Saudi Arabia Health Insurance Market Size, Share, Trends and Forecast by Type and Service Provider, 2026-2034

Saudi Arabia Health Insurance Market Size, Share, Trends & Forecast (2026-2034)

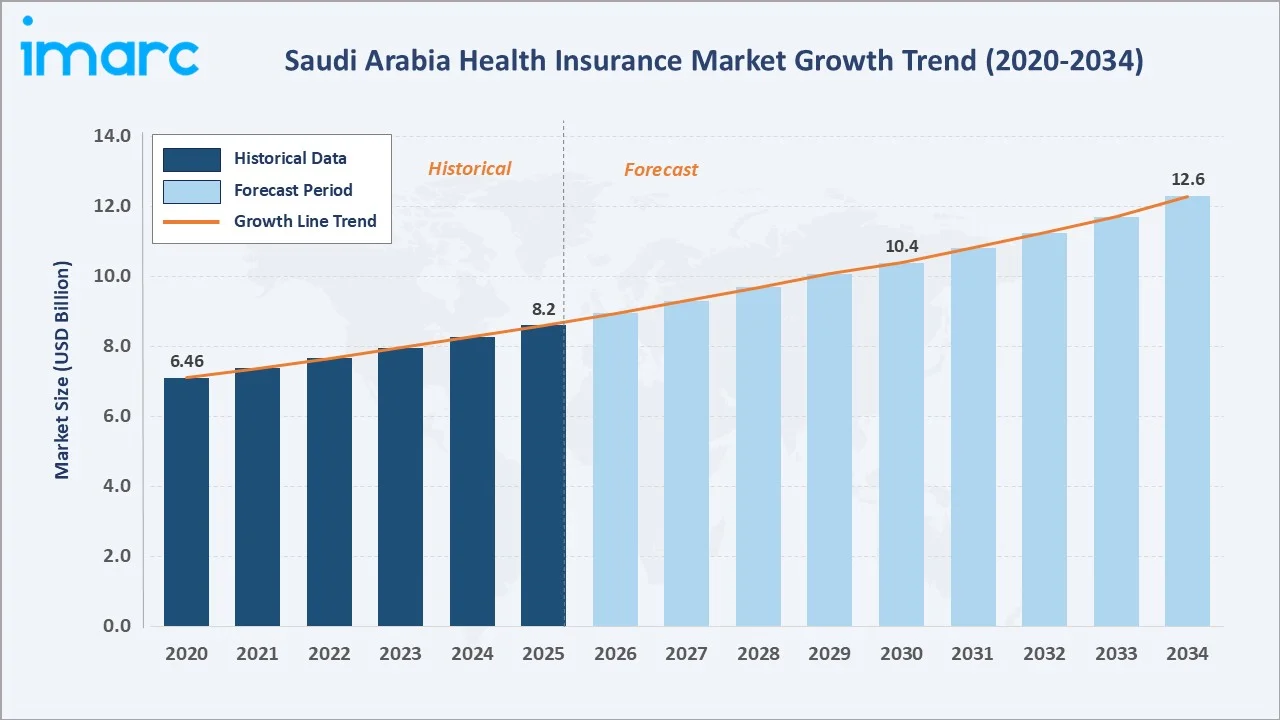

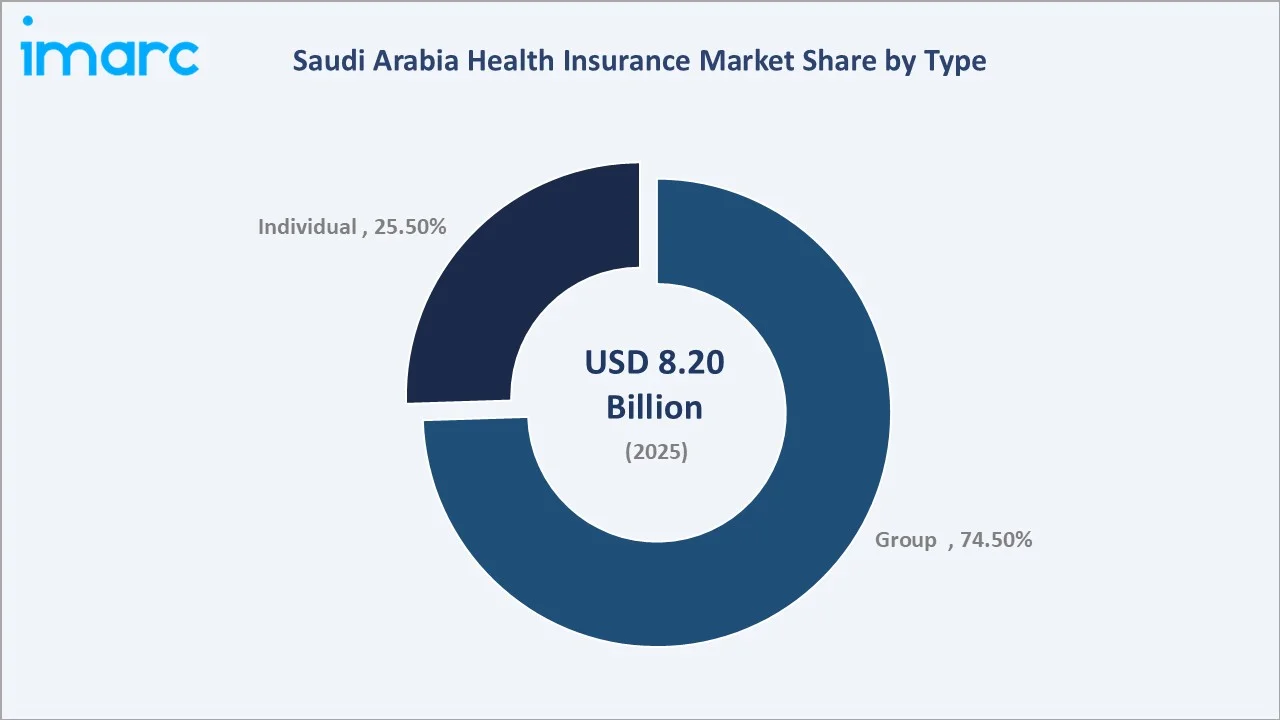

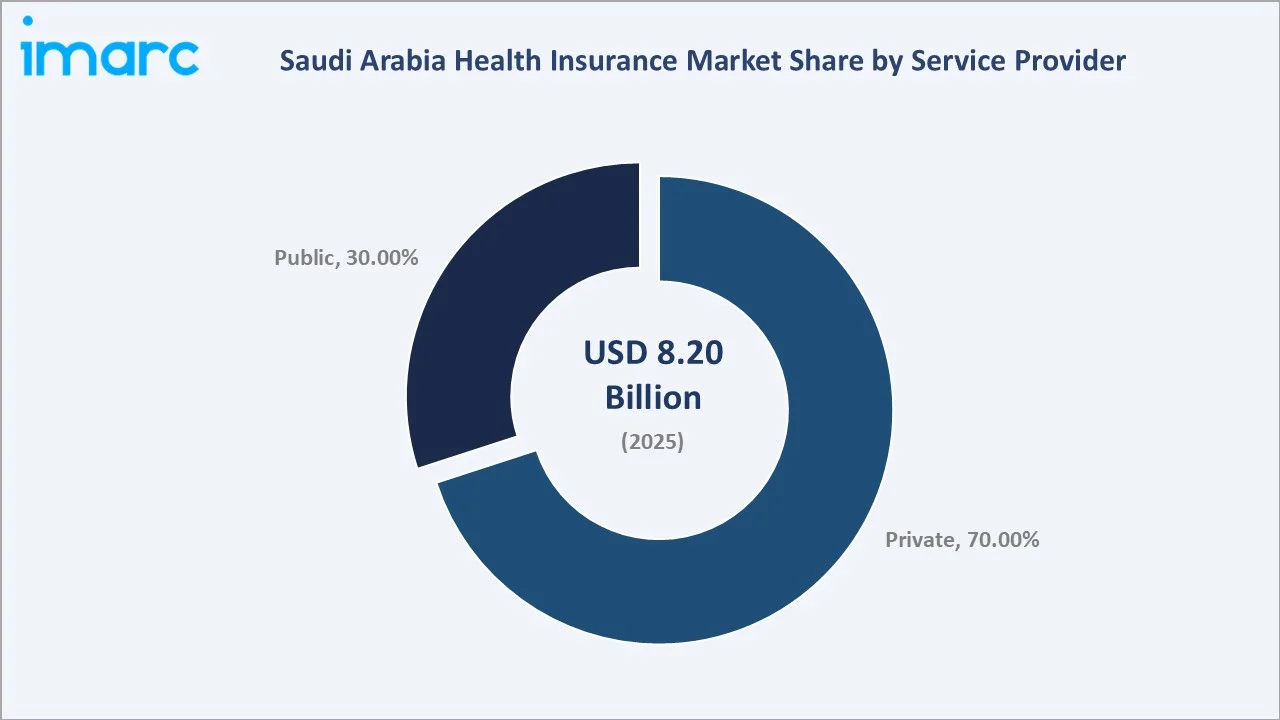

The Saudi Arabia health insurance market was valued at USD 8.20 Billion in 2025 and is projected to reach USD 12.60 Billion by 2034, growing at a CAGR of 4.88% during the forecast period 2026-2034. The market's expansion is anchored by mandatory coverage regulations for private sector employees and expatriates, Vision 2030-led healthcare reforms, and rising healthcare utilization driven by chronic disease prevalence.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.20 Billion |

