Satellite Antenna Market Size, Share, Trends and Forecast by Frequency Band, Technology, Antenna Type, Platform, and Region, 2026-2034

Satellite Antenna Market Size and Share:

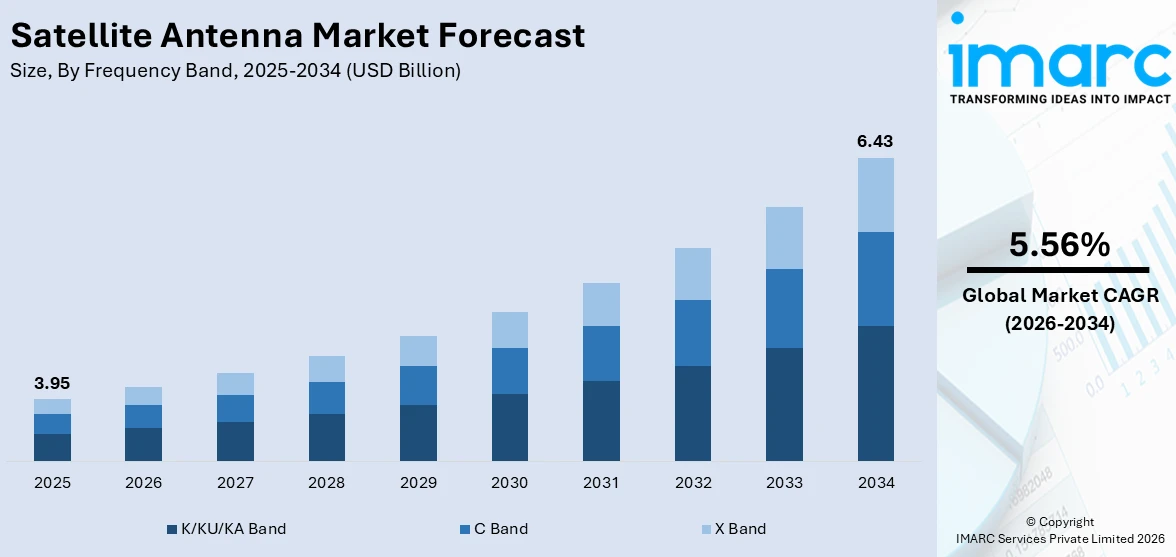

The global satellite antenna market size was valued at USD 3.95 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 6.43 Billion by 2034, exhibiting a CAGR of 5.56% from 2026-2034. North America currently dominates the market, holding a market share of 39.9% in 2025. The region benefits from significant defense expenditure on satellite communication systems, a well-established aerospace and defense industrial base, the presence of leading antenna manufacturers, and robust demand for high-throughput satellite connectivity across government and commercial sectors, all contributing to the satellite antenna market share.

The rising demand for high-speed, reliable satellite communication services across diverse industries is propelling the satellite antenna market growth. The rapid proliferation of low Earth orbit (LEO) satellite constellations is transforming connectivity paradigms, necessitating advanced antenna systems capable of tracking multiple fast-moving satellites simultaneously. Moreover, the integration of satellite networks with 5G terrestrial infrastructure is opening new frontiers for seamless global connectivity, particularly in remote and underserved areas. The growing adoption of Internet of Things (IoT) devices across maritime, aviation, and logistics sectors further amplifies the need for compact, high-performance satellite antennas. Additionally, the growing investments in space exploration missions and commercial satellite launches are generating sustained demand for technologically advanced antenna solutions that support broadband, navigation, and Earth observation applications worldwide.

The United States is emerging as a crucial region in the satellite antenna market owing to many factors. The country maintains substantial defense budgets directed toward space-based communication systems, creating steady procurement of multi-band, jam-resistant satellite antennas for military applications. For instance, in 2026, Congress released the fiscal 2026 defense spending bill funding the U.S. Space Force at USD 26 Billion, with total planned resources nearing USD 40 Billion, including previous mandatory spending. Besides this, the rapid expansion of commercial LEO broadband constellations and the growing adoption of phased array antennas for in-flight connectivity are further driving the market demand. Furthermore, robust private-sector innovation, coupled with federal initiatives supporting commercial satellite integration, is accelerating the deployment of next-generation antenna systems across both government and civilian sectors.

To get more information on this market Request Sample

Satellite Antenna Market Trends:

Expansion of Low Earth Orbit Satellite Constellations

The rapid deployment of LEO satellite constellations is impelling the satellite antenna market growth, as these constellations require extensive ground infrastructure and user terminals equipped with advanced antenna technologies. Unlike traditional geostationary systems, LEO networks involve satellites moving at high speeds, creating a need for electronically steered antennas that can maintain seamless connectivity. This shift is encouraging investment in phased array antennas, tracking systems, and compact antenna designs suitable for mobility applications. The increasing number of constellation projects is generating sustained demand for antennas across user broadband, enterprise connectivity, and defense communications. For instance, in 2026, AST SpaceMobile, Inc. successfully completed the unfolding of its BlueBird 6 satellite, deploying the largest commercial communications array antenna ever in low Earth orbit. The 2,400-square-foot phased array is designed to deliver peak speeds of up to 120 Mbps directly to standard smartphones. The milestone supports the company’s plan to launch 45–60 satellites by the end of 2026 to expand its space-based 4G/5G broadband network.

Rise of Advanced Earth Observation Missions Requiring High-Performance Antennas

The growing investment in advanced Earth observation satellites that rely on sophisticated antenna systems to achieve precise, repeatable measurements is offering a favorable satellite antenna market outlook. These missions demand large, deployable antennas capable of supporting multi-frequency radar instruments, long operational lifetimes, and high data accuracy. In 2025, NISAR was reported ready for launch as a joint Earth observation mission between NASA and the Indian Space Research Organisation (ISRO). The satellite was supposed to orbit at 747 km and operate dual L-band and S-band synthetic aperture radar instruments using a 12-metre mesh antenna to scan Earth’s land and ice surfaces every 12 days. During its three-year mission, NISAR aimed to measure millimeter-scale surface changes to support monitoring of glaciers, earthquakes, soil moisture, and ecosystems. Missions of this nature place strict requirements on antenna precision, structural stability, and deployment reliability in space environments.

Growing Need for Connectivity in Remote and Underserved Regions

Many areas lack adequate terrestrial networks due to geographic, economic, or logistical barriers, making satellite communication the most viable option for broadband access. Satellite antennas enable connectivity for rural communities, emergency response operations, resource extraction industries, and remote research facilities. Governments and service providers are prioritizing satellite-based solutions to bridge digital divides and ensure communication resilience during disasters or infrastructure failures. This priority is increasingly reflected in large-scale initiatives aimed at extending high-speed coverage beyond traditional network boundaries. The Indian Space Research Organisation (ISRO) rescheduled the launch of the BlueBird-6 satellite to December 21, 2025, as part of an Indo-US collaboration with AST SpaceMobile. The 6.5-ton satellite, equipped with a massive 2,400-square-foot phased array antenna, aimed to deliver direct-to-device global broadband from low Earth orbit. It launched aboard ISRO’s LVM3 rocket from Sriharikota to expand high-speed connectivity in underserved regions worldwide.

Satellite Antenna Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global satellite antenna market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on frequency band, technology, antenna type, and platform.

Analysis by Frequency Band:

- C Band

- K/KU/KA Band

- X Band

K/KU/KA band holds 45% of the market share, driven by their ability to support high-capacity data transmission and broadband communication services. These bands offer higher frequencies, enabling faster data rates, reduced latency, and better spectral efficiency, which are critical for modern applications like satellite internet, in-flight connectivity, and direct-to-home broadcasting. For instance, in 2025, Qorvo launched its new Ku-band beamformer ICs, AWMF-0240 (Rx) and AWMF-0241 (Tx), for phased-array SATCOM terminals, improving transmit and receive efficiency by 25% and 14%, respectively. Additionally, the growing demand for mobility and flexible communication services across air, land, and maritime platforms has amplified the adoption of these bands. Regulatory approvals and frequency allocations in major markets further reinforce their preference. Ka-band, in particular, is gaining momentum due to its suitability for high-throughput satellites (HTS), supporting applications like 5G backhaul and IoT networks. Combined, the technological advantages and increasing commercial adoption are contributing to the dominance of K/Ku/Ka band in the market.

Analysis by Technology:

Access the comprehensive market breakdown Request Sample

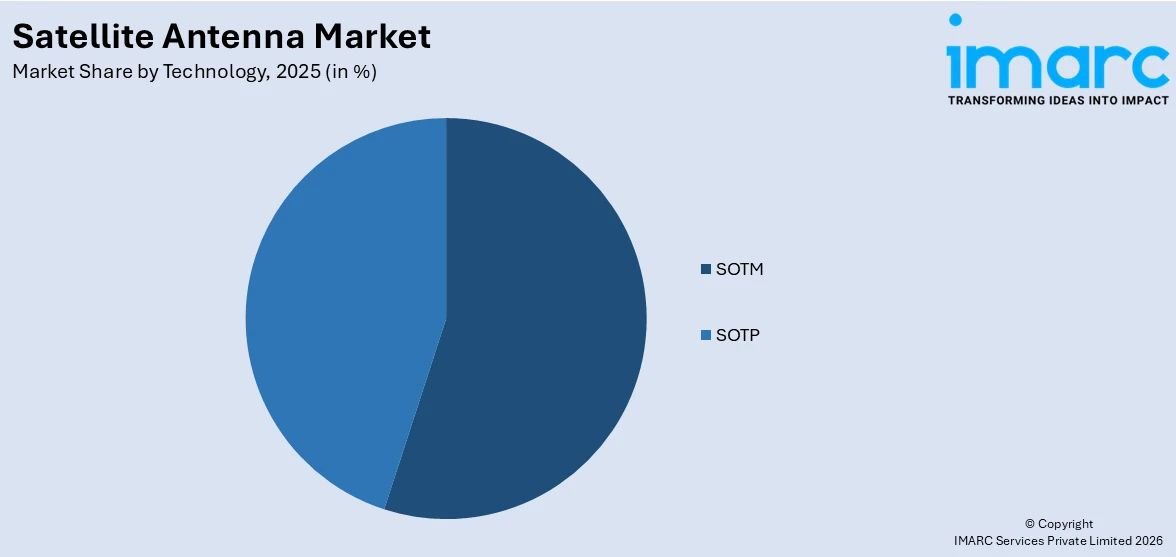

- SOTM

- SOTP

SOTM leads the market with a share of 52%. Satcom-on-the-move (SOTM) technology enables continuous satellite communication from mobile platforms, including ground vehicles, aircraft, and maritime vessels, without requiring stationary positioning. This capability is critical for military operations, emergency response, and commercial transportation where uninterrupted connectivity during movement is essential. SOTM systems incorporate advanced stabilization mechanisms, automatic beam tracking, and increasingly, electronically steered antenna arrays that maintain reliable links even under dynamic motion conditions. For instance, in 2025, L3Harris completed the Critical Design Review for the U.S. Army’s Large Wideband Satellite Communications Terminal (LWST). The LWST enhanced tactical SATCOM for C4ISR and battle management, featuring optimized RF chains, reduced size/weight/power, and virtualization-ready control. The growing demand from defense sectors for assured battlefield connectivity, combined with expanding commercial requirements in aviation and maritime industries, continues to drive SOTM adoption.

Analysis by Antenna Type:

- Flat Panel Antenna

- Parabolic Reflector Antenna

- Horn Antenna

Flat panel antenna dominates the market, with a share of 40%, due to its compact size, low profile, and enhanced performance in modern communication networks. Flat panel designs employ phased-array technology, enabling electronic beam steering without mechanical movement, which significantly reduces weight and maintenance requirements. This makes it highly suitable for applications where space and aerodynamics are critical, such as airborne, maritime, and vehicular platforms. Moreover, flat panel antenna supports multi-band and multi-beam operations, allowing seamless connectivity with high-throughput satellites and next-generation broadband services. The growing deployment of satellite-based internet, especially in regions with limited terrestrial infrastructure, is resulting in a widespread adoption of this antenna. Additionally, continuous advancements in manufacturing and material technology are reducing costs, further boosting market penetration. The satellite antenna market forecast indicates sustained growth as flat panel solutions remain central to future connectivity demands because of its high reliability, scalability, and adaptability.

Analysis by Platform:

- Land Fixed

- Land Mobile

- Airborne

- Maritime

- Space

Airborne represents the leading segment, with a market share of 26%. Airborne satellite antennas are specifically designed to provide in-flight connectivity for commercial aviation, business jets, military aircraft, and unmanned aerial vehicles (UAVs). The demand for high-speed internet access during flights, driven by passenger expectations and operational requirements, is making airborne satellite terminals one of the fastest-growing application areas. These antenna systems must withstand extreme environmental conditions, maintain reliable satellite links during high-speed travel, and comply with stringent aviation certification standards. For instance, in 2025, Viasat launched its next-generation in-flight connectivity solution, Viasat Amara, offering scalable, airline-specific connectivity powered by innovations in multi-orbit satellite networks and digital services. The company also announced the Viasat Aera electronically steered antenna, enabling simultaneous connections across GEO, HEO, and LEO satellites. Amara aimed to deliver high-capacity, customizable passenger experiences, with Aera terminals expected for commercial service in 2028.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America holds 39.9% of the market share, supported by substantial defense spending on space-based communication systems, a well-established aerospace manufacturing base, and the presence of major satellite constellation operators that continually advance antenna and terminal technologies. The region benefits from strong collaboration between government agencies, private space companies, and specialized component suppliers, enabling rapid development of high-performance antenna systems across military and commercial applications. Its expanding commercial satellite ecosystem, including broadband LEO constellation providers, in-flight connectivity services, and enterprise communication networks, sustains steady demand for multi-band, electronically steered, and phased-array antennas. A notable example occurred in 2025, when AST SpaceMobile’s stock (ASTS) surged near $68 following the completion of its next-generation BlueBird-6 satellite, equipped with a large phased-array antenna designed to connect directly with standard smartphones. Such advancements reflect the region’s technological leadership and reinforce North America’s dominant position in the global Satellite Antenna market.

Key Regional Takeaways:

United States Satellite Antenna Market Analysis

The satellite antenna market in the United States is being driven by significant and expanding federal investment in space-based defense infrastructure, including secure military satellite communications, missile detection networks, and positioning, navigation, and timing systems. Alongside defense demand, the commercial sector is experiencing rapid growth through the expansion of LEO broadband constellations, which require large-scale deployment of user terminal antennas across households, enterprises, and remote communities. In-flight connectivity operators are also upgrading aircraft fleets with advanced antenna systems to support higher bandwidth and uninterrupted service. The United States benefits from a strong venture capital environment and technology innovation hubs that accelerate the development of scalable, cost-efficient, and mass-producible antenna designs for diverse applications. A key example emerged in 2026, when the U.S. Senate Commerce Committee advanced legislation to speed satellite approvals in order to expand national broadband access. The bill proposed streamlining FCC licensing, preventing harmful interference, and increasing scrutiny of untested designs, following SpaceX’s application to launch up to one million satellites to support AI-powered data centers and broadband expansion.

Europe Satellite Antenna Market Analysis

The Europe satellite antenna market is supported by sustained institutional investment in sovereign satellite communication systems and a strong policy focus on technological independence and secure connectivity. Regional space agencies and national governments are prioritizing the development of indigenous satellite infrastructure to reduce reliance on external providers, which is driving the demand for advanced antenna technologies across communication and Earth observation platforms. Public funding programs and collaborative research initiatives are encouraging innovation in lightweight, deployable, and high-frequency antenna designs suited for next-generation missions. A notable development in 2026 highlights this direction, as the UK-based Oxford Space Systems prepared to launch the CarbSAR satellite featuring a mesh radar antenna knitted from tungsten wire coated in gold using a modified industrial knitting machine. The phased antenna is designed to deliver high-resolution Earth imagery and was developed in partnership with Surrey Satellite Technology Limited for a cost-efficient observation mission. These developments align closely with emerging satellite antenna market trends emphasizing advanced materials, compact deployable structures, and greater regional technological self-reliance.

Asia-Pacific Satellite Antenna Market Analysis

The Asia-Pacific satellite antenna market is experiencing growth because of large-scale government investments in space programs, expanding commercial satellite deployments, and rising demand for broadband connectivity across vast and geographically diverse territories. Major nations in the region are actively developing indigenous satellite launch capabilities and communication satellite constellations that require corresponding ground-segment antenna infrastructure. For instance, India’s space budget has nearly tripled over the past decade from INR 5,615 Crores in 2013-14 to INR 13,416 Crores in 2025-26, reflecting the government’s strong commitment to advancing space capabilities. The maritime sector across Asia-Pacific is also generating significant antenna requirements as shipping routes expand and connectivity expectations for commercial vessels increase.

Latin America Satellite Antenna Market Analysis

The Latin American Satellite Antenna market is supported by rising demand for satellite broadband connectivity in remote and underserved regions, along with expanding needs in maritime communication and resource monitoring. Governments and service providers are increasingly adopting advanced antenna systems to strengthen coverage and ensure reliable links across challenging terrains. A notable example in 2025 was the preparation by ESA and Hisdesat to launch the SpainSat Next Generation I satellite via SpaceX Falcon 9, featuring advanced X-band antennas and real-time beam steering to deliver secure, resilient communications across South America and beyond.

Middle East and Africa Satellite Antenna Market Analysis

The Middle East and Africa satellite antenna market is growing due to rising investment in Earth observation, security monitoring, and advanced space-based communication infrastructure. Governments across the region are strengthening geospatial and remote sensing capabilities to support disaster management, maritime surveillance, and national development initiatives. In 2024, Bayanat and Yahsat, in partnership with ICEYE, launched their first LEO synthetic aperture radar satellite to deliver high-resolution, all-weather imaging. The mission marked the beginning of a broader SAR constellation under the UAE’s Earth Observation Space Programme, reinforcing regional demand for advanced satellite antenna systems.

Competitive Landscape:

The satellite antenna market features intense competition among established aerospace and defense companies and innovative technology startups, with key players investing heavily in research and development (R&D) to advance electronically steered antenna technologies, phased array systems, and metamaterial-based solutions. Companies are pursuing strategic partnerships, technology licensing agreements, and vertical integration to strengthen their competitive positions across military and commercial segments. The market is witnessing significant consolidation as ground-segment specialists merge to broaden product portfolios, while defense contractors secure large government procurement contracts for next-generation multi-band antenna systems. Innovation in software-defined beam steering, lightweight composite materials, and integrated chipsets is enabling manufacturers to deliver higher-performance antenna solutions at reduced costs, intensifying competition for market share across LEO, MEO, and GEO service platforms.

The report provides a comprehensive analysis of the competitive landscape in the satellite antenna market with detailed profiles of all major companies, including:

- C-COM Satellite Systems Inc

- Cobham Satcom

- General Dynamics Mission Systems, Inc.

- Gilat Satellite Networks

- Honeywell International Inc.

- Hughes Network Systems, LLC

- Kymeta Corporation

- L3Harris Technologies, Inc.

- Norsat International Inc.

- Viasat Inc.

Latest News and Developments:

- In February 2026, Viasat Inc. announced that Astralintu has purchased two advanced S/X/Ka-band ground antennas to build its Equatorial Ground Station Network. The antennas, to be installed in Ecuador at 0° latitude, will expand Viasat’s Real-Time Earth (RTE) network and improve coverage across South America and the Caribbean. The systems are expected to be operational before the end of 2026, enhancing real-time satellite data access for government and commercial users.

- In February 2026, Japan Display Inc. (JDI) signed a strategic master supply agreement with Kymeta to develop glass substrates for next-generation multi-band Ku/Ka metasurface antennas. The collaboration aims to advance mobile satellite communications using metamaterials technology. This partnership supports the development of high-performance, next-gen satellite connectivity solutions.

Satellite Antenna Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Frequency Bands Covered | C Band, K/KU/KA Band, X Band |

| Technologies Covered | SOTM, SOTP |

| Antenna Types Covered | Flat Panel Antenna, Parabolic Reflector Antenna, Horn Antenna |

| Platforms Covered | Land Fixed, Land Mobile, Airborne, Maritime, Space |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | C-COM Satellite Systems Inc, Cobham Satcom, General Dynamics Mission Systems, Inc., Gilat Satellite Networks, Honeywell International Inc., Hughes Network Systems, LLC, Kymeta Corporation, L3Harris Technologies, Inc., Norsat International Inc., Viasat Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the satellite antenna market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global satellite antenna market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the satellite antenna industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Satellite Antenna Market Report

The satellite antenna market was valued at USD 3.95 Billion in 2025.

The satellite antenna market is projected to exhibit a CAGR of 5.56% during 2026-2034, reaching a value of USD 6.43 Billion by 2034.

The satellite antenna market is driven by the rapid expansion of Low Earth Orbit satellite constellations, rising investment in advanced Earth observation missions requiring high-performance antenna systems, and the growing need for reliable connectivity solutions in remote and underserved regions worldwide.

North America currently dominates the satellite antenna market, accounting for a share of 39.9%. The region benefits from the largest defense budget allocation toward space capabilities, a mature aerospace industrial base, and substantial commercial satellite constellation deployments.

Some of the major players in the satellite antenna market include C-COM Satellite Systems Inc, Cobham Satcom, General Dynamics Mission Systems, Inc., Gilat Satellite Networks, Honeywell International Inc., Hughes Network Systems, LLC, Kymeta Corporation, L3Harris Technologies, Inc., Norsat International Inc., Viasat Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)