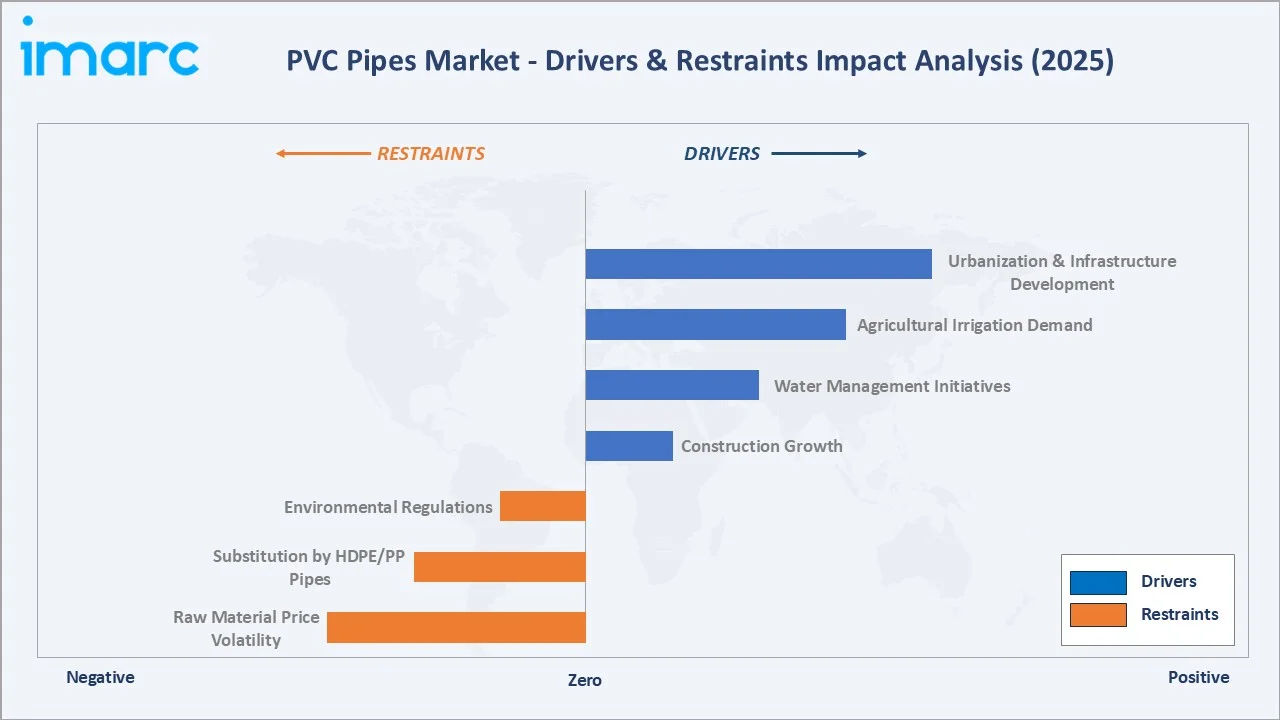

Market Drivers

- Rapid Urbanization and Infrastructure Development: With 55% currently residing in urban areas and the global urban population expected to nearly double by 2050, demand for water supply, sewerage, and plumbing infrastructure has intensified. PVC pipes are the material of choice for these applications.

- Growing Emphasis on Water Conservation and Management: Over 2 billion people lack access to safe drinking water at home (WHO/UNICEF, 2025), while aging municipal pipe networks in developed markets suffer significant leakage, and 6.75 billion gallons of treated water are lost daily in the U.S. alone.

- Rising Agricultural Irrigation Demand: PVC pipes serve as the backbone of modern drip and sprinkler irrigation systems globally. With over 307 million hectares under irrigation worldwide and growing food security imperatives, governments in India, China, Brazil, and across Africa are investing in irrigation modernization.

- Expanding Construction and Housing Activity: The global construction sector continues to expand, with residential and commercial building development fueling consistent demand for PVC pipes in plumbing, drainage, and conduit applications across North America, Europe, and the Asia Pacific.

These drivers collectively reinforce a virtuous demand cycle, rising urban populations stimulate infrastructure investment, which in turn drives consistent volume growth for PVC pipes across application verticals and geographies, supporting the PVC pipes market outlook through 2034.

