Satellite Transponder Market Size, Share, Trends and Forecast by Bandwidth, Service, Application, and Region, 2026-2034

Satellite Transponder Market Size and Share:

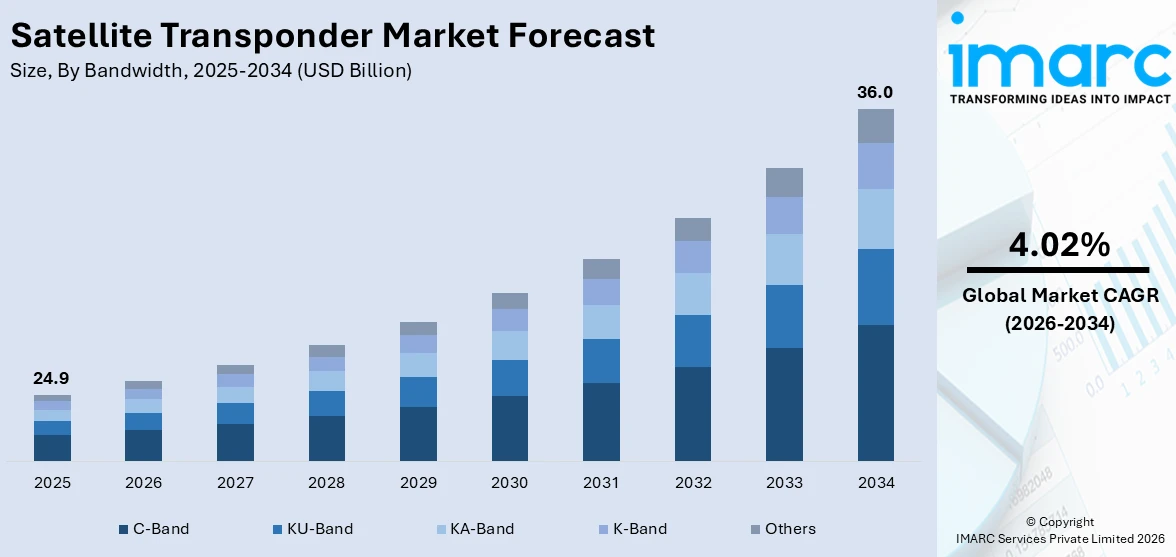

The global satellite transponder market size was valued at USD 24.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 36.0 Billion by 2034, exhibiting a CAGR of 4.02% from 2026-2034. North America currently dominates the market, holding a market share of 41.5% in 2025. The market is driven by the expanding demand for broadband at high speeds, expanding use of Direct-to-Home (DTH) services, and increased use of satellite-based communications in defense, naval, and aviation industries. Improvement in satellite technology in the form of miniaturized payloads and high-throughput satellites (HTS) increases efficiency and coverage. In addition, the increase in data traffic, growth in Internet of Things (IoT) networks, and demand for dependable global connectivity in far-flung areas also drive satellite transponder market share, drawing investments from private and government sectors.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 24.9 Billion |

| Market Forecast in 2034 | USD 36.0 Billion |

| Market Growth Rate (2026-2034) | 4.02% |

The growth driver for the satellite transponder industry is the ever-growing demand for high-speed broadband connectivity worldwide. As internet usage, streaming, and cloud computing continue to grow rapidly, the conventional terrestrial networks fail to deliver consistent cover in distant and rural locations. Satellite transponders facilitate smooth communication by sending large amounts of data over long distances, covering both consumer and business requirements. Moreover, industries such as defense, maritime, and aviation totally depend on satellite connectivity for imperative operations, thus further increasing satellite transponder market demand. The demand for reliable, high-capacity worldwide connectivity is still driving investment in leading-edge satellite transponder technologies.