|

Forecast Market Size (2034) |

USD 12.60 Billion |

|

CAGR (2026-2034) |

4.88% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (Type) |

Group – 74.5% share (2025) |

|

Largest Segment (Service Provider) |

Private – 70.0% share (2025) |

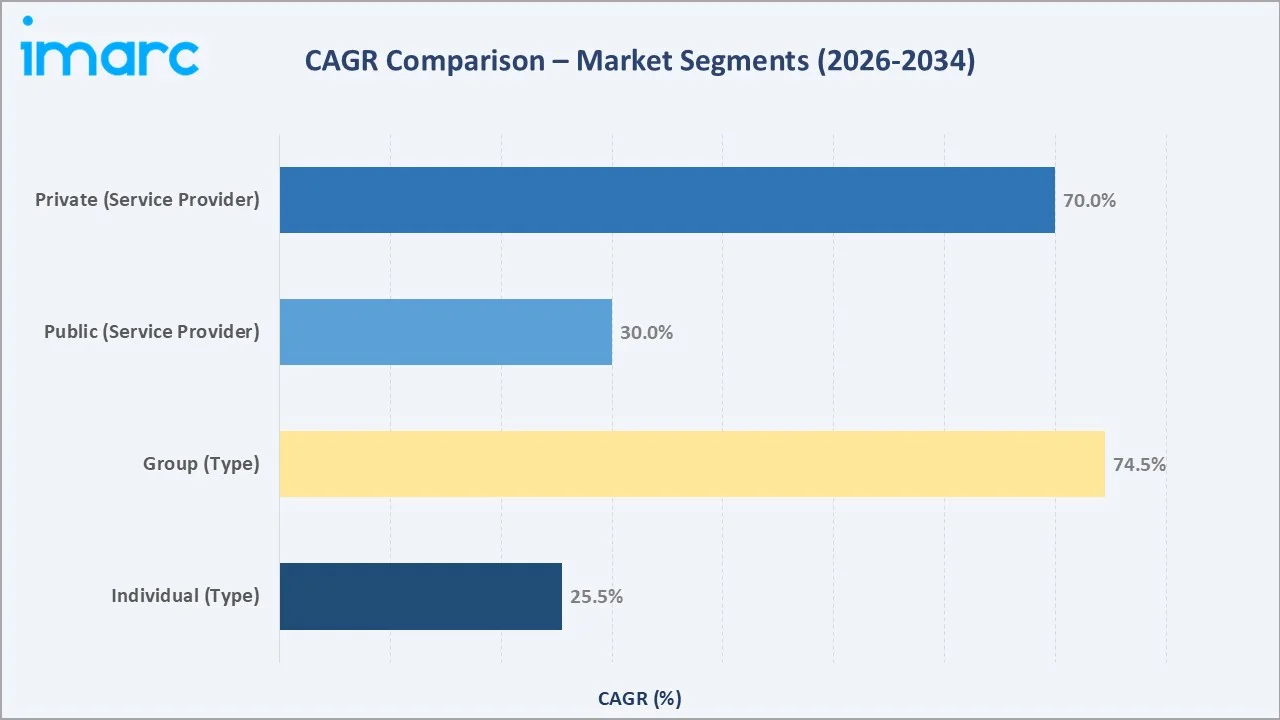

The private service provider segment dominates with a 70.0% share in 2025, while the group insurance type leads at 74.5%, reflecting strong employer-sponsored enrollment across Saudi Arabia's corporate and industrial sectors.

To get more information on this market, Request Sample

The Saudi Arabia health insurance market is expanding rapidly, supported by compulsory health coverage policies for expatriates and increasing enrollment of Saudi nationals under public-private healthcare initiatives. Growth is further driven by rising healthcare costs and a shift toward private sector participation.

Executive Summary

The Saudi Arabia health insurance market continues to demonstrate robust expansion, underpinned by regulatory mandates, demographic shifts, and accelerating digital transformation. Valued at USD 8.20 Billion in 2025, the market is forecasted to reach USD 12.60 Billion by 2034, growing at a CAGR of 4.88%.

Among the key structural drivers, mandatory health insurance for private sector employees and expatriates ensures broad enrollment stability. The group type segment commands 74.5% of the market in 2025, reflecting widespread employer-sponsored adoption, while the individual segment holds 25.5% with growing uptake among self-employed professionals and high-income residents.

Recent market developments, including Bupa Arabia's no-pre-approval insurance model and Walaa Insurance's AI-powered claims platform, highlight the sector's commitment to technology-led service excellence. Private providers lead with 70.0% of market share in 2025, leveraging advanced digital capabilities and expanded provider networks.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Group Insurance – 74.5% share (2025) |

|

Largest Segment (Service Provider) |

Private Providers – 70.0% share (2025) |

|

Leading Growth Driver |

Mandatory Coverage Regulations & Vision 2030 Reforms |

|

Key Regulatory Body |

Council of Cooperative Health Insurance (CCHI) |

|

Key Demographic Driver |

Expatriate population – 15.7 million in 2024 |

|

Market Opportunity |

AI-driven digital platforms & value-based care models |

Key Analytical Observations Supporting the Above Data:

- Group insurance dominates with a 74.5% market share in 2025, driven by regulatory mandates requiring employers to provide health coverage for all private sector workers and their dependents across corporate and industrial segments.

- Private service providers account for 70.0% of market revenues in 2025, driven by healthcare privatization policies, wider hospital networks, competitive pricing, and advanced digital claims processing capabilities that outperform public insurance schemes.

- Vision 2030 reforms are the structural backbone of market growth, accelerating privatization, PPP hospital expansion, and digital health infrastructure investment, all of which increase insurance-based healthcare access and policy uptake.

- Chronic disease burden, with 18.95% of adults having at least one chronic condition, including diabetes (9.1%) and hypertension (7.9%), is increasing healthcare utilization and compelling employers and individuals to invest in comprehensive coverage plans.

- Expatriate population growth reaching 15.7 million in 2024 (up from 14.5 million in 2023) is expanding the pool of mandatory health insurance enrollees, directly supporting premium volume growth and market scale.

Saudi Arabia Health Insurance Market Overview

The Saudi Arabia health insurance sector forms a critical pillar of the Kingdom's broader healthcare financing ecosystem. Operating under the regulatory oversight of the Council of Cooperative Health Insurance (CCHI), the market encompasses mandatory cooperative health insurance products offered through a network of licensed domestic and international insurers.

The sector's macroeconomic drivers include Saudi Arabia's GDP growth trajectory, urbanization trends, government expenditure on healthcare infrastructure, and demographic expansion. Approximately 4.8% of the total population was aged 60 years and above in 2025, indicating a growing elderly segment that requires sustained medical attention and drives long-term insurance demand.

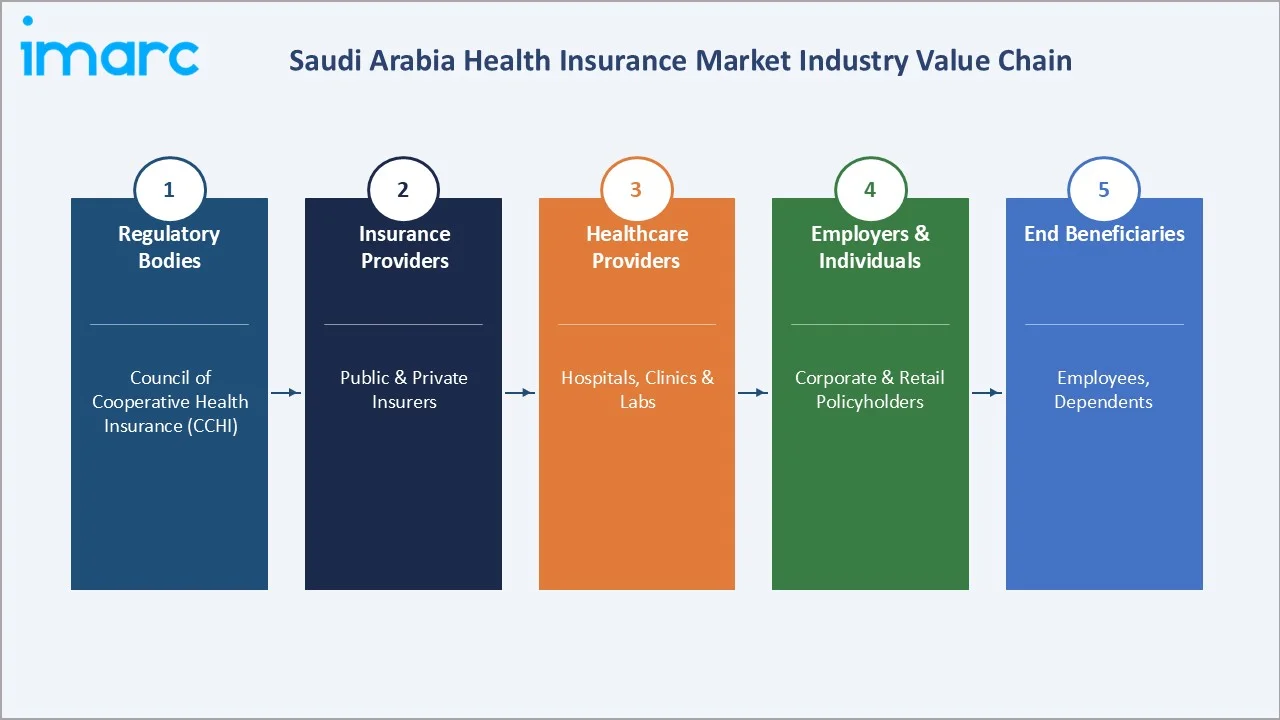

The value chain illustrates the sequential flow from regulatory oversight through CCHI to insurance product issuance by public and private providers, to healthcare delivery via hospitals, clinics, and diagnostic centers, and finally to policyholders. Claims processing, digital health platforms, and insurer-provider partnership models are increasingly integrated at each value chain stage, improving efficiency and care quality.

Market Dynamics

To evaluate market opportunities, Request Sample

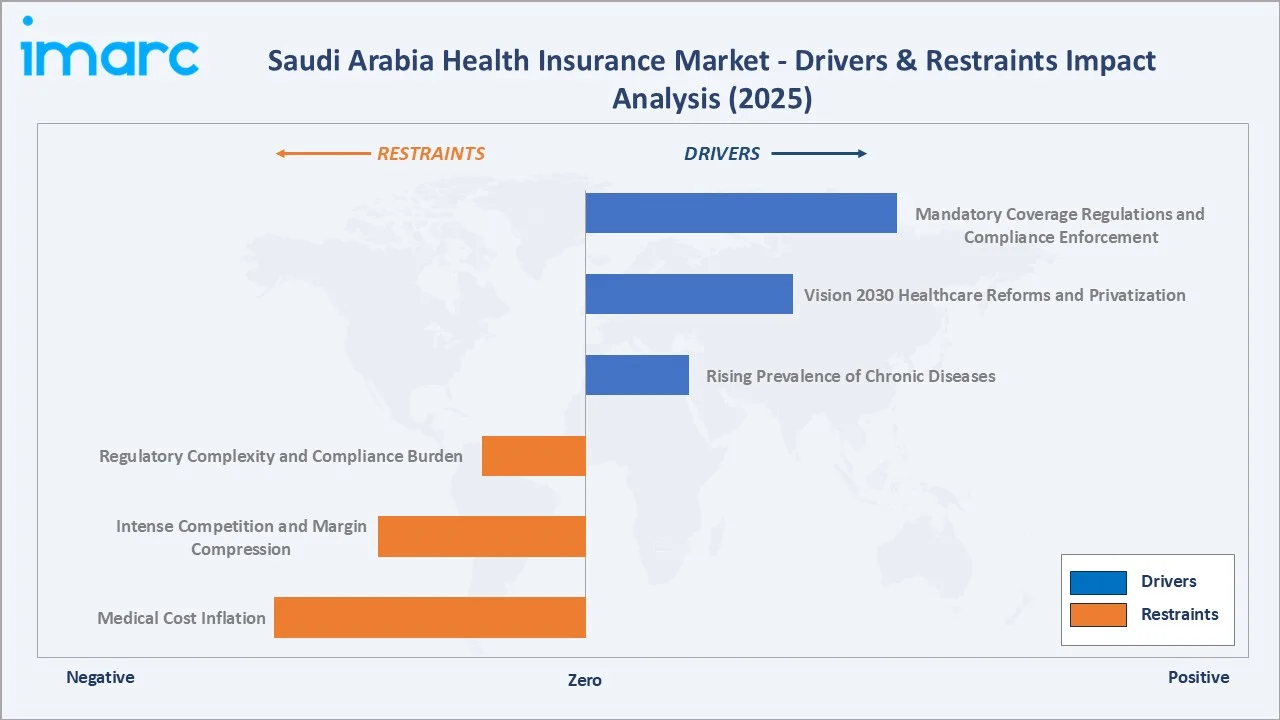

Market Drivers

- Mandatory Coverage Regulations and Compliance Enforcement: Regulatory requirements mandating health insurance for all private sector employees and expatriates ensure a structurally stable enrolled population.

- Vision 2030 Healthcare Reforms and Privatization: Government initiatives are expanding PPP hospitals, digital health platforms, and unified insurance databases, all of which increase reliance on insurance-based healthcare access and raise insured population coverage levels.

- Rising Prevalence of Chronic Diseases: According to the 2024 Health Status Statistics Publication, among children under 15 years, 9.4% were found to have a chronic disease, leading to the demand for comprehensive health insurance covering long-term treatment and chronic care management, which is intensifying.

These drivers collectively reinforce the Saudi Arabia health insurance market forecast of sustained compound growth at 4.88% CAGR through 2034. The interplay of regulatory mandates with demographic expansion creates a structurally favorable demand environment that supports stable insurer revenues and long-term market scalability across policy types and provider categories.

Market Restraints

- Medical Cost Inflation: Rising treatment costs, driven by advanced medical technologies, specialty pharmaceuticals, and increased chronic care utilization, are escalating claims ratios. This compresses insurer margins and creates pressure to raise premiums, which can encounter regulatory pricing constraints and employer resistance.

- Intense Competition and Margin Compression: The presence of numerous licensed insurers competing aggressively for large corporate and government-linked contracts drives pricing pressure and reduces profitability margins, particularly for smaller market participants with limited scale advantages.

- Regulatory Complexity and Compliance Burden: Frequent updates to benefit standards, solvency norms, and digital integration requirements increase administrative workloads and technology investment needs for insurers, raising operational costs and limiting agility among smaller players.

Market Opportunities

- Digital Health Platform Integration: Expanding investment in AI-powered claims platforms, telemedicine integration, and digital wellness programs creates differentiation opportunities for insurers and improves customer retention through enhanced service delivery.

- SME and Micro-Employer Coverage Expansion: Regulatory initiatives to extend mandatory coverage to small and medium enterprises represent a significant untapped enrollment opportunity, adding new premium volumes and diversifying insurer client portfolios.

- Value-Based Care and Preventive Insurance Models: Council of Health Insurance (CHI) 2025–2027 strategy focusing on beneficiary-centered healthcare creates opportunities for insurers to develop wellness-linked products, preventive care incentives, and outcomes-based coverage innovations.

Market Challenges

- Healthcare Workforce Shortages: Limited availability of specialized medical professionals can constrain healthcare delivery quality and create bottlenecks in claims authorization, potentially impacting policyholder satisfaction and renewal rates.

- Managing Claims for Chronic Disease Populations: Escalating claims from a growing chronic patient base require advanced data analytics and population health management capabilities that demand significant investment and operational expertise from insurers.

Emerging Market Trends

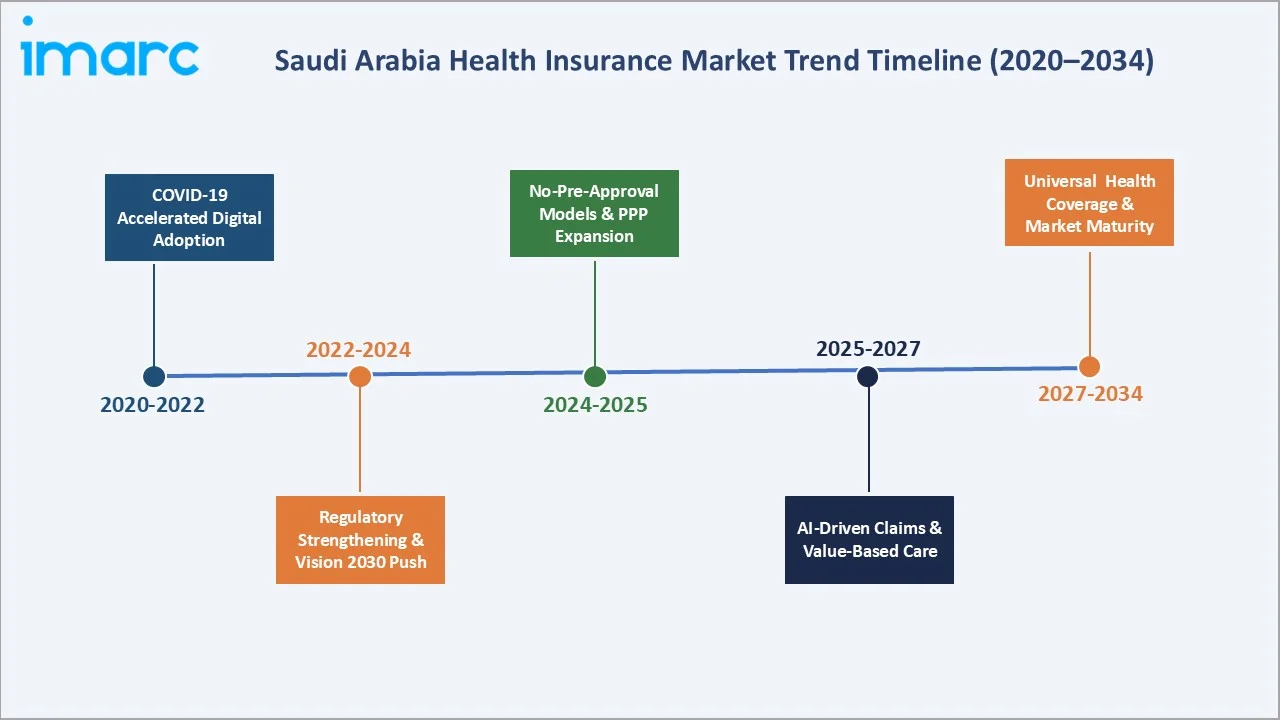

The Saudi Arabia health insurance market trends reflect the Kingdom's accelerating healthcare transformation, regulatory evolution, and technology adoption. From COVID-19-driven digital adoption to AI-powered claims automation, the sector is experiencing successive waves of disruption that are reshaping competitive dynamics and service delivery standards. The timeline above captures the critical inflection points from 2020 through 2034.

1. Digital Transformation and AI-Driven Claims Management

In January 2026, Walaa Insurance launched a fully digital, AI-powered health claims platform in partnership with CoverGo, streamlining claim processes and reducing costs while improving customer experience. This trend is setting new benchmarks for operational efficiency across the Saudi Arabia health insurance market.

2. Regulatory Strengthening and Benefits Standardization

In 2025, the Council of Health Insurance launched its 2025–2027 strategy anchored on five key pillars, focusing on a beneficiary-centric system, employer empowerment, and the integration of smart technologies. It also prioritizes quality healthcare, strengthens regulatory compliance, and reinforces the council’s role as an innovative, sustainable, and digitally advanced organization.

3. Innovation in Health Insurance Service Models

In March 2025, Bupa Arabia launched Saudi Arabia's first no-pre-approval health insurance model, enabling immediate treatment access through partnerships with over seven hospitals, with plans to expand to 15–20 additional facilities.

4. Population Growth and Demographic-Driven Demand

Saudi Arabia's expanding population is a structural driver of sustained health insurance demand. The non-Saudi population reached 15.7 million in 2024, while the elderly segment (60+ years) comprised approximately 4.8% of the total population in 2025. Aging demographics increase healthcare utilization and renewal rates, while expatriate population growth expands the mandatory insurance enrollment base.

Industry Value Chain Analysis

The Saudi Arabia health insurance value chain encompasses interconnected stages from regulatory oversight to end-beneficiary healthcare delivery. Each stage involves specialized participants whose performance directly influences product quality, cost management, and service responsiveness. The following table summarizes the key stakeholders at each stage.

|

Stage |

Key Players/Examples |

|

Regulatory Bodies |

Council of Cooperative Health Insurance (CCHI), Saudi Central Bank (SAMA) |

|

Insurance Providers |

Tawuniya, Bupa Arabia, MedGulf, Walaa Insurance, Al Rajhi Takaful, Gulf Insurance Group (GIG) |

|

Healthcare Providers |

Ministry of Health facilities, government specialist hospitals, and private hospital/clinic networks |

|

Technology Partners |

Digital claims platforms, health information exchange/integration partners, telehealth platforms, and AI-enabled claims/fraud tools |

|

Distribution Channels |

Brokers, direct corporate sales, employer HR/procurement channels, digital sales platforms |

|

Employers & Policyholders |

Private-sector employers, SMEs, government-linked enterprises, and covered group policyholders |

|

End Beneficiaries |

Employees, dependents, expatriate residents, and covered members under employer-sponsored plans |

The healthcare provider network is a critical enabler of the health insurance ecosystem, directly influencing policyholder satisfaction, claims frequency, and cost management. Saudi Arabia's expanding hospital infrastructure is broadening insurer provider networks and improving care accessibility.

Technology Landscape in the Saudi Arabia Health Insurance Industry

AI-Powered Claims Processing and Automation

In January 2026, Walaa Insurance deployed Saudi Arabia's first fully AI-powered health claims platform in partnership with CoverGo, achieving measurable reductions in administrative processing costs while simultaneously improving claims accuracy and fraud detection capabilities. The platform leverages real-time eligibility verification, predictive coding, and automated audit trails to meet CCHI compliance standards.

Digital Health Platforms and Telemedicine Integration

The total number of virtual consultations (VCs) in the Kingdom of Saudi Arabia reached 1,008,228 across home-based and hospital-based, with females accounting for a higher share of usage at 54.73%. The broader adoption of unified digital health IDs and interoperable EHR platforms under Vision 2030's National Health Information Center (NHIC) is further enabling insurers to access real-time patient history data and proactive chronic disease management.

Predictive Analytics and Data-Driven Underwriting

Insurers are leveraging large-scale health data, drawn from national health surveys, EHR systems, wearable device data, and pharmacy records, to identify high-risk enrollees, anticipate claims trajectories, and design targeted wellness interventions that reduce long-term costs. Predictive underwriting tools are also enabling more precise group plan pricing for corporate clients, improving loss ratios and supporting more competitive premium structures.

Compliance Platforms

The entry of global insurance technology specialists such as Lockton, which launched Saudi Arabia operations in November 2025 with dedicated healthcare insurance technology capabilities, is further accelerating the adoption of sophisticated compliance and risk management platforms.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Group |

74.5% |

2025 |

|

Service Provider |

Private |

70.0% |

2025 |

By Type

Group insurance dominates with a 74.5% market share in 2025, driven by mandatory employer-sponsored coverage for private sector employees and their dependents. Employers actively prefer group policies for their cost efficiency, simplified administration, and standardized benefits packages that align with labor law compliance obligations.

To access detailed market analysis, Request Sample

The individual insurance segment accounts for 25.5% of the market in 2025 and reflects growing demand among self-employed professionals, freelancers, and high-income residents who supplement employer plans with personal coverage.

By Service Provider

The private service provider segment commands a dominant 70.0% share of the Saudi Arabia health insurance market in 2025, driven by healthcare privatization policies and extensive hospital networks. Private insurers attract employers and individuals seeking flexible coverage, faster claims settlement, and broader hospital access across urban and regional markets.

The public service provider segment represents 30.0% of the market in 2025, primarily serving government employees, military personnel, and subsidized coverage programs. While growth in this segment is more constrained by budget allocations and policy frameworks, ongoing healthcare reform initiatives under Vision 2030 are improving the efficiency, standardization, and digital readiness of public insurance schemes.

Competitive Landscape

The Saudi Arabia health insurance market exhibits moderate competitive intensity, characterized by established domestic cooperative insurers competing alongside regional and international players across premium segments and distribution channels.

|

Company Name |

Market Position |

Core Strength |

|

Tawuniya (The Company for Cooperative Insurance) |

Market Leader |

Large corporate contracts, government-linked policies, and broad national coverage |

|

Bupa Arabia for Cooperative Insurance |

Market Leader |

Strong digital capabilities and premium employer segment focus |

|

MedGulf (Mediterranean & Gulf Insurance and Reinsurance Company) |

Strong Challenger |

Strong corporate and SME coverage offerings |

|

Walaa Cooperative Insurance |

Digital Pioneer |

AI-powered claims platform (CoverGo partnership, 2026), SME and retail focus |

|

Al Rajhi Takaful |

Emerging Player |

Sharia-compliant (Takaful) products, retail banking distribution synergies |

|

Gulf Insurance Group (GIG Saudi) |

Regional Competitor |

International underwriting standards, diversified personal and group insurance |

Market dynamics reflect strategic positioning ranging from volume-focused approaches emphasizing scale and cost efficiency to differentiation strategies leveraging product innovation, digital capabilities, and specialized healthcare partnerships.

Tawuniya and Bupa Arabia are market leaders, combining high market presence with strong digital and innovation capabilities. MedGulf and Walaa Insurance are positioned as strong challengers, with Walaa's AI-driven digital pivot enhancing its innovation score significantly.

Key Company Profiles

Tawuniya (The Company for Cooperative Insurance)

Tawuniya is Saudi Arabia's largest cooperative insurer and a publicly listed market leader, offering comprehensive health, motor, property, and life insurance products. The company commands a leading market position through scale, regulatory relationships, and an extensive hospital network.

- Product Portfolio: Comprehensive group health, individual medical, travel, and specialized corporate coverage plans.

- Recent Developments: Secured major health insurance contracts with Saudia and the Ministry of Foreign Affairs in 2025, expanding its insured corporate population base.

- Strategic Focus: Maintaining market leadership through large-scale corporate contracts, digital claims processing enhancements, and network expansion across all regions of the Kingdom.

Bupa Arabia for Cooperative Insurance

Bupa Arabia is a leading private health insurer in Saudi Arabia, recognized for its innovation-driven approach and premium employer segment positioning. The company co-founded and operates one of the Kingdom's most extensive private hospital and clinic networks.

- Product Portfolio: Group health plans for corporates and SMEs, individual and family health coverage, dental and optical riders, and international health insurance options.

- Recent Developments: Launched the no-pre-approval health insurance model in 2025 with seven hospital partners, with a planned expansion to 15–20 additional hospitals within the year.

- Strategic Focus: Technology-first service innovation, premium employer segment retention, and provider network expansion to differentiate on patient experience and care accessibility.

MedGulf (Mediterranean & Gulf Insurance and Reinsurance Company)

MedGulf is a well-established insurer serving large corporate and state-linked enterprises with comprehensive group health and property insurance solutions. The company provides comprehensive coverage to SEC employees and dependents and reinforces MedGulf's credibility in the government-affiliated group segment.

- Product Portfolio: Group medical insurance, property, motor, engineering, and liability coverage for corporate and state-owned enterprise clients.

- Recent Developments: Signed a health insurance contract with Saudi Electricity Company (SEC) in 2024, effective January 2025, covering employees and dependents comprehensively.

- Strategic Focus: Deepening relationships with state-owned and government-affiliated enterprises through reliable service delivery, competitive group pricing, and long-term contract retention.

Walaa Cooperative Insurance

Walaa Insurance is positioning itself as the Kingdom's digital insurance pioneer, leveraging technology partnerships to differentiate on operational efficiency and customer experience. The company aligns with Walaa's growth strategy of technology-led market penetration across SME and retail insurance segments.

- Product Portfolio: Group health insurance, motor, property, and SME-focused commercial insurance packages with embedded digital service capabilities.

- Recent Developments: Launched a fully digital, AI-powered health claims platform in partnership with CoverGo in January 2026, establishing a new operational efficiency benchmark for the market.

- Strategic Focus: Digital-first market penetration through AI automation, SME segment growth, and cost-efficiency leadership through technology-driven claims and underwriting processes.

Market Concentration Analysis

The Saudi Arabia health insurance market exhibits moderate concentration, with the top five players, Tawuniya, Bupa Arabia, MedGulf, Walaa Insurance, and Al Rajhi Takaful, collectively accounting for a significant majority of total premium revenues in 2025. The domestic cooperative insurer structure, mandated by regulatory frameworks, creates a defined pool of licensed participants.

The group health insurance segment is notably more concentrated than the individual segment, given the tendency for large corporate clients to consolidate coverage under a single insurer for administrative efficiency and cost management. State-owned enterprise and government-linked contracts represent a high-value contract segment that reinforces the market positions of established players.

Regulatory pressure for stronger solvency positions, digital infrastructure investment requirements, and rising competition for large corporate mandates are creating structural incentives for mergers and acquisitions. Smaller licensed insurers with limited capital and distribution networks face increasing challenges sustaining competitive operations independently, suggesting that the market will progressively concentrate among a smaller number of insurers through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

SME group coverage expansion and technology-enabled individual insurance plans represent the highest-growth investment vectors in the Saudi Arabia health insurance market through 2034. These segments collectively address an expanding addressable market driven by regulatory mandates, demographic growth, and rising health awareness among Saudi and expatriate populations.

Emerging Market Expansion

The Vision 2030 framework is catalyzing investment opportunities across previously underserved insurance segments, including micro and small enterprise employee coverage, gig economy worker health plans, and senior citizen-focused individual policies. Geographic expansion of private insurer networks into secondary cities and underserved regions presents further volume growth opportunities aligned with Saudi Arabia's urbanization trajectory.

Venture and Strategic Investment Trends

Strategic investment in Saudi Arabia's health insurance ecosystem is accelerating across digital health infrastructure, InsurTech platforms, and healthcare provider network development. The entry of Lockton into Saudi Arabia in November 2025 reflects growing international investor confidence in the Kingdom's expanding insurance market.

- Key growth bets: AI-powered underwriting automation, digital wellness programs, chronic disease management coverage, and SME enrollment platform development.

- Regulatory tailwinds: CCHI's 2025–2027 strategy with digital and AI initiatives directly supports investment in compliant InsurTech solutions and data-driven insurance platforms.

- International investor interest: Growing regional expansion by global brokers and reinsurers reflects increasing confidence in Saudi Arabia's healthcare financing reforms and market growth trajectory through 2034.

Future Market Outlook (2026-2034)

The Saudi Arabia health insurance market is poised for sustained, broad-based growth through 2034, anchored by regulatory compliance mandates, demographic expansion, and progressive digitalization of healthcare financing. From a base of USD 8.20 Billion in 2025, the market is forecast to reach USD 12.60 Billion by 2034, representing an absolute incremental value of approximately USD 4.40 Billion over the forecast period.

Insurers achieving significant cost efficiency gains through automation and data-driven risk management will establish decisive competitive advantages in the high-volume corporate contract segment by 2028–2030. The CCHI's 2025–2027 strategy is setting the regulatory foundation for these technological transitions, creating a coordinated modernization pathway for the entire sector.

Preventive care integration, wellness incentives, and personalized coverage models will transition from competitive differentiators to baseline requirements for market-leading insurers. Organizations that successfully embed data-driven personalization, value-based care linkages, and digital service excellence into their core product strategy will capture disproportionate growth in the Saudi Arabia health insurance market outlook beyond 2030.

Research Methodology

Primary Research

Primary research for this report was conducted through structured interactions with key industry participants, including health insurance executives, CCHI regulatory officials, hospital administrators, corporate HR professionals, benefits consultants, and individual policyholders across Saudi Arabia.

Secondary Research

Secondary research encompassed a comprehensive review of CCHI regulatory publications, Saudi Ministry of Health statistical reports, company annual reports and financial disclosures, Vision 2030 healthcare program documentation, trade publications, and publicly available demographic data, including the National Health Survey 2024, Elderly Survey 2025, and Saudi General Authority for Statistics population data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting methodologies, incorporating GDP growth rates, employment statistics, insured population data, premium volume trends, and historical market performance patterns from 2020 to 2025. Scenario analysis, covering base, optimistic, and conservative cases, was performed to account for regulatory, demographic, and macroeconomic uncertainty.

Saudi Arabia Health Insurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Individual, Group |

| Service Providers Covered | Public, Private |

| Key Companies | Tawuniya (The Company for Cooperative Insurance), Bupa Arabia for Cooperative Insurance, MedGulf (Mediterranean & Gulf Insurance and Reinsurance Company), Walaa Cooperative Insurance, Al Rajhi Takaful, Gulf Insurance Group (GIG Saudi) |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Saudi Arabia Health Insurance Market Report

The Saudi Arabia health insurance market was valued at USD 8.20 Billion in 2025, supported by mandatory coverage regulations, Vision 2030 healthcare reforms, and rising healthcare utilization across all insured population segments.

The Saudi Arabia health insurance market is expected to grow at a CAGR of 4.88% during the forecast period from 2026 to 2034, reaching USD 12.60 Billion by 2034.

The group insurance type dominates with a 74.5% market share in 2025, driven by mandatory employer-sponsored coverage for private sector employees and regulatory enforcement across corporate and industrial sectors.

Private service providers lead with a 70.0% market share in 2025, benefiting from diversified product offerings, wider hospital networks, competitive pricing, and advanced digital claims capabilities that outperform public insurance schemes.

Key drivers include mandatory coverage regulations, Vision 2030 privatization reforms, rising chronic disease prevalence, expatriate population growth reaching 15.7 million in 2024, and accelerating digital transformation across insurance operations.

Key challenges include medical cost inflation pressuring premium sustainability, intense competition compressing profit margins, escalating regulatory compliance demands, healthcare workforce shortages, and rising claims from growing chronic disease populations.

Vision 2030 is accelerating healthcare privatization, strengthening regulatory governance, expanding PPP hospital infrastructure, and promoting digital health platforms, all of which increase insurance-based healthcare access and support sustained market growth.

Digital transformation is improving claims efficiency and customer experience. Walaa Insurance's AI-powered claims platform and Bupa Arabia's no-pre-approval model are establishing new service benchmarks across the sector.

High-growth opportunities include AI-driven claims automation, SME group coverage expansion, senior citizen health plans, digital wellness programs, and value-based care products aligned with CCHI's 2025–2027 strategy and Vision 2030 objectives.

Leading companies include Tawuniya, Bupa Arabia, MedGulf, Walaa Cooperative Insurance, Al Rajhi Takaful, and GIG Gulf, collectively shaping competitive dynamics through innovation, network expansion, and corporate partnership strategies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)