Salmon Market Size, Share, Trends and Forecast by Type, Species, End Product Type, Distribution Chanel, and Region, 2026-2034

Global Salmon Market Size, Share, Trends & Forecast (2026-2034)

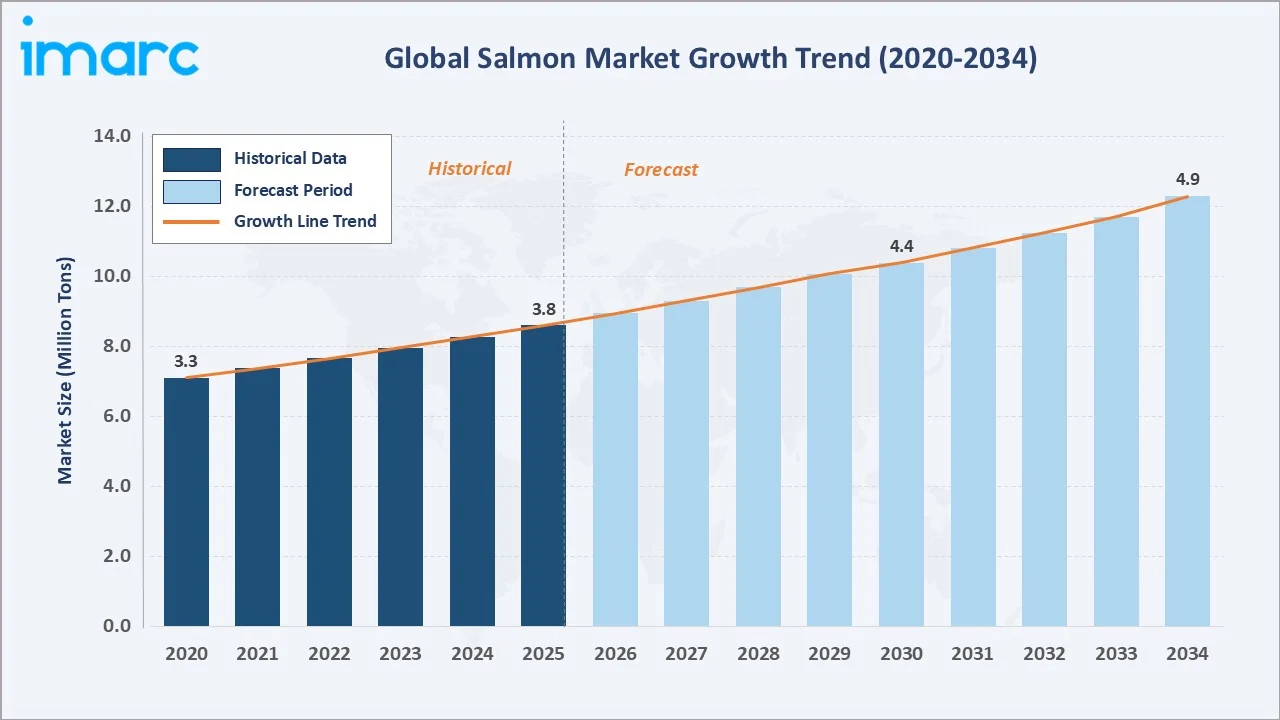

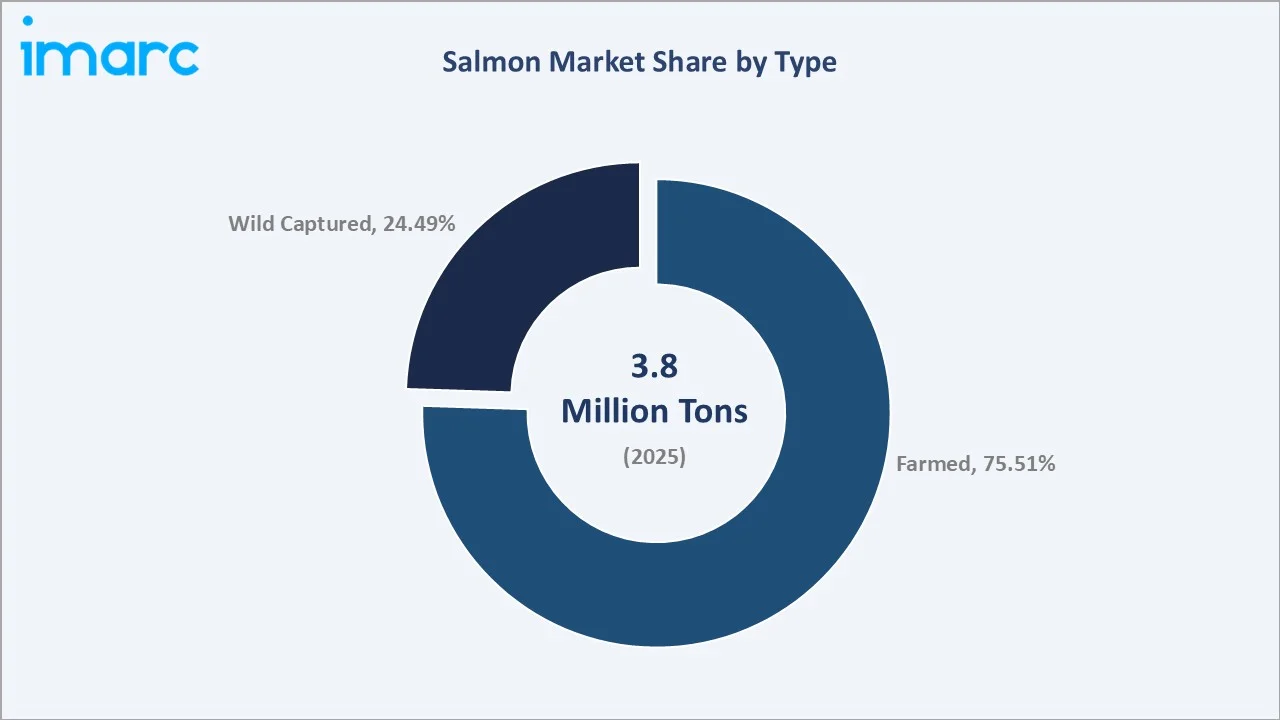

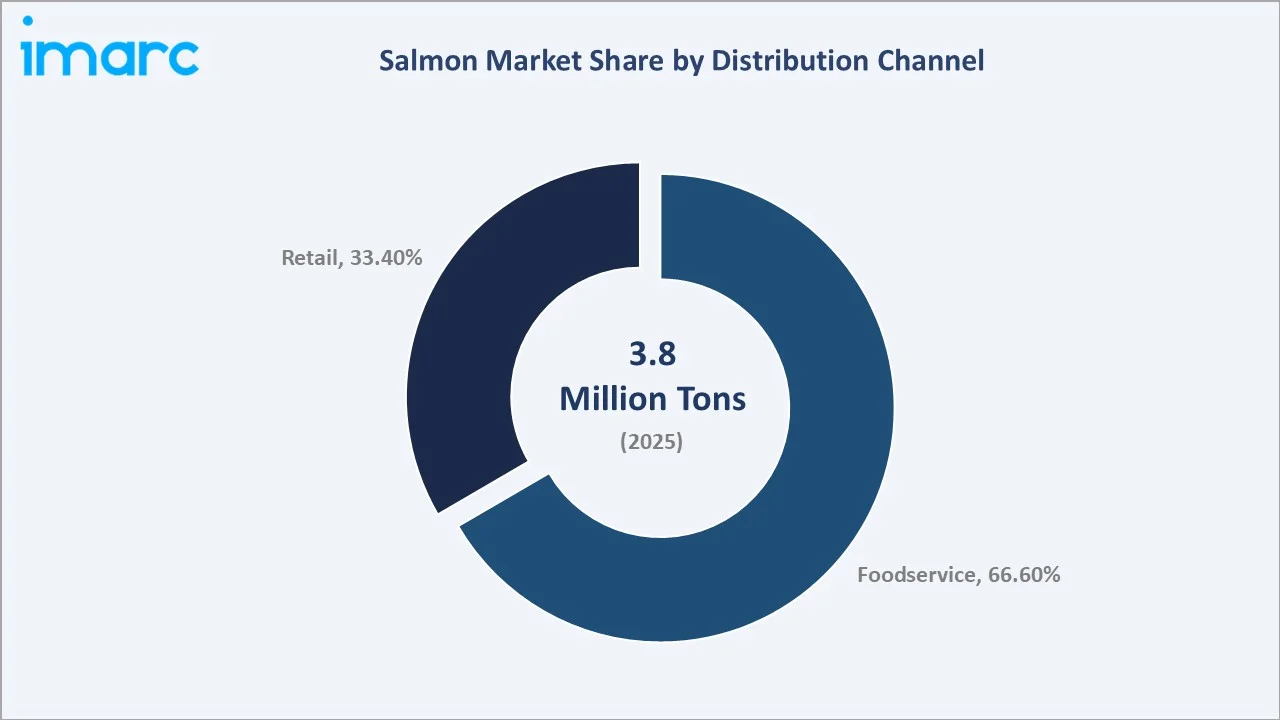

The global salmon market reached a production volume of 3.8 Million Tons in 2025 and is projected to reach 4.9 Million Tons by 2034, expanding at a CAGR of 2.80% during 2026-2034. The salmon market growth is driven by rising consumer demand for omega-3-rich protein, expanding sushi and foodservice culture globally, and continued advances in aquaculture sustainability.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