To get more information on this market Request Sample

The U.S. holds a dominant position in the satellite transponder market with a market share of 86.70%, supported by its advanced space infrastructure, strong satellite industry, and substantial investments in communication technologies. In 2024, U.S. companies accounted for 65% of global launch revenue, built 83% of commercial satellites, and operated over 70% of satellites in orbit, reflecting their market leadership. The country’s emphasis on expanding broadband access, particularly in rural and underserved regions, drives demand for high-capacity transponders. Additionally, defense and government reliance on secure satellite communication, coupled with the rise of commercial ventures including LEO and high-throughput satellites, strengthens the U.S. market, making it a global hub for innovation, deployment, and adoption of satellite transponder services.

Satellite Transponder Market Trends:

Rising Demand for High-Speed Broadband and Data Connectivity

The worldwide growth of internet use, streaming, cloud computing, and working from home has directly boosted the need for broadband connectivity at high speeds. In 2024, an estimated 5.5 billion individuals, representing 68% of the world's population, were online, representing a 3.4% year-over-year increase, the fast shift to digital services. Conventional ground-based networks tend to fail to deliver consistent coverage in far-flung, rural, and underserved communities, thus an urgent need for relief through alternative means. Satellite transponders fill this gap through the transmission of high amounts of data over extended distances, providing continuous and unbroken connectivity. HTS and innovative payload technologies improve bandwidth efficiency, supporting speedier, more dependable internet services. The growth in IoT devices and digital applications in various industries again reinforces the demand, and satellite transponders become crucial for expanding global digital infrastructure and connectivity.

Expansion of Direct-to-Home (DTH) and Media Broadcasting Services

Another significant satellite transponder market trends is rising DTH television and multimedia broadcasting popularity across the globe propels high demand for satellite transponders. Consumers are looking for varied content of high-definition and ultra-high-definition quality, which commands high bandwidth and high-transmission capacity. Satellite transponders make it possible for broadcasters to transport content smoothly across various regions, including those with no terrestrial infrastructure. Emerging market growth and the growing disposable incomes have, in turn, driven DTH service adoption faster. Additionally, the shift to digital broadcasting and the advent of over-the-top (OTT) platforms maximize reliance on satellite communication infrastructure, with transponders acting as a key enabler of uninterrupted, high-quality media dissemination across the world.

Growing Adoption in Defense, Aviation, and Maritime Sectors

Satellite transponders are also essential in defense, aviation, and maritime uses, and thus satellite transponder market growth. The military depends upon satellite communication for secure, real-time data transmission, monitoring, and reconnaissance activities in far-flung and distant locations. Airlines and shipping companies utilize satellite transponders to provide uninterrupted communications, navigation, and monitoring. Global coverage, particularly in distant or disaster-stricken regions, further enhances demand. Advanced technologies like high-throughput satellites (HTS) promote signal integrity and bandwidth optimization, and satellite transponders become a requirement for strategic, commercial, and safety-critical applications in these industries.

Satellite Transponder Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global satellite transponder market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on bandwidth, service, and application.

Analysis by Bandwidth:

- C-Band

- KU-Band

- KA-Band

- K-Band

- Others

C-Band accounts for the majority of shares of 36.7% in the satellite transponder market primarily due to its reliability, wide coverage, and resistance to signal degradation from weather conditions. Unlike higher frequency bands, C-Band signals experience minimal rain fade, making them ideal for consistent, long-distance communication, particularly in tropical and high-precipitation regions. This band is extensively used for broadcasting, DTH services, and enterprise connectivity, where stable signal quality is critical. Additionally, C-Band’s proven infrastructure and global adoption make it a preferred choice for large-scale deployments, including rural broadband expansion and defense communication. Its balance of capacity, coverage, and signal stability continues to drive market preference, maintaining its dominance over higher-frequency bands such as Ku and Ka.

