Saudi Arabia Ceramic Tiles Market Size, Share, Trends and Forecast by Product, Application, Construction Type, End User, and Region, 2026-2034

Saudi Arabia Ceramic Tiles Market Size, Share, Trends & Forecast (2026-2034)

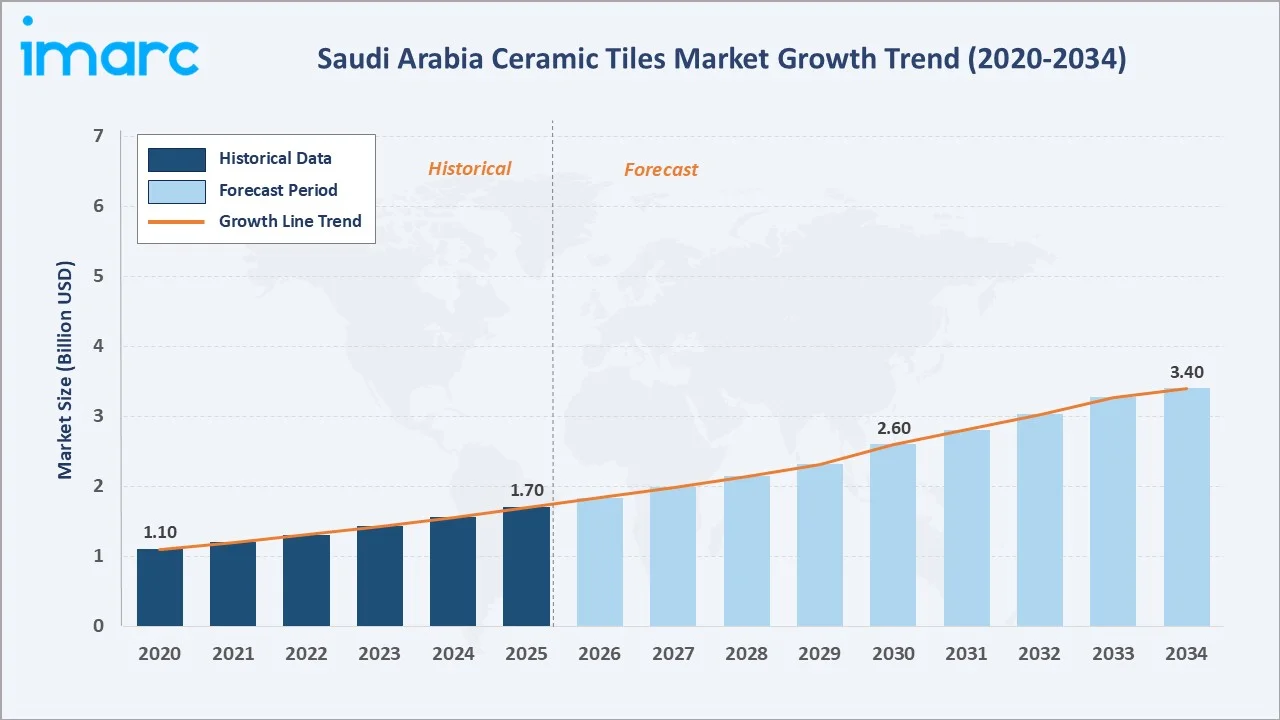

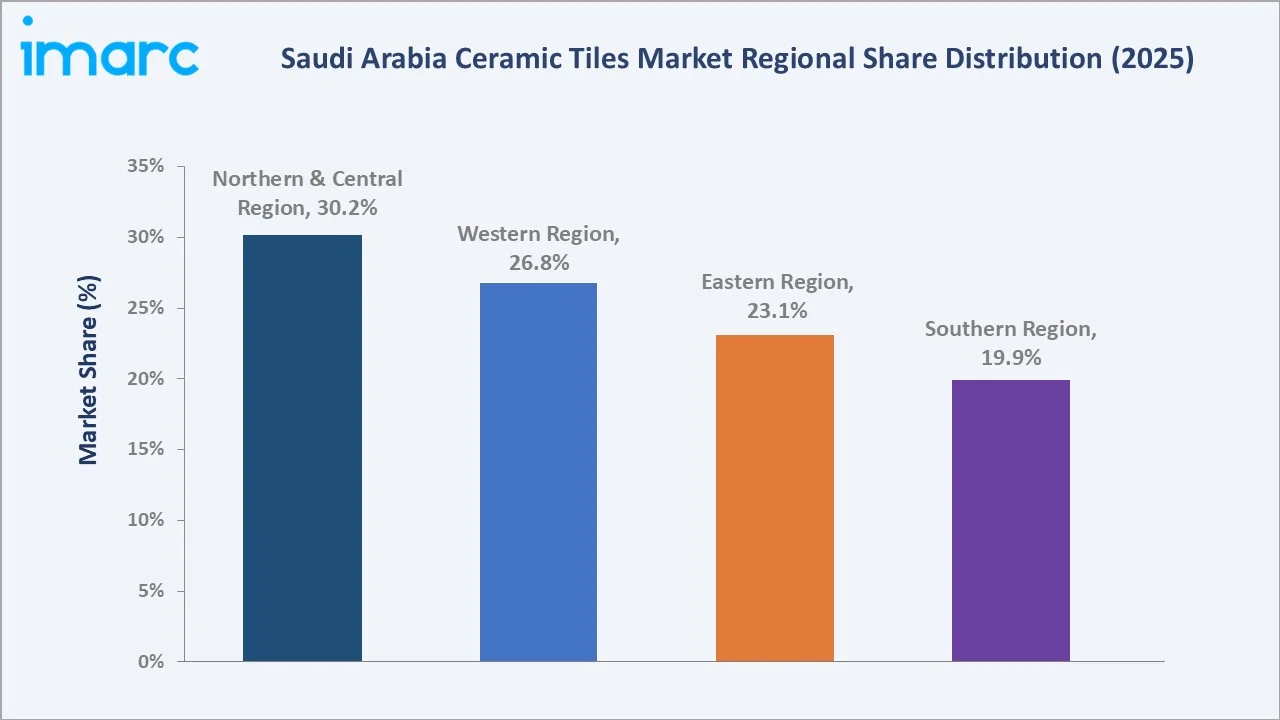

The Saudi Arabia ceramic tiles market reached USD 1.70 Billion in 2025 and is projected to reach USD 3.40 Billion by 2034, growing at a CAGR of 7.30% during 2026-2034. Vision 2030 mega projects, surging residential construction, and the expansion of hospitality and tourism infrastructure are the primary growth catalysts. The Northern and Central Region leads all sub-markets with a 30.2% share in 2025, anchored by Riyadh's construction boom and NEOM-related developments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.70 Billion |