3.8 Million Tons |

|

Forecast Market Size (2034) |

4.9 Million Tons |

|

CAGR (2026-2034) |

2.80% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

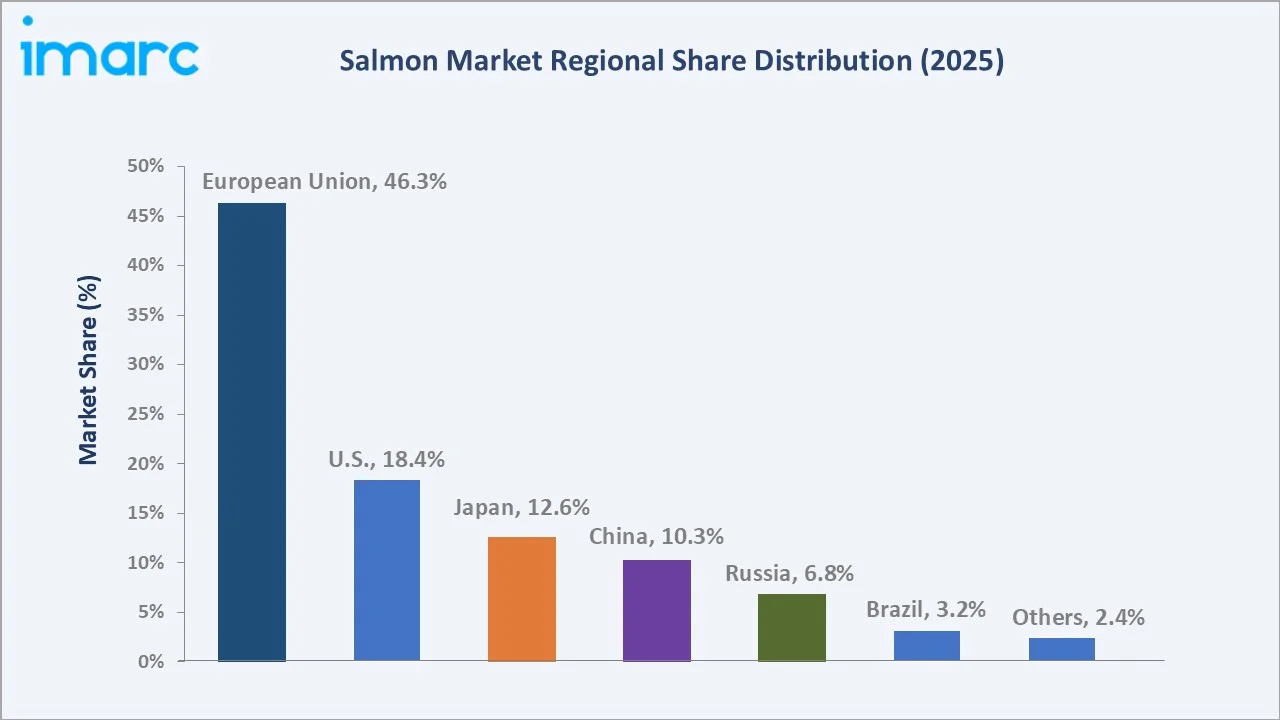

Largest Consuming Region (2025) |

European Union (46.3%) |

|

Fastest Growing Consumer Region |

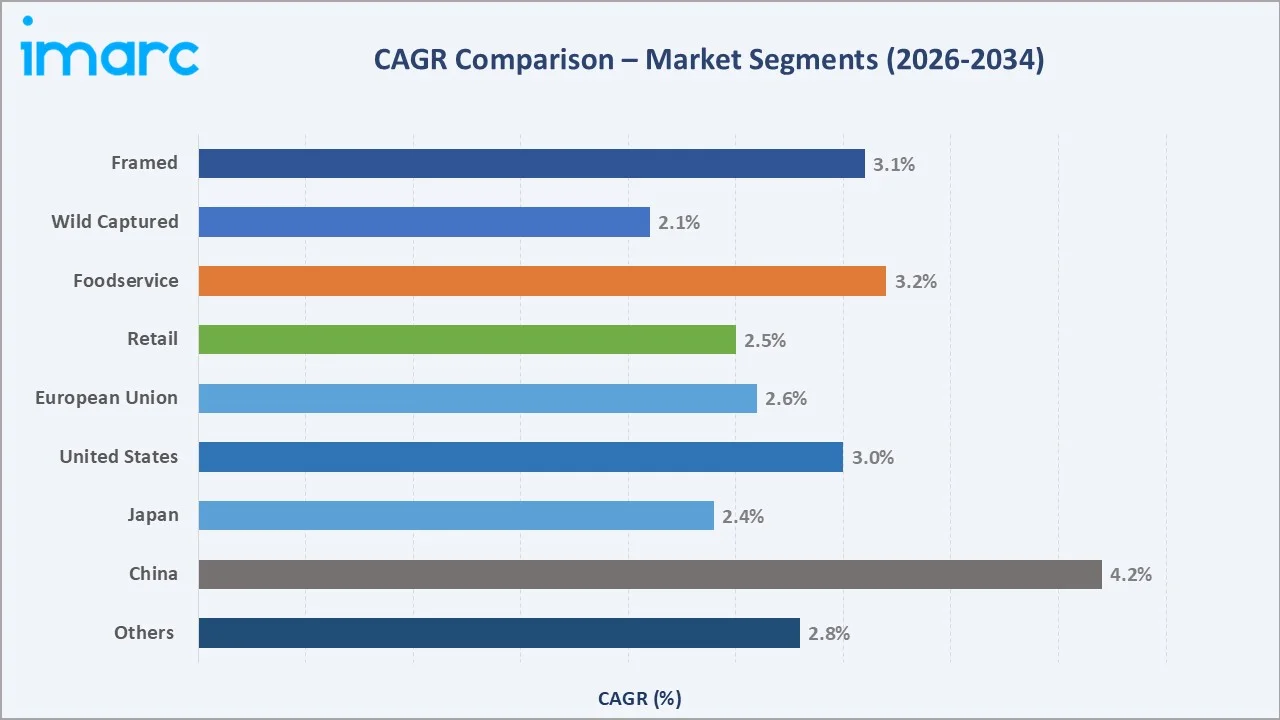

China (CAGR ~4.2%) |

Salmon farming, particularly in countries like Norway, Chile, and Canada, plays a vital role in meeting global demand. The market is also witnessing advancements in farming techniques, aimed at improving efficiency and reducing environmental impact.

To get more information on this market, Request Sample

As consumer awareness of health benefits grows, salmon's popularity as a nutritious protein source continues to rise. Additionally, the market is adapting to changing consumer preferences with a focus on premium, organic, and sustainable products.

Executive Summary

The global salmon market continues to demonstrate steady expansion, underpinned by health-conscious eating trends, aquaculture technology advancements, and the global proliferation of sushi and seafood foodservice culture. Measured at a production volume of 3.8 Million Tons in 2025, the market is projected to reach 4.9 Million Tons by 2034, at a CAGR of 2.80%.

Among key growth drivers, the rising global awareness of omega-3 fatty acids and lean protein benefits is propelling per capita salmon consumption across both established and emerging markets. The European Union retains its position as the largest consuming region with a 46.3% share, driven by deep-rooted seafood culture, strong cold chain infrastructure, and well-established retail and foodservice demand for fresh, smoked, and value-added salmon.

China is the fastest-growing consuming region at a CAGR of ~4.2%, driven by dietary westernization and expanding premium seafood import channels. Norway exported seafood valued at NOK 13.9 billion (USD 1.36 billion) in July 2025, representing a 8% year-on-year increase, according to the Norwegian Seafood Council (NSC). The growth was primarily driven by higher salmon volumes and strong value expansion in the Chinese market.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Farmed Salmon - 75.51% share (2025) |

|

Largest Distribution Channel |

Foodservice - 66.6% share (2025) |

|

Leading Consuming Region |

European Union - 46.3% share (2025) |

|

Fastest Growing Region |

China – CAGR ~4.2% (2026-2034) |

|

Top Producing Nation (Atlantic Salmon) |

Norway - output of 1,238,000 tons (January–September 2025) |

|

Top Companies |

Mowi ASA, SalMar ASA, Lerøy Seafood, AquaChile, Bakkafrost, Cermaq |

Key Analytical Observations Supporting The Above Data:

- Farmed salmon dominates at 75.51% (2025), driven by Norway's extensive fjord aquaculture infrastructure, Chile's Atlantic salmon farms, and Scotland's biosecurity recovery. Farmed salmon contains about 18% fat, three times more than wild salmon, which helps promote faster growth and higher yield.

- Wild captured salmon represents 24.49% (2025), concentrated primarily in Alaskan Pacific salmon fisheries (pink, sockeye, chum) and Russian Far East operations. Pacific salmon make up over 99% of the global wild salmon catch, with pink salmon contributing the largest share of total landings.

- Foodservice leads distribution at 66.6% (2025), reflecting robust demand from sushi restaurants, hotel breakfast buffets, and premium dining establishments globally. The rapid expansion of Japanese-style sushi chains across Southeast Asia, Latin America, and the Middle East is a structural driver of foodservice volume growth through 2034.

- The European Union accounts for 46.3% of global consumption (2025). High per capita seafood consumption, premium cold chain infrastructure, and strong institutional demand from hotel-restaurant-catering (HoReCa) channels underpin the EU's market leadership.

- China is the fastest-growing market (CAGR ~4.2%), fueled by Norway's diplomatic re-entry into Chinese premium seafood channels. China remained the primary destination for raw Atlantic salmon, with imports surpassing 100,000 tons from January to September, marking a 46.4% increase compared to the same period in 2024.

Global Salmon Market Overview

Salmon is among the most nutritionally dense and commercially important seafood species globally. Belonging to the family Salmonidae, salmon are native to cold North Atlantic and Pacific waters, and are commercially harvested through both wild capture fisheries and intensive aquaculture operations. Rich in omega-3 fatty acids, high-quality protein, vitamin D, and selenium, salmon occupies a premium position in healthy diets across developed and emerging markets.

The salmon market's commercial ecosystem is structured across two primary supply streams. Farmed salmon – predominantly Atlantic salmon produced in Norway, Chile, Scotland, Canada, and the Faroe Islands – provides a year-round, consistent supply calibrated to quality specifications for retail and foodservice. Wild captured salmon, primarily Pacific species harvested in Alaska and Russia, deliver seasonal volume with strong sustainability credentials, particularly under MSC certification.

The salmon market outlook through 2034 is shaped by three structural forces: the biological ceiling on traditional open-net farming (constrained by sea lice, disease, and jellyfish incursion); the capital migration toward land-based RAS and offshore hybrid farming systems offering biological insulation; and the expanding geographic demand base as sushi culture, health-conscious diets, and rising middle-class disposable incomes penetrate new markets in Asia, Latin America, and the Middle East.