Analysis by Service:

- Leasing

- Maintenance and Support

- Others

According to the satellite transponder market forecast, the leasing represents the majority of shares of 77.7% owing to its cost-effectiveness, flexibility, and lower entry barriers for service providers. Leasing allows broadcasters, telecom operators, and enterprises to access high-capacity transponder bandwidth without the substantial capital expenditure of owning and maintaining satellites. This model is particularly advantageous for temporary projects, regional coverage, or scaling operations based on demand fluctuations. It also provides operators the ability to quickly adopt advanced technologies, upgrade capacity, and expand coverage without long-term commitments. The flexibility and scalability offered by leasing make it an attractive option for both emerging and established players, driving widespread adoption and contributing significantly to the overall market share of leased satellite transponder services.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Commercial Communications

- Government Communications

- Navigation

- Remote Sensing

- R&D

- Others

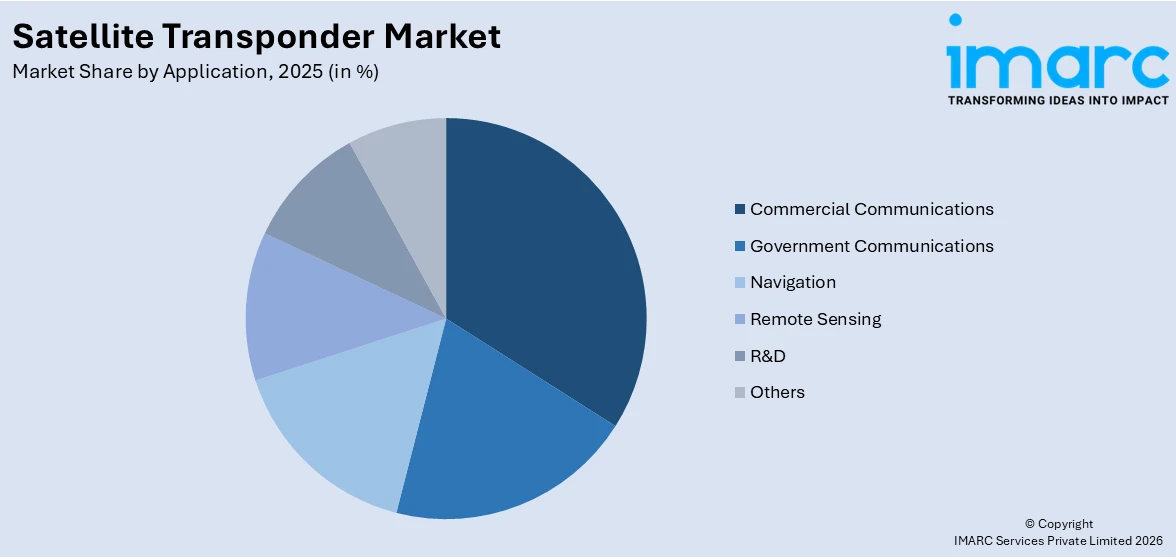

Commercial communications hold the majority of positions in the satellite transponder market because of increasing demand for dependable, high-capacity connectivity in industries and consumer markets. These consist of broadcasting, Direct-to-Home (DTH) TV, corporate data services, and broadband internet, all depending on satellite transponders for smooth transmission over large geographic regions. The growth in digital media, streaming services, and cloud-based applications also has boosted the demand for strong satellite communication infrastructure. Commercial sectors also gain with scalable solutions, i.e., leased transponders, which are cost-effective and offer flexibility. The marriage of widespread adoption, ongoing technology enhancements, and requirements for constant, global connectivity guarantees that commercial communications is the largest application segment to continue dominating the market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

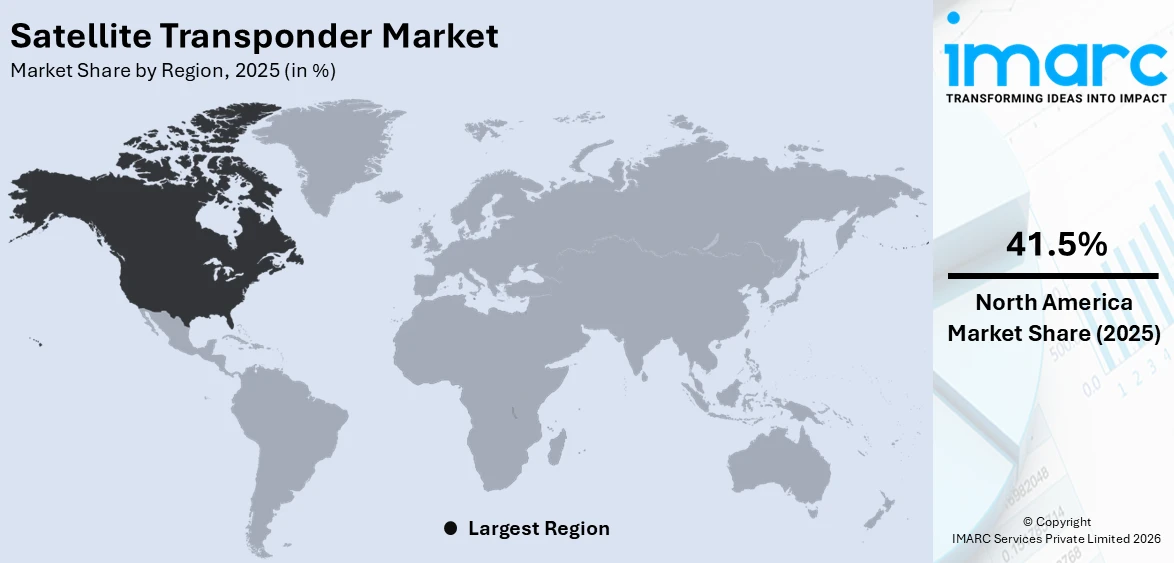

According to the satellite transponder market analysis, the North America is the top region with a market share of 41.5% due to its developed technological infrastructure, intense usage of satellite-based services, and heavy investments in space and communications technologies. Presence of major satellite operators and ongoing government and private sector efforts to increase broadband penetration, even in rural and underserved communities, propels market growth. In addition, the defense, aviation, and maritime industries in North America are dependent on satellite transponders for secure real-time communication and monitoring. The swift deployment of next-generation and high-throughput satellites, along with complementary regulatory environments, further enhances the regional market strength. All these factors put together enable North America to become a leading hub of innovation and adoption of satellite transponders.

Key Regional Takeaways:

United States Satellite Transponder Market Analysis

The United States satellite transponder market is primarily driven by the increasing demand for high-speed data transmission, particularly in remote and underserved areas where traditional infrastructure is limited or absent. The expansion of broadband connectivity, fueled by government initiatives and private sector investments, is encouraging the deployment of satellite-based communication systems that rely heavily on transponders. In a 2024 survey in the United States, 79% of respondents reported having a broadband internet subscription service. Moreover, growth in direct-to-home television services, mobile backhaul, and enterprise network connectivity is significantly boosting transponder usage. The proliferation of data-intensive applications, including streaming services, cloud computing, and real-time communications, also requires robust satellite infrastructure capable of handling large volumes of data efficiently. Additionally, advancements in satellite technology, such as the development of high-throughput satellites and reusable launch systems, are making satellite communications more cost-effective and accessible. The defense and aerospace sectors are also contributing substantially to market demand, as secure and reliable satellite communication remains essential for military operations and national security. Other than this, the increasing need for disaster response and emergency communication networks is also propelling the adoption of satellite transponders in maintaining connectivity during critical situations.

Asia Pacific Satellite Transponder Market Analysis

The Asia Pacific satellite transponder market is growing due to the rapid expansion of digital services and the rising need for reliable communication infrastructure across both urban and rural areas. Numerous countries in the region are focusing on bridging the digital divide, making satellite-based connectivity essential where terrestrial networks are limited. Rising demand for direct-to-home television, high-speed internet, and mobile backhaul services is also propelling the need for more transponder capacity. Additionally, regional growth in air travel and maritime trade is increasing the demand for satellite communication systems that ensure connectivity across vast and remote geographies. For instance, domestic air passenger traffic in India reached 161.3 Million passengers in 2024, recording a growth of 6.12%, as per the India Brand Equity Foundation (IBEF). Besides this, governments and private sectors in the region are also investing in domestic satellite programs to support national security, disaster management, and economic development. The adoption of advanced satellite technologies and growing partnerships between telecom providers and satellite operators are also contributing to market momentum.

Europe Satellite Transponder Market Analysis

The growth of the Europe satellite transponder market is largely propelled by the growing demand for reliable communication infrastructure across a range of sectors, including broadcasting, defense, aviation, maritime, and emergency services. As digital transformation accelerates, there is a greater need for high-capacity data transmission, particularly in remote and rural regions where terrestrial networks are limited. According to reports, the European Union established two primary objectives for enterprises to undergo digital transformation by 2030: 90% of SMEs are required to reach a basic level of digital intensity and 75% of businesses in the EU are required to utilize artificial intelligence (AI) or cloud computing technologies. Satellite transponders also play a crucial role in enabling seamless connectivity for television broadcasting, live event coverage, and mobile communications. The increasing adoption of high-definition and ultra-high-definition content is further driving the need for advanced transponder capacity. Additionally, Europe’s focus on space innovation, supported by regional space agencies and collaborations with private industry, is fostering the development of next-generation satellites with improved efficiency and coverage. Other than this, heightened security concerns and geopolitical developments are prompting governments to invest in secure satellite communication systems for defense and surveillance operations. Sustainability goals are also encouraging the design of more energy-efficient satellites and transponders, aligning with broader environmental initiatives across the region.

Latin America Satellite Transponder Market Analysis

The Latin America satellite transponder market is experiencing robust growth due to the region’s increasing focus on improving connectivity in geographically challenging and underserved areas. Satellite transponders are essential for delivering communication services where ground infrastructure is difficult to deploy. The growing adoption of 5G technology across urban and semi-urban centers is also boosting demand for satellite backhaul solutions to support broader network coverage. As per recent industry reports, the number of 5G network connections in Latin America reached 67 Million in Q3 2024, recording a growth rate of 19%. Additionally, rising interest in digital broadcasting, including high-definition and regional content, is also propelling broadcasters to secure additional transponder capacity. Furthermore, industries such as mining, oil, and agriculture are increasingly utilizing satellite services for real-time data and remote operations, contributing to consistent transponder demand across the region.

Middle East and Africa Satellite Transponder Market Analysis

The Middle East and Africa satellite transponder market is significantly influenced by the need for reliable communication infrastructure across vast and often remote areas where terrestrial networks are limited or unavailable. Satellite transponders play a critical role in supporting television broadcasting, internet access, and mobile connectivity in both urban and rural regions. The growing demand for digital content, including direct-to-home television and live broadcasts, is also increasing the need for transponder capacity. Additionally, the rise of smart city projects and digital transformation efforts in several countries is creating further demand for dependable satellite links. According to a report by the IMARC Group, the smart cities market in the Middle East reached USD 62,965.8 Million in 2024 and is projected to grow at a CAGR of 21.89% during 2025-2033.

Competitive Landscape:

The competitive market is dominated by high-technology innovation, strategic partnerships, and efforts to broaden service coverage. Firms are allocating more funds toward high-throughput and next-generation satellite technologies for increased capacity, efficiency, and reliability. Market participants are turning to strategies like partnerships, mergers, and alliances to improve their global reach and access emerging markets. The competition also stems from increased demand for broadband connectivity, DTH services, and defense applications, leading to ongoing innovation of flexible, high-performance transponders. Furthermore, focus on cost optimization, fast deployment, and provision of customized solutions for various industries also distinguishes players, resulting in a very dynamic and innovation-focused market.

The report provides a comprehensive analysis of the competitive landscape in the satellite transponder market with detailed profiles of all major companies, including:

- SES S.A.

- Arabsat

- Eutelsat S.A.

- Intelsat Corporation

- Embratel Star One

- Thaicom Public Company Limited

- Sky Satellite LLC

- SKY Perfect JSAT Corporation

- HISPASAT S.A.

- Singtel Group

- Telesat

Latest News and Developments:

- March 2025: The Indian Space Research Organization (ISRO) reported that its 300 Milli Newton Stationary Plasma Thruster, specifically built for integration into the Electric Propulsion Systems of satellites, successfully completed a 1000-hour life test. The Electric Propulsion System is expected to potentially replace chemical propulsion systems in future satellites, which will significantly increase transponder capabilities in communication satellites.

- March 2025: Rocket Lab successfully finished deploying a constellation of Internet-of-Things satellites for Kinéis, an international provider of IoT connectivity solutions headquartered in France. The satellites are equipped with advanced Automatic Identification System (AIS) transponders for providing IoT communications services and monitoring vessels.

- January 2025: The Indian Space Research Organization (ISRO) successfully launched its 100th satellite, the NVS-02. The satellite’s ranging payload comprises an advanced transponder to assist the navigation satellite in sending time-stamped navigational signals to the ground station's receivers, ensuring uninterrupted operation regardless of Earth's weather.

- November 2024: SpaceX officially launched ISRO’s newest communication satellite, the GSAT-N2, from Cape Canaveral, Florida, in the United States. The satellite is equipped with wideband Ka x Ka transponders and is intended to serve a broad subscriber base with small user terminals.

- February 2024: The Indian Space Research Organization (ISRO) completed the successful launch of the INSAT-3DS satellite on launch vehicle GSLV-F14. Completely financed by the Ministry of Earth Sciences (MoES), the satellite features cutting-edge payloads, including a satellite-assisted search and rescue transponder that transmits an emergency signal or alert from beacon transmitting devices with worldwide coverage and a data relay transponder that receives hydrological, oceanographic, and meteorological data from automated data collection systems.

Satellite transponder Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Bandwidths Covered | C-Band, KU-Band, KA-Band, K-Band, Others |

| Services Covered | Leasing, Maintenance and Support, Others |

| Applications Covered | Commercial Communications, Government Communications, Navigation, Remote Sensing, R&D, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | SES S.A., Arabsat, Eutelsat S.A., Intelsat Corporation, Embratel Star One, Thaicom Public Company Limited, Sky Satellite LLC, SKY Perfect JSAT Corporation, HISPASAT S.A., Singtel Group, and Telesat |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the satellite transponder market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global satellite transponder market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the satellite transponder industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Satellite Transponder Market Report

The satellite transponder market was valued at USD 24.9 Billion in 2025.

The satellite transponder market is projected to exhibit a CAGR of 4.02% during 2026-2034, reaching a value of USD 36.0 Billion by 2034.

Key factors driving the satellite transponder market include the rising demand for high-speed broadband, expanding Direct-to-Home (DTH) and multimedia broadcasting, and growing adoption in defense, aviation, and maritime sectors. Technological advancements like high-throughput satellites (HTS) and increased global connectivity needs further fuel market growth.

North America leads the satellite transponder market with a market share of 41.5% due to its advanced technological infrastructure, widespread adoption of satellite services, and substantial investments in space and communication technologies. Strong government support, robust defense and commercial sectors, and the deployment of high-throughput and next-generation satellites further reinforce the region’s market dominance.

Some of the major players in the satellite transponder market include SES S.A., Arabsat, Eutelsat S.A., Intelsat Corporation, Embratel Star One, Thaicom Public Company Limited, Sky Satellite LLC, SKY Perfect JSAT Corporation, HISPASAT S.A., Singtel Group, Telesat, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)