Market Restraints

- Raw Material Price Volatility: PVC resin prices are sensitive to ethylene and chlorine feedstock costs, which fluctuate with energy prices and supply chain disruptions. Significant price spikes, as experienced in 2021–2022, can compress manufacturer margins and temporarily suppress demand in price-sensitive markets.

- Competition from Alternative Piping Materials: HDPE and PP-R pipes are gaining share in specific applications such as chemical-resistant industrial piping and high-temperature systems, where PVC's thermal limitation creates competitive vulnerability.

- Environmental and Regulatory Pressures: Growing scrutiny over PVC additives and end-of-life disposal challenges is increasing compliance costs for manufacturers, particularly in regions with evolving environmental regulations.

Market Opportunities

- PVC-O Technology Adoption: Molecularly oriented PVC (PVC-O) pipes, offering 50% greater tensile strength with reduced material use. Their adoption in municipal pressure water and irrigation systems is accelerating, supported by Prayag Polymers' PVC-O product launch in India (April 2025), targeting agricultural and urban supply applications.

- Emerging Market Water Infrastructure: Sub-Saharan Africa, Southeast Asia, and South Asia collectively represent hundreds of billions of dollars in planned water infrastructure investment through 2034.

- Recycled Content Innovation: With new underground PVC ducts already incorporating recycled PVC content, this trend is expanding across the continent and represents a sustainable growth avenue for manufacturers with recycling capabilities.

Market Challenges

- Skilled Installation Workforce Shortages: The adoption of advanced piping systems, including PVC-O and CPVC, requires skilled installation contractors. In many emerging markets, shortages of trained installers slow the pace of infrastructure project completion and limit market penetration of premium pipe products.

- Supply Chain Complexity: Global PVC pipe supply chains span resin production, additive sourcing, compounding, extrusion, and multi-tier distribution. Disruptions at any stage, as demonstrated during COVID-19, can create significant delays and price dislocations across regional markets.

- Counterfeit and Substandard Products: In developing markets, the prevalence of substandard or counterfeit PVC pipes undermines market quality benchmarks, creates pricing pressure for compliant manufacturers, and generates end-user trust challenges that slow adoption of branded premium products.