Market Dynamics

To evaluate market opportunities, Request Sample

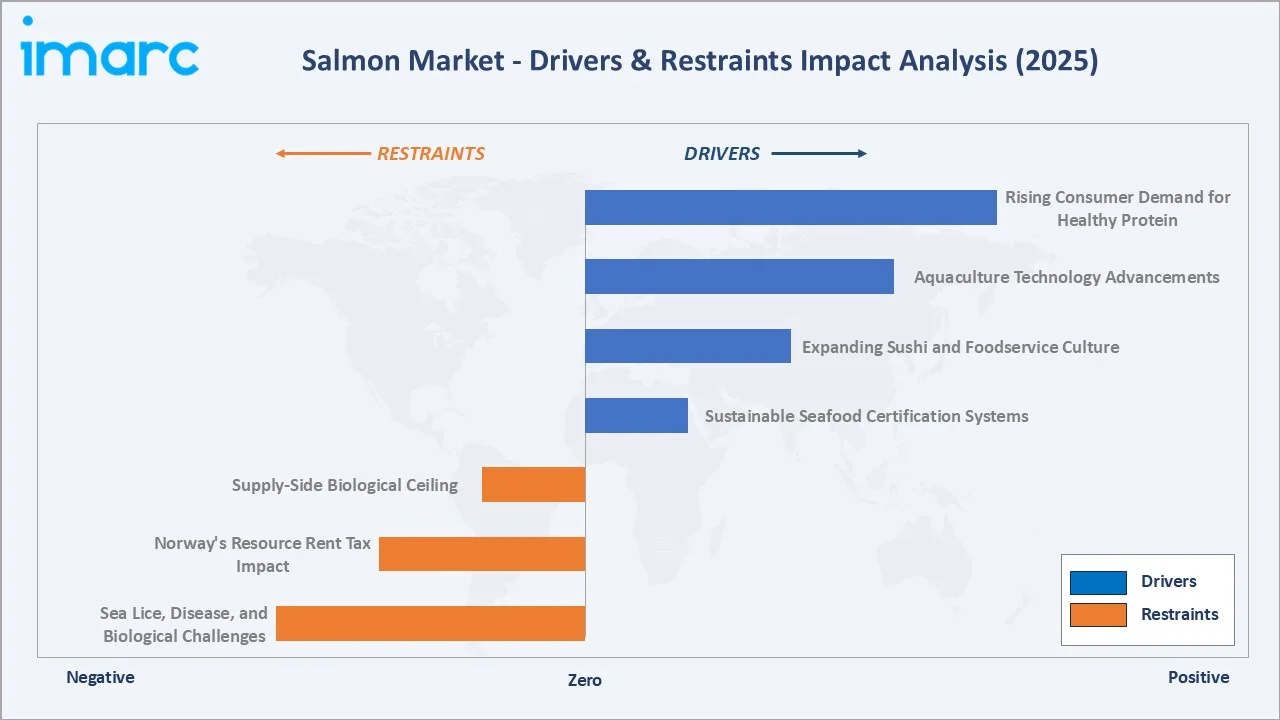

Market Drivers

- Rising Consumer Demand for Healthy Protein: Global shift toward health-conscious diets positions salmon as a premium protein source. A weekly intake of 300–450 grams of fish is recommended, including at least 200 grams of fatty fish. Omega-3 fatty acid awareness is driving per capita salmon consumption growth across North America, Europe, and Asia.

- Aquaculture Technology Advancements: Recirculating aquaculture systems (RAS) and offshore net-pen technology (SalMar's Ocean Farm) are improving biological performance and enabling salmon farming in geographically new locations. In November 2024, Multigen Akva (Norway) introduced a modular RAS system for closed coastal sea farming, eliminating viral/bacterial contamination via ultrafiltration.

- Expanding Sushi and Foodservice Culture: The global proliferation of Japanese-style sushi chains across Southeast Asia, Latin America, Brazil, and the Middle East is creating structural new demand channels for fresh farmed salmon.

- Sustainable Seafood Certification Systems: ASC (Aquaculture Stewardship Council) and MSC (Marine Stewardship Council) certifications have become market access prerequisites for premium retail and foodservice channels in the EU, U.S., and Japan.

Market Restraints

- Sea Lice, Disease, and Biological Challenges: Parasitic sea lice infestations remain the industry's primary operational challenge, costing the global salmon industry an estimated USD 1 billion annually in treatment and lost production.

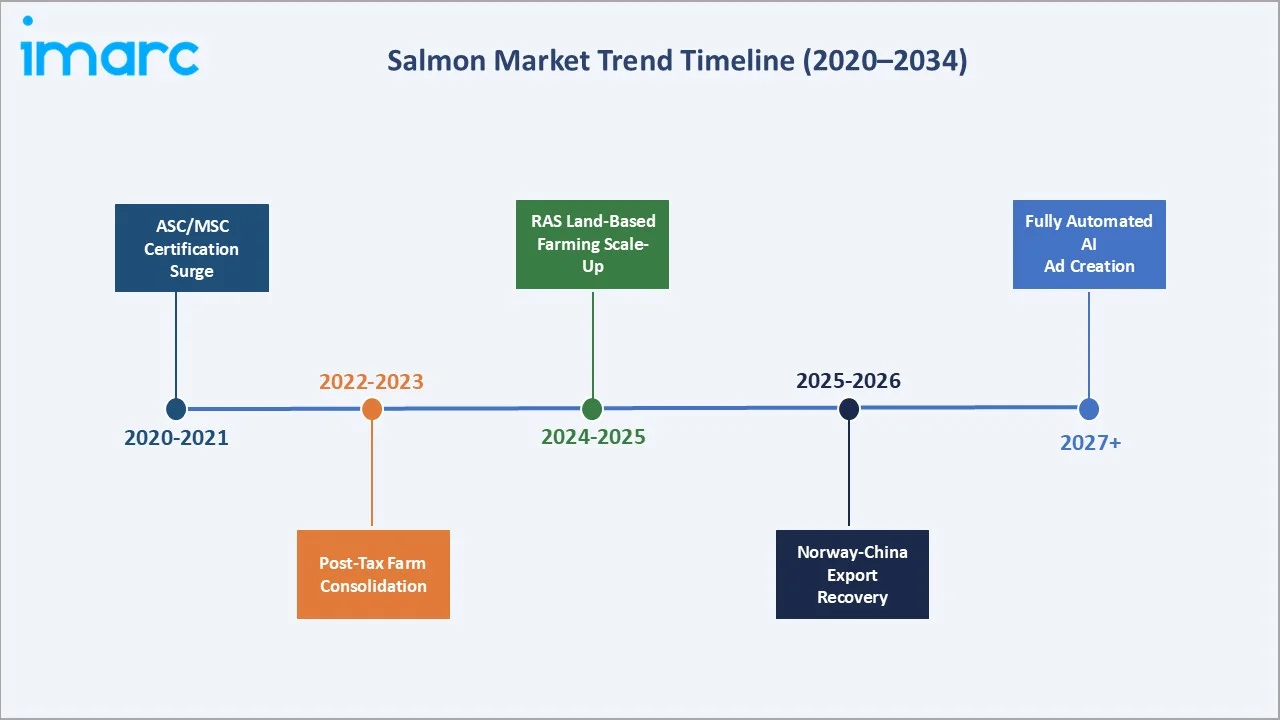

- Norway's Resource Rent Tax Impact: Norway's 25% resource rent tax on sea-phase profits (effective 2023) has fundamentally altered capital allocation in the world's largest salmon-producing nation. Major producers Mowi and SalMar have frozen offshore expansion projects, diverting capital to efficiency upgrades and tax-exempt jurisdictions.

- Supply-Side Biological Ceiling: Traditional open-net coastal farming has reached a biological plateau in key producing nations. Chilean Atlantic salmon production has stalled due to a freeze on new aquaculture concessions. The industry is increasingly reliant on technology-enabled intensification rather than geographic expansion to grow volumes, limiting supply-side response to demand growth.

Market Opportunities

- Land-Based RAS Farming Expansion: In February 2025, Pan Ocean Aquaculture (Netherlands) launches a USD 66 million fundraising to develop a salmon-producing vessel to grow and transport salmon across oceans in a fully enclosed aquaculture system, representing the frontier of production innovation.

- China and Asia Pacific Market Penetration: Norway's recovery of Chinese market share and the rapid expansion of sushi restaurant chains across Southeast Asia create a substantial demand opportunity. Captain Fresh's July 2024 acquisition of Koral (Poland), a branded salmon specialist, reflects growing capital interest in positioning along the premium salmon supply chain into emerging Asia markets.

- Value-Added Product Development: The February 2025 launch of Norway's first land-based RAS smoked salmon under the premium Lofoten brand exemplifies the premiumization opportunity available to producers combining sustainable credentials with innovative formats.