|

Forecast Market Size (2034) |

USD 3.40 Billion |

|

CAGR (2026-2034) |

7.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Northern & Central Region (30.2% share, 2025) |

|

Fastest Growing Region |

Western Region (Jeddah & Red Sea Project) |

To get more information on this market, Request Sample

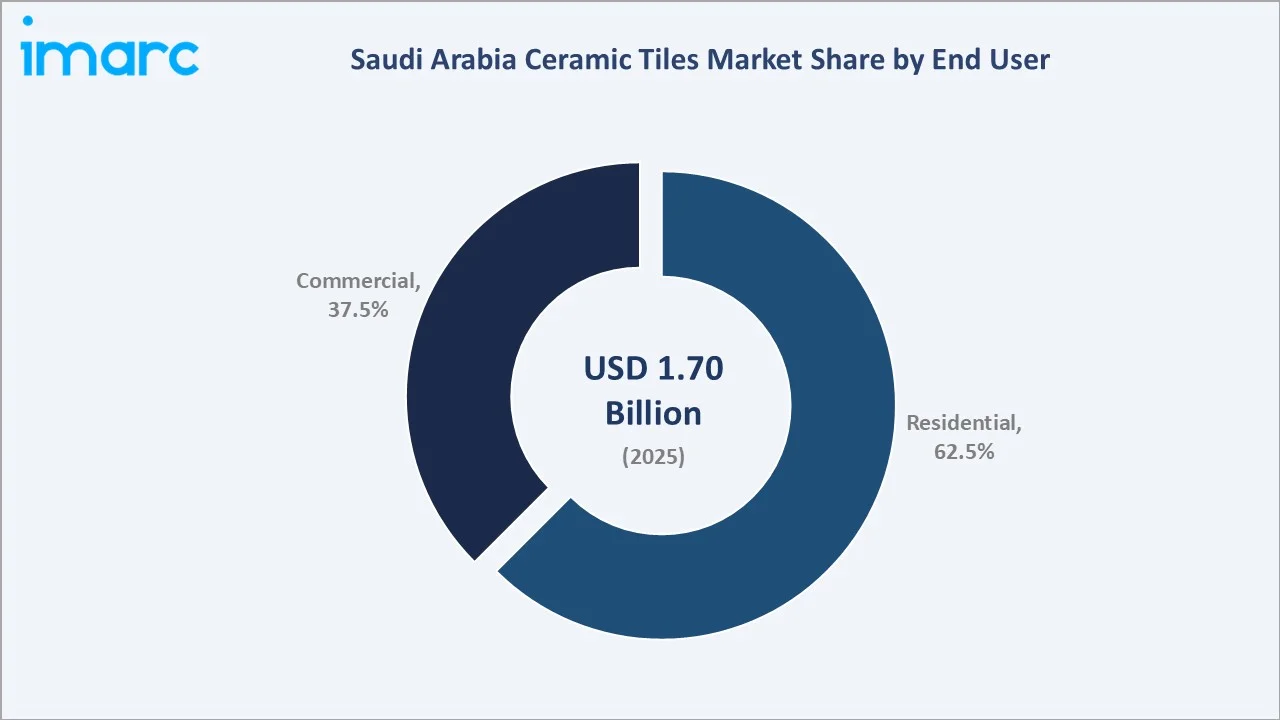

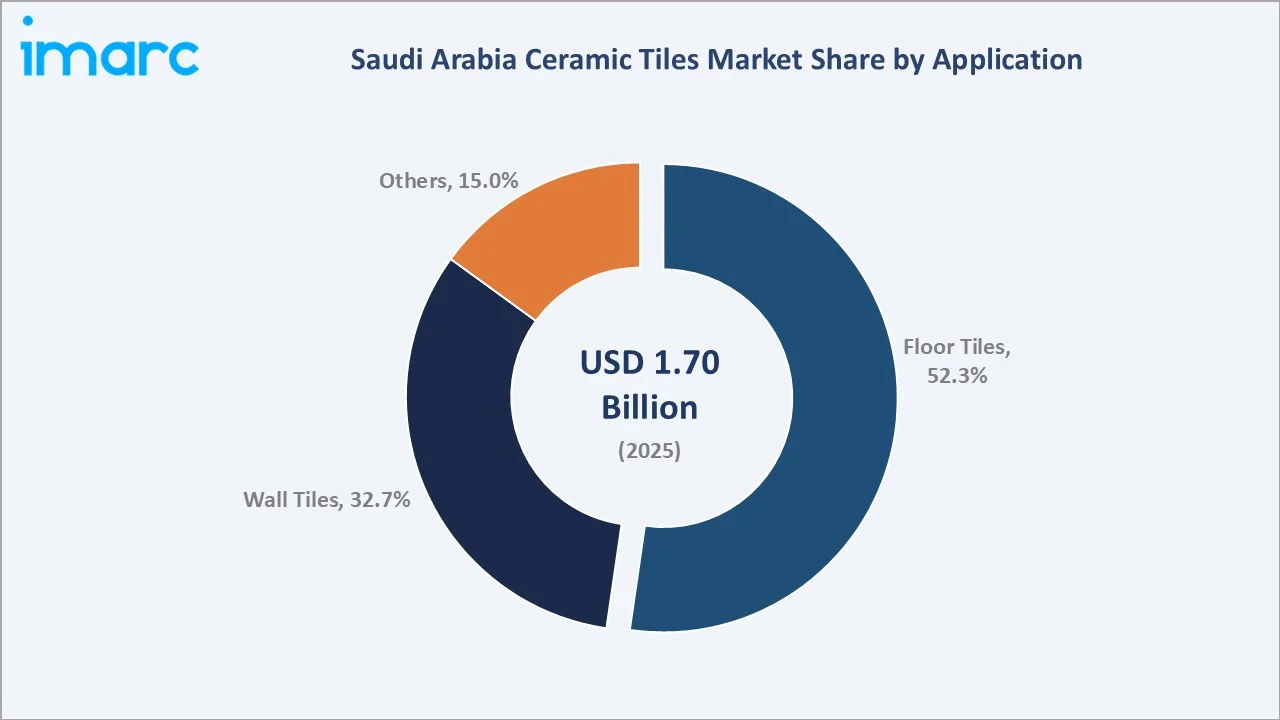

Residential applications dominate with a 62.5% end-user share in 2025, driven by government housing programmes and private villa construction across the Kingdom. Floor tiles represent the largest application at 52.3%. Growing consumer preference for large-format porcelain and digitally printed ceramic tiles is elevating average selling prices and supporting market value expansion beyond volume growth.

Executive Summary

The Saudi Arabia ceramic tiles market is experiencing robust growth, driven by unprecedented construction activity under Vision 2030, a rapidly expanding hospitality sector, and rising consumer demand for premium interior surfaces. The market reached USD 1.70 Billion in 2025 and is forecast to reach USD 3.40 Billion by 2034, reflecting a CAGR of 7.30%.

Residential end users account for 62.5% of demand in 2025, supported by housing programs such as Sakani, which aims to house over 70% of Saudi families in owned homes, and large-scale villa and apartment developments across Riyadh, Jeddah, and Dammam. Commercial demand (37.5%) is expanding rapidly, driven by hotel, retail, and institutional projects linked to Vision 2030 mega developments, including NEOM, the Red Sea Project, and Qiddiya.

Leading market participants, including Saudi Ceramic Company, RAK Ceramics, Arabian Ceramics Manufacturing Company (ACMC), and Alfanar Group, are investing in digital printing technology, large-format tile production, and sustainable manufacturing to align with evolving market preferences and regulatory standards.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (End User) |

Residential – 62.5% share (2025) |

|

Largest Segment (Application) |

Floor Tiles – 52.3% share (2025) |

|

Leading Region |

Northern & Central Region – 30.2% share (2025) |

|

Fastest Growing Application |

Floor Tiles (CAGR 7.90%, 2026-2034) |

|

Top Companies |

Saudi Ceramic Company, RAK Ceramics, Arabian Ceramics Manufacturing Company (ACMC), and alfanar Group |

|

Market Opportunity |

NEOM & mega-project tile demand estimated at USD 1.8 Billion through 2020-2025 |

Key Analytical Observations Supporting the Above Data:

- Residential – 62.5% end-user share (2025): The "Sakani" program has helped 93,622 Saudi families since early 2023, with 90,837 families moving into their first housing units. This aligns with Vision 2030's goal of increasing Saudi homeownership to 70% by 2030 through diverse housing products and financing solutions.

- Floor Tiles – 52.3% application share (2025): Floor tiles dominate due to the preference for large-format (600x600 mm and above) porcelain tiles in Saudi interior design. High ambient temperatures and sandstorm exposure increase wear-resistance requirements, making durable ceramic and porcelain floor tiles the preferred choice over carpets and vinyl.

- Northern & Central Region – 30.2% share (2025): Riyadh's construction pipeline is the largest in the Kingdom, with over USD 1.2 trillion in active projects as of 2025. Riyadh Metro, King Salman Park, and New Murabba developments are generating significant ceramic tile demand across residential, commercial, and public infrastructure categories.

- Western Region – fastest growing sub-market: The Red Sea Project (USD 28 Billion), Jeddah Central Development (USD 20 Billion), and the expansion of Madinah and Makkah hospitality infrastructure are driving the Western Region's accelerated tile demand, positioning it for above-market CAGR through 2034.

- Digital and large-format tile trend: Tiles measuring 1200x600 mm and 1200x1200 mm grew from 8% to 22% of Saudi tile sales between 2020-2025. Italian-inspired designs, wood-effect porcelain, and marble-look large slabs command 35–55% price premiums, elevating market value per sqm significantly.

Saudi Arabia Ceramic Tiles Market Overview

Ceramic tiles are versatile, durable building materials composed of clay, minerals, and water, fired at high temperatures to produce hard, glazed surfaces resistant to moisture, heat, stains, and wear. In the Saudi context, their durability under extreme heat conditions, low maintenance requirements, and aesthetic versatility make them the preferred surface material for both residential and commercial applications across all climate zones.

The Saudi ceramic tiles market is served by a combination of domestic manufacturers, led by Saudi Ceramic Company and Al-Jazira Factory, and substantial imports from China, India, Italy, and Spain. Imported tiles account for approximately 55–60% of total market volume in 2025, though SASO (Saudi Standards, Metrology and Quality Organisation) certification requirements are increasingly used to ensure product quality and support domestic manufacturers.

Market Dynamics

To evaluate market opportunities, Request Sample

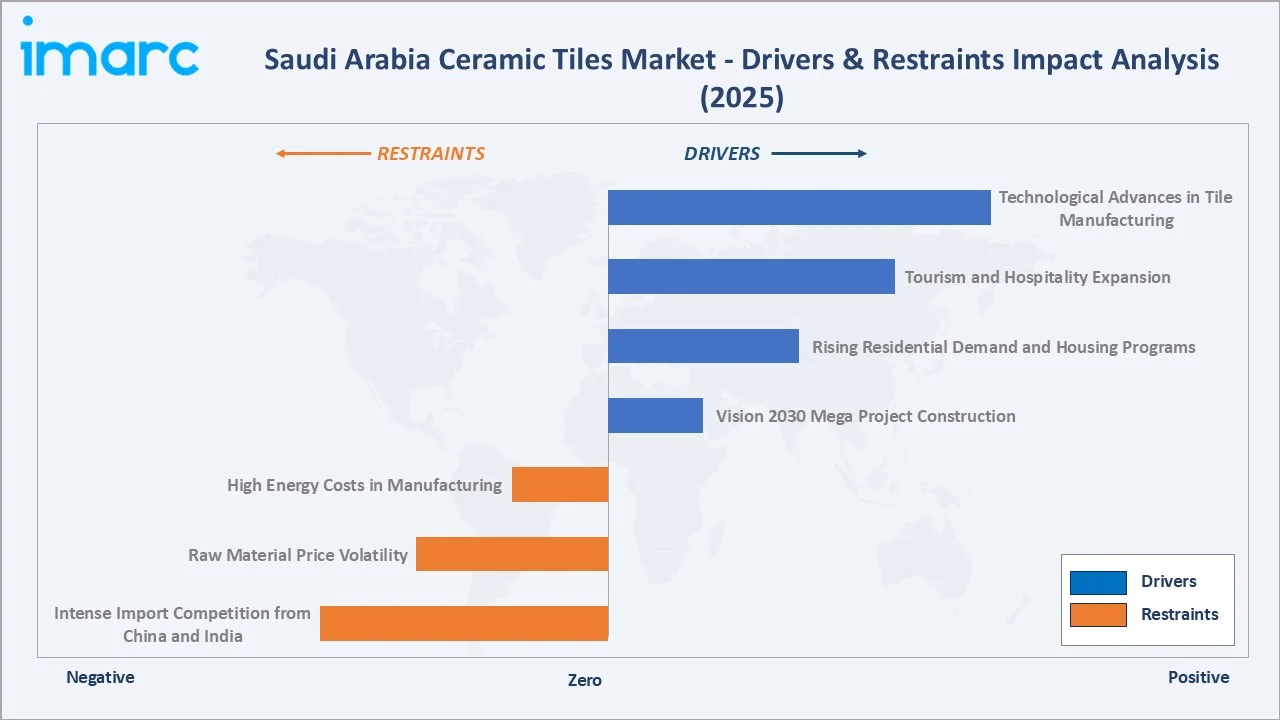

Market Drivers

- Vision 2030 Mega Project Construction: Saudi Arabia's Vision 2030 investment pipeline exceeds USD 1.5 Trillion across NEOM, the Red Sea Project, Qiddiya, Diriyah Gate, and New Murabba. NEOM alone covers 26,500 km2 and requires ceramic tile for The Line's 170 km of residential and commercial interiors, the Sindalah luxury island, and NEOM Bay hospitality developments.

- Rising Residential Demand and Housing Programs: Saudi Arabia achieved its 2025 homeownership goal a year ahead of schedule, with 65.4% of families owning homes in 2024, according to an official report.

- Tourism and Hospitality Expansion: Saudi Arabia aims to receive 150 million tourists annually by 2030, up from 100 million in 2023. Hotel room supply is expanding by 320,000 rooms by 2030 (Knight Frank data), with each hotel room requiring 25–40 sqm of ceramic tile across bathrooms, corridors, and lobby areas.

- Technological Advances in Tile Manufacturing: Digital inkjet printing technology enables photorealistic designs mimicking marble, wood, and stone at ceramic tile price points. Rectified tiles with zero-gap installation and anti-bacterial glazes are gaining market share in healthcare and food service applications, expanding the premium tile addressable market.

These drivers are mutually reinforcing. Vision 2030 investment in tourism infrastructure drives hotel construction, which expands commercial tile demand, which incentivizes investment in domestic manufacturing capacity, which increases supply-side competitiveness and market development.

Market Restraints

- Intense Import Competition from China and India: Chinese and Indian ceramic tiles offer 20–35% price advantages over domestically manufactured products, intensifying price competition in the mid-market and budget segments. In 2024, China’s ceramic tile exports totaled about CNY 228.38 billion (~USD 3.21 billion), with the top 20 export destinations accounting for 82.60 % of total export volume.

- Raw Material Price Volatility: Key raw materials, including kaolin, feldspar, and natural gas (used as kiln fuel), experienced significant price volatility between 2022 and 2025. Saudi Arabia's domestic clay resources require development, with some manufacturers dependent on imported raw materials that create exposure to global commodity price cycles.

- High Energy Costs in Manufacturing: Ceramic tile production is energy-intensive, with kiln firing accounting for approximately 35–40% of total production costs. Despite Saudi Arabia's advantageous natural gas prices for industrial users, energy efficiency improvements remain a critical focus area for domestic manufacturers competing against cost-optimized Asian imports.

Market Opportunities

- NEOM and Mega-Project Procurement: NEOM's procurement specifications for The Line, Sindalah, and Epicon developments favor premium porcelain tiles with sustainability certifications. International tile brands establishing preferred supplier status with NEOM procurement teams can capture long-term, high-value contracts worth USD 400–600 Million through 2034.

- Domestic Manufacturing Investment under Vision 2030: New ceramic tile plants under construction in the Sudair Industrial City and King Salman Energy Park (SPARK) benefit from subsidized energy, logistics infrastructure, and proximity to raw material deposits.

- Premium and Sustainable Tile Segments: ISO 14001-certified, low-VOC, and recycled-content ceramic tiles are in growing demand from luxury developers and hotel operators seeking LEED and EDGE green building certifications.

Market Challenges

- SASO Certification Compliance Burden: Saudi Standards, Metrology and Quality Organisation (SASO) requires all ceramic tiles to meet SASO 77 and SASO EN 14411 standards. Compliance adds 8–12% to import costs for non-GCC manufacturers, creating administrative burdens that smaller international suppliers struggle to manage.

- Design and Distribution Fragmentation: Saudi Arabia's 13 provinces are served by a fragmented distribution network with varying design preferences by region. Northern and Central Region buyers favour marble-look large-format tiles; Western Region coastal projects favour coastal-themed designs.