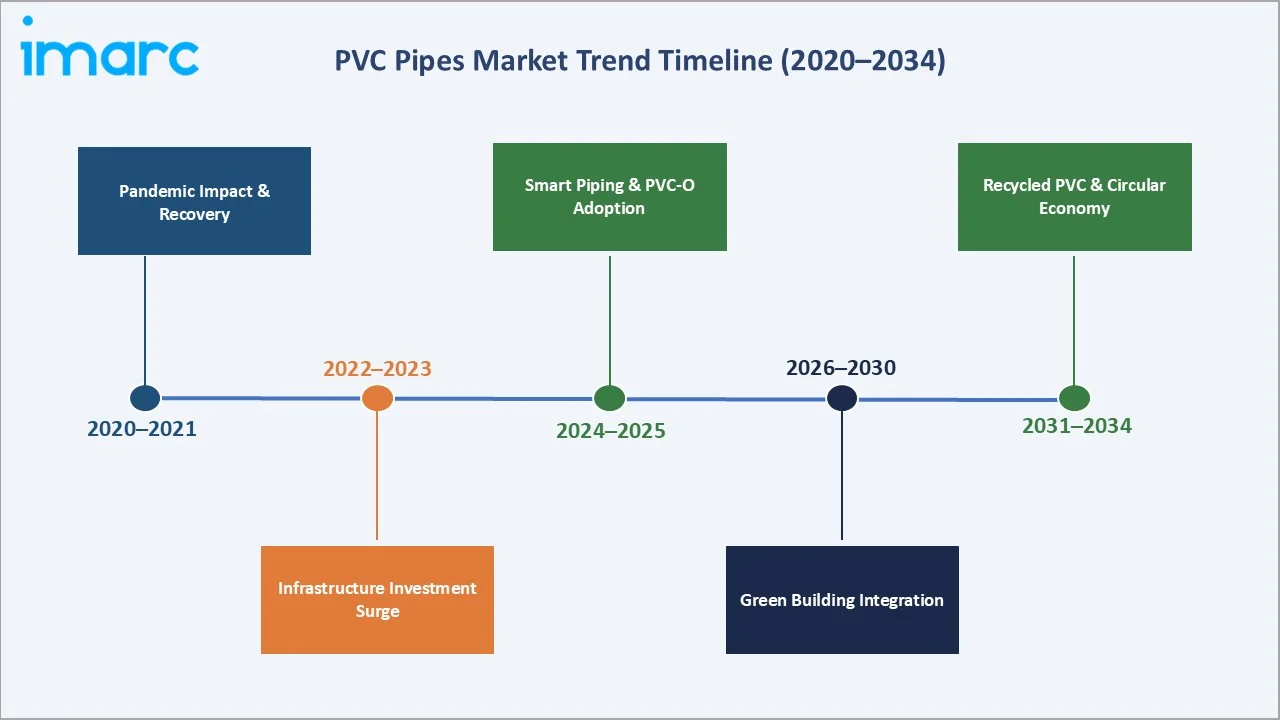

Emerging Market Trends

1. Rapid Urbanization and Smart City Infrastructure Development

As governments in Asia, Africa, and Latin America accelerate smart city development, demand for integrated water supply, sewerage, and underground conduit systems is intensifying. India's smart cities mission, China's 14th Five-Year Plan water infrastructure programs, and Africa's expanding urban housing projects are collectively deploying hundreds of thousands of kilometers of new PVC pipe networks annually.

2. Advancement of Molecularly Oriented PVC (PVC-O) Technology

Molecor's TOM PVC-O pipes, including the record-breaking DN1200 mm diameter variant, showcased at Vinyl India 2025, and Westlake Pipe & Fittings' USD investment in a 190,000 sq ft PVC-O production facility (2024), signal accelerating commercial adoption of this technology globally.

3. Growing Government Investments in Water and Sanitation Infrastructure

The U.S. EPA's USD 48 billion commitment to water, wastewater, and stormwater infrastructure by 2026, India's Jal Jeevan Mission targeting universal rural household tap connections, and Saudi Arabia's Vision 2030 water desalination and distribution expansion are among the most prominent examples.

4. Digitalization of Supply Chain and Distribution Channels

Wavin, the building and infrastructure business of Orbia, has partnered with digital transformation firm Xebia to enhance its digital customer experience and streamline online sales channels. In parallel, Building Information Modeling (BIM) integration is enabling contractors to specify, plan, and manage PVC piping installations digitally, reducing material waste and improving project efficiency across residential, commercial, and infrastructure construction projects.