Market Challenges

- Feed Price Volatility and Fish Meal Dependency: In aquaculture, feed represents 40–50% of total production costs. Fishmeal and fish oil prices are subject to supply shocks from anchovy and capelin harvest cycles. Producers are investing in alternative feed ingredients, including insect meal, algae-derived oil, and plant-based proteins, but transitioning feed formulas without compromising growth performance and omega-3 content remains technically challenging.

- Antibiotic Use in Chilean Production: A report from the National Fisheries and Aquaculture Service (Sernapesca) reveals that the Chilean salmon farming sector's use of antibiotics rose by 22.6% in the first half of 2024 compared to the same period in 2023. As U.S. retailers enforce stricter 2026 procurement standards, Chilean producers risk losing premium market access and compressing margins.

Emerging Salmon Market Trends

1. Rise of Land-Based Recirculating Aquaculture Systems (RAS)

In November 2024, Multigen Akva introduced a modular closed-sea RAS system for coastal Norwegian waters using ultrafiltration to eliminate pathogens. In February 2025, Salmon Evolution partnered with Lofotprodukt to produce and sell Norway's first smoked land-based RAS salmon under the premium Lofoten brand.

2. Norwegian Seafood Export Surge and Strengthening Asian Market Ties

According to the Norwegian Seafood Council (NSC), Norwegian seafood exports hit a record NOK 13.9 billion in July, representing an increase of NOK 1.1 billion, or 8%, compared to the same month in 2023. This recovery is reshaping global trade flows, reflecting the growing demand for Norwegian salmon in Asia.

3. Sustainability Certification as a Market Access Prerequisite

ASC and MSC certifications have transitioned from voluntary differentiators to market access requirements across premium retail and foodservice channels in the EU, U.S., and Japan. European retailers, including Carrefour, Tesco, and Ahold Delhaize, require ASC certification for fresh salmon listings. U.S. retailers Whole Foods and Costco are tightening 2026 procurement standards that prioritize third-party verified sustainability claims.

4. Offshore and Hybrid Aquaculture Innovation

Offshore operations are exempt from Norway's resource rent tax applied to coastal farming, creating a fiscal incentive aligned with biological advantage. Similarly, Bakkafrost in the Faroe Islands operates in a jurisdiction free from Norway's tax structure, allowing reinvestment of free cash flow into biological improvement. Chile's pivot toward Coho salmon reflects producers finding biological hedges within existing footprints.

5. Value-Added Products and Premiumization

In July 2024, Captain Fresh acquired Koral (Poland) to expand premium salmon distribution into global markets and integrate downstream brand value into its supply chain. Launch of the Lofoten-branded land-based RAS smoked salmon in February 2025 demonstrates how sustainability provenance is becoming a premium marketing narrative capable of commanding retail price premiums.

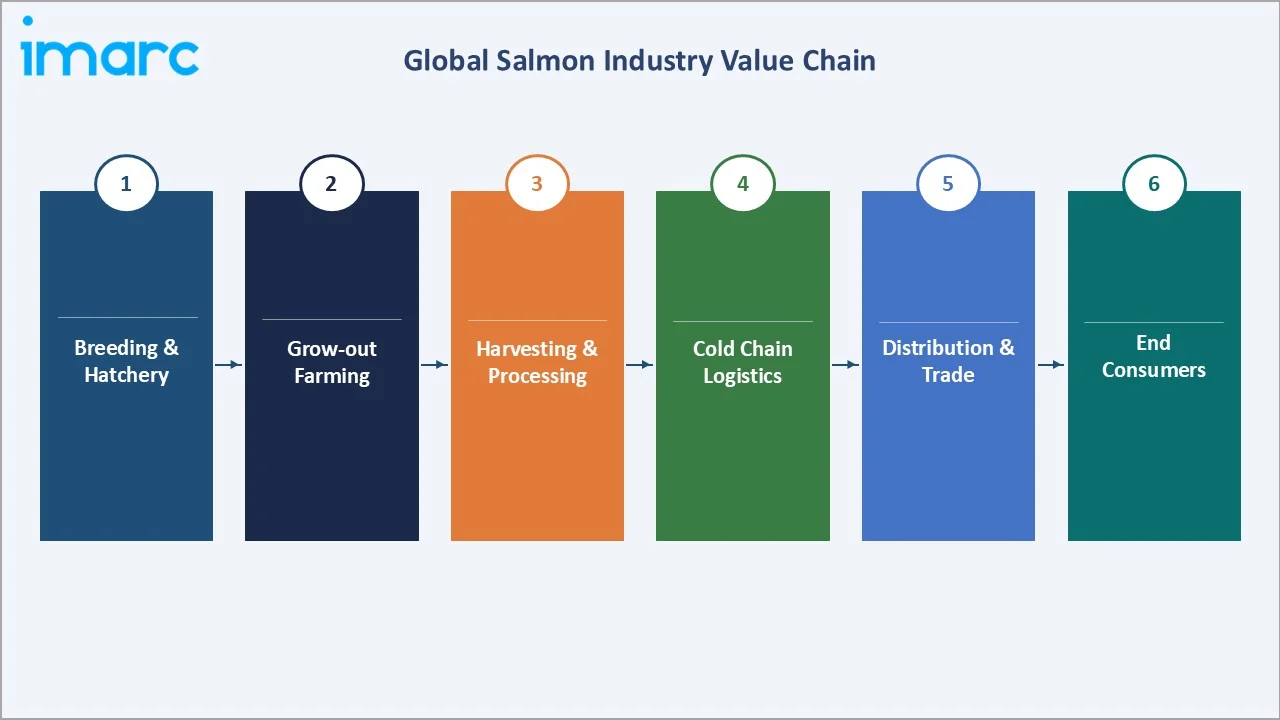

Industry Value Chain Analysis

The salmon value chain spans breeding operations through final consumer delivery, with each stage requiring specialized cold chain management to maintain product quality and regulatory compliance.

|

Stage |

Key Activities & Examples |

|

Breeding & Hatchery |

Broodstock management, ova sourcing, smolt production; Norway, Chile, Scotland |

|

Grow-out Farming |

Sea-cage net-pen farming, RAS land-based, offshore platforms; Mowi, SalMar, AquaChile, Bakkafrost |

|

Harvesting & Processing |

Slaughter, gutting, filleting, portioning, smoking, freezing; processing plants in Norway, Chile, Scotland |

|

Cold Chain Logistics |

Refrigerated air freight (fresh), reefer container shipping (frozen); Lerøy, Cermaq logistics networks |

|

Distribution & Trade |

Wholesale fish markets, international brokers, export agencies; Seafood Norway, SIF, FHL |

|

Retail Channel |

Supermarkets, hypermarkets, online grocery, specialty fishmongers; Tesco, Carrefour, Walmart |

|

Foodservice Channel |

Sushi restaurants, hotels, airlines, QSR; HoReCa operators across the EU, U.S., Japan, China |

|

End Consumers |

Health-conscious households, premium dining consumers, and sushi enthusiasts globally |

Technology Landscape in the Salmon Industry

Recirculating Aquaculture Systems (RAS)

In February 2026, AKVA Group signed a NOK 200 million contract with Årdal Aqua to design and deliver a land‑based recirculating aquaculture system (RAS) smolt facility in Årdal, Rogaland, Norway. The new facility is planned to produce around 6 million smolt per year at about 100 g each, with engineering work starting in the first half of 2026.

Offshore Net-Pen Technology

SalMar's Ocean Farm semi-submersible offshore platform represents the industry's most advanced open-sea aquaculture innovation. Offshore operations benefit from tax exemption under Norway's resource rent tax framework, improving economic returns. Multiple global operators are evaluating offshore development as a scalable complement to traditional coastal farming.

Digital Health Monitoring and AI Feeding Systems

The project by IVL Swedish Environmental Research Institute is developing digital monitoring tools to assess fish health in land‑based fish farms using sensors and data analytics. It aims to improve early disease detection and welfare management to support sustainable aquaculture operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Farmed |

75.51% |

2025 |

|

Species |

Atlantic |

63.7% |

2025 |

|

End Product Type |

Frozen |

58.3% |

2025 |

|

Distribution Channel |

Foodservice |

66.6% |

2025 |

| Producing Region |

|

|

2025 |

|

Consuming Region |

European Union |

46.03% |

2025 |

By Type

To access detailed market analysis, Request Sample

Farmed salmon dominates global production with a 75.51% share, driven by year-round consistent supply from Norway, Chile, Scotland, Canada, and the Faroe Islands. Atlantic salmon is the dominant farmed species, valued for its fat content, color, and large fillet yield, which are favorable to both retail and foodservice applications. The Wild Captured segment (24.5%) encompasses Pacific salmon species, pink, sockeye, chum, coho, and Chinook, harvested primarily in Alaskan, Russian, and Japanese waters.

By Distribution Channel

Foodservice channel leads distribution channel with 66.6%, driven by global HoReCa demand from sushi restaurants, hotel breakfast programs, premium dining establishments, and airline catering. The rapid expansion of sushi restaurant chains across Brazil, Southeast Asia, and the Middle East is a structural demand driver elevating foodservice's long-term share trajectory.

Retail accounted for 33.4% share (2025), reflecting strong consumer demand for fresh, frozen, and smoked salmon across supermarkets, hypermarkets, and increasingly online grocery platforms. Fresh salmon fillets and smoked salmon are anchor premium seafood categories across EU and U.S. retail, supported by a well-developed cold chain and short shelf-life management infrastructure. The

Regional Market Insights

European Union commands 46.3% of global consumption (2025), driven by the region's deeply embedded seafood culture, premium retail salmon offerings, and the largest HoReCa sushi and fine dining sector outside Asia. Norway's geographical proximity enables next-day fresh delivery to EU markets, maintaining the freshness quality standards that underpin premium pricing.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Context |

Supply Source |

|

European Union |

46.3% |

High per-capita seafood consumption; premium retail demand; HoReCa sushi/fine dining; strong cold chain |

EU Farm to Fork Strategy; ASC/MSC mandatory; EU aquaculture sustainability guidelines |

Norway (primary), Scotland, the Faroe Islands, Chile |

|

U.S. |

18.4% |

Health-conscious protein demand; sushi restaurant expansion; wild Alaska salmon culture |

FDA seafood safety; MSC labeling standards |

Alaska wild (sockeye, pink); Norway/Chile farmed |

|

Japan |

12.6% |

Salmon is #1 sushi topping; strong fresh/frozen demand; traditional seafood culture |

Ministry of Fisheries sustainability guidelines; strict import quality standards |

Norway, Chile; domestic hatchery trout |

|

China |

10.3% |

Rapidly growing sushi market; Norway-China trade recovery (121% export surge, Jul 2025); rising middle class |

GACC import registration; cold chain infrastructure development |

Norway (71% market share, 2025); Chile; Russia |

|

Russia |

6.8% |

Domestic wild capture (Far East); traditional smoked and salted salmon culture; import substitution |

Federal fisheries regulations; export controls on wild capture; ASC emerging |

Domestic wild Pacific; Norway farmed (pre-sanctions) |

|

Brazil |

3.2% |

Sushi culture expansion into secondary cities; rising disposable incomes |

MAPA food safety standards; cold import regulations |

Chile; Norway |

|

Others |

2.4% |

Middle East hotel/restaurant demand; Southeast Asia sushi growth |

Halal certification requirements; region-specific cold chain investment |

Norway, Chile, mixed sources |

China (10.3%) is the standout demand growth story of 2025, as data from the Norwegian Seafood Council (NSC) showed that the U.S. share of Norway's salmon export value decreased in the second half of the year, as companies shifted more volumes to Asia, including China. China notably increased its role as a key destination, with Norway gaining a larger share of total salmon imports.

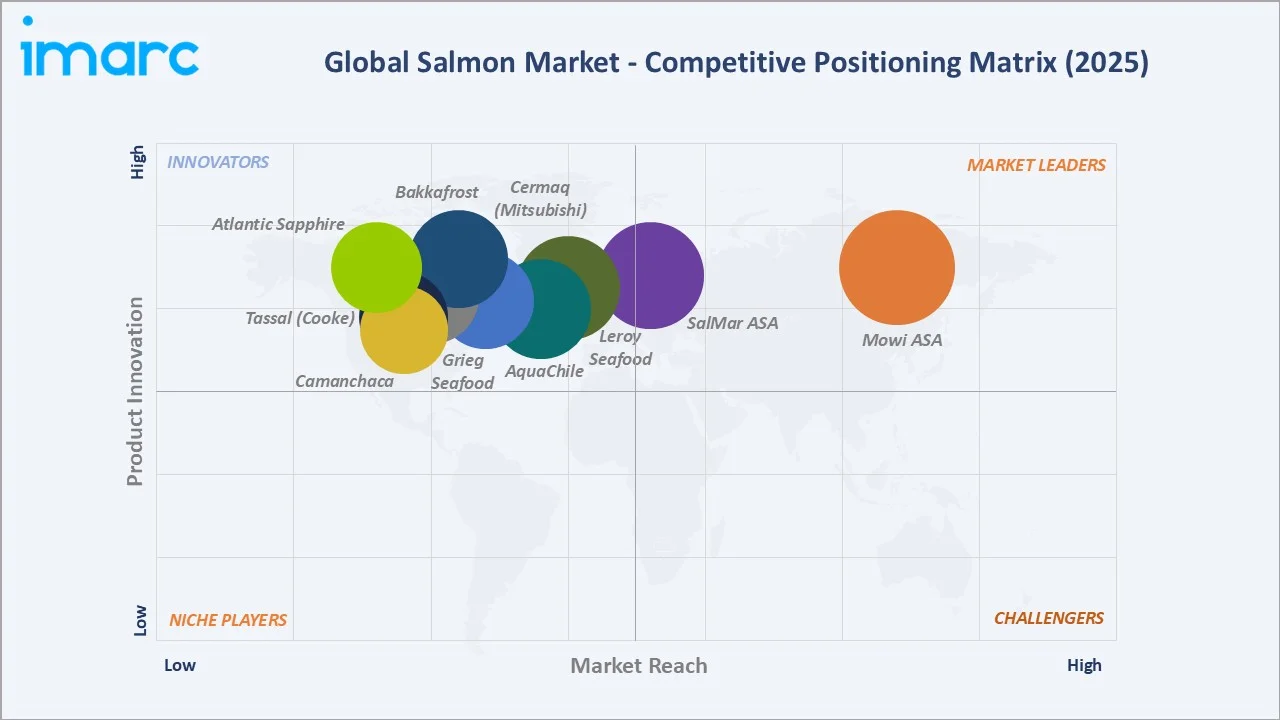

Competitive Landscape

The global salmon market is moderately consolidated at the production level, with the top five producers, Mowi ASA, SalMar ASA, Lerøy Seafood Group, AquaChile, and Cermaq Group, collectively accounting for approximately 55–60% of global farmed Atlantic salmon production in 2025.

|

Company Name |

Key Product |

Market Position |

Core Strength |

|

Mowi ASA |

Atlantic Salmon (Premium, Organic) |

Market Leader (~22%) |

Vertical integration (hatchery to retail); 600,000 MT target by 2029; Mowi Feed division |

|

SalMar ASA |

SalMar Atlantic Salmon |

Market Leader (~13%) |

Ocean Farm offshore innovation; biomass build strategy Q1 2025; Icelandic Salmon assets |

|

Lerøy Seafood Group ASA |

Lerøy Salmon |

Market Leader (~10%) |

Fully integrated: farming to distribution; Scottish Sea Farms JV (SalMar/Lerøy); global retail presence |

|

AquaChile S.A. (Agrosuper S.A.) |

Atlantic & Coho Salmon |

Strong Challenger (~9%) |

Chile's largest producer; sustainability certification focus |

|

Cermaq Group AS (Mitsubishi Corporation) |

Cermaq Atlantic Salmon |

Strong Challenger (~7%) |

Norway, Chile, Canada operations; Mitsubishi Corporation backing; strong sustainability credentials |

|

Bakkafrost P/F |

Bakkafrost Atlantic Salmon |

Regional Leader (~6%) |

Faroe Islands – tax-exempt, biologically superior; vertically integrated; reinvesting free cash flow into biology |

|

Grieg Seafood ASA |

Grieg Atlantic Salmon |

Regional Leader (~5%) |

Norway, Faroe Islands, British Columbia; BCG-certified sustainability; premium focus |

|

Atlantic Sapphire |

Bluehouse Salmon (RAS) |

Innovator |

Land-based RAS salmon in Miami; restructuring after 2024 valuation reset; Hybrid flow-through pivot |

|

Camanchaca S.A. |

Camanchaca Atlantic & Coho |

Emerging (~4%) |

Chilean producer; growing Coho sales to Japan; value-added processing capabilities |

|

Tassal Group (Cooke Aquaculture Inc.) |

Tassal Atlantic Salmon |

Regional Specialist |

Australia's largest salmon producer; ASC-certified; Cooke Aquaculture integration (2022) |

Mowi ASA commands the largest individual share at ~22%, with ambitions to reach 600,000 metric tons annual harvest by 2029 through post-smolt capacity expansion and proprietary feed division (Mowi Feed) integration. Competitive dynamics are being reshaped by Norway's Resource Rent Tax, which is driving capital away from traditional Norwegian coastal expansion toward Iceland, the Faroe Islands, offshore platforms, and RAS technology.

Key Company Profiles

Mowi ASA

Headquartered in Bergen, Norway, Mowi ASA is the world's largest producer of Atlantic salmon with operations in 25+ countries across Norway, Chile, Canada, Ireland, Scotland, and the Faroe Islands. Mowi produced approximately 108,000 metric tons (gutted weight) in Q1 2025, representing an 11,500 MT increase over Q1 2024, as the company inches toward its 600,000 MT annual harvest target for 2029.

- Product Portfolio: Fresh and frozen Atlantic salmon fillets, portions, and whole fish; smoked salmon; value-added products; fish feed (Mowi Feed division).

- Recent Developments: Q1 2025 – Record quarterly harvest of 108,000 MT GWT, 11,500 MT above prior year; expanding post-smolt capacity to reduce sea-phase biological risk by 30%; acquisition of Arctic Fish (Iceland, 10 ASC-approved sites, 27,100 MT MAB) completed in 2022.

- Strategic Focus: Post-smolt rearing expansion; Mowi Feed vertical integration for feed cost control; sustainability reporting under ASC and Marine Stewardship Council frameworks; target 600,000 MT annual production by 2029.

SalMar ASA

SalMar ASA, headquartered in Frøya, Norway, is a leading Norwegian salmon farmer known for its innovative Ocean Farm offshore technology and strong commitment to sustainable aquaculture. SalMar harvested 42,700 GWT in Q1 2025, with volumes intentionally below the prior year as part of a biomass-building strategy targeting higher harvest volumes in H2 2025.

- Product Portfolio: Atlantic salmon (fresh, frozen, smoked); SalMar Aker Ocean Farm offshore platform salmon; Scottish Sea Farms (SalMar/Lerøy JV) Atlantic salmon.

- Recent Developments: Q1 2025 – Intentional 10,200 GWT harvest reduction to build biomass for Q3-Q4 delivery; continuing investment in Ocean Farm 2 offshore platform development; Icelandic Salmon assets contributing 1,100 MT in Q1 2025.

- Strategic Focus: Offshore aquaculture at scale via SalMar Aker Ocean, biomass build for volume step-change in 2025 H2; sustainability-led brand premium in EU and Asian markets.

Bakkafrost P/F

Bakkafrost, headquartered in Glyvrar, Faroe Islands, is the premier salmon producer in the Faroe Islands and one of the most financially robust operators in the global industry. Operating outside Norway's Resource Rent Tax jurisdiction, Bakkafrost reinvests its free cash flow entirely into biological improvement and capacity expansion.

- Product Portfolio: Faroese Atlantic salmon (fresh, frozen, smoked, value-added); fishmeal and fish oil from processing by-products; salmon feed.

- Recent Developments: Ongoing biological improvement investments targeting superior feed conversion ratios and reduced lice treatments; growing premium market presence in Japan, China, and the U.S. East Coast; fully vertically integrated from feed to retail.

- Strategic Focus: Tax-advantaged Faroese jurisdiction reinvestment; premium market positioning; vertical integration from feed production to consumer retail; sustainability leadership in ASC and GlobalG.A.P. certification.

AquaChile S.A. (Agrosuper S.A.)

AquaChile, a subsidiary of Agrosuper S.A. and Chile's largest salmon producer, operates across Atlantic and Coho salmon production segments in southern Chile. Facing a freeze on new concessions for Atlantic salmon in southern regions, AquaChile has strategically pivoted toward Coho salmon production, targeting Japanese and Brazilian demand channels.

- Product Portfolio: Atlantic salmon fillets and whole fish; Coho (Pacific) salmon; value-added smoked and portioned products.

- Recent Developments: Significant biomass shift toward Coho salmon; Coho’s immunity to sea lice reducing treatment costs; expanded export volumes to Japan and Brazil; sustainability certification expansion across farming sites.

- Strategic Focus: Coho salmon as a growth strategy within Chilean concession freeze constraints; geographic diversification of export markets toward Asia-Pacific and Latin America; reducing antibiotic dependency to protect premium market access.

Market Concentration Analysis

The global salmon market exhibits moderate production-side concentration, with the top five farmed salmon producers collectively accounting for ~55–60% of global farmed Atlantic salmon output. Mowi ASA alone commands approximately 22% of global farmed production, with SalMar, Lerøy, AquaChile, and Cermaq forming the next tier at 7–13% each.

The Norwegian resource rent tax is accelerating consolidation pressure, as smaller operators struggle to absorb the effective ~47% marginal tax rate on coastal farming profits. Capital is migrating toward tax-exempt offshore operations and Faroese/Icelandic jurisdictions, suggesting that the next 5–8 years may see meaningful consolidation among mid-tier Norwegian operators.

Investment & Growth Opportunities

Fastest Growing Segments

China (CAGR ~4.2%), Brazil (CAGR ~3.2%), and value-added product formats represent the highest-growth investment vectors in the salmon market through 2034. Premium value-added categories (smoked, ready-to-eat, sushi-grade portions) command significantly higher revenue per ton than commodity fresh and frozen, making premiumization a value-accretive growth lever for integrated producers.

Emerging Market Expansion

Southeast Asia (Vietnam, Thailand, Indonesia) and the Middle East (UAE, Saudi Arabia) represent the next geographic frontier for premium salmon consumption growth. Entry via export partnerships with regional cold chain operators and premium retail chains is the preferred strategy, with ASC-certified Norwegian and Scottish salmon commanding entry-level premium positioning.

Technology Investment Priorities

RAS and hybrid flow-through systems, AI-powered aquaculture health monitoring, and sustainable feed ingredient development represent the three highest-return technology investment themes in the salmon value chain. Companies that solve the "RAS cost equation", achieving commercial viability through hybrid systems rather than pure full-recirculation, will capture the next wave of geographic market expansion opportunities.

- Key growth bets: Post-smolt rearing infrastructure, offshore net-pen platforms, and premium RAS-certified product development.

- ESG-aligned institutional capital is increasing exposure to sustainable aquaculture, with blue economy funds targeting ASC-certified salmon producers as core holdings.

- Captain Fresh's July 2024 acquisition of Koral (Poland) reflects growing private equity interest in downstream branded salmon distribution and supply chain integration.

Future Salmon Market Outlook (2026-2034)

The global salmon market is set for steady, sustainable volume growth from 3.8 Million Tons (2025) to 4.9 Million Tons (2034), representing incremental production of 1.1 Million Tons over the forecast decade. This growth will be primarily aquaculture-driven, as global farmed salmon production expands via technology-enabled intensification rather than linear geographic expansion of traditional open-net capacity.

Technological disruptions, offshore farming platforms, RAS hybrid systems, AI health monitoring, and sustainable feed alternatives will materially reduce biological risk and production costs, enabling the industry to grow through the constraint period imposed by sea lice, disease, and regulatory capacity ceilings. By 2028–2030, commercial-scale hybrid RAS systems are expected to demonstrate fully competitive economics with traditional open-net farming in high-cost jurisdictions.

China's continued premium market recovery, Japan's structurally stable high-value demand, and Southeast Asia's sushi culture expansion collectively represent the region most likely to close the share gap with the European Union by 2034. Salmon's positioning as a health-positive will sustain its outperformance versus other seafood proteins in health-driven retail and foodservice channels globally.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 120 industry participants in 2025, comprising salmon farm operators, seafood brokers, retail category managers, foodservice procurement directors, and sustainability certification bodies across Norway, Chile, Scotland, the EU, the United States, Japan, and China.

Secondary Research

Secondary research encompassed company annual reports (Mowi, SalMar, Bakkafrost, Lerøy), regulatory filings, trade publications (IntraFish, Undercurrent News, SeafoodSource), FAO global fisheries data, Kontali Analyse production statistics, and publicly available ASC/MSC certification databases.

Forecasting Models

Production volume estimates and forecasts were derived using bottom-up aquaculture capacity models, wild capture quota trend analysis, and top-down consumption demand modeling incorporating GDP growth, per capita protein intake trajectories, and regional consumption index data. Scenario analysis covering biological risk events, regulatory changes, and trade policy shifts was applied.

Salmon Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Farmed, Wild Captured |

| Species Covered | Atlantic, Pink, Chum/Dog, Coho, Sockeye, Others |

| End Product Types Covered | Frozen, Fresh, Canned, Others |

| Distribution Channels Covered | Foodservice, Retail |

| Regions Covered (Based on Production) |

|

| Regions Covered (Based on Consumption) | European Union, Russia, the United States, Brazil, Japan, China, Others |

| Companies Covered | Mowi ASA, SalMar ASA, Lerøy Seafood Group ASA, AquaChile S.A. (Agrosuper S.A.), Cermaq Group AS (Mitsubishi Corporation), Bakkafrost P/F, Grieg Seafood ASA, Atlantic Sapphire, Camanchaca S.A., Tassal Group (Cooke Aquaculture Inc.), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the salmon market from 2020-2034.

- The salmon market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the salmon industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Salmon Market Report

The global salmon market reached a production volume of 3.8 Million Tons in 2025 and is projected to reach 4.9 Million Tons by 2034.

The salmon market is expected to grow at a CAGR of 2.80% during 2026-2034, driven by rising consumer demand for omega-3-rich protein, expanding sushi culture globally, and continued advances in sustainable aquaculture technology.

The European Union is the dominant consuming region with approximately 46.3% of global salmon consumption in 2025, driven by high per capita seafood consumption, premium retail demand, and a deeply established HoReCa salmon market.

China is the fastest-growing consuming region at a CAGR of ~4.2% (2026-2034), driven by sushi culture expansion, Norway–China trade recovery, and a rapidly growing affluent middle class incorporating salmon into daily diets.

Key drivers include rising consumer awareness of omega-3 and health benefits, global sushi culture proliferation, advances in RAS and offshore aquaculture technology, sustainable certification driving premium pricing, and expanding retail e-commerce salmon channels.

Farmed salmon dominates with a 75.5% share (2025), led by Norway's Atlantic salmon production of global farmed output. Consistent year-round supply, favorable fillet yield, and premium quality certification underpin farmed salmon's market leadership.

Foodservice leads with a 66.6% share (2025), driven by expanding restaurant chains, rising dining-out trends, and strong demand from hospitality sectors.

Land-based RAS farming, Norway–China export recovery, ASC/MSC certification as market access prerequisites, offshore aquaculture innovation (SalMar Ocean Farm), and value-added premium product development are the fastest-growing trends through 2034.

Leading companies include Mowi ASA, SalMar ASA, Lerøy Seafood Group ASA, AquaChile S.A. (Agrosuper S.A.), Bakkafrost P/F, Cermaq Group AS (Mitsubishi Corporation), Grieg Seafood ASA, Atlantic Sapphire, Camanchaca S.A., Tassal Group Limited (Cooke Aquaculture Inc.), etc.

The top five farmed salmon producers, Mowi, SalMar, Lerøy, AquaChile, and Cermaq, collectively account for approximately 55–60% of global farmed Atlantic salmon production in 2025.

Key challenges include sea lice and disease outbreaks constraining Norwegian production, the Resource Rent Tax reducing Norwegian CAPEX, feed price volatility, Chilean antibiotic use risking losing premium retail access, and biological ceilings on traditional open-net coastal farming capacity expansion.

High-growth opportunities include RAS hybrid farming infrastructure, premium value-added product development, China and Southeast Asia market entry partnerships, ASC-certified sustainable salmon supply chains, and AI-powered aquaculture health monitoring and feed optimization technology.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)