Saudi Arabia Data Center Market Size, Share, Trends and Forecast by Data Center Size, Tier Type, Absorption, and Region, 2026-2034

Saudi Arabia Data Center Market Size, Share, Trends & Forecast (2026-2034)

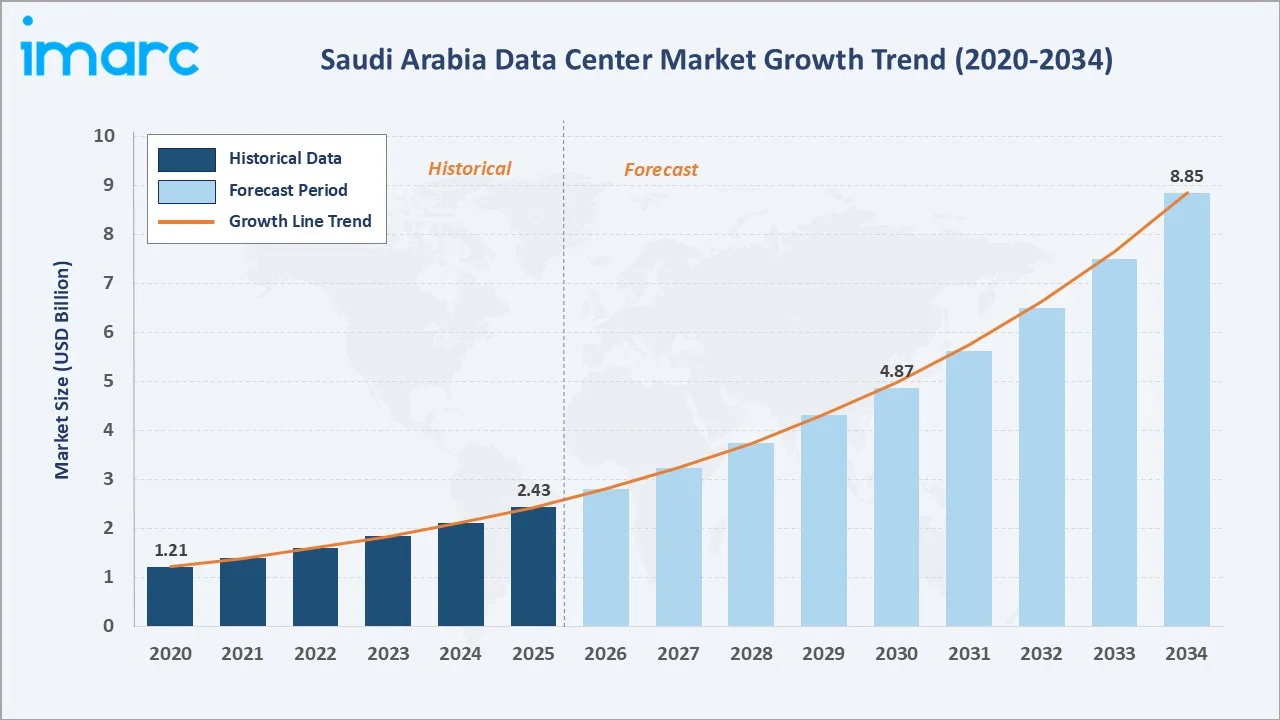

The Saudi Arabia data center market reached USD 2.43 Billion in 2025 and is projected to reach USD 8.85 Billion by 2034, growing at a CAGR of 14.93% during 2026-2034. Saudi Vision 2030, rapid cloud adoption, surge in AI workloads, and major hyperscaler investments are the primary catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.43 Billion |

|

Forecast Market Size (2034) |

USD 8.85 Billion |

|

CAGR (2026-2034) |

14.93% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Northern and Central Region (48.2%, 2025) |

|

Fastest Growing Region |

Western Region |

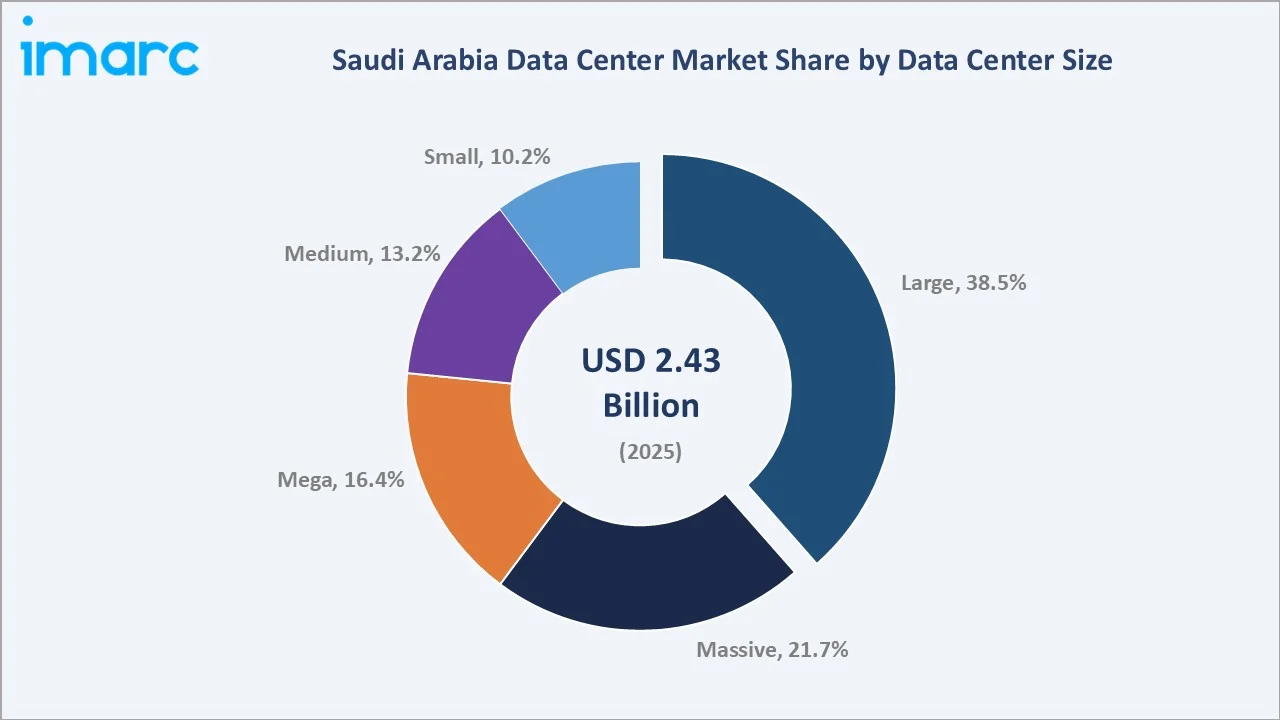

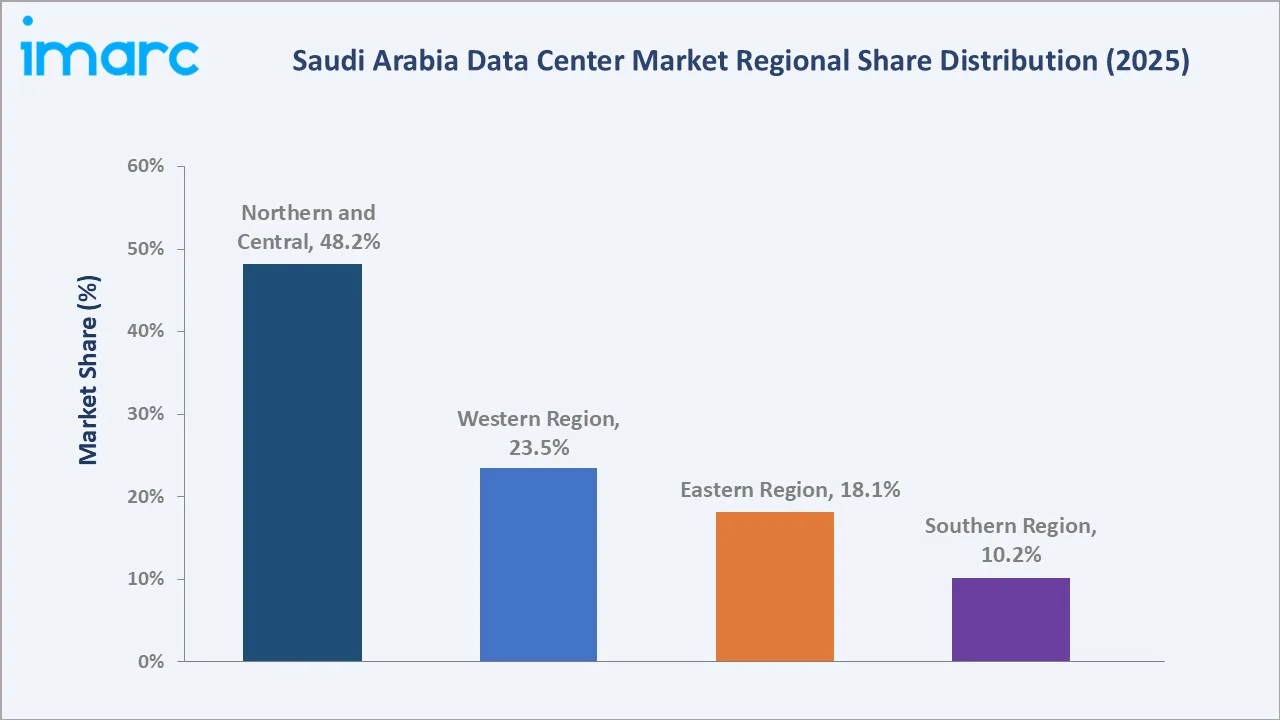

The Northern and Central Region commands the largest share at 48.2% in 2025, anchored by Riyadh’s status as a hyperscale hub. Large data centers hold 38.5% of capacity share, reflecting the kingdom’s preference for enterprise-grade, hyperscale-ready infrastructure aligned with Vision 2030’s digital transformation goals.

To get more information on this market, Request Sample

With applications spanning cloud computing, enterprise IT, artificial intelligence, IoT analytics, and government digital services, the market is set for exceptional compound expansion, underpinned by multi-billion-dollar investments from Amazon Web Services, Microsoft Azure, Google, and Oracle in the 2024–2026 window.

Executive Summary

The Saudi Arabia data center market is experiencing an extraordinary growth phase. It reached USD 2.43 Billion in 2025, up from USD 1.21 Billion in 2020, and is forecast to reach USD 8.85 Billion by 2034 at a CAGR of 14.93%. This trajectory is among the fastest in the Middle East and positions Saudi Arabia as the region's leading data center destination.