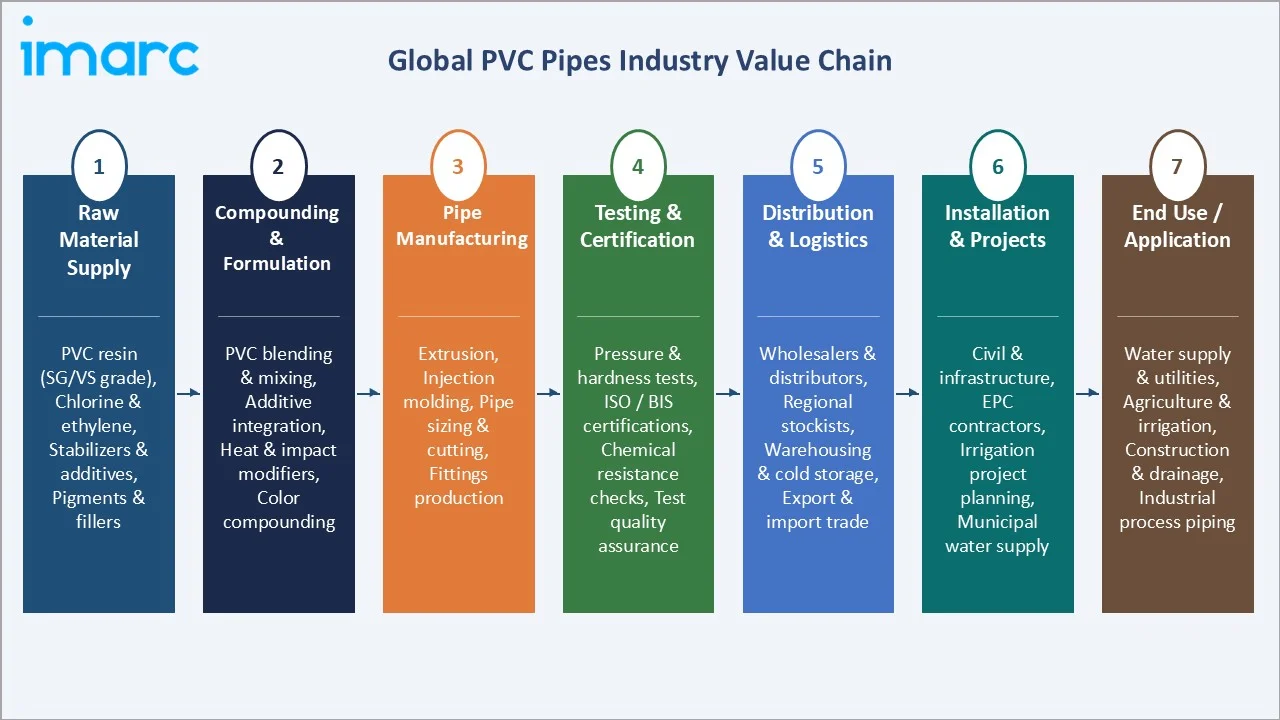

Industry Value Chain Analysis

The PVC pipes value chain is a vertically integrated system spanning petrochemical feedstock production through end-user installation and maintenance. Each stage is populated by specialized operators whose efficiency and innovation capabilities directly influence product quality, cost structure, and market competitiveness globally.

|

Stage |

Key Players / Examples |

|

PVC Resin Production |

Shin-Etsu Chemical, Formosa Plastics, Westlake Corp., Oxy Vinyls, INEOS Inovyn |

|

Additives & Stabilizers |

Baerlocher, Clariant, Lanxess |

|

Pipe Manufacturing |

JM Eagle, China Lesso Group, Wavin (Orbia), Aliaxis Holdings, Finolex Industries, Sekisui Chemical, Westlake Corp. |

|

Quality Testing & Standards |

ASTM International, ISO, Bureau Veritas, SGS, and national standards bodies |

|

Distribution & Logistics |

Harrington, DNOW, regional building materials distributors |

|

Installation & Contracting |

Civil contractors, irrigation system installers, plumbing professionals |

|

End Users |

Municipal water utilities, agricultural enterprises, construction developers, and industrial operators |

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Irrigation |

43.9% |

2025 |

|

Region |

Asia |

59.6% |

2025 |

By Application

Irrigation represents the largest application segment with a 43.9% share of the global PVC pipes market in 2025, reflecting the material's critical role in modern agricultural water management. Government programs promoting agricultural modernization, particularly in India (Pradhan Mantri Krishi Sinchayee Yojana), China (rural water conservancy programs), and across Sub-Saharan Africa, are generating substantial volume demand.

To access detailed market analysis, Request Sample

Water supply follows at 22.4%, driven by urban water distribution network investments, aging infrastructure replacement initiatives, and expanding access programs in developing regions. Together, irrigation and water supply account for 66.3% of total revenues, underscoring the market's concentration in water management applications and the central role of PVC pipes in global water security efforts.

Regional Analysis

Asia Pacific is the dominant region, commanding 59.6% of global PVC pipes revenues in 2025. India is the second-largest contributor, with the launch of the Jal Jeevan Mission (JJM) in 2019, 77.65% of rural households. This equates to 15,00,27,135 homes, which have been provided with tap water connections, generating massive PVC pipe procurement volumes.

|

Region |

Share (2025) |

Key Drivers |

Regulatory Impact |

Major Companies |

|

Asia Pacific |

59.6% |

Urbanization, agricultural irrigation, China & India infrastructure programs |

Govt. mandates; BIS/GB/T standards |

China Lesso, Finolex, Sekisui |

|

North America |

18.4% |

Aging infrastructure replacement, EPA investments, and residential construction growth |

EPA Safe Drinking Water Act; ASTM/NSF |

JM Eagle, Westlake, North American Pipe Corporation (NAPCO) |

|

Europe |

13.2% |

Sustainable building regulations, recycled PVC adoption, and wastewater system upgrades |

EU REACH; circular economy directives |

Wavin, Georg Fischer, Aliaxis |

|

Middle East & Africa |

5.4% |

Water scarcity solutions, desalination infrastructure, and urban housing expansion |

Vision 2030 policy; ISO compliance |

National Plastic Factory (UAE) or Saudi Arabian Amiantit Company, GF, Aliaxis |

|

Latin America |

3.4% |

Agriculture modernization, municipal water access programs, and construction growth |

ABNT standards; local content rules |

Tigre SA, Amanco Wavin (Orbia), Durman (Aliaxis) |

North America represents 18.4% of global market revenues, with the U.S. as the primary market. The country's 2.2 million miles of underground water pipes, much of it aging and leaking, are generating substantial replacement demand. The U.S. EPA's allocation of USD 48 billion in water, wastewater, and stormwater infrastructure funding through 2026 is the single largest government demand catalyst in the region.

Competitive Landscape

The global PVC pipes market is characterized by a moderately fragmented competitive landscape, with a mix of large multinational manufacturers and strong regional players. Leading global operators, JM Eagle (US), China Lesso Group (China), Wavin/Orbia (Netherlands/Mexico), Aliaxis (Belgium), and Georg Fischer (Switzerland), compete through product innovation, geographic expansion, and capacity investments.

|

Company Name |

Brand Name |

Position |

Core Strength |

|

JM Eagle |

Eagle Green PE |

Global Leader |

Largest US PVC pipe producer; Eagle Green PE; capacity expansion in Iowa (March 2024) |

|

China Lesso Group |

LESSO/SNOW (Singapore-specific brand) |

Global Leader |

Dominant Asia Pacific presence; diversified plastic pipe portfolio; export expansion |

|

Wavin (Orbia) |

Wavin |

Global Leader |

Digital platform launch (October 2024); USD 52.6M Indonesia facility; circular economy focus |

|

Aliaxis Holdings |

IPEX, Nicoll, Vinidex, Philmac, Durman, Marley, and Ashirvad (Inauguration by Aug 2026) |

Challenger |

CPVC acquisition (Aug 2024); two India greenfield plants by FY27; portfolio diversification |

|

Finolex Industries |

Finolex |

Regional Leader |

Agriculture & plumbing PVC; manufacturing capacity expansion |

|

Georg Fischer |

GF Piping Systems / +GF+ |

Regional Leader |

Premium industrial piping systems, chemical resistance specialty, European leadership |

|

Sekisui Chemical |

ESLON |

Challenger |

Strong Asia-Pacific presence; advanced PVC compounding technology; infrastructure and housing segment focus |

|

Westlake Corp. |

Westlake |

Challenger |

Vertically integrated PVC resin and pipe producer; North American manufacturing scale; cost-competitive positioning |

Consolidation activity is accelerating: Aliaxis acquired Johnson Controls' CPVC pipe business in August 2024, while JM Eagle expanded its Iowa production plant in March 2024. The competitive intensity is driven by pricing competition in commodity segments, product differentiation through PVC-O and sustainable formulations, and digital platform investments.

Key Company Profiles

JM Eagle

JM Eagle is one of the world’s largest PVC and PE pipe manufacturers, operating around 22 production facilities across North America as of 2025. The company supplies municipal water utilities, agricultural operators, and the construction sector with a comprehensive range of pressure, drainage, and conduit pipe products.

- Product Portfolio: PVC pressure pipes, HDPE pipes, conduit pipes, and fittings for irrigation, water supply, sewerage, and electrical conduit applications.

- Recent Developments: Launched the Eagle Green PE pipe line and completed a major capacity expansion at its Iowa manufacturing facility in March 2024, enhancing output for Midwest water infrastructure projects.

- Strategic Focus: Strengthening domestic US manufacturing capacity, expanding sustainable product lines, and targeting municipal water infrastructure replacement programs supported by EPA funding.

China Lesso Group

China Lesso Group is one of the largest plastic pipe and fittings manufacturers in Asia, headquartered in Guangdong, China. The company operates across residential, commercial, agricultural, and infrastructure segments, with a diversified portfolio spanning PVC, PE, and PP-R pipe systems.

- Product Portfolio: PVC-U, PVC-M, and PVC-O pressure pipes; HDPE, PP-R, and CPVC pipe systems; fittings and valves for water supply, drainage, irrigation, and HVAC applications.

- Recent Developments: Expanded export operations under the SNOW brand in Singapore; continued capacity investment across Chinese manufacturing hubs to support domestic infrastructure demand.

- Strategic Focus: Dominance in the Asia Pacific market through scale and cost competitiveness, export expansion into Southeast Asia and Africa, and diversification into value-added plastic building materials.

Wavin (Orbia)

Wavin, the building and infrastructure business of Orbia, is a leading global manufacturer of plastic pipe systems headquartered in the Netherlands. With operations in over 90 countries, Wavin serves the residential, commercial, and civil infrastructure sectors with a strong emphasis on sustainability and digital innovation.

- Product Portfolio: PVC, PE, and PP pipe systems for water supply, sewerage, drainage, and underfloor heating; smart water management solutions; climate-resilient urban drainage systems.

- Recent Developments: Launched a digital customer experience platform in partnership with Xebia in March 2024; commenced operations at its USD 52.6 million manufacturing facility in Indonesia to serve Southeast Asian market growth.

- Strategic Focus: Circular economy leadership through recycled-content pipe development; digital supply chain transformation; geographic expansion in high-growth Asia Pacific markets; sustainable building solutions.

Aliaxis Holdings

Aliaxis is a Belgian multinational and one of the world’s largest manufacturers and distributors of advanced piping systems, serving the construction, utilities, and industrial sectors across more than 40 countries through a portfolio of strong regional brands.

- Product Portfolio: PVC, CPVC, PE, and PP pipe systems for plumbing, drainage, irrigation, and industrial applications; marketed under brands including IPEX, Nicoll, Vinidex, Philmac, Durman, Marley, and Ashirvad.

- Recent Developments: Acquired Johnson Controls’ CPVC pipe business in August 2024, strengthening its position in high-performance piping; announced two greenfield manufacturing plants in India expected to be inaugurated by FY27.

- Strategic Focus: Portfolio diversification through CPVC and specialty pipe expansion; strengthening the India and Southeast Asia market position; leveraging multi-brand architecture for regional market penetration.

Market Concentration Analysis

The global PVC pipes market exhibits moderate concentration at the top tier, with the leading five manufacturers holding a significant but non-dominant revenue share. This reflects the industry's dual structure: a concentrated upper tier of large multinational and national champions, and a highly fragmented long tail of regional and local producers, particularly in Asia and the Latin America, that serve domestic markets with commodity-grade products in the PVC Pipes Market in Latin America.

The premium and specialty pipe segments (PVC-O, CPVC, industrial-grade) exhibit a higher concentration than standard pressure and drain pipes, as technical barriers to entry are more significant. M&A activity is gradually consolidating market share among global players: Aliaxis's CPVC acquisition, Orbia's consolidation of Wavin, and potential further bolt-on acquisitions in India and Southeast Asia are expected to reshape the competitive structure over the forecast period.

Investment & Growth Opportunities

Fastest Growing Segments

HVAC (est. CAGR ~5.1%), Oil and Gas (~4.8%), and Irrigation (~4.2%) represent the highest-growth investment vectors in the global PVC pipes market through 2034. HVAC growth is underpinned by expanding commercial real estate and smart building development, while oil and gas demand is driven by cost-competitive PVC pipe adoption in non-critical upstream and midstream applications.

Emerging Market Expansion

India's pipe market alone is expected to add millions of tons of incremental demand through 2030, supported by Jal Jeevan Mission, AMRUT 2.0 urban water projects, and expanding agricultural irrigation. Indonesia's rapidly urbanizing population and Wavin's USD 52.6 Million manufacturing investment (2024) signal the Southeast Asian market's strategic importance for global operators.

Sustainability and Technology Investment Themes

Investment in recycled PVC compound technology, PVC-O pipe manufacturing lines, and digital supply chain platforms are the three highest-return innovation themes through 2034. European circular economy compliance is creating immediate demand for recycled-content products, while PVC-O adoption is gaining traction across markets seeking superior performance at lower material cost.

Future Market Outlook (2026-2034)

The global PVC pipes market is positioned for sustained, broad-based growth through 2034, anchored by structural drivers of urban population growth, water infrastructure investment urgency, and agricultural modernization. From a 2025 base of 26.89 Million Tons, the market is forecast to reach 37.60 Million Tons by 2034, representing an absolute incremental volume addition of 10.71 Million Tons over the forecast horizon.

Technological disruptions, including PVC-O commercialization at scale, AI-enabled quality control in manufacturing, and digital pipe network monitoring, will reshape cost and performance benchmarks. Manufacturers that combine scale, product innovation, and geographic diversification into emerging markets will be best positioned to capture a disproportionate share of the PVC pipes market forecast through 2034.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 180 industry participants in 2024–2025, comprising PVC pipe manufacturers, raw material suppliers, municipal water utility procurement officers, agricultural contractors, construction engineers, and industry associations across Asia Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, government infrastructure program databases, WHO/UNICEF water access publications, EPA investment announcements, trade associations, and publicly available financial disclosures. Over 280 secondary sources were reviewed, validated, and triangulated to ensure data accuracy and consistency.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, per capita water consumption data, government infrastructure expenditure budgets, and historical market performance patterns. Scenario analysis was conducted to account for raw material price volatility and macroeconomic uncertainty.

PVC Pipes Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Irrigation, Water Supply, Sewerage, Plumbing, HVAC, Oil and Gas |

| Regions Covered | Asia, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | JM Eagle, China Lesso Group, Wavin (Orbia), Aliaxis Holdings, Finolex Industries, Georg Fischer, Sekisui Chemical, Westlake Corp., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the PVC Pipes market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global PVC Pipes market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the PVC Pipes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the PVC Pipes Market Report

The global PVC pipes market was volumed at 26.89 Million Tons in 2025, driven by rising urbanization, agricultural irrigation demand, and government-led water infrastructure investments worldwide.

The market is projected to reach 37.60 Million Tons by 2034, exhibiting a CAGR of 3.66% during 2026-2034, supported by expanding construction activity, smart irrigation systems, and aging infrastructure replacement programs.

Key drivers include rapid urbanization, rising investments in water supply and sewerage infrastructure, agricultural modernization programs, growth in residential and commercial construction, and increasing adoption of PVC-O technology for municipal applications.

Asia Pacific currently dominates the PVC pipes market, accounting for a share of 59.6% in 2025, driven by China's infrastructure programs, India's Jal Jeevan Mission, and Southeast Asia's rapid urbanization and agricultural development.

Irrigation is the largest application segment with a 43.9% share in 2025, reflecting PVC pipes' essential role in drip and sprinkler systems across over 307 million globally irrigated hectares.

HVAC is the fastest-growing application segment (est. CAGR ~5.1%), driven by expanding commercial real estate development, smart building adoption, and industrial facility construction globally.

Key trends include PVC-O (molecularly oriented PVC) technology adoption, government water infrastructure investment surges, circular economy-driven recycled PVC pipe development, digitalization of supply chains, and agricultural irrigation modernization.

Major players include JM Eagle, China Lesso Group, Wavin (Orbia), Aliaxis Holdings, Finolex Industries, Georg Fischer, Sekisui Chemical, Westlake Corp., etc.

Water supply demand is driven by aging pipeline replacement (the U.S. loses 6 billion gallons of treated water daily), the EPA's USD 48 Billion water infrastructure investment through 2026, and global programs to extend safe drinking water access to 2+ billion people currently lacking it.

High-growth opportunities include PVC-O manufacturing technology, recycled-content pipe production for European markets, agricultural irrigation systems in Asia/Africa, and digital distribution platform development for enhanced market reach.

Sustainability is reshaping procurement, with over 60% of new Dutch underground PVC ducts using recycled content (2025). European circular economy mandates and green building certifications are accelerating demand for eco-certified PVC pipes globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade