Robotics Technology Market Size, Share, Trends and Forecast by Component, Robot Type, Application, and Region, 2026-2034

Robotics Technology Market Size and Share:

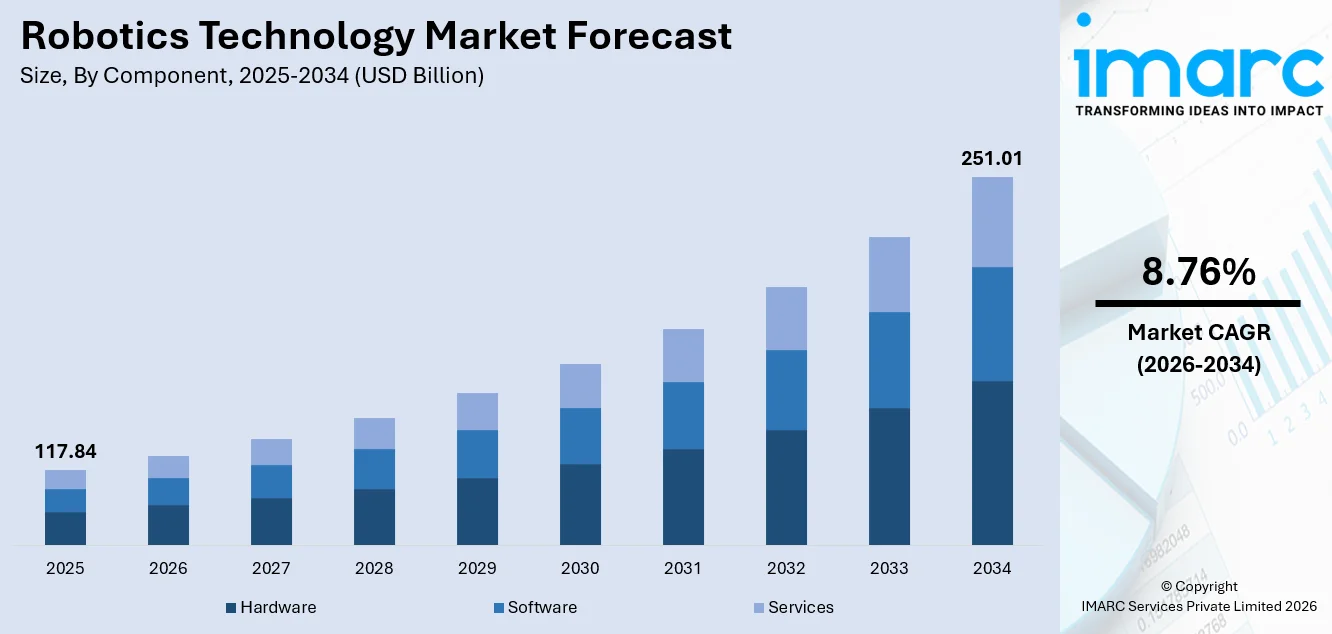

The global robotics technology market size was valued at USD 117.84 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 251.01 Billion by 2034, exhibiting a CAGR of 8.76% from 2026-2034. North America currently dominates the market, holding a market share of 31% in 2025. The region benefits from strong investments in industrial automation, the presence of leading technological companies, growing demand for collaborative robots in manufacturing, and supportive government initiatives promoting advanced robotics adoption across key sectors, all contributing to the robotics technology market share.

The utmost use of robotics in manufacturing and service industries is one of the key factors driving robotic technology market growth. The demand for accuracy, efficiency, and precision in production is driving companies towards robotic solutions now than before. Moreover, decreasing prices of robotic parts such as sensors, actuators and processors are making robotics solutions affordable for small and medium enterprises. As labor scarcity intensifies in developed nations, many industries are turning towards robotics to ensure consistent productivity. The increasing importance of safety at the workplace as well as a need to minimize human interaction with hazardous-working environments is expected to drive the adoption of robots over varying industry verticals. Thus, supporting the robotic technology market growth.

The United States has emerged as a major region in the robotics technology market owing to many factors. The country has a well-established technology infrastructure and a strong ecosystem of research institutions and technology companies that continuously advance robotics capabilities. In February 2026, North American robot orders rose by 6.6 % in 2025, led by non‑automotive sectors as collaborative robots gained traction, signaling broader adoption beyond traditional automotive use. [CK2] The increasing adoption of automation in automotive, electronics, and food processing industries is accelerating the demand for industrial and collaborative robots. Additionally, the growing focus on reshoring manufacturing operations is further propelling investments in robotic automation. Moreover, the rising demand for service robots in healthcare, logistics, and defense applications is creating new avenues for market expansion, strengthening the overall robotics technology market outlook.

To get more information on this market Request Sample

Robotics Technology Market Trends:

Expansion of Collaborative Robotics

Collaborative robots, commonly known as cobots, are increasingly being deployed across various industries to work alongside human operators in shared workspaces. Unlike traditional industrial robots that require safety cages and separated work zones, cobots are designed with advanced sensors and force-limiting capabilities that allow them to operate safely near humans. As per sources, Doosan Robotics announced new AI‑driven cobot systems aimed at simplifying robot programming and accelerating adoption in logistics and industrial settings, illustrating how manufacturers are enhancing usability for end users. The integration of intuitive programming interfaces and drag-and-teach functionality is making cobots more accessible to operators without specialized programming skills. Industries such as automotive, electronics, food processing, and pharmaceuticals are adopting cobots to enhance productivity while maintaining flexibility in production lines.

Integration of Artificial Intelligence

The convergence of artificial intelligence (AI) with robotic systems is transforming the capabilities and applications of modern robots, supporting the robotics technology market forecast. Machine learning (ML) algorithms and deep learning models are enabling robots to perceive their environments more accurately, make real-time decisions, and adapt to dynamic conditions without requiring manual reprogramming. In 2026, Google DeepMind and Tesla announced a collaboration to integrate advanced AI perception models into Tesla’s Optimus humanoid robots to improve environmental awareness and task adaptability, highlighting cross‑industry AI‑robotics partnerships. Computer vision systems powered by AI are allowing robots to identify objects, detect defects, and navigate complex environments with greater precision. Natural language processing capabilities are enabling more intuitive human-robot interactions, facilitating deployment in customer-facing roles across retail and hospitality sectors.

Rising Adoption of Autonomous Mobile Robots

Autonomous mobile robots are gaining significant traction across logistics, warehousing, and manufacturing environments as organizations seek to optimize material handling and internal transportation processes. These robots utilize a combination of simultaneous localization and mapping technologies, light detection and ranging sensors, and sophisticated path planning algorithms to navigate dynamic environments independently. In December 2024, ABB opens Autonomous Mobile Robotics training and showroom facility highlighting advanced AMRs with AI‑based Visual SLAM navigation and software for easier deployment in complex warehouse and factory operations . The healthcare sector is also adopting autonomous mobile robots for tasks such as medication delivery, specimen transport, and facility disinfection. As warehouse and factory layouts become increasingly complex, the demand for flexible and scalable autonomous navigation solutions continues to expand, reflecting the key robotics technology market trends shaping the broader automation landscape.

Robotics Technology Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global robotics technology market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on component, robot type, and application.

Analysis by Component:

- Hardware

- Software

- Services

Hardware holds 45% of the market share, encompassing physical components, including robotic arms, end-effectors, controllers, sensors, actuators, and drive systems that form the structural and functional foundation of robotic systems. The demand for hardware components is driven by the expanding deployment of robots in manufacturing, logistics, and service industries, where mechanical precision and reliability are essential. In November 2025, Viam announced a strategic partnership with Universal Robots to integrate UR’s cobot hardware into its industrial automation platforms, underscoring growing collaboration between robotics software engineers and hardware manufacturers to accelerate real‑world deployments. Advances in lightweight materials and miniaturized components are enabling the development of more compact and efficient robotic platforms suitable for diverse applications. Additionally, the growing adoption of collaborative robots is creating demand for safety-rated hardware components, including force-torque sensors and compliant actuators.

Analysis by Robot Type:

- Traditional Industrial Robots

- Cobots

- Professional Service Robots

- Others

The traditional industrial robots still dominate the industry, with a market share of 40%. Majority of the application is in the automotive, electronics, metal processing and heavy industry. The robots carry out repetitive jobs with precision like welding, painting, assembling and material transfer. The reason traditional industrial robots are more popular is due to them being faster, having a heavier payload and higher accuracy, usually in a big production plant. These robots operate in a limited environment on pre-programmed commands so, the output quality is consistent and very high. The conventional industrial robot functionality will be enhanced with the addition of advanced servo motors and motion control technology that allow for shorter cycle times and increased energy efficiency. Manufacturing processes, particularly in the automotive industry and the aerospace sector, are growing increasingly complex. This is giving rise to multi-axis industrial robots that can perform various motions with a high degree of repeatability. Furthermore, the increasing popularity of lean manufacturing techniques is fueling the adoption of industrial robots in order to eliminate waste and optimise resource usage in factories.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Manufacturing

- Healthcare

- Aerospace and Defence

- Media and Entertainment

- Logistics

- Others

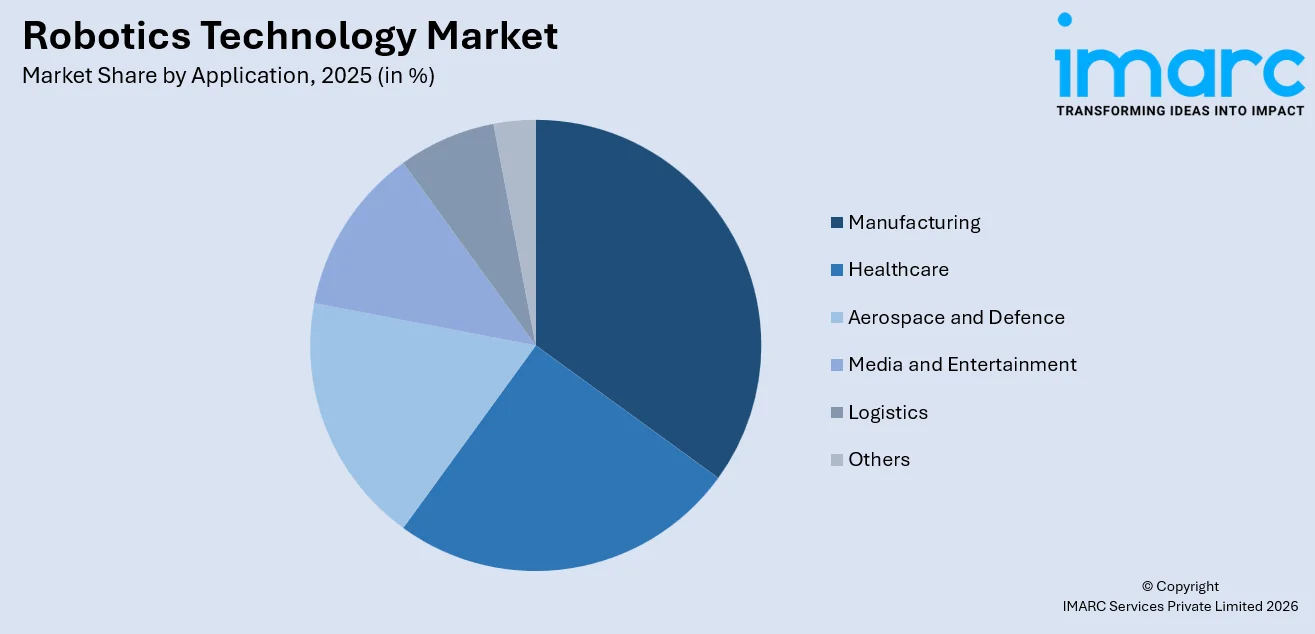

Manufacturing dominates the market, with a share of 28%, representing the most significant application area for robotics technology, driven by the need for automated production systems that deliver consistent precision, high throughput, and operational efficiency. Robotic systems are extensively deployed across automotive assembly lines, electronics fabrication facilities, metal processing plants, and consumer goods production units. The demand for manufacturing automation is fueled by the need to reduce production costs, minimize defects, and improve workplace safety by replacing manual labor in hazardous or ergonomically challenging tasks. The growing trend toward smart manufacturing and Industry 4.0 integration is further accelerating the adoption of advanced robotic systems that can communicate with other machines and enterprise resource planning platforms. Flexible manufacturing systems that leverage robotic automation are enabling producers to adapt quickly to changing product specifications and market demands, reducing lead times while maintaining quality standards across diverse product portfolios.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 31% of the share, enjoys the leading position in the market. The region benefits from a mature industrial base, strong technological infrastructure, and substantial investments in research and development across automotive, aerospace, defense, and healthcare sectors. The presence of established robotics manufacturers and a robust ecosystem of technology integrators support the continued adoption of both industrial and service robots. Additionally, the emphasis on advanced manufacturing initiatives and digital transformation programs is driving the integration of robotic systems across production facilities. The growing demand for warehouse automation and autonomous logistics solutions is further contributing to regional market expansion. Favorable government policies and funding mechanisms supporting robotics innovation and workforce development are strengthening the competitive position of North American markets. The region also benefits from a strong venture capital ecosystem that supports the commercialization of emerging robotic technologies and accelerates the deployment of next-generation automation solutions across diverse industries.

Key Regional Takeaways:

United States Robotics Technology Market Analysis

The United States represents a dominant force in the North American robotics technology market, driven by a combination of strong industrial infrastructure, significant research and development capabilities, and a favorable environment for technological innovation. The country's automotive industry remains one of the largest consumers of industrial robots, with robotic systems extensively deployed across assembly, welding, and painting operations. The growing adoption of collaborative robots in electronics manufacturing and food processing is expanding the application base beyond traditional heavy industries. Additionally, the logistics and warehousing sector is experiencing rapid automation, with autonomous mobile robots being deployed to address rising e-commerce fulfillment demands. The healthcare industry is also emerging as a significant adopter of robotic technology, with surgical robots and rehabilitation systems gaining broader acceptance among medical institutions. Government initiatives aimed at promoting advanced manufacturing and maintaining global competitiveness are supporting investments in robotic automation. The strong presence of technology companies and academic research institutions focused on AI and ML is further accelerating the development of next-generation robotic systems, creating a comprehensive ecosystem for sustained innovation and widespread deployment.

Europe Robotics Technology Market Analysis

Europe represents a significant market for robotics technology, supported by a well-developed manufacturing sector and strong emphasis on industrial automation. The automotive industry in countries such as Germany, France, and Italy has been a longstanding driver of industrial robot adoption, with robotic systems integrated into assembly lines and precision machining operations. The increasing focus on sustainable manufacturing practices and energy efficiency is encouraging the deployment of advanced robotic systems that optimize resource consumption and reduce waste generation. Additionally, the European Union's strategic initiatives promoting digital transformation and Industry 4.0 adoption are accelerating investments in robotics across small and medium enterprises. The healthcare sector is witnessing growing adoption of surgical and rehabilitation robots, supported by aging demographics and rising demand for precision medical procedures. The logistics sector is also contributing to market expansion, with automated guided vehicles and autonomous mobile robots being deployed in warehousing and distribution operations. Furthermore, stringent occupational safety regulations are encouraging manufacturers to adopt robotic solutions that minimize human exposure to hazardous environments across industrial and commercial settings.

Asia-Pacific Robotics Technology Market Analysis

Asia-Pacific is experiencing rapid expansion in the robotics technology market, driven by the large-scale manufacturing activities in countries such as China, Japan, South Korea, and India. The region is a global hub for electronics, automotive, and semiconductor manufacturing, industries that are significant consumers of industrial and collaborative robots. Government policies in several countries are actively promoting robotic automation to enhance manufacturing competitiveness and address labor challenges associated with demographic shifts. Japan and South Korea maintain established positions as leading producers and adopters of advanced robotic systems, with strong capabilities in robot design and integration. China is rapidly scaling its domestic robotics industry, supported by substantial government investments and growing demand across manufacturing and logistics applications. Additionally, the increasing adoption of service robots in hospitality, retail, and healthcare settings is broadening the scope of robotics deployment across the region.

Latin America Robotics Technology Market Analysis

Latin America is gradually emerging as a growing market for robotics technology, supported by expanding manufacturing activities and increasing foreign direct investment in automation infrastructure. Countries such as Brazil and Mexico are leading the regional adoption of industrial robots, particularly in the automotive and consumer goods manufacturing sectors. The growing emphasis on improving production efficiency and product quality is encouraging manufacturers to integrate robotic systems into their operations. Additionally, government initiatives aimed at modernizing industrial capabilities and enhancing export competitiveness are supporting the deployment of automated solutions. The logistics sector is also contributing to rising demand for robotic technologies, with warehousing and distribution facilities increasingly exploring automation to meet evolving supply chain requirements.

Middle East and Africa Robotics Technology Market Analysis

The Middle East and Africa region is witnessing a gradual increase in the adoption of robotics technology, driven by economic diversification programs and growing investments in advanced manufacturing and infrastructure development. Countries in the Gulf Cooperation Council are actively investing in automation technologies as part of broader industrialization strategies aimed at reducing dependence on hydrocarbon revenues. The construction, oil and gas, and logistics sectors are primary areas of robotic deployment in the region. Additionally, the healthcare sector is beginning to explore robotic solutions for surgical applications and facility management. The growing focus on smart city development and digital transformation initiatives is further creating opportunities for the adoption of service and inspection robots across urban infrastructure and commercial applications.

Competitive Landscape:

The global robotics technology market is characterized by the presence of several established players and a growing number of innovative entrants competing across industrial, collaborative, and service robotics segments. Leading companies are focusing on expanding their product portfolios through the development of advanced robotic platforms that incorporate ML, machine vision, and enhanced connectivity features. Strategic partnerships between robotics manufacturers and technology companies are facilitating the integration of software capabilities with hardware systems, enabling more comprehensive automation solutions. Companies are actively investing in research and development to improve robotic dexterity, payload capacity, and operational versatility to address evolving application requirements. Geographic expansion through partnerships and distribution agreements is a key strategy employed by major players to strengthen their presence in high-growth markets.

The report provides a comprehensive analysis of the competitive landscape in the robotics technology market with detailed profiles of all major companies, including:

- ABB Ltd.

- DENSO Products and Services Americas, Inc.

- Epson America, Inc.

- FANUC Corporation

- Kawasaki Heavy Industries Ltd.

- KUKA AG

- Mitsubishi Electric Corporation

- Nachi Robotic Systems, Inc

- Omron Robotics

- Stäubli International AG

- Yaskawa America, Inc.

Latest News and Developments:

- In October 2025, DEEP Robotics launched the DR02, the world’s first all-weather humanoid robot with an IP66 rating. Designed for rain, dust, and extreme temperatures, it features modular components, high compute power, and human-like payload capacity, enabling applications in industrial operations, security patrols, and harsh-environment tasks.

- In April 2025, Geekplus, a top 50 global robotics company, launched three next-generation warehouse automation solutions at LogiMAT 2025. PopPick v2, RoboShuttle v4, and SkyCube v2 enhance efficiency, storage density, and ergonomics for logistics operations, enabling scalable, safe, and intelligent automation across warehouses while setting new benchmarks for the robotics technology market.

Robotics Technology Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software, Services |

| Robot Types Covered | Liquid, Dry |

| Applications Covered | Manufacturing, Healthcare, Aerospace and Defence, Media and Entertainment, Logistics, Others |

| Region Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | ABB Ltd., DENSO Products and Services Americas, Inc., Epson America, Inc., FANUC Corporation, Kawasaki Heavy Industries Ltd., KUKA AG, Mitsubishi Electric Corporation, Nachi Robotic Systems, Inc, Omron Robotics, Stäubli International AG, Yaskawa America, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the robotics technology market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global robotics technology market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the robotics technology industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Robotics Technology Market Report

The robotics technology market was valued at USD 117.84 Billion in 2025.

The robotics technology market is projected to exhibit a CAGR of 8.76% during 2026-2034, reaching a value of USD 251.01 Billion by 2034.

The robotics technology market is primarily driven by the rising demand for automation across manufacturing, logistics, and healthcare industries, the declining costs of robotic components, and the growing integration of AI capabilities. Additionally, increasing labor shortages, the emphasis on workplace safety, and the expansion of collaborative robotics are further supporting market expansion.

North America currently dominates the robotics technology market, accounting for a share of 31%. The region benefits from strong industrial infrastructure, significant research and development investments, widespread adoption of automation across manufacturing, logistics, and healthcare sectors, and a favorable environment for technological innovation.

Some of the major players in the robotics technology market include ABB Ltd., DENSO Products and Services Americas, Inc., Epson America, Inc., FANUC Corporation, Kawasaki Heavy Industries Ltd., KUKA AG, Mitsubishi Electric Corporation, Nachi Robotic Systems, Inc, Omron Robotics, Stäubli International AG, Yaskawa America, Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)