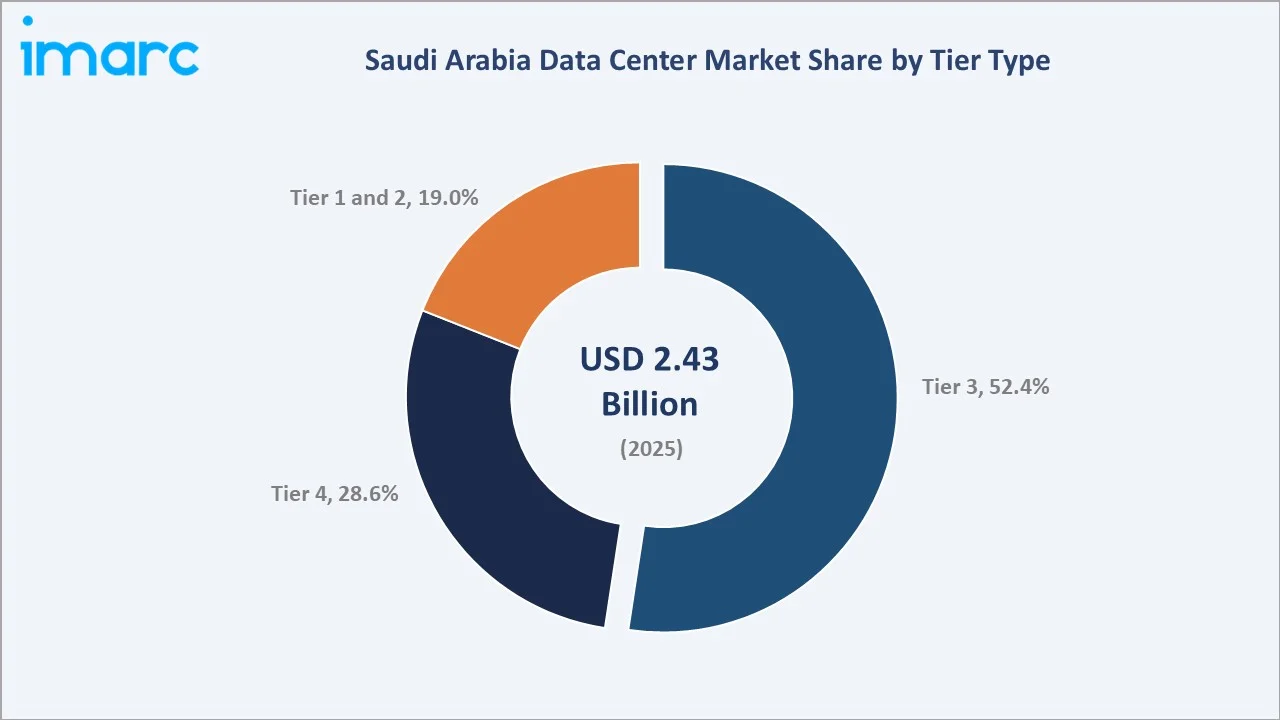

Saudi Vision 2030 and the National Digital Transformation Program provide structural, policy-backed demand. Cloud hyperscalers, including AWS, Microsoft Azure, Google Cloud, and Oracle, have collectively committed over USD 15 billion to infrastructure in Saudi infrastructure between 2023 and 2027. Tier 3 facilities dominate at 52.4% as enterprises balance uptime requirements with capital efficiency. The Northern and Central Region holds 48.2% market share in 2025, driven by Riyadh’s established ICT ecosystem.

Large data centers (38.5% share) reflect hyperscaler demand. AI inference and model training workloads are reshaping power density requirements. The Saudi government’s 100% digital service target by 2030 and NEOM’s smart city requirements are catalyzing significant new capacity additions.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (DC Size) |

Large – 38.5% share (2025) |

|

Largest Segment (Tier Type) |

Tier 3 – 52.4% share (2025) |

|

Leading Region |

Northern and Central Region – 48.2% share (2025) |

|

Fastest Growing Region |

Western Region (Jeddah expansion) |

|

Top Companies |

stc, Mobily, DETASAD Cloud, Amazon Web Services, Inc., and Microsoft |

|

Market Opportunity |

AI-ready & renewable-powered data centers |

Key Analytical Observations:

- Large data centers hold a 38.5% share in 2025, driven by hyperscaler co-location demand and government cloud infrastructure projects requiring high-density compute environments.

- Tier 3 facilities command 52.4% of the market, balancing 99.982% uptime SLAs with cost-effective capital expenditure, the preferred choice for enterprise and cloud operators.

- The Northern and Central Region holds 48.2%, anchored by Riyadh's data center corridor hosting AWS, Microsoft, and Google cloud regions.

- The Western Region is the fastest-growing region, benefitting from Jeddah's position as a submarine cable landing hub for Africa-Europe-Asia connectivity.

- AI-driven power density is accelerating, with new facilities targeting 60 or more kW per rack versus the traditional 5–10 kW, fundamentally changing facility design economics.

Saudi Arabia Data Center Market Overview

Saudi Arabia's data center market encompasses colocation facilities, hyperscale campuses, edge deployments, and government-owned data centers providing compute, storage, and networking infrastructure. The kingdom is transitioning from a net data consumer to a regional data hub, catalyzed by Vision 2030's USD 6.4 billion National Digital Transformation program and the Communications, Space & Technology Commission's (CST) cloud-first mandate.

Macroeconomic tailwinds are compelling. Saudi Arabia's GDP reached USD 1.068 trillion in 2023, with the digital economy is projected to contribute 19.2% to GDP by 2025, marking an increase of approximately 26% compared to 2023. The kingdom recorded 36.84 million internet users in 2024 (99.0% penetration), generating explosive data growth across e-commerce, fintech, media streaming, and government services.

Market Dynamics

To evaluate market opportunities, Request Sample

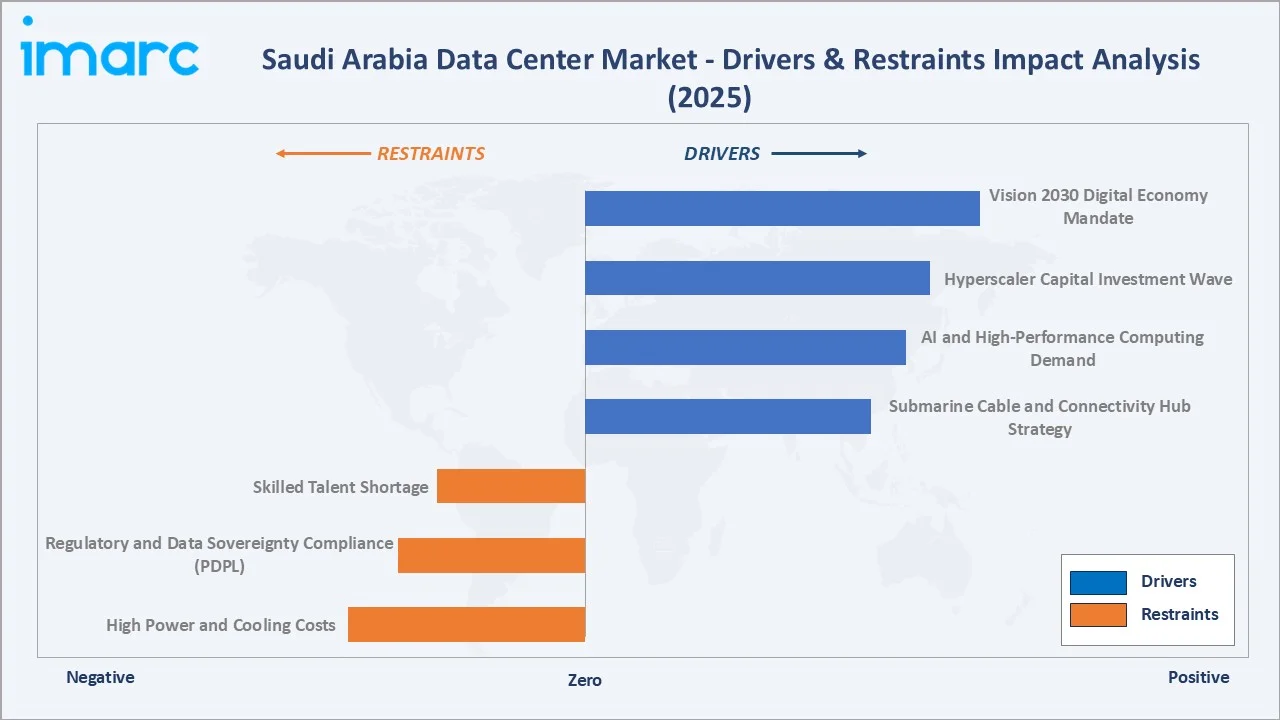

Market Drivers

- Vision 2030 Digital Economy Mandate: The Saudi government has mandated 100% digitalization of government services by 2030. The National Data Management Office (NDMO) oversees data sovereignty requirements, compelling government agencies to migrate to sovereign cloud hosted in Saudi facilities, directly generating USD 450+ million in annual data center demand by 2025.