Emerging Market Trends

1. Large-Format Porcelain Tiles and Slabs

Large-format tiles (600x1200 mm and above) and full-body porcelain slabs are transforming Saudi interiors. Saudi Ceramic Company launched a new large-format production line in 2024, targeting villa and luxury apartment segments. Slab formats (1200x2400 mm) used as countertops, cladding, and feature walls grew 45% in sales value between 2022 and 2025.

2. Sustainable and Eco-Certified Tiles

Vision 2030's commitment to environmental sustainability is driving demand for eco-certified tiles in government and institutional projects. NEOM's environmental specifications require tiles with a minimum of 20% recycled content and low embodied carbon certifications. RAK Ceramics' participation in Saudi Build 2025 showcased its Re-Use range, the world's first porcelain tile using 100% pre-consumer recycled materials, targeting Vision 2030-aligned construction projects.

3. Anti-Bacterial and Functional Tiles

The Ministry of Health (MOH) has awarded Altakassusi Alliance Medical a Public-Private Partnership (PPP) to enhance radiology services across seven hospitals, with plans to privatize 290 hospitals and 2,300 healthcare institutions. Saudi Ceramic Company's NanoClean product line, incorporating titanium dioxide photo-catalytic coatings, addresses this segment.

4. Digital Commerce and Virtual Visualisation

Online tile sales in Saudi Arabia grew from 3% of total sales in 2020 to an estimated 11% in 2025, driven by e-commerce platforms and virtual room visualization tools. RAK Ceramics and Saudi Ceramic Company have launched AR-based mobile apps enabling customers to visualize tile designs in their own spaces before purchase.

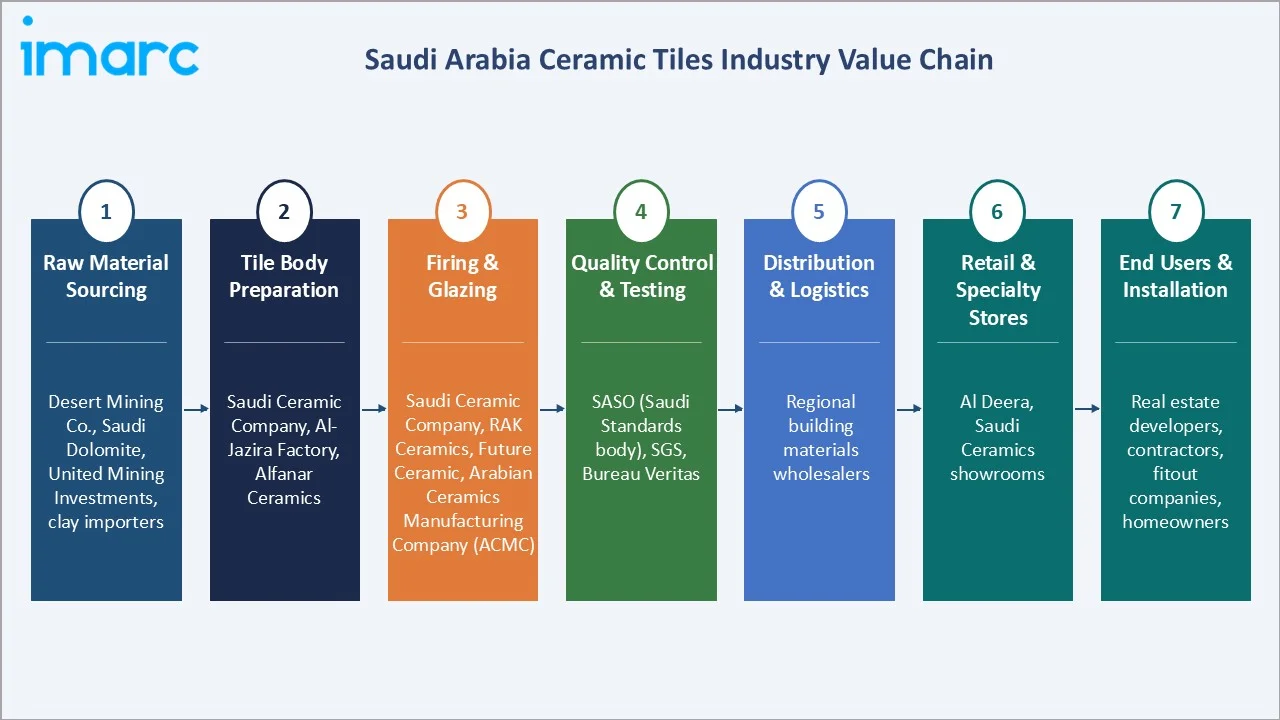

Industry Value Chain Analysis

The Saudi ceramic tiles value chain encompasses raw material sourcing, body preparation, firing and surface treatment, quality certification, and multi-channel distribution to residential and commercial end users. Each stage is supported by distinct regulatory requirements and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Desert Mining Co. (Saudi Ceramics), Saudi Dolomite, United Mining Investments, clay importers |

|

Tile Body Preparation |

Saudi Ceramic Company, Al-Jazira Factory for Ceramic Tiles, Alfanar Ceramics |

|

Firing & Glazing |

Saudi Ceramic Company, RAK Ceramics, Future Ceramic Company, Arabian Ceramics Manufacturing Company (ACMC) |

|

Quality Control & Testing |

SASO (Saudi Standards body), SGS, Bureau Veritas |

|

Distribution & Logistics |

Regional electrical and building materials wholesalers |

|

Retail & Specialty Stores |

Al Deera, Saudi Ceramics showrooms |

|

End Users & Installation |

Real estate developers, contractors, fitout companies, homeowners |

Technology Landscape in the Saudi Arabia Ceramic Tiles Industry

Digital Inkjet Printing Technology

Saudi Ceramic Company and RAK Ceramics' Saudi operations use 8-colour, high-resolution inkjet systems, achieving 400+ DPI resolution. Ink consumption per sqm has fallen 22% since 2020, reducing production costs while expanding the design catalogue to thousands of SKUs per production line.

Rectification and Precision Manufacturing

Saudi Ceramic Company invested SAR 120 million in new rectification lines in 2024. Rectified tiles command a 25–40% price premium over standard tiles and are the specification choice in NEOM, Red Sea Project, and premium villa developments targeting LEED certification.

Sustainable Manufacturing and Kiln Technology

Roller kiln technology has reduced firing time from 45 minutes to under 28 minutes for standard tiles at Saudi Ceramic's facilities, reducing energy consumption per sqm by 18% between 2020 and 2025. RAK Ceramics' heat recovery systems capture waste kiln gases to pre-heat incoming raw materials, reducing natural gas consumption by 12%.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

🔒 |

🔒 |

2025 |

|

Application |

Floor Tiles |

52.3% |

2025 |

|

Construction Type |

🔒 |

🔒 |

2025 |

|

End User |

Residential |

62.5% |

2025 |

|

Region |

Northern and Central Region |

30.2% |

2025 |

By End User

The residential segment dominates with a 62.5% share in 2025. Saudi Arabia's housing market is underpinned by structural demand from a young, rapidly urbanizing population, with more than seven in ten citizens of the population under 35 years old. Government initiatives, including the Wafi off-plan sales program, Real Estate Development Fund (REDF) mortgage subsidies, and the Sakani housing allocation system, are sustaining residential construction volumes at record levels.

To access detailed market analysis, Request Sample

The commercial segment holds 37.5%, driven by hotel, retail, healthcare, and educational facility construction under Vision 2030. Hospitality accounts for the largest share of commercial tile consumption, with Saudi Arabia's 320,000 new hotel room pipeline (2025–2030) requiring approximately 30–40 sqm of tile per room across bathrooms, corridors, and lobby areas.

By Application

Floor tiles dominate the application mix at 52.3% in 2025, reflecting the Saudi preference for hard-surface, easy-to-clean flooring in the region's dry, dusty climate. Large-format porcelain floor tiles are the premium category, with 600x600 mm and 800x800 mm formats standard in residential villas, and 1200x600 mm formats common in commercial spaces.

Wall tiles represent 32.7% of the market, primarily used in bathrooms, kitchens, and building facades. The growing adoption of full-height wall tile installations (replacing painted walls) in premium residential and hotel projects is expanding average tile consumption per unit. Others (15.0%) include outdoor terrace tiles, swimming pool tiles, and specialized anti-bacterial tiles for healthcare applications.

Regional Market Insights

The Northern and Central Region's market leadership (30.2%, 2025) is anchored by Riyadh, which hosts over SAR 1.3 trillion in active construction projects. The King Salman Park (16 km2), New Murabba development (19 km2 mixed-use city), and continued residential expansion across Riyadh's northern districts are sustaining the highest ceramic tile demand concentration in the Kingdom.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory / Market Notes |

|

Northern & Central Region |

30.2% |

Riyadh construction boom, King Salman Park, New Murabba, Qiddiya |

SASO compliance; Riyadh Municipality building codes |

|

Western Region |

26.8% |

Red Sea Project, Jeddah Central, Madinah/Makkah hospitality |

Vision 2030 tourism zone standards; heritage district specs |

|

Eastern Region |

23.1% |

Oil sector housing, ARAMCO facilities, Jubail Industrial City |

Saudi Aramco procurement standards; SABIC supplier specs |

|

Southern Region |

19.9% |

Aseer Vision, eco-tourism, residential expansion in Abha, Najran |

Aseer Mountain architecture standards; eco-cert requirements |

The Western Region (26.8%) is the fastest-growing sub-market, driven by the USD 28 Billion Red Sea Project, which includes 50 hotels and over 1,000 residential villas, and Jeddah Central Development's USD 20 billion mixed-use regeneration. The Eastern Region (23.1%) benefits from continued Saudi Aramco and SABIC industrial facility construction, alongside residential development serving the oil sector workforce.

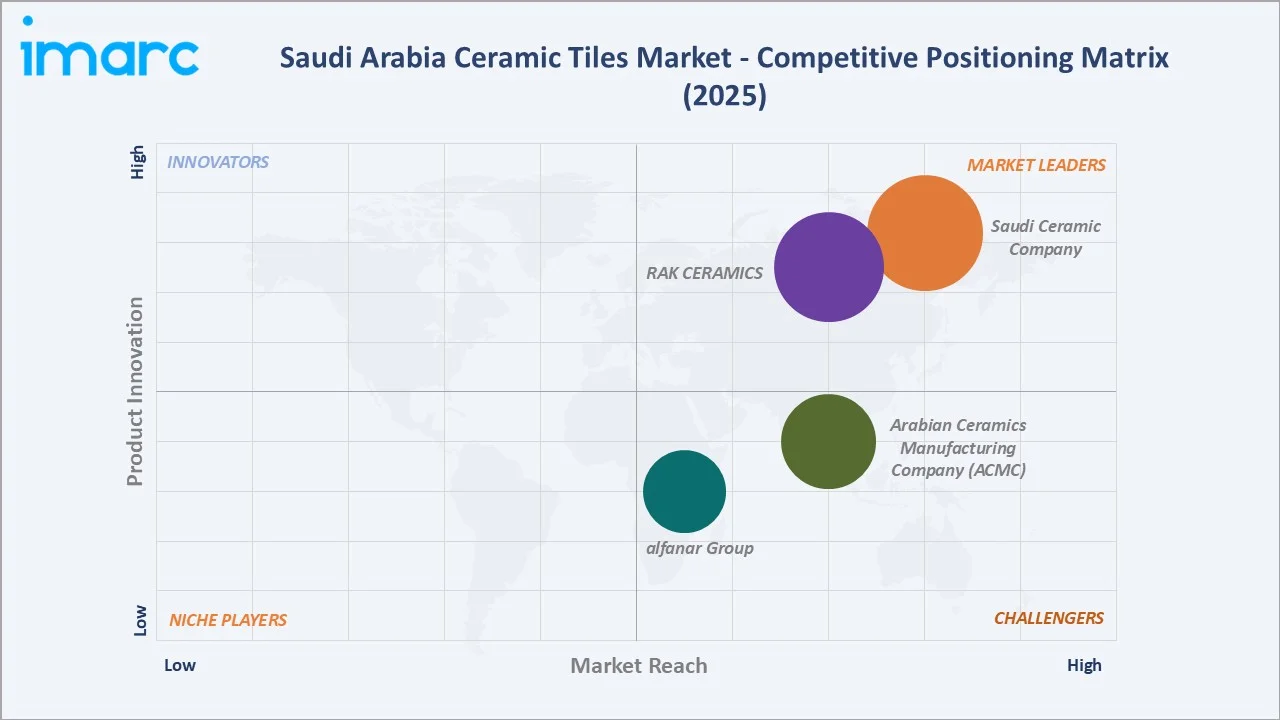

Competitive Landscape

The Saudi Arabia ceramic tiles market exhibits a moderately fragmented competitive structure. Domestic producers coexist with large-volume importers from China, India, Italy, and Spain. Saudi Ceramic Company, the largest listed ceramic manufacturer in the Kingdom, and RAK Ceramics are the two dominant players, collectively holding approximately 35–40% of the organized market.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Saudi Ceramic Company |

Saudi Ceramics |

Market Leader |

Largest domestic producer; full product range from standard to premium; Riyadh-based manufacturing |

|

RAK CERAMICS |

RAK; Maximus |

Market Leader |

Premium international brand; active Saudi Build presence; Re-Use sustainability range |

|

Arabian Ceramics Manufacturing Company (ACMC) |

Arabian Ceramics |

Strong Challenger |

Strong Western Region distribution; hotel and hospitality project focus; Italian design partnerships |

|

alfanar Group |

EXA Alfanar Ceramic |

Challenger |

Industrial group vertical integration, competitive pricing, and a growing retail distribution network |

Key Company Profiles

Saudi Ceramic Company

Saudi Ceramic Company (SCC), headquartered in Riyadh and listed on Tadawul (TADAWUL: 2040), is the Kingdom's largest ceramic tile and sanitaryware manufacturer.

- Product Portfolio: Glazed ceramic floor and wall tiles (standard and large-format), porcelain tiles, scratch-free tiles, sanitaryware, and adhesives.

- Recent Developments: Saudi Ceramics Company accounted for a net profit of SAR 181 million in 2025, driven by stronger sales and cost improvements.

- Strategic Focus: Capacity expansion for porcelain and large-format tiles; NEOM and mega-project supply contracts; premiumization through digital printing investment.

RAK Ceramics

RAK Ceramics, headquartered in Ras Al Khaimah, UAE, and listed on the Abu Dhabi Securities Exchange, is one of the world's largest ceramic tile manufacturers with operations in 4 geographic territories.

- Product Portfolio: Porcelain tiles (standard and large-format), glazed ceramic tiles, Re-Use recycled-content tiles, sanitaryware, and faucets.

- Recent Developments: In October 2025, at Saudi Build 2025 in Riyadh, RAK Ceramics showcased its newest ceramic and porcelain tiles alongside sanitaryware and faucet collections, highlighting innovations like SOFTECH and Scratch Guard that blend advanced performance, design, and sustainability.

- Strategic Focus: Sustainability leadership through recycled-content and low-carbon products; digital showroom and e-commerce expansion; NEOM and Red Sea Project premium supply positioning.

Arabian Ceramics Manufacturing Company (ACMC)

Arabian Ceramics Manufacturing Company (ACMC), established in Saudi Arabia, focuses on the Western Region and hospitality project segments. The company maintains strong relationships with hotel and resort developers, positioning its products in premium commercial applications where Italian-inspired design aesthetics are preferred.

- Product Portfolio: Glazed and porcelain floor and wall tiles; decorative and feature tiles for hotel lobbies, spa facilities, and resort developments.

- Strategic Focus: Hospitality segment deepening; premium design partnership with Italian tile studios; coastal and eco-resort tile range development.

Market Concentration Analysis

The Saudi Arabia ceramic tiles market exhibits moderate concentration at the top tier, with Saudi Ceramic Company and RAK Ceramics collectively holding approximately 35–40% of organized market revenue. Below this, a mid-tier of 5–7 domestic Saudi manufacturers and specialist importers shares a further 30–35%.

Market formalization is accelerating, driven by SASO certification requirements that raise compliance barriers for smaller, non-certified importers. Vision 2030 mega-project procurement standards favor certified, quality-assured suppliers, creating a competitive moat for established players. Saudi Ceramic Company's Tadawul listing and RAK Ceramics' Gulf Cooperation Council presence give both companies access to public capital markets for capacity expansion financing unavailable to private competitors.

Investment & Growth Opportunities

Fastest Growing Segments

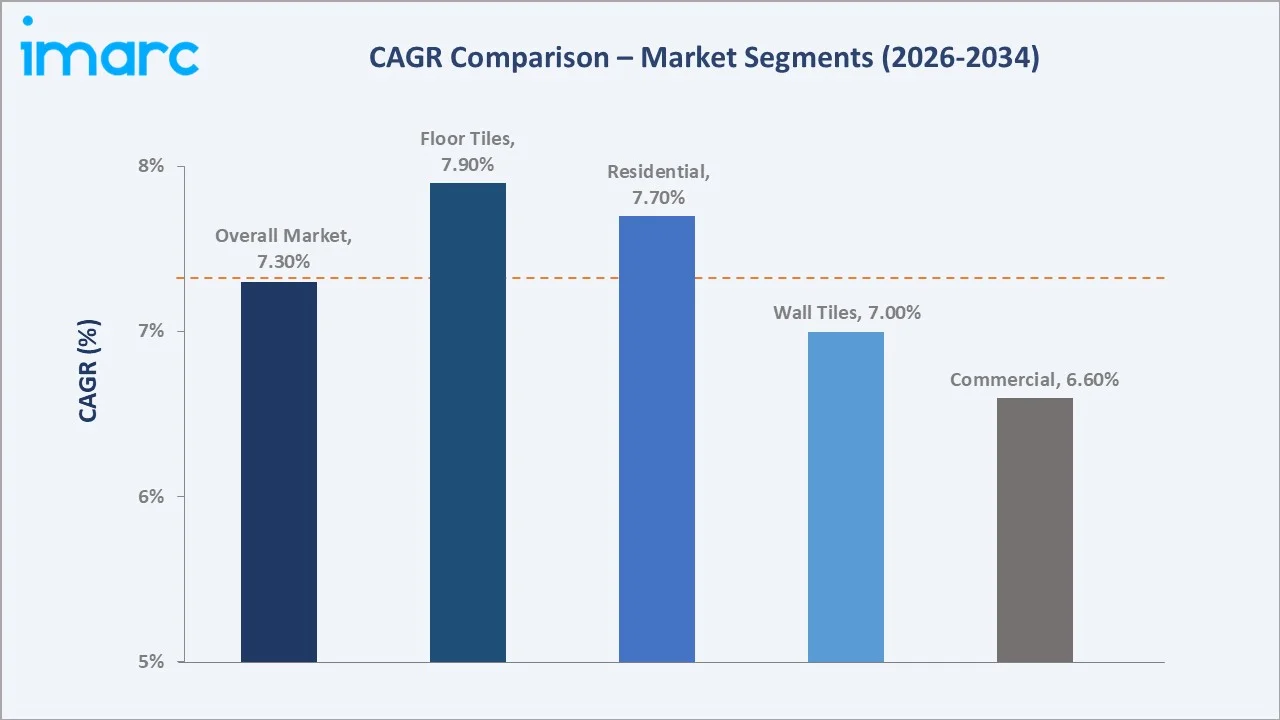

Floor tiles (CAGR 7.90%), premium large-format porcelain (CAGR 8.5% within floor tiles), and commercial hospitality tiles (CAGR 7.2% within commercial end-use) represent the three highest-growth investment vectors through 2034.

Premium porcelain and large-format slab sub-segment are projected to grow from approximately USD 135 Million in 2025 to over USD 291 Million by 2034.

Mega-Project Supply Partnerships

NEOM, the Red Sea Project, Qiddiya, Diriyah Gate, and New Murabba collectively represent an estimated USD 1.8 Billion in ceramic tile procurement through 2034. Manufacturers establishing preferred vendor status with Aramco, NEOM Company, and Red Sea Global procurement teams gain access to long-term, high-value supply contracts.

Domestic Manufacturing Investment

- Industrial Development Fund (IDF): Low-interest SAR-denominated financing for manufacturing investments under the National Industrial Development Program.

- Sudair Industrial City: New ceramic tile manufacturing investments in Sudair benefit from logistics infrastructure, subsidized energy, and proximity to Riyadh demand centers.

- IKTVA Program: Saudi Aramco's IKTVA program and government project tendering prefer local content; SASO-certified domestic producers qualify for procurement advantages across USD 100+ Billion in active construction projects.

Future Market Outlook (2026-2034)

The Saudi Arabia ceramic tiles market is positioned for sustained strong growth through 2034. From a base of USD 1.70 Billion in 2025, the market is projected to reach USD 3.40 Billion by 2034.

The primary structural driver remains Vision 2030's construction program, which is front-loaded with major project completions between 2026–2030 (NEOM Phase 1, Red Sea Project Phase 2, Qiddiya Phase 1). These completions will generate concentrated, high-value tile procurement demand between 2026 and 2029.

Beyond 2030, organic demand growth from a rising Saudi population (projected at 42 million by 2034), increasing homeownership rates, and an expanding hospitality sector will sustain the market trajectory.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews with over 120 industry participants in 2024–2025, including domestic ceramic tile manufacturers, import distributors, construction material wholesalers, real estate developers, hotel procurement managers, and interior designers across Saudi Arabia.

Secondary Research

Secondary research included Saudi Ceramic Company annual reports, SASO regulatory documentation, Ministry of Housing construction statistics, Real Estate General Authority data, NEOM and Red Sea Global project publications, and industry databases. Over 240 secondary sources were reviewed and validated for consistency.

Forecasting Models

Market size estimations used top-down (GDP and construction investment-driven) and bottom-up (residential unit completions × average tile consumption per unit) forecasting approaches. The base-case CAGR of 7.30% reflects consensus construction activity projections validated against Saudi Ceramic Company's reported revenue growth trajectory of 5.5–6.2% during 2022–2025.

Saudi Arabia Ceramic Tiles Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Glazed, Porcelain, Scratch Free, Others |

| Applications Covered | Floor Tiles, Wall Tiles, Others |

| Construction Types Covered | New Construction, Replacement and Renovation |

| End Users Covered |

|

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Saudi Ceramic Company, RAK CERAMICS, Arabian Ceramics Manufacturing Company (ACMC), alfanar Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia ceramic tiles market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia ceramic tiles market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia ceramic tiles industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Ceramic Tiles Market Report

The Saudi Arabia ceramic tiles market reached USD 1.70 Billion in 2025 and is projected to reach USD 3.40 Billion by 2034, growing at a CAGR of 7.30%.

The market is expected to grow at a CAGR of 7.30% during 2026-2034, driven by Vision 2030 construction, residential demand growth, and tourism and hospitality expansion.

The Northern and Central Region leads with a 30.2% share in 2025, driven by Riyadh's SAR 1.3 trillion construction pipeline, including New Murabba, King Salman Park, and Qiddiya.

Residential end users dominate with a 62.5% share in 2025 (approx. USD 2.82 Billion), supported by the Sakani programme, REDF mortgage financing, and over 800,000 residential units under construction.

Key players include Saudi Ceramic Company, RAK Ceramics, Arabian Ceramics Manufacturing Company (ACMC), and alfanar Group.

Key trends include the rising sustainable and eco-certified tile demand from Vision 2030 projects, anti-bacterial functional tiles for healthcare facilities, and the growth of digital commerce and AR visualization tools.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)