- Hyperscaler Capital Investment Wave: AWS launched three Availability Zones in Riyadh in 2024, Microsoft confirmed its Saudi Arabia East datacenter region will be available from Q4 2026, and Google Cloud announced its Saudi region in 2024.

- AI and High-Performance Computing Demand: Saudi Aramco, NEOM, and the Public Investment Fund (PIF) are deploying large language models and AI inference platforms. These workloads require GPU clusters with 30–100x the power density of traditional servers, necessitating new-generation data center builds.

- Submarine Cable & Connectivity Hub Strategy: Saudi Arabia's geographic position at the intersection of Asia, Africa, and Europe makes it a natural connectivity hub. The 2Africa cable (Meta-backed), the AAE-1, and the upcoming EIG-2 system connect through Saudi landing stations, reinforcing the kingdom's role in regional internet infrastructure.

Market Restraints

- High Power and Cooling Costs: As of 2024, data centers consume around 1–2% of global electricity, with projections indicating this could increase to 3–5% by 2030 as computational demand continues to grow. This elevates operating expenditures by 20–30% compared to temperate-climate facilities, pressuring the total cost of ownership.

- Regulatory and Data Sovereignty Compliance: The PDPL (Personal Data Protection Law, effective 2021, amended 2023) and SAMA cybersecurity frameworks impose stringent data residency, localization, and audit requirements that increase compliance costs for operators and delay facility certifications.

- Skilled Talent Shortage: Data center engineers, network architects, and AI infrastructure specialists are in short supply domestically. Saudi operators spend 25–35% above global benchmarks on specialist talent. Nationalization (Saudization) requirements under Vision 2030 add workforce development complexity.

Market Opportunities

- AI-Ready and GPU-Optimized Facilities: Facilities designed around 50–100 kW/rack power density, liquid cooling, and high-speed interconnect represent a USD 2+ billion incremental opportunity by 2030. Saudi Aramco's AIOps initiative and NEOM's smart city AI platform are anchor tenants for this segment.

- Renewable-Powered Green Data Centers: The Kingdom aims to generate 50% of its power from renewable energy sources by 2030, provides a pathway to green data center operations. ESG-compliant facilities attract international tenants (particularly European enterprises) with sustainability mandates, commanding 15–20% premium rents.

- Edge and Tier 2 City Expansion: The rollout of 5G coverage now reaching 77% of the country and the development of economic zones in Yanbu, Tabuk, and Jizan creates demand for edge computing nodes. Edge data centers below 1 MW represent an underpenetrated USD 380 million market by 2030.

Market Challenges

- Water Scarcity for Cooling: Saudi Arabia is one of the world's most water-scarce countries (annual water supply of roughly 89.5 m3 per person). Air-side economizers are limited by ambient conditions, and water-cooled systems face sustainability criticism, pushing operators toward higher-cost air-cooled and immersion cooling technologies.

- Power Infrastructure Constraints: National grid capacity in some secondary cities lags demand growth. Power connection timelines of 18–36 months create bottlenecks for new data center projects. SEC’s smart meter deployment program, targeting 100 percent coverage aims to address this, but near-term constraints persist.

Emerging Market Trends

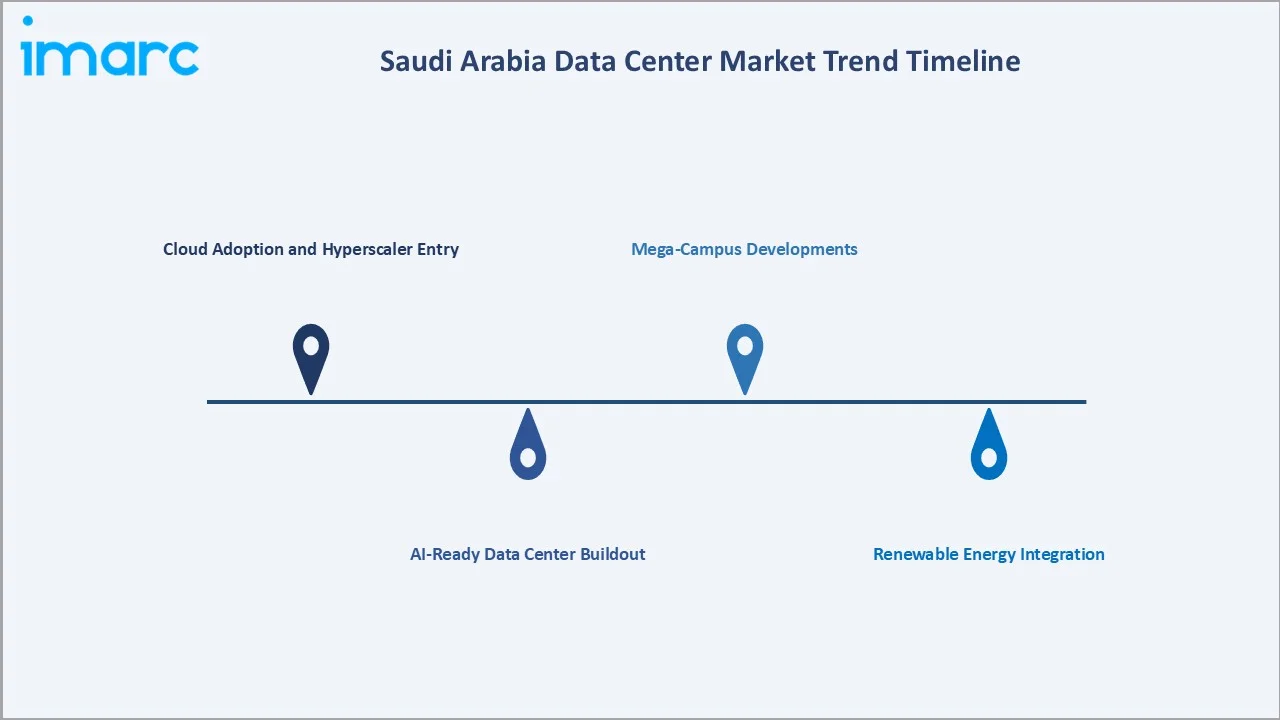

1. Cloud Adoption and Hyperscaler Entry (2021–2023)

AWS, Microsoft Azure, and Google Cloud launched Saudi cloud regions between 2021 and 2024, triggering an enterprise cloud migration wave. Cloud adoption across Saudi enterprises grew from 28% in 2020 to 67% in 2025, directly translating into co-location and managed services demand at hyperscale-adjacent facilities.

2. AI-Ready Data Center Buildout (2024–2026)

AI infrastructure requirements are reshaping data center design in Saudi Arabia. Facilities now specify GPU-dense pods (NVIDIA H100/H200 clusters) requiring 50–80 kW/rack, direct liquid cooling (DLC), and 400G network fabrics. The SDAIA's National AI Strategy 2030 mandates AI capability across 16 government sectors, creating a structural tailwind for specialized facilities.

3. Renewable Energy Integration (2025–2027)

Data center operators are signing power purchase agreements (PPAs) with NEOM's solar and wind projects. In February 2025, DataVolt signed an agreement with NEOM to develop the region’s first net-zero AI factory campus in Oxagon, backed by an initial $5 billion investment and targeting a total capacity of 1.5 GW.

4. Mega-Campus Developments (2028–2030)

NEOM's 26 km² Sindalah island and THE LINE’s integrated ICT infrastructure require multi-hundred-megawatt data center campuses. In August 2024, Oracle announced the launch of a new public cloud region in Riyadh as part of its USD 1.5 billion investment to expand cloud infrastructure and support Saudi Arabia’s digital economy and AI growth.

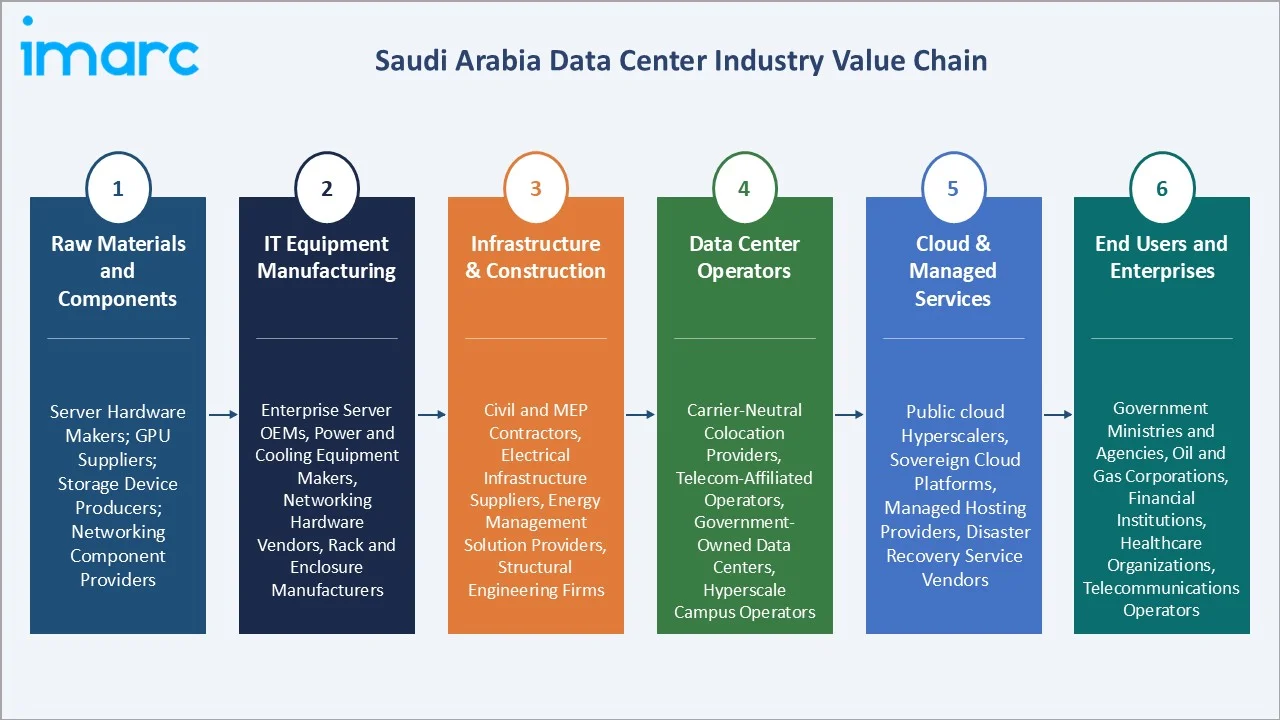

Industry Value Chain Analysis

The Saudi data center value chain spans semiconductor-level component manufacturing through to enterprise end-user service delivery, with specialized operators at each stage whose performance influences facility reliability, efficiency, and competitiveness.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Server hardware manufacturers, GPU suppliers, storage device producers, networking component providers |

|

IT Equipment Manufacturing |

Enterprise server OEMs, power and cooling equipment makers, networking hardware vendors, rack and enclosure manufacturers |

|

Infrastructure & Construction |

Civil and MEP contractors, electrical infrastructure suppliers, energy management solution providers, structural engineering firms |

|

Data Center Operators |

Carrier-neutral colocation providers, telecom-affiliated operators, government-owned data centers, hyperscale campus operators |

|

Cloud & Managed Services |

Public cloud hyperscalers, sovereign cloud platforms, managed hosting providers, disaster recovery service vendors |

|

End Users & Enterprises |

Government ministries and agencies, oil and gas corporations, financial institutions, healthcare organisations, telecommunications operators |

Technology Landscape in the Saudi Arabia Data Center Industry

Liquid Cooling and Immersion Technology

Given Saudi Arabia's extreme ambient temperatures, liquid cooling adoption is accelerating. Direct liquid cooling (DLC) and two-phase immersion cooling systems reduce PUE from 1.7 to sub-1.3. In January 2026, Vertiv, in collaboration with Uptime Institute, launched its AI Innovation Roadshow in Riyadh to showcase advanced AI and high-performance computing (HPC) infrastructure solutions.

AI Infrastructure and GPU Clusters

SDAIA's deployment of NVIDIA DGX SuperPOD clusters (September 2024) and Saudi Aramco's AI supercomputer (Shaheen III at KAUST) represent the leading edge of AI infrastructure in the kingdom. Facilities hosting GPU clusters require specialized power distribution units (PDUs) at 208/480V, precision air flow management, and sub-millisecond latency interconnects.

Modular and Pre-Fabricated Data Centers

Modular data center deployments (factory-assembled, shipped as containers) enable deployment timelines of 6–9 months versus 24–36 months for traditional builds. Huawei, Schneider Electric, and Delta Electronics supply modular solutions adopted in Saudi edge deployments in Medina, Dammam, and Abha.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Data Center Size | Large | 38.5% | 2025 |

| Tier Type | Tier 3 | 52.4% | 2025 |

| Absorption | Utilized | 72.3% | 2025 |

| Region | Northern and Central Region | 48.2% | 2025 |

By Data Center Size

Large data centers dominate the market with a 38.5% share in 2025. These facilities, typically 20–50 MW in power capacity, serve hyperscaler co-location and government cloud requirements. They benefit from economies of scale in power procurement, cooling infrastructure, and security staffing, making them the cost-optimal solution for enterprise-scale workloads.

To access detailed market analysis, Request Sample

Massive data centers (21.7%) represent hyperscaler-owned campuses operated by AWS, Microsoft, and Google within their Saudi cloud regions. Mega facilities (16.4%) are emerging in NEOM and Riyadh's new digital zones. Medium (13.2%) and Small (10.2%) facilities serve edge computing, telecom-adjacent, and enterprise private cloud requirements across secondary cities.

By Tier Type

Tier 3 facilities lead with a 52.4% market share in 2025, reflecting the enterprise preference for facilities offering 99.982% uptime (96 minutes maximum downtime per year). Tier 3's dual-powered infrastructure and concurrently maintainable design provide the reliability required by Saudi banking, government, and energy sector clients without the full capital cost of Tier 4.

Tier 4 facilities (28.6%) are deployed for mission-critical applications in oil and gas (Saudi Aramco), the financial sector (SAMA-regulated institutions), and defense. They provide 99.995% uptime with fault-tolerant power equating to less than 30 minutes of downtime per year, predominantly serving SME, government departmental, and managed service provider requirements in secondary cities.

Regional Market Insights

The Northern and Central Region, anchored by Riyadh, commands a 48.2% share in 2025, supported by the highest concentration of enterprise customers, government ministries, and the kingdom's three major cloud regions (AWS, Azure, Google). The KAFD in Riyadh, developed by KAFD DMC, a 1.6 million sq. m. digitally integrated, LEED Platinum-certified vertical city, is expected to add 300+ MW of planned data center capacity through 2030.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northern & Central |

48.2% |

Riyadh cloud regions, SDAIA HQ, government demand |

|

Western Region |

23.5% |

Jeddah cable hub, fintech, Hajj ICT demand |

|

Eastern Region |

18.1% |

Saudi Aramco, SABIC, petrochemical IT |

|

Southern Region |

10.2% |

NEOM connectivity, edge expansion |

The Western Region (23.5%) is the fastest-growing, driven by Jeddah's submarine cable landing stations connecting Saudi Arabia to Europe, Asia, and Africa. The Eastern Region (18.1%) hosts Saudi Aramco's internal data centers and private cloud infrastructure, one of the largest enterprise IT estates in the Middle East. The Southern Region (10.2%) is nascent but growing rapidly with NEOM's USD 500 billion infrastructure project requiring extensive edge computing deployments.

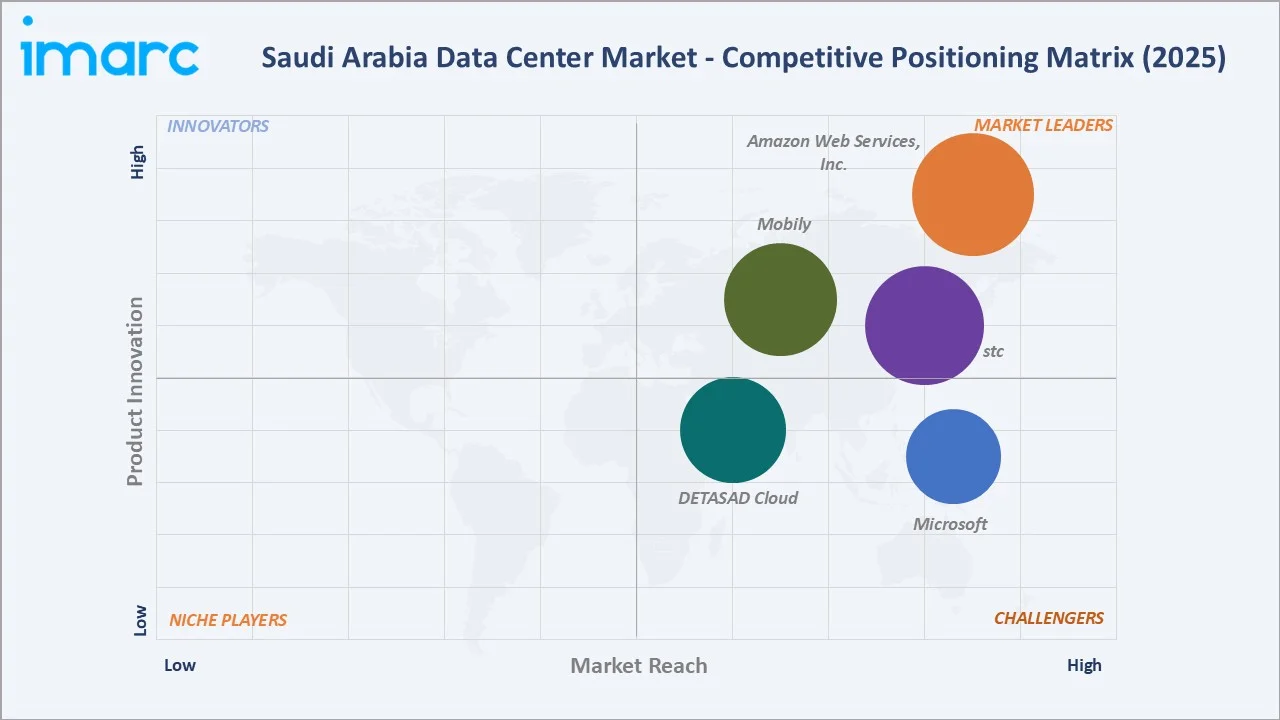

Competitive Landscape

The Saudi Arabia data center market exhibits a moderately concentrated structure at the tier-one operator level, with stc, Mobily, and DETASAD Cloud collectively holding approximately 55–62% of domestic colocation revenue in 2025. International hyperscalers (AWS, Microsoft Azure, Google, Oracle) command the managed cloud segment.

|

Company |

Brand / Entity |

Market Position |

Core Strength |

| stc | center3 | Market Leader | Largest domestic operator; Center3 operates 25+ data centers across Saudi Arabia |

| Mobily | Mobily | Market Leader | Western Region leader; Jeddah submarine cable hub |

| DETASAD Cloud | Detecon Al Saudia | Strong Challenger | ICT managed services; government DC specialist |

| Amazon Web Services, Inc. | Amazon Web Services | Market Leader | Three AZs in Riyadh; the largest cloud market share in KSA |

| Microsoft | Azure (Q4 2026) | Strong Challenger | Deep government & enterprise integration |

At the same time, new entrants are expanding aggressively, making the market increasingly fragmented yet innovation-driven, with competition centered on scale, energy efficiency, interconnection capabilities, and alignment with Saudi Arabia’s digital transformation strategy.

Key Company Profiles

stc

stc, the enterprise IT arm of Saudi Arabia's largest telecom operator, operates the kingdom's most extensive carrier-neutral data center network. Its facilities in Riyadh, Jeddah, and Dammam total over 30,000 m² of white space and 60 MW of power capacity. Additionally, the company is targeting 300MW of total installed capacity by 2027, and 1 GW by 2030.

- Product Portfolio: Tier 3 and Tier 4 colocation, managed hosting, cloud gateway services, and cybersecurity-integrated facilities.

- Recent Developments: In December 2025, Saudi Telecom Company (stc) signed a joint venture agreement with PIF-backed Humain to accelerate data center development in Saudi Arabia. The partnership focuses on building large-scale AI-focused data center infrastructure, supporting the Kingdom’s ambition to become a regional hub for advanced digital and AI capabilities.

- Strategic Focus: Hyperscale-adjacent co-location; AI-infrastructure readiness; sovereign cloud for government.

DETASAD Cloud

DETASAD Cloud, a joint venture between DETECON International GmbH and FAL Holdings Arabia Co., is a pioneer in managed ICT services and government data center operations in the kingdom. The company manages critical infrastructure for multiple Saudi ministries.

- Product Portfolio: Managed colocation, disaster recovery, government private cloud, and ICT outsourcing.

- Recent Developments: In November 2023, DETASAD and Arqit partnered to deploy a quantum-safe cybersecurity platform in Saudi Arabia, integrating Arqit’s Symmetric Key Agreement technology with DETASAD’s cloud and infrastructure solutions to create a fully data-sovereign security stack.

- Strategic Focus: Government digital transformation; hybrid cloud managed services; NDMO-compliant data sovereignty solutions.

Mobily

Mobily (Etihad Etisalat Company), Saudi Arabia's second-largest telecommunications operator, operates one of the kingdom's most geographically distributed data center networks. With 14 Tier-certified facilities across Riyadh, Jeddah, Dammam, and other cities.

- Product Portfolio: Carrier-neutral colocation services, managed hosting, cloud on-ramp and connectivity services, GPU-ready and AI-capable infrastructure.

- Recent Developments: In February 2025, Mobily announced a USD 905 million (SAR 3.4 billion) investment in data centers and submarine cables to strengthen Saudi Arabia’s digital infrastructure and global connectivity. The initiative includes building data centers with around 39 MW capacity and expanding subsea cable networks to support growing demand for AI, cloud, and advanced digital services.

- Strategic Focus: Positioning Saudi Arabia as a three-continent digital hub connecting Asia, Africa, and Europe; submarine cable-anchored connectivity leadership for international carriers and cloud providers; AI and GPU infrastructure expansion to serve hyperscaler and enterprise demand.

Market Concentration Analysis

The Saudi Arabia data center market is moderately concentrated among domestic operators but highly concentrated in the cloud services layer, where three hyperscalers (AWS, Azure, Google) collectively hold an estimated 70–75% of public cloud infrastructure revenue in 2025. Consolidation is accelerating, driven by the capital intensity of Tier 3/4 builds (USD 8–15 million per MW installed) and the technical complexity of AI-ready facility design.

Between 2022 and 2025, six significant M&A and joint venture transactions reshaped the competitive map, including STC's acquisition of a minority stake in a regional colocation platform and a foreign hyperscaler’s partnership with a domestic telecom for sovereign cloud delivery. Private equity interest is elevated, with GCC-focused infrastructure funds targeting carrier-neutral assets with long-term anchor tenant agreements.

Investment & Growth Opportunities

Fastest Growing Segments

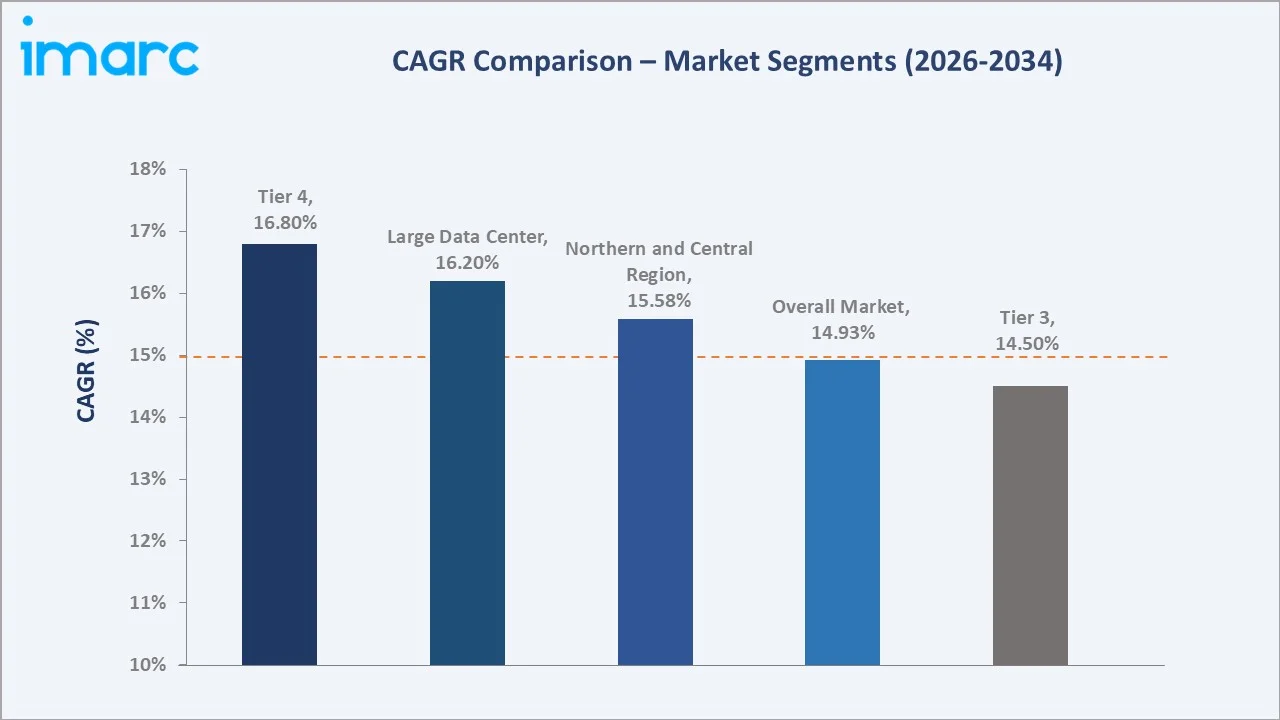

AI-optimized hyperscale facilities (estimated CAGR 22–25%), green/renewable-powered data centers (18% CAGR), and edge computing nodes (16% CAGR) represent the three highest-growth investment vectors through 2034. Together these segments address a total addressable market of approximately USD 4.2 Billion by 2030 within the Saudi data center ecosystem.

Emerging Market Expansion

NEOM and the Red Sea Project collectively represent an incremental USD 1.2 Billion data center opportunity by 2034. Investment via joint ventures with domestic telecom operators, alignment with NEOM Tech & Digital (NTD) procurement programs, and participation in the Saudi Data Center Zone (industrial area designations providing tax incentives and pre-permitted power connections) are preferred modalities.

Venture and Institutional Investment Trends

- Key investment themes include AI-specific GPU co-location platforms, liquid cooling technology suppliers, and data center automation software (DCIM) catering to Saudi operators.

- The Public Investment Fund (PIF) has signaled intent to anchor domestic data center investments, with NEOM’s smart city infrastructure representing a USD 500 billion project with embedded data center requirements.

- Saudi Aramco Ventures and Saudi Aramco’s digital transformation program present strategic co-investment opportunities in energy-sector AI data infrastructure.

Future Market Outlook (2026-2034)

The Saudi Arabia data center market is positioned for exceptional, sustained growth through 2034. From USD 2.43 Billion in 2025, the market will reach USD 4.87 Billion by 2030 and USD 8.85 Billion by 2034, representing total incremental value creation of approximately USD 6.42 Billion over the forecast decade at a CAGR of 14.93%.

Three structural macro-themes define the trajectory: Saudi Vision 2030 mandating digital infrastructure investment as economic diversification (providing long-horizon policy certainty); the hyperscaler capital commitment cycle that is building irreversible demand for co-location, power, and fiber infrastructure; and the AI revolution that is multiplying per-workload compute and power requirements by orders of magnitude, compressing demand timelines and raising power density expectations across every facility class.

Regulatory evolution, particularly PDPL amendments, SAMA’s cloud framework updates, and NEOM’s sovereign technology zone regulations, will continue to shape operational frameworks. Operators that achieve Tier 3/4 certifications, secure renewable energy supply agreements, and demonstrate PDPL compliance will be positioned to capture disproportionate share of the USD 8.85 billion market by 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 120 industry participants in 2024–2025, including data center operators, hyperscaler infrastructure teams, telecom executives, government digital officers, and enterprise IT procurement managers across Riyadh, Jeddah, and Dammam.

Secondary Research

Secondary research encompassed CST regulatory filings, PIF investment announcements, hyperscaler press releases, SDAIA strategy documents, Uptime Institute certifications, and industry publications (DatacenterDynamics, Structure Research). Over 200 secondary sources were reviewed.

Forecasting Models

Market estimations used bottom-up facility capacity modeling and top-down spend allocation from Vision 2030 digital budgets, validated against hyperscaler revenue disclosures and CST annual data center capacity reports. Base-case CAGR of 14.93% reflects consensus analyst estimates and PIF infrastructure investment pipeline data.

Saudi Arabia Data Center Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Data Center Sizes Covered | Large, Massive, Medium, Mega, Small |

| Tier Types Covered | Tier 1 and 2, Tier 3, Tier 4 |

| Absorptions Covered | Non-Utilized, Utilized |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | stc, Mobily, DETASAD Cloud, Amazon Web Services, Inc., Microsoft, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Data Center Market Report

The Saudi Arabia data center market reached USD 2.43 Billion in 2025, up from USD 1.21 Billion in 2020, and is projected to reach USD 8.85 Billion by 2034.

The market is projected to grow at a CAGR of 14.93% during 2026-2034, driven by Vision 2030, hyperscaler investments, AI workload growth, and cloud-first government mandates.

The Northern and Central Region leads with a 48.2% share in 2025, anchored by Riyadh's hyperscale cloud regions (AWS, Azure, Google) and the concentration of government and enterprise demand.

Large data centers dominate with a 38.5% share in 2025, driven by hyperscaler co-location requirements and government cloud infrastructure projects demanding high-density, high-uptime facilities.

Tier 3 facilities command 52.4% of the market in 2025. Their concurrently maintainable, dual-powered design offers 99.982% uptime, making them the preferred choice for enterprise and cloud operator tenants.

Key players include stc, Mobily, DETASAD Cloud, Amazon Web Services, Inc., and Microsoft.

Key opportunities include AI-optimized hyperscale co-location (CAGR 22–25%), green/renewable-powered facilities (18% CAGR), NEOM and smart city edge infrastructure, and sovereign cloud platforms compliant with PDPL and NDMO data residency